Financial Resources and Decisions: Analysis and Management Report

VerifiedAdded on 2020/01/07

|18

|5045

|278

Report

AI Summary

This report delves into the critical aspects of managing financial resources within a small-scale public enterprise. It begins by exploring various sources of finance, such as bank loans, SBA loans, loans from relatives, share issues, and retained earnings, evaluating their implications and appropriateness. The report then examines the costs associated with each source, including interest rates, fees, and dilution of ownership. Financial planning is highlighted as essential for business stability, covering objectives, policies, and the importance of stakeholder information. Internal and external stakeholders, including employees, owners, managers, creditors, and investors, and their information needs are discussed. Finally, the report emphasizes the impact of financial transactions on financial statements, such as the balance sheet and profit and loss account. The report concludes with a recommendation for a bank loan as a suitable funding source for the enterprise.

Managing Financial

Resources and Decisions

Resources and Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1.............................................................................................................................................. .1

1.2.............................................................................................................................................. .2

1.3.............................................................................................................................................. .3

2.1.............................................................................................................................................. .3

2.2.............................................................................................................................................. .4

2.3.............................................................................................................................................. .5

2.4.............................................................................................................................................. .5

3.1.............................................................................................................................................. .6

3.2.............................................................................................................................................. .7

3.3.............................................................................................................................................. .7

TASK 2............................................................................................................................................8

4.1.............................................................................................................................................. .8

4.2.............................................................................................................................................. .9

4.3.............................................................................................................................................. .9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1.............................................................................................................................................. .1

1.2.............................................................................................................................................. .2

1.3.............................................................................................................................................. .3

2.1.............................................................................................................................................. .3

2.2.............................................................................................................................................. .4

2.3.............................................................................................................................................. .5

2.4.............................................................................................................................................. .5

3.1.............................................................................................................................................. .6

3.2.............................................................................................................................................. .7

3.3.............................................................................................................................................. .7

TASK 2............................................................................................................................................8

4.1.............................................................................................................................................. .8

4.2.............................................................................................................................................. .9

4.3.............................................................................................................................................. .9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management of funds is an important function of every business entity. It aids in

determining needs and requirements of organization by properly analysing the objectives of firm.

Present study deals with the management of finance in context with a small scale public

enterprise. Main purpose of the current research is to provide learners with an overview of the

way and time for using various sources of finance along with making appropriate use of financial

resources in decision making process. Readers will also get a brief overview of various

techniques such as Net Present Value to make pricing decisions. Further, a cash budget is being

prepared and presented along with the unit cost.

TASK 1

1.1

Arrangement of finance is the most crucial part of setting a new business enterprise. It

requires complete analysis of various sources of finance in terms of its strengths and weaknesses.

With regard to the present research, various sources of funds are available with the government

entrepreneur which are discussed beneath: Bank Loan: It is the most common and well known external source of finance. Banks

provide loans to the businessman in order to setup a new business. On the behalf of

offering loan, it requires some kind of security from the entrepreneur. The loan is offered

for a particular period in which businessman has to refund the original amount with

prevailing interest rates (Bose, 2006). SBA loans: These are small business government owned organizations who offer loans to

the new businessman. Some amount of guarantee is being provided to lender in respect to

the non-payment of amount. Furthermore, the amount of interest also differs on the basis

of size of loans. Larger the amount would be, lesser will be its interest rate. Loans from relatives: Funds can also be arranged from the relatives and friends of

individuals if they are willing to invest in business. This is the best and easiest form of

source available to a businessman although there exist many pitfalls. Share Issues: By the means of issuing shares in market, a company can raise funds for its

start-up. Issuing of shares also relates to sharing of decision making power with the

shareholders of company (Brigham, 2001).

1

Management of funds is an important function of every business entity. It aids in

determining needs and requirements of organization by properly analysing the objectives of firm.

Present study deals with the management of finance in context with a small scale public

enterprise. Main purpose of the current research is to provide learners with an overview of the

way and time for using various sources of finance along with making appropriate use of financial

resources in decision making process. Readers will also get a brief overview of various

techniques such as Net Present Value to make pricing decisions. Further, a cash budget is being

prepared and presented along with the unit cost.

TASK 1

1.1

Arrangement of finance is the most crucial part of setting a new business enterprise. It

requires complete analysis of various sources of finance in terms of its strengths and weaknesses.

With regard to the present research, various sources of funds are available with the government

entrepreneur which are discussed beneath: Bank Loan: It is the most common and well known external source of finance. Banks

provide loans to the businessman in order to setup a new business. On the behalf of

offering loan, it requires some kind of security from the entrepreneur. The loan is offered

for a particular period in which businessman has to refund the original amount with

prevailing interest rates (Bose, 2006). SBA loans: These are small business government owned organizations who offer loans to

the new businessman. Some amount of guarantee is being provided to lender in respect to

the non-payment of amount. Furthermore, the amount of interest also differs on the basis

of size of loans. Larger the amount would be, lesser will be its interest rate. Loans from relatives: Funds can also be arranged from the relatives and friends of

individuals if they are willing to invest in business. This is the best and easiest form of

source available to a businessman although there exist many pitfalls. Share Issues: By the means of issuing shares in market, a company can raise funds for its

start-up. Issuing of shares also relates to sharing of decision making power with the

shareholders of company (Brigham, 2001).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained Earnings: It is a methods of using the profit earned by the organization in a

specific period of time and reusing it again by reinvesting in the company.

Business Angels: As per the current method there are several firms that deliver the goods

to the business organization on behalf of certain ownership of shares of the company.

