Investment Appraisal for Victoria Babies Ltd - Report

VerifiedAdded on 2020/06/06

|11

|2644

|32

Report

AI Summary

This report provides a comprehensive analysis of investment appraisal techniques for Victoria Babies Ltd, focusing on the company's expansion plans. It explores four key techniques: payback period, Net Present Value (NPV), Accounting Rate of Return (ARR), and Internal Rate of Return (IRR), detailing their advantages, disadvantages, and applications. The report includes detailed calculations for three investment options: expanding the existing plant, building a new production plant in the UK, and international expansion to China. The findings reveal that building a new production plant in the UK is the most financially viable option, as it yields a positive NPV, a shorter payback period, and a higher IRR. The report concludes by recommending against the other two options based on their lower NPVs and longer payback periods, providing a clear financial strategy for Victoria Babies Ltd's expansion.

MFR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Appraisal techniques..............................................................................................................1

Application.............................................................................................................................4

Findings..................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

Appraisal techniques..............................................................................................................1

Application.............................................................................................................................4

Findings..................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Investment appraisal techniques are quite useful for assessing effectiveness and

attractiveness of new project of company in effectual way. The present report deals with Victoria

Babies Ltd which is planning for expansion. It has various investment options which is required

to be evaluated and best one is to be chosen. Four techniques are discussed such as payback

period, NPV, ARR, IRR listing out shortcomings and advantages of each of them. Moreover,

calculations of various appraisal techniques are also made to chose the best option among

various options available to company. The computations of all the appraisal techniques are made

and findings are imparted for selecting the best option to investment in by the company to yield

adequate returns.

Appraisal techniques

Investment appraisal techniques play vital role in the company to make better decisions

related to investment. Victoria Babies Ltd is planning for expansion in varied aspects. It is

essential for taking decision with the help of appraisal techniques. These include IRR (Internal

Rate of Return), NPV (Net Present Value), Payback period and ARR (Accounting Rate of

Return). These all techniques are discussed below-

Payback period

It shows recovery period of invested project. It is quite essential technique which

provides clarity about risk associated with project. This paves the way for company to opt in for

investment or not. Generally, shorter payback period is considered to be the best. This is because

investors get the returns within short span of time (Li and Trutnevyte, 2017).

Advantages

1. The main advantage of payback period is that it evaluates risk associated with the project.

2. Moreover, it provides clarity about when investment will yield desired returns.

3. Another advantage of this method is that it is simple to calculate and provide better results by

utilising time factor.

4. It is focused on risk factor of the project so that adequate returns can be generated with much

ease.

Disadvantages

1. There are shortcomings as well of this method.

1

Investment appraisal techniques are quite useful for assessing effectiveness and

attractiveness of new project of company in effectual way. The present report deals with Victoria

Babies Ltd which is planning for expansion. It has various investment options which is required

to be evaluated and best one is to be chosen. Four techniques are discussed such as payback

period, NPV, ARR, IRR listing out shortcomings and advantages of each of them. Moreover,

calculations of various appraisal techniques are also made to chose the best option among

various options available to company. The computations of all the appraisal techniques are made

and findings are imparted for selecting the best option to investment in by the company to yield

adequate returns.

Appraisal techniques

Investment appraisal techniques play vital role in the company to make better decisions

related to investment. Victoria Babies Ltd is planning for expansion in varied aspects. It is

essential for taking decision with the help of appraisal techniques. These include IRR (Internal

Rate of Return), NPV (Net Present Value), Payback period and ARR (Accounting Rate of

Return). These all techniques are discussed below-

Payback period

It shows recovery period of invested project. It is quite essential technique which

provides clarity about risk associated with project. This paves the way for company to opt in for

investment or not. Generally, shorter payback period is considered to be the best. This is because

investors get the returns within short span of time (Li and Trutnevyte, 2017).

Advantages

1. The main advantage of payback period is that it evaluates risk associated with the project.

2. Moreover, it provides clarity about when investment will yield desired returns.

3. Another advantage of this method is that it is simple to calculate and provide better results by

utilising time factor.

4. It is focused on risk factor of the project so that adequate returns can be generated with much

ease.

Disadvantages

1. There are shortcomings as well of this method.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. It ignores cash flows which occurs after computation of payback period. Furthermore, another

drawback of such method is that it ignores time value of money.

