Report on Managing Financial Resources and Decisions (Finance Module)

VerifiedAdded on 2019/12/03

|22

|4678

|246

Report

AI Summary

This report provides a comprehensive analysis of financial resources and decision-making within a business context. It begins by exploring various sources of finance, including bank loans, trade credit, and issuing shares, along with their implications and suitability for different business needs, such as startups, expansions, and takeovers. The report then delves into the cost of different financing options and the importance of financial planning for maximizing fund utilization and avoiding financial shocks. It outlines the types of financial information, such as financial statements and audit reports, required for informed decision-making. Additionally, the report includes sample templates for profit and loss accounts and balance sheets, providing a practical guide to financial statement analysis. The report also includes calculation of various ratios in order to find out the best project and the position of companies. Finally, it examines the uses of different types of accounts and the differences between various organizational structures, concluding with an overview of financial performance and the importance of sound financial management.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

RESOURCES AND

DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

Task 1...............................................................................................................................................1

1.1 Sources of finance available to the business. .......................................................................1

1.2 implication of various sources..............................................................................................2

1.3 Sources of finance available to fulfill the following needs...................................................3

Task 2...............................................................................................................................................3

2.1 Cost of different sources of finance. ....................................................................................3

2.2 Importance of financial planning..........................................................................................4

2.3 Types of financial information required for decision making purposes..............................4

2.4 Sample templates of profit and loss account and balance sheet............................................5

Task 3 ..............................................................................................................................................8

3.1 Finding and recommendation for the budgets analyzed.......................................................8

3.3 Calculation of various ratios in order to find out the best project.........................................8

3.2 Calculation of different types of unit cost. .........................................................................10

Task 4.............................................................................................................................................13

4.1 Uses and purpose of various types of accounts...................................................................13

4.2 Difference between different types of organization............................................................14

4.3 Calculation of different ration in order to find out the companies positions......................14

Conclusion ....................................................................................................................................16

References......................................................................................................................................16

INTRODUCTION ..........................................................................................................................1

Task 1...............................................................................................................................................1

1.1 Sources of finance available to the business. .......................................................................1

1.2 implication of various sources..............................................................................................2

1.3 Sources of finance available to fulfill the following needs...................................................3

Task 2...............................................................................................................................................3

2.1 Cost of different sources of finance. ....................................................................................3

2.2 Importance of financial planning..........................................................................................4

2.3 Types of financial information required for decision making purposes..............................4

2.4 Sample templates of profit and loss account and balance sheet............................................5

Task 3 ..............................................................................................................................................8

3.1 Finding and recommendation for the budgets analyzed.......................................................8

3.3 Calculation of various ratios in order to find out the best project.........................................8

3.2 Calculation of different types of unit cost. .........................................................................10

Task 4.............................................................................................................................................13

4.1 Uses and purpose of various types of accounts...................................................................13

4.2 Difference between different types of organization............................................................14

4.3 Calculation of different ration in order to find out the companies positions......................14

Conclusion ....................................................................................................................................16

References......................................................................................................................................16

INTRODUCTION

Finance is a science that describes the management of money, credit, investments, banking and

assets and liabilities. Finance consists of financial system and financial instruments. Finance is

divided into three categories (i.e. public, personal and corporate finance). The following report

interprets the various sources of finance available to the business in order to raise capital for the

expansion or starting a new business. This report shows the various implications of finance faced

by the business at the time of allocation of the resources. In this report various financial

decisions are also taken after analyzing the various financial accounts. At last financial

performance of the business are also evaluated considering the fixed, variable cost and break

even.

Task 1

1.1 Sources of finance available to the business.

There are different types of sources available with the business in order to raise their

capital. These available sources help to meet short term and long term funds requirement of the

organization.

Short term sources of finance

Bank Loan: - in case of bank loan bank lends small amount of money to the company by

charging the high interest rate (Anheier and Winder, 2007). This method is used by the company

who want to start up a new business or expand its business.

Trade Credit: - This is another method used by the company in order to raise its funds.

In this case company purchases the assets from the vendor without making him any due

payment. The period for trade credit runs for 28 days only. This method can be used by the in

order to meet its quick requirement of the assets.

Long term sources of finance

Issue of Shares: - Company can raise its funds by issuing shares to the general public.

This method is used by the company in order to expand its business which requires a large

amount of capital.

Leasing: - It is a contract made between two parties in order to borrow the assets for some

time period without making the full payment (Barth, 2008). Leasing is a type of rental. It is used

1

Finance is a science that describes the management of money, credit, investments, banking and

assets and liabilities. Finance consists of financial system and financial instruments. Finance is

divided into three categories (i.e. public, personal and corporate finance). The following report

interprets the various sources of finance available to the business in order to raise capital for the

expansion or starting a new business. This report shows the various implications of finance faced

by the business at the time of allocation of the resources. In this report various financial

decisions are also taken after analyzing the various financial accounts. At last financial

performance of the business are also evaluated considering the fixed, variable cost and break

even.

Task 1

1.1 Sources of finance available to the business.

There are different types of sources available with the business in order to raise their

capital. These available sources help to meet short term and long term funds requirement of the

organization.

Short term sources of finance

Bank Loan: - in case of bank loan bank lends small amount of money to the company by

charging the high interest rate (Anheier and Winder, 2007). This method is used by the company

who want to start up a new business or expand its business.

Trade Credit: - This is another method used by the company in order to raise its funds.

In this case company purchases the assets from the vendor without making him any due

payment. The period for trade credit runs for 28 days only. This method can be used by the in

order to meet its quick requirement of the assets.

Long term sources of finance

Issue of Shares: - Company can raise its funds by issuing shares to the general public.

This method is used by the company in order to expand its business which requires a large

amount of capital.

Leasing: - It is a contract made between two parties in order to borrow the assets for some

time period without making the full payment (Barth, 2008). Leasing is a type of rental. It is used

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by the company in order to expand its business. Company leases the property, machine, vehicles

and so on.