1.2

Implications of various sources of finance depend largely upon the size, type and duration

of business, cost of financing, etc. So, the feasibility of different kinds of sources can be easily

analysed by reviewing its benefits and drawbacks.

Sources of

finance

Financial Implication Legal Implication Dilution implication

Bank Loan The company's liability

will be raised resulting in a

consequent increase in the

liquidity of the firm.

The bank is entitled to

seize the assets of the

company if it is unable

to repay the entire

amount. Apart from

it,the bank has the right

to sell assets of the firm

at times of bankruptcy.

The firm needs to refund

the exact remaining

amount to the bank after

selling his business as

well as personal assets if

the amount is not

sufficient.

SBA Loans It is likely to affect the

liquidity and profitability

of the firm as the loan

taken from government

will be regarded as a

liability for the company.

The company needs to

perform under the set

guidelines which is

provided by the

government.

At times of dilution of

the company need not to

refund any sort of

amount back to the

government taken in

form of loan.

Loans from

relatives

It is likely to impact on the

balance sheet of the firm

in the form of increase in

liability of the company.

If the business is proved

to be bankrupt then the

repayment of loan is not

necessary.

At times of diluting the

company, the relatives

are entitled to receive all

the amount back.

2

specific period of time and reusing it again by reinvesting in the company.

Business Angels: As per the current method there are several firms that deliver the goods

to the business organization on behalf of certain ownership of shares of the company.

1.2

Implications of various sources of finance depend largely upon the size, type and duration

of business, cost of financing, etc. So, the feasibility of different kinds of sources can be easily

analysed by reviewing its benefits and drawbacks.

Sources of

finance

Financial Implication Legal Implication Dilution implication

Bank Loan The company's liability

will be raised resulting in a

consequent increase in the

liquidity of the firm.

The bank is entitled to

seize the assets of the

company if it is unable

to repay the entire

amount. Apart from

it,the bank has the right

to sell assets of the firm

at times of bankruptcy.

The firm needs to refund

the exact remaining

amount to the bank after

selling his business as

well as personal assets if

the amount is not

sufficient.

SBA Loans It is likely to affect the

liquidity and profitability

of the firm as the loan

taken from government

will be regarded as a

liability for the company.

The company needs to

perform under the set

guidelines which is

provided by the

government.

At times of dilution of

the company need not to

refund any sort of

amount back to the

government taken in

form of loan.

Loans from

relatives

It is likely to impact on the

balance sheet of the firm

in the form of increase in

liability of the company.

If the business is proved

to be bankrupt then the

repayment of loan is not

necessary.