3. This is required to assess project and generate good results. Moreover, it leads to poor

investment decisions. Another disadvantage is that it does not consider profitability of the project

which leads to wrong results.

4. It does not take into account subsequent investments which is considered the biggest limitation

of the method (Laird and Venables, 2017.).

NPV

NPV is useful as it evaluates project on the basis of profitability aspect. NPV help to

assess project on the basis of difference of present value of cash inflows and outflows of project.

Victoria Babies Ltd can easily assess profitability of project whether to opt for expansion in

abroad or any other options. There are positive as well as negative cash flows. It is recommended

by market analysts that Higher the NPV, better for the company to invest in the project.

Advantages

1. The advantage of NPV is that it takes into account time value of money.

2. It aids in making effective decision as it rejects project having less NPV.

3. NPV aids in maximising organisation's value as higher NPV of project maximises

organisation's worth.

4. It takes into account all the cash flows over a life of the project.

Disadvantages

1. It is not suitable for the company as it is purely based on discounting rate.

2. This inculcates complexity which is the biggest limitation of using NPV.

3. NPV is merely based on forecasting and this leads to incomplete information and as such,

wrong decisions are made.

4. Another disadvantage of this method is that relying on discounting rate may result into forego

of better investment projects.

ARR

ARR is a capital investment technique which provides clarity about return on investment

made by the company (Mayer, Breun and Schultmann, 2017). It highlights effectiveness of

project on the basis of profitability. Basic evaluation can be made with reference to profitability

of the project. Moreover, it is useful for extracting results in the best possible way.

2

drawback of such method is that it ignores time value of money.

3. This is required to assess project and generate good results. Moreover, it leads to poor

investment decisions. Another disadvantage is that it does not consider profitability of the project

which leads to wrong results.

4. It does not take into account subsequent investments which is considered the biggest limitation

of the method (Laird and Venables, 2017.).

NPV

NPV is useful as it evaluates project on the basis of profitability aspect. NPV help to

assess project on the basis of difference of present value of cash inflows and outflows of project.

Victoria Babies Ltd can easily assess profitability of project whether to opt for expansion in

abroad or any other options. There are positive as well as negative cash flows. It is recommended

by market analysts that Higher the NPV, better for the company to invest in the project.

Advantages

1. The advantage of NPV is that it takes into account time value of money.

2. It aids in making effective decision as it rejects project having less NPV.

3. NPV aids in maximising organisation's value as higher NPV of project maximises

organisation's worth.

4. It takes into account all the cash flows over a life of the project.

Disadvantages

1. It is not suitable for the company as it is purely based on discounting rate.

2. This inculcates complexity which is the biggest limitation of using NPV.

3. NPV is merely based on forecasting and this leads to incomplete information and as such,

wrong decisions are made.

4. Another disadvantage of this method is that relying on discounting rate may result into forego

of better investment projects.

ARR

ARR is a capital investment technique which provides clarity about return on investment

made by the company (Mayer, Breun and Schultmann, 2017). It highlights effectiveness of

project on the basis of profitability. Basic evaluation can be made with reference to profitability

of the project. Moreover, it is useful for extracting results in the best possible way.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

