Financial Analysis and Resource Management at Radisson Plc

VerifiedAdded on 2020/01/07

|16

|4344

|25

Report

AI Summary

This report provides a comprehensive analysis of Radisson Plc's financial resource management and decision-making processes. It begins by identifying and evaluating appropriate sources of finance, including internal and external options like retained profits, bank loans, and equity shares, considering their implications for an expansion project. The report then delves into the analysis of debt versus equity financing, emphasizing the costs and benefits of each, and the significance of financial planning for effective decision-making. Furthermore, it examines the impact of funding options on financial statements, highlighting the effects on the statement of comprehensive income and the statement of financial position. Budgeting, cost analysis, pricing decisions, and the assessment of expansion project viability are also discussed. The report concludes with an in-depth analysis of Radisson Plc's financial statements, including comparisons and the use of financial ratios to interpret performance, providing a thorough understanding of the company's financial health and strategic choices.

Managing Financial

Resources and

Decisions

1

Resources and

Decisions

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A. Identifying the appropriate sources of finance for selected business.....................................3

B. Evaluating the appropriate sources of finance for expansion plan of Radisson plc................5

TASK 2............................................................................................................................................5

A. Analysis and evaluation of cost of debt versus equity financing............................................5

B. Significance of monetary planning and information need of decision-makers.......................6

C. Impact of recommended funding option on the financial statements.....................................7

TASK 3............................................................................................................................................8

A. Importance of budget for variation........................................................................................8

B. Calculating unit cost and making pricing decision.................................................................9

C. Assessing the viability of the expansion project...................................................................10

TASK 4..........................................................................................................................................11

A. Discussion of financial statement of Radisson Plc...............................................................11

B. Comparison of financial statement of two companies..........................................................12

C. Interpretation of financial statement using suitable ratios....................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A. Identifying the appropriate sources of finance for selected business.....................................3

B. Evaluating the appropriate sources of finance for expansion plan of Radisson plc................5

TASK 2............................................................................................................................................5

A. Analysis and evaluation of cost of debt versus equity financing............................................5

B. Significance of monetary planning and information need of decision-makers.......................6

C. Impact of recommended funding option on the financial statements.....................................7

TASK 3............................................................................................................................................8

A. Importance of budget for variation........................................................................................8

B. Calculating unit cost and making pricing decision.................................................................9

C. Assessing the viability of the expansion project...................................................................10

TASK 4..........................................................................................................................................11

A. Discussion of financial statement of Radisson Plc...............................................................11

B. Comparison of financial statement of two companies..........................................................12

C. Interpretation of financial statement using suitable ratios....................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

2

INTRODUCTION

Financial resources are considered as one of the imperative aspect for success of business

as it helps in arranging other sources for maintaining higher rate of return of business. It covers

different activities through which cost of production can be controlled and rate of return for

business can be increased. Present report is based on Radisson plc a medium size computer

software manufacturing company which is operating in international marketplace. Furthermore,

sources of finance are explained for expansion project of the business. Furthermore, implication

of different sources of finance are also explained whereby corporation to get affected. In addition

to this, budgeting control, investment appraisal techniques and ratio analysis are also explained

along for selection of most appropriate project for the business.

TASK 1

A. Identifying the appropriate sources of finance for selected business

There are different sources of finance which can be accessed by business for successful

operation of corporation in the marketplace. For this purpose, below mentioned sources of

finance can be accessed by selected business-

Internal sources

According to the given case study, management of Radison is planning to expand its

venture in the marketplace which can be made possible only with the help of acquiring cost

effective sources such as retained profit, sale of old assets and owner's capital. It would be

effective Radisson plc to expand its business at large level and meet expectations of all related

stakeholders in an effectual manner (Lapsley, Miller and Panozzo, 2010). Furthermore, retained

profit is another aspect which is generally kept aside for investment purpose. This proves to be

effective for corporation to expand business at international level. It enables management to

deliver good quality of services to large number of so that accordingly competitive edge of the

business can be created in the marketplace. Moreover, sale of old assets reflects that management

acquire internal source of fund in order to meet short term requirement of corporation in the

marketplace.

External sources

3

Financial resources are considered as one of the imperative aspect for success of business

as it helps in arranging other sources for maintaining higher rate of return of business. It covers

different activities through which cost of production can be controlled and rate of return for

business can be increased. Present report is based on Radisson plc a medium size computer

software manufacturing company which is operating in international marketplace. Furthermore,

sources of finance are explained for expansion project of the business. Furthermore, implication

of different sources of finance are also explained whereby corporation to get affected. In addition

to this, budgeting control, investment appraisal techniques and ratio analysis are also explained

along for selection of most appropriate project for the business.

TASK 1

A. Identifying the appropriate sources of finance for selected business

There are different sources of finance which can be accessed by business for successful

operation of corporation in the marketplace. For this purpose, below mentioned sources of

finance can be accessed by selected business-

Internal sources

According to the given case study, management of Radison is planning to expand its

venture in the marketplace which can be made possible only with the help of acquiring cost

effective sources such as retained profit, sale of old assets and owner's capital. It would be

effective Radisson plc to expand its business at large level and meet expectations of all related

stakeholders in an effectual manner (Lapsley, Miller and Panozzo, 2010). Furthermore, retained

profit is another aspect which is generally kept aside for investment purpose. This proves to be

effective for corporation to expand business at international level. It enables management to

deliver good quality of services to large number of so that accordingly competitive edge of the

business can be created in the marketplace. Moreover, sale of old assets reflects that management

acquire internal source of fund in order to meet short term requirement of corporation in the

marketplace.

External sources

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

External sources of finance includes bank loan, issue of shares and leasing companies and

hire purchase etc. These sources can be acquired by corporation in order to increase flow of

production in the marketplace. Furthermore, issue of share is considered as the another important

aspect for raising the finance (Prorokowski, 2011). On the other hand, bank loan is also the

important source through which huge finance can be acquired for meeting the expansion related

requirement of Radisson plc. Moreover, leasing companies facilitates to provide highly equipped

assets for meeting requirement business in an effectual manner.