At times of diluting the

company, the relatives

are entitled to receive all

the amount back.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

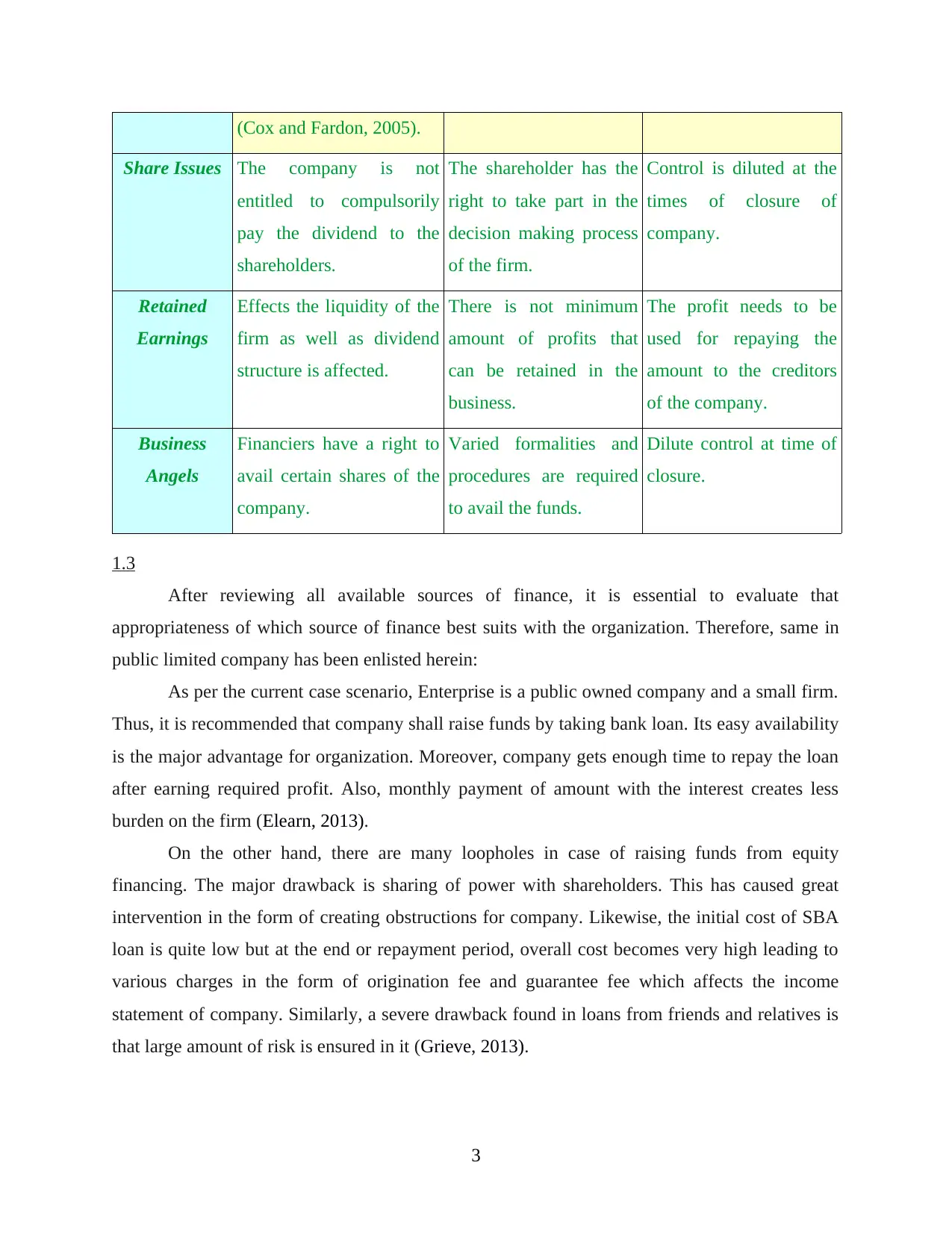

(Cox and Fardon, 2005).

Share Issues The company is not

entitled to compulsorily

pay the dividend to the

shareholders.

The shareholder has the

right to take part in the

decision making process

of the firm.

Control is diluted at the

times of closure of

company.

Retained

Earnings

Effects the liquidity of the

firm as well as dividend

structure is affected.

There is not minimum

amount of profits that

can be retained in the

business.

The profit needs to be

used for repaying the

amount to the creditors

of the company.

Business

Angels

Financiers have a right to

avail certain shares of the

company.

Varied formalities and

procedures are required

to avail the funds.

Dilute control at time of

closure.

1.3

After reviewing all available sources of finance, it is essential to evaluate that

appropriateness of which source of finance best suits with the organization. Therefore, same in

public limited company has been enlisted herein:

As per the current case scenario, Enterprise is a public owned company and a small firm.

Thus, it is recommended that company shall raise funds by taking bank loan. Its easy availability

is the major advantage for organization. Moreover, company gets enough time to repay the loan

after earning required profit. Also, monthly payment of amount with the interest creates less

burden on the firm (Elearn, 2013).

On the other hand, there are many loopholes in case of raising funds from equity

financing. The major drawback is sharing of power with shareholders. This has caused great

intervention in the form of creating obstructions for company. Likewise, the initial cost of SBA

loan is quite low but at the end or repayment period, overall cost becomes very high leading to

various charges in the form of origination fee and guarantee fee which affects the income

statement of company. Similarly, a severe drawback found in loans from friends and relatives is

that large amount of risk is ensured in it (Grieve, 2013).

3

Share Issues The company is not

entitled to compulsorily

pay the dividend to the

shareholders.

The shareholder has the

right to take part in the

decision making process

of the firm.

Control is diluted at the

times of closure of

company.

Retained

Earnings

Effects the liquidity of the

firm as well as dividend

structure is affected.

There is not minimum

amount of profits that

can be retained in the

business.

The profit needs to be

used for repaying the

amount to the creditors

of the company.

Business

Angels

Financiers have a right to

avail certain shares of the

company.

Varied formalities and

procedures are required

to avail the funds.

Dilute control at time of

closure.

1.3

After reviewing all available sources of finance, it is essential to evaluate that

appropriateness of which source of finance best suits with the organization. Therefore, same in

public limited company has been enlisted herein:

As per the current case scenario, Enterprise is a public owned company and a small firm.

Thus, it is recommended that company shall raise funds by taking bank loan. Its easy availability

is the major advantage for organization. Moreover, company gets enough time to repay the loan

after earning required profit. Also, monthly payment of amount with the interest creates less

burden on the firm (Elearn, 2013).

On the other hand, there are many loopholes in case of raising funds from equity

financing. The major drawback is sharing of power with shareholders. This has caused great

intervention in the form of creating obstructions for company. Likewise, the initial cost of SBA

loan is quite low but at the end or repayment period, overall cost becomes very high leading to

various charges in the form of origination fee and guarantee fee which affects the income

statement of company. Similarly, a severe drawback found in loans from friends and relatives is

that large amount of risk is ensured in it (Grieve, 2013).

3

2.1

Various costs derived by the said organization from above mentioned sources of finance

are discussed underneath: Cost of taking bank loan: Entrepreneur needs to understand the difference between

nominal and effective interest rate. Further, government companies need to spend various

amounts in the form of commissions, tax rates, monthly interest fees, etc. Moreover, if

company repays the amount of loan before maturity date, it needs to pay certain amount

in the form of compensation of paying early. Cost of taking SBA loan: Amount of original loan and interest is not the only cost

incurred by borrower. The lender charges origination fee in order to cover its marketing

cost. It is set by the financial institution usually at 4%. For instance, the current amount

required by entrepreneur is £280000 to start its business (Helfert, 2004). The actual

amount received by him will be merely £16800. Along with that, guarantee fee and

annual percentage yield is the amount that borrower needs to pay at the time of

repayment. Loans from friends and relatives: There is no or very minimal cost incurred by taking

loans from friends and family. Actual amount that the entrepreneur will incur is amount

of repayment of loan along with a very less interest rate charged by the lender.

Equity financing: The owner needs to spend a huge amount in terms of application

money, advertisement in newspaper, etc. Owner needs to evaluate the actual return on

equity by identifying dividend per share of the next year and current market value of

share. This will enable the firm to know actual profit derived from equity financing

(Hildreth, 2004).

