Financial Resource Management and Investment Decisions Report

VerifiedAdded on 2019/12/03

|20

|8190

|151

Report

AI Summary

This report provides a comprehensive analysis of financial resource management and investment appraisal techniques, focusing on a case study of Taste Plc, a medium-sized catering business. It identifies various sources of finance, including trade credit, bank overdrafts, retained earnings, bank loans, issuing shares, and leasing, along with their respective advantages and disadvantages. The report compares and contrasts right issues of shares and loan notes, discussing their implications on the company's financial structure and control. It evaluates the appropriateness of different financing sources for acquiring buildings and non-current assets, recommending the issuance of equity shares. Furthermore, the report delves into working capital management, the interpretation of financial statements, including profit and loss, financial position, and cash flow statements, and the application of investment appraisal techniques like payback period and net present value. It also examines the relationship between cash flow and profit, emphasizing the importance of financial planning and the needs of financial statement users. Finally, the report concludes with an overall opinion on the company's current performance and recommendations for future financial strategies.

Managing financial

resources

and Decisions

1

resources

and Decisions

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

2.0 Identifying sources of finance available to business............................................................4

2.1 Types of business..................................................................................................................4

2.2 Sources of finance available to business...............................................................................4

The table consists of following sources of finance along with advantages and disadvantages-.4

2.3 Compare and contrast right issue of share and loan notes....................................................6

2.3.3 Implication of right issues and loan stock..........................................................................7

2.4 Appropriateness of source of finance for buildings and NCA............................................7

2.5 Working capital- Advising board of directors on a source of finance..................................8

2.5.1 Definition...........................................................................................................................8

2.5.2 Importance of working capital...........................................................................................8

2.5.3 Sources available for WC...................................................................................................9

3.1 Statement of profit and loss................................................................................................10

3.2 Statement of financial position...........................................................................................10

3.3 Statement of cash flow........................................................................................................10

3.4.1 WACC for each three options..........................................................................................10

3.4.2 Gearing for each three option...........................................................................................11

3.4.3 How did it impact financial statements............................................................................11

3.5 Earning per share................................................................................................................12

3.5.1 what information does this provides................................................................................12

3.5.2 Earning per share calculation..........................................................................................12

3.5.3 Explaining the answer......................................................................................................12

4 Investment appraisal..............................................................................................................13

4.1 Why it is important to appraise potential investment..........................................................13

4.2 What are the risks to future cash flow?...............................................................................13

4.3 Different type of techniques................................................................................................13

4.3.2 Calculating pay back period.............................................................................................13

4.3.3 net present value method of appraisal.............................................................................14

4.3.4 Calculation of net present value.......................................................................................14

4.4 Recommending board of directors......................................................................................15

4.5 Unit cost..............................................................................................................................16

5.0 Cash flow vs profit..............................................................................................................17

5.1 Main trends and messages contained within cash flow......................................................17

5.2 Importance of financial planning........................................................................................17

5.3 Explain why company may be profitable but run into liquidity problem..........................17

5.4 Users of financial statements and their needs....................................................................17

5.4.2 What information they need.............................................................................................18

6.0 Interpretation of the financial statements.....................................................................................18

6.1 Ratio Analysis.....................................................................................................................18

6.1.1 Profitability ratios............................................................................................................18

6.1.2 Liquidity ratio..................................................................................................................19

6.2 Overall opinion on the company’s current performance.....................................................19

7.0 Main difference in financial statements........................................................................................19

CONCLUSION..................................................................................................................................19

REFERENCES...................................................................................................................................21

2

INTRODUCTION................................................................................................................................4

2.0 Identifying sources of finance available to business............................................................4

2.1 Types of business..................................................................................................................4

2.2 Sources of finance available to business...............................................................................4

The table consists of following sources of finance along with advantages and disadvantages-.4

2.3 Compare and contrast right issue of share and loan notes....................................................6

2.3.3 Implication of right issues and loan stock..........................................................................7

2.4 Appropriateness of source of finance for buildings and NCA............................................7

2.5 Working capital- Advising board of directors on a source of finance..................................8

2.5.1 Definition...........................................................................................................................8

2.5.2 Importance of working capital...........................................................................................8

2.5.3 Sources available for WC...................................................................................................9

3.1 Statement of profit and loss................................................................................................10

3.2 Statement of financial position...........................................................................................10

3.3 Statement of cash flow........................................................................................................10

3.4.1 WACC for each three options..........................................................................................10

3.4.2 Gearing for each three option...........................................................................................11

3.4.3 How did it impact financial statements............................................................................11

3.5 Earning per share................................................................................................................12

3.5.1 what information does this provides................................................................................12

3.5.2 Earning per share calculation..........................................................................................12

3.5.3 Explaining the answer......................................................................................................12

4 Investment appraisal..............................................................................................................13

4.1 Why it is important to appraise potential investment..........................................................13

4.2 What are the risks to future cash flow?...............................................................................13

4.3 Different type of techniques................................................................................................13

4.3.2 Calculating pay back period.............................................................................................13

4.3.3 net present value method of appraisal.............................................................................14

4.3.4 Calculation of net present value.......................................................................................14

4.4 Recommending board of directors......................................................................................15

4.5 Unit cost..............................................................................................................................16

5.0 Cash flow vs profit..............................................................................................................17

5.1 Main trends and messages contained within cash flow......................................................17

5.2 Importance of financial planning........................................................................................17

5.3 Explain why company may be profitable but run into liquidity problem..........................17

5.4 Users of financial statements and their needs....................................................................17

5.4.2 What information they need.............................................................................................18

6.0 Interpretation of the financial statements.....................................................................................18

6.1 Ratio Analysis.....................................................................................................................18

6.1.1 Profitability ratios............................................................................................................18

6.1.2 Liquidity ratio..................................................................................................................19

6.2 Overall opinion on the company’s current performance.....................................................19

7.0 Main difference in financial statements........................................................................................19

CONCLUSION..................................................................................................................................19

REFERENCES...................................................................................................................................21

2

INTRODUCTION

Finance is regarded as one of the most crucial resource of the enterprise as it is directly

associated with the aims and objectives of organization. Further, initiatives are taken by

management of every company so that it is possible to deal with unfavourable situations such as

inadequacy of finance etc. Proper management of financial resources provides base to organization

in gaining competitive advantage and in turn acts as development tool. Moreover, different sources

of finance are available to business with the help of which company can satisfy its requirement. IT

is the first and foremost duty of management to decide which source to adopt for raising funds such

as internal or external one (Wahlen and et.al., 2011).

Apart from this to judge the feasibility of project investment appraisal techniques are

effective which involves net present value, internal rate of return etc. Such methods helps in

selecting the appropriate proposal and in turn funds can be allocated accordingly. For carrying out

the present study organization chosen is Taste which is a medium sized company and at present

management wants to expand its catering business which has been growing over the past six years.

