BA4F04 - Financial Resources Management: Financial Performance

VerifiedAdded on 2024/06/04

|13

|2563

|153

Report

AI Summary

This report provides a comprehensive financial analysis of Stratford Yachts Ltd., differentiating between management and financial accounting and outlining key financial statements used by both profit and non-profit organizations. It identifies various stakeholders and their specific information needs, f...

Unit BA4F04 Managing Financial

Resources

1

Resources

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary:

The project offers insights into the difference between management and financial

accounting where one is made for internal decision and other for external decision

making, and then it explains the different financial statements which are used in profit and

non-profit organizations. It further explains different stakeholders and the information

required by them form the Stratford Yachts Ltd. Further, there are calculations of

important ratios which show that the company is performing well in most areas. Finally, it

has been recommended that the company should reduce its costs to increase its

profitability and improve its collection period.

2

The project offers insights into the difference between management and financial

accounting where one is made for internal decision and other for external decision

making, and then it explains the different financial statements which are used in profit and

non-profit organizations. It further explains different stakeholders and the information

required by them form the Stratford Yachts Ltd. Further, there are calculations of

important ratios which show that the company is performing well in most areas. Finally, it

has been recommended that the company should reduce its costs to increase its

profitability and improve its collection period.

2

Introduction

The project starts with the difference between management and financial accounts and

then it explains various financial statements of the profit and non-profit organizations. It

further adds the information required by various stakeholders in the Stratford Yachts Ltd.

In the next task calculation of various ratios has been done and a detailed report about

the profitability of the firm has been made. The project ends with a recommendation

which is made to the company.

3

The project starts with the difference between management and financial accounts and

then it explains various financial statements of the profit and non-profit organizations. It

further adds the information required by various stakeholders in the Stratford Yachts Ltd.

In the next task calculation of various ratios has been done and a detailed report about

the profitability of the firm has been made. The project ends with a recommendation

