Financial Analysis of Stratford Yachts Ltd

VerifiedAdded on 2020/06/04

|10

|2487

|36

AI Summary

This assignment requires a detailed financial analysis of Stratford Yachts Ltd. The analysis involves calculating and interpreting key financial ratios such as liquidity, profitability, and efficiency ratios to assess the company's financial health and performance. The report should highlight strengths and weaknesses in the company's financial position and provide recommendations for improvement in areas like profitability margin, debtors collection period, and operating expenses management.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Managing Financial Resources

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

1. Assessing difference between financial and management accounts..................................3

2. Defining purpose of Stratford Yachts Ltd and non-profit making units behind the

preparation of financial statements........................................................................................5

3. Presenting Stratford Yachts Ltd’s stakeholders and evaluating their information need....6

TASK 2......................................................................................................................................7

1. Analyzing financial performance of Stratford Yachts Ltd for the year ended on 2015 and

2016 through ratio analysis....................................................................................................7

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................10

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

1. Assessing difference between financial and management accounts..................................3

2. Defining purpose of Stratford Yachts Ltd and non-profit making units behind the

preparation of financial statements........................................................................................5

3. Presenting Stratford Yachts Ltd’s stakeholders and evaluating their information need....6

TASK 2......................................................................................................................................7

1. Analyzing financial performance of Stratford Yachts Ltd for the year ended on 2015 and

2016 through ratio analysis....................................................................................................7

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................10

INTRODUCTION

In the recent times, for gaining and sustaining competitive edge over others business

unit has to perform several activities such as promotional, R&D etc. For this purpose

company requires enough fund so it is the accountability of the manager to develop

prominent financial strategies. To manage financial resources more effectually business unit

needs to prioritize activities as per their importance in the context of growth or success. The

present report is based on case scenario of Stratford Yachts Ltd which is working or traded

from last 30 years. Business unit is highly concerned pertaining to its financial performance

that has changed in the recent times. Moreover, business unit still relies on traditional product

lines which seem unsuitable in the strategic environment. In this, report will provide deeper

insight about the manner in which financial accounts differs from management. It also entails

the purposes of Stratford Yachts Ltd behind the preparation of final accounts and highlights

its financial performance.

TASK 1

1. Assessing difference between financial and management accounts

Now, both financial and management accounting becomes the main part of business

unit. Hence, for attaining success and gaining competitive edge over others company prepares

reports by taking into account both the accounting systems. Thus, it is vital for the manager

of Stratford Yachts Ltd to understand differences that take place between financial and

management accounting which as follows:

Differential aspects Financial accounting Management accounting

Meaning FA places emphasis on

recording monetary records

associated with business unit.

Hence, financial statements

and reports which are

prepared on the basis of such

accounting system assists

manager as well as other

stakeholders in making

Management accounting

system lays focus on

maintaining records

pertaining to internal

operations. This in turn helps

manager in setting goals and

policies for the upcoming

time period.

In the recent times, for gaining and sustaining competitive edge over others business

unit has to perform several activities such as promotional, R&D etc. For this purpose

company requires enough fund so it is the accountability of the manager to develop

prominent financial strategies. To manage financial resources more effectually business unit

needs to prioritize activities as per their importance in the context of growth or success. The

present report is based on case scenario of Stratford Yachts Ltd which is working or traded

from last 30 years. Business unit is highly concerned pertaining to its financial performance

that has changed in the recent times. Moreover, business unit still relies on traditional product

lines which seem unsuitable in the strategic environment. In this, report will provide deeper

insight about the manner in which financial accounts differs from management. It also entails

the purposes of Stratford Yachts Ltd behind the preparation of final accounts and highlights

its financial performance.

TASK 1

1. Assessing difference between financial and management accounts

Now, both financial and management accounting becomes the main part of business

unit. Hence, for attaining success and gaining competitive edge over others company prepares

reports by taking into account both the accounting systems. Thus, it is vital for the manager

of Stratford Yachts Ltd to understand differences that take place between financial and

management accounting which as follows:

Differential aspects Financial accounting Management accounting

Meaning FA places emphasis on

recording monetary records

associated with business unit.

Hence, financial statements

and reports which are

prepared on the basis of such

accounting system assists

manager as well as other

stakeholders in making

Management accounting

system lays focus on

maintaining records

pertaining to internal

operations. This in turn helps

manager in setting goals and

policies for the upcoming

time period.

appropriate decision.

Aim or objective Motive behind financial

accounting practices is to

disclose monetary

information at the end of

accounting year (Warren and

Jones, 2018).