2.2

Financial planning is essential for every business organization in order to manage funds

in the most appropriate manner. It is the process of setting objectives, planning policies,

procedures, budgets and programmes for the given organization. The importance of financial

planning has been highlighted as below:

It aids in ensuring appropriate funds for carrying out the business operations.

Financial planning assists in measuring the supply and demand of funds for business

enterprise to maintain stability (Jenkins, 2002).

4

Various costs derived by the said organization from above mentioned sources of finance

are discussed underneath: Cost of taking bank loan: Entrepreneur needs to understand the difference between

nominal and effective interest rate. Further, government companies need to spend various

amounts in the form of commissions, tax rates, monthly interest fees, etc. Moreover, if

company repays the amount of loan before maturity date, it needs to pay certain amount

in the form of compensation of paying early. Cost of taking SBA loan: Amount of original loan and interest is not the only cost

incurred by borrower. The lender charges origination fee in order to cover its marketing

cost. It is set by the financial institution usually at 4%. For instance, the current amount

required by entrepreneur is £280000 to start its business (Helfert, 2004). The actual

amount received by him will be merely £16800. Along with that, guarantee fee and

annual percentage yield is the amount that borrower needs to pay at the time of

repayment. Loans from friends and relatives: There is no or very minimal cost incurred by taking

loans from friends and family. Actual amount that the entrepreneur will incur is amount

of repayment of loan along with a very less interest rate charged by the lender.

Equity financing: The owner needs to spend a huge amount in terms of application

money, advertisement in newspaper, etc. Owner needs to evaluate the actual return on

equity by identifying dividend per share of the next year and current market value of

share. This will enable the firm to know actual profit derived from equity financing

(Hildreth, 2004).

2.2

Financial planning is essential for every business organization in order to manage funds

in the most appropriate manner. It is the process of setting objectives, planning policies,

procedures, budgets and programmes for the given organization. The importance of financial

planning has been highlighted as below:

It aids in ensuring appropriate funds for carrying out the business operations.

Financial planning assists in measuring the supply and demand of funds for business

enterprise to maintain stability (Jenkins, 2002).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It also helps in meeting uncertainties regardless of the changing market trends.

The main purpose of financial planning is to ensure future growth and expansion by

proper allocation and preservation of funds.

Moreover, financial planning is done to ensure timely investment of funds by the money

suppliers. This will not affect the operations of business organization.

Therefore, in context with the new business entity, entrepreneur needs to conduct

financial planning in order to meets its objectives (Keller, 2013). For this purpose, it needs to

collect various data regarding current supply of funds from different sources. Along with that,

proper evaluation of the client’s financial status needs to be addressed. It will further help in

presenting suggestions and alternatives to manage the funds for company.

2.3

Various stakeholders and owners of company are interested in knowing its financial

information. It aids them in making decisions and knowing their future in the present enterprise.

Internal users of information: Employees: Financial position of company has a direct impact on the salary of

employees. Therefore, they require financial information to ascertain their remuneration

and job security. Moreover if the firm earns more then the employees are entitled to

receive increase salary. (Khamees, Al-Fayoumi and Al-Thuneibat, 2010). Owners: This information becomes the basis for owner’s decision making regarding the

future investment in company. Owners need to review the balance sheet and profit and

loss statement periodically in order to ascertain the current profit that company is making.

If the company's assets are liquid enough then the owners shall take decisions to

minimise the same. Management: Managers of the firm make decisions and strategies based on this

information. It also provides them an outlook of the overall position and performance of

organization in market. They are also responsible to ascertain the current profitability and

liquidity of the firm so as to undertaken various actions to meet the obligations of the

company.

External Users: Creditors: They need information to review the credit worthiness of firm. Their decisions

of providing credit and loans entirely depend upon these facts and figures. If the firm is

5

The main purpose of financial planning is to ensure future growth and expansion by

proper allocation and preservation of funds.

Moreover, financial planning is done to ensure timely investment of funds by the money

suppliers. This will not affect the operations of business organization.

Therefore, in context with the new business entity, entrepreneur needs to conduct

financial planning in order to meets its objectives (Keller, 2013). For this purpose, it needs to

collect various data regarding current supply of funds from different sources. Along with that,

proper evaluation of the client’s financial status needs to be addressed. It will further help in

presenting suggestions and alternatives to manage the funds for company.

2.3

Various stakeholders and owners of company are interested in knowing its financial

information. It aids them in making decisions and knowing their future in the present enterprise.

Internal users of information: Employees: Financial position of company has a direct impact on the salary of

employees. Therefore, they require financial information to ascertain their remuneration

and job security. Moreover if the firm earns more then the employees are entitled to

receive increase salary. (Khamees, Al-Fayoumi and Al-Thuneibat, 2010). Owners: This information becomes the basis for owner’s decision making regarding the

future investment in company. Owners need to review the balance sheet and profit and

loss statement periodically in order to ascertain the current profit that company is making.

If the company's assets are liquid enough then the owners shall take decisions to

minimise the same. Management: Managers of the firm make decisions and strategies based on this

information. It also provides them an outlook of the overall position and performance of

organization in market. They are also responsible to ascertain the current profitability and

liquidity of the firm so as to undertaken various actions to meet the obligations of the

company.

External Users: Creditors: They need information to review the credit worthiness of firm. Their decisions

of providing credit and loans entirely depend upon these facts and figures. If the firm is

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

making more profit in a particular period then the creditors are likely to provide loans and

goods on credit basis (Melo, 2012). Regulatory and tax authorities: They require information to ensure that company is

worthy enough to pay taxes and also, to make sure that information provided to its

shareholders is appropriate. If the profit of the company is nominal and high enough then

the organization is obliged to repay the appropriate amount of tax. This will enable the

firm to maintain its liquidity and provide a true picture of its profitability to the company.

