Financial Resource Management: Budgeting, Statements, and Analysis

VerifiedAdded on 2023/06/15

|15

|2986

|223

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, covering key areas such as cash budgeting, financial statement preparation, and ratio analysis. It includes a detailed cash budget for a four-month period, comments on bank balance management strategies, and an analysis of trade receivable and payable days. The report also discusses share premium and its appearance in financial statements. Furthermore, it examines profit calculations for ordinary and preference shareholders under different financing options and calculates profit per share. The analysis extends to a comparative study of financial ratios for two companies, Bopp Plc and Bill Plc, providing insights into their financial performance. Desklib offers this and many other solved assignments for students.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1..................................................................................................................................3

a. Cash budget for the period of four months from June till September.....................................3

b. Comment on bank balance of the business..............................................................................4

c. Strategies to avoid withdrawing above overdraft limit............................................................4

QUESTION 2..................................................................................................................................4

(a) Preparation of Financial Statement of Storm Ltd. For the year ended 30th April 2021.........4

(b) Calculation and comment on trade receivable days and trade payable days of Storm Ltd....7

(c) Share Premium.......................................................................................................................8

QUESTION 3..................................................................................................................................9

a. Profits available to both ordinary and preference shareholders through option 1 and 2 in 3rd

and 4th year...................................................................................................................................9

b. Comment on findings............................................................................................................10

c. Calculation of profit per share for ordinary shareholders in 3rd and 4th year.........................10

d. Other means from which fund can be raised.........................................................................11

QUESTION 4................................................................................................................................11

A................................................................................................................................................11

B.................................................................................................................................................12

C.................................................................................................................................................13

REFERENCES..............................................................................................................................15

QUESTION 1..................................................................................................................................3

a. Cash budget for the period of four months from June till September.....................................3

b. Comment on bank balance of the business..............................................................................4

c. Strategies to avoid withdrawing above overdraft limit............................................................4

QUESTION 2..................................................................................................................................4

(a) Preparation of Financial Statement of Storm Ltd. For the year ended 30th April 2021.........4

(b) Calculation and comment on trade receivable days and trade payable days of Storm Ltd....7

(c) Share Premium.......................................................................................................................8

QUESTION 3..................................................................................................................................9

a. Profits available to both ordinary and preference shareholders through option 1 and 2 in 3rd

and 4th year...................................................................................................................................9

b. Comment on findings............................................................................................................10

c. Calculation of profit per share for ordinary shareholders in 3rd and 4th year.........................10

d. Other means from which fund can be raised.........................................................................11

QUESTION 4................................................................................................................................11

A................................................................................................................................................11

B.................................................................................................................................................12

C.................................................................................................................................................13

REFERENCES..............................................................................................................................15

QUESTION 1

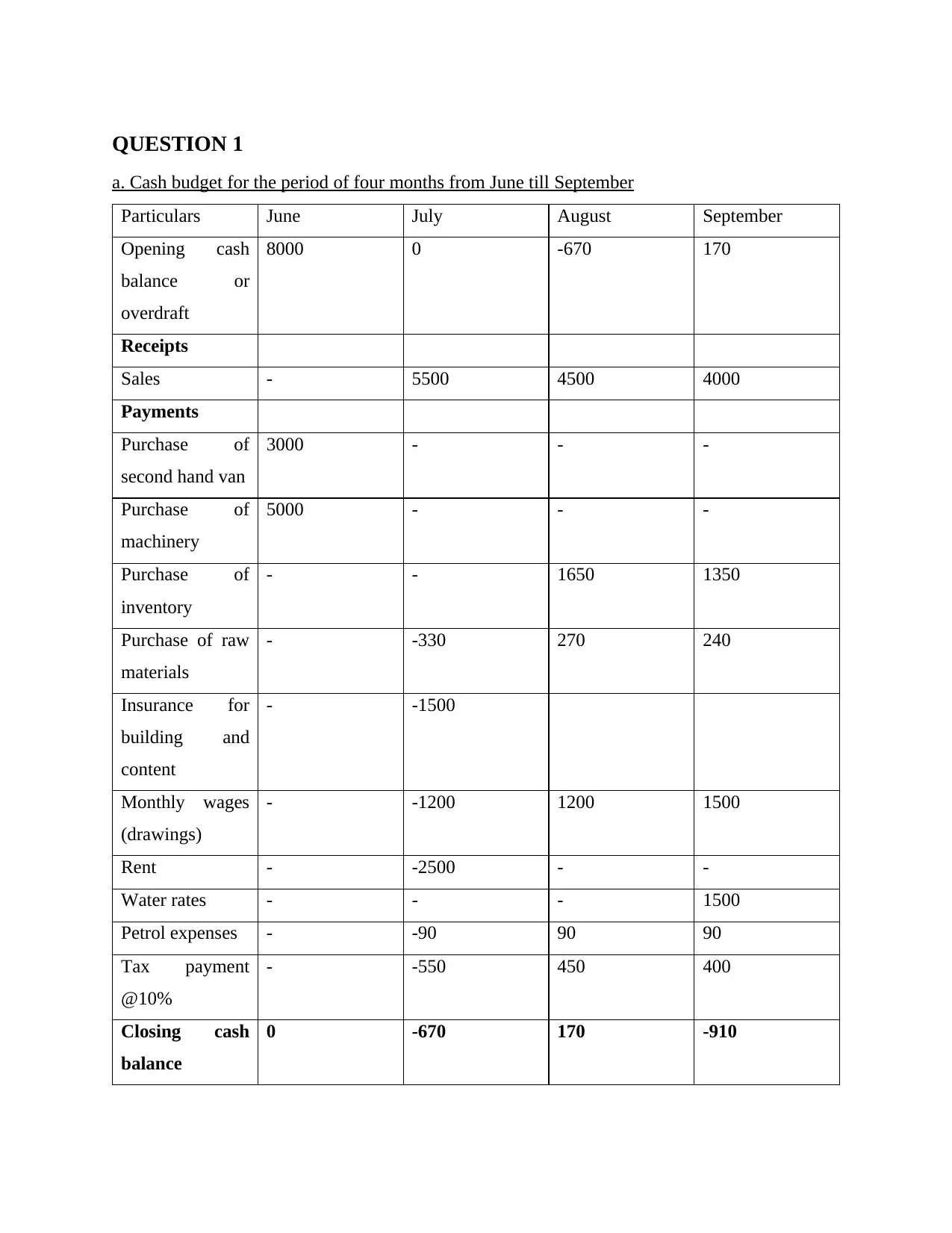

a. Cash budget for the period of four months from June till September

Particulars June July August September

Opening cash

balance or

overdraft

8000 0 -670 170

Receipts

Sales - 5500 4500 4000

Payments

Purchase of

second hand van

3000 - - -

Purchase of

machinery

5000 - - -

Purchase of

inventory

- - 1650 1350

Purchase of raw

materials

- -330 270 240

Insurance for

building and

content

- -1500

Monthly wages

(drawings)

- -1200 1200 1500

Rent - -2500 - -

Water rates - - - 1500

Petrol expenses - -90 90 90

Tax payment

@10%

- -550 450 400

Closing cash

balance

0 -670 170 -910

a. Cash budget for the period of four months from June till September

Particulars June July August September

Opening cash

balance or

overdraft

8000 0 -670 170

Receipts

Sales - 5500 4500 4000

Payments

Purchase of

second hand van

3000 - - -

Purchase of

machinery

5000 - - -

Purchase of

inventory

- - 1650 1350

Purchase of raw

materials

- -330 270 240

Insurance for

building and

content

- -1500

Monthly wages

(drawings)

- -1200 1200 1500

Rent - -2500 - -

Water rates - - - 1500

Petrol expenses - -90 90 90

Tax payment

@10%

- -550 450 400

Closing cash

balance

0 -670 170 -910

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b. Comment on bank balance of the business

In the month of June, with the help of initial capital Christina has purchased business assets and

have no cash in hand at the beginning of trading period. Then the trading period begins from July

with 0 bank balance and further many of the yearly and quarterly transaction as falling in the

month of July, there were negative bank balance or overdraft with the business at the end of July.

