Financial Planning & Management Accounting

VerifiedAdded on 2020/02/14

|17

|5831

|117

AI Summary

This assignment delves into the realm of financial planning and management accounting. It examines various aspects of financial planning, including capital budgeting, internal finance, and strategic water utility management. The assignment also emphasizes the importance of ratio analysis for evaluating firm performance, with a focus on applications in commercial banking and small enterprises. Key concepts covered include unit cost calculations, multi-objective optimization, and the perception of financial planning within specific business contexts.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Managing Financial Resources and

decisions

1

decisions

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1....................................................................................................................................................3

1.2....................................................................................................................................................4

1.3....................................................................................................................................................5

TASK 2.................................................................................................................................................6

2.1....................................................................................................................................................6

2.2....................................................................................................................................................6

2.3....................................................................................................................................................7

2.4....................................................................................................................................................8

TASK 3.................................................................................................................................................8

3.1....................................................................................................................................................8

3.2..................................................................................................................................................10

3.3..................................................................................................................................................10

TASK 4...............................................................................................................................................12

4.1..................................................................................................................................................12

4.2..................................................................................................................................................12

4.3..................................................................................................................................................13

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................16

2

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1....................................................................................................................................................3

1.2....................................................................................................................................................4

1.3....................................................................................................................................................5

TASK 2.................................................................................................................................................6

2.1....................................................................................................................................................6

2.2....................................................................................................................................................6

2.3....................................................................................................................................................7

2.4....................................................................................................................................................8

TASK 3.................................................................................................................................................8

3.1....................................................................................................................................................8

3.2..................................................................................................................................................10

3.3..................................................................................................................................................10

TASK 4...............................................................................................................................................12

4.1..................................................................................................................................................12

4.2..................................................................................................................................................12

4.3..................................................................................................................................................13

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................16

2

INTRODUCTION

Money is the primarily need of every new as well as established business organization to run

their operations successfully. Commercial as well as service rendering entrepreneurs need adequate

funds for different purpose i.e. payment of revenue and capital nature expenses, expansion,

investment in profitable purpose and managing financial risk to achieve set targets. There are wide

ranges of resources available to every entrepreneur through which they can gather sufficient amount

of capital resources to meet their financial need. Thus, the present report here emphasizes on

identifying variety of capital sources along with its positive as well as negative impact to Sweet

Menu Restaurant for its expansion programme. It will enable restaurant to select the best source

among all. Moreover, the assignment also aims to evaluating the role and importance of budgetary

analysis in effective financial management. Furthermore, the report also shed light on the

significance of project evaluation techniques, comprising both discounting and non-discounting

methods to test project viability. In the end, operational performance of Sweet Menu Restaurant

(SMR) and Blue Island Restaurant (BLR) will be examined through applying ratio analysis

technique. It will enable restaurant to take necessary decisions for performing well in future period.

TASK 1

1.1

According to the scenario, SMR is a reputable restaurant which is operating in Gants Hill,

East London from past 10 year. It built-up a strong reputation in the market by offering various

inter-continental food items at an acceptable prices. Now, in order to expand operations, it is

planning to begin two branches in Central London and Croydon requiring investment worth

£300,000 and £500,000 respectively. In order to finance its proposed expansion plan, it can gather

funds through following sources:

Debt fund: In UK and all the other countries, commercial banks and financial institutions

provide funding facilities to the corporations to meet their capital need at an interest rate. Thus, one

of the options available to SMR to gather funds is to raise capital through external borrowings.

Hire purchase (HP): At the time of beginning branches in Central London and Croydon,

SMR can decide to use rented office rather than purchasing it (Berger and Black, 2011). In this,

SMR can purchase property on HP system through making some initial down payment and rest in

equal periodical instalments.

Retained earnings: Companies distribute some proportion of their net earnings to

shareholders and rest of the part is called retained earnings. It is another option available to SMR to

3

Money is the primarily need of every new as well as established business organization to run

their operations successfully. Commercial as well as service rendering entrepreneurs need adequate

funds for different purpose i.e. payment of revenue and capital nature expenses, expansion,

investment in profitable purpose and managing financial risk to achieve set targets. There are wide

ranges of resources available to every entrepreneur through which they can gather sufficient amount

of capital resources to meet their financial need. Thus, the present report here emphasizes on

identifying variety of capital sources along with its positive as well as negative impact to Sweet

Menu Restaurant for its expansion programme. It will enable restaurant to select the best source

among all. Moreover, the assignment also aims to evaluating the role and importance of budgetary

analysis in effective financial management. Furthermore, the report also shed light on the

significance of project evaluation techniques, comprising both discounting and non-discounting

methods to test project viability. In the end, operational performance of Sweet Menu Restaurant

(SMR) and Blue Island Restaurant (BLR) will be examined through applying ratio analysis

technique. It will enable restaurant to take necessary decisions for performing well in future period.

TASK 1

1.1

According to the scenario, SMR is a reputable restaurant which is operating in Gants Hill,

East London from past 10 year. It built-up a strong reputation in the market by offering various

inter-continental food items at an acceptable prices. Now, in order to expand operations, it is

planning to begin two branches in Central London and Croydon requiring investment worth

£300,000 and £500,000 respectively. In order to finance its proposed expansion plan, it can gather

funds through following sources:

Debt fund: In UK and all the other countries, commercial banks and financial institutions

provide funding facilities to the corporations to meet their capital need at an interest rate. Thus, one

of the options available to SMR to gather funds is to raise capital through external borrowings.

Hire purchase (HP): At the time of beginning branches in Central London and Croydon,

SMR can decide to use rented office rather than purchasing it (Berger and Black, 2011). In this,

SMR can purchase property on HP system through making some initial down payment and rest in

equal periodical instalments.

Retained earnings: Companies distribute some proportion of their net earnings to

shareholders and rest of the part is called retained earnings. It is another option available to SMR to

3

meet their capital requirement through ploughing back their available retains profits in the business

to support proposed expansion plan.

Trade credit: It is an arrangement between manufacturer and creditors, in which, supplier

agrees to deliver material on credit (Brandimarte, 2013). Through this, restaurant can take some

time to make payment to the suppliers after gathering sales revenues.

Overdraft: Commercial banks allow their customers to withdraw some extent amount than

their available balance in account, called overdraft. It can provide huge help to SMR to meet their

urgent short-term capital requirement.