The main objective of

management accounting is

providing managers with

suitable information that can

be used for planning, setting

and evaluating goals.

Regulatory compliance Publicly listed companies are

accountable to prepare and

publish reports by following

accounting standards such as

GAAP and IFRS.

Such accounting is highly

depending on the discretion

of management. Irrespective

of not having mandatory

requirements some

frameworks are followed by

the firm.

Governance principles Accounts are prepared on the

basis of rules contained in

IFRS.

No standardization exists in

the preparation of

management accounts.

Time horizon or period In the context of financial

accounting, time horizon

implies for one year.

Management accounts are

prepared by the management

team as per their

requirements such as

monthly, quarterly, half

yearly.

Beneficiaries of report Reports that are based on

financial accounting provide

both internal and external

stakeholders with valuable

information for decision

making.

Management accounting

reports gives input to the

internal stakeholders such as

managers etc and thereby

helps in developing

competent strategies as well

as policy framework

(Difference between financial

and management accounting,

2018).

Aim or objective Motive behind financial

accounting practices is to

disclose monetary

information at the end of

accounting year (Warren and

Jones, 2018).

The main objective of

management accounting is

providing managers with

suitable information that can

be used for planning, setting

and evaluating goals.

Regulatory compliance Publicly listed companies are

accountable to prepare and

publish reports by following

accounting standards such as

GAAP and IFRS.

Such accounting is highly

depending on the discretion

of management. Irrespective

of not having mandatory

requirements some

frameworks are followed by

the firm.

Governance principles Accounts are prepared on the

basis of rules contained in

IFRS.

No standardization exists in

the preparation of

management accounts.

Time horizon or period In the context of financial

accounting, time horizon

implies for one year.

Management accounts are

prepared by the management

team as per their

requirements such as

monthly, quarterly, half

yearly.

Beneficiaries of report Reports that are based on

financial accounting provide

both internal and external

stakeholders with valuable

information for decision

making.

Management accounting

reports gives input to the

internal stakeholders such as

managers etc and thereby

helps in developing

competent strategies as well

as policy framework

(Difference between financial

and management accounting,

2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Focus By making focus on past

records reports are prepared

under financial accounting.

Unlike financial, under

management accounting

considering current

performance strategies are

prepared for the near future

regarding growth and

improvement.

2. Defining purpose of Stratford Yachts Ltd and non-profit making units behind the

preparation of financial statements

Financial statements contain record about business activities that can be measured in

quantitative terms. In order to assess monetary performance and meeting the need of

stakeholders Stratford Yachts Ltd focuses on preparing mainly three financial statements

which are as follows:

Income statement: Company prepares such statement to indentify how much income

is generated during the year in against to the expenses incurred. This statement renders

information about sales revenue, gross and net profit, direct as well as indirect expenses etc.

Hence, using such statement manager can develop strategies for the enhancement of sales

revenue and margin.

Balance sheet: Statement of financial position includes information about assets and

liabilities. The aim of company behind the preparation of balance is to evaluate liquidity,

solvency and efficiency aspects. Such statement helps company in determining source that

needs to be considered for raising fund in the near future (Kavussanos, Visvikis and

Alexopoulos, 2017). Besides this, balance sheet also gives indication about the extent to

which current assets need to be maintained for fulfilling obligations.

Statement of cash flows: Stratford Yachts Ltd prepares such statement for analyzing

operating, investing and financing activities that has contributed in both cash inflow as well

as outflow. Hence, by undertaking cash flow statement business unit can easily identify

activities that place negative influence on monetary position. Thus, by evaluating such

statement company can develop strategies for cash control (Merianos and Gotsis, 2018). By

doing this, firm would become able to employ excess cash in the other productive activities

or investments and thereby attain high margin.

records reports are prepared

under financial accounting.

Unlike financial, under

management accounting

considering current

performance strategies are

prepared for the near future

regarding growth and

improvement.

2. Defining purpose of Stratford Yachts Ltd and non-profit making units behind the

preparation of financial statements

Financial statements contain record about business activities that can be measured in

quantitative terms. In order to assess monetary performance and meeting the need of

stakeholders Stratford Yachts Ltd focuses on preparing mainly three financial statements

which are as follows:

Income statement: Company prepares such statement to indentify how much income

is generated during the year in against to the expenses incurred. This statement renders

information about sales revenue, gross and net profit, direct as well as indirect expenses etc.

Hence, using such statement manager can develop strategies for the enhancement of sales

revenue and margin.