However, at the end of August there were positive bank balance with the business as small

expenses associated with the month of August has been made only. Again at the end of

September there were bank overdraft due to higher monthly wages and water rates payment

falling in this month.

c. Strategies to avoid withdrawing above overdraft limit

In the month of September, there were overdraft equivalent to 910 which is above an overdraft

limit which leads to extra charges by bank such as interest and other fees (Kolomytseva,

Medvedeva and Kolomiets, 2019). To avoid such situation, following strategies could be

employed:

Asking better terms from suppliers of raw materials to provide extended credit period.

Withdrawing less in terms of drawings by postponing personal expenses.

Increasing sales through providing discounts and offers.

Obtaining short terms loan at a lower interest rates as compared to interest and fees

charged on overdraft facility.

QUESTION 2

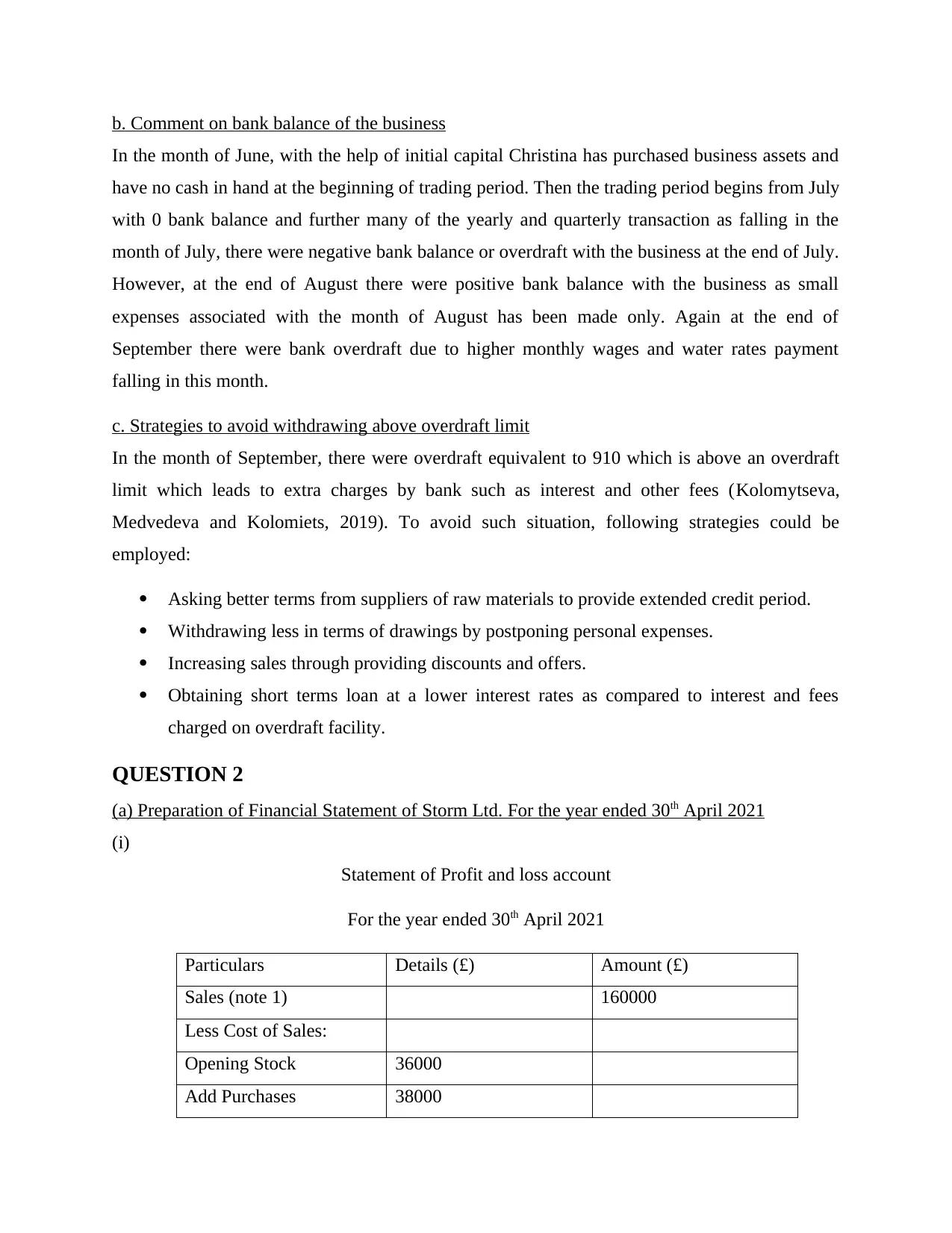

(a) Preparation of Financial Statement of Storm Ltd. For the year ended 30th April 2021

(i)

Statement of Profit and loss account

For the year ended 30th April 2021

Particulars Details (£) Amount (£)

Sales (note 1) 160000

Less Cost of Sales:

Opening Stock 36000

Add Purchases 38000

In the month of June, with the help of initial capital Christina has purchased business assets and

have no cash in hand at the beginning of trading period. Then the trading period begins from July

with 0 bank balance and further many of the yearly and quarterly transaction as falling in the

month of July, there were negative bank balance or overdraft with the business at the end of July.

However, at the end of August there were positive bank balance with the business as small

expenses associated with the month of August has been made only. Again at the end of

September there were bank overdraft due to higher monthly wages and water rates payment

falling in this month.

c. Strategies to avoid withdrawing above overdraft limit

In the month of September, there were overdraft equivalent to 910 which is above an overdraft

limit which leads to extra charges by bank such as interest and other fees (Kolomytseva,

Medvedeva and Kolomiets, 2019). To avoid such situation, following strategies could be

employed:

Asking better terms from suppliers of raw materials to provide extended credit period.

Withdrawing less in terms of drawings by postponing personal expenses.

Increasing sales through providing discounts and offers.

Obtaining short terms loan at a lower interest rates as compared to interest and fees

charged on overdraft facility.