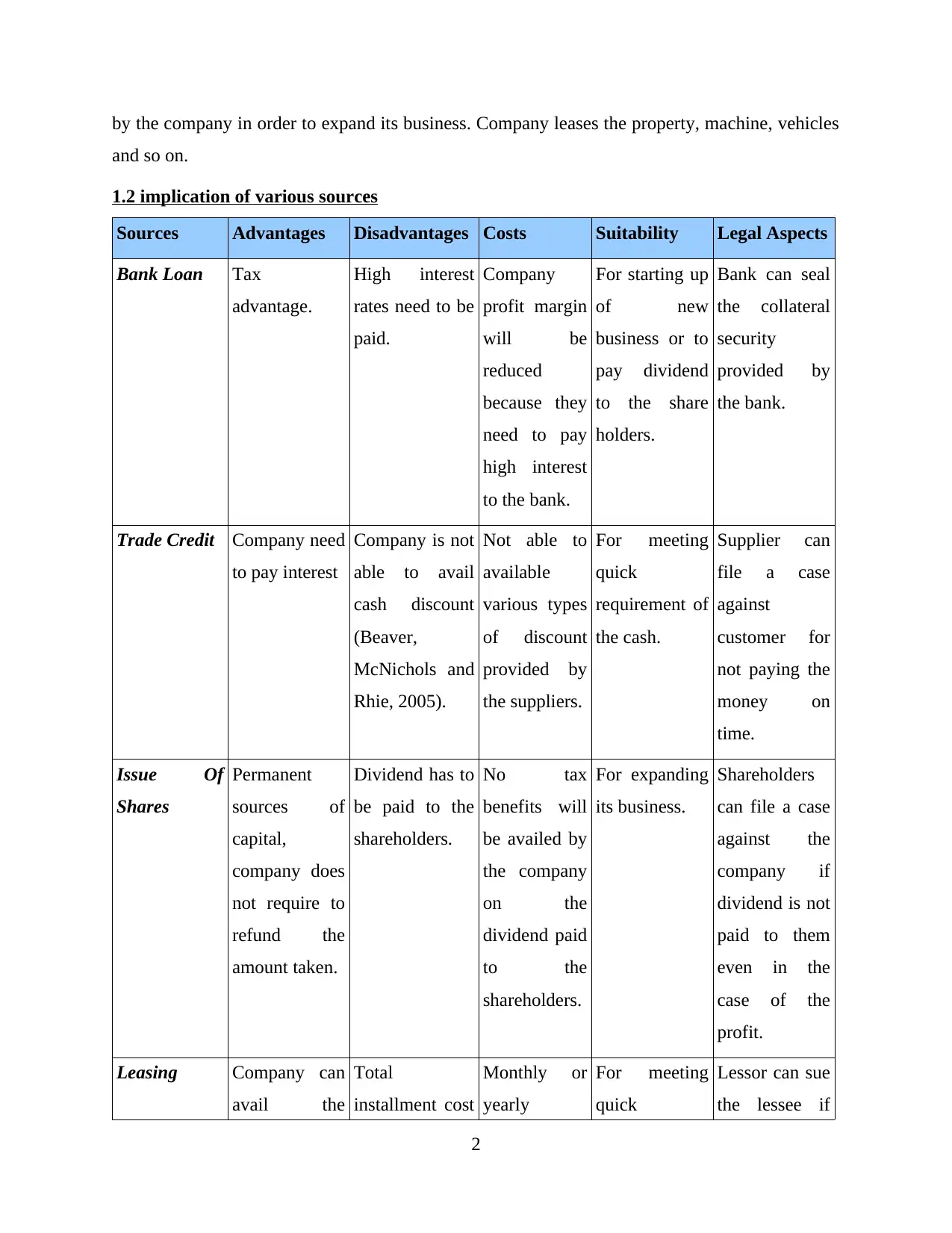

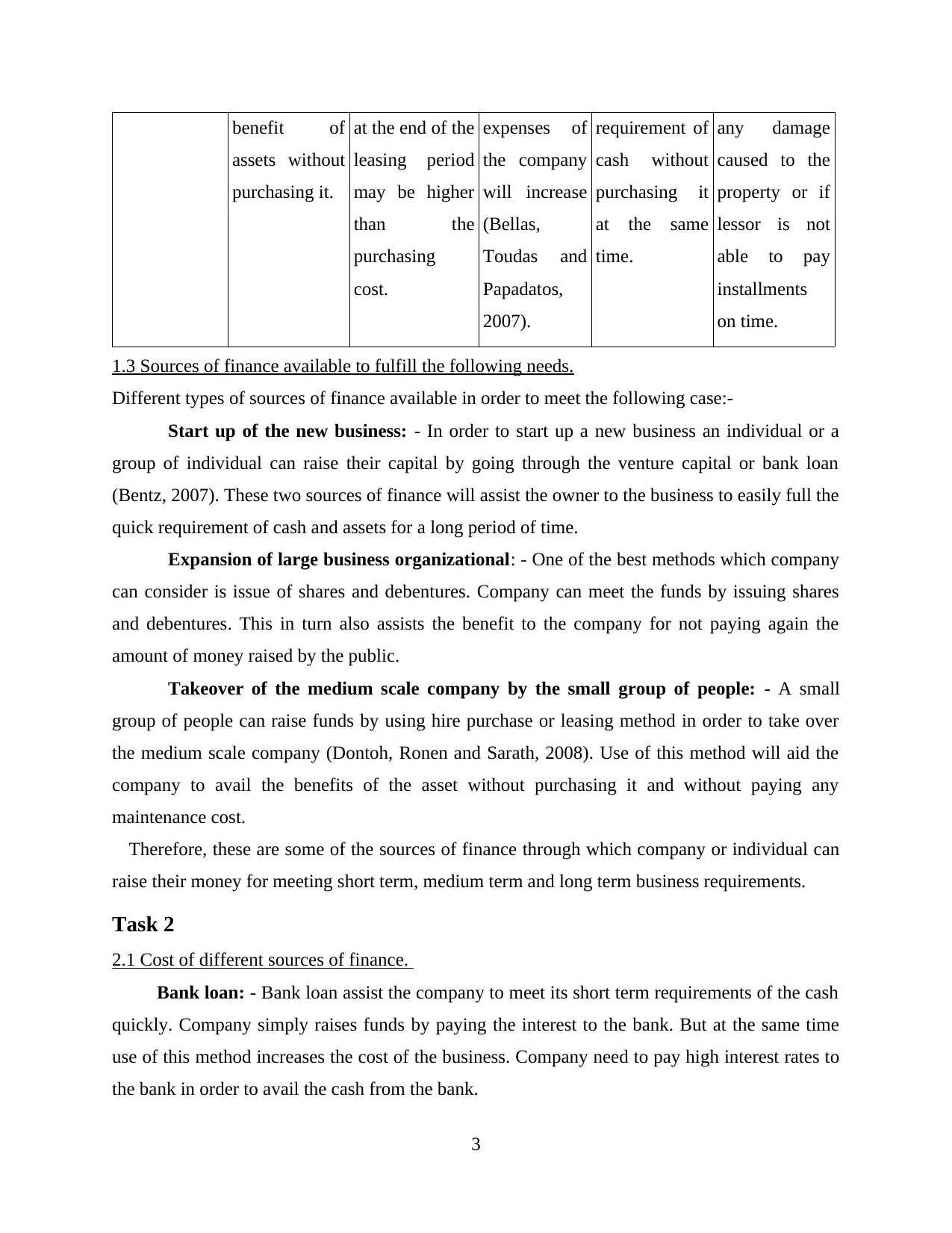

1.2 implication of various sources

Sources Advantages Disadvantages Costs Suitability Legal Aspects

Bank Loan Tax

advantage.