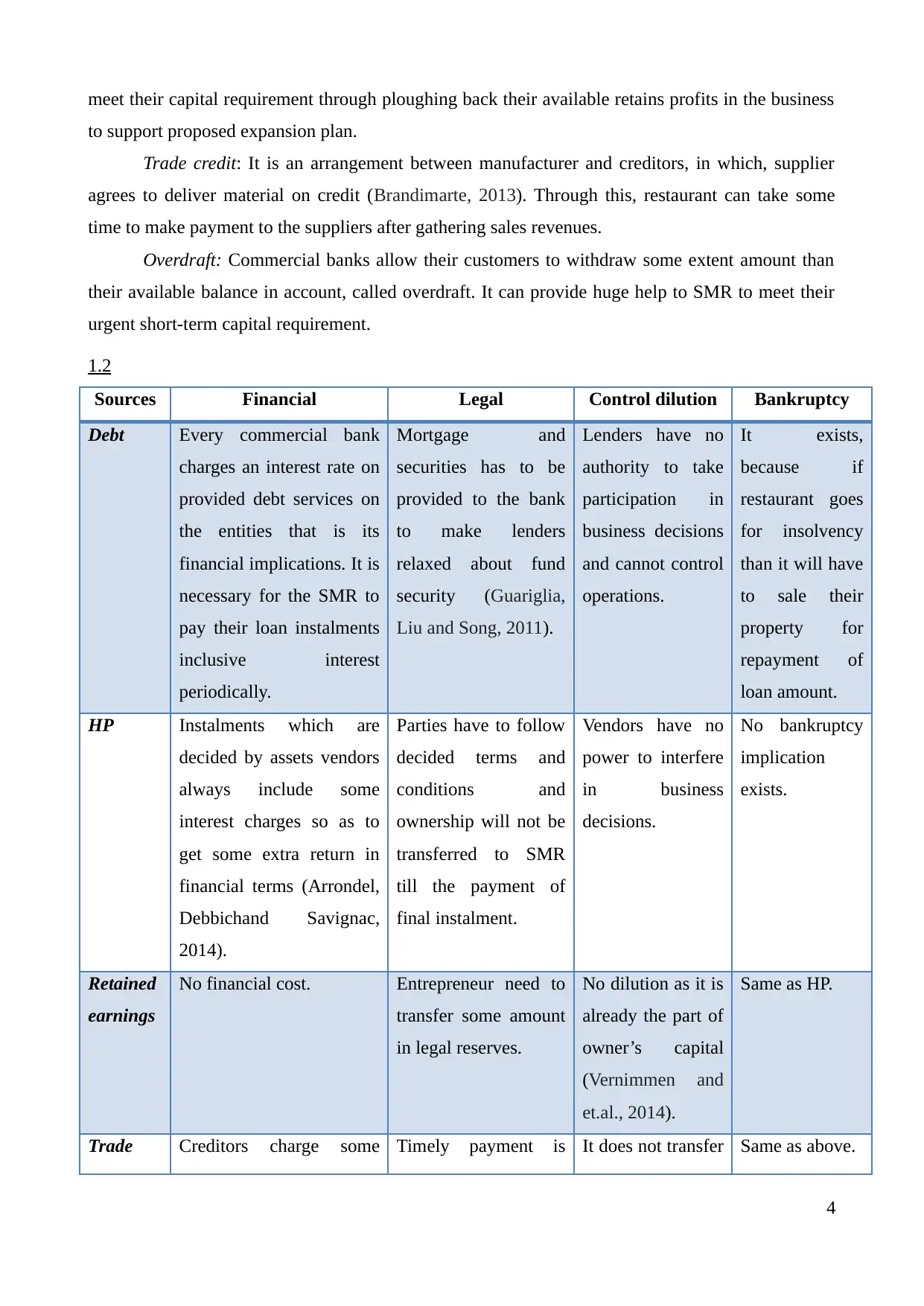

1.2

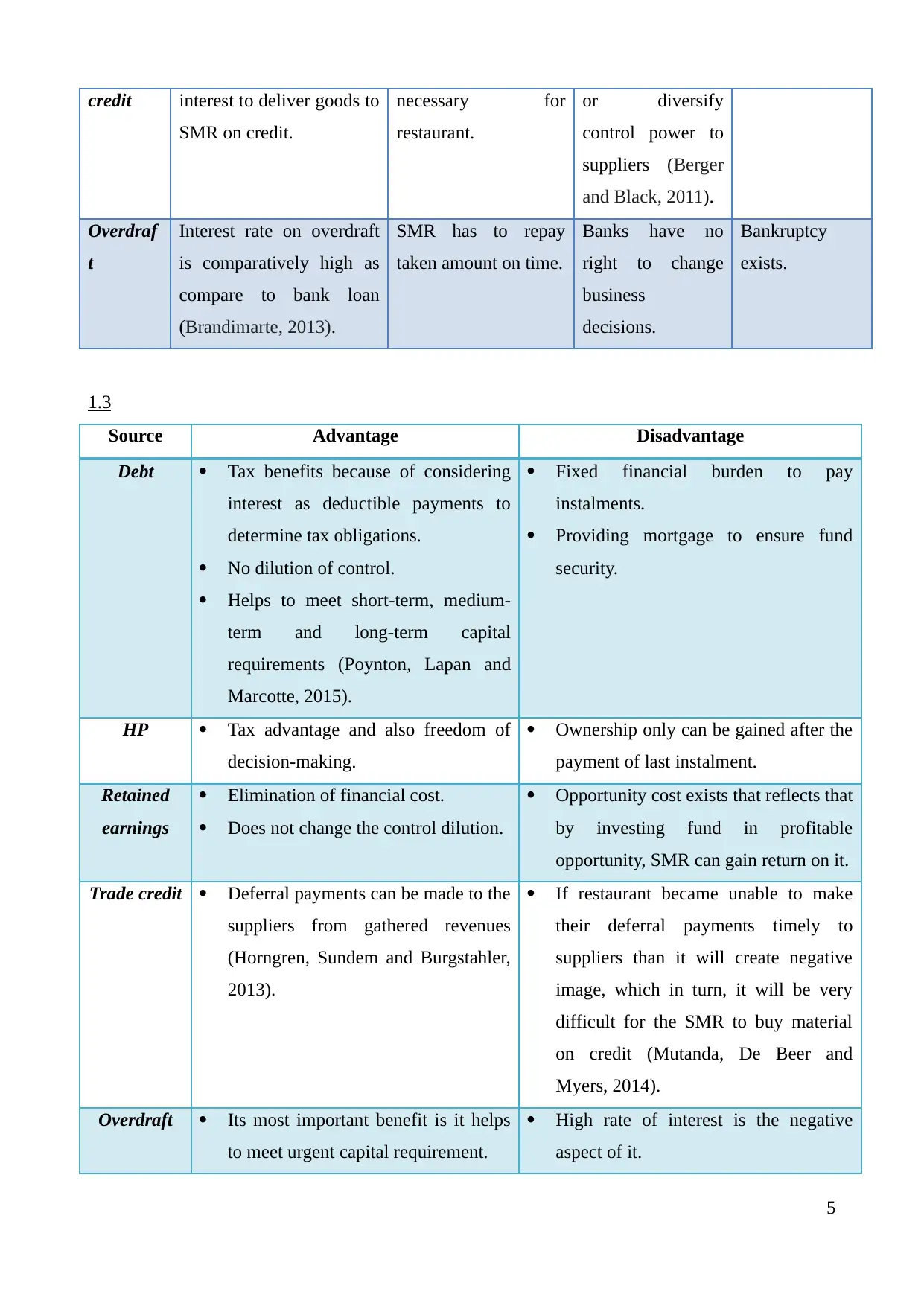

Sources Financial Legal Control dilution Bankruptcy

Debt Every commercial bank

charges an interest rate on

provided debt services on

the entities that is its

financial implications. It is

necessary for the SMR to

pay their loan instalments

inclusive interest

periodically.

Mortgage and

securities has to be

provided to the bank

to make lenders

relaxed about fund

security (Guariglia,

Liu and Song, 2011).

Lenders have no

authority to take

participation in

business decisions

and cannot control

operations.

It exists,

because if

restaurant goes

for insolvency

than it will have

to sale their

property for

repayment of

loan amount.

HP Instalments which are

decided by assets vendors

always include some

interest charges so as to

get some extra return in

financial terms (Arrondel,

Debbichand Savignac,

2014).

Parties have to follow

decided terms and

conditions and

ownership will not be

transferred to SMR

till the payment of

final instalment.

Vendors have no

power to interfere

in business

decisions.

No bankruptcy

implication

exists.

Retained

earnings

No financial cost. Entrepreneur need to

transfer some amount

in legal reserves.

No dilution as it is

already the part of

owner’s capital

(Vernimmen and

et.al., 2014).

Same as HP.

Trade Creditors charge some Timely payment is It does not transfer Same as above.

4

to support proposed expansion plan.

Trade credit: It is an arrangement between manufacturer and creditors, in which, supplier

agrees to deliver material on credit (Brandimarte, 2013). Through this, restaurant can take some

time to make payment to the suppliers after gathering sales revenues.

Overdraft: Commercial banks allow their customers to withdraw some extent amount than

their available balance in account, called overdraft. It can provide huge help to SMR to meet their

urgent short-term capital requirement.

1.2

Sources Financial Legal Control dilution Bankruptcy

Debt Every commercial bank

charges an interest rate on

provided debt services on

the entities that is its

financial implications. It is

necessary for the SMR to

pay their loan instalments

inclusive interest

periodically.

Mortgage and

securities has to be

provided to the bank

to make lenders

relaxed about fund

security (Guariglia,

Liu and Song, 2011).

Lenders have no

authority to take

participation in

business decisions

and cannot control

operations.

It exists,

because if

restaurant goes

for insolvency

than it will have

to sale their

property for

repayment of

loan amount.

HP Instalments which are

decided by assets vendors

always include some

interest charges so as to

get some extra return in

financial terms (Arrondel,

Debbichand Savignac,

2014).

Parties have to follow

decided terms and

conditions and

ownership will not be

transferred to SMR

till the payment of

final instalment.

Vendors have no

power to interfere

in business

decisions.

No bankruptcy

implication

exists.

Retained

earnings

No financial cost. Entrepreneur need to

transfer some amount

in legal reserves.

No dilution as it is

already the part of

owner’s capital

(Vernimmen and

et.al., 2014).

Same as HP.

Trade Creditors charge some Timely payment is It does not transfer Same as above.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

credit interest to deliver goods to

SMR on credit.

necessary for

restaurant.

or diversify

control power to

suppliers (Berger

and Black, 2011).

Overdraf

t

Interest rate on overdraft

is comparatively high as

compare to bank loan

(Brandimarte, 2013).

SMR has to repay

taken amount on time.

Banks have no

right to change

business

decisions.

Bankruptcy

exists.

1.3

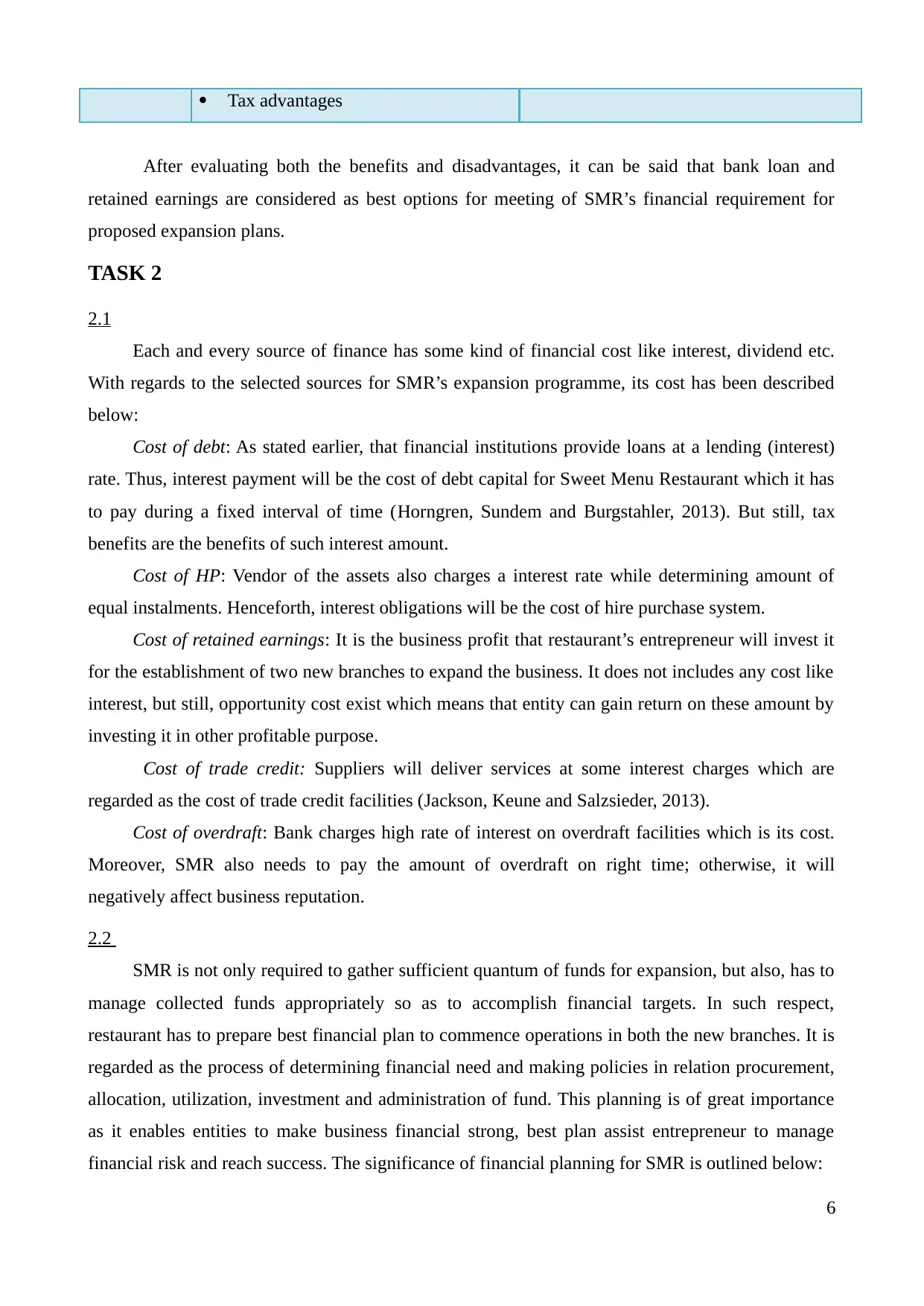

Source Advantage Disadvantage

Debt Tax benefits because of considering

interest as deductible payments to

determine tax obligations.