QUESTION 2

(a) Preparation of Financial Statement of Storm Ltd. For the year ended 30th April 2021

(i)

Statement of Profit and loss account

For the year ended 30th April 2021

Particulars Details (£) Amount (£)

Sales (note 1) 160000

Less Cost of Sales:

Opening Stock 36000

Add Purchases 38000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

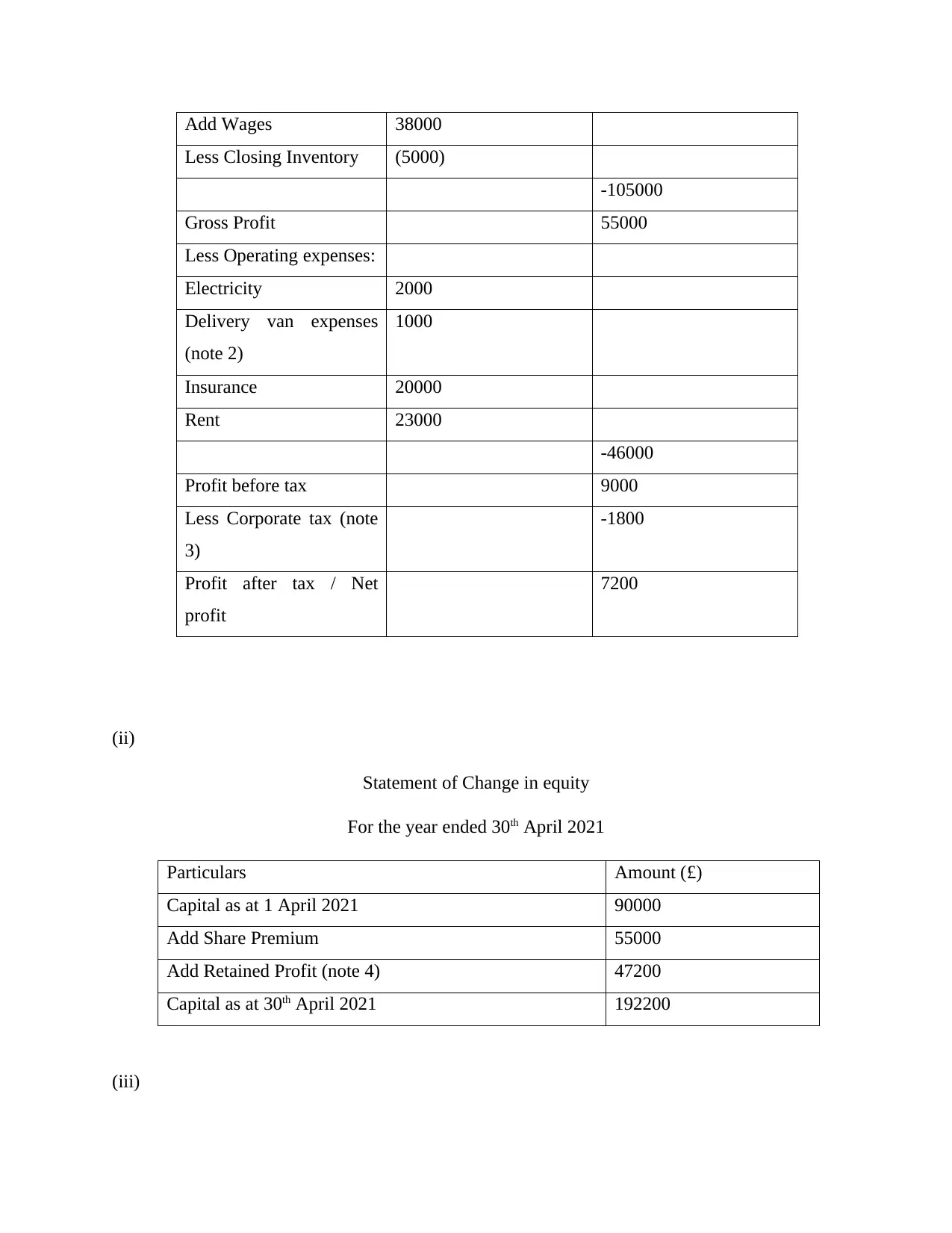

Add Wages 38000

Less Closing Inventory (5000)

-105000

Gross Profit 55000

Less Operating expenses:

Electricity 2000

Delivery van expenses

(note 2)

1000

Insurance 20000

Rent 23000

-46000

Profit before tax 9000

Less Corporate tax (note

3)

-1800

Profit after tax / Net

profit

7200

(ii)

Statement of Change in equity

For the year ended 30th April 2021

Particulars Amount (£)

Capital as at 1 April 2021 90000

Add Share Premium 55000

Add Retained Profit (note 4) 47200

Capital as at 30th April 2021 192200

(iii)

Less Closing Inventory (5000)

-105000

Gross Profit 55000

Less Operating expenses:

Electricity 2000

Delivery van expenses

(note 2)

1000

Insurance 20000

Rent 23000

-46000

Profit before tax 9000

Less Corporate tax (note

3)

-1800

Profit after tax / Net

profit

7200

(ii)

Statement of Change in equity

For the year ended 30th April 2021

Particulars Amount (£)

Capital as at 1 April 2021 90000

Add Share Premium 55000

Add Retained Profit (note 4) 47200

Capital as at 30th April 2021 192200

(iii)

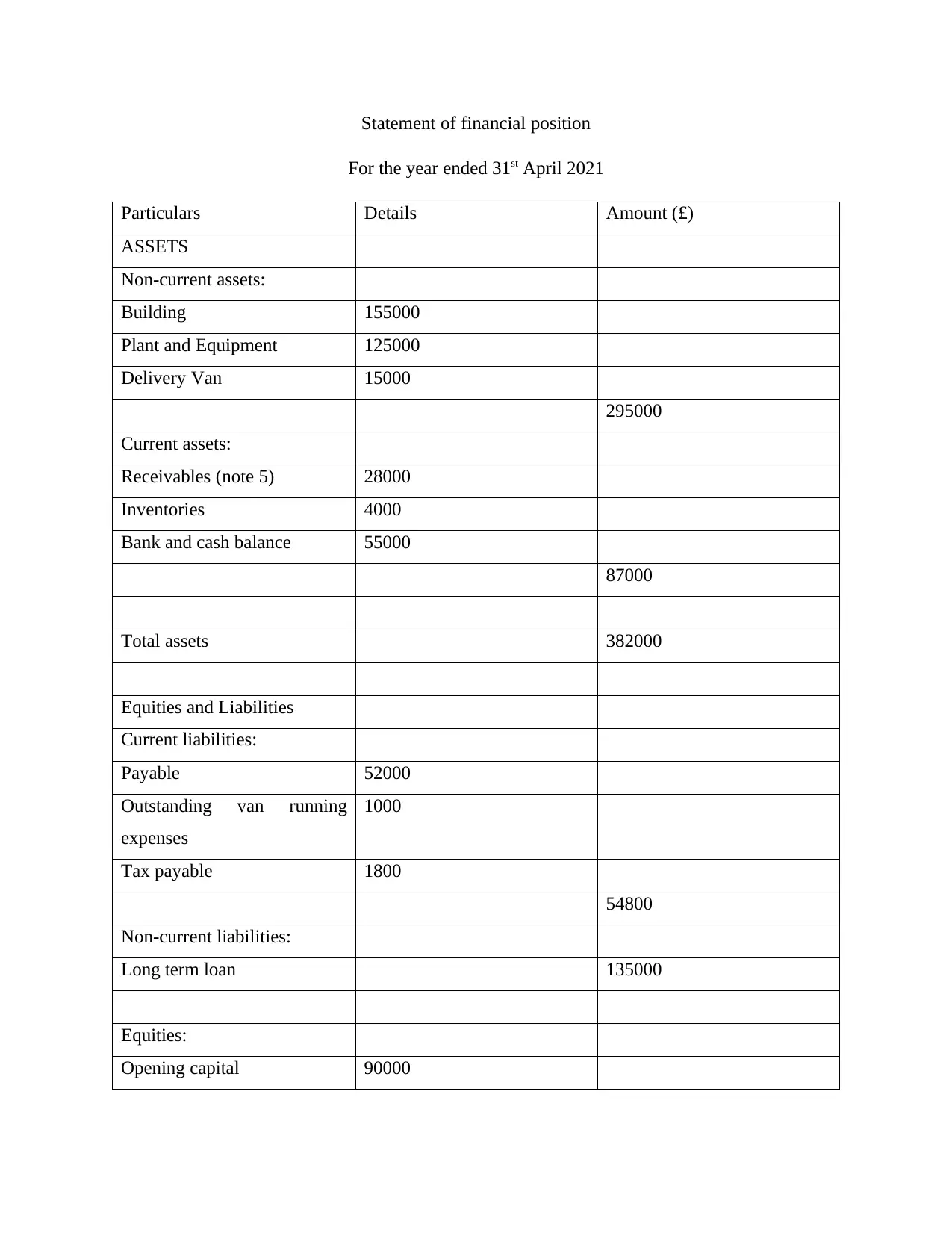

Statement of financial position

For the year ended 31st April 2021

Particulars Details Amount (£)