Balance sheet: Statement of financial position includes information about assets and

liabilities. The aim of company behind the preparation of balance is to evaluate liquidity,

solvency and efficiency aspects. Such statement helps company in determining source that

needs to be considered for raising fund in the near future (Kavussanos, Visvikis and

Alexopoulos, 2017). Besides this, balance sheet also gives indication about the extent to

which current assets need to be maintained for fulfilling obligations.

Statement of cash flows: Stratford Yachts Ltd prepares such statement for analyzing

operating, investing and financing activities that has contributed in both cash inflow as well

as outflow. Hence, by undertaking cash flow statement business unit can easily identify

activities that place negative influence on monetary position. Thus, by evaluating such

statement company can develop strategies for cash control (Merianos and Gotsis, 2018). By

doing this, firm would become able to employ excess cash in the other productive activities

or investments and thereby attain high margin.

Unlike, profit making firm such as Stratford Yachts Ltd, NPO’s focuses on preparing

income and expenditure account. Objective of non-profit making units behind the preparation

of such account is to maintain proper record regarding receipts and payment. Hence, by

preparing such account non-profit can provide information about the source from where

receipts are generated and payment made during the specified time frame.

3. Presenting Stratford Yachts Ltd’s stakeholders and evaluating their information need

All the business units have some stakeholders, in terms of internal and external, who

have an interest in their operations. Hence, Stratford Yachts Ltd prepares financial statements

at the end of financial year and publishes the same. This in turn significantly aid in the

decision making aspect of both internal and external stakeholders.

Internal stakeholders

Management: Owners undertake final accounts to determine profitability of their

investments. Along with this, such statements also help owners in doing comparison

of current performance in against to past years and rival units (Davies, 2017). Thus,

referring such information managers of Stratford Yachts Ltd can determine future

course of action.

Employees: Stratford Yachts Ltd’s employees are highly interested in making

assessment of company’s profitability statement. This in turn helps them in

identifying or assessing the impact of company’s profit on their remuneration and job

security.

External stakeholders

Owners or investors: Financial statements are undertaken by both existing and

potential investors for the purpose of decision making regarding investment. Through

evaluating final accounts via ratio analysis investors can determine whether company

and its stocks will grow in the near future or not.

Trade creditors or suppliers: Usually, suppliers prefer to give credit to the customers

who make payment within the suitable time frame. Thus, for generating information

regarding such aspect both income statement and balance sheet is evaluated by the

suppliers (Introduction to accounting, 2018). Level of profit margin, assets and

liabilities help in determining the creditworthiness of suppliers in relation to making

payment on due date.

income and expenditure account. Objective of non-profit making units behind the preparation

of such account is to maintain proper record regarding receipts and payment. Hence, by

preparing such account non-profit can provide information about the source from where

receipts are generated and payment made during the specified time frame.

3. Presenting Stratford Yachts Ltd’s stakeholders and evaluating their information need

All the business units have some stakeholders, in terms of internal and external, who

have an interest in their operations. Hence, Stratford Yachts Ltd prepares financial statements

at the end of financial year and publishes the same. This in turn significantly aid in the

decision making aspect of both internal and external stakeholders.

Internal stakeholders

Management: Owners undertake final accounts to determine profitability of their

investments. Along with this, such statements also help owners in doing comparison

of current performance in against to past years and rival units (Davies, 2017). Thus,

referring such information managers of Stratford Yachts Ltd can determine future

course of action.

Employees: Stratford Yachts Ltd’s employees are highly interested in making

assessment of company’s profitability statement. This in turn helps them in

identifying or assessing the impact of company’s profit on their remuneration and job

security.

External stakeholders

Owners or investors: Financial statements are undertaken by both existing and

potential investors for the purpose of decision making regarding investment. Through

evaluating final accounts via ratio analysis investors can determine whether company

and its stocks will grow in the near future or not.

Trade creditors or suppliers: Usually, suppliers prefer to give credit to the customers

who make payment within the suitable time frame. Thus, for generating information

regarding such aspect both income statement and balance sheet is evaluated by the

suppliers (Introduction to accounting, 2018). Level of profit margin, assets and

liabilities help in determining the creditworthiness of suppliers in relation to making

payment on due date.

Lenders of financial institution: Banks assess credit worthiness of the company

before granting loan to it. Thus, statement of financial position is evaluated by the

institutions to ascertain the level of current debt level, assets and liabilities. It helps in

determining whether company is capable to pay interest and loan amount on time or

not.

Government or tax authorities: Regulatory and tax authorities are highly interested in

the financial statements of firm (Titman, Keown and Martin, 2017). Hence, for

determining and confirming tax obligations such authorities lay focus on the

evaluation of income statement.