Investors: These are the people who invest in company and they require this information

to ensure that they will receive reasonable returns on investment made. Higher the

profitability of the firm more will be the investment made by the investors.

2.4

Every transaction of business has an equal and subsequent impact on the balance sheet

and profit and loss account of company. Likewise, the issuance of new shares or taking of loan

from banks also affects these statements (Murphy and Yetmar, 2010).

When a company takes loan for sum of £280000, then it will affect the balance sheet in

form of increase in cash and contrary on the liability side, same shall be shown in order to track

the loan. Therefore, it can be said that all these finance have consequent impact on the income

statement.

Likewise, other sources of finance such as SBA and loan from relatives will also possess

a similar impact as that of the bank loan. Moreover, in the former source of funds, some amount

of expenses is also incurred by the firm which shall be shown in the income statement of the

company (Nelson, 2012).

In case of issuing shares by new business enterprise, it needs to increase the interest rates.

It is because; in order to issue new shares, company requires capital to be invested. Further, rise

in interest rates also demonstrate that the firm needs to pay higher dividends from profit (Nga

and Yien, 2013). All these transactions affect the balance sheet as issuing of shares lead to rise in

capital which shall be highlighted in the balance sheet. Likewise, rise in dividends is also shown

and marked in profit and loss account.

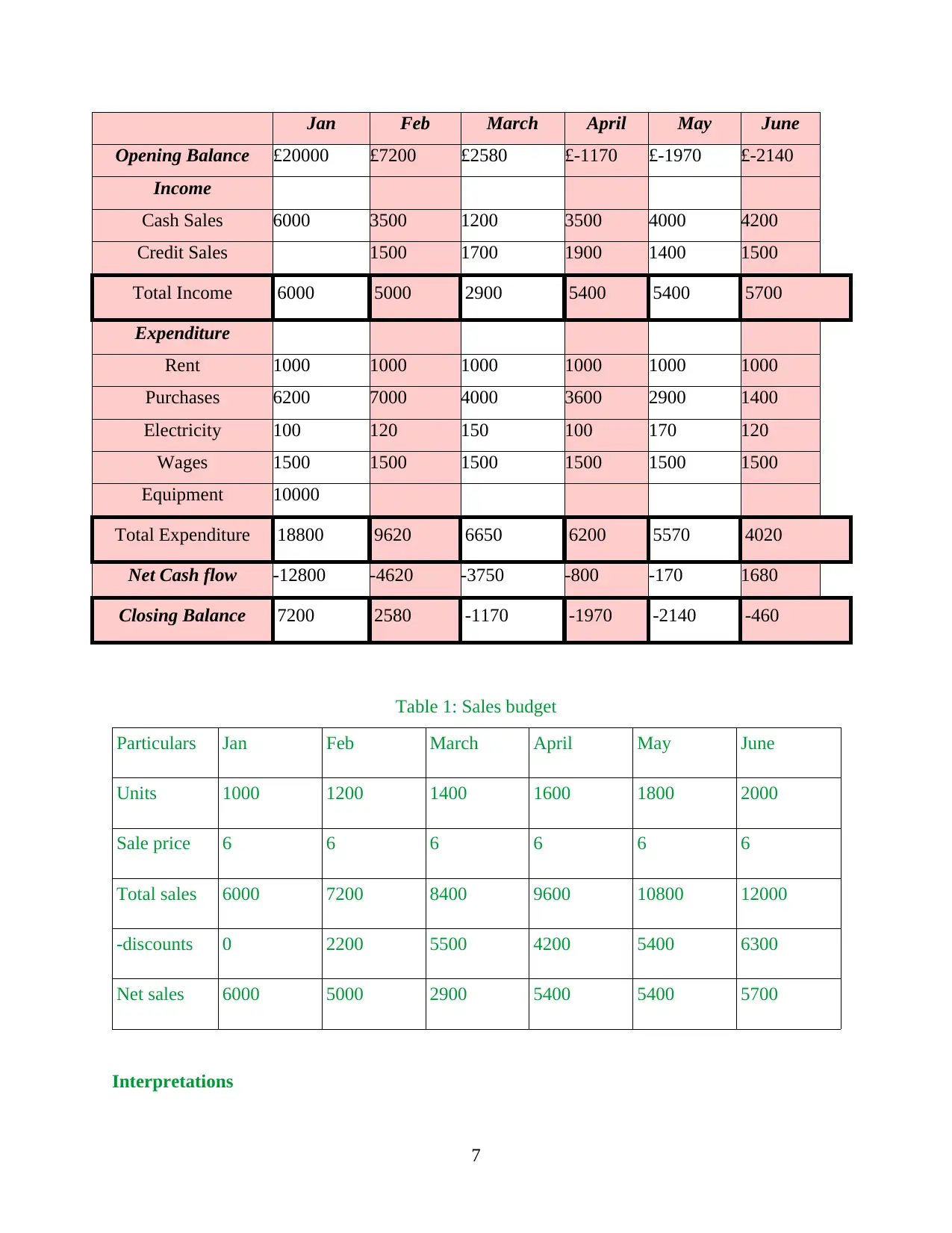

3.1

Cash Budget statement for January to June 2016

6

goods on credit basis (Melo, 2012). Regulatory and tax authorities: They require information to ensure that company is

worthy enough to pay taxes and also, to make sure that information provided to its

shareholders is appropriate. If the profit of the company is nominal and high enough then

the organization is obliged to repay the appropriate amount of tax. This will enable the

firm to maintain its liquidity and provide a true picture of its profitability to the company.

