MANAGING FINANCIAL RESOURCES AND DECISON MAKING TABLE OF CONTENTS Task 13

20 Pages3797 Words267 Views

Added on 2019-12-03

About This Document

• Issue of debentures: Every business unit has an option to raise debentures for acquisition of funds.The debt fund helpsin acquisition of large amount of funds so as to meet its capital requirements for long-term.

MANAGING FINANCIAL RESOURCES AND DECISON MAKING TABLE OF CONTENTS Task 13

Added on 2019-12-03

ShareRelated Documents

MANAGING FINANCIAL

RESOURCES AND DECISON

MAKING

RESOURCES AND DECISON

MAKING

TABLE OF CONTENTS

Introduction ...............................................................................................................................3

Task 1.........................................................................................................................................3

1.1 Sources of finance available to Sweet Menu Restaurant Ltd. ........................................3

1.2 Implications of sources of finance ..................................................................................4

1.3 Appropriate sources of finance........................................................................................5

TASK 2 ....................................................................................................................................5

2.1 Cost of different sources of finance.................................................................................5

2.2 Importance of financial planning.....................................................................................5

2.3 Information needs of different decisions makers............................................................6

2.4 Impact of sources of finance on the firm financial statements........................................6

TASK 3......................................................................................................................................7

3.1 Analysis of budget...........................................................................................................7

3.2 Calculation of meal cost..................................................................................................8

3.3 Project evaluation techniques..........................................................................................8

TASK 4......................................................................................................................................9

4.1 Main financial statements................................................................................................9

4.2 Financial statements of different business.....................................................................10

4.3 Ratio analysis.................................................................................................................16

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................19

INDEX OF TABLES

Table 1: Implications of sources of finance...............................................................................4

Table 2: Income statement.........................................................................................................6

Table 3: Balance sheet as at 31 December, 2014.......................................................................7

Table 4: Analysis of budget........................................................................................................7

Table 5: Calculation of unit cost................................................................................................8

Table 6: Calculation of payback period.....................................................................................8

Table 7: Calculation of NPV......................................................................................................9

Table 8: Ratio analysis of Sweet menu and Blue Island restaurant.........................................16

Introduction ...............................................................................................................................3

Task 1.........................................................................................................................................3

1.1 Sources of finance available to Sweet Menu Restaurant Ltd. ........................................3

1.2 Implications of sources of finance ..................................................................................4

1.3 Appropriate sources of finance........................................................................................5

TASK 2 ....................................................................................................................................5

2.1 Cost of different sources of finance.................................................................................5

2.2 Importance of financial planning.....................................................................................5

2.3 Information needs of different decisions makers............................................................6

2.4 Impact of sources of finance on the firm financial statements........................................6

TASK 3......................................................................................................................................7

3.1 Analysis of budget...........................................................................................................7

3.2 Calculation of meal cost..................................................................................................8

3.3 Project evaluation techniques..........................................................................................8

TASK 4......................................................................................................................................9

4.1 Main financial statements................................................................................................9

4.2 Financial statements of different business.....................................................................10

4.3 Ratio analysis.................................................................................................................16

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................19

INDEX OF TABLES

Table 1: Implications of sources of finance...............................................................................4

Table 2: Income statement.........................................................................................................6

Table 3: Balance sheet as at 31 December, 2014.......................................................................7

Table 4: Analysis of budget........................................................................................................7

Table 5: Calculation of unit cost................................................................................................8

Table 6: Calculation of payback period.....................................................................................8

Table 7: Calculation of NPV......................................................................................................9

Table 8: Ratio analysis of Sweet menu and Blue Island restaurant.........................................16

INTRODUCTION

An efficient management of financial resources is considered to be highly important

for determining the success of an organization. It is essential for the business unit to

efficiently manage and administer the financial resources. The organization should conduct

an in-depth evaluation of various sources of finance so as to select the most suitable one.