TASK 2

1. Analyzing financial performance of Stratford Yachts Ltd for the year ended on 2015 and

2016 through ratio analysis

Ratio analysis: It is the most effectual form of financial statement analysis that

investors undertake for evaluating and monitoring performance of the company in several key

areas. This technique facilitates comparison of monetary aspects over the years and in against

to the industry average (Barr, 2018). By taking into account such tool Stratford Yachts Ltd

itself and its stakeholders can measure performance under several key areas such as

profitability, liquidity, solvency and efficiency.

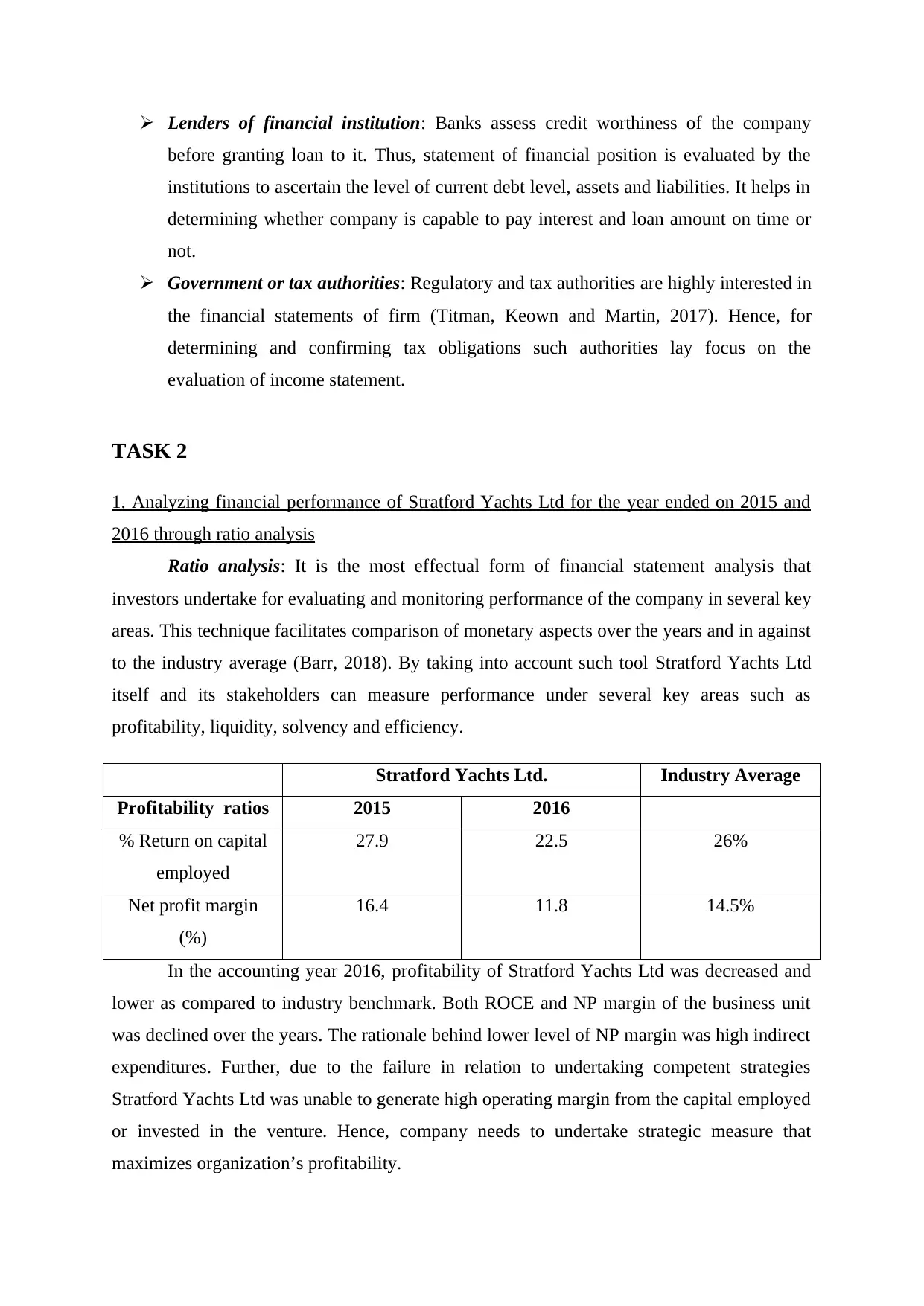

Stratford Yachts Ltd. Industry Average

Profitability ratios 2015 2016

% Return on capital

employed

27.9 22.5 26%

Net profit margin

(%)