Apart from this, the local authority has granted business planning permission to extend its current

premises. Various tasks have been covered in the report which involves sources of finance,

importance of financial planning, investment appraisal techniques etc.

2.0 Identifying sources of finance available to business

2.1 Types of business

There are different types of businesses such as public, private and partnership etc. which

carry out their businesses effectively in order to produce good quality of products and services. All

of these businesses have different requirement in conducting their business and completing all

business activities. However, it is highly depend on management that what kind of sources are

preferred to satisfy their business purpose.

2.2 Sources of finance available to business

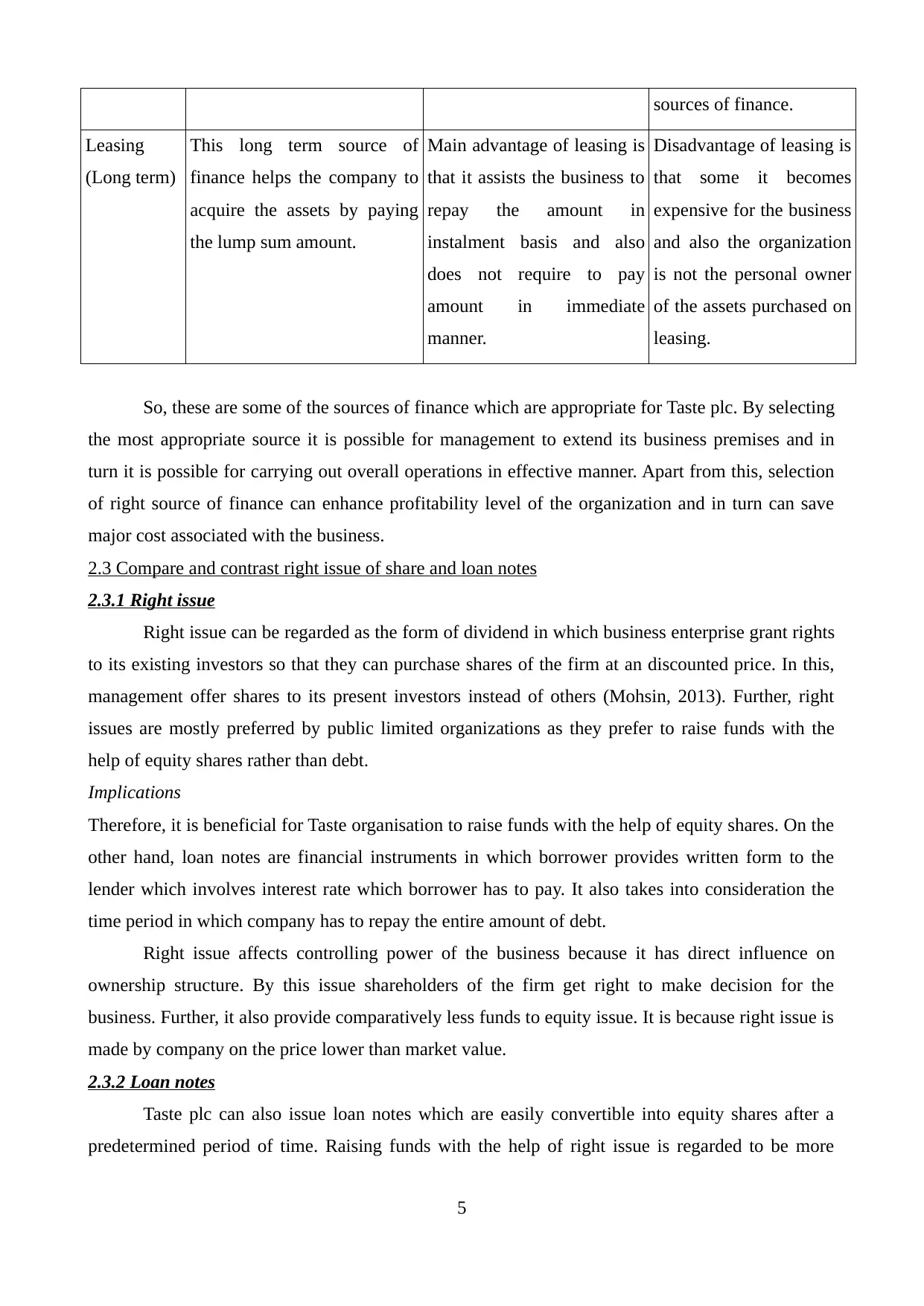

The table consists of following sources of finance along with advantages and disadvantages-

Sources Feature Advantage Disadvantage

Trade credit

(Short term)

It is considered as one of the

most effective practice of

vendors which allows

business to place and receive

orders without giving

immediate payment.

Main advantage of adopting

this source is minimal cash

outlay through which

shelves of business can be

stocked. Discount received

on the payment made within

Main disadvantage of

adopting this source is

fess and penalties when

supplier has right to

impose penalty on the late

payment made by

3

Finance is regarded as one of the most crucial resource of the enterprise as it is directly

associated with the aims and objectives of organization. Further, initiatives are taken by

management of every company so that it is possible to deal with unfavourable situations such as

inadequacy of finance etc. Proper management of financial resources provides base to organization

in gaining competitive advantage and in turn acts as development tool. Moreover, different sources

of finance are available to business with the help of which company can satisfy its requirement. IT

is the first and foremost duty of management to decide which source to adopt for raising funds such

as internal or external one (Wahlen and et.al., 2011).

Apart from this to judge the feasibility of project investment appraisal techniques are

effective which involves net present value, internal rate of return etc. Such methods helps in

selecting the appropriate proposal and in turn funds can be allocated accordingly. For carrying out

the present study organization chosen is Taste which is a medium sized company and at present

management wants to expand its catering business which has been growing over the past six years.

Apart from this, the local authority has granted business planning permission to extend its current

premises. Various tasks have been covered in the report which involves sources of finance,

importance of financial planning, investment appraisal techniques etc.

2.0 Identifying sources of finance available to business

2.1 Types of business

There are different types of businesses such as public, private and partnership etc. which

carry out their businesses effectively in order to produce good quality of products and services. All

of these businesses have different requirement in conducting their business and completing all

business activities. However, it is highly depend on management that what kind of sources are

preferred to satisfy their business purpose.

2.2 Sources of finance available to business

The table consists of following sources of finance along with advantages and disadvantages-

Sources Feature Advantage Disadvantage

Trade credit

(Short term)

It is considered as one of the

most effective practice of

vendors which allows

business to place and receive

orders without giving

immediate payment.