Assessing implication of sources of finance

The implication of different sources of finance can be understood effectively by focusing

upon its positive and negative aspects. It is because all sources of finance cannot be considered

as the same due to its higher cost and its direct impact of performance of business. Here,

management tend to focus upon both aspects so that accordingly well being company can be

ensured in the marketplace. For example, bank loan is granted only on the basis of collateral

securities and promise to pay off loan amount on right time (Vimpari, Kajander and Junnila,

2014). It would be effective for management maintain its credit rating in the marketplace. At this

juncture, they must pay off cost on right time along with payment of full installment on the basis

of agreed terms and conditions.

In addition to this, issue of equity share is another source of finance under which

company require to pay its dividend in case of profitability. However, in case business occur loss

then they are not required to pay return to the liable party. Furthermore, leasing companies

follow the long procedure for granting the loan which tend to affect rate of return of the business

to a great extent. Furthermore, sale of old assets tend might create chance of undervaluation of

the assets due to hurry. In this manner, Radisson plc must focus upon both positive and negative

aspect and then accordingly financial resources can be selected for its expansion project (Adams,

Litan and Pomerleano, 2010).

In addition to this, issue of equity share interfere the managerial decision to a great

extent. This happens because of dilution of control. For example, all shareholders are invited in

the board meeting so their views and suggestions can be incorporated in the decision making

process.

4

hire purchase etc. These sources can be acquired by corporation in order to increase flow of

production in the marketplace. Furthermore, issue of share is considered as the another important

aspect for raising the finance (Prorokowski, 2011). On the other hand, bank loan is also the

important source through which huge finance can be acquired for meeting the expansion related

requirement of Radisson plc. Moreover, leasing companies facilitates to provide highly equipped

assets for meeting requirement business in an effectual manner.

Assessing implication of sources of finance

The implication of different sources of finance can be understood effectively by focusing

upon its positive and negative aspects. It is because all sources of finance cannot be considered

as the same due to its higher cost and its direct impact of performance of business. Here,

management tend to focus upon both aspects so that accordingly well being company can be

ensured in the marketplace. For example, bank loan is granted only on the basis of collateral

securities and promise to pay off loan amount on right time (Vimpari, Kajander and Junnila,

2014). It would be effective for management maintain its credit rating in the marketplace. At this

juncture, they must pay off cost on right time along with payment of full installment on the basis

of agreed terms and conditions.

In addition to this, issue of equity share is another source of finance under which

company require to pay its dividend in case of profitability. However, in case business occur loss

then they are not required to pay return to the liable party. Furthermore, leasing companies

follow the long procedure for granting the loan which tend to affect rate of return of the business

to a great extent. Furthermore, sale of old assets tend might create chance of undervaluation of

the assets due to hurry. In this manner, Radisson plc must focus upon both positive and negative

aspect and then accordingly financial resources can be selected for its expansion project (Adams,

Litan and Pomerleano, 2010).

In addition to this, issue of equity share interfere the managerial decision to a great

extent. This happens because of dilution of control. For example, all shareholders are invited in

the board meeting so their views and suggestions can be incorporated in the decision making

process.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B. Evaluating the appropriate sources of finance for expansion plan of Radisson plc

Selection of appropriate source of finance is the most important task which assists

management to raise their capital and invest the same in a profitable project (Lapsley, Miller and

Panozzo, 2010). According to the given scenario, following suitable sources can be accessed by

management of Radisson plc. In this manner, appropriate sources of finance are listed as follows

which can effectively determine successful operation of business. Bank loan-It is also considered as the most appropriate source of finance as it provide

huge finance for expansion of business. This assists corporation to take loan on the basis

of agreed interest and amount of installment (Allen and Economy 2011). It supports

corporation to deliver good quality of services to large number of buyers as company

might be able to extent variety of its products and services also. Issue of share-Under this, management must raise their capital by issuing equity share.

This is considered as the most secured source of finance which facilitates Radisson plc to

expand the business. However, it incurs cost in term of dividend but proves to be

effective for long run success of company (Brotman, 2010).

Leasing companies-It provides equipment for reducing financial burden of the business.

However, assets requirement is the most important for starting the business of firm. In

this manner, Radisson plc can access leasing companies for expansion. However,

corporation can rely on leasing companies due to varied option provided for assets

development. In this manner, management of Radisson plc must go for this option for

expansion project. This facilitates to start the operation in a relatively less time span

(Heberle and Christensen, 2011).

TASK 2

A. Analysis and evaluation of cost of debt versus equity financing

Equity and debt funding are the two most common and often use sources of long-term

funds but have different costs associated with it. With the collection of money through issue of

further shares upto the maximum extent of authorized share capital, Radisson Plc will have to

bear the cost of dividend to provide some extra as a monetary return to their investors. Further,

company will also have to bear the cost of listing shares and printing charges which is the part of

5

Selection of appropriate source of finance is the most important task which assists

management to raise their capital and invest the same in a profitable project (Lapsley, Miller and

Panozzo, 2010). According to the given scenario, following suitable sources can be accessed by

management of Radisson plc. In this manner, appropriate sources of finance are listed as follows

which can effectively determine successful operation of business. Bank loan-It is also considered as the most appropriate source of finance as it provide

huge finance for expansion of business. This assists corporation to take loan on the basis

of agreed interest and amount of installment (Allen and Economy 2011). It supports

corporation to deliver good quality of services to large number of buyers as company

might be able to extent variety of its products and services also. Issue of share-Under this, management must raise their capital by issuing equity share.

This is considered as the most secured source of finance which facilitates Radisson plc to

expand the business. However, it incurs cost in term of dividend but proves to be

effective for long run success of company (Brotman, 2010).

Leasing companies-It provides equipment for reducing financial burden of the business.

However, assets requirement is the most important for starting the business of firm. In

this manner, Radisson plc can access leasing companies for expansion. However,

corporation can rely on leasing companies due to varied option provided for assets

development. In this manner, management of Radisson plc must go for this option for

expansion project. This facilitates to start the operation in a relatively less time span

(Heberle and Christensen, 2011).

TASK 2

A. Analysis and evaluation of cost of debt versus equity financing

Equity and debt funding are the two most common and often use sources of long-term

funds but have different costs associated with it. With the collection of money through issue of

further shares upto the maximum extent of authorized share capital, Radisson Plc will have to

bear the cost of dividend to provide some extra as a monetary return to their investors. Further,

company will also have to bear the cost of listing shares and printing charges which is the part of

5

its cost. But still, dividend is not a legal obligation to the firm hence, dividend decisions is taken

by the managers on the basis of their willingness to control operations and availability of residual

return (Coleman, Cotei and Farhat, 2016). However, raising money through borrowings makes it

mandatory for the Radisson Plc to discharge the borrowed fund along with the interest as cost.