High interest

rates need to be

paid.

Company

profit margin

will be

reduced

because they

need to pay

high interest

to the bank.

For starting up

of new

business or to

pay dividend

to the share

holders.

Bank can seal

the collateral

security

provided by

the bank.

Trade Credit Company need

to pay interest

Company is not

able to avail

cash discount

(Beaver,

McNichols and

Rhie, 2005).

Not able to

available

various types

of discount

provided by

the suppliers.

For meeting

quick

requirement of

the cash.

Supplier can

file a case

against

customer for

not paying the

money on

time.

Issue Of

Shares

Permanent

sources of

capital,

company does

not require to

refund the

amount taken.

Dividend has to

be paid to the

shareholders.

No tax

benefits will

be availed by

the company

on the

dividend paid

to the

shareholders.

For expanding

its business.

Shareholders

can file a case

against the

company if

dividend is not

paid to them

even in the

case of the

profit.

Leasing Company can

avail the

Total

installment cost

Monthly or

yearly

For meeting

quick

Lessor can sue

the lessee if

2

and so on.

1.2 implication of various sources

Sources Advantages Disadvantages Costs Suitability Legal Aspects

Bank Loan Tax

advantage.

High interest

rates need to be

paid.

Company

profit margin

will be

reduced

because they

need to pay

high interest

to the bank.

For starting up

of new

business or to

pay dividend

to the share

holders.

Bank can seal

the collateral

security

provided by

the bank.

Trade Credit Company need

to pay interest

Company is not

able to avail

cash discount

(Beaver,

McNichols and

Rhie, 2005).

Not able to

available

various types

of discount

provided by

the suppliers.

For meeting

quick

requirement of

the cash.

Supplier can

file a case

against

customer for

not paying the

money on

time.

Issue Of

Shares

Permanent

sources of

capital,

company does

not require to

refund the

amount taken.

Dividend has to

be paid to the

shareholders.

No tax

benefits will

be availed by

the company

on the

dividend paid

to the

shareholders.

For expanding

its business.

Shareholders

can file a case

against the

company if

dividend is not

paid to them

even in the

case of the

profit.

Leasing Company can

avail the

Total

installment cost

Monthly or

yearly

For meeting

quick

Lessor can sue

the lessee if

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

benefit of

assets without

purchasing it.

at the end of the

leasing period

may be higher

than the

purchasing

cost.

expenses of

the company

will increase

(Bellas,

Toudas and

Papadatos,

2007).

requirement of

cash without

purchasing it

at the same

time.

any damage

caused to the

property or if

lessor is not

able to pay

installments

on time.

1.3 Sources of finance available to fulfill the following needs.

Different types of sources of finance available in order to meet the following case:-

Start up of the new business: - In order to start up a new business an individual or a

group of individual can raise their capital by going through the venture capital or bank loan

(Bentz, 2007). These two sources of finance will assist the owner to the business to easily full the

quick requirement of cash and assets for a long period of time.

Expansion of large business organizational: - One of the best methods which company

can consider is issue of shares and debentures. Company can meet the funds by issuing shares

and debentures. This in turn also assists the benefit to the company for not paying again the

amount of money raised by the public.

Takeover of the medium scale company by the small group of people: - A small

group of people can raise funds by using hire purchase or leasing method in order to take over

the medium scale company (Dontoh, Ronen and Sarath, 2008). Use of this method will aid the

company to avail the benefits of the asset without purchasing it and without paying any

maintenance cost.

Therefore, these are some of the sources of finance through which company or individual can

raise their money for meeting short term, medium term and long term business requirements.

Task 2

2.1 Cost of different sources of finance.

Bank loan: - Bank loan assist the company to meet its short term requirements of the cash

quickly. Company simply raises funds by paying the interest to the bank. But at the same time

use of this method increases the cost of the business. Company need to pay high interest rates to

the bank in order to avail the cash from the bank.

3

assets without

purchasing it.

at the end of the

leasing period

may be higher

than the

purchasing

cost.

expenses of

the company

will increase

(Bellas,

Toudas and

Papadatos,

2007).

requirement of

cash without

purchasing it

at the same

time.

any damage

caused to the

property or if

lessor is not

able to pay

installments

on time.

1.3 Sources of finance available to fulfill the following needs.

Different types of sources of finance available in order to meet the following case:-

Start up of the new business: - In order to start up a new business an individual or a

group of individual can raise their capital by going through the venture capital or bank loan

(Bentz, 2007). These two sources of finance will assist the owner to the business to easily full the

quick requirement of cash and assets for a long period of time.

Expansion of large business organizational: - One of the best methods which company

can consider is issue of shares and debentures. Company can meet the funds by issuing shares

and debentures. This in turn also assists the benefit to the company for not paying again the

amount of money raised by the public.

Takeover of the medium scale company by the small group of people: - A small

group of people can raise funds by using hire purchase or leasing method in order to take over

the medium scale company (Dontoh, Ronen and Sarath, 2008). Use of this method will aid the

company to avail the benefits of the asset without purchasing it and without paying any

maintenance cost.

Therefore, these are some of the sources of finance through which company or individual can

raise their money for meeting short term, medium term and long term business requirements.

Task 2

2.1 Cost of different sources of finance.

Bank loan: - Bank loan assist the company to meet its short term requirements of the cash

quickly. Company simply raises funds by paying the interest to the bank. But at the same time

use of this method increases the cost of the business. Company need to pay high interest rates to

the bank in order to avail the cash from the bank.

3

Trade credit: - It also said He Company to meet its short term requirement of the fund.

Company can avail this method according to their needs and wants (Eccles and Holt, 2005).

Company does not require paying any interest. But at the same time it is also seen that this type

of credit facility is available to the business for a small time period only.