Main advantage of adopting

this source is minimal cash

outlay through which

shelves of business can be

stocked. Discount received

on the payment made within

Main disadvantage of

adopting this source is

fess and penalties when

supplier has right to

impose penalty on the late

payment made by

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

certain number of days is

also another benefit

(Mumford, Schultz and

Osburn, 2001)

company.

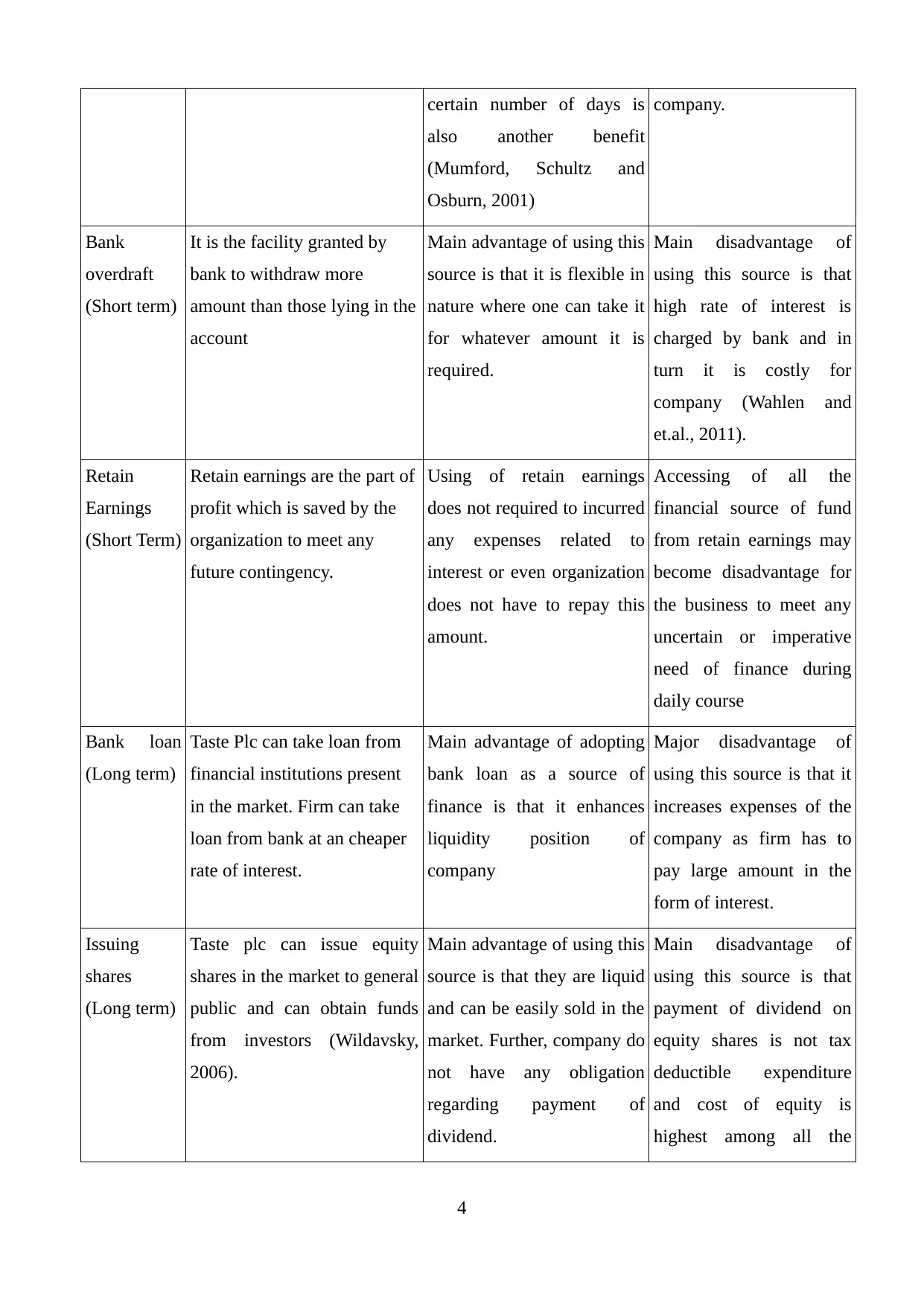

Bank

overdraft

(Short term)

It is the facility granted by

bank to withdraw more

amount than those lying in the

account

Main advantage of using this

source is that it is flexible in

nature where one can take it

for whatever amount it is

required.

Main disadvantage of

using this source is that

high rate of interest is

charged by bank and in

turn it is costly for

company (Wahlen and

et.al., 2011).

Retain

Earnings

(Short Term)

Retain earnings are the part of

profit which is saved by the

organization to meet any

future contingency.

Using of retain earnings

does not required to incurred

any expenses related to

interest or even organization

does not have to repay this

amount.

Accessing of all the

financial source of fund

from retain earnings may

become disadvantage for

the business to meet any

uncertain or imperative

need of finance during

daily course

Bank loan

(Long term)

Taste Plc can take loan from

financial institutions present

in the market. Firm can take

loan from bank at an cheaper

rate of interest.

Main advantage of adopting

bank loan as a source of

finance is that it enhances

liquidity position of

company

Major disadvantage of

using this source is that it

increases expenses of the

company as firm has to

pay large amount in the

form of interest.

Issuing

shares

(Long term)

Taste plc can issue equity

shares in the market to general

public and can obtain funds

from investors (Wildavsky,

2006).

Main advantage of using this

source is that they are liquid

and can be easily sold in the

market. Further, company do

not have any obligation

regarding payment of

dividend.

Main disadvantage of

using this source is that

payment of dividend on

equity shares is not tax

deductible expenditure

and cost of equity is

highest among all the

4

also another benefit

(Mumford, Schultz and

Osburn, 2001)

company.

Bank

overdraft

(Short term)

It is the facility granted by

bank to withdraw more

amount than those lying in the

account

Main advantage of using this

source is that it is flexible in

nature where one can take it

for whatever amount it is

required.

Main disadvantage of

using this source is that

high rate of interest is

charged by bank and in

turn it is costly for

company (Wahlen and

et.al., 2011).

Retain

Earnings

(Short Term)

Retain earnings are the part of

profit which is saved by the

organization to meet any

future contingency.

Using of retain earnings

does not required to incurred

any expenses related to

interest or even organization

does not have to repay this

amount.

Accessing of all the

financial source of fund

from retain earnings may

become disadvantage for

the business to meet any

uncertain or imperative

need of finance during

daily course

Bank loan

(Long term)

Taste Plc can take loan from

financial institutions present

in the market. Firm can take

loan from bank at an cheaper

rate of interest.

Main advantage of adopting

bank loan as a source of

finance is that it enhances

liquidity position of

company

Major disadvantage of

using this source is that it

increases expenses of the

company as firm has to

pay large amount in the

form of interest.