Unlike equity, firm has to bear fixed burden and needs to pay interest as per the scheduled

payments and contract norms (Cost of debt, 2015). Further, collateral security also may needs to

keep to the financial institute to satisfy lender regarding fund safety. At the same time, UK

taxation body, HMRC provided deductions to the corporations to the extent of cost of debt

(interest) incurred results in lowering tax burden and maximize net yield (Florou and Kosi,

2015). Hence, it seems very clear that debt is considered appropriate and cheaper financial

source.

B. Significance of monetary planning and information need of decision-makers

The process of setting out a financial framework such as objectives, budget, policies and

procedures for the procurement, utilisation, supervision and controlling of the monetary business

activities and functions of Radisson Plc is called financial planning. It is extremely significant

for the firm due to below narrated reasons:

Financial planning greatly assists entrepreneurs to collect enough and adequate quantity

of funds for short, medium and long-term period. Moreover, funds also can be raised at

the time of establishment’s requirement through an excellent plan.

Through budgeting, Radisson Plc’s managers will be greatly able to maintain a right

balance between inflow and outflow, which in turn, result in long-run survival and

stability (Vyas and et.al., 2016).

In the competitive and dynamic era, establishments like Radisson Plc and others can

develop growth and expansion plans through designing a right financial plan.

Monetary planning in advance delivers assistance to resolve monetary challenges due to

changing market conditions and meet financial commitments successfully (Sabri and

et.al., 2015).

Another benefit of it is it enable entrepreneur to maintain surplus cash resources any

time, thus, Radisson Plc’s managers will not face difficulties due to cash shortage.

6

by the managers on the basis of their willingness to control operations and availability of residual

return (Coleman, Cotei and Farhat, 2016). However, raising money through borrowings makes it

mandatory for the Radisson Plc to discharge the borrowed fund along with the interest as cost.

Unlike equity, firm has to bear fixed burden and needs to pay interest as per the scheduled

payments and contract norms (Cost of debt, 2015). Further, collateral security also may needs to

keep to the financial institute to satisfy lender regarding fund safety. At the same time, UK

taxation body, HMRC provided deductions to the corporations to the extent of cost of debt

(interest) incurred results in lowering tax burden and maximize net yield (Florou and Kosi,

2015). Hence, it seems very clear that debt is considered appropriate and cheaper financial

source.

B. Significance of monetary planning and information need of decision-makers

The process of setting out a financial framework such as objectives, budget, policies and

procedures for the procurement, utilisation, supervision and controlling of the monetary business

activities and functions of Radisson Plc is called financial planning. It is extremely significant

for the firm due to below narrated reasons:

Financial planning greatly assists entrepreneurs to collect enough and adequate quantity

of funds for short, medium and long-term period. Moreover, funds also can be raised at

the time of establishment’s requirement through an excellent plan.

Through budgeting, Radisson Plc’s managers will be greatly able to maintain a right

balance between inflow and outflow, which in turn, result in long-run survival and

stability (Vyas and et.al., 2016).

In the competitive and dynamic era, establishments like Radisson Plc and others can

develop growth and expansion plans through designing a right financial plan.

Monetary planning in advance delivers assistance to resolve monetary challenges due to

changing market conditions and meet financial commitments successfully (Sabri and

et.al., 2015).

Another benefit of it is it enable entrepreneur to maintain surplus cash resources any

time, thus, Radisson Plc’s managers will not face difficulties due to cash shortage.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