ASSETS

Non-current assets:

Building 155000

Plant and Equipment 125000

Delivery Van 15000

295000

Current assets:

Receivables (note 5) 28000

Inventories 4000

Bank and cash balance 55000

87000

Total assets 382000

Equities and Liabilities

Current liabilities:

Payable 52000

Outstanding van running

expenses

1000

Tax payable 1800

54800

Non-current liabilities:

Long term loan 135000

Equities:

Opening capital 90000

For the year ended 31st April 2021

Particulars Details Amount (£)

ASSETS

Non-current assets:

Building 155000

Plant and Equipment 125000

Delivery Van 15000

295000

Current assets:

Receivables (note 5) 28000

Inventories 4000

Bank and cash balance 55000

87000

Total assets 382000

Equities and Liabilities

Current liabilities:

Payable 52000

Outstanding van running

expenses

1000

Tax payable 1800

54800

Non-current liabilities:

Long term loan 135000

Equities:

Opening capital 90000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Share Premium 55000

Retained profit 47200

192200

Total equities and liabilities 382000

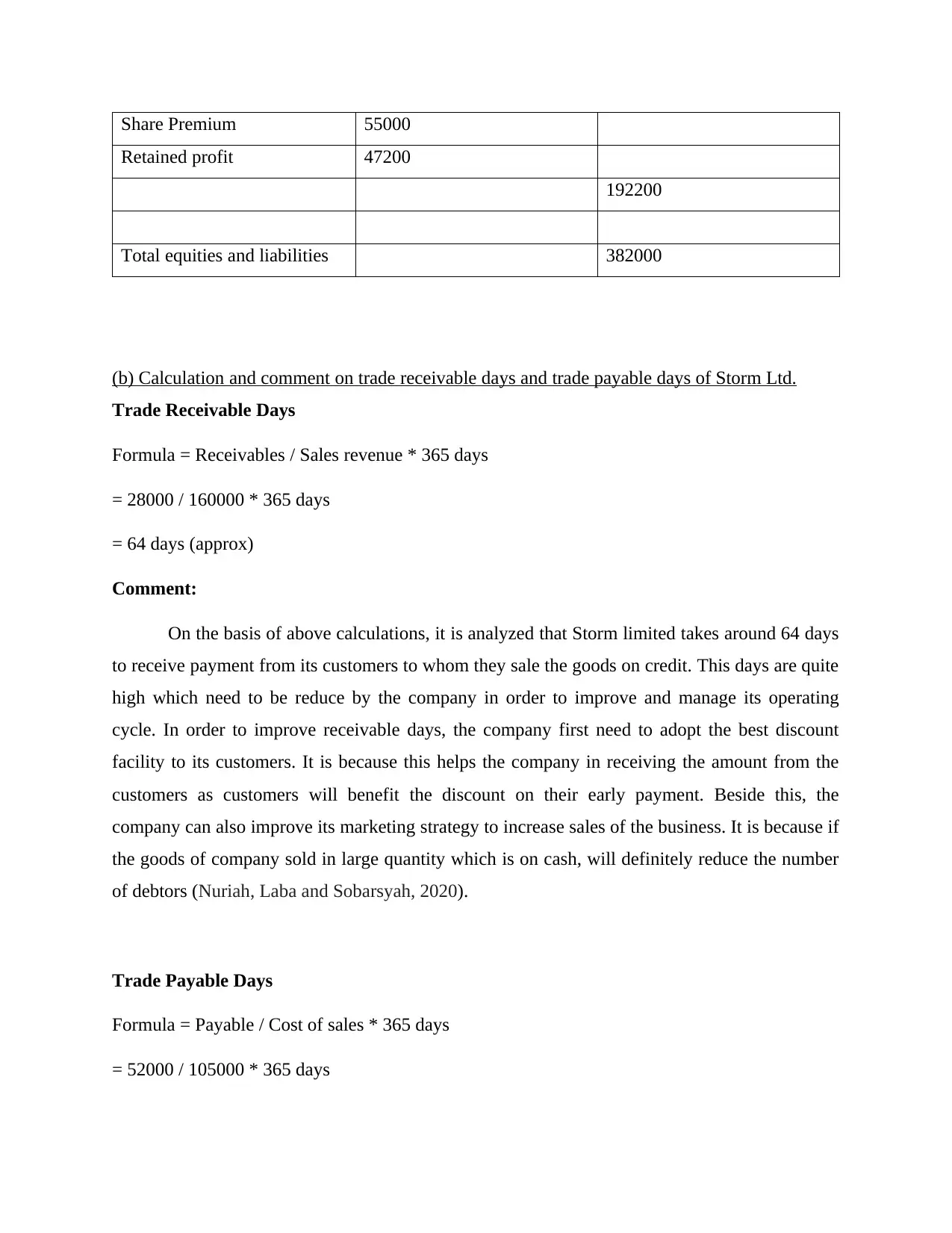

(b) Calculation and comment on trade receivable days and trade payable days of Storm Ltd.

Trade Receivable Days

Formula = Receivables / Sales revenue * 365 days

= 28000 / 160000 * 365 days

= 64 days (approx)

Comment:

On the basis of above calculations, it is analyzed that Storm limited takes around 64 days

to receive payment from its customers to whom they sale the goods on credit. This days are quite

high which need to be reduce by the company in order to improve and manage its operating

cycle. In order to improve receivable days, the company first need to adopt the best discount

facility to its customers. It is because this helps the company in receiving the amount from the

customers as customers will benefit the discount on their early payment. Beside this, the

company can also improve its marketing strategy to increase sales of the business. It is because if

the goods of company sold in large quantity which is on cash, will definitely reduce the number

of debtors (Nuriah, Laba and Sobarsyah, 2020).

Trade Payable Days

Formula = Payable / Cost of sales * 365 days

= 52000 / 105000 * 365 days

Retained profit 47200

192200

Total equities and liabilities 382000

(b) Calculation and comment on trade receivable days and trade payable days of Storm Ltd.

Trade Receivable Days

Formula = Receivables / Sales revenue * 365 days

= 28000 / 160000 * 365 days

= 64 days (approx)

Comment:

On the basis of above calculations, it is analyzed that Storm limited takes around 64 days

to receive payment from its customers to whom they sale the goods on credit. This days are quite

high which need to be reduce by the company in order to improve and manage its operating

cycle. In order to improve receivable days, the company first need to adopt the best discount

facility to its customers. It is because this helps the company in receiving the amount from the

customers as customers will benefit the discount on their early payment. Beside this, the

company can also improve its marketing strategy to increase sales of the business. It is because if

the goods of company sold in large quantity which is on cash, will definitely reduce the number

of debtors (Nuriah, Laba and Sobarsyah, 2020).