Investors: These are the people who invest in company and they require this information

to ensure that they will receive reasonable returns on investment made. Higher the

profitability of the firm more will be the investment made by the investors.

2.4

Every transaction of business has an equal and subsequent impact on the balance sheet

and profit and loss account of company. Likewise, the issuance of new shares or taking of loan

from banks also affects these statements (Murphy and Yetmar, 2010).

When a company takes loan for sum of £280000, then it will affect the balance sheet in

form of increase in cash and contrary on the liability side, same shall be shown in order to track

the loan. Therefore, it can be said that all these finance have consequent impact on the income

statement.

Likewise, other sources of finance such as SBA and loan from relatives will also possess

a similar impact as that of the bank loan. Moreover, in the former source of funds, some amount

of expenses is also incurred by the firm which shall be shown in the income statement of the

company (Nelson, 2012).

In case of issuing shares by new business enterprise, it needs to increase the interest rates.

It is because; in order to issue new shares, company requires capital to be invested. Further, rise

in interest rates also demonstrate that the firm needs to pay higher dividends from profit (Nga

and Yien, 2013). All these transactions affect the balance sheet as issuing of shares lead to rise in

capital which shall be highlighted in the balance sheet. Likewise, rise in dividends is also shown

and marked in profit and loss account.

3.1

Cash Budget statement for January to June 2016

6

Jan Feb March April May June

Opening Balance £20000 £7200 £2580 £-1170 £-1970 £-2140

Income

Cash Sales 6000 3500 1200 3500 4000 4200

Credit Sales 1500 1700 1900 1400 1500

Total Income 6000 5000 2900 5400 5400 5700

Expenditure

Rent 1000 1000 1000 1000 1000 1000

Purchases 6200 7000 4000 3600 2900 1400

Electricity 100 120 150 100 170 120

Wages 1500 1500 1500 1500 1500 1500

Equipment 10000

Total Expenditure 18800 9620 6650 6200 5570 4020

Net Cash flow -12800 -4620 -3750 -800 -170 1680

Closing Balance 7200 2580 -1170 -1970 -2140 -460

Table 1: Sales budget

Particulars Jan Feb March April May June

Units 1000 1200 1400 1600 1800 2000

Sale price 6 6 6 6 6 6

Total sales 6000 7200 8400 9600 10800 12000

-discounts 0 2200 5500 4200 5400 6300

Net sales 6000 5000 2900 5400 5400 5700

Interpretations

7

Opening Balance £20000 £7200 £2580 £-1170 £-1970 £-2140

Income

Cash Sales 6000 3500 1200 3500 4000 4200

Credit Sales 1500 1700 1900 1400 1500

Total Income 6000 5000 2900 5400 5400 5700

Expenditure

Rent 1000 1000 1000 1000 1000 1000

Purchases 6200 7000 4000 3600 2900 1400

Electricity 100 120 150 100 170 120

Wages 1500 1500 1500 1500 1500 1500

Equipment 10000

Total Expenditure 18800 9620 6650 6200 5570 4020

Net Cash flow -12800 -4620 -3750 -800 -170 1680

Closing Balance 7200 2580 -1170 -1970 -2140 -460

Table 1: Sales budget

Particulars Jan Feb March April May June

Units 1000 1200 1400 1600 1800 2000

Sale price 6 6 6 6 6 6

Total sales 6000 7200 8400 9600 10800 12000

-discounts 0 2200 5500 4200 5400 6300

Net sales 6000 5000 2900 5400 5400 5700

Interpretations

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It has been recommended that company must first appropriately allocate its resources and keep

aside some amount for the recurring expenses. Currently, the firm is facing problem of budgeting

and it is not able to meet its expenses. For this purpose, the said organization needs to start using

option of credit purchase. This will enable the organization to meet its expenses at the end of

period.