16.4 11.8 14.5%

In the accounting year 2016, profitability of Stratford Yachts Ltd was decreased and

lower as compared to industry benchmark. Both ROCE and NP margin of the business unit

was declined over the years. The rationale behind lower level of NP margin was high indirect

expenditures. Further, due to the failure in relation to undertaking competent strategies

Stratford Yachts Ltd was unable to generate high operating margin from the capital employed

or invested in the venture. Hence, company needs to undertake strategic measure that

maximizes organization’s profitability.

before granting loan to it. Thus, statement of financial position is evaluated by the

institutions to ascertain the level of current debt level, assets and liabilities. It helps in

determining whether company is capable to pay interest and loan amount on time or

not.

Government or tax authorities: Regulatory and tax authorities are highly interested in

the financial statements of firm (Titman, Keown and Martin, 2017). Hence, for

determining and confirming tax obligations such authorities lay focus on the

evaluation of income statement.

TASK 2

1. Analyzing financial performance of Stratford Yachts Ltd for the year ended on 2015 and

2016 through ratio analysis

Ratio analysis: It is the most effectual form of financial statement analysis that

investors undertake for evaluating and monitoring performance of the company in several key

areas. This technique facilitates comparison of monetary aspects over the years and in against

to the industry average (Barr, 2018). By taking into account such tool Stratford Yachts Ltd

itself and its stakeholders can measure performance under several key areas such as

profitability, liquidity, solvency and efficiency.

Stratford Yachts Ltd. Industry Average

Profitability ratios 2015 2016

% Return on capital

employed

27.9 22.5 26%

Net profit margin

(%)

16.4 11.8 14.5%

In the accounting year 2016, profitability of Stratford Yachts Ltd was decreased and

lower as compared to industry benchmark. Both ROCE and NP margin of the business unit

was declined over the years. The rationale behind lower level of NP margin was high indirect

expenditures. Further, due to the failure in relation to undertaking competent strategies

Stratford Yachts Ltd was unable to generate high operating margin from the capital employed

or invested in the venture. Hence, company needs to undertake strategic measure that

maximizes organization’s profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