Moreover, it is essential for the organization to judge the viability of various projects before

making investments into the same. The report proposed herewith emphasizes on identifying

ways through which financial resources are managed in an efficient manner within the

organization. It is through analysis of various cases that the monetary decisions within the

business unit are evaluated.

TASK 1

1.1 Sources of finance available to Sweet Menu Restaurant Ltd.

Sweet Menu restaurant ltd. is a reputed restaurant unit that is conducting its operations

at Gants Hills in East London. Management of the restaurant unit is planning to expand its

operations in Central London and Croydon. Henceforth, the organization requires additional

investment of £300,000 and £500,000. Different sources of finance are available with

business unit for the acquisition of required funds which are discussed underneath in detail.

Bank Loan: The restaurant can acquire required funds by availing bank loan facility.

The financing option helps in easy acquisition of funds on regular payments of

nominal interest amount (Adams, 2003). It is suitable for financing all kinds of

business requirements such as long-term, short-term and medium-term.

Issue of debentures: Every business unit has an option to raise debentures for

acquisition of funds. The debt fund helps in acquisition of large amount of funds for

required duration.

Issue of equity capital: The restaurant unit can issue equity shares so as to meet its

capital requirements for long-term. It is through issue of equity capital that the

business unit is able to acquire any amount of funds required to support operations

and expansion plans.

Retained earnings: It refers to the part of profit that remains after deducting all

expenses form the cash inflows of the business. This is an internal source of finance

and cost free in nature (Beddow and Cohen, 2003). Due to these roans every sort of

firm irrespective of its size uses this source of finance to fund its operations.

An efficient management of financial resources is considered to be highly important

for determining the success of an organization. It is essential for the business unit to

efficiently manage and administer the financial resources. The organization should conduct

an in-depth evaluation of various sources of finance so as to select the most suitable one.

Moreover, it is essential for the organization to judge the viability of various projects before

making investments into the same. The report proposed herewith emphasizes on identifying

ways through which financial resources are managed in an efficient manner within the

organization. It is through analysis of various cases that the monetary decisions within the

business unit are evaluated.

TASK 1

1.1 Sources of finance available to Sweet Menu Restaurant Ltd.

Sweet Menu restaurant ltd. is a reputed restaurant unit that is conducting its operations

at Gants Hills in East London. Management of the restaurant unit is planning to expand its

operations in Central London and Croydon. Henceforth, the organization requires additional

investment of £300,000 and £500,000. Different sources of finance are available with

business unit for the acquisition of required funds which are discussed underneath in detail.

Bank Loan: The restaurant can acquire required funds by availing bank loan facility.

The financing option helps in easy acquisition of funds on regular payments of

nominal interest amount (Adams, 2003). It is suitable for financing all kinds of

business requirements such as long-term, short-term and medium-term.

Issue of debentures: Every business unit has an option to raise debentures for

acquisition of funds. The debt fund helps in acquisition of large amount of funds for

required duration.

Issue of equity capital: The restaurant unit can issue equity shares so as to meet its

capital requirements for long-term. It is through issue of equity capital that the

business unit is able to acquire any amount of funds required to support operations

and expansion plans.

Retained earnings: It refers to the part of profit that remains after deducting all

expenses form the cash inflows of the business. This is an internal source of finance

and cost free in nature (Beddow and Cohen, 2003). Due to these roans every sort of

firm irrespective of its size uses this source of finance to fund its operations.