Issuing

shares

(Long term)

Taste plc can issue equity

shares in the market to general

public and can obtain funds

from investors (Wildavsky,

2006).

Main advantage of using this

source is that they are liquid

and can be easily sold in the

market. Further, company do

not have any obligation

regarding payment of

dividend.

Main disadvantage of

using this source is that

payment of dividend on

equity shares is not tax

deductible expenditure

and cost of equity is

highest among all the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sources of finance.

Leasing

(Long term)

This long term source of

finance helps the company to

acquire the assets by paying

the lump sum amount.

Main advantage of leasing is

that it assists the business to

repay the amount in

instalment basis and also

does not require to pay

amount in immediate

manner.

Disadvantage of leasing is

that some it becomes

expensive for the business

and also the organization

is not the personal owner

of the assets purchased on

leasing.

So, these are some of the sources of finance which are appropriate for Taste plc. By selecting

the most appropriate source it is possible for management to extend its business premises and in

turn it is possible for carrying out overall operations in effective manner. Apart from this, selection

of right source of finance can enhance profitability level of the organization and in turn can save

major cost associated with the business.

2.3 Compare and contrast right issue of share and loan notes

2.3.1 Right issue

Right issue can be regarded as the form of dividend in which business enterprise grant rights

to its existing investors so that they can purchase shares of the firm at an discounted price. In this,

management offer shares to its present investors instead of others (Mohsin, 2013). Further, right

issues are mostly preferred by public limited organizations as they prefer to raise funds with the

help of equity shares rather than debt.

Implications

Therefore, it is beneficial for Taste organisation to raise funds with the help of equity shares. On the

other hand, loan notes are financial instruments in which borrower provides written form to the

lender which involves interest rate which borrower has to pay. It also takes into consideration the

time period in which company has to repay the entire amount of debt.

Right issue affects controlling power of the business because it has direct influence on

ownership structure. By this issue shareholders of the firm get right to make decision for the

business. Further, it also provide comparatively less funds to equity issue. It is because right issue is

made by company on the price lower than market value.

2.3.2 Loan notes

Taste plc can also issue loan notes which are easily convertible into equity shares after a

predetermined period of time. Raising funds with the help of right issue is regarded to be more

5

Leasing

(Long term)

This long term source of

finance helps the company to

acquire the assets by paying

the lump sum amount.

Main advantage of leasing is

that it assists the business to

repay the amount in

instalment basis and also

does not require to pay

amount in immediate

manner.

Disadvantage of leasing is

that some it becomes

expensive for the business

and also the organization

is not the personal owner

of the assets purchased on

leasing.

So, these are some of the sources of finance which are appropriate for Taste plc. By selecting

the most appropriate source it is possible for management to extend its business premises and in

turn it is possible for carrying out overall operations in effective manner. Apart from this, selection

of right source of finance can enhance profitability level of the organization and in turn can save

major cost associated with the business.

2.3 Compare and contrast right issue of share and loan notes

2.3.1 Right issue

Right issue can be regarded as the form of dividend in which business enterprise grant rights

to its existing investors so that they can purchase shares of the firm at an discounted price. In this,

management offer shares to its present investors instead of others (Mohsin, 2013). Further, right

issues are mostly preferred by public limited organizations as they prefer to raise funds with the

help of equity shares rather than debt.

Implications

Therefore, it is beneficial for Taste organisation to raise funds with the help of equity shares. On the

other hand, loan notes are financial instruments in which borrower provides written form to the

lender which involves interest rate which borrower has to pay. It also takes into consideration the

time period in which company has to repay the entire amount of debt.

Right issue affects controlling power of the business because it has direct influence on

ownership structure. By this issue shareholders of the firm get right to make decision for the

business. Further, it also provide comparatively less funds to equity issue. It is because right issue is

made by company on the price lower than market value.

2.3.2 Loan notes

Taste plc can also issue loan notes which are easily convertible into equity shares after a

predetermined period of time. Raising funds with the help of right issue is regarded to be more

5

effective for Taste plc as compared with debt issue. In case when business enterprise satisfies its

financial needs with the help of existing shareholders then it is not required by firm to incur extra

expenses for attracting them (Mumford, Schultz and Osburn, 2001).

Implications

Apart from this, Taste plc is having sound financial position and therefore it is easy for

enterprise to attract existing investors in short period of time. Business entity can satisfy its

financial needs with the help of debt issue. In case when loan notes are issued then management has

to pay interest to its holders after regular interval (Jury, 2012) . Moreover, as compared with equity

sources, raising finance with the help of loan notes imposes high cost in front of company. For loan

notes company has to provide security in against of loan. For this financial source company has to

pay interest cost in regular time period. In addition to this organization has liability to repay the

principle amount as per the described contract. This source does not affect controlling power of the

business.

2.3.3 Implication of right issues and loan stock

The implication of right issues can be understood in term of cost and time take to issue of

shares. Also, management need to pay the dividend on right time so as to determine long run

success of the firm with increased rate of return. Furthermore, loan is the another imperative aspect

of finance which take high interest rate on loan. Accordingly, corporation need to pay cost on right

otherwise credit rating of organization get affected.

2.4 Appropriateness of source of finance for buildings and NCA

Equity finance

Advantages

On the other hand main advantage of equity financing is that it enables company to have

more cash in hand, it is less risky as compared with loan. The right business angels and venture

capitalist can bring value and they can explore growth ideas. Further, investors are often prepared to

provide follow up funding as business expands. All these are main benefits of employing equity

financing and is beneficial for the business.

Disadvantage

Further, main disadvantage of this source is that time is required to search for right investor of firm.

After analysing both the sources of finance right issue of shares and loan notes it has been

found that appropriate source for company is issuing shares in the market for purchasing building

and non current assets. By issuing equity shares in the market firm can attract large number of

investors and main advantage of this source is that it does not creates financial burden on the

enterprise as compared with debt financing (Murphy, 2001). Depending on the type of investors

6

financial needs with the help of existing shareholders then it is not required by firm to incur extra

expenses for attracting them (Mumford, Schultz and Osburn, 2001).

Implications

Apart from this, Taste plc is having sound financial position and therefore it is easy for

enterprise to attract existing investors in short period of time. Business entity can satisfy its

financial needs with the help of debt issue. In case when loan notes are issued then management has

to pay interest to its holders after regular interval (Jury, 2012) . Moreover, as compared with equity

sources, raising finance with the help of loan notes imposes high cost in front of company. For loan

notes company has to provide security in against of loan. For this financial source company has to

pay interest cost in regular time period. In addition to this organization has liability to repay the

principle amount as per the described contract. This source does not affect controlling power of the

business.