No dilution of control.

Helps to meet short-term, medium-

term and long-term capital

requirements (Poynton, Lapan and

Marcotte, 2015).

Fixed financial burden to pay

instalments.

Providing mortgage to ensure fund

security.

HP Tax advantage and also freedom of

decision-making.

Ownership only can be gained after the

payment of last instalment.

Retained

earnings

Elimination of financial cost.

Does not change the control dilution.

Opportunity cost exists that reflects that

by investing fund in profitable

opportunity, SMR can gain return on it.

Trade credit Deferral payments can be made to the

suppliers from gathered revenues

(Horngren, Sundem and Burgstahler,

2013).

If restaurant became unable to make

their deferral payments timely to

suppliers than it will create negative

image, which in turn, it will be very

difficult for the SMR to buy material

on credit (Mutanda, De Beer and

Myers, 2014).

Overdraft Its most important benefit is it helps

to meet urgent capital requirement.

High rate of interest is the negative

aspect of it.

5

SMR on credit.

necessary for

restaurant.

or diversify

control power to

suppliers (Berger

and Black, 2011).

Overdraf

t

Interest rate on overdraft

is comparatively high as

compare to bank loan

(Brandimarte, 2013).

SMR has to repay

taken amount on time.

Banks have no

right to change

business

decisions.

Bankruptcy

exists.

1.3

Source Advantage Disadvantage

Debt Tax benefits because of considering

interest as deductible payments to

determine tax obligations.

No dilution of control.

Helps to meet short-term, medium-

term and long-term capital

requirements (Poynton, Lapan and

Marcotte, 2015).

Fixed financial burden to pay

instalments.

Providing mortgage to ensure fund

security.

HP Tax advantage and also freedom of

decision-making.

Ownership only can be gained after the

payment of last instalment.

Retained

earnings

Elimination of financial cost.

Does not change the control dilution.

Opportunity cost exists that reflects that

by investing fund in profitable

opportunity, SMR can gain return on it.

Trade credit Deferral payments can be made to the

suppliers from gathered revenues

(Horngren, Sundem and Burgstahler,

2013).

If restaurant became unable to make

their deferral payments timely to

suppliers than it will create negative

image, which in turn, it will be very

difficult for the SMR to buy material

on credit (Mutanda, De Beer and

Myers, 2014).

Overdraft Its most important benefit is it helps

to meet urgent capital requirement.

High rate of interest is the negative

aspect of it.

5

Tax advantages

After evaluating both the benefits and disadvantages, it can be said that bank loan and

retained earnings are considered as best options for meeting of SMR’s financial requirement for

proposed expansion plans.

TASK 2

2.1

Each and every source of finance has some kind of financial cost like interest, dividend etc.

With regards to the selected sources for SMR’s expansion programme, its cost has been described

below:

Cost of debt: As stated earlier, that financial institutions provide loans at a lending (interest)

rate. Thus, interest payment will be the cost of debt capital for Sweet Menu Restaurant which it has

to pay during a fixed interval of time (Horngren, Sundem and Burgstahler, 2013). But still, tax

benefits are the benefits of such interest amount.

Cost of HP: Vendor of the assets also charges a interest rate while determining amount of

equal instalments. Henceforth, interest obligations will be the cost of hire purchase system.

Cost of retained earnings: It is the business profit that restaurant’s entrepreneur will invest it

for the establishment of two new branches to expand the business. It does not includes any cost like

interest, but still, opportunity cost exist which means that entity can gain return on these amount by

investing it in other profitable purpose.

Cost of trade credit: Suppliers will deliver services at some interest charges which are

regarded as the cost of trade credit facilities (Jackson, Keune and Salzsieder, 2013).

Cost of overdraft: Bank charges high rate of interest on overdraft facilities which is its cost.

Moreover, SMR also needs to pay the amount of overdraft on right time; otherwise, it will

negatively affect business reputation.

2.2

SMR is not only required to gather sufficient quantum of funds for expansion, but also, has to

manage collected funds appropriately so as to accomplish financial targets. In such respect,

restaurant has to prepare best financial plan to commence operations in both the new branches. It is

regarded as the process of determining financial need and making policies in relation procurement,

allocation, utilization, investment and administration of fund. This planning is of great importance

as it enables entities to make business financial strong, best plan assist entrepreneur to manage

financial risk and reach success. The significance of financial planning for SMR is outlined below:

6

After evaluating both the benefits and disadvantages, it can be said that bank loan and

retained earnings are considered as best options for meeting of SMR’s financial requirement for

proposed expansion plans.

TASK 2

2.1

Each and every source of finance has some kind of financial cost like interest, dividend etc.

With regards to the selected sources for SMR’s expansion programme, its cost has been described

below:

Cost of debt: As stated earlier, that financial institutions provide loans at a lending (interest)

rate. Thus, interest payment will be the cost of debt capital for Sweet Menu Restaurant which it has

to pay during a fixed interval of time (Horngren, Sundem and Burgstahler, 2013). But still, tax

benefits are the benefits of such interest amount.

Cost of HP: Vendor of the assets also charges a interest rate while determining amount of

equal instalments. Henceforth, interest obligations will be the cost of hire purchase system.

Cost of retained earnings: It is the business profit that restaurant’s entrepreneur will invest it

for the establishment of two new branches to expand the business. It does not includes any cost like

interest, but still, opportunity cost exist which means that entity can gain return on these amount by

investing it in other profitable purpose.

Cost of trade credit: Suppliers will deliver services at some interest charges which are

regarded as the cost of trade credit facilities (Jackson, Keune and Salzsieder, 2013).

Cost of overdraft: Bank charges high rate of interest on overdraft facilities which is its cost.

Moreover, SMR also needs to pay the amount of overdraft on right time; otherwise, it will

negatively affect business reputation.

2.2

SMR is not only required to gather sufficient quantum of funds for expansion, but also, has to

manage collected funds appropriately so as to accomplish financial targets. In such respect,

restaurant has to prepare best financial plan to commence operations in both the new branches. It is

regarded as the process of determining financial need and making policies in relation procurement,

allocation, utilization, investment and administration of fund. This planning is of great importance

as it enables entities to make business financial strong, best plan assist entrepreneur to manage

financial risk and reach success. The significance of financial planning for SMR is outlined below:

6

Plan of monetary arrangement will assist entrepreneur in ensuring better execution of fund

related activities and operations.

Revenue management is also an important advantage of financial management. It is because,

with the help of different types of budget, restaurant’s manager can determine that whether

they will have surplus or shortfall of cash (Brigham and Ehrhardt, 2013). This in turn,

appropriate decisions can be taken to minimize expenditures and maximize revenues to meet

goals.

Effective money-based arrangement will provide great assistance to the SMR to accept

market challenges due to proper availability of funds. Moreover, it will also support further

expansion and growth plans and ensure long-run sustainability (Toth, 2015).

Constructing best financial plan enable restaurant to effectively utilize their funding sources

and gain maximum yield to compete effectively.

Comparison of the planned activities with actual outcome also helps restaurant’s manager to

identify the reasons for not achieving target goals (Poynton, Lapan and Marcotte, 2015)..

This in turn, they can overcome the limitations that they have done in past years and prepare

a suitable plan to accomplish targets.

2.3

Every commercial establishment have wide range of stakeholders, categorized in two parts

that are internal and external. They require some valuable information about company’s operations

to take qualitative decisions for different purpose, presenting here as under:

Shareholders: They take risk by investing their own money in the business so as to generate

more dividends. They require information about current investors return, growth prospectus, and

return on capital employed and increase in market price. Investors will only put their money in

SMR, if there is a possibility of getting higher return.

Creditors: Companies often purchase some proportion of inventory on credit from the

creditors/suppliers (Dhaliwal and et.al., 2014). Thus, they are interested in knowing liquidity

position and creditworthiness of the SMR, because they provided credit facilities to corporations

that are able to make deferral payments on right time.

Government: Regulatory authorities have some kind of stake in the business success. For

instance, taxation department aims in collecting appropriate amount of taxes on net corporate yield.

Moreover, regulatory bodies also aim in ensuring legality and ethnicity of SMR’s regular activities

and functions.

Lenders: Commercial banks and financial institutions need important information about

7

related activities and operations.

Revenue management is also an important advantage of financial management. It is because,

with the help of different types of budget, restaurant’s manager can determine that whether

they will have surplus or shortfall of cash (Brigham and Ehrhardt, 2013). This in turn,

appropriate decisions can be taken to minimize expenditures and maximize revenues to meet

goals.

Effective money-based arrangement will provide great assistance to the SMR to accept

market challenges due to proper availability of funds. Moreover, it will also support further

expansion and growth plans and ensure long-run sustainability (Toth, 2015).

Constructing best financial plan enable restaurant to effectively utilize their funding sources

and gain maximum yield to compete effectively.