which is made to the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

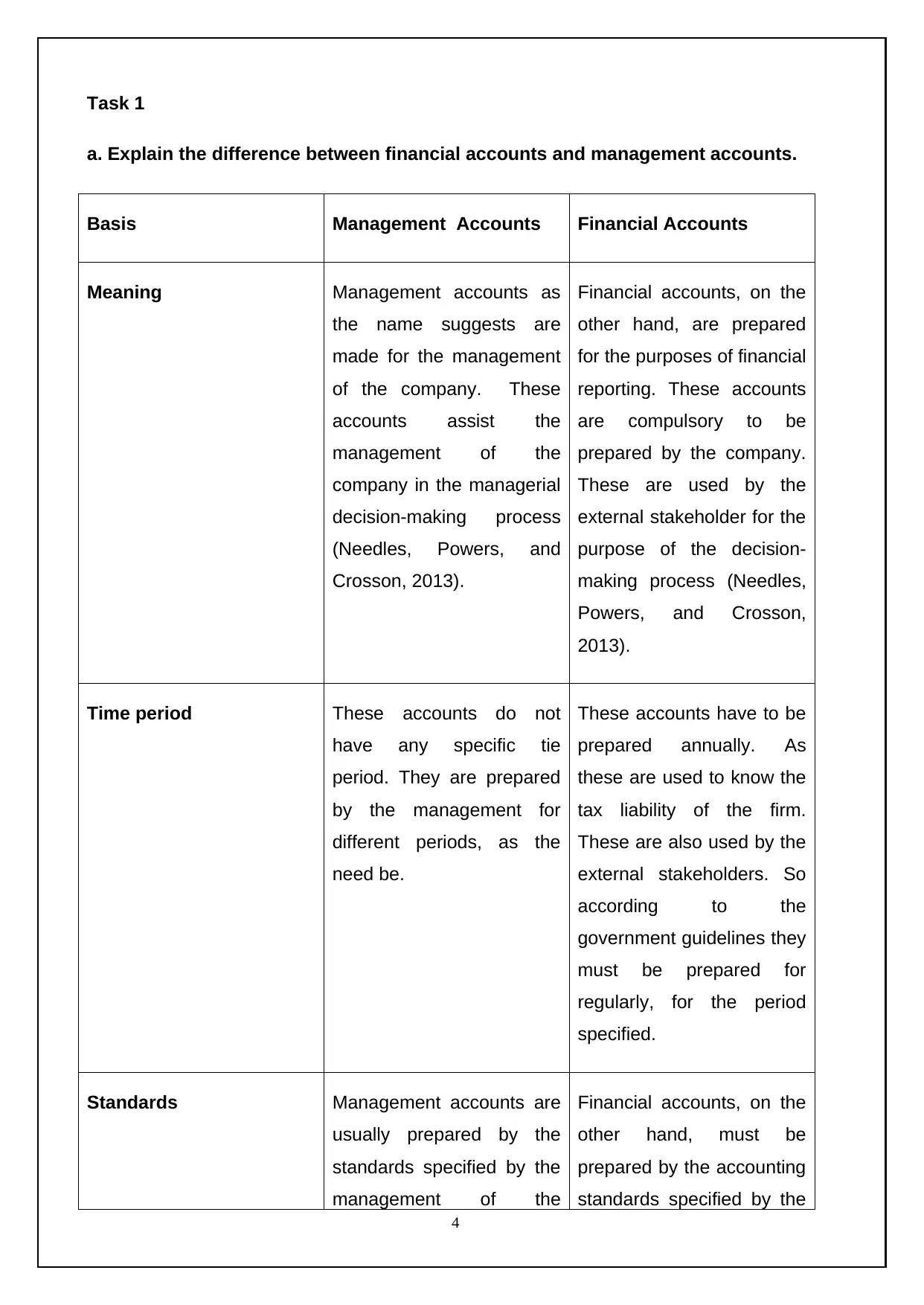

Task 1

a. Explain the difference between financial accounts and management accounts.

Basis Management Accounts Financial Accounts

Meaning Management accounts as

the name suggests are

made for the management

of the company. These

accounts assist the

management of the

company in the managerial

decision-making process

(Needles, Powers, and

Crosson, 2013).

Financial accounts, on the

other hand, are prepared

for the purposes of financial

reporting. These accounts

are compulsory to be

prepared by the company.

These are used by the

external stakeholder for the

purpose of the decision-

making process (Needles,

Powers, and Crosson,

2013).

Time period These accounts do not

have any specific tie

period. They are prepared

by the management for

different periods, as the

need be.

These accounts have to be

prepared annually. As

these are used to know the

tax liability of the firm.

These are also used by the

external stakeholders. So

according to the

government guidelines they

must be prepared for

regularly, for the period

specified.

Standards Management accounts are

usually prepared by the

standards specified by the

management of the

Financial accounts, on the

other hand, must be

prepared by the accounting

standards specified by the

4

a. Explain the difference between financial accounts and management accounts.

Basis Management Accounts Financial Accounts

Meaning Management accounts as

the name suggests are

made for the management

of the company. These

accounts assist the

management of the

company in the managerial

decision-making process

(Needles, Powers, and

Crosson, 2013).

Financial accounts, on the

other hand, are prepared

for the purposes of financial

reporting. These accounts

are compulsory to be

prepared by the company.

These are used by the

external stakeholder for the

purpose of the decision-

making process (Needles,

Powers, and Crosson,

2013).

Time period These accounts do not

have any specific tie

period. They are prepared

by the management for

different periods, as the

need be.

These accounts have to be

prepared annually. As

these are used to know the

tax liability of the firm.

These are also used by the

external stakeholders. So

according to the

government guidelines they

must be prepared for

regularly, for the period

specified.