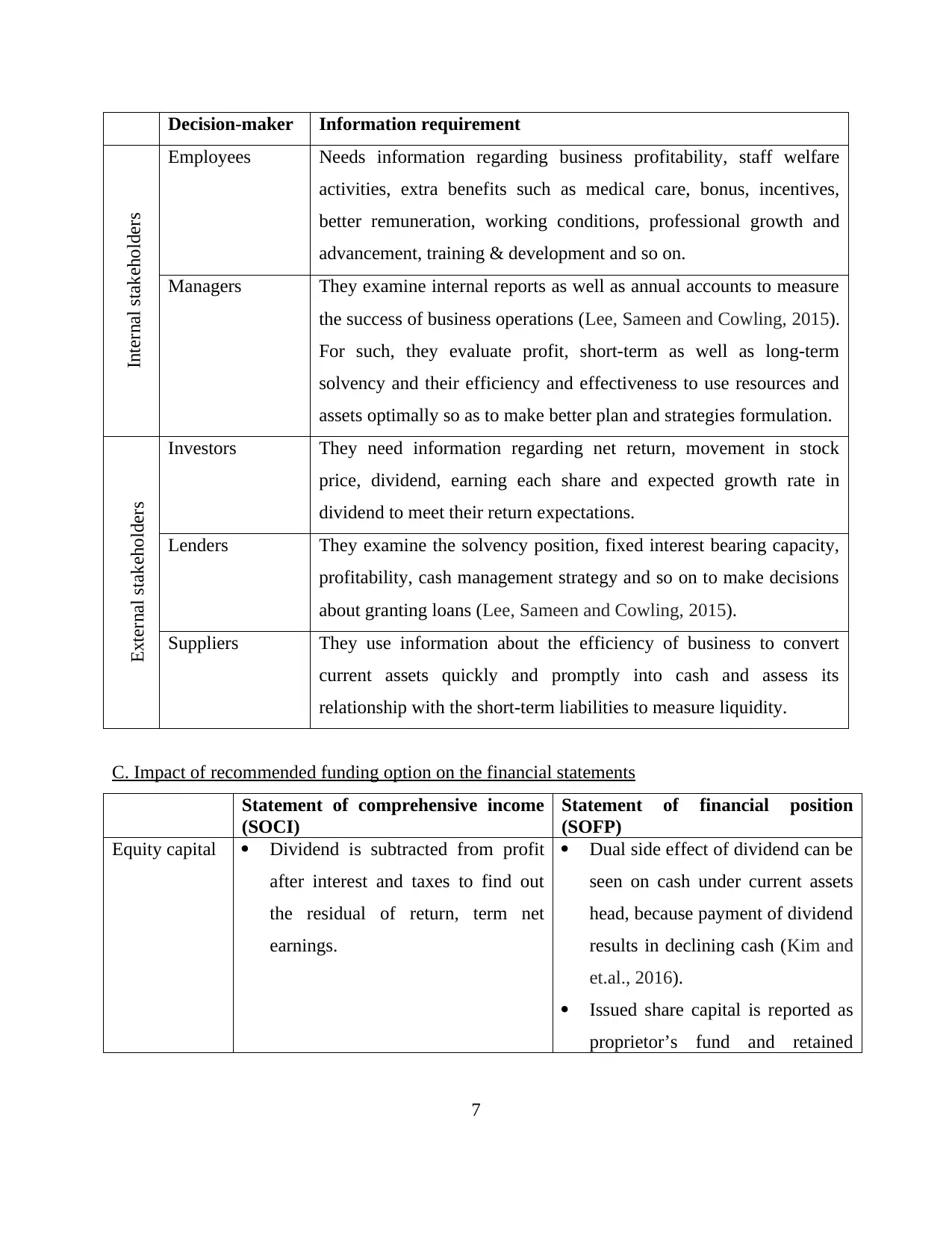

Decision-maker Information requirement

Internal stakeholders

Employees Needs information regarding business profitability, staff welfare

activities, extra benefits such as medical care, bonus, incentives,

better remuneration, working conditions, professional growth and

advancement, training & development and so on.

Managers They examine internal reports as well as annual accounts to measure

the success of business operations (Lee, Sameen and Cowling, 2015).

For such, they evaluate profit, short-term as well as long-term

solvency and their efficiency and effectiveness to use resources and

assets optimally so as to make better plan and strategies formulation.

External stakeholders

Investors They need information regarding net return, movement in stock

price, dividend, earning each share and expected growth rate in

dividend to meet their return expectations.

Lenders They examine the solvency position, fixed interest bearing capacity,

profitability, cash management strategy and so on to make decisions

about granting loans (Lee, Sameen and Cowling, 2015).

Suppliers They use information about the efficiency of business to convert

current assets quickly and promptly into cash and assess its

relationship with the short-term liabilities to measure liquidity.

C. Impact of recommended funding option on the financial statements

Statement of comprehensive income

(SOCI)

Statement of financial position

(SOFP)

Equity capital Dividend is subtracted from profit

after interest and taxes to find out

the residual of return, term net

earnings.

Dual side effect of dividend can be

seen on cash under current assets

head, because payment of dividend

results in declining cash (Kim and

et.al., 2016).

Issued share capital is reported as

proprietor’s fund and retained

7

Internal stakeholders

Employees Needs information regarding business profitability, staff welfare

activities, extra benefits such as medical care, bonus, incentives,

better remuneration, working conditions, professional growth and

advancement, training & development and so on.

Managers They examine internal reports as well as annual accounts to measure

the success of business operations (Lee, Sameen and Cowling, 2015).

For such, they evaluate profit, short-term as well as long-term

solvency and their efficiency and effectiveness to use resources and

assets optimally so as to make better plan and strategies formulation.

External stakeholders

Investors They need information regarding net return, movement in stock

price, dividend, earning each share and expected growth rate in

dividend to meet their return expectations.

Lenders They examine the solvency position, fixed interest bearing capacity,

profitability, cash management strategy and so on to make decisions

about granting loans (Lee, Sameen and Cowling, 2015).

Suppliers They use information about the efficiency of business to convert

current assets quickly and promptly into cash and assess its

relationship with the short-term liabilities to measure liquidity.

C. Impact of recommended funding option on the financial statements

Statement of comprehensive income

(SOCI)

Statement of financial position

(SOFP)

Equity capital Dividend is subtracted from profit

after interest and taxes to find out

the residual of return, term net

earnings.

Dual side effect of dividend can be

seen on cash under current assets

head, because payment of dividend

results in declining cash (Kim and

et.al., 2016).

Issued share capital is reported as

proprietor’s fund and retained

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

earnings are also a part of it.

Debt funding Interest expense is subtracted from

operating profit in P&L a/c

(Sources of funds, 2014).

Interest payment is deducted from

the cash/bank balance in SOFP.

Debt fund is the part of non-

current also called long-term

liabilities (Kim and et.al., 2016).

Money raised through external

borrowings maximize cash/bank

under the head current assets.