Comparison of the planned activities with actual outcome also helps restaurant’s manager to

identify the reasons for not achieving target goals (Poynton, Lapan and Marcotte, 2015)..

This in turn, they can overcome the limitations that they have done in past years and prepare

a suitable plan to accomplish targets.

2.3

Every commercial establishment have wide range of stakeholders, categorized in two parts

that are internal and external. They require some valuable information about company’s operations

to take qualitative decisions for different purpose, presenting here as under:

Shareholders: They take risk by investing their own money in the business so as to generate

more dividends. They require information about current investors return, growth prospectus, and

return on capital employed and increase in market price. Investors will only put their money in

SMR, if there is a possibility of getting higher return.

Creditors: Companies often purchase some proportion of inventory on credit from the

creditors/suppliers (Dhaliwal and et.al., 2014). Thus, they are interested in knowing liquidity

position and creditworthiness of the SMR, because they provided credit facilities to corporations

that are able to make deferral payments on right time.

Government: Regulatory authorities have some kind of stake in the business success. For

instance, taxation department aims in collecting appropriate amount of taxes on net corporate yield.

Moreover, regulatory bodies also aim in ensuring legality and ethnicity of SMR’s regular activities

and functions.

Lenders: Commercial banks and financial institutions need important information about

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

restaurant’s debt burden capability, solvency, long-term financial risk, cash generating ability and

profit position. The main aim to examine this information is to assure loan security.

Employees: They are willing to put their efforts in that organization, in which, there is a

greater chance of growth and progress (Horngren, Sundem and Burgstahler, 2013). It is because;

workers are mainly aims at getting better hike in salary, appraisal, rewards and other benefits like

holidays, more responsibility, club membership etc.

2.4

Collection of fund through debt will increase the amount of long-term and loan and cash in

balance sheet from £31000 and £11000 respectively. On the other hand, interest payment will be

reported in profit and loss account and increase total interest payment from £10000. Its dual impact

will be reflecting on closing cash balance which will be decrease by the amount of interest payment.

However, instalment payment on hire purchase will be recorded in P&L a/c and also decline total

cash and bank balance. Moreover, payment of instalments along with interest will be subtracted

from cash position and result in lower return. On the contrary to this, use of retained profit will be

recorded in the statement of change in retained earnings only. Buying material on credit will

increase accounts payable in balance sheet whereas in P&L a/c, total amount of goods purchase will

be recorded resulting less net profit. However, on the other side, overdraft will be the part of short-

term liabilities and increase total cash balance under the head current assets. Whereas, interest

payment will be recorded as expenditures and at the same time, it will also decline net cash

position.

TASK 3

3.1

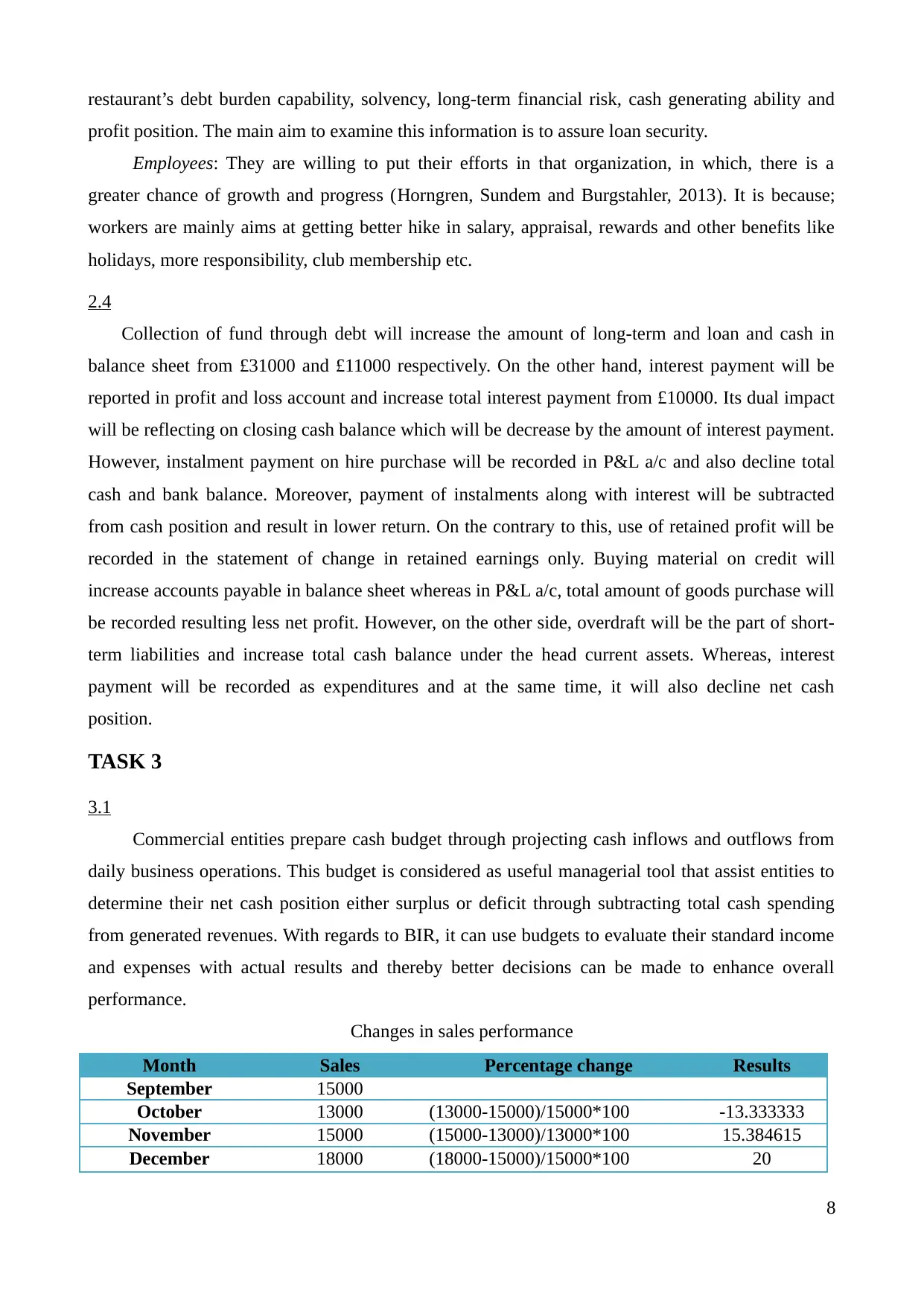

Commercial entities prepare cash budget through projecting cash inflows and outflows from

daily business operations. This budget is considered as useful managerial tool that assist entities to

determine their net cash position either surplus or deficit through subtracting total cash spending

from generated revenues. With regards to BIR, it can use budgets to evaluate their standard income

and expenses with actual results and thereby better decisions can be made to enhance overall

performance.

Changes in sales performance

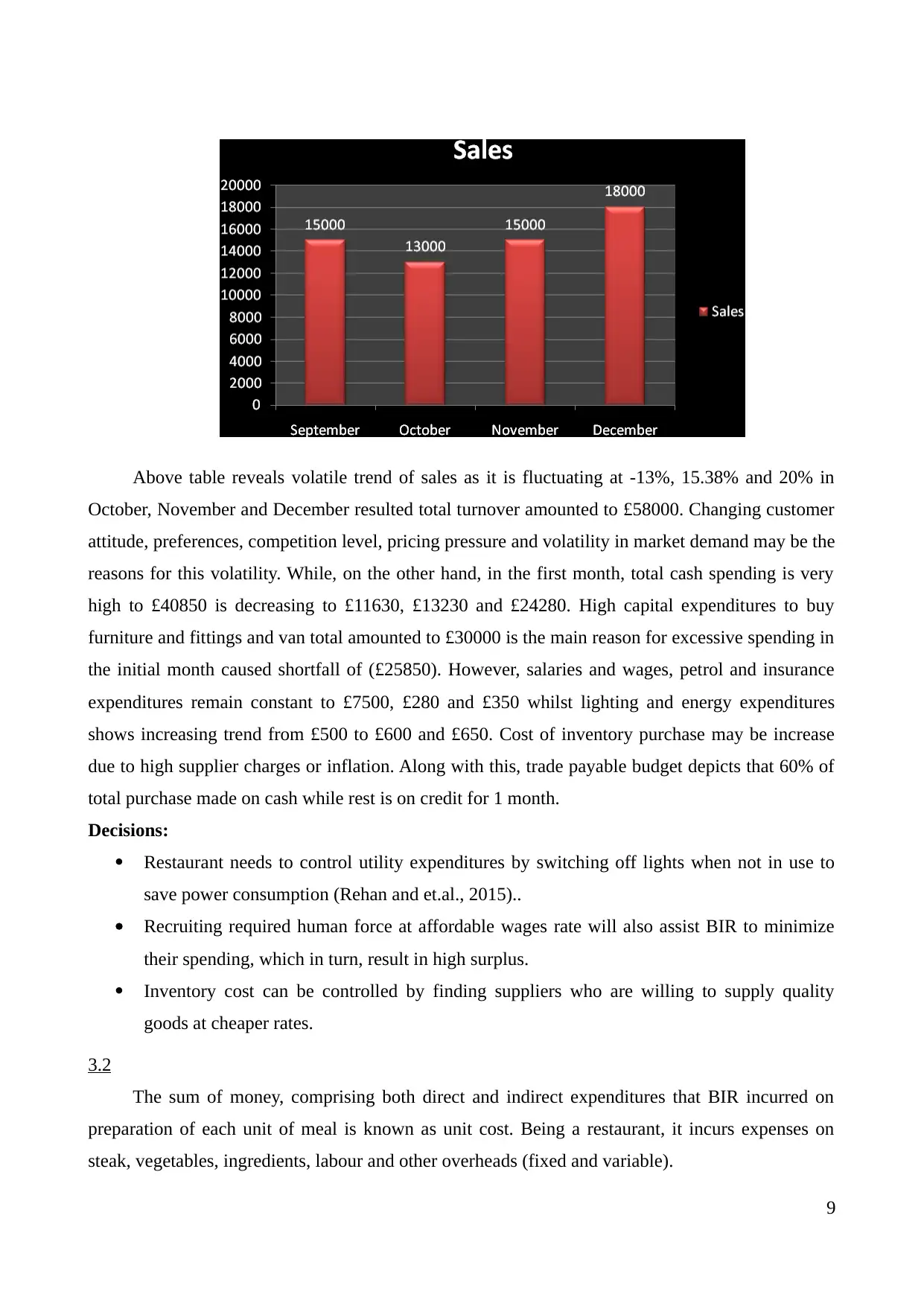

Month Sales Percentage change Results

September 15000

October 13000 (13000-15000)/15000*100 -13.333333

November 15000 (15000-13000)/13000*100 15.384615

December 18000 (18000-15000)/15000*100 20

8

profit position. The main aim to examine this information is to assure loan security.