Standards Management accounts are

usually prepared by the

standards specified by the

management of the

Financial accounts, on the

other hand, must be

prepared by the accounting

standards specified by the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

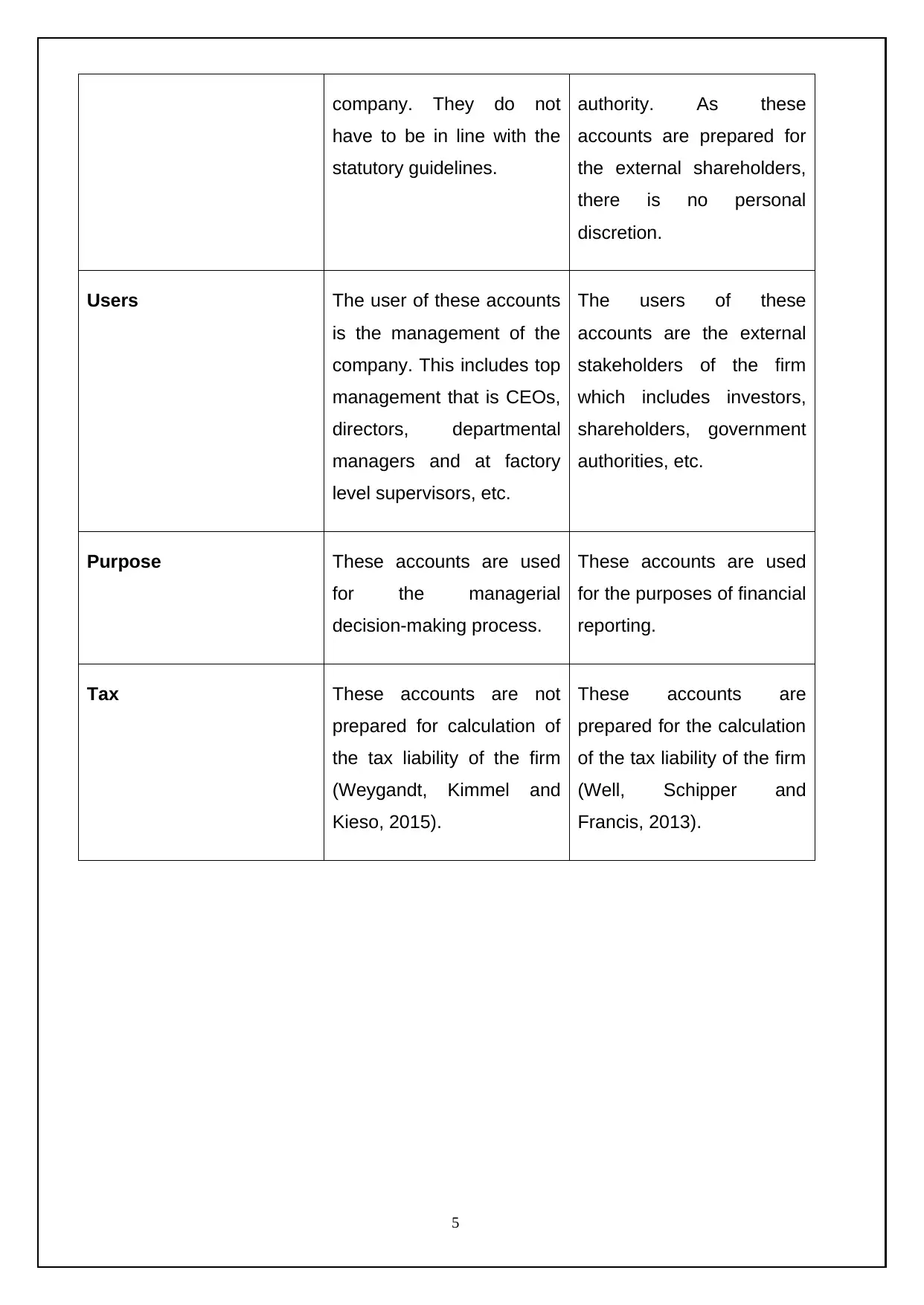

company. They do not

have to be in line with the

statutory guidelines.

authority. As these

accounts are prepared for

the external shareholders,

there is no personal

discretion.

Users The user of these accounts

is the management of the

company. This includes top

management that is CEOs,

directors, departmental

managers and at factory

level supervisors, etc.

The users of these

accounts are the external

stakeholders of the firm

which includes investors,

shareholders, government

authorities, etc.

Purpose These accounts are used

for the managerial

decision-making process.

These accounts are used

for the purposes of financial

reporting.

Tax These accounts are not

prepared for calculation of

the tax liability of the firm

(Weygandt, Kimmel and

Kieso, 2015).

These accounts are

prepared for the calculation

of the tax liability of the firm

(Well, Schipper and

Francis, 2013).

5

have to be in line with the

statutory guidelines.

authority. As these

accounts are prepared for

the external shareholders,

there is no personal

discretion.

Users The user of these accounts

is the management of the

company. This includes top

management that is CEOs,

directors, departmental

managers and at factory

level supervisors, etc.

The users of these

accounts are the external

stakeholders of the firm

which includes investors,

shareholders, government

authorities, etc.

Purpose These accounts are used

for the managerial

decision-making process.

These accounts are used

for the purposes of financial

reporting.

Tax These accounts are not

prepared for calculation of

the tax liability of the firm

(Weygandt, Kimmel and

Kieso, 2015).

These accounts are

prepared for the calculation

of the tax liability of the firm

(Well, Schipper and

Francis, 2013).

5

b. The purpose of various financial statements in a profit and non- profit

organizations.

Financial statements

Financial statements are the financial records of the company which show the financial

transactions for the previous year. These statements show the net income of the

company along with its sources, the tax liability of the firm and statement of the assets

and liabilities of the firm at the end of the accounting period.

For-profit organizations

Income statement

Income statement of the for-profit firms shows all the expenses and revenues of the firm.

These are used to calculate the tax liability of the firm. Finally, the amount left after

paying taxes is considered as profit which is either transferred to the balance sheet

under owner’s funds or is send to the profit and loss appropriation account to carry out

appropriations.

Balance sheet

The balance sheet of the for-profit entity represents the position of its assets and

liabilities on the last day of the accounting year. These statements are prepared to show

the financial position of the firm at the end of the year to its stakeholders. These

statements are used for the purpose of making decisions by the investors.

Statement of cash flows

The statement of cash flows represents the position of cash flow for the company. This

statement is prepared to know the cash position of the firm They help the managers of

the firm to know the liquidity position of the firm and make a vital decision about making

the investment. It also shows if a company is going to face a financial crisis in the future

and ensures that the management will take the necessary action to prevent it (Lee and

Parker, 2013).