TASK 3

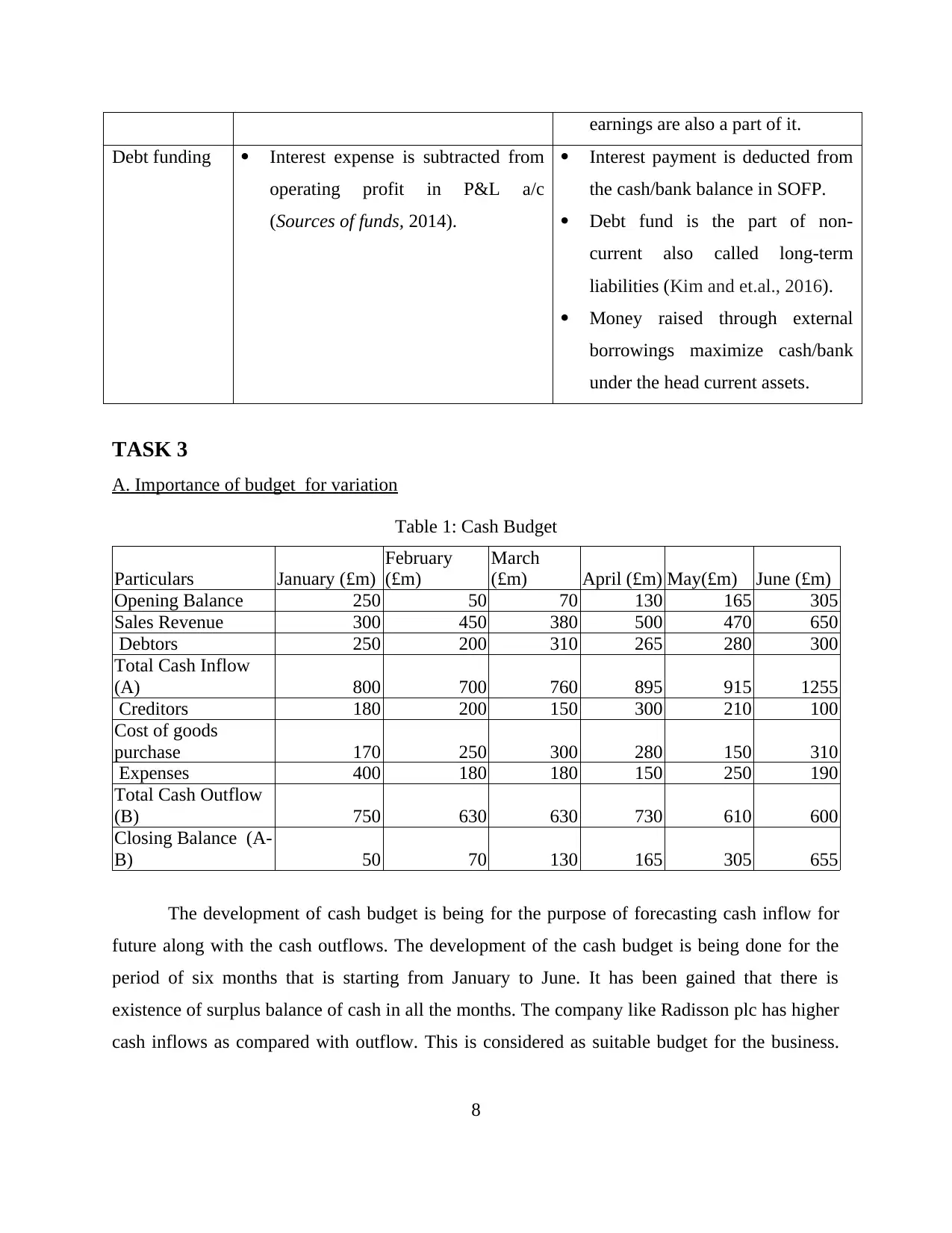

A. Importance of budget for variation

Table 1: Cash Budget

Particulars January (£m)

February

(£m)

March

(£m) April (£m) May(£m) June (£m)

Opening Balance 250 50 70 130 165 305

Sales Revenue 300 450 380 500 470 650

Debtors 250 200 310 265 280 300

Total Cash Inflow

(A) 800 700 760 895 915 1255

Creditors 180 200 150 300 210 100

Cost of goods

purchase 170 250 300 280 150 310

Expenses 400 180 180 150 250 190

Total Cash Outflow

(B) 750 630 630 730 610 600

Closing Balance (A-

B) 50 70 130 165 305 655

The development of cash budget is being for the purpose of forecasting cash inflow for

future along with the cash outflows. The development of the cash budget is being done for the

period of six months that is starting from January to June. It has been gained that there is

existence of surplus balance of cash in all the months. The company like Radisson plc has higher

cash inflows as compared with outflow. This is considered as suitable budget for the business.

8

Debt funding Interest expense is subtracted from

operating profit in P&L a/c

(Sources of funds, 2014).

Interest payment is deducted from

the cash/bank balance in SOFP.

Debt fund is the part of non-

current also called long-term

liabilities (Kim and et.al., 2016).

Money raised through external

borrowings maximize cash/bank

under the head current assets.

TASK 3

A. Importance of budget for variation

Table 1: Cash Budget

Particulars January (£m)

February

(£m)

March

(£m) April (£m) May(£m) June (£m)

Opening Balance 250 50 70 130 165 305

Sales Revenue 300 450 380 500 470 650

Debtors 250 200 310 265 280 300

Total Cash Inflow

(A) 800 700 760 895 915 1255

Creditors 180 200 150 300 210 100

Cost of goods

purchase 170 250 300 280 150 310

Expenses 400 180 180 150 250 190

Total Cash Outflow

(B) 750 630 630 730 610 600

Closing Balance (A-

B) 50 70 130 165 305 655

The development of cash budget is being for the purpose of forecasting cash inflow for

future along with the cash outflows. The development of the cash budget is being done for the

period of six months that is starting from January to June. It has been gained that there is

existence of surplus balance of cash in all the months. The company like Radisson plc has higher

cash inflows as compared with outflow. This is considered as suitable budget for the business.

8

Enhancement in the revenues demonstrates increase in the sales of the product. This results in

enhancement of the organizational potential towards fulfilling the expenses. The closing balance

of the firm is positive in all the months which reflects that company has sound financial position.

This has greater impact on the goodwill of the organization with greater effectiveness.

B. Calculating unit cost and making pricing decision

A unit cost can be defined as the total expenditure incurred by a company at the time of

producing the products, store it and sell it on the outlet. This calculates for only single unit of

service or products. It includes different costs such as fixed costs, overhead costs, variable costs,

direct and indirect labour and material costs, production costs etc. Unit cost identification is one

of the best methods to determine if companies are able to manufacture their commodities or not.

It has calculated by dividing the total cost with the number of units produced at the time of

production. Formula regarding calculating unit cost is as follows:

Total cost = Total fixed cost + Total variable cost

Unit cost = Total cost/ Number of units manufactured

In case of Radisson Plc, company has prepared 3000 units of medium-size computer

software which has included different costs such as direct material 40000, direct labour 55000,

Fixed cost 30000.

Thus the total cost is (40000+55000+30000) = 125000

Unit cost would be 125000/ 3000 = 41 pounds

55

Companies sell services and goods by setting of prices of them. This is one of the most

important decisions for management. Pricing decision for a commodity is based on cost plus

method. In this technique, organization, adding some level of percentage of margin of total cost.

The reason of doing this such thing because of earns some profit margin level. Pricing decision is

a profit planning exercise for the firms

In the case of Radisson Plc, organization has decided to keep 20% profit margin then

selling price will be

Selling price = 41+ (41*(20/100)) = 49

Thus Radisson Plc can plan to sell its medium-size computer software at 49 pounds

selling prices and this will cost of production.

9

enhancement of the organizational potential towards fulfilling the expenses. The closing balance

of the firm is positive in all the months which reflects that company has sound financial position.

This has greater impact on the goodwill of the organization with greater effectiveness.