Employees: They are willing to put their efforts in that organization, in which, there is a

greater chance of growth and progress (Horngren, Sundem and Burgstahler, 2013). It is because;

workers are mainly aims at getting better hike in salary, appraisal, rewards and other benefits like

holidays, more responsibility, club membership etc.

2.4

Collection of fund through debt will increase the amount of long-term and loan and cash in

balance sheet from £31000 and £11000 respectively. On the other hand, interest payment will be

reported in profit and loss account and increase total interest payment from £10000. Its dual impact

will be reflecting on closing cash balance which will be decrease by the amount of interest payment.

However, instalment payment on hire purchase will be recorded in P&L a/c and also decline total

cash and bank balance. Moreover, payment of instalments along with interest will be subtracted

from cash position and result in lower return. On the contrary to this, use of retained profit will be

recorded in the statement of change in retained earnings only. Buying material on credit will

increase accounts payable in balance sheet whereas in P&L a/c, total amount of goods purchase will

be recorded resulting less net profit. However, on the other side, overdraft will be the part of short-

term liabilities and increase total cash balance under the head current assets. Whereas, interest

payment will be recorded as expenditures and at the same time, it will also decline net cash

position.

TASK 3

3.1

Commercial entities prepare cash budget through projecting cash inflows and outflows from

daily business operations. This budget is considered as useful managerial tool that assist entities to

determine their net cash position either surplus or deficit through subtracting total cash spending

from generated revenues. With regards to BIR, it can use budgets to evaluate their standard income

and expenses with actual results and thereby better decisions can be made to enhance overall

performance.

Changes in sales performance

Month Sales Percentage change Results

September 15000

October 13000 (13000-15000)/15000*100 -13.333333

November 15000 (15000-13000)/13000*100 15.384615

December 18000 (18000-15000)/15000*100 20

8

Above table reveals volatile trend of sales as it is fluctuating at -13%, 15.38% and 20% in

October, November and December resulted total turnover amounted to £58000. Changing customer

attitude, preferences, competition level, pricing pressure and volatility in market demand may be the

reasons for this volatility. While, on the other hand, in the first month, total cash spending is very

high to £40850 is decreasing to £11630, £13230 and £24280. High capital expenditures to buy

furniture and fittings and van total amounted to £30000 is the main reason for excessive spending in

the initial month caused shortfall of (£25850). However, salaries and wages, petrol and insurance

expenditures remain constant to £7500, £280 and £350 whilst lighting and energy expenditures

shows increasing trend from £500 to £600 and £650. Cost of inventory purchase may be increase

due to high supplier charges or inflation. Along with this, trade payable budget depicts that 60% of

total purchase made on cash while rest is on credit for 1 month.

Decisions:

Restaurant needs to control utility expenditures by switching off lights when not in use to

save power consumption (Rehan and et.al., 2015)..

Recruiting required human force at affordable wages rate will also assist BIR to minimize

their spending, which in turn, result in high surplus.

Inventory cost can be controlled by finding suppliers who are willing to supply quality

goods at cheaper rates.

3.2

The sum of money, comprising both direct and indirect expenditures that BIR incurred on

preparation of each unit of meal is known as unit cost. Being a restaurant, it incurs expenses on

steak, vegetables, ingredients, labour and other overheads (fixed and variable).

9

October, November and December resulted total turnover amounted to £58000. Changing customer

attitude, preferences, competition level, pricing pressure and volatility in market demand may be the

reasons for this volatility. While, on the other hand, in the first month, total cash spending is very

high to £40850 is decreasing to £11630, £13230 and £24280. High capital expenditures to buy

furniture and fittings and van total amounted to £30000 is the main reason for excessive spending in

the initial month caused shortfall of (£25850). However, salaries and wages, petrol and insurance

expenditures remain constant to £7500, £280 and £350 whilst lighting and energy expenditures

shows increasing trend from £500 to £600 and £650. Cost of inventory purchase may be increase

due to high supplier charges or inflation. Along with this, trade payable budget depicts that 60% of

total purchase made on cash while rest is on credit for 1 month.

Decisions:

Restaurant needs to control utility expenditures by switching off lights when not in use to

save power consumption (Rehan and et.al., 2015)..

Recruiting required human force at affordable wages rate will also assist BIR to minimize

their spending, which in turn, result in high surplus.

Inventory cost can be controlled by finding suppliers who are willing to supply quality

goods at cheaper rates.

3.2

The sum of money, comprising both direct and indirect expenditures that BIR incurred on

preparation of each unit of meal is known as unit cost. Being a restaurant, it incurs expenses on

steak, vegetables, ingredients, labour and other overheads (fixed and variable).

9

Total cost (TC) = Direct cost (DC) + Indirect cost (IC)

Unit cost computation is also necessary to determine the selling price. In the cost-oriented,

also called cost-centric approach, BIR can add an appropriate profit mark-up in their total cost and

determine net selling price, computed below:

Items Cost (£)

Steak 3

Vegetables and other ingredients 1.5

Labor 3.5

Overheads 2

Meal cost 10

Value Added Tax 2

Mark-up 4

Selling price 16

Food cost % = (Total cost / Selling price)*100

= (10/16)*100

= 62.5%

According to the table, it can be seen that cost per unit of meal is £10 and at 40% mark-up

and 20% VAT, selling price will be £16. While, on the other hand, its cost percentage on sales price

is 62.5%.

3.3

Many-times, businesses have to make capital investment in fixed assets such as acquisition of

machinery, plant and building and advanced technology etc. Every capital projects is associated

with both the risk and return, therefore, it is important for the companies to examine potential return

of all the projects and thereby determine the most suitable ones (Dellavigna and Pollet, 2013).

According to the scenario, BIR available an empty space in its one branch which it can use to

expand the production of ready meals supplied to local supermarkets. In this respect, two projects

are available to the restaurant, both are mutually-exclusive but BIR can adopt only one of these.

Thus, it becomes essential for the restaurant to determine the best project through applying various

investment appraisal techniques, done below:

Payback period: It refers to the length of time which BIR requires to get back initial cash

outlay worth £1200 through generating cash flows over the project life. The best benefit of this

method is to it helps to identify the time lag in which project cost can be recovered ( Bierman and

Smidt, 2012). However, on the other side, it does not pay attention to the time value of money and

also do not consider cash flows beyond payback period (PP). As per this method, shorter PP is

considered suitable and highly preferred by others.

10

Unit cost computation is also necessary to determine the selling price. In the cost-oriented,

also called cost-centric approach, BIR can add an appropriate profit mark-up in their total cost and

determine net selling price, computed below:

Items Cost (£)

Steak 3

Vegetables and other ingredients 1.5

Labor 3.5

Overheads 2

Meal cost 10

Value Added Tax 2

Mark-up 4

Selling price 16

Food cost % = (Total cost / Selling price)*100

= (10/16)*100

= 62.5%

According to the table, it can be seen that cost per unit of meal is £10 and at 40% mark-up

and 20% VAT, selling price will be £16. While, on the other hand, its cost percentage on sales price

is 62.5%.

3.3

Many-times, businesses have to make capital investment in fixed assets such as acquisition of

machinery, plant and building and advanced technology etc. Every capital projects is associated

with both the risk and return, therefore, it is important for the companies to examine potential return

of all the projects and thereby determine the most suitable ones (Dellavigna and Pollet, 2013).

According to the scenario, BIR available an empty space in its one branch which it can use to

expand the production of ready meals supplied to local supermarkets. In this respect, two projects

are available to the restaurant, both are mutually-exclusive but BIR can adopt only one of these.

Thus, it becomes essential for the restaurant to determine the best project through applying various

investment appraisal techniques, done below:

Payback period: It refers to the length of time which BIR requires to get back initial cash

outlay worth £1200 through generating cash flows over the project life. The best benefit of this

method is to it helps to identify the time lag in which project cost can be recovered ( Bierman and

Smidt, 2012). However, on the other side, it does not pay attention to the time value of money and

also do not consider cash flows beyond payback period (PP). As per this method, shorter PP is

considered suitable and highly preferred by others.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Year Proposal 1 Cumulative cash

flows

Proposal

2

Cumulative cash

flows

1 800 800 300 300

2 600 1400 500 800

3 400 1800 600 1400

4 200 2000 600 2000

5 50 2050 500 2500

Residual value Nil 2050 50 2550

PP (A) = 1 year + (£1200 - £800)/ £600

= 1.67 year

PP (B) = 2 year + (£1200-£800)/ £600

= 2.67 year

Net present value: This method use discounting to determine the present value of forecasted

cash flows over the future period. It is because; NPV believes that having today a sum of money is

worth more than receiving the amount in future due to inflation (Grob, 2013). Thus, this capital

budgeting technique makes use of an appropriate discounting factor to identify the present value of

projected cash flows and subtract the total of it to find out the NPV. As per the method, project that

has highest NPV is considered the most viable (Andor, Mohanty and Toth, 2015).