2.3.3 Implication of right issues and loan stock

The implication of right issues can be understood in term of cost and time take to issue of

shares. Also, management need to pay the dividend on right time so as to determine long run

success of the firm with increased rate of return. Furthermore, loan is the another imperative aspect

of finance which take high interest rate on loan. Accordingly, corporation need to pay cost on right

otherwise credit rating of organization get affected.

2.4 Appropriateness of source of finance for buildings and NCA

Equity finance

Advantages

On the other hand main advantage of equity financing is that it enables company to have

more cash in hand, it is less risky as compared with loan. The right business angels and venture

capitalist can bring value and they can explore growth ideas. Further, investors are often prepared to

provide follow up funding as business expands. All these are main benefits of employing equity

financing and is beneficial for the business.

Disadvantage

Further, main disadvantage of this source is that time is required to search for right investor of firm.

After analysing both the sources of finance right issue of shares and loan notes it has been

found that appropriate source for company is issuing shares in the market for purchasing building

and non current assets. By issuing equity shares in the market firm can attract large number of

investors and main advantage of this source is that it does not creates financial burden on the

enterprise as compared with debt financing (Murphy, 2001). Depending on the type of investors

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business losses power to to take effective management decisions and sometime company has to face

legal along with regulatory issues to comply with the raising finance. Moreover, it is possible for

enterprise to better satisfy need of its shareholders and in turn it will have positive impact on brand

image of firm. Taste plc is having good financial position in the market and due to this basic reason

business enterprise can easily provide good return to its investors as per their expectations. Apart

from this, in near future firm can easily accomplish its desired goals along with objectives which is

beneficial for the enterprise in every possible manner. This source of finance has been selected for

firm by considering its pros and cons. Financial needs of enterprise can be easily satisfied when

shares are issued in the market and this provides large number of opportunities to business in terms

of rise in profitability level along with sales. Main implications of choosing issue of shares as

source of finance is that firm has to pay dividend to its investors and voting rights along with major

share in the decision making is transferred to shareholders of organization. This is one of the major

implication of this source of finance which company has to consider necessarily.

Debt finance

Advantages

Main advantage of debt financing to Taste plc is that interest on loan is tax deductible, loans

can be taken for both short and long term and business relationship ends when money is paid back

(Broadbent and Cullen, 2012). It supports business in satisfying short term needs. Further, loan

repayment is quite simple along with interest on loan. Debt does not dilute ownership of the

businesses especially those who are operating on smaller basis.

Disadvantages

Main disadvantage of this source is that money has to be paid within a fixed period of time

and in case if company focuses on too much debt then management has to deal with cash problems.

Further, other cons of this source is that mostly of the lenders provide severe penalties for late

payment which takes into consideration charging fees, late fees etc.

Issue of shares

Company can issue shares in the market through which it is possible to satisfy financial needs of the

business and in turn it acts as development tool for the business (Nofsinger and Varma, 2005)

Advantage

Main advantage of considering this source to business is that it supports in satisfying financial

needs of the business and large amount of funds can be obtained easily for carrying out operations

in the market.

Disadvantage

Main drawback of this source is that it increases overall cost of the company where company has to

7

legal along with regulatory issues to comply with the raising finance. Moreover, it is possible for

enterprise to better satisfy need of its shareholders and in turn it will have positive impact on brand

image of firm. Taste plc is having good financial position in the market and due to this basic reason

business enterprise can easily provide good return to its investors as per their expectations. Apart

from this, in near future firm can easily accomplish its desired goals along with objectives which is

beneficial for the enterprise in every possible manner. This source of finance has been selected for

firm by considering its pros and cons. Financial needs of enterprise can be easily satisfied when

shares are issued in the market and this provides large number of opportunities to business in terms

of rise in profitability level along with sales. Main implications of choosing issue of shares as

source of finance is that firm has to pay dividend to its investors and voting rights along with major

share in the decision making is transferred to shareholders of organization. This is one of the major

implication of this source of finance which company has to consider necessarily.

Debt finance

Advantages

Main advantage of debt financing to Taste plc is that interest on loan is tax deductible, loans

can be taken for both short and long term and business relationship ends when money is paid back

(Broadbent and Cullen, 2012). It supports business in satisfying short term needs. Further, loan

repayment is quite simple along with interest on loan. Debt does not dilute ownership of the

businesses especially those who are operating on smaller basis.

Disadvantages

Main disadvantage of this source is that money has to be paid within a fixed period of time

and in case if company focuses on too much debt then management has to deal with cash problems.

Further, other cons of this source is that mostly of the lenders provide severe penalties for late

payment which takes into consideration charging fees, late fees etc.

Issue of shares

Company can issue shares in the market through which it is possible to satisfy financial needs of the

business and in turn it acts as development tool for the business (Nofsinger and Varma, 2005)

Advantage

Main advantage of considering this source to business is that it supports in satisfying financial

needs of the business and large amount of funds can be obtained easily for carrying out operations

in the market.

Disadvantage

Main drawback of this source is that it increases overall cost of the company where company has to

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pay dividend to its investors along with voting rights. Therefore, it is unfavourable for the business.

2.5 Working capital- Advising board of directors on a source of finance

2.5.1 Definition

The term working capital refers the fund available to business for carrying out operation or

production activities. It is calculated by getting difference of current assets and liabilities.

Furthermore, Working capital is regarded as the cash which company uses in order to successfully

carry out its business operations. Key components of working capital are debtors, creditors and

stock. This source of finance is most appropriate as through this liquidity position of enterprise can

be enhanced easily and in short period of time and company can easily cover all the major

expenses.

2.5.2 Importance of working capital

Working capital is required by business for conducting day to day operations and is the

difference between current assets and liabilities. Main components of working capital are inventory

which takes into consideration raw material, work in progress and finished goods. In case of

excessive stock it will have high burden on cash resources of enterprise and can lead to decline in

sales volume. In order to keep better inventory control it is required to keep a track of stocks for all

the major items of inventory (Wildavsky, 2006). Receivable is another major component of working

capital which contributes large portion of current assets. Investment into receivables requires certain

costs such as opportunity and time value that business has to bear. Further, to manage receivables in

better manner management must have control on credits and must develop effective credit policies.

Cash and cash equivalents is also major component where proper management of cash supports in

determining the optimal size of the firm's asset balance. It represents correlation between

maintaining adequate liquidity with minimum cash in bank. So, these are some of the key

components of working capital and supports firm in conducting operations in better manner.

2.5.3 Sources available for WC

Different sources of finance are present for working capital of Taste plc which organization

can easily consider for satisfying its financial needs and in turn it acts as development tool. Further,

the major sources of working capital are bank loan, retained earnings etc which are appropriate for

taste plc in every possible manner (Nofsinger and Varma, 2005). Moreover, to meet working capital

requirement it is beneficial for company to adopt retained earning as source where internal savings

of the firm can be utilized. Apart from this taking loan from financial institution is also appropriate

as it can support management to deal with unfavourable situations and can assist in effective

utilization of financial resources. It can boost overall productivity and can enhance profitability of

the business in effective manner.