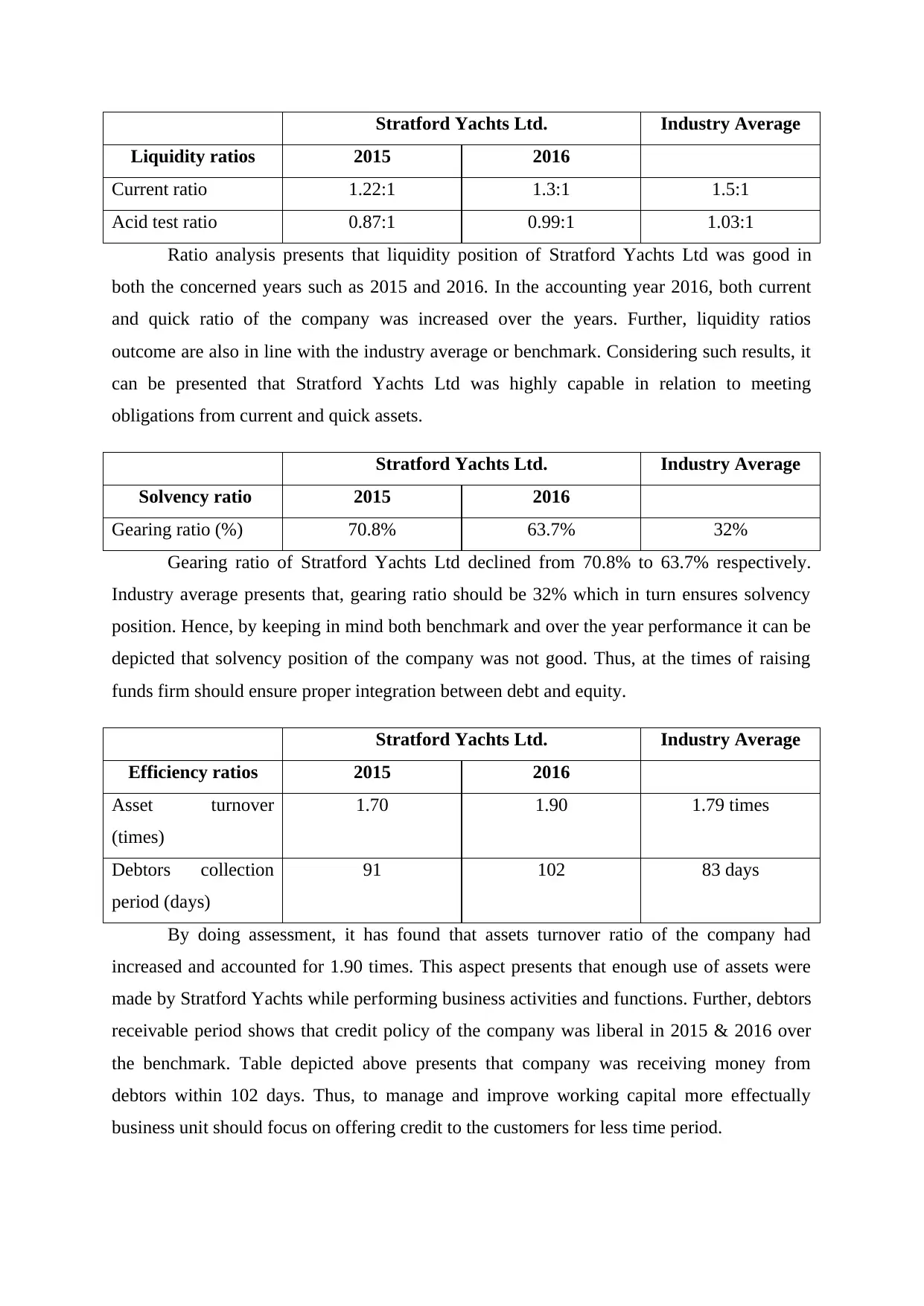

Stratford Yachts Ltd. Industry Average

Liquidity ratios 2015 2016

Current ratio 1.22:1 1.3:1 1.5:1

Acid test ratio 0.87:1 0.99:1 1.03:1

Ratio analysis presents that liquidity position of Stratford Yachts Ltd was good in

both the concerned years such as 2015 and 2016. In the accounting year 2016, both current

and quick ratio of the company was increased over the years. Further, liquidity ratios

outcome are also in line with the industry average or benchmark. Considering such results, it

can be presented that Stratford Yachts Ltd was highly capable in relation to meeting

obligations from current and quick assets.

Stratford Yachts Ltd. Industry Average

Solvency ratio 2015 2016

Gearing ratio (%) 70.8% 63.7% 32%

Gearing ratio of Stratford Yachts Ltd declined from 70.8% to 63.7% respectively.

Industry average presents that, gearing ratio should be 32% which in turn ensures solvency

position. Hence, by keeping in mind both benchmark and over the year performance it can be

depicted that solvency position of the company was not good. Thus, at the times of raising

funds firm should ensure proper integration between debt and equity.

Stratford Yachts Ltd. Industry Average

Efficiency ratios 2015 2016

Asset turnover

(times)

1.70 1.90 1.79 times

Debtors collection

period (days)

91 102 83 days

By doing assessment, it has found that assets turnover ratio of the company had

increased and accounted for 1.90 times. This aspect presents that enough use of assets were

made by Stratford Yachts while performing business activities and functions. Further, debtors

receivable period shows that credit policy of the company was liberal in 2015 & 2016 over

the benchmark. Table depicted above presents that company was receiving money from

debtors within 102 days. Thus, to manage and improve working capital more effectually

business unit should focus on offering credit to the customers for less time period.

Liquidity ratios 2015 2016

Current ratio 1.22:1 1.3:1 1.5:1

Acid test ratio 0.87:1 0.99:1 1.03:1

Ratio analysis presents that liquidity position of Stratford Yachts Ltd was good in

both the concerned years such as 2015 and 2016. In the accounting year 2016, both current

and quick ratio of the company was increased over the years. Further, liquidity ratios

outcome are also in line with the industry average or benchmark. Considering such results, it

can be presented that Stratford Yachts Ltd was highly capable in relation to meeting

obligations from current and quick assets.

Stratford Yachts Ltd. Industry Average

Solvency ratio 2015 2016

Gearing ratio (%) 70.8% 63.7% 32%

Gearing ratio of Stratford Yachts Ltd declined from 70.8% to 63.7% respectively.

Industry average presents that, gearing ratio should be 32% which in turn ensures solvency

position. Hence, by keeping in mind both benchmark and over the year performance it can be

depicted that solvency position of the company was not good. Thus, at the times of raising

funds firm should ensure proper integration between debt and equity.