For non-profit organizations

Statement of financial position

6

organizations.

Financial statements

Financial statements are the financial records of the company which show the financial

transactions for the previous year. These statements show the net income of the

company along with its sources, the tax liability of the firm and statement of the assets

and liabilities of the firm at the end of the accounting period.

For-profit organizations

Income statement

Income statement of the for-profit firms shows all the expenses and revenues of the firm.

These are used to calculate the tax liability of the firm. Finally, the amount left after

paying taxes is considered as profit which is either transferred to the balance sheet

under owner’s funds or is send to the profit and loss appropriation account to carry out

appropriations.

Balance sheet

The balance sheet of the for-profit entity represents the position of its assets and

liabilities on the last day of the accounting year. These statements are prepared to show

the financial position of the firm at the end of the year to its stakeholders. These

statements are used for the purpose of making decisions by the investors.

Statement of cash flows

The statement of cash flows represents the position of cash flow for the company. This

statement is prepared to know the cash position of the firm They help the managers of

the firm to know the liquidity position of the firm and make a vital decision about making

the investment. It also shows if a company is going to face a financial crisis in the future

and ensures that the management will take the necessary action to prevent it (Lee and

Parker, 2013).

For non-profit organizations

Statement of financial position

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This statement is like to the balance sheet of the for-profit company. The difference is

that the net assets section takes place of the equity section that is used in the for-profit

financial statements. Secondly. The assets section of the balance sheet is divided into

unrestricted, permanently restricted and temporarily restricted net assets (Drucker, 2012).

Statement of activities

This statement shows the revenues and expenses of the non-profit for the reporting

period. Thee revenues and expenses of the firm are divided into three categories namely

unrestricted, permanently restricted and temporarily restricted. The revenue can be from

the following sources contribution, member dues, grants and program fees. The expense

of the entity includes program expenses and support service expenses. After the above

calculation, the net effect of the above statement will be shown as a change in net assets

(Drucker, 2012).

Statement of cash flows

These statements show the cash inflows and cash outflows of the firm. This statement is

important as the statement of cash flows is not based on the accrual principle of

accounting which says that the accounting transactions are recording in the books of

accounts when they take place not when they are settled in cash. This creates a

misbalance in the cash balances of the firm. Cash flow statement aims to correct this by

only recording cash transactions Further noncash transaction are also removed and it

helps to know the real cash balances of the firm (Anheeler, 2014).

Statement of functional expenses

This statement is used to show how expenses are incurred for each functional area of a

non-profit entity. The functional areas of the non-profit entity include –

Management and administration

Fundraising

Programs (Anheeler, 2014)

7

that the net assets section takes place of the equity section that is used in the for-profit

financial statements. Secondly. The assets section of the balance sheet is divided into

unrestricted, permanently restricted and temporarily restricted net assets (Drucker, 2012).

Statement of activities

This statement shows the revenues and expenses of the non-profit for the reporting

period. Thee revenues and expenses of the firm are divided into three categories namely

unrestricted, permanently restricted and temporarily restricted. The revenue can be from

the following sources contribution, member dues, grants and program fees. The expense

of the entity includes program expenses and support service expenses. After the above

calculation, the net effect of the above statement will be shown as a change in net assets

(Drucker, 2012).

Statement of cash flows

These statements show the cash inflows and cash outflows of the firm. This statement is

important as the statement of cash flows is not based on the accrual principle of

accounting which says that the accounting transactions are recording in the books of

accounts when they take place not when they are settled in cash. This creates a

misbalance in the cash balances of the firm. Cash flow statement aims to correct this by

only recording cash transactions Further noncash transaction are also removed and it

helps to know the real cash balances of the firm (Anheeler, 2014).

Statement of functional expenses

This statement is used to show how expenses are incurred for each functional area of a

non-profit entity. The functional areas of the non-profit entity include –

Management and administration

Fundraising

Programs (Anheeler, 2014)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. Identify the various groups of stakeholders and evaluate their different

information needs.

The various group's shareholders in the Stratford Yachts Ltd. are –

Internal stakeholders

These stakeholders are within Stratford Yachts Ltd.

Employees

The employees of a Stratford Yachts Ltd. work help the company to achieve its

objectives by performing their duties. They need information regarding payment rate in

the company, security of the job they are performing, respect while performing the

duties, appreciation for the work done and recognition in the company.

Owner

The owners of the firm want to know whether the firm is performing in the best possible

manner. They do so by analyzing the financial statements of the business. They are

interested in profitability, market standing, and longevity.

External stakeholders

These stakeholders are outside Stratford Yachts Ltd.