Trade Payable Days

Formula = Payable / Cost of sales * 365 days

= 52000 / 105000 * 365 days

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

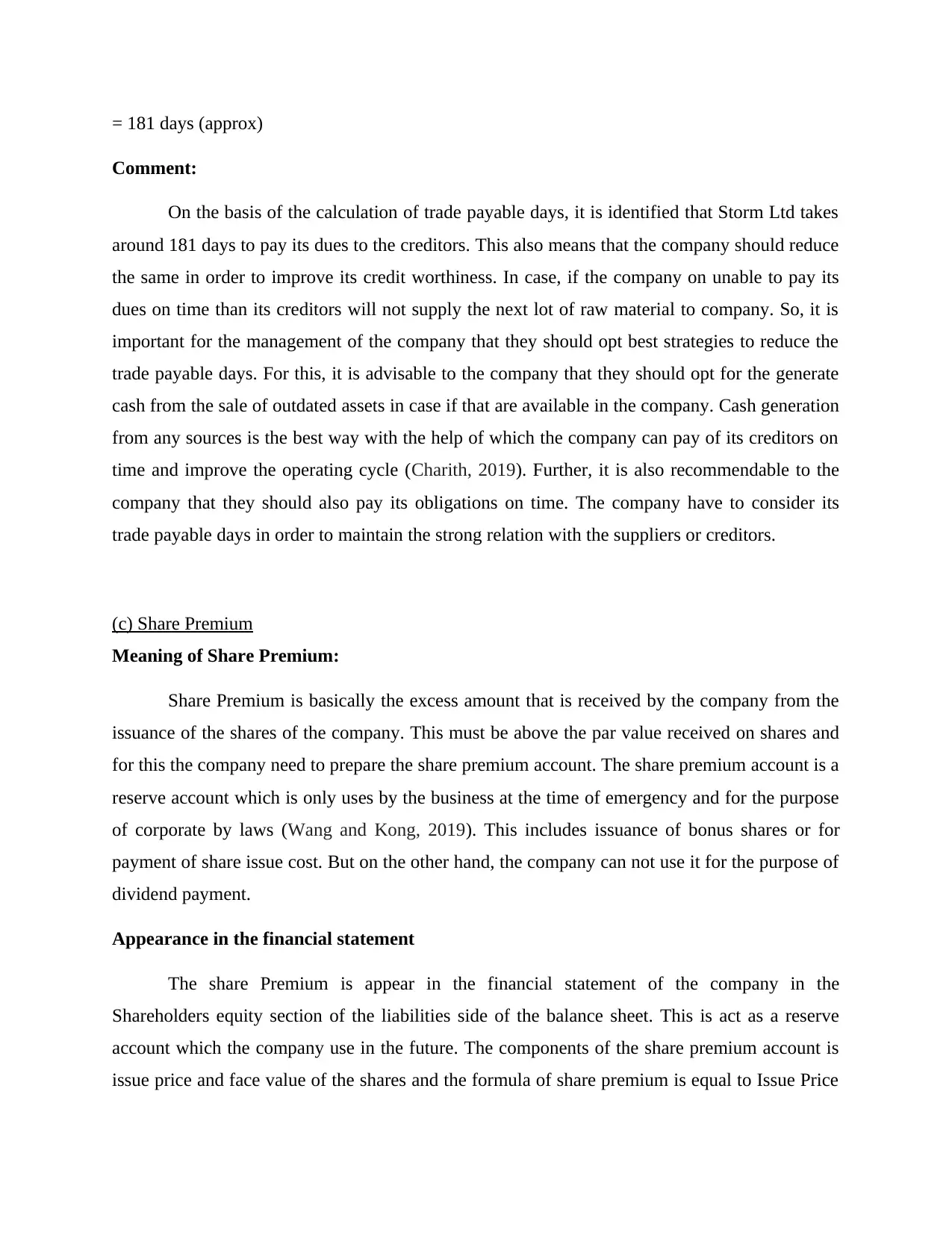

= 181 days (approx)

Comment:

On the basis of the calculation of trade payable days, it is identified that Storm Ltd takes

around 181 days to pay its dues to the creditors. This also means that the company should reduce

the same in order to improve its credit worthiness. In case, if the company on unable to pay its

dues on time than its creditors will not supply the next lot of raw material to company. So, it is

important for the management of the company that they should opt best strategies to reduce the

trade payable days. For this, it is advisable to the company that they should opt for the generate

cash from the sale of outdated assets in case if that are available in the company. Cash generation

from any sources is the best way with the help of which the company can pay of its creditors on

time and improve the operating cycle (Charith, 2019). Further, it is also recommendable to the

company that they should also pay its obligations on time. The company have to consider its

trade payable days in order to maintain the strong relation with the suppliers or creditors.

(c) Share Premium

Meaning of Share Premium:

Share Premium is basically the excess amount that is received by the company from the

issuance of the shares of the company. This must be above the par value received on shares and

for this the company need to prepare the share premium account. The share premium account is a

reserve account which is only uses by the business at the time of emergency and for the purpose

of corporate by laws (Wang and Kong, 2019). This includes issuance of bonus shares or for

payment of share issue cost. But on the other hand, the company can not use it for the purpose of

dividend payment.

Appearance in the financial statement

The share Premium is appear in the financial statement of the company in the

Shareholders equity section of the liabilities side of the balance sheet. This is act as a reserve

account which the company use in the future. The components of the share premium account is

issue price and face value of the shares and the formula of share premium is equal to Issue Price

Comment:

On the basis of the calculation of trade payable days, it is identified that Storm Ltd takes

around 181 days to pay its dues to the creditors. This also means that the company should reduce

the same in order to improve its credit worthiness. In case, if the company on unable to pay its

dues on time than its creditors will not supply the next lot of raw material to company. So, it is

important for the management of the company that they should opt best strategies to reduce the

trade payable days. For this, it is advisable to the company that they should opt for the generate

cash from the sale of outdated assets in case if that are available in the company. Cash generation

from any sources is the best way with the help of which the company can pay of its creditors on

time and improve the operating cycle (Charith, 2019). Further, it is also recommendable to the

company that they should also pay its obligations on time. The company have to consider its

trade payable days in order to maintain the strong relation with the suppliers or creditors.

(c) Share Premium

Meaning of Share Premium:

Share Premium is basically the excess amount that is received by the company from the

issuance of the shares of the company. This must be above the par value received on shares and

for this the company need to prepare the share premium account. The share premium account is a

reserve account which is only uses by the business at the time of emergency and for the purpose

of corporate by laws (Wang and Kong, 2019). This includes issuance of bonus shares or for

payment of share issue cost. But on the other hand, the company can not use it for the purpose of

dividend payment.

Appearance in the financial statement

The share Premium is appear in the financial statement of the company in the

Shareholders equity section of the liabilities side of the balance sheet. This is act as a reserve

account which the company use in the future. The components of the share premium account is

issue price and face value of the shares and the formula of share premium is equal to Issue Price

- Face value. The company receives premium on their shares when they issue shares at the higher

price which is above face value (Wang and Kong, 2019).