Stratford Yachts Ltd. Industry Average

Efficiency ratios 2015 2016

Asset turnover

(times)

1.70 1.90 1.79 times

Debtors collection

period (days)

91 102 83 days

By doing assessment, it has found that assets turnover ratio of the company had

increased and accounted for 1.90 times. This aspect presents that enough use of assets were

made by Stratford Yachts while performing business activities and functions. Further, debtors

receivable period shows that credit policy of the company was liberal in 2015 & 2016 over

the benchmark. Table depicted above presents that company was receiving money from

debtors within 102 days. Thus, to manage and improve working capital more effectually

business unit should focus on offering credit to the customers for less time period.

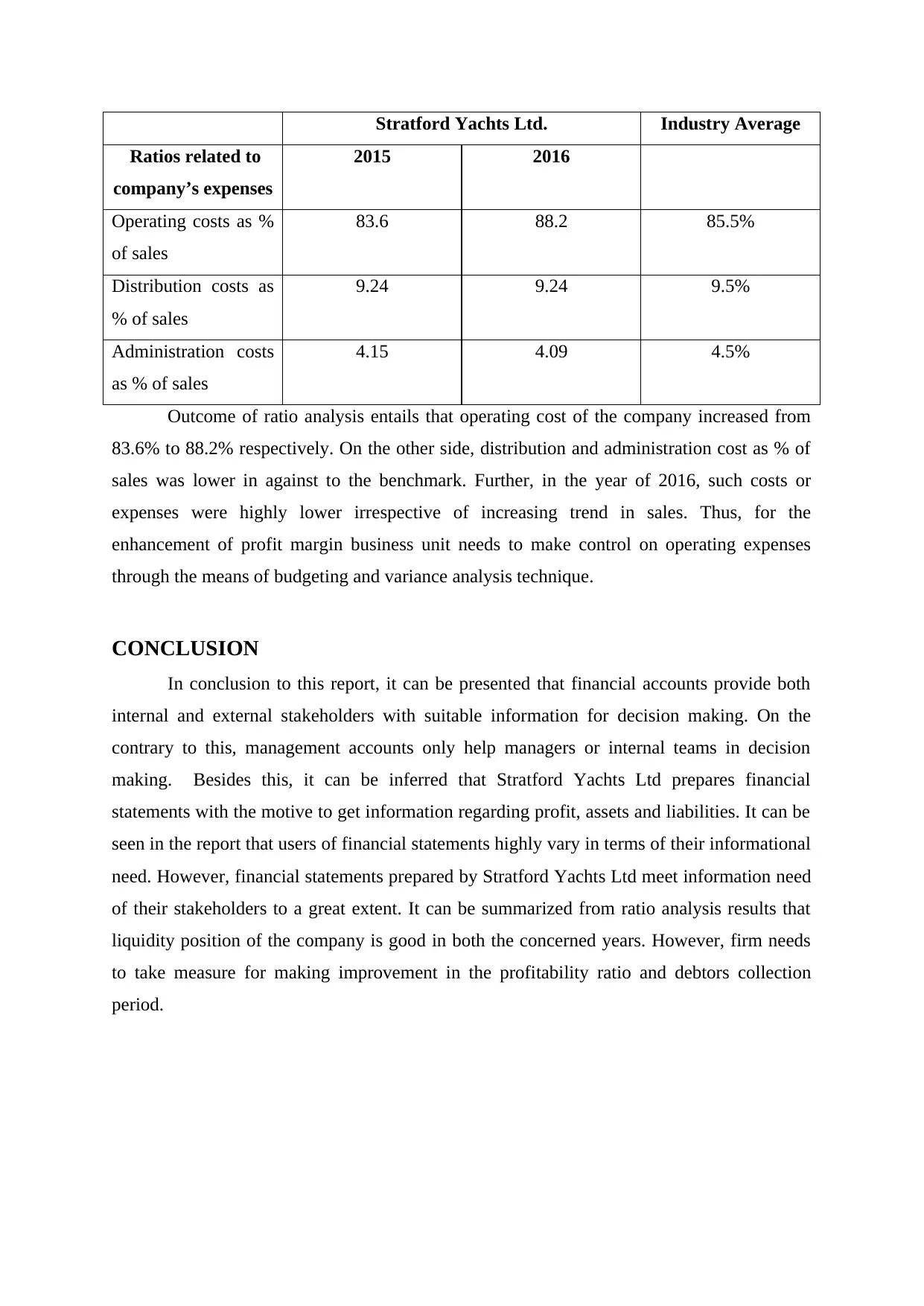

Stratford Yachts Ltd. Industry Average

Ratios related to

company’s expenses

2015 2016

Operating costs as %

of sales

83.6 88.2 85.5%

Distribution costs as

% of sales

9.24 9.24 9.5%

Administration costs

as % of sales

4.15 4.09 4.5%

Outcome of ratio analysis entails that operating cost of the company increased from

83.6% to 88.2% respectively. On the other side, distribution and administration cost as % of

sales was lower in against to the benchmark. Further, in the year of 2016, such costs or

expenses were highly lower irrespective of increasing trend in sales. Thus, for the

enhancement of profit margin business unit needs to make control on operating expenses

through the means of budgeting and variance analysis technique.