Year Proposal

1

Proposal

2

Discounting

factor

Present value

(A)

Present value

(B)

1 800 300 0.9091 727.2727 272.7273

2 600 500 0.8264 495.8678 413.2231

3 400 600 0.7513 300.5259 450.7889

4 200 600 0.6830 136.6027 409.8081

5 50 500 0.6209 31.0461 310.4607

Residual

value

0 50 0.6209 0.0000 31.0461

Total present value 1691.3152 1888.0541

Initial investment 1200 1200

Net present value 491.3152 688.0541

Recommendation:

By taking into account derived output, it can be seen that payback period of proposal 1 is

comparatively less to 1.67 year whereas NPV is higher in another proposal to £688.0541 which

indicates that project B has greater chance of more return in future period. BIR can be advised to

accept 2nd proposal because NPV is considered as best technique which provides more realistic

results about net project yield. Thus, by investing amount worth £1200 in this proposal, restaurant

can gain maximum return of £688.0541.

11

flows

Proposal

2

Cumulative cash

flows

1 800 800 300 300

2 600 1400 500 800

3 400 1800 600 1400

4 200 2000 600 2000

5 50 2050 500 2500

Residual value Nil 2050 50 2550

PP (A) = 1 year + (£1200 - £800)/ £600

= 1.67 year

PP (B) = 2 year + (£1200-£800)/ £600

= 2.67 year

Net present value: This method use discounting to determine the present value of forecasted

cash flows over the future period. It is because; NPV believes that having today a sum of money is

worth more than receiving the amount in future due to inflation (Grob, 2013). Thus, this capital

budgeting technique makes use of an appropriate discounting factor to identify the present value of

projected cash flows and subtract the total of it to find out the NPV. As per the method, project that

has highest NPV is considered the most viable (Andor, Mohanty and Toth, 2015).

Year Proposal

1

Proposal

2

Discounting

factor

Present value

(A)

Present value

(B)

1 800 300 0.9091 727.2727 272.7273

2 600 500 0.8264 495.8678 413.2231

3 400 600 0.7513 300.5259 450.7889

4 200 600 0.6830 136.6027 409.8081

5 50 500 0.6209 31.0461 310.4607

Residual

value

0 50 0.6209 0.0000 31.0461

Total present value 1691.3152 1888.0541

Initial investment 1200 1200

Net present value 491.3152 688.0541

Recommendation:

By taking into account derived output, it can be seen that payback period of proposal 1 is

comparatively less to 1.67 year whereas NPV is higher in another proposal to £688.0541 which

indicates that project B has greater chance of more return in future period. BIR can be advised to

accept 2nd proposal because NPV is considered as best technique which provides more realistic

results about net project yield. Thus, by investing amount worth £1200 in this proposal, restaurant

can gain maximum return of £688.0541.

11

TASK 4

4.1

Every business entity needs to measure their operational success timely so that they can

examine their strength and weakness as well. Moreover, financial statements also deliver credible

and valuable information to various stakeholders like investors, creditors and lenders.

Statement of comprehensive income (SOCI): It is also called profitability statement, in which,

information has been recorded about routine business expenditures and revenues, prepared on

accrual accounting concept. The main objective of SOCI is to determine gross profit and net profit

of the business, calculated through using following formula:

Gross profit = Turnover – Cost of goods sold

Net profit = Total revenues – Total expenditures

Statement of financial position (SOFP): BIR and SMR needs to prepare balance sheet at the

end of every accounting year, in this, entity record their assets as well as liabilities (Deegan, 2013).

This statement is of huge importance to determine the financial position or strength by examining

solvency and, liquidity position.

Assets = Liabilities + Owner’s capital

Owner’s capital = Assets – Liabilities

Statement of cash flows (SOCF): SOCI records income and spending on accrual concept

whereas SOCF take into account only cash inflows and outflows from operating (routine

functioning), investing (purchase and disposal of fixed assets) and financial activities (collection

and repayment of debt and equity capital) (Edwards, 2013). Restaurant can prepare this statement to

determine the reasons for having distinguished cash funds at the end of two different financial

years.

4.2

With regards to preparation of financial statements, there is not high level of legal

compulsion on sole trader and partnership organizations. Sole trader contributed their own capital,

do business himself/herself and gained profit or loss through operations. They prepare SOCI, SOFP

and SOCF by taking into account UK Generally Accepted Accounted Principles (GAAP) and

conventions. While, on the other hand, in partnership, all partner’s contributed their money and run

operations by putting their combined efforts. Moreover, they receive interest on capital (IOC) as a

return for their money invested. These organizations prepare profit and loss appropriation account

to share total business profit among all in decided ratio whilst capital account is prepared to

determine the capital contribution of each partner (Deegan, 2013). They follow UK GAAP,

12

4.1

Every business entity needs to measure their operational success timely so that they can

examine their strength and weakness as well. Moreover, financial statements also deliver credible

and valuable information to various stakeholders like investors, creditors and lenders.

Statement of comprehensive income (SOCI): It is also called profitability statement, in which,

information has been recorded about routine business expenditures and revenues, prepared on

accrual accounting concept. The main objective of SOCI is to determine gross profit and net profit

of the business, calculated through using following formula:

Gross profit = Turnover – Cost of goods sold

Net profit = Total revenues – Total expenditures

Statement of financial position (SOFP): BIR and SMR needs to prepare balance sheet at the

end of every accounting year, in this, entity record their assets as well as liabilities (Deegan, 2013).

This statement is of huge importance to determine the financial position or strength by examining

solvency and, liquidity position.

Assets = Liabilities + Owner’s capital

Owner’s capital = Assets – Liabilities

Statement of cash flows (SOCF): SOCI records income and spending on accrual concept

whereas SOCF take into account only cash inflows and outflows from operating (routine

functioning), investing (purchase and disposal of fixed assets) and financial activities (collection

and repayment of debt and equity capital) (Edwards, 2013). Restaurant can prepare this statement to

determine the reasons for having distinguished cash funds at the end of two different financial

years.

4.2

With regards to preparation of financial statements, there is not high level of legal

compulsion on sole trader and partnership organizations. Sole trader contributed their own capital,

do business himself/herself and gained profit or loss through operations. They prepare SOCI, SOFP

and SOCF by taking into account UK Generally Accepted Accounted Principles (GAAP) and

conventions. While, on the other hand, in partnership, all partner’s contributed their money and run

operations by putting their combined efforts. Moreover, they receive interest on capital (IOC) as a

return for their money invested. These organizations prepare profit and loss appropriation account

to share total business profit among all in decided ratio whilst capital account is prepared to

determine the capital contribution of each partner (Deegan, 2013). They follow UK GAAP,

12

accounting concepts and principles along with partnership act legislations. Besides this, large sized

companies do operations at wider scale and also have number of internal as well as external

stakeholders. They are legally liable to comply with Company Act, 2006, UK GAAP, International

Accounting Standard (IAS) and International Financial Reporting Standard (IFRS) (Pratt, 2013).

Through complying with all the laws and regulations, it can deliver credible and authentic

information to the users. Along with this, CA, 2006 also impose legal obligations to the companies

to verify their accuracy of financial statements through an independent auditor to communicate

information about their financial position to bank, investors and taxation authority.

4.3

In the actual market place, companies not only need to prepare their annual accounts but also

require evaluating and comparing their own performance with that of competitors so that more

qualitative decisions can be taken. Ratio analysis is an effectual way to compare financial strength

and operational results both internally and externally, done here as under:

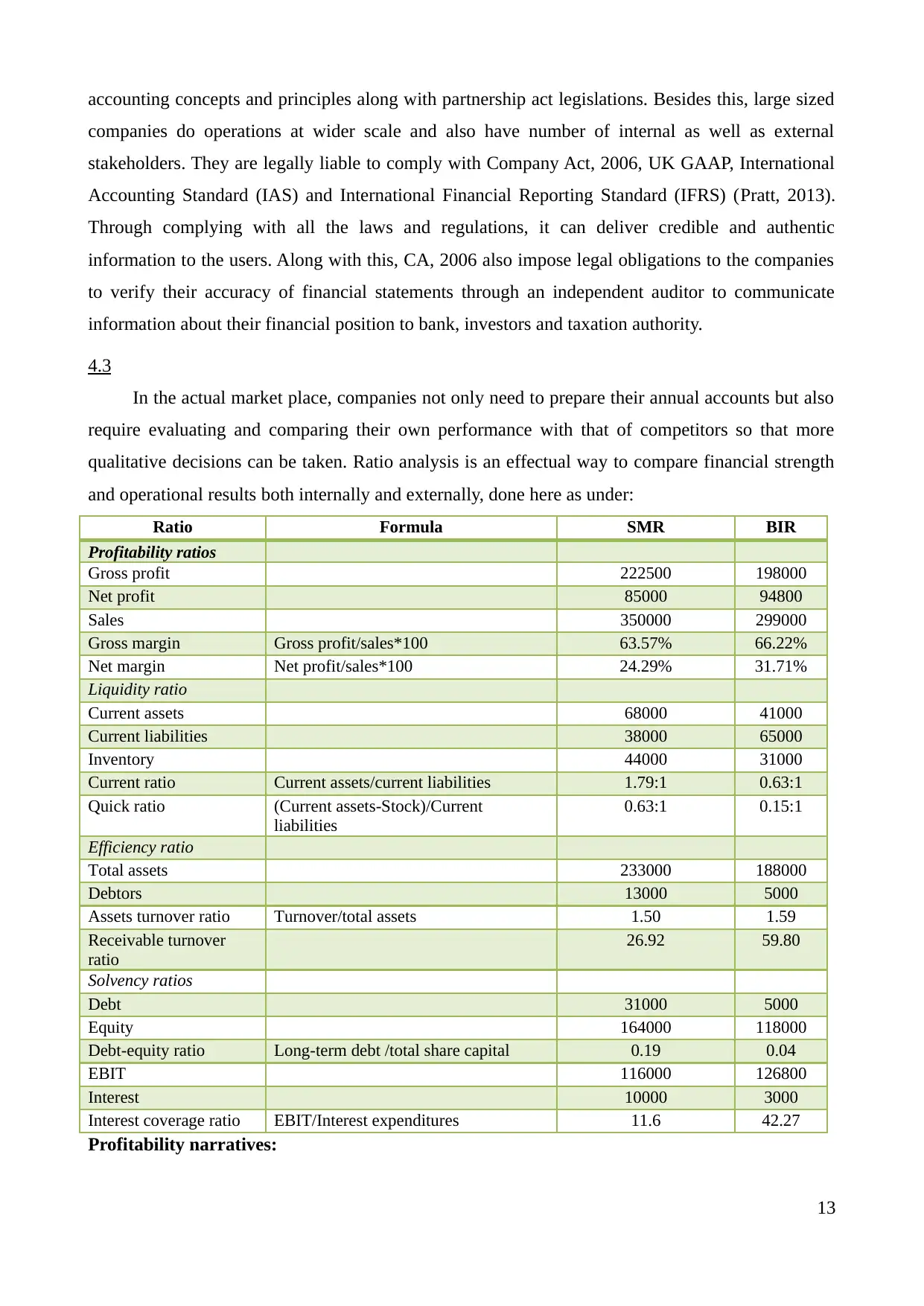

Ratio Formula SMR BIR

Profitability ratios

Gross profit 222500 198000

Net profit 85000 94800

Sales 350000 299000

Gross margin Gross profit/sales*100 63.57% 66.22%

Net margin Net profit/sales*100 24.29% 31.71%

Liquidity ratio

Current assets 68000 41000

Current liabilities 38000 65000

Inventory 44000 31000

Current ratio Current assets/current liabilities 1.79:1 0.63:1

Quick ratio (Current assets-Stock)/Current

liabilities

0.63:1 0.15:1

Efficiency ratio

Total assets 233000 188000

Debtors 13000 5000

Assets turnover ratio Turnover/total assets 1.50 1.59

Receivable turnover

ratio

26.92 59.80

Solvency ratios

Debt 31000 5000

Equity 164000 118000

Debt-equity ratio Long-term debt /total share capital 0.19 0.04

EBIT 116000 126800

Interest 10000 3000

Interest coverage ratio EBIT/Interest expenditures 11.6 42.27

Profitability narratives:

13

companies do operations at wider scale and also have number of internal as well as external

stakeholders. They are legally liable to comply with Company Act, 2006, UK GAAP, International

Accounting Standard (IAS) and International Financial Reporting Standard (IFRS) (Pratt, 2013).

Through complying with all the laws and regulations, it can deliver credible and authentic

information to the users. Along with this, CA, 2006 also impose legal obligations to the companies

to verify their accuracy of financial statements through an independent auditor to communicate

information about their financial position to bank, investors and taxation authority.

4.3

In the actual market place, companies not only need to prepare their annual accounts but also

require evaluating and comparing their own performance with that of competitors so that more

qualitative decisions can be taken. Ratio analysis is an effectual way to compare financial strength

and operational results both internally and externally, done here as under:

Ratio Formula SMR BIR

Profitability ratios

Gross profit 222500 198000

Net profit 85000 94800

Sales 350000 299000

Gross margin Gross profit/sales*100 63.57% 66.22%

Net margin Net profit/sales*100 24.29% 31.71%

Liquidity ratio

Current assets 68000 41000

Current liabilities 38000 65000

Inventory 44000 31000

Current ratio Current assets/current liabilities 1.79:1 0.63:1

Quick ratio (Current assets-Stock)/Current

liabilities

0.63:1 0.15:1

Efficiency ratio

Total assets 233000 188000

Debtors 13000 5000

Assets turnover ratio Turnover/total assets 1.50 1.59

Receivable turnover

ratio

26.92 59.80

Solvency ratios

Debt 31000 5000

Equity 164000 118000

Debt-equity ratio Long-term debt /total share capital 0.19 0.04

EBIT 116000 126800

Interest 10000 3000

Interest coverage ratio EBIT/Interest expenditures 11.6 42.27

Profitability narratives:

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

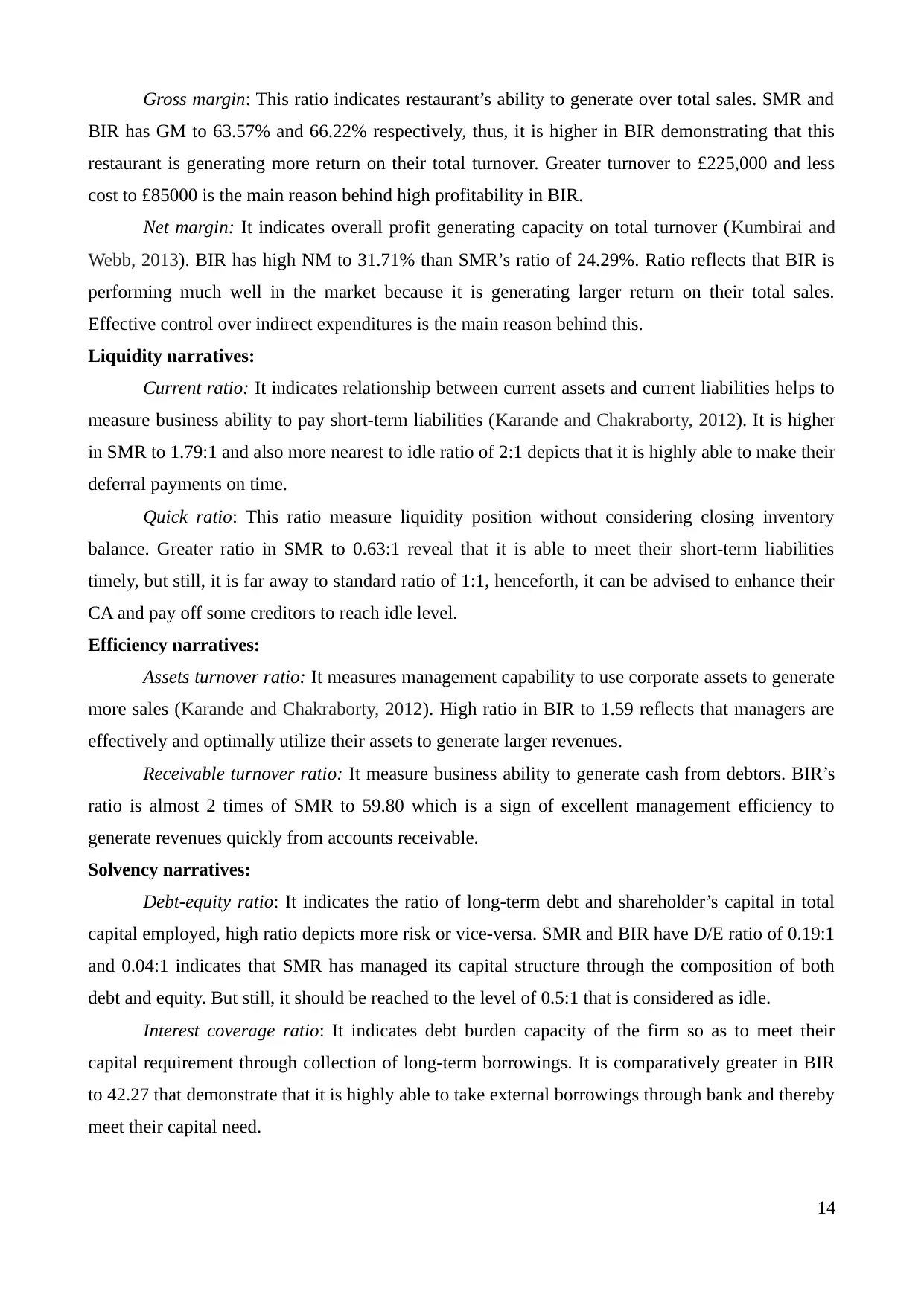

Gross margin: This ratio indicates restaurant’s ability to generate over total sales. SMR and

BIR has GM to 63.57% and 66.22% respectively, thus, it is higher in BIR demonstrating that this

restaurant is generating more return on their total turnover. Greater turnover to £225,000 and less

cost to £85000 is the main reason behind high profitability in BIR.

Net margin: It indicates overall profit generating capacity on total turnover (Kumbirai and

Webb, 2013). BIR has high NM to 31.71% than SMR’s ratio of 24.29%. Ratio reflects that BIR is

performing much well in the market because it is generating larger return on their total sales.

Effective control over indirect expenditures is the main reason behind this.

Liquidity narratives:

Current ratio: It indicates relationship between current assets and current liabilities helps to

measure business ability to pay short-term liabilities (Karande and Chakraborty, 2012). It is higher

in SMR to 1.79:1 and also more nearest to idle ratio of 2:1 depicts that it is highly able to make their

deferral payments on time.

Quick ratio: This ratio measure liquidity position without considering closing inventory

balance. Greater ratio in SMR to 0.63:1 reveal that it is able to meet their short-term liabilities

timely, but still, it is far away to standard ratio of 1:1, henceforth, it can be advised to enhance their

CA and pay off some creditors to reach idle level.

Efficiency narratives:

Assets turnover ratio: It measures management capability to use corporate assets to generate

more sales (Karande and Chakraborty, 2012). High ratio in BIR to 1.59 reflects that managers are

effectively and optimally utilize their assets to generate larger revenues.

Receivable turnover ratio: It measure business ability to generate cash from debtors. BIR’s

ratio is almost 2 times of SMR to 59.80 which is a sign of excellent management efficiency to

generate revenues quickly from accounts receivable.

Solvency narratives:

Debt-equity ratio: It indicates the ratio of long-term debt and shareholder’s capital in total

capital employed, high ratio depicts more risk or vice-versa. SMR and BIR have D/E ratio of 0.19:1

and 0.04:1 indicates that SMR has managed its capital structure through the composition of both

debt and equity. But still, it should be reached to the level of 0.5:1 that is considered as idle.