8

2.5 Working capital- Advising board of directors on a source of finance

2.5.1 Definition

The term working capital refers the fund available to business for carrying out operation or

production activities. It is calculated by getting difference of current assets and liabilities.

Furthermore, Working capital is regarded as the cash which company uses in order to successfully

carry out its business operations. Key components of working capital are debtors, creditors and

stock. This source of finance is most appropriate as through this liquidity position of enterprise can

be enhanced easily and in short period of time and company can easily cover all the major

expenses.

2.5.2 Importance of working capital

Working capital is required by business for conducting day to day operations and is the

difference between current assets and liabilities. Main components of working capital are inventory

which takes into consideration raw material, work in progress and finished goods. In case of

excessive stock it will have high burden on cash resources of enterprise and can lead to decline in

sales volume. In order to keep better inventory control it is required to keep a track of stocks for all

the major items of inventory (Wildavsky, 2006). Receivable is another major component of working

capital which contributes large portion of current assets. Investment into receivables requires certain

costs such as opportunity and time value that business has to bear. Further, to manage receivables in

better manner management must have control on credits and must develop effective credit policies.

Cash and cash equivalents is also major component where proper management of cash supports in

determining the optimal size of the firm's asset balance. It represents correlation between

maintaining adequate liquidity with minimum cash in bank. So, these are some of the key

components of working capital and supports firm in conducting operations in better manner.

2.5.3 Sources available for WC

Different sources of finance are present for working capital of Taste plc which organization

can easily consider for satisfying its financial needs and in turn it acts as development tool. Further,

the major sources of working capital are bank loan, retained earnings etc which are appropriate for

taste plc in every possible manner (Nofsinger and Varma, 2005). Moreover, to meet working capital

requirement it is beneficial for company to adopt retained earning as source where internal savings

of the firm can be utilized. Apart from this taking loan from financial institution is also appropriate

as it can support management to deal with unfavourable situations and can assist in effective

utilization of financial resources. It can boost overall productivity and can enhance profitability of

the business in effective manner.

8

On the other hand, company like taste plc is financially strong and its savings are quite high

due to which retained earning can be considered as most appropriate source which can support in

satisfying financial needs. Apart from this, if business enterprise is earning higher amount of profits

then sometime it is not possible to pay dividend to the investors and in turn it is having negative

impact on the firm (Jin, Yu and Mi, 2011). In case when taking loan from bank is considered as an

option by firm then organization has to pay large amount in the form of interest which is also an

major expense. Therefore, this are some of the major reason due to which retained earning and bank

loan has been considered as the sources for satisfying financial needs of the enterprise.

Through effective management of working capital it is possible for enterprise to meet its day

to day expenses and in turn raises overall profitability level of the organization. By appropriate

management of working capital organization can manage their liquidity in order to pay their current

obligation in timely manner. In addition to this, they can avail trading opportunity in order to

enahcne their profitability.

Most effective source of finance for working capital is bank overdraft as it is the facility

granted by bank to withdraw more amount than those lying in the account. Moreover, firm can

easily satisfy its financial requirement by considering this financial source. For this financial source

organization is required to pay bank charges i.e. interest on the additional amount withdrawn

(Kastantin, 2005). In addition to this, they can manager their components of working capital to

generate financial source. For this aspect, they can delay their creditor payment and can make

policies to recover amount from debtors early. For this they are required to provide cash discount to

the debtors so they will be influenced to make cash purchase instead of credit one.

3 Financial statements

3.1 Statement of profit and loss

The statement of profit and loss is prepared for meeting the business requirement by

calculating the profitability. It facilitates to record the transaction related to indirect income and

expenses to be incurred.

3.2 Statement of financial position

Balance sheet is known as statement of financial position which consists detail information

related to liabilities, assets and liquidity of corporation. This assists investors to take right decision

with regard to investment. Thus it aids to assess the performance of corporation in the marketplace

and meet need of different stakeholders in an effectual manner.

3.3 Statement of cash flow

This is another important statement which reflect financial information related to three

major activities of business. This includes income from operating activities, investing as well as

9

due to which retained earning can be considered as most appropriate source which can support in

satisfying financial needs. Apart from this, if business enterprise is earning higher amount of profits

then sometime it is not possible to pay dividend to the investors and in turn it is having negative

impact on the firm (Jin, Yu and Mi, 2011). In case when taking loan from bank is considered as an

option by firm then organization has to pay large amount in the form of interest which is also an

major expense. Therefore, this are some of the major reason due to which retained earning and bank

loan has been considered as the sources for satisfying financial needs of the enterprise.

Through effective management of working capital it is possible for enterprise to meet its day

to day expenses and in turn raises overall profitability level of the organization. By appropriate

management of working capital organization can manage their liquidity in order to pay their current

obligation in timely manner. In addition to this, they can avail trading opportunity in order to

enahcne their profitability.

Most effective source of finance for working capital is bank overdraft as it is the facility

granted by bank to withdraw more amount than those lying in the account. Moreover, firm can

easily satisfy its financial requirement by considering this financial source. For this financial source

organization is required to pay bank charges i.e. interest on the additional amount withdrawn

(Kastantin, 2005). In addition to this, they can manager their components of working capital to

generate financial source. For this aspect, they can delay their creditor payment and can make

policies to recover amount from debtors early. For this they are required to provide cash discount to

the debtors so they will be influenced to make cash purchase instead of credit one.

3 Financial statements

3.1 Statement of profit and loss

The statement of profit and loss is prepared for meeting the business requirement by

calculating the profitability. It facilitates to record the transaction related to indirect income and

expenses to be incurred.

3.2 Statement of financial position

Balance sheet is known as statement of financial position which consists detail information

related to liabilities, assets and liquidity of corporation. This assists investors to take right decision

with regard to investment. Thus it aids to assess the performance of corporation in the marketplace

and meet need of different stakeholders in an effectual manner.

3.3 Statement of cash flow

This is another important statement which reflect financial information related to three

major activities of business. This includes income from operating activities, investing as well as

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financing activities. Under this transaction regarding payment of loan and sale of old assets all are

recorded so as to analyse the actual performance of corporation.