Issue of shares: - issue of shares will assist the company to meet it s long term

requirement of the cash. It also helps the company to expand its business by attracting more

customers. But at the same time it increases the cost of the company. Company need to pay

dividend to this shareholders and also the decision making power.

Leasing: - It said the company to meet to quick requirement of assets. Company can easily

use the asset without purchasing it (Efendi, Srivastava and Swanson, 2007). But at the same

time it reduces the profitability of the company because company need to pay installment on the

regular basis to the lessor which in turn increases the cost of the cost.

2.2 Importance of financial planning

Maximum utilization of funds: - Planning of all the financial activities in advance assist

the company to utilize the available resources and funds with the organization to the full extent.

Advance planning also said the company to reduce the wastage of the resources.

Avoid shocks: - Planning of all the financial activities assist the company to avoid shocks

and alteration which could be faced by the company due to sudden change in internal and

external environment.

Helps in maintaining balance between inflow and outflow of cash: - Financial planning

aids the company to maintain the balance between the inflow and outflow of the cash from

within and outside the organization (Mahotra and Malhotra, 2008). Advance planning help the

company to reduce the expenses by generating more income.

Helps in achieving organization objectives: - Advance planning of all the financial

activities aids the company to move towards the achievement of the organizational objective.

Planning of all the activities helps the company to maintain balance between all activities which

in turn assist the company to achieve the set target.

2.3 Types of financial information required for decision making purposes

Decision maker of the company wants the financial statements and company's audit report in

order to take various decisions.

4

Company can avail this method according to their needs and wants (Eccles and Holt, 2005).

Company does not require paying any interest. But at the same time it is also seen that this type

of credit facility is available to the business for a small time period only.

Issue of shares: - issue of shares will assist the company to meet it s long term

requirement of the cash. It also helps the company to expand its business by attracting more

customers. But at the same time it increases the cost of the company. Company need to pay

dividend to this shareholders and also the decision making power.

Leasing: - It said the company to meet to quick requirement of assets. Company can easily

use the asset without purchasing it (Efendi, Srivastava and Swanson, 2007). But at the same

time it reduces the profitability of the company because company need to pay installment on the

regular basis to the lessor which in turn increases the cost of the cost.

2.2 Importance of financial planning

Maximum utilization of funds: - Planning of all the financial activities in advance assist

the company to utilize the available resources and funds with the organization to the full extent.

Advance planning also said the company to reduce the wastage of the resources.

Avoid shocks: - Planning of all the financial activities assist the company to avoid shocks

and alteration which could be faced by the company due to sudden change in internal and

external environment.

Helps in maintaining balance between inflow and outflow of cash: - Financial planning

aids the company to maintain the balance between the inflow and outflow of the cash from

within and outside the organization (Mahotra and Malhotra, 2008). Advance planning help the

company to reduce the expenses by generating more income.

Helps in achieving organization objectives: - Advance planning of all the financial

activities aids the company to move towards the achievement of the organizational objective.

Planning of all the activities helps the company to maintain balance between all activities which

in turn assist the company to achieve the set target.

2.3 Types of financial information required for decision making purposes

Decision maker of the company wants the financial statements and company's audit report in

order to take various decisions.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial statements: - It is a type of statements which aid the company to know the

actual position of the business. It helps the company to analyze the inflow and outflow of the

cash (Penman and Penman, 2007). Different types of financial statements which are required by

the profit and loss account, balance sheet, cash flow statements, income statements and many

more.

Company audit report:- Company audit report is prepared by the company in order to

find out whether any fraud or illegal practices is taking place within the business organization. It

also aid to find out various measures which are not included in the financial statements.

Company audit is done by the auditor appointed by the organization or the government depends

upon the size of business.