Interest coverage ratio: It indicates debt burden capacity of the firm so as to meet their

capital requirement through collection of long-term borrowings. It is comparatively greater in BIR

to 42.27 that demonstrate that it is highly able to take external borrowings through bank and thereby

meet their capital need.

14

BIR has GM to 63.57% and 66.22% respectively, thus, it is higher in BIR demonstrating that this

restaurant is generating more return on their total turnover. Greater turnover to £225,000 and less

cost to £85000 is the main reason behind high profitability in BIR.

Net margin: It indicates overall profit generating capacity on total turnover (Kumbirai and

Webb, 2013). BIR has high NM to 31.71% than SMR’s ratio of 24.29%. Ratio reflects that BIR is

performing much well in the market because it is generating larger return on their total sales.

Effective control over indirect expenditures is the main reason behind this.

Liquidity narratives:

Current ratio: It indicates relationship between current assets and current liabilities helps to

measure business ability to pay short-term liabilities (Karande and Chakraborty, 2012). It is higher

in SMR to 1.79:1 and also more nearest to idle ratio of 2:1 depicts that it is highly able to make their

deferral payments on time.

Quick ratio: This ratio measure liquidity position without considering closing inventory

balance. Greater ratio in SMR to 0.63:1 reveal that it is able to meet their short-term liabilities

timely, but still, it is far away to standard ratio of 1:1, henceforth, it can be advised to enhance their

CA and pay off some creditors to reach idle level.

Efficiency narratives:

Assets turnover ratio: It measures management capability to use corporate assets to generate

more sales (Karande and Chakraborty, 2012). High ratio in BIR to 1.59 reflects that managers are

effectively and optimally utilize their assets to generate larger revenues.

Receivable turnover ratio: It measure business ability to generate cash from debtors. BIR’s

ratio is almost 2 times of SMR to 59.80 which is a sign of excellent management efficiency to

generate revenues quickly from accounts receivable.

Solvency narratives:

Debt-equity ratio: It indicates the ratio of long-term debt and shareholder’s capital in total

capital employed, high ratio depicts more risk or vice-versa. SMR and BIR have D/E ratio of 0.19:1

and 0.04:1 indicates that SMR has managed its capital structure through the composition of both

debt and equity. But still, it should be reached to the level of 0.5:1 that is considered as idle.

Interest coverage ratio: It indicates debt burden capacity of the firm so as to meet their

capital requirement through collection of long-term borrowings. It is comparatively greater in BIR

to 42.27 that demonstrate that it is highly able to take external borrowings through bank and thereby

meet their capital need.

14

CONCLUSION

After evaluating the report, it can be concluded that debt fund and retained profit are identified

the most suitable and appropriate source for funding SMR’s expansion plan. Moreover, report

identified the fact that budgeting is of huge importance for the financial planners to administrate

and effectively manage their money-related activities. While, application of project evaluation

methods identified 2nd proposed more viable, hence, BIR must invest funds in this project. At the

end, comparative evaluation of financial performance of SMR and BIR examined that BIR is

performing much well in the market whereas liquidity and solvency position of SMR is much better

reflected that it is able to pay their creditors and lenders on right time.

15

After evaluating the report, it can be concluded that debt fund and retained profit are identified

the most suitable and appropriate source for funding SMR’s expansion plan. Moreover, report

identified the fact that budgeting is of huge importance for the financial planners to administrate

and effectively manage their money-related activities. While, application of project evaluation

methods identified 2nd proposed more viable, hence, BIR must invest funds in this project. At the

end, comparative evaluation of financial performance of SMR and BIR examined that BIR is

performing much well in the market whereas liquidity and solvency position of SMR is much better

reflected that it is able to pay their creditors and lenders on right time.

15

REFERENCES

Books and Journals

Andor, G., Mohanty, S. K. and Toth, T., 2015. Capital budgeting practices: a survey of Central and

Eastern European firms. Emerging Markets Review. 23(3). pp. 148-172.

Arrondel, L., Debbich, M. and Savignac, F., 2014. Financial literacy and financial planning in

France.

Berger, A. N. and Black, L. K., 2011. Bank size, lending technologies, and small business

finance. Journal of Banking & Finance. 35(3). pp.724-735.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Brandimarte, P., 2013. Numerical methods in finance and economics: a MATLAB-based

introduction. John Wiley & Sons.

Brigham, E. and Ehrhardt, M., 2013. Financial management: Theory & practice. Cengage

Learning.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Dellavigna, S. and Pollet, J. M., 2013. Capital budgeting versus market timing: An evaluation using

demographics. The Journal of Finance. 68(1). pp. 237-270.

Dhaliwal, D. and et.al., 2014. Corporate social responsibility disclosure and the cost of equity

capital: The roles of stakeholder orientation and financial transparency. Journal of Accounting

and Public Policy. 33(4). pp. 328-355.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Grob, H. L., 2013. Capital budgeting with financial plans: an introduction. Springer-Verlag.

Guariglia, A., Liu, X. and Song, L., 2011. Internal finance and growth: microeconometric evidence

on Chinese firms. Journal of Development Economics. 96(1). pp.79-94.

Horngren, C. T., Sundem, G. L., and Burgstahler, D., 2013. Introduction to management accounting.

Pearson Higher Ed.

Jackson, S. B., Keune, T. M. and Salzsieder, L., 2013. Debt, equity, and capital investment. Journal

of Accounting and Economics. 56(2). pp. 291-310.

Karande, P. and Chakraborty, S., 2012. Application of multi-objective optimization on the basis of

ratio analysis (MOORA) method for materials selection. Materials & Design. 37(3). pp.317-

324.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank performance in

South Africa. African Review of Economics and Finance. 2(1). pp. 30-53.

16

Books and Journals

Andor, G., Mohanty, S. K. and Toth, T., 2015. Capital budgeting practices: a survey of Central and

Eastern European firms. Emerging Markets Review. 23(3). pp. 148-172.

Arrondel, L., Debbich, M. and Savignac, F., 2014. Financial literacy and financial planning in

France.

Berger, A. N. and Black, L. K., 2011. Bank size, lending technologies, and small business

finance. Journal of Banking & Finance. 35(3). pp.724-735.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Brandimarte, P., 2013. Numerical methods in finance and economics: a MATLAB-based

introduction. John Wiley & Sons.

Brigham, E. and Ehrhardt, M., 2013. Financial management: Theory & practice. Cengage

Learning.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Dellavigna, S. and Pollet, J. M., 2013. Capital budgeting versus market timing: An evaluation using

demographics. The Journal of Finance. 68(1). pp. 237-270.

Dhaliwal, D. and et.al., 2014. Corporate social responsibility disclosure and the cost of equity

capital: The roles of stakeholder orientation and financial transparency. Journal of Accounting

and Public Policy. 33(4). pp. 328-355.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Grob, H. L., 2013. Capital budgeting with financial plans: an introduction. Springer-Verlag.

Guariglia, A., Liu, X. and Song, L., 2011. Internal finance and growth: microeconometric evidence

on Chinese firms. Journal of Development Economics. 96(1). pp.79-94.

Horngren, C. T., Sundem, G. L., and Burgstahler, D., 2013. Introduction to management accounting.

Pearson Higher Ed.

Jackson, S. B., Keune, T. M. and Salzsieder, L., 2013. Debt, equity, and capital investment. Journal

of Accounting and Economics. 56(2). pp. 291-310.

Karande, P. and Chakraborty, S., 2012. Application of multi-objective optimization on the basis of

ratio analysis (MOORA) method for materials selection. Materials & Design. 37(3). pp.317-

324.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank performance in

South Africa. African Review of Economics and Finance. 2(1). pp. 30-53.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Mutanda, M., De Beer, M. and Myers, G. T., 2014. The perception of small and micro enterprises in

the city of Durban Central Business District (CBD),(Kwazulu-Natal)(KZN) towards financial

planning. 14(2). pp. 16-24.

Poynton, T. A., Lapan, R. T. and Marcotte, A. M., 2015. Financial planning strategies of high school

seniors: Removing barriers to career success. The Career Development Quarterly. 63(1).

pp.57-73.

Pratt, J., 2013. Financial accounting in an economic context. Wiley Global Education.

Rehan, R. and et.al., 2015. Strategic Water Utility Management and Financial Planning Using a

New System Dynamics Tool (PDF). Journal-American Water Works Association. 107(1). pp.

E22-E36.

Vernimmen, P. and et.al., 2014.Corporate finance: theory and practice. John Wiley & Sons.

Online

Kumar, V., 2012. Unit cost in cost accounting. [Online]. Available through:

http://www.svtuition.org/2012/09/cost-unit-in-cost-accounting.html>. [Accessed on 21st

October 2016].

Toth, T., 2015. The Importance of Personal Financial Planning. 2015. [Online]. Available through:

<http://www.captivate-tips.com/financial_planning_imprtnc.php>. [Accessed on 5th December

2015].

17

the city of Durban Central Business District (CBD),(Kwazulu-Natal)(KZN) towards financial

planning. 14(2). pp. 16-24.

Poynton, T. A., Lapan, R. T. and Marcotte, A. M., 2015. Financial planning strategies of high school

seniors: Removing barriers to career success. The Career Development Quarterly. 63(1).

pp.57-73.

Pratt, J., 2013. Financial accounting in an economic context. Wiley Global Education.

Rehan, R. and et.al., 2015. Strategic Water Utility Management and Financial Planning Using a

New System Dynamics Tool (PDF). Journal-American Water Works Association. 107(1). pp.

E22-E36.

Vernimmen, P. and et.al., 2014.Corporate finance: theory and practice. John Wiley & Sons.

Online

Kumar, V., 2012. Unit cost in cost accounting. [Online]. Available through:

http://www.svtuition.org/2012/09/cost-unit-in-cost-accounting.html>. [Accessed on 21st

October 2016].

Toth, T., 2015. The Importance of Personal Financial Planning. 2015. [Online]. Available through:

<http://www.captivate-tips.com/financial_planning_imprtnc.php>. [Accessed on 5th December

2015].

17

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.