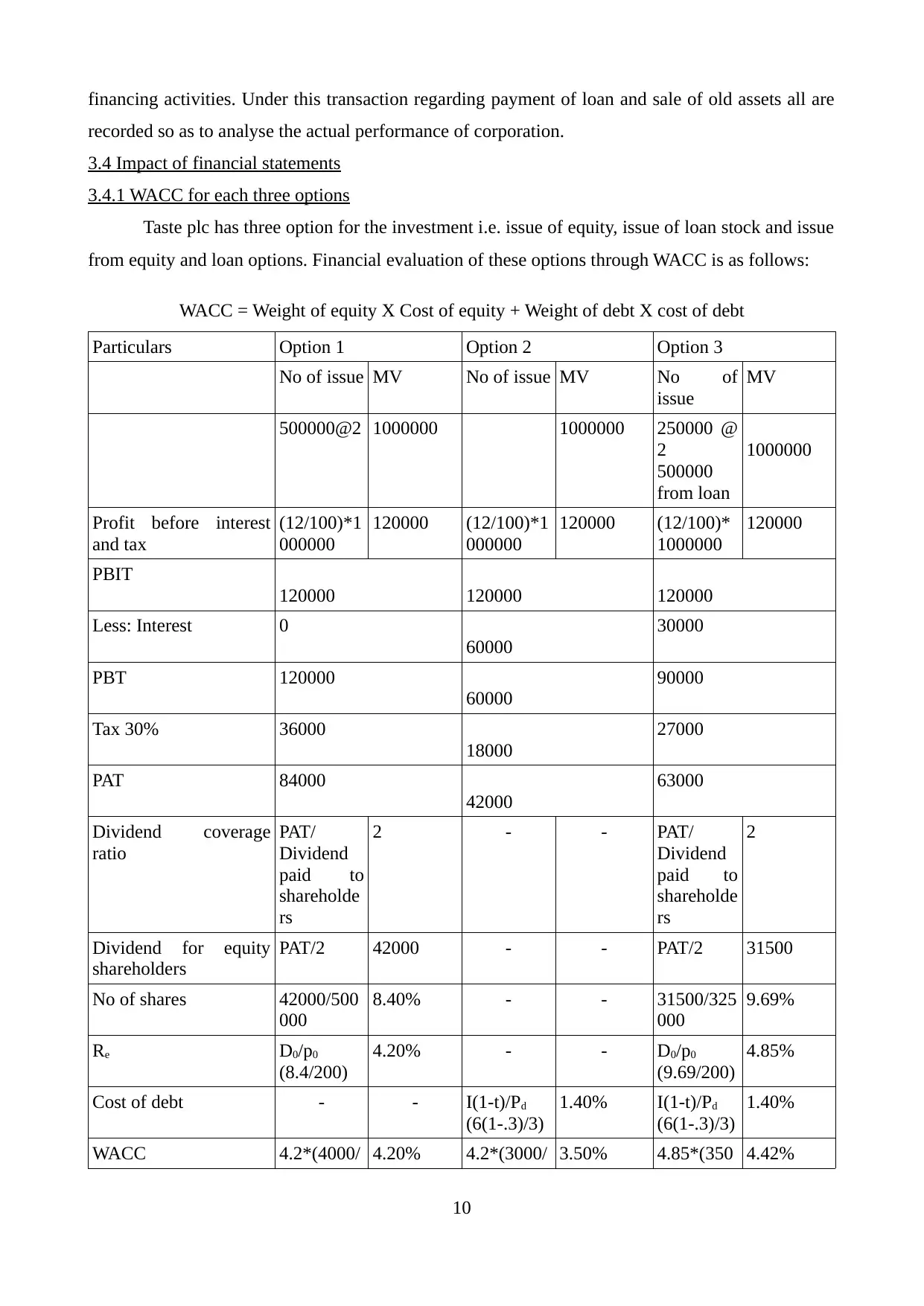

3.4 Impact of financial statements

3.4.1 WACC for each three options

Taste plc has three option for the investment i.e. issue of equity, issue of loan stock and issue

from equity and loan options. Financial evaluation of these options through WACC is as follows:

WACC = Weight of equity X Cost of equity + Weight of debt X cost of debt

Particulars Option 1 Option 2 Option 3

No of issue MV No of issue MV No of

issue

MV

500000@2 1000000 1000000 250000 @

2

500000

from loan

1000000

Profit before interest

and tax

(12/100)*1

000000

120000 (12/100)*1

000000

120000 (12/100)*

1000000

120000

PBIT

120000 120000 120000

Less: Interest 0

60000

30000

PBT 120000

60000

90000

Tax 30% 36000

18000

27000

PAT 84000

42000

63000

Dividend coverage

ratio

PAT/

Dividend

paid to

shareholde

rs

2 - - PAT/

Dividend

paid to

shareholde

rs

2

Dividend for equity

shareholders

PAT/2 42000 - - PAT/2 31500

No of shares 42000/500

000

8.40% - - 31500/325

000

9.69%

Re D0/p0

(8.4/200)

4.20% - - D0/p0

(9.69/200)

4.85%

Cost of debt - - I(1-t)/Pd

(6(1-.3)/3)

1.40% I(1-t)/Pd

(6(1-.3)/3)

1.40%

WACC 4.2*(4000/ 4.20% 4.2*(3000/ 3.50% 4.85*(350 4.42%

10

recorded so as to analyse the actual performance of corporation.

3.4 Impact of financial statements

3.4.1 WACC for each three options

Taste plc has three option for the investment i.e. issue of equity, issue of loan stock and issue

from equity and loan options. Financial evaluation of these options through WACC is as follows:

WACC = Weight of equity X Cost of equity + Weight of debt X cost of debt

Particulars Option 1 Option 2 Option 3

No of issue MV No of issue MV No of

issue

MV

500000@2 1000000 1000000 250000 @

2

500000

from loan

1000000

Profit before interest

and tax

(12/100)*1

000000

120000 (12/100)*1

000000

120000 (12/100)*

1000000

120000

PBIT

120000 120000 120000

Less: Interest 0

60000

30000

PBT 120000

60000

90000

Tax 30% 36000

18000

27000

PAT 84000

42000

63000

Dividend coverage

ratio

PAT/

Dividend

paid to

shareholde

rs

2 - - PAT/

Dividend

paid to

shareholde

rs

2

Dividend for equity

shareholders

PAT/2 42000 - - PAT/2 31500

No of shares 42000/500

000

8.40% - - 31500/325

000

9.69%

Re D0/p0

(8.4/200)

4.20% - - D0/p0

(9.69/200)

4.85%

Cost of debt - - I(1-t)/Pd

(6(1-.3)/3)

1.40% I(1-t)/Pd

(6(1-.3)/3)

1.40%

WACC 4.2*(4000/ 4.20% 4.2*(3000/ 3.50% 4.85*(350 4.42%

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4000) 4000)+1.4(

1000/4000

)

0/4000)+1

.4(500/40

00)

It is recommended to the board of directors of Taste plc to adopt second alternative which is

beneficial for management. By adopting this option it is possible for business enterprise to raise

funds by taking loan of 1000000 @ 6%. It supports in granting more balance upon the financial

obligations of the business enterprise. This source will provide tax shield to the company and they

have less financial cost (Jury, 2012).