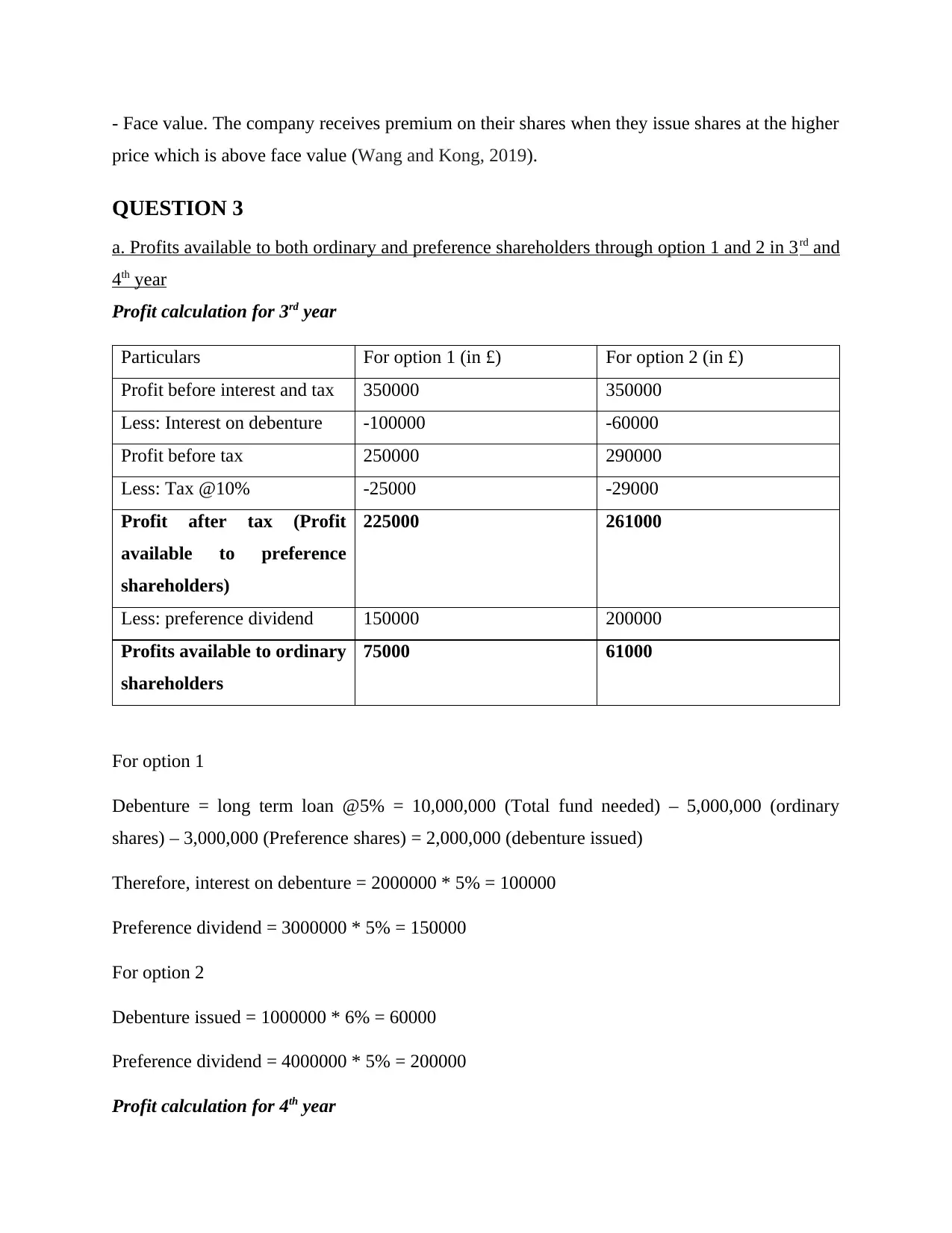

QUESTION 3

a. Profits available to both ordinary and preference shareholders through option 1 and 2 in 3rd and

4th year

Profit calculation for 3rd year

Particulars For option 1 (in £) For option 2 (in £)

Profit before interest and tax 350000 350000

Less: Interest on debenture -100000 -60000

Profit before tax 250000 290000

Less: Tax @10% -25000 -29000

Profit after tax (Profit

available to preference

shareholders)

225000 261000

Less: preference dividend 150000 200000

Profits available to ordinary

shareholders

75000 61000

For option 1

Debenture = long term loan @5% = 10,000,000 (Total fund needed) – 5,000,000 (ordinary

shares) – 3,000,000 (Preference shares) = 2,000,000 (debenture issued)

Therefore, interest on debenture = 2000000 * 5% = 100000

Preference dividend = 3000000 * 5% = 150000

For option 2

Debenture issued = 1000000 * 6% = 60000

Preference dividend = 4000000 * 5% = 200000

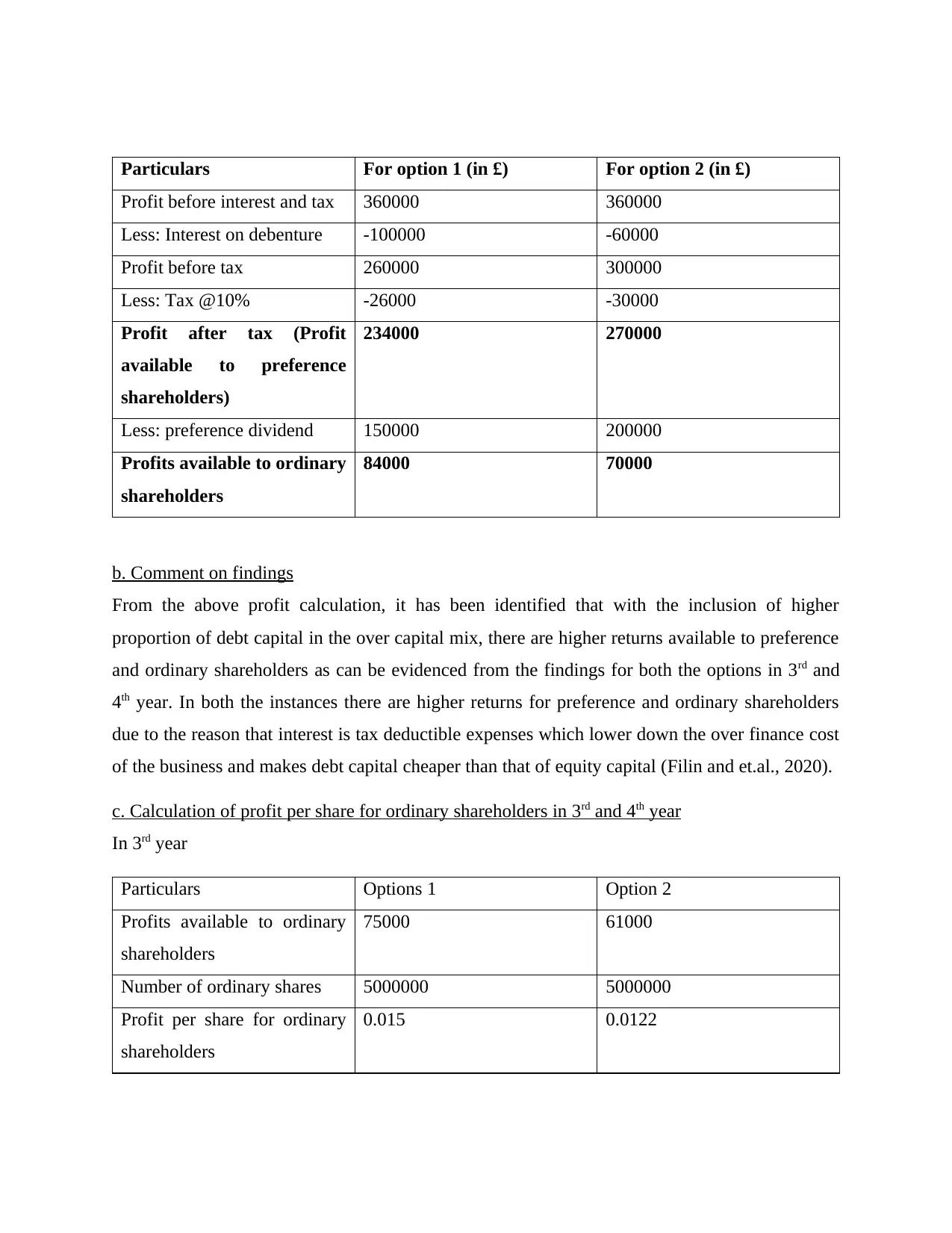

Profit calculation for 4th year

price which is above face value (Wang and Kong, 2019).