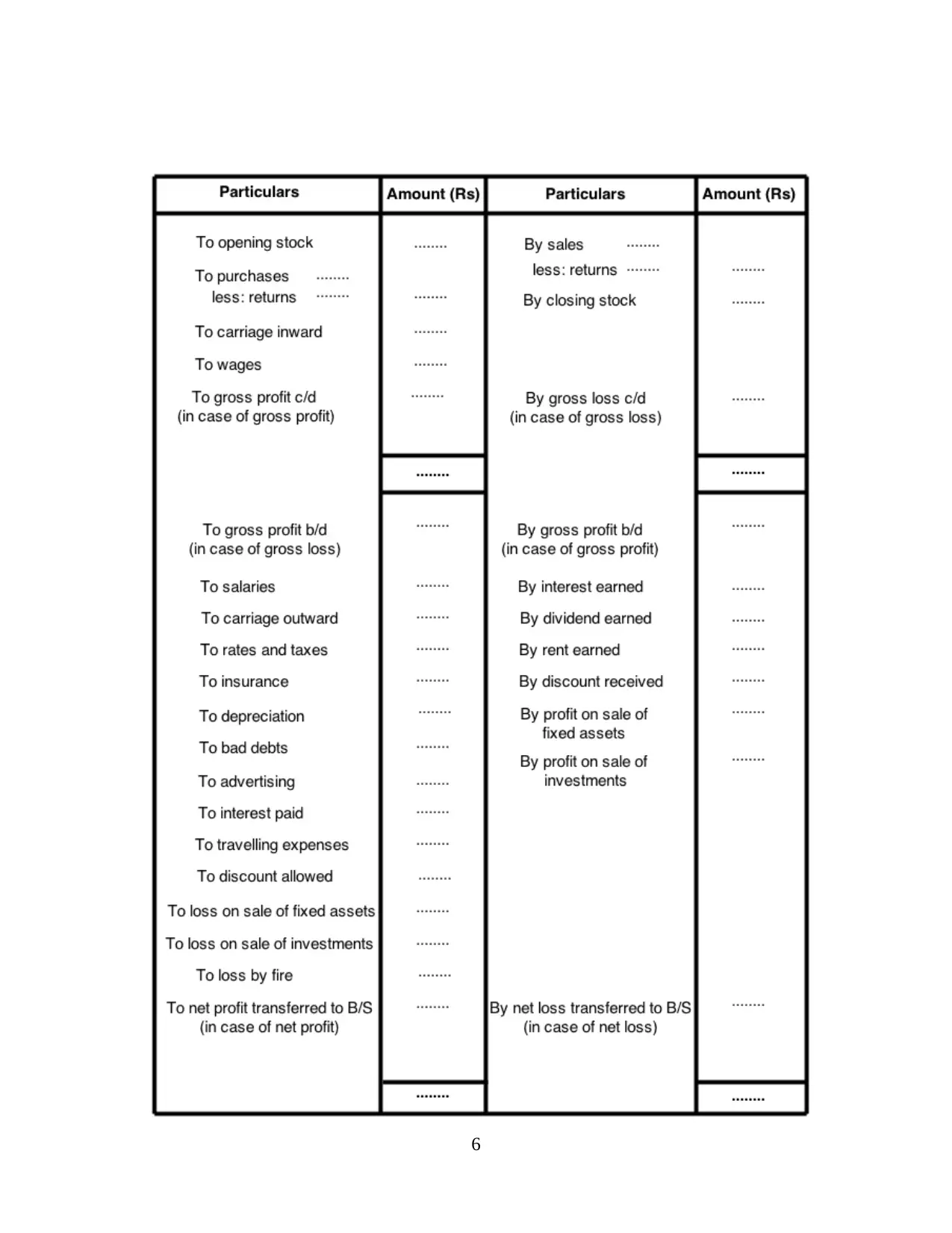

2.4 Sample templates of profit and loss account and balance sheet.

Format of profit and loss account

In trading account all the income generated and expenses made at the time of

manufacturing process are recorded (Ross, 2008). By preparing trading account company is able

to find out the gross profit or loss of the company. Similarly continuing the profit and loss

account net profit or loss of the company is calculated. In this all the income earned and

expenses made after the manufacturing process are recorded. Net profit or loss calculated assists

them to find out the financial position of the business. After the calculation of net profit or loss

company decides the amount of tax and dividend and need to be paid to government and

shareholders.

Trading and Profit and Loss account of.... (Company name)

For the year ending on …. (Year)

5

actual position of the business. It helps the company to analyze the inflow and outflow of the

cash (Penman and Penman, 2007). Different types of financial statements which are required by

the profit and loss account, balance sheet, cash flow statements, income statements and many

more.

Company audit report:- Company audit report is prepared by the company in order to

find out whether any fraud or illegal practices is taking place within the business organization. It

also aid to find out various measures which are not included in the financial statements.

Company audit is done by the auditor appointed by the organization or the government depends

upon the size of business.

2.4 Sample templates of profit and loss account and balance sheet.

Format of profit and loss account

In trading account all the income generated and expenses made at the time of

manufacturing process are recorded (Ross, 2008). By preparing trading account company is able

to find out the gross profit or loss of the company. Similarly continuing the profit and loss

account net profit or loss of the company is calculated. In this all the income earned and

expenses made after the manufacturing process are recorded. Net profit or loss calculated assists

them to find out the financial position of the business. After the calculation of net profit or loss

company decides the amount of tax and dividend and need to be paid to government and

shareholders.

Trading and Profit and Loss account of.... (Company name)

For the year ending on …. (Year)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

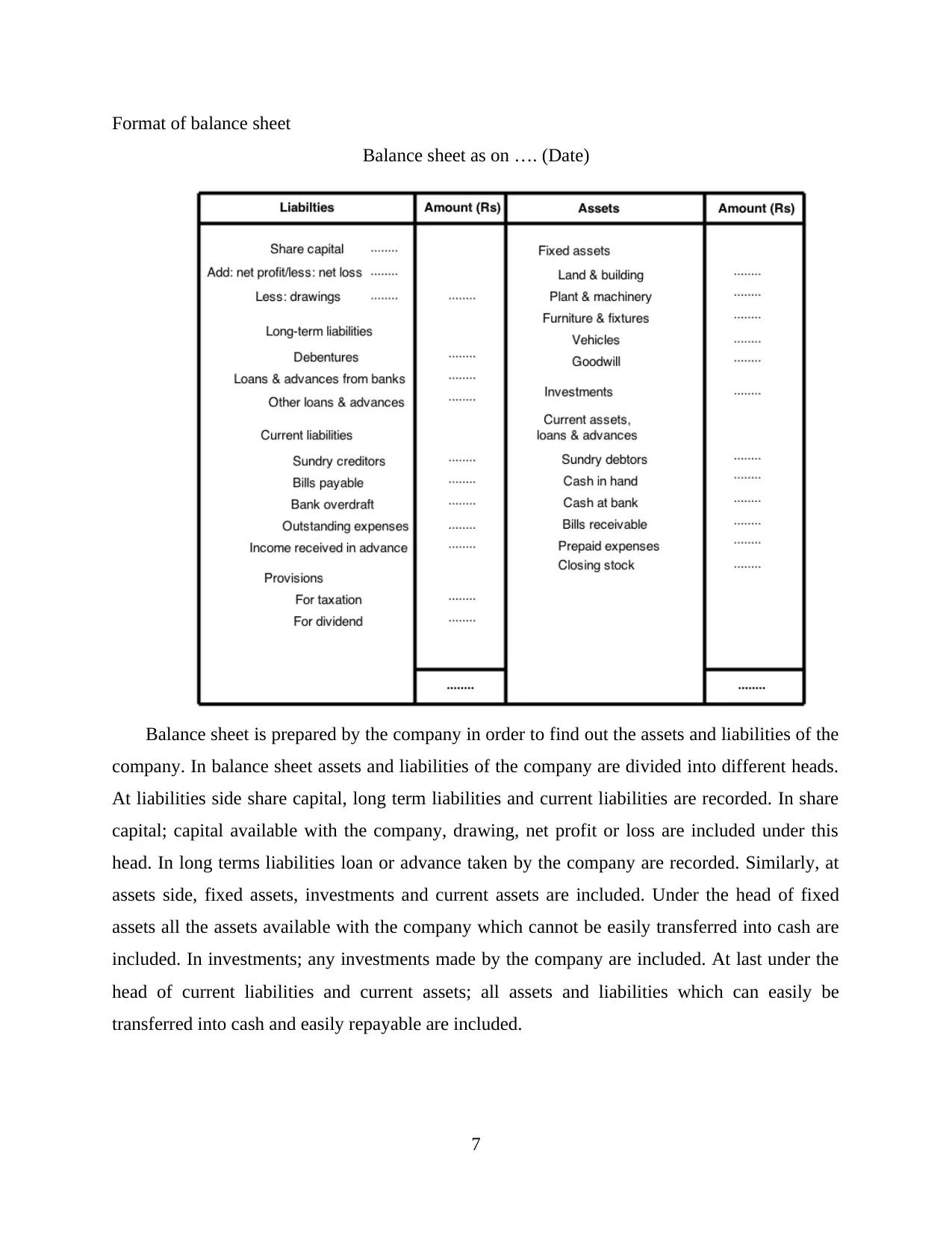

Format of balance sheet

Balance sheet as on …. (Date)

Balance sheet is prepared by the company in order to find out the assets and liabilities of the

company. In balance sheet assets and liabilities of the company are divided into different heads.