3.2

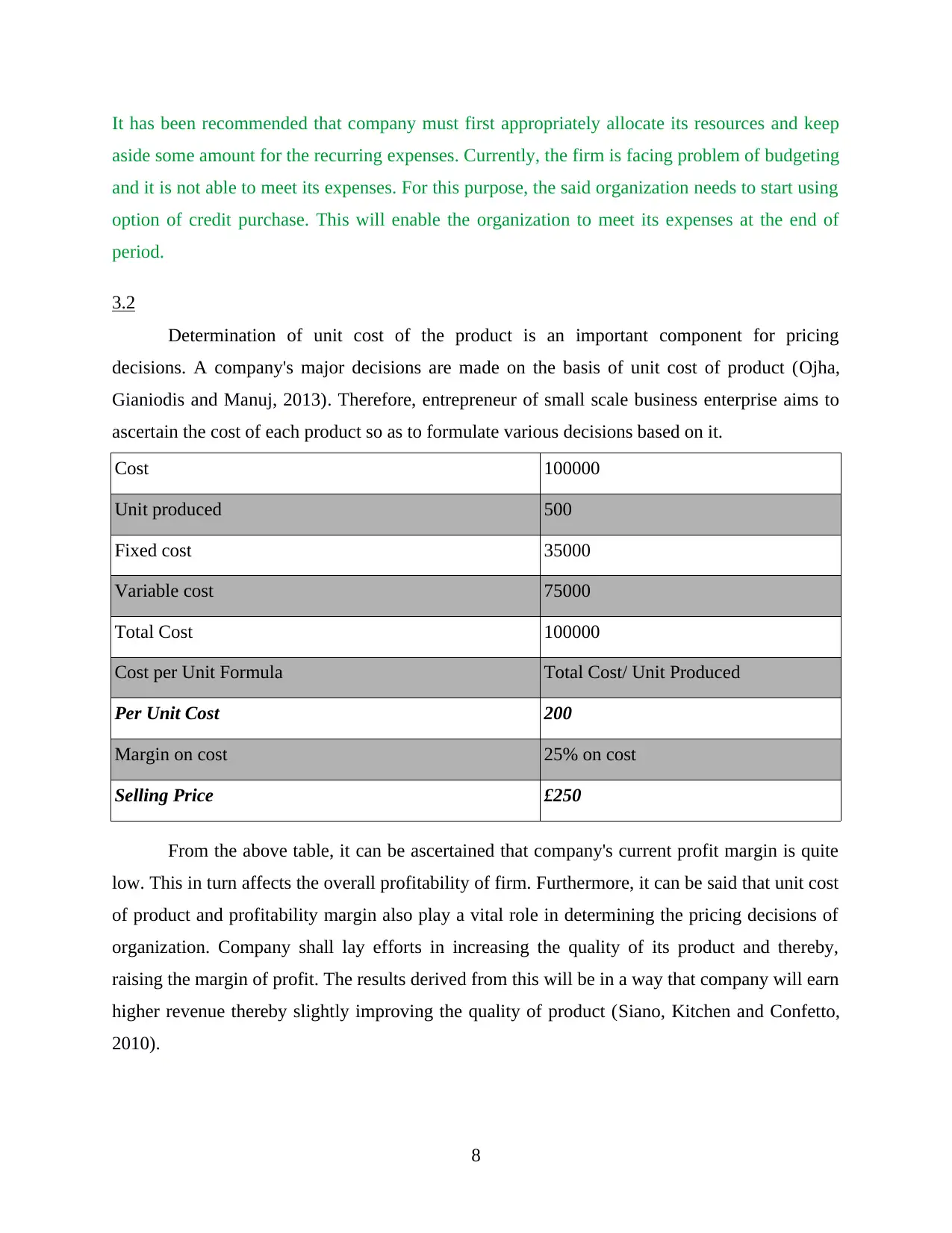

Determination of unit cost of the product is an important component for pricing

decisions. A company's major decisions are made on the basis of unit cost of product (Ojha,

Gianiodis and Manuj, 2013). Therefore, entrepreneur of small scale business enterprise aims to

ascertain the cost of each product so as to formulate various decisions based on it.

Cost 100000

Unit produced 500

Fixed cost 35000

Variable cost 75000

Total Cost 100000

Cost per Unit Formula Total Cost/ Unit Produced

Per Unit Cost 200

Margin on cost 25% on cost

Selling Price £250

From the above table, it can be ascertained that company's current profit margin is quite

low. This in turn affects the overall profitability of firm. Furthermore, it can be said that unit cost

of product and profitability margin also play a vital role in determining the pricing decisions of

organization. Company shall lay efforts in increasing the quality of its product and thereby,

raising the margin of profit. The results derived from this will be in a way that company will earn

higher revenue thereby slightly improving the quality of product (Siano, Kitchen and Confetto,

2010).

8

aside some amount for the recurring expenses. Currently, the firm is facing problem of budgeting

and it is not able to meet its expenses. For this purpose, the said organization needs to start using

option of credit purchase. This will enable the organization to meet its expenses at the end of

period.

3.2

Determination of unit cost of the product is an important component for pricing

decisions. A company's major decisions are made on the basis of unit cost of product (Ojha,

Gianiodis and Manuj, 2013). Therefore, entrepreneur of small scale business enterprise aims to

ascertain the cost of each product so as to formulate various decisions based on it.

Cost 100000

Unit produced 500

Fixed cost 35000

Variable cost 75000

Total Cost 100000

Cost per Unit Formula Total Cost/ Unit Produced

Per Unit Cost 200

Margin on cost 25% on cost

Selling Price £250

From the above table, it can be ascertained that company's current profit margin is quite

low. This in turn affects the overall profitability of firm. Furthermore, it can be said that unit cost

of product and profitability margin also play a vital role in determining the pricing decisions of

organization. Company shall lay efforts in increasing the quality of its product and thereby,

raising the margin of profit. The results derived from this will be in a way that company will earn

higher revenue thereby slightly improving the quality of product (Siano, Kitchen and Confetto,