QUESTION 3

a. Profits available to both ordinary and preference shareholders through option 1 and 2 in 3rd and

4th year

Profit calculation for 3rd year

Particulars For option 1 (in £) For option 2 (in £)

Profit before interest and tax 350000 350000

Less: Interest on debenture -100000 -60000

Profit before tax 250000 290000

Less: Tax @10% -25000 -29000

Profit after tax (Profit

available to preference

shareholders)

225000 261000

Less: preference dividend 150000 200000

Profits available to ordinary

shareholders

75000 61000

For option 1

Debenture = long term loan @5% = 10,000,000 (Total fund needed) – 5,000,000 (ordinary

shares) – 3,000,000 (Preference shares) = 2,000,000 (debenture issued)

Therefore, interest on debenture = 2000000 * 5% = 100000

Preference dividend = 3000000 * 5% = 150000

For option 2

Debenture issued = 1000000 * 6% = 60000

Preference dividend = 4000000 * 5% = 200000

Profit calculation for 4th year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars For option 1 (in £) For option 2 (in £)

Profit before interest and tax 360000 360000

Less: Interest on debenture -100000 -60000

Profit before tax 260000 300000

Less: Tax @10% -26000 -30000

Profit after tax (Profit

available to preference

shareholders)

234000 270000

Less: preference dividend 150000 200000

Profits available to ordinary

shareholders

84000 70000

b. Comment on findings

From the above profit calculation, it has been identified that with the inclusion of higher

proportion of debt capital in the over capital mix, there are higher returns available to preference

and ordinary shareholders as can be evidenced from the findings for both the options in 3rd and

4th year. In both the instances there are higher returns for preference and ordinary shareholders

due to the reason that interest is tax deductible expenses which lower down the over finance cost

of the business and makes debt capital cheaper than that of equity capital (Filin and et.al., 2020).

c. Calculation of profit per share for ordinary shareholders in 3rd and 4th year

In 3rd year

Particulars Options 1 Option 2

Profits available to ordinary

shareholders

75000 61000

Number of ordinary shares 5000000 5000000

Profit per share for ordinary

shareholders

0.015 0.0122

Profit before interest and tax 360000 360000

Less: Interest on debenture -100000 -60000

Profit before tax 260000 300000

Less: Tax @10% -26000 -30000

Profit after tax (Profit

available to preference

shareholders)

234000 270000

Less: preference dividend 150000 200000

Profits available to ordinary

shareholders

84000 70000

b. Comment on findings

From the above profit calculation, it has been identified that with the inclusion of higher

proportion of debt capital in the over capital mix, there are higher returns available to preference

and ordinary shareholders as can be evidenced from the findings for both the options in 3rd and

4th year. In both the instances there are higher returns for preference and ordinary shareholders

due to the reason that interest is tax deductible expenses which lower down the over finance cost

of the business and makes debt capital cheaper than that of equity capital (Filin and et.al., 2020).

c. Calculation of profit per share for ordinary shareholders in 3rd and 4th year

In 3rd year

Particulars Options 1 Option 2

Profits available to ordinary

shareholders

75000 61000

Number of ordinary shares 5000000 5000000

Profit per share for ordinary

shareholders

0.015 0.0122

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In 4th year

Particulars Options 1 Option 2

Profits available to ordinary

shareholders

84000 70000

Number of ordinary shares 5000000 5000000

Profit per share for ordinary

shareholders

0.0168 0.014

d. Other means from which fund can be raised

Other than equity and debt instruments as mentioned above, there is another most important

sources from which the company can finance its business expansion is retained earnings

(Merianos and Gotsis, 2018). It is the fund that is available through company reserves which

they maintained for the surpluses left after distributing dividend to ordinary shareholders. The

funding available through this sources is the cheapest of all other sources as company need not

require to bear the cost of raising fund through external sources.

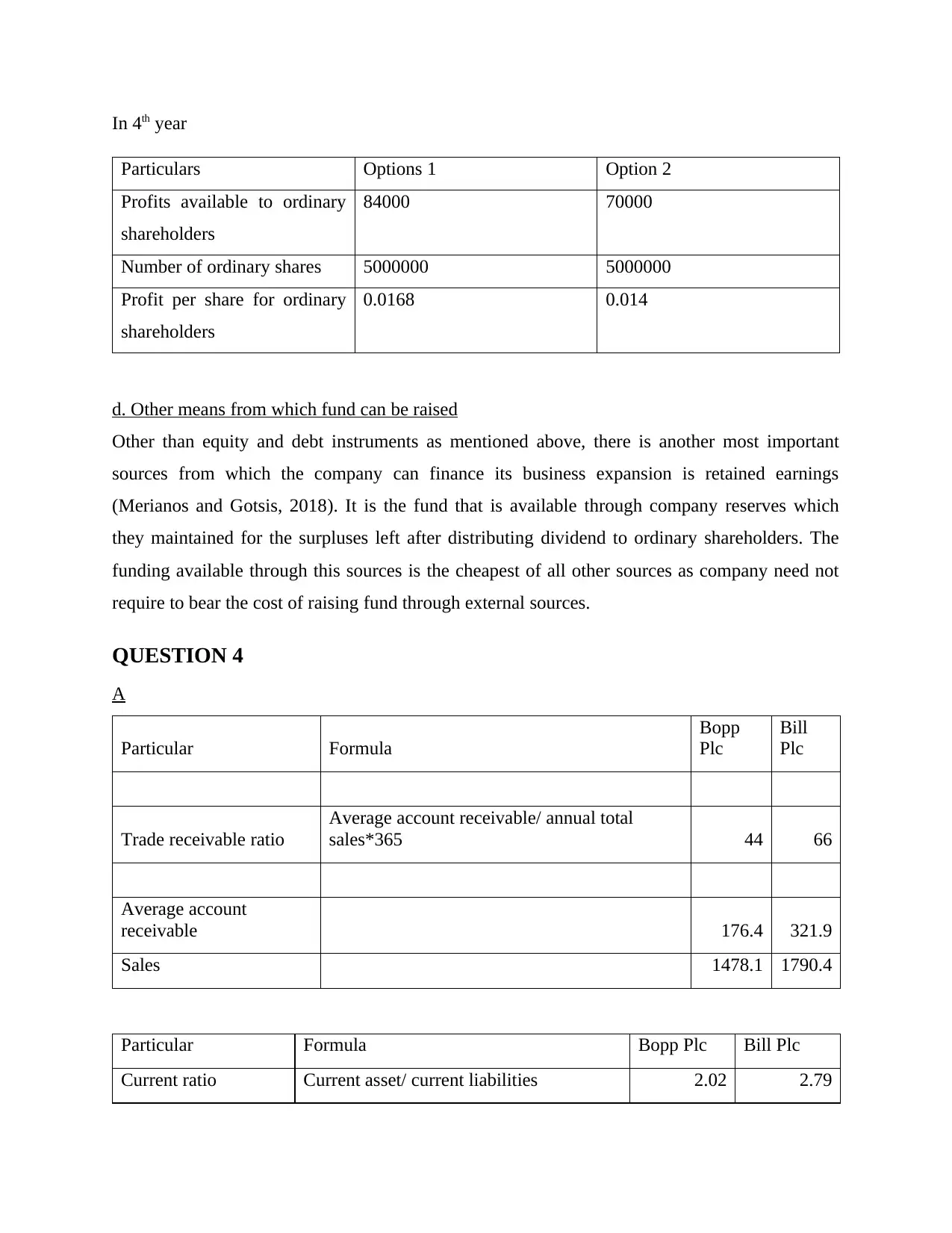

QUESTION 4

A

Particular Formula

Bopp

Plc

Bill

Plc

Trade receivable ratio

Average account receivable/ annual total

sales*365 44 66

Average account

receivable 176.4 321.9

Sales 1478.1 1790.4

Particular Formula Bopp Plc Bill Plc

Current ratio Current asset/ current liabilities 2.02 2.79

Particulars Options 1 Option 2

Profits available to ordinary

shareholders

84000 70000

Number of ordinary shares 5000000 5000000

Profit per share for ordinary

shareholders

0.0168 0.014

d. Other means from which fund can be raised

Other than equity and debt instruments as mentioned above, there is another most important