At liabilities side share capital, long term liabilities and current liabilities are recorded. In share

capital; capital available with the company, drawing, net profit or loss are included under this

head. In long terms liabilities loan or advance taken by the company are recorded. Similarly, at

assets side, fixed assets, investments and current assets are included. Under the head of fixed

assets all the assets available with the company which cannot be easily transferred into cash are

included. In investments; any investments made by the company are included. At last under the

head of current liabilities and current assets; all assets and liabilities which can easily be

transferred into cash and easily repayable are included.

7

Balance sheet as on …. (Date)

Balance sheet is prepared by the company in order to find out the assets and liabilities of the

company. In balance sheet assets and liabilities of the company are divided into different heads.

At liabilities side share capital, long term liabilities and current liabilities are recorded. In share

capital; capital available with the company, drawing, net profit or loss are included under this

head. In long terms liabilities loan or advance taken by the company are recorded. Similarly, at

assets side, fixed assets, investments and current assets are included. Under the head of fixed

assets all the assets available with the company which cannot be easily transferred into cash are

included. In investments; any investments made by the company are included. At last under the

head of current liabilities and current assets; all assets and liabilities which can easily be

transferred into cash and easily repayable are included.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 3

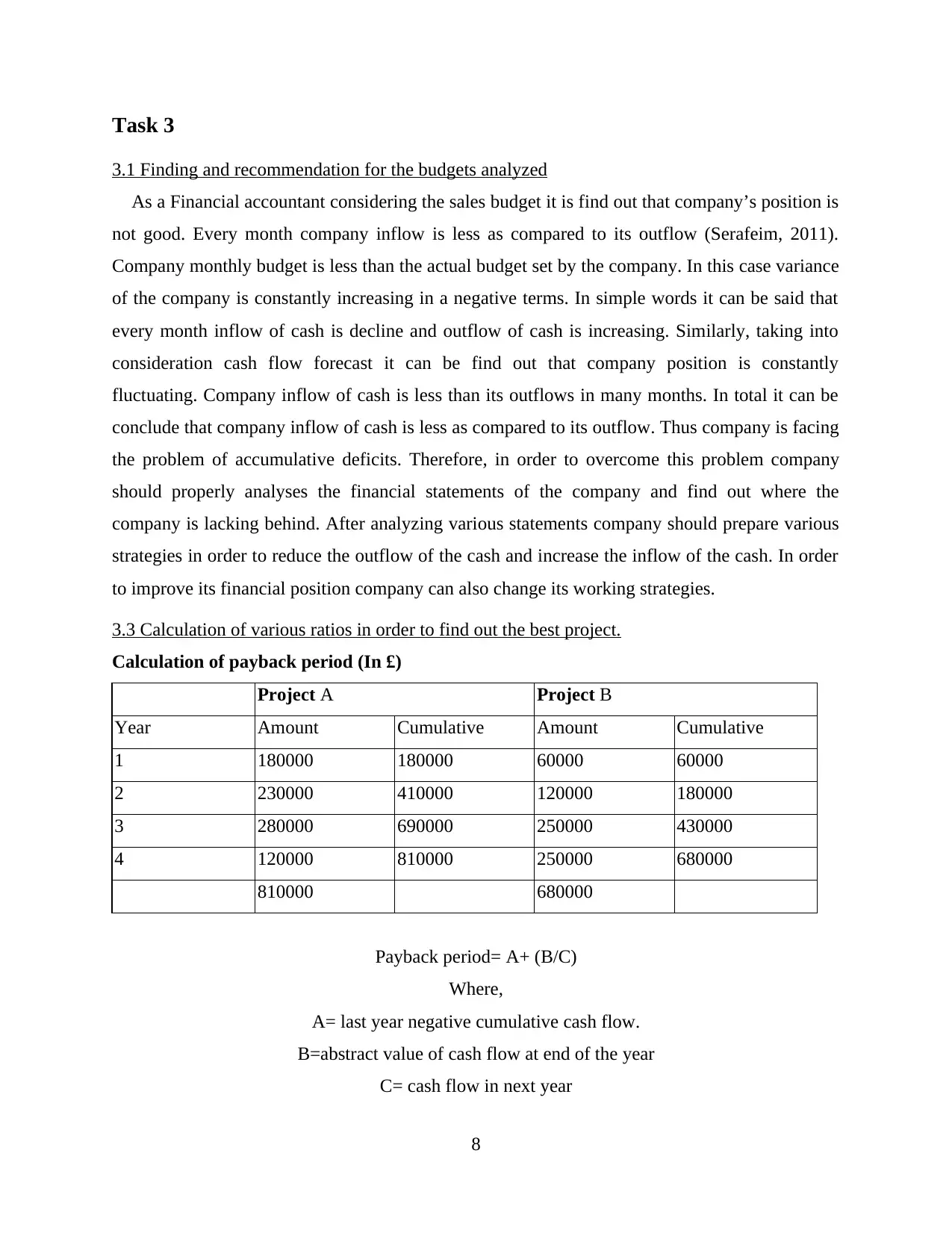

3.1 Finding and recommendation for the budgets analyzed

As a Financial accountant considering the sales budget it is find out that company’s position is

not good. Every month company inflow is less as compared to its outflow (Serafeim, 2011).

Company monthly budget is less than the actual budget set by the company. In this case variance

of the company is constantly increasing in a negative terms. In simple words it can be said that

every month inflow of cash is decline and outflow of cash is increasing. Similarly, taking into

consideration cash flow forecast it can be find out that company position is constantly

fluctuating. Company inflow of cash is less than its outflows in many months. In total it can be

conclude that company inflow of cash is less as compared to its outflow. Thus company is facing

the problem of accumulative deficits. Therefore, in order to overcome this problem company

should properly analyses the financial statements of the company and find out where the

company is lacking behind. After analyzing various statements company should prepare various

strategies in order to reduce the outflow of the cash and increase the inflow of the cash. In order

to improve its financial position company can also change its working strategies.