B. Calculating unit cost and making pricing decision

A unit cost can be defined as the total expenditure incurred by a company at the time of

producing the products, store it and sell it on the outlet. This calculates for only single unit of

service or products. It includes different costs such as fixed costs, overhead costs, variable costs,

direct and indirect labour and material costs, production costs etc. Unit cost identification is one

of the best methods to determine if companies are able to manufacture their commodities or not.

It has calculated by dividing the total cost with the number of units produced at the time of

production. Formula regarding calculating unit cost is as follows:

Total cost = Total fixed cost + Total variable cost

Unit cost = Total cost/ Number of units manufactured

In case of Radisson Plc, company has prepared 3000 units of medium-size computer

software which has included different costs such as direct material 40000, direct labour 55000,

Fixed cost 30000.

Thus the total cost is (40000+55000+30000) = 125000

Unit cost would be 125000/ 3000 = 41 pounds

55

Companies sell services and goods by setting of prices of them. This is one of the most

important decisions for management. Pricing decision for a commodity is based on cost plus

method. In this technique, organization, adding some level of percentage of margin of total cost.

The reason of doing this such thing because of earns some profit margin level. Pricing decision is

a profit planning exercise for the firms

In the case of Radisson Plc, organization has decided to keep 20% profit margin then

selling price will be

Selling price = 41+ (41*(20/100)) = 49

Thus Radisson Plc can plan to sell its medium-size computer software at 49 pounds

selling prices and this will cost of production.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

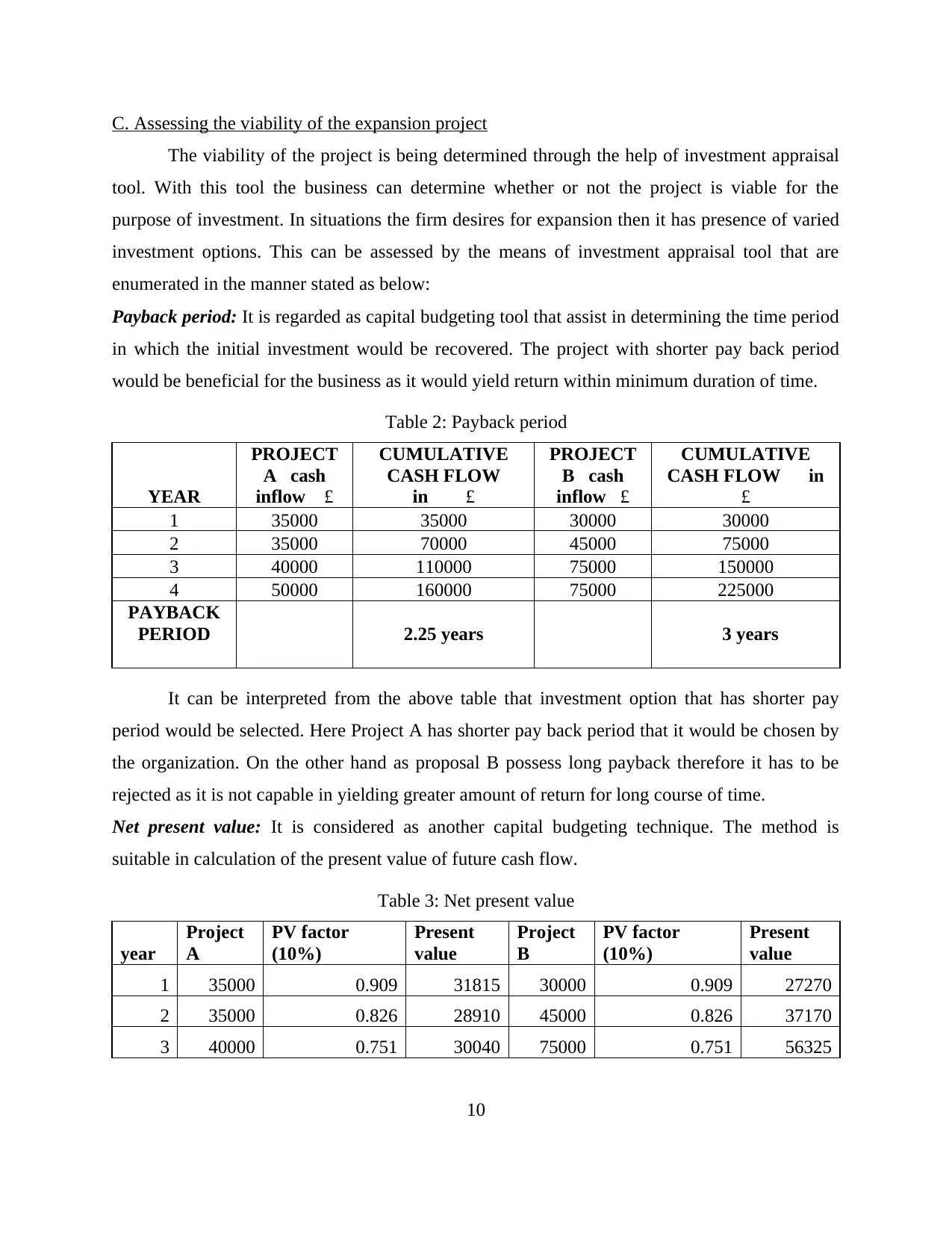

C. Assessing the viability of the expansion project

The viability of the project is being determined through the help of investment appraisal

tool. With this tool the business can determine whether or not the project is viable for the

purpose of investment. In situations the firm desires for expansion then it has presence of varied

investment options. This can be assessed by the means of investment appraisal tool that are

enumerated in the manner stated as below:

Payback period: It is regarded as capital budgeting tool that assist in determining the time period

in which the initial investment would be recovered. The project with shorter pay back period

would be beneficial for the business as it would yield return within minimum duration of time.

Table 2: Payback period

YEAR

PROJECT

A cash

inflow £

CUMULATIVE

CASH FLOW

in £

PROJECT

B cash

inflow £

CUMULATIVE

CASH FLOW in

£

1 35000 35000 30000 30000

2 35000 70000 45000 75000

3 40000 110000 75000 150000

4 50000 160000 75000 225000

PAYBACK

PERIOD 2.25 years 3 years

It can be interpreted from the above table that investment option that has shorter pay

period would be selected. Here Project A has shorter pay back period that it would be chosen by

the organization. On the other hand as proposal B possess long payback therefore it has to be

rejected as it is not capable in yielding greater amount of return for long course of time.