CONCLUSION

In conclusion to this report, it can be presented that financial accounts provide both

internal and external stakeholders with suitable information for decision making. On the

contrary to this, management accounts only help managers or internal teams in decision

making. Besides this, it can be inferred that Stratford Yachts Ltd prepares financial

statements with the motive to get information regarding profit, assets and liabilities. It can be

seen in the report that users of financial statements highly vary in terms of their informational

need. However, financial statements prepared by Stratford Yachts Ltd meet information need

of their stakeholders to a great extent. It can be summarized from ratio analysis results that

liquidity position of the company is good in both the concerned years. However, firm needs

to take measure for making improvement in the profitability ratio and debtors collection

period.

Ratios related to

company’s expenses

2015 2016

Operating costs as %

of sales

83.6 88.2 85.5%

Distribution costs as

% of sales

9.24 9.24 9.5%

Administration costs

as % of sales

4.15 4.09 4.5%

Outcome of ratio analysis entails that operating cost of the company increased from

83.6% to 88.2% respectively. On the other side, distribution and administration cost as % of

sales was lower in against to the benchmark. Further, in the year of 2016, such costs or

expenses were highly lower irrespective of increasing trend in sales. Thus, for the

enhancement of profit margin business unit needs to make control on operating expenses

through the means of budgeting and variance analysis technique.

CONCLUSION

In conclusion to this report, it can be presented that financial accounts provide both

internal and external stakeholders with suitable information for decision making. On the

contrary to this, management accounts only help managers or internal teams in decision

making. Besides this, it can be inferred that Stratford Yachts Ltd prepares financial

statements with the motive to get information regarding profit, assets and liabilities. It can be

seen in the report that users of financial statements highly vary in terms of their informational

need. However, financial statements prepared by Stratford Yachts Ltd meet information need

of their stakeholders to a great extent. It can be summarized from ratio analysis results that

liquidity position of the company is good in both the concerned years. However, firm needs

to take measure for making improvement in the profitability ratio and debtors collection

period.

REFERENCES

Books and Journals

Barr, M. J., 2018. Budgets and financial management in higher education. John Wiley &

Sons.

Davies, D., 2017. Managing financial information. Kogan Page Publishers.

Kavussanos, M. G., Visvikis, I. D. and Alexopoulos, I., 2017. Managing Financial Resources

in Shipping. In Shipping Operations Management (pp. 153-175). Springer, Cham.

Merianos, G. and Gotsis, G., 2018. Managing Financial Resources in Late Antiquity: Greek

Fathers' Views on Hoarding and Saving. Springer.

Titman, S., Keown, A. J. and Martin, J. D., 2017. Financial management: Principles and

applications. Pearson.

Warren, C. S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Online

Difference between financial and management accounting. 2018. [Online]. Available

through:

<https://www.diffen.com/difference/Financial_Accounting_vs_Management_Accounting

>.

Introduction to accounting. 2018. [Online]. Available through: <http://accounting-

simplified.com/financial/users-of-accounting-information.html>.

Books and Journals

Barr, M. J., 2018. Budgets and financial management in higher education. John Wiley &

Sons.

Davies, D., 2017. Managing financial information. Kogan Page Publishers.

Kavussanos, M. G., Visvikis, I. D. and Alexopoulos, I., 2017. Managing Financial Resources

in Shipping. In Shipping Operations Management (pp. 153-175). Springer, Cham.

Merianos, G. and Gotsis, G., 2018. Managing Financial Resources in Late Antiquity: Greek

Fathers' Views on Hoarding and Saving. Springer.

Titman, S., Keown, A. J. and Martin, J. D., 2017. Financial management: Principles and

applications. Pearson.

Warren, C. S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Online

Difference between financial and management accounting. 2018. [Online]. Available

through:

<https://www.diffen.com/difference/Financial_Accounting_vs_Management_Accounting

>.

Introduction to accounting. 2018. [Online]. Available through: <http://accounting-

simplified.com/financial/users-of-accounting-information.html>.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.