Suppliers

The suppliers include individuals who supply goods and services to the Stratford Yachts

Ltd. They want to know about the long-term health of the company as they supply their

products on credit.

Investors

The investors in Stratford Yachts Ltd. have invested their money in the company. They

want to know their return on investment and income from the investment made. They are

also interested to know about the financial position of the company as their money is

invested in the company.

8

information needs.

The various group's shareholders in the Stratford Yachts Ltd. are –

Internal stakeholders

These stakeholders are within Stratford Yachts Ltd.

Employees

The employees of a Stratford Yachts Ltd. work help the company to achieve its

objectives by performing their duties. They need information regarding payment rate in

the company, security of the job they are performing, respect while performing the

duties, appreciation for the work done and recognition in the company.

Owner

The owners of the firm want to know whether the firm is performing in the best possible

manner. They do so by analyzing the financial statements of the business. They are

interested in profitability, market standing, and longevity.

External stakeholders

These stakeholders are outside Stratford Yachts Ltd.

Suppliers

The suppliers include individuals who supply goods and services to the Stratford Yachts

Ltd. They want to know about the long-term health of the company as they supply their

products on credit.

Investors

The investors in Stratford Yachts Ltd. have invested their money in the company. They

want to know their return on investment and income from the investment made. They are

also interested to know about the financial position of the company as their money is

invested in the company.

8

Task 2

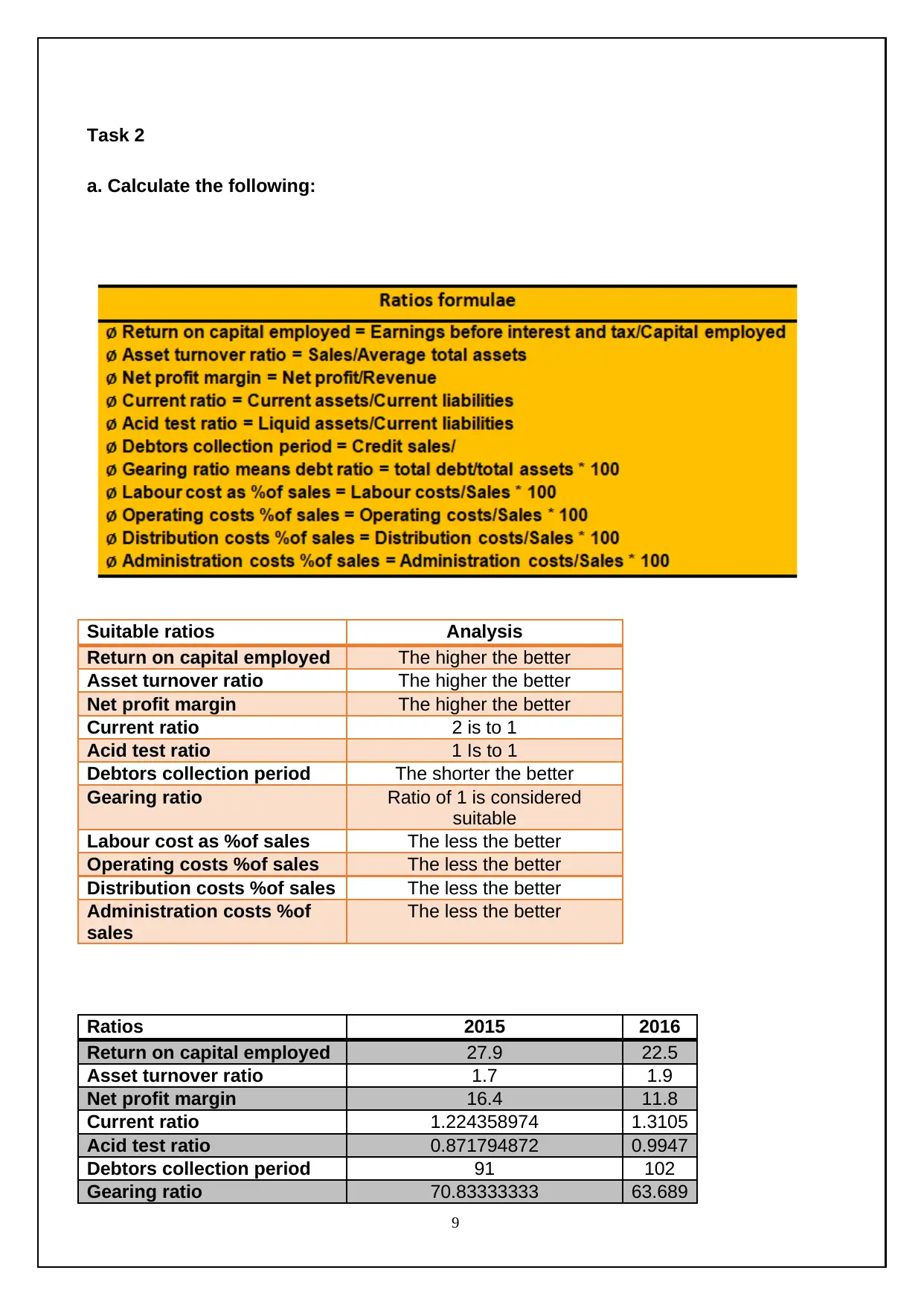

a. Calculate the following:

Suitable ratios Analysis

Return on capital employed The higher the better

Asset turnover ratio The higher the better

Net profit margin The higher the better

Current ratio 2 is to 1

Acid test ratio 1 Is to 1

Debtors collection period The shorter the better

Gearing ratio Ratio of 1 is considered

suitable

Labour cost as %of sales The less the better

Operating costs %of sales The less the better

Distribution costs %of sales The less the better

Administration costs %of

sales

The less the better

Ratios 2015 2016

Return on capital employed 27.9 22.5

Asset turnover ratio 1.7 1.9

Net profit margin 16.4 11.8

Current ratio 1.224358974 1.3105

Acid test ratio 0.871794872 0.9947

Debtors collection period 91 102

Gearing ratio 70.83333333 63.689

9

a. Calculate the following:

Suitable ratios Analysis

Return on capital employed The higher the better

Asset turnover ratio The higher the better

Net profit margin The higher the better

Current ratio 2 is to 1

Acid test ratio 1 Is to 1

Debtors collection period The shorter the better

Gearing ratio Ratio of 1 is considered

suitable

Labour cost as %of sales The less the better

Operating costs %of sales The less the better

Distribution costs %of sales The less the better

Administration costs %of

sales

The less the better

Ratios 2015 2016

Return on capital employed 27.9 22.5

Asset turnover ratio 1.7 1.9

Net profit margin 16.4 11.8

Current ratio 1.224358974 1.3105

Acid test ratio 0.871794872 0.9947

Debtors collection period 91 102

Gearing ratio 70.83333333 63.689

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

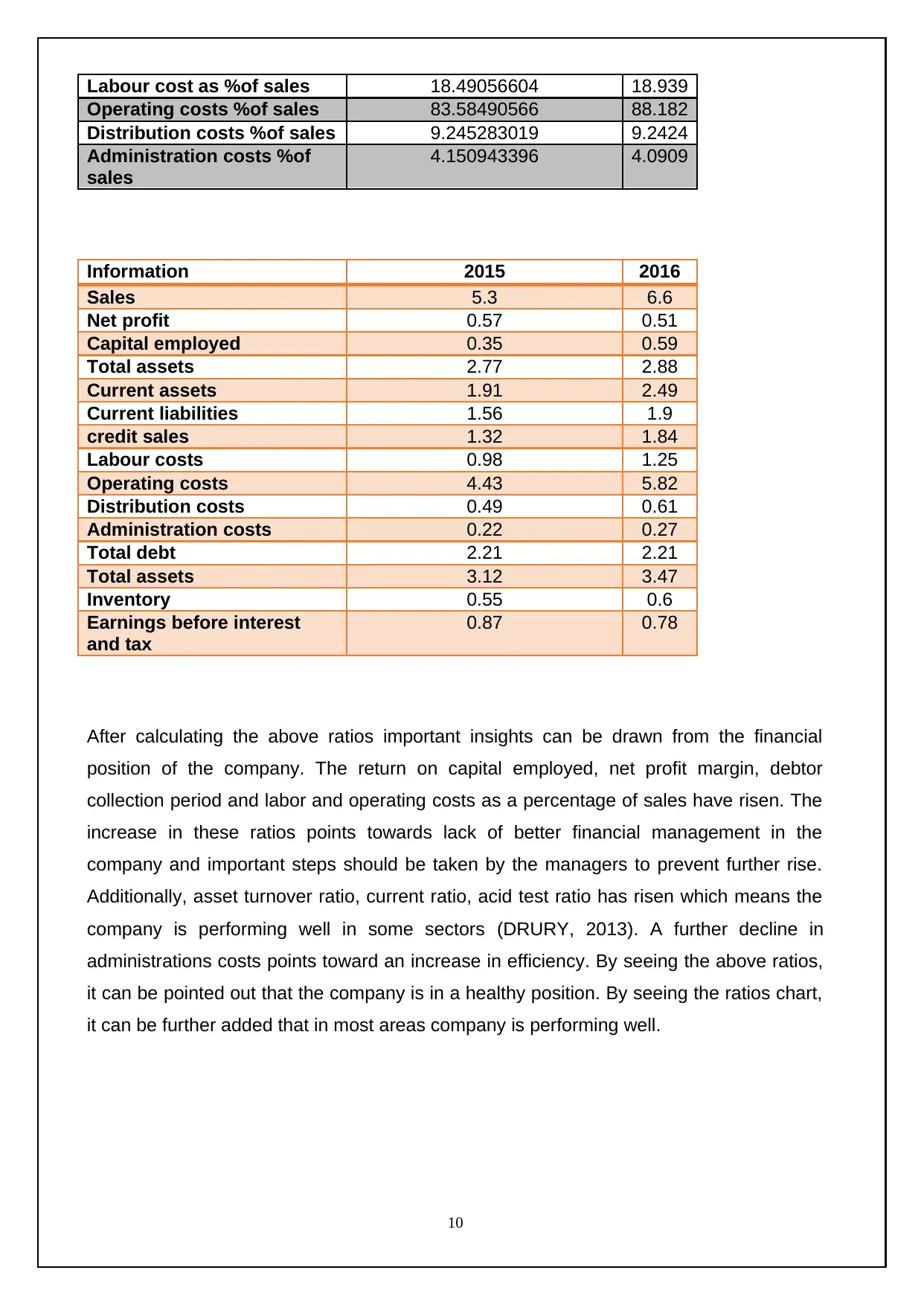

Labour cost as %of sales 18.49056604 18.939

Operating costs %of sales 83.58490566 88.182

Distribution costs %of sales 9.245283019 9.2424

Administration costs %of

sales

4.150943396 4.0909

Information 2015 2016

Sales 5.3 6.6

Net profit 0.57 0.51

Capital employed 0.35 0.59

Total assets 2.77 2.88

Current assets 1.91 2.49

Current liabilities 1.56 1.9

credit sales 1.32 1.84

Labour costs 0.98 1.25

Operating costs 4.43 5.82

Distribution costs 0.49 0.61

Administration costs 0.22 0.27

Total debt 2.21 2.21

Total assets 3.12 3.47

Inventory 0.55 0.6

Earnings before interest

and tax

0.87 0.78

After calculating the above ratios important insights can be drawn from the financial

position of the company. The return on capital employed, net profit margin, debtor

collection period and labor and operating costs as a percentage of sales have risen. The

increase in these ratios points towards lack of better financial management in the

company and important steps should be taken by the managers to prevent further rise.

Additionally, asset turnover ratio, current ratio, acid test ratio has risen which means the

company is performing well in some sectors (DRURY, 2013). A further decline in