Net present value: It is considered as another capital budgeting technique. The method is

suitable in calculation of the present value of future cash flow.

Table 3: Net present value

year

Project

A

PV factor

(10%)

Present

value

Project

B

PV factor

(10%)

Present

value

1 35000 0.909 31815 30000 0.909 27270

2 35000 0.826 28910 45000 0.826 37170

3 40000 0.751 30040 75000 0.751 56325

10

The viability of the project is being determined through the help of investment appraisal

tool. With this tool the business can determine whether or not the project is viable for the

purpose of investment. In situations the firm desires for expansion then it has presence of varied

investment options. This can be assessed by the means of investment appraisal tool that are

enumerated in the manner stated as below:

Payback period: It is regarded as capital budgeting tool that assist in determining the time period

in which the initial investment would be recovered. The project with shorter pay back period

would be beneficial for the business as it would yield return within minimum duration of time.

Table 2: Payback period

YEAR

PROJECT

A cash

inflow £

CUMULATIVE

CASH FLOW

in £

PROJECT

B cash

inflow £

CUMULATIVE

CASH FLOW in

£

1 35000 35000 30000 30000

2 35000 70000 45000 75000

3 40000 110000 75000 150000

4 50000 160000 75000 225000

PAYBACK

PERIOD 2.25 years 3 years

It can be interpreted from the above table that investment option that has shorter pay

period would be selected. Here Project A has shorter pay back period that it would be chosen by

the organization. On the other hand as proposal B possess long payback therefore it has to be

rejected as it is not capable in yielding greater amount of return for long course of time.

Net present value: It is considered as another capital budgeting technique. The method is

suitable in calculation of the present value of future cash flow.

Table 3: Net present value

year

Project

A

PV factor

(10%)

Present

value

Project

B

PV factor

(10%)

Present

value

1 35000 0.909 31815 30000 0.909 27270

2 35000 0.826 28910 45000 0.826 37170

3 40000 0.751 30040 75000 0.751 56325

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

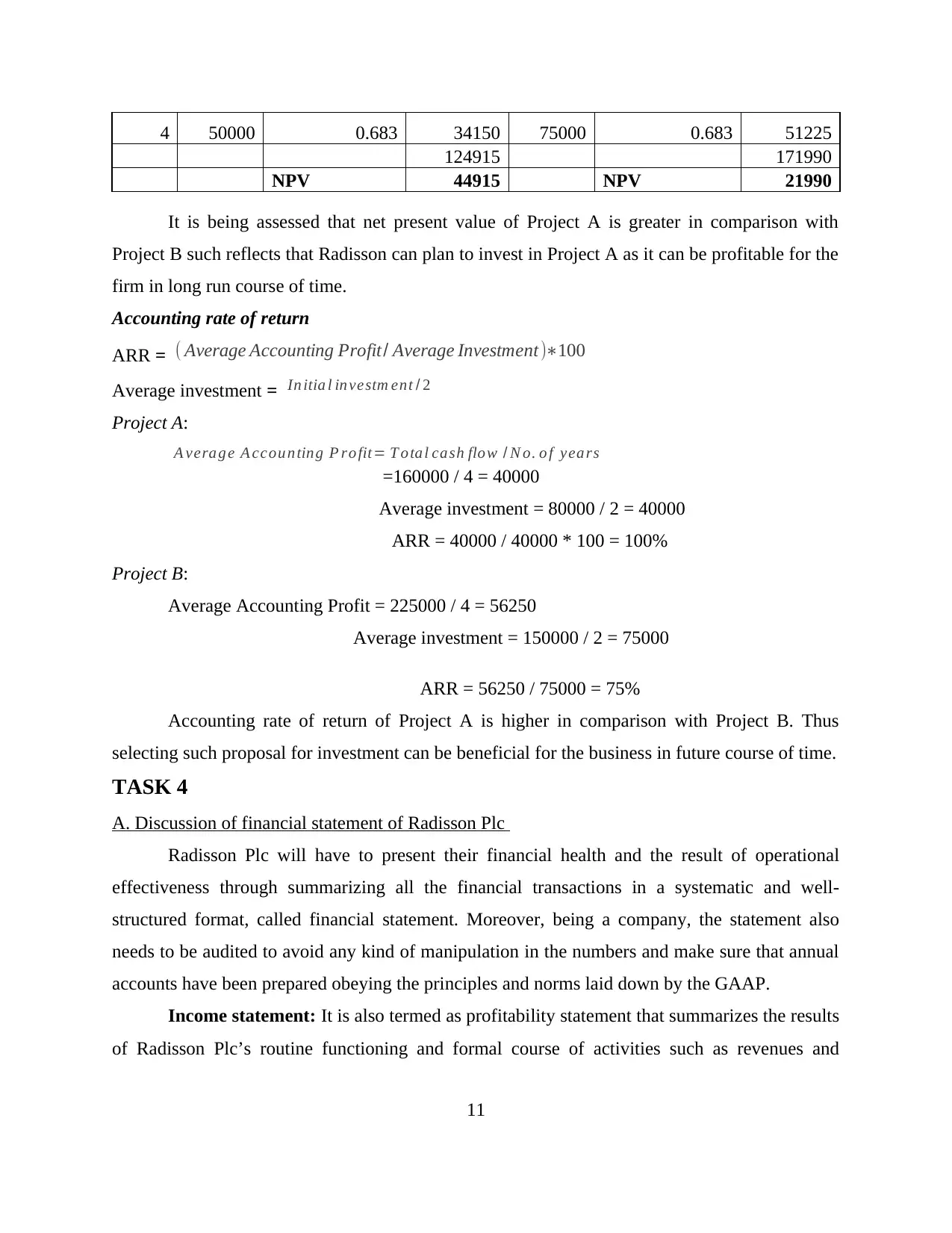

4 50000 0.683 34150 75000 0.683 51225

124915 171990

NPV 44915 NPV 21990

It is being assessed that net present value of Project A is greater in comparison with

Project B such reflects that Radisson can plan to invest in Project A as it can be profitable for the

firm in long run course of time.