3.3 Calculation of various ratios in order to find out the best project.

Calculation of payback period (In £)

Project A Project B

Year Amount Cumulative Amount Cumulative

1 180000 180000 60000 60000

2 230000 410000 120000 180000

3 280000 690000 250000 430000

4 120000 810000 250000 680000

810000 680000

Payback period= A+ (B/C)

Where,

A= last year negative cumulative cash flow.

B=abstract value of cash flow at end of the year

C= cash flow in next year

8

3.1 Finding and recommendation for the budgets analyzed

As a Financial accountant considering the sales budget it is find out that company’s position is

not good. Every month company inflow is less as compared to its outflow (Serafeim, 2011).

Company monthly budget is less than the actual budget set by the company. In this case variance

of the company is constantly increasing in a negative terms. In simple words it can be said that

every month inflow of cash is decline and outflow of cash is increasing. Similarly, taking into

consideration cash flow forecast it can be find out that company position is constantly

fluctuating. Company inflow of cash is less than its outflows in many months. In total it can be

conclude that company inflow of cash is less as compared to its outflow. Thus company is facing

the problem of accumulative deficits. Therefore, in order to overcome this problem company

should properly analyses the financial statements of the company and find out where the

company is lacking behind. After analyzing various statements company should prepare various

strategies in order to reduce the outflow of the cash and increase the inflow of the cash. In order

to improve its financial position company can also change its working strategies.

3.3 Calculation of various ratios in order to find out the best project.

Calculation of payback period (In £)

Project A Project B

Year Amount Cumulative Amount Cumulative

1 180000 180000 60000 60000

2 230000 410000 120000 180000

3 280000 690000 250000 430000

4 120000 810000 250000 680000

810000 680000

Payback period= A+ (B/C)

Where,

A= last year negative cumulative cash flow.

B=abstract value of cash flow at end of the year

C= cash flow in next year

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

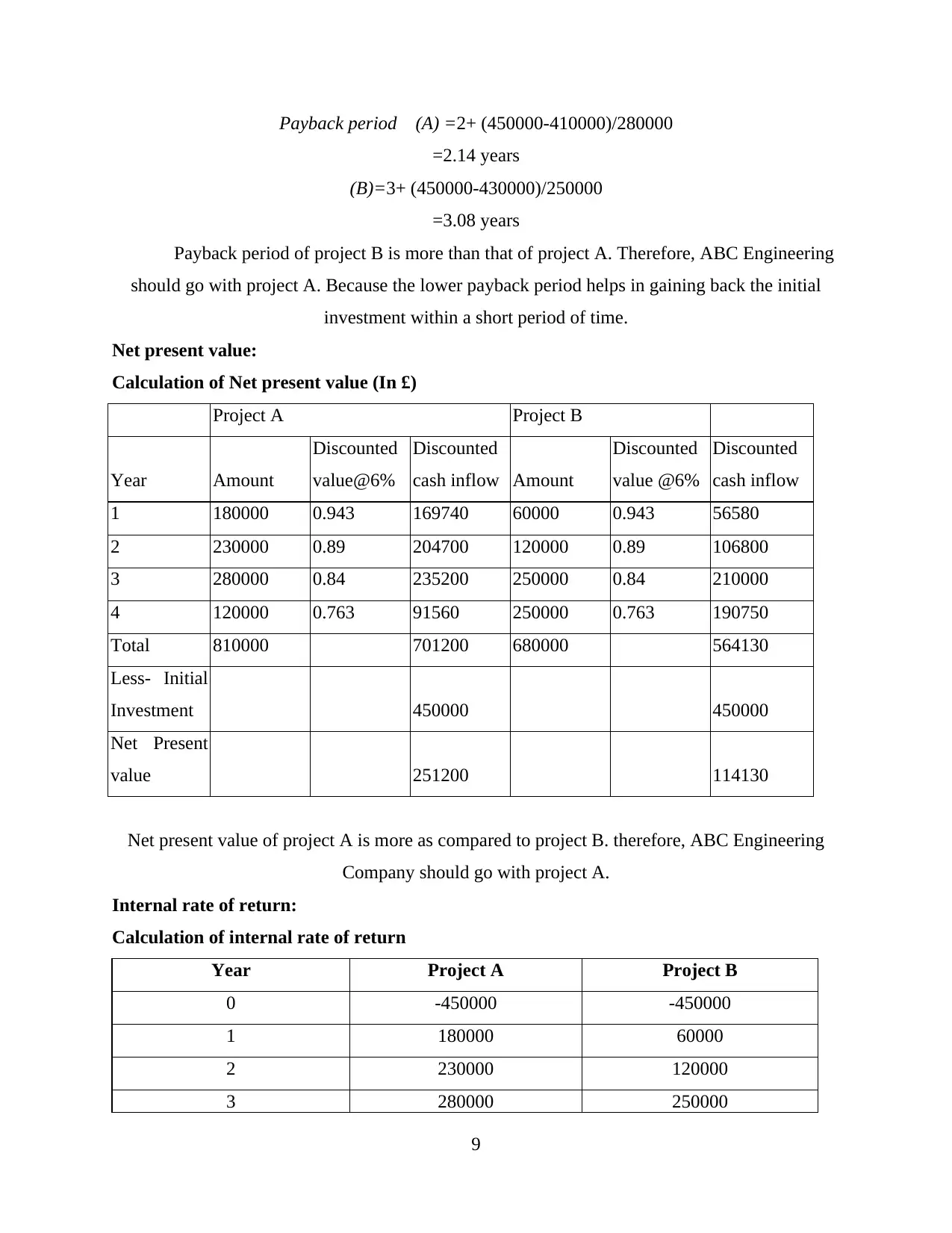

Payback period (A) =2+ (450000-410000)/280000

=2.14 years

(B)=3+ (450000-430000)/250000

=3.08 years

Payback period of project B is more than that of project A. Therefore, ABC Engineering

should go with project A. Because the lower payback period helps in gaining back the initial

investment within a short period of time.

Net present value:

Calculation of Net present value (In £)

Project A Project B

Year Amount

Discounted

value@6%

Discounted

cash inflow Amount

Discounted

value @6%

Discounted

cash inflow

1 180000 0.943 169740 60000 0.943 56580

2 230000 0.89 204700 120000 0.89 106800

3 280000 0.84 235200 250000 0.84 210000

4 120000 0.763 91560 250000 0.763 190750

Total 810000 701200 680000 564130

Less- Initial

Investment 450000 450000

Net Present

value 251200 114130

Net present value of project A is more as compared to project B. therefore, ABC Engineering

Company should go with project A.