administrations costs points toward an increase in efficiency. By seeing the above ratios,

it can be pointed out that the company is in a healthy position. By seeing the ratios chart,

it can be further added that in most areas company is performing well.

10

Operating costs %of sales 83.58490566 88.182

Distribution costs %of sales 9.245283019 9.2424

Administration costs %of

sales

4.150943396 4.0909

Information 2015 2016

Sales 5.3 6.6

Net profit 0.57 0.51

Capital employed 0.35 0.59

Total assets 2.77 2.88

Current assets 1.91 2.49

Current liabilities 1.56 1.9

credit sales 1.32 1.84

Labour costs 0.98 1.25

Operating costs 4.43 5.82

Distribution costs 0.49 0.61

Administration costs 0.22 0.27

Total debt 2.21 2.21

Total assets 3.12 3.47

Inventory 0.55 0.6

Earnings before interest

and tax

0.87 0.78

After calculating the above ratios important insights can be drawn from the financial

position of the company. The return on capital employed, net profit margin, debtor

collection period and labor and operating costs as a percentage of sales have risen. The

increase in these ratios points towards lack of better financial management in the

company and important steps should be taken by the managers to prevent further rise.

Additionally, asset turnover ratio, current ratio, acid test ratio has risen which means the

company is performing well in some sectors (DRURY, 2013). A further decline in

administrations costs points toward an increase in efficiency. By seeing the above ratios,

it can be pointed out that the company is in a healthy position. By seeing the ratios chart,

it can be further added that in most areas company is performing well.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. Prepare a detailed report on the company's performance in terms of

profitability and liquidity compared with the average of the sector over the period.

Introduction:

This report is prepared for analysing the financial performance of Stratford Yachts Limited

through ratios analysis regarding the liquidity and profitability ratios of the organisation.

Financial ratios make use of financial figures and makes analyses.

Analysis:

After making the comparison with the industry average that the company once had a

higher percentage of return on capital employed which has declined and is now below the

industry average. The asset turnover of the Stratford Yachts Ltd. is better but the net

profit margin is lower. The current ratio of the company is 1.3:1 which is lower than the

industry average of 1.5 but the suitable ratio is 2. The quick ratio of the business is close

to the average of the industry and is suitable (Hoyle, Schaefer and Doupnik, 2015). The

debtor’s collection period of the firm is higher than the average of the industry which is

not good.