Accounting rate of return

ARR = ( Average Accounting Profit/ Average Investment )∗100

Average investment = In itia l in vestm ent / 2

Project A:

A vera ge A ccoun ting P ro fit= T o tal cash flow / N o. o f yea rs

=160000 / 4 = 40000

Average investment = 80000 / 2 = 40000

ARR = 40000 / 40000 * 100 = 100%

Project B:

Average Accounting Profit = 225000 / 4 = 56250

Average investment = 150000 / 2 = 75000

ARR = 56250 / 75000 = 75%

Accounting rate of return of Project A is higher in comparison with Project B. Thus

selecting such proposal for investment can be beneficial for the business in future course of time.

TASK 4

A. Discussion of financial statement of Radisson Plc

Radisson Plc will have to present their financial health and the result of operational

effectiveness through summarizing all the financial transactions in a systematic and well-

structured format, called financial statement. Moreover, being a company, the statement also

needs to be audited to avoid any kind of manipulation in the numbers and make sure that annual

accounts have been prepared obeying the principles and norms laid down by the GAAP.

Income statement: It is also termed as profitability statement that summarizes the results

of Radisson Plc’s routine functioning and formal course of activities such as revenues and

11

124915 171990

NPV 44915 NPV 21990

It is being assessed that net present value of Project A is greater in comparison with

Project B such reflects that Radisson can plan to invest in Project A as it can be profitable for the

firm in long run course of time.

Accounting rate of return

ARR = ( Average Accounting Profit/ Average Investment )∗100

Average investment = In itia l in vestm ent / 2

Project A:

A vera ge A ccoun ting P ro fit= T o tal cash flow / N o. o f yea rs

=160000 / 4 = 40000

Average investment = 80000 / 2 = 40000

ARR = 40000 / 40000 * 100 = 100%

Project B:

Average Accounting Profit = 225000 / 4 = 56250

Average investment = 150000 / 2 = 75000

ARR = 56250 / 75000 = 75%

Accounting rate of return of Project A is higher in comparison with Project B. Thus

selecting such proposal for investment can be beneficial for the business in future course of time.

TASK 4

A. Discussion of financial statement of Radisson Plc

Radisson Plc will have to present their financial health and the result of operational

effectiveness through summarizing all the financial transactions in a systematic and well-

structured format, called financial statement. Moreover, being a company, the statement also

needs to be audited to avoid any kind of manipulation in the numbers and make sure that annual

accounts have been prepared obeying the principles and norms laid down by the GAAP.

Income statement: It is also termed as profitability statement that summarizes the results

of Radisson Plc’s routine functioning and formal course of activities such as revenues and

11

expenditures (Kim and et.al., 2016). This statement use following accounting equation to

measure or ascertain net results, mentioned below:

Net income/earnings = Revenue/Income – Expenditures/Cost incurred

Revenue comprises all those elements which drive earnings or inflow to the Radisson Plc

whilst opposed to this, spending refers to the outgoing or outflow like administrative cost, selling

and distribution expense, research cost and so on. It follows accrual accounting principle which

records all the transactions when incurred rather than at the time of actual cash outgoing and

incoming.

Balance sheet: Unlike P&L, this statement gives an insight to the financial health or

position at a particular date follows the mentioned equation:

Shareholders equity / Proprietor’s fund = Total assets – total liabilities

Assets classified into current and fixed assets, whereas liabilities are divided into current

and non-current liabilities (Vyas and et.al., 2016). All those monetary items which will drive

cash inflow to the firm within twelve month period, called current assets, whilst those which will

result in cash outflow is regarded as current liabilities. On the other side, assets which is utilised

by Radisson Plc for a very long period, is called fixed assets like plant & machinery, building

etc. whilst liabilities that company has to pay after a long-term period is termed as

non-current/long-term obligations.

Cash flow statement: In accordance with the IAS 7, this statement follows cash

accounting principles to reports about inflow and outflow of cash & its equivalent (Malik, Awais

and Khursheed, 2016). Under the operational activities, it considers routine functioning,

financing activities report about change in long-term financial sources like debt & equity whilst

investing activities records sources of cash through disposal of fixed assets whereas outflow will

be the result of purchase of long-term equipment & assets.

B. Comparison of financial statement of two companies

Partnership Company (Radisson Plc)

Accounts Profit and loss account

Profit and loss appropriation a/c

Partner’s capital a/c

Partner’s current a/c

Statement of income statement

Balance sheet

Cash flow statement

Fund flow statement

12

measure or ascertain net results, mentioned below:

Net income/earnings = Revenue/Income – Expenditures/Cost incurred

Revenue comprises all those elements which drive earnings or inflow to the Radisson Plc

whilst opposed to this, spending refers to the outgoing or outflow like administrative cost, selling

and distribution expense, research cost and so on. It follows accrual accounting principle which

records all the transactions when incurred rather than at the time of actual cash outgoing and

incoming.

Balance sheet: Unlike P&L, this statement gives an insight to the financial health or

position at a particular date follows the mentioned equation:

Shareholders equity / Proprietor’s fund = Total assets – total liabilities

Assets classified into current and fixed assets, whereas liabilities are divided into current

and non-current liabilities (Vyas and et.al., 2016). All those monetary items which will drive

cash inflow to the firm within twelve month period, called current assets, whilst those which will

result in cash outflow is regarded as current liabilities. On the other side, assets which is utilised

by Radisson Plc for a very long period, is called fixed assets like plant & machinery, building

etc. whilst liabilities that company has to pay after a long-term period is termed as

non-current/long-term obligations.

Cash flow statement: In accordance with the IAS 7, this statement follows cash

accounting principles to reports about inflow and outflow of cash & its equivalent (Malik, Awais

and Khursheed, 2016). Under the operational activities, it considers routine functioning,

financing activities report about change in long-term financial sources like debt & equity whilst

investing activities records sources of cash through disposal of fixed assets whereas outflow will

be the result of purchase of long-term equipment & assets.

B. Comparison of financial statement of two companies

Partnership Company (Radisson Plc)

Accounts Profit and loss account

Profit and loss appropriation a/c

Partner’s capital a/c

Partner’s current a/c

Statement of income statement

Balance sheet

Cash flow statement

Fund flow statement

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.