3.4.2 Gearing for each three option

According to the above table in the first option debt financial resources are not available to

raise the finance. Owing to this, cost of equity is considered as cost of capital and the gearing ratio

cannot be calculated due to abase of debt in the capital structure. On the other hand, debt to equity

is 3:1 and 7: 1 in second and third option respectively. Thus, second option is feasible for

corporation in order to mitigate risk and to ensure stability.

It can be suggested from to board of directors that second alternative is the most optimal

option for the organization as it proves to be effective to raise loan of 1000000 @ 6%. Furthermore,

this option facilitates to provide tax shield and accordingly balance will be created in financial

structure of corporation.

3.4.3 How did it impact financial statements

By using second option of debt financial changes can be seen in balance sheet and income

statement of corporation. This is because long term obligation of company will be increased due to

access to debt financing. Similarly, cash equivalence will also be increased. Apart from this income

statement will be affected because profitability decreases due to financial cost.

3.5 Earning per share

3.5.1 what information does this provides

Earning per share is the most important information for shareholders because by this they

come to know regarding rate of return. Earning per share is regarded as the dividend or income

which shareholders of the enterprise receives by investing funds into the shares of company.

Further, investors of the organization are highly interested in knowing about income of the business

as through this they get idea regarding the level of return. Apart from this, taste plc is receiving high

income due to which it is possible for company to satisfy need of its shareholders in effective

manner (Mayer, Schoors and Yafeh, 2005). Further, investment decisions taken by investors are

directly linked with the growth and development aspect of the business enterprise. In order to

11

1000/4000

)

0/4000)+1

.4(500/40

00)

It is recommended to the board of directors of Taste plc to adopt second alternative which is

beneficial for management. By adopting this option it is possible for business enterprise to raise

funds by taking loan of 1000000 @ 6%. It supports in granting more balance upon the financial

obligations of the business enterprise. This source will provide tax shield to the company and they

have less financial cost (Jury, 2012).

3.4.2 Gearing for each three option

According to the above table in the first option debt financial resources are not available to

raise the finance. Owing to this, cost of equity is considered as cost of capital and the gearing ratio

cannot be calculated due to abase of debt in the capital structure. On the other hand, debt to equity

is 3:1 and 7: 1 in second and third option respectively. Thus, second option is feasible for

corporation in order to mitigate risk and to ensure stability.

It can be suggested from to board of directors that second alternative is the most optimal

option for the organization as it proves to be effective to raise loan of 1000000 @ 6%. Furthermore,

this option facilitates to provide tax shield and accordingly balance will be created in financial

structure of corporation.

3.4.3 How did it impact financial statements

By using second option of debt financial changes can be seen in balance sheet and income

statement of corporation. This is because long term obligation of company will be increased due to

access to debt financing. Similarly, cash equivalence will also be increased. Apart from this income

statement will be affected because profitability decreases due to financial cost.

3.5 Earning per share

3.5.1 what information does this provides

Earning per share is the most important information for shareholders because by this they

come to know regarding rate of return. Earning per share is regarded as the dividend or income

which shareholders of the enterprise receives by investing funds into the shares of company.

Further, investors of the organization are highly interested in knowing about income of the business

as through this they get idea regarding the level of return. Apart from this, taste plc is receiving high

income due to which it is possible for company to satisfy need of its shareholders in effective

manner (Mayer, Schoors and Yafeh, 2005). Further, investment decisions taken by investors are

directly linked with the growth and development aspect of the business enterprise. In order to

11

determine the level of return profit after tax is divided by number of shares which they usually

receive from organization.

3.5.2 Earning per share calculation

Profit before interest and tax= 720000

Profit after interest= 720000 – 60000 = 660000

Profit after interest = 660000*(1-.3)

=462000

= PAIT/ no. of equity shareholders

=182/3000

=6.06%

Assuming option only debt has been used

£ 1000000 of 6% loan stock

Interest = 6 /100 * 1000000

= £ 60,000

No of ordinary shares = 3000000

EPS = 462000 / 3000000 = 0.154 p

3.5.3 Explaining the answer

So the calculation of earning per share represents that company is profitable on a

shareholder basis. Further, this is assisting enterprise in satisfying need of its target market in

efficient manner. Moreover, with the help of this it is possible for business to well satisfy need of its

target market and can act as development tool. This can allow business to attract large number of

investors and business can easily deal with the challenges present in business environment. On the

other hand, it is well known fact that every shareholder expects high return from company and this

need can be satisfied by management only when higher profits are earned and this in turn acts as

development tool for the entire company (Penman and Penman, 2007). Moreover, taste plc has to

apply larger efforts in enhancing its profitability level so that more return can be provided to the

target market and it can become easy for management to enhance overall performance of firm in the

market.

4 Investment appraisal

4.1 Why it is important to appraise potential investment

In order to know feasibility of the proposal investment appraisal technique has been applied

through which appropriate project can be adopted in which funds can be easily allocated. Further,

investment decisions are crucial in nature as large amount of funds are allocated by company with

aim to receive good return (Diefenbach, 2006). In short it directly leads to accomplishment of

12

receive from organization.

3.5.2 Earning per share calculation

Profit before interest and tax= 720000

Profit after interest= 720000 – 60000 = 660000

Profit after interest = 660000*(1-.3)

=462000

= PAIT/ no. of equity shareholders

=182/3000

=6.06%

Assuming option only debt has been used

£ 1000000 of 6% loan stock

Interest = 6 /100 * 1000000

= £ 60,000

No of ordinary shares = 3000000

EPS = 462000 / 3000000 = 0.154 p

3.5.3 Explaining the answer

So the calculation of earning per share represents that company is profitable on a

shareholder basis. Further, this is assisting enterprise in satisfying need of its target market in

efficient manner. Moreover, with the help of this it is possible for business to well satisfy need of its

target market and can act as development tool. This can allow business to attract large number of

investors and business can easily deal with the challenges present in business environment. On the

other hand, it is well known fact that every shareholder expects high return from company and this

need can be satisfied by management only when higher profits are earned and this in turn acts as

development tool for the entire company (Penman and Penman, 2007). Moreover, taste plc has to

apply larger efforts in enhancing its profitability level so that more return can be provided to the

target market and it can become easy for management to enhance overall performance of firm in the

market.

4 Investment appraisal

4.1 Why it is important to appraise potential investment

In order to know feasibility of the proposal investment appraisal technique has been applied

through which appropriate project can be adopted in which funds can be easily allocated. Further,

investment decisions are crucial in nature as large amount of funds are allocated by company with

aim to receive good return (Diefenbach, 2006). In short it directly leads to accomplishment of

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.