2010).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

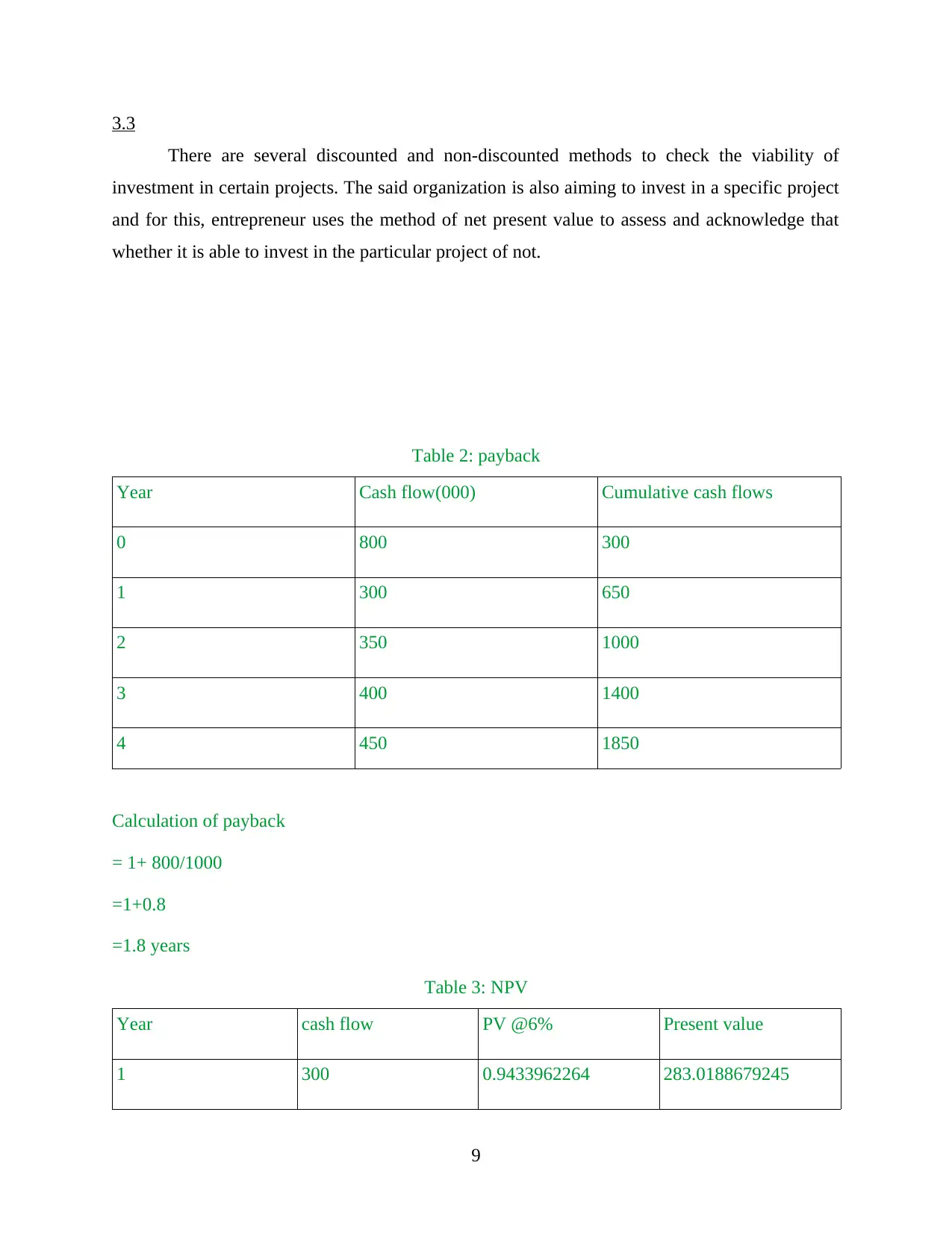

3.3

There are several discounted and non-discounted methods to check the viability of

investment in certain projects. The said organization is also aiming to invest in a specific project

and for this, entrepreneur uses the method of net present value to assess and acknowledge that

whether it is able to invest in the particular project of not.

Table 2: payback

Year Cash flow(000) Cumulative cash flows

0 800 300

1 300 650

2 350 1000

3 400 1400

4 450 1850

Calculation of payback

= 1+ 800/1000

=1+0.8

=1.8 years

Table 3: NPV

Year cash flow PV @6% Present value

1 300 0.9433962264 283.0188679245

9

There are several discounted and non-discounted methods to check the viability of

investment in certain projects. The said organization is also aiming to invest in a specific project

and for this, entrepreneur uses the method of net present value to assess and acknowledge that

whether it is able to invest in the particular project of not.

Table 2: payback

Year Cash flow(000) Cumulative cash flows

0 800 300

1 300 650

2 350 1000

3 400 1400

4 450 1850

Calculation of payback

= 1+ 800/1000

=1+0.8

=1.8 years

Table 3: NPV

Year cash flow PV @6% Present value

1 300 0.9433962264 283.0188679245

9

2 350 0.88999644 311.498754005

3 400 0.839619283 335.8477132129

4 450 0.7920936632 356.4421484571

Total 1286.8074835996

NPV 486.8074835995

Interpretations

Table 4: IRR

Year cash flow PV @6%

Present

value Cash flow Pv @ 8%

Present

value

1 300

0.94339622

64 283.01 300

0.92592592

59 277.77

2 350 0.88999644 311.49 350

0.85733882

03 300.06

3 400

0.83961928

3 335.84 400

0.79383224

1 317.53

4 450

0.79209366

32 356.44 450

0.73502985

28 330.76

Total 1286.80 1226.14

NPV

486.807483

5995 426.14

Calculation of IRR

= A+ PVA- initial investment/PVA-PVB*(B-A)

10

3 400 0.839619283 335.8477132129

4 450 0.7920936632 356.4421484571

Total 1286.8074835996

NPV 486.8074835995

Interpretations

Table 4: IRR

Year cash flow PV @6%

Present

value Cash flow Pv @ 8%

Present

value

1 300

0.94339622

64 283.01 300

0.92592592

59 277.77

2 350 0.88999644 311.49 350

0.85733882

03 300.06

3 400

0.83961928

3 335.84 400

0.79383224

1 317.53

4 450

0.79209366

32 356.44 450

0.73502985

28 330.76

Total 1286.80 1226.14

NPV

486.807483

5995 426.14

Calculation of IRR

= A+ PVA- initial investment/PVA-PVB*(B-A)

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.