Internal rate of return:

Calculation of internal rate of return

Year Project A Project B

0 -450000 -450000

1 180000 60000

2 230000 120000

3 280000 250000

9

=2.14 years

(B)=3+ (450000-430000)/250000

=3.08 years

Payback period of project B is more than that of project A. Therefore, ABC Engineering

should go with project A. Because the lower payback period helps in gaining back the initial

investment within a short period of time.

Net present value:

Calculation of Net present value (In £)

Project A Project B

Year Amount

Discounted

value@6%

Discounted

cash inflow Amount

Discounted

value @6%

Discounted

cash inflow

1 180000 0.943 169740 60000 0.943 56580

2 230000 0.89 204700 120000 0.89 106800

3 280000 0.84 235200 250000 0.84 210000

4 120000 0.763 91560 250000 0.763 190750

Total 810000 701200 680000 564130

Less- Initial

Investment 450000 450000

Net Present

value 251200 114130

Net present value of project A is more as compared to project B. therefore, ABC Engineering

Company should go with project A.

Internal rate of return:

Calculation of internal rate of return

Year Project A Project B

0 -450000 -450000

1 180000 60000

2 230000 120000

3 280000 250000

9

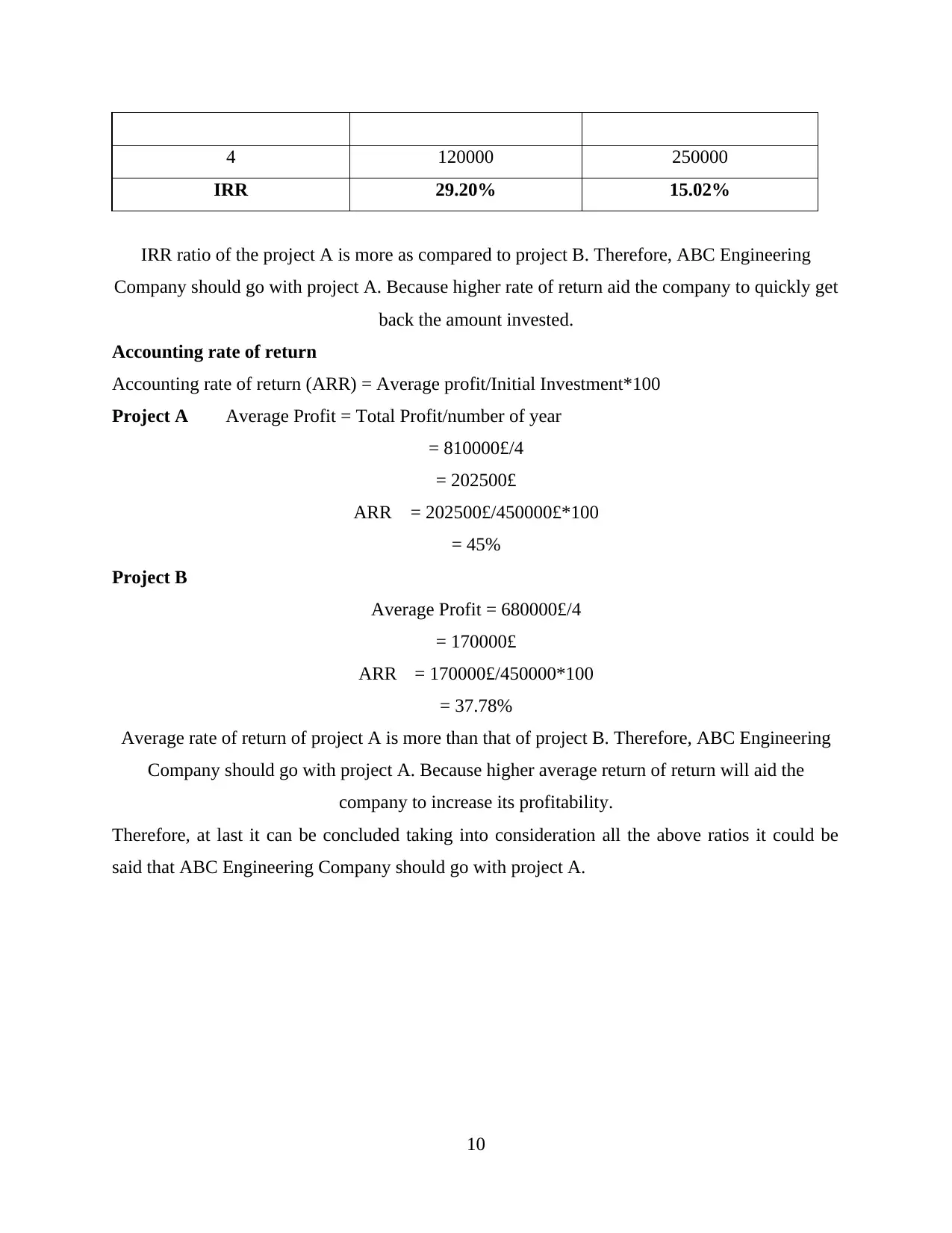

4 120000 250000

IRR 29.20% 15.02%

IRR ratio of the project A is more as compared to project B. Therefore, ABC Engineering

Company should go with project A. Because higher rate of return aid the company to quickly get

back the amount invested.

Accounting rate of return

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A Average Profit = Total Profit/number of year

= 810000£/4

= 202500£

ARR = 202500£/450000£*100

= 45%

Project B

Average Profit = 680000£/4

= 170000£

ARR = 170000£/450000*100

= 37.78%

Average rate of return of project A is more than that of project B. Therefore, ABC Engineering

Company should go with project A. Because higher average return of return will aid the

company to increase its profitability.

Therefore, at last it can be concluded taking into consideration all the above ratios it could be

said that ABC Engineering Company should go with project A.

10

IRR 29.20% 15.02%

IRR ratio of the project A is more as compared to project B. Therefore, ABC Engineering

Company should go with project A. Because higher rate of return aid the company to quickly get

back the amount invested.

Accounting rate of return

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A Average Profit = Total Profit/number of year

= 810000£/4

= 202500£

ARR = 202500£/450000£*100

= 45%

Project B

Average Profit = 680000£/4

= 170000£

ARR = 170000£/450000*100

= 37.78%

Average rate of return of project A is more than that of project B. Therefore, ABC Engineering

Company should go with project A. Because higher average return of return will aid the

company to increase its profitability.

Therefore, at last it can be concluded taking into consideration all the above ratios it could be

said that ABC Engineering Company should go with project A.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.