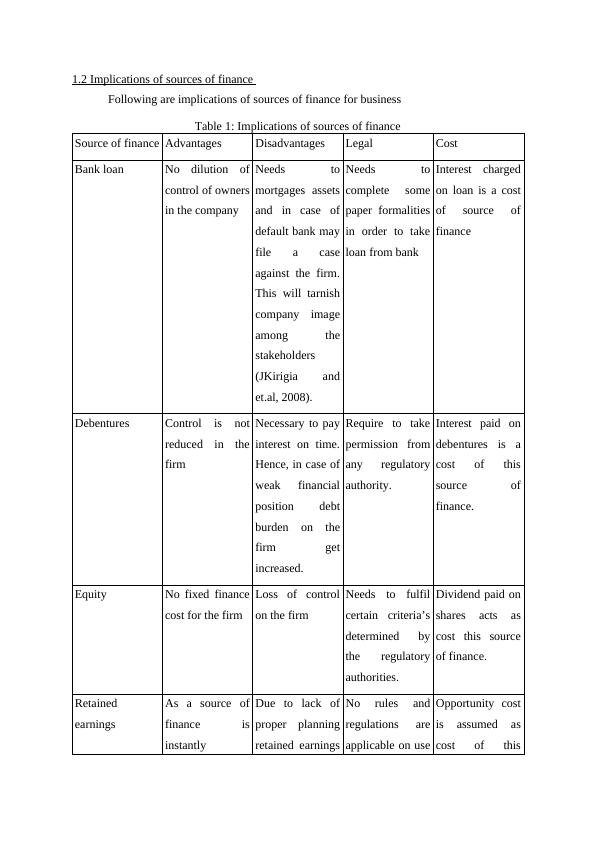

1.2 Implications of sources of finance

Following are implications of sources of finance for business

Table 1: Implications of sources of finance

Source of finance Advantages Disadvantages Legal Cost

Bank loan No dilution of

control of owners

in the company

Needs to

mortgages assets

and in case of

default bank may

file a case

against the firm.

This will tarnish

company image

among the

stakeholders

(JKirigia and

et.al, 2008).

Needs to

complete some

paper formalities

in order to take

loan from bank

Interest charged

on loan is a cost

of source of

finance

Debentures Control is not

reduced in the

firm

Necessary to pay

interest on time.

Hence, in case of

weak financial

position debt

burden on the

firm get

increased.

Require to take

permission from

any regulatory

authority.

Interest paid on

debentures is a

cost of this

source of

finance.

Equity No fixed finance

cost for the firm

Loss of control

on the firm

Needs to fulfil

certain criteria’s

determined by

the regulatory

authorities.

Dividend paid on

shares acts as

cost this source

of finance.

Retained

earnings

As a source of

finance is

instantly

Due to lack of

proper planning

retained earnings

No rules and

regulations are

applicable on use

Opportunity cost

is assumed as

cost of this

Following are implications of sources of finance for business

Table 1: Implications of sources of finance

Source of finance Advantages Disadvantages Legal Cost

Bank loan No dilution of

control of owners

in the company

Needs to

mortgages assets

and in case of

default bank may

file a case

against the firm.

This will tarnish

company image

among the

stakeholders

(JKirigia and

et.al, 2008).

Needs to

complete some

paper formalities

in order to take

loan from bank

Interest charged

on loan is a cost

of source of

finance

Debentures Control is not

reduced in the

firm

Necessary to pay

interest on time.

Hence, in case of

weak financial

position debt

burden on the

firm get

increased.

Require to take

permission from

any regulatory

authority.

Interest paid on

debentures is a

cost of this

source of

finance.

Equity No fixed finance

cost for the firm

Loss of control

on the firm

Needs to fulfil

certain criteria’s

determined by

the regulatory

authorities.

Dividend paid on

shares acts as

cost this source

of finance.

Retained

earnings

As a source of

finance is

instantly

Due to lack of

proper planning

retained earnings

No rules and

regulations are

applicable on use

Opportunity cost

is assumed as

cost of this

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Planning in Sweet Menu Restaurant Ltd | Reportlg...

|15

|4460

|438

MANAGING FINANCIAL RESORCES AND DECISION INTRODUCTIONlg...

|23

|5627

|386

(solved) Assignment Managing Financial resources and decisionslg...

|19

|5342

|33

Project Of Sweet Menu Restaurant - Sources Of Finance & Implicationslg...

|20

|6727

|96

Managing Financial Resources and Decisions | Projectlg...

|18

|5575

|47

(solved) Managing Financial Resources and Decisionslg...

|17

|5116

|74