sources from which the company can finance its business expansion is retained earnings

(Merianos and Gotsis, 2018). It is the fund that is available through company reserves which

they maintained for the surpluses left after distributing dividend to ordinary shareholders. The

funding available through this sources is the cheapest of all other sources as company need not

require to bear the cost of raising fund through external sources.

QUESTION 4

A

Particular Formula

Bopp

Plc

Bill

Plc

Trade receivable ratio

Average account receivable/ annual total

sales*365 44 66

Average account

receivable 176.4 321.9

Sales 1478.1 1790.4

Particular Formula Bopp Plc Bill Plc

Current ratio Current asset/ current liabilities 2.02 2.79

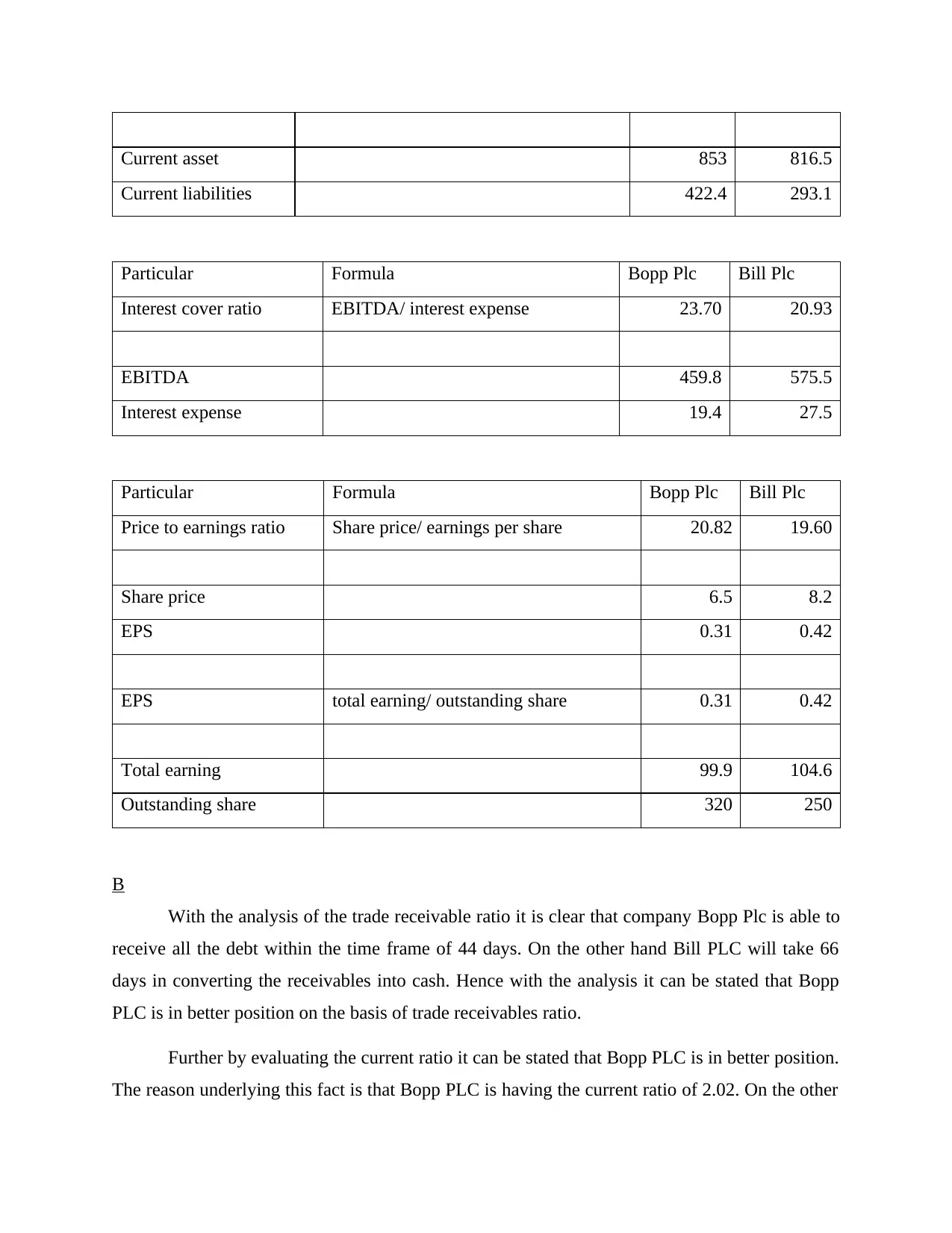

Current asset 853 816.5

Current liabilities 422.4 293.1

Particular Formula Bopp Plc Bill Plc

Interest cover ratio EBITDA/ interest expense 23.70 20.93

EBITDA 459.8 575.5

Interest expense 19.4 27.5

Particular Formula Bopp Plc Bill Plc

Price to earnings ratio Share price/ earnings per share 20.82 19.60

Share price 6.5 8.2

EPS 0.31 0.42

EPS total earning/ outstanding share 0.31 0.42

Total earning 99.9 104.6

Outstanding share 320 250

B

With the analysis of the trade receivable ratio it is clear that company Bopp Plc is able to

receive all the debt within the time frame of 44 days. On the other hand Bill PLC will take 66

days in converting the receivables into cash. Hence with the analysis it can be stated that Bopp

PLC is in better position on the basis of trade receivables ratio.

Further by evaluating the current ratio it can be stated that Bopp PLC is in better position.

The reason underlying this fact is that Bopp PLC is having the current ratio of 2.02. On the other

Current liabilities 422.4 293.1

Particular Formula Bopp Plc Bill Plc

Interest cover ratio EBITDA/ interest expense 23.70 20.93

EBITDA 459.8 575.5

Interest expense 19.4 27.5

Particular Formula Bopp Plc Bill Plc

Price to earnings ratio Share price/ earnings per share 20.82 19.60

Share price 6.5 8.2

EPS 0.31 0.42

EPS total earning/ outstanding share 0.31 0.42

Total earning 99.9 104.6

Outstanding share 320 250

B

With the analysis of the trade receivable ratio it is clear that company Bopp Plc is able to

receive all the debt within the time frame of 44 days. On the other hand Bill PLC will take 66

days in converting the receivables into cash. Hence with the analysis it can be stated that Bopp

PLC is in better position on the basis of trade receivables ratio.

Further by evaluating the current ratio it can be stated that Bopp PLC is in better position.

The reason underlying this fact is that Bopp PLC is having the current ratio of 2.02. On the other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.