The gearing ratio: Both the labor and operating cost of the company is higher than the

industry average which will reduce the company’s profitability. On the other hand, the

distribution and administration costs are lower than the industry average which is a

positive sign for the company.

After comparing the company’s ratios with the industry it can be said that the company is

almost par if consider the liquidity position lagging in current ratio only which can be

corrected by taking proper measures. On the other hand, the profitability of the firm is far

lower than the industry average which shows that the Stratford Yachts Ltd. needs to

reduce its cost, which is also higher than the average of the industry, to increase its

profitability. The reduction in costs will bring the company’s ratios closer to the industry

average and will also increase the profitability (Bragg, 2012).

Conclusion:

It can be concluded that the company’s liquidity position is quite good but requires

significant amount of consideration. Company need to improve its profitability option.

11

profitability and liquidity compared with the average of the sector over the period.

Introduction:

This report is prepared for analysing the financial performance of Stratford Yachts Limited

through ratios analysis regarding the liquidity and profitability ratios of the organisation.

Financial ratios make use of financial figures and makes analyses.

Analysis:

After making the comparison with the industry average that the company once had a

higher percentage of return on capital employed which has declined and is now below the

industry average. The asset turnover of the Stratford Yachts Ltd. is better but the net

profit margin is lower. The current ratio of the company is 1.3:1 which is lower than the

industry average of 1.5 but the suitable ratio is 2. The quick ratio of the business is close

to the average of the industry and is suitable (Hoyle, Schaefer and Doupnik, 2015). The

debtor’s collection period of the firm is higher than the average of the industry which is

not good.

The gearing ratio: Both the labor and operating cost of the company is higher than the

industry average which will reduce the company’s profitability. On the other hand, the

distribution and administration costs are lower than the industry average which is a

positive sign for the company.

After comparing the company’s ratios with the industry it can be said that the company is

almost par if consider the liquidity position lagging in current ratio only which can be

corrected by taking proper measures. On the other hand, the profitability of the firm is far

lower than the industry average which shows that the Stratford Yachts Ltd. needs to

reduce its cost, which is also higher than the average of the industry, to increase its

profitability. The reduction in costs will bring the company’s ratios closer to the industry

average and will also increase the profitability (Bragg, 2012).

Conclusion:

It can be concluded that the company’s liquidity position is quite good but requires

significant amount of consideration. Company need to improve its profitability option.

11

Recommendations

After seeing the ratios of the company it can be recommended that the company

should reduce its costs as this is reducing its profitability. Further, the company

should collect money from its debtors quickly as the company’s debt collection

period is higher than the industry average. Additionally, the company has to increase

its current assets to improve its liquidity position. The company can set targets for

achieving this. Costs targets and cost control mechanism will help the company to

reduce the costs. The employee targets can reduce the debt collection period.

Finally, by increasing cash in hand or other short-term investments will improve the

liquidity position of the company. Even increasing the inventory level will help. The

company can further use management information system to keep better check on

costs and debtors.

12

After seeing the ratios of the company it can be recommended that the company

should reduce its costs as this is reducing its profitability. Further, the company

should collect money from its debtors quickly as the company’s debt collection

period is higher than the industry average. Additionally, the company has to increase

its current assets to improve its liquidity position. The company can set targets for

achieving this. Costs targets and cost control mechanism will help the company to

reduce the costs. The employee targets can reduce the debt collection period.

Finally, by increasing cash in hand or other short-term investments will improve the

liquidity position of the company. Even increasing the inventory level will help. The

company can further use management information system to keep better check on

costs and debtors.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Anheier, H.K., 2014. Nonprofit organizations: Theory, management, policy.

Routledge.

Bragg, S.M., 2012. Business ratios and formulas: a comprehensive guide

(Vol. 577). John Wiley & Sons

Drucker, P., 2012. Managing the non-profit organization. Routledge.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting.

McGraw Hill.

Lee, T.A. and Parker, R.H. eds., 2013. Towards a theory and practice of cash

flow accounting (RLE Accounting) (Vol. 50). Routledge.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial

accounting. Cengage Learning.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an

introduction to concepts, methods and uses. Cengage Learning.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial

accounting. John Wiley & Sons.

13

Anheier, H.K., 2014. Nonprofit organizations: Theory, management, policy.

Routledge.

Bragg, S.M., 2012. Business ratios and formulas: a comprehensive guide

(Vol. 577). John Wiley & Sons

Drucker, P., 2012. Managing the non-profit organization. Routledge.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting.

McGraw Hill.

Lee, T.A. and Parker, R.H. eds., 2013. Towards a theory and practice of cash

flow accounting (RLE Accounting) (Vol. 50). Routledge.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial

accounting. Cengage Learning.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an

introduction to concepts, methods and uses. Cengage Learning.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial

accounting. John Wiley & Sons.

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.