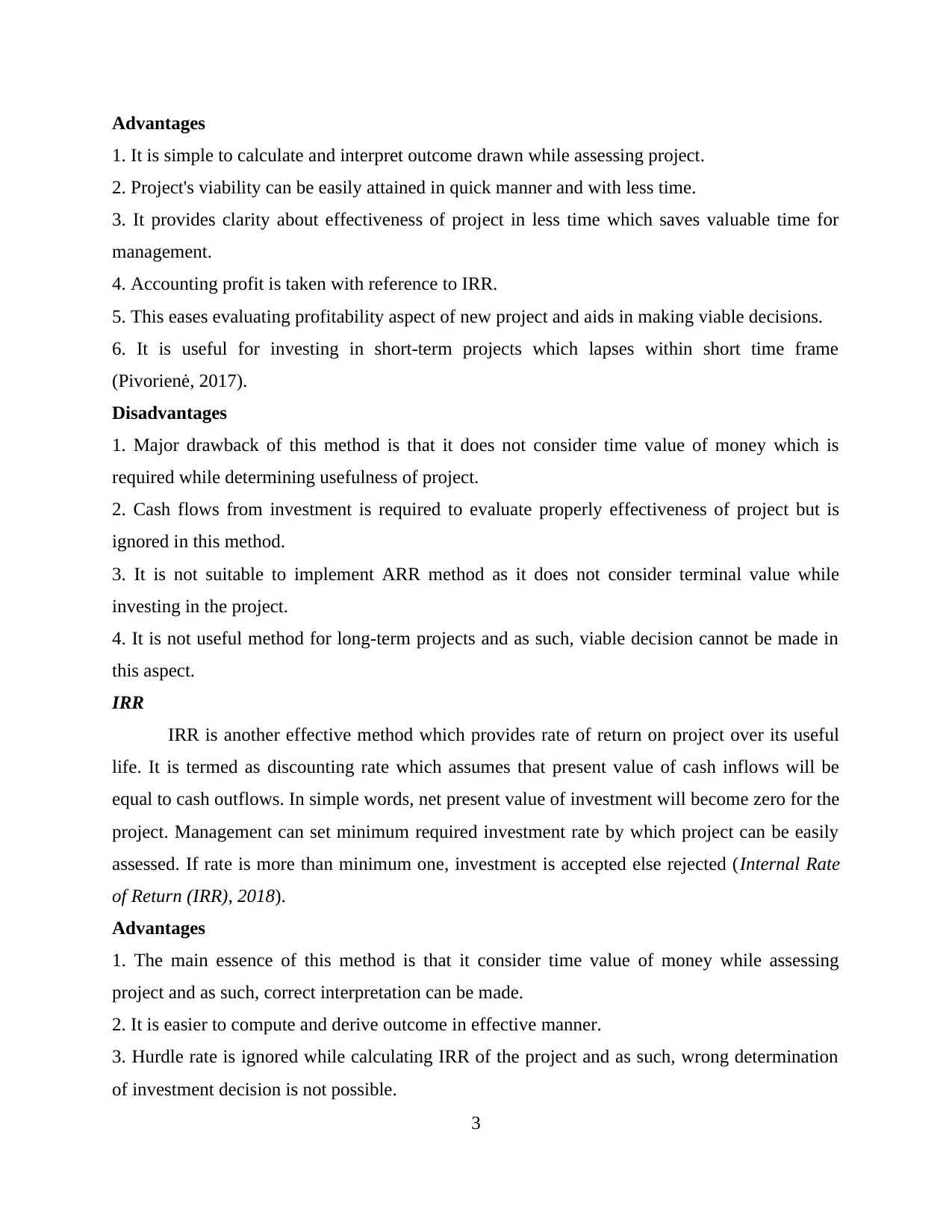

Advantages

1. It is simple to calculate and interpret outcome drawn while assessing project.

2. Project's viability can be easily attained in quick manner and with less time.

3. It provides clarity about effectiveness of project in less time which saves valuable time for

management.

4. Accounting profit is taken with reference to IRR.

5. This eases evaluating profitability aspect of new project and aids in making viable decisions.

6. It is useful for investing in short-term projects which lapses within short time frame

(Pivorienė, 2017).

Disadvantages

1. Major drawback of this method is that it does not consider time value of money which is

required while determining usefulness of project.

2. Cash flows from investment is required to evaluate properly effectiveness of project but is

ignored in this method.

3. It is not suitable to implement ARR method as it does not consider terminal value while

investing in the project.

4. It is not useful method for long-term projects and as such, viable decision cannot be made in

this aspect.

IRR

IRR is another effective method which provides rate of return on project over its useful

life. It is termed as discounting rate which assumes that present value of cash inflows will be

equal to cash outflows. In simple words, net present value of investment will become zero for the

project. Management can set minimum required investment rate by which project can be easily

assessed. If rate is more than minimum one, investment is accepted else rejected (Internal Rate

of Return (IRR), 2018).

Advantages

1. The main essence of this method is that it consider time value of money while assessing

project and as such, correct interpretation can be made.

2. It is easier to compute and derive outcome in effective manner.

3. Hurdle rate is ignored while calculating IRR of the project and as such, wrong determination

of investment decision is not possible.

3

1. It is simple to calculate and interpret outcome drawn while assessing project.

2. Project's viability can be easily attained in quick manner and with less time.

3. It provides clarity about effectiveness of project in less time which saves valuable time for

management.

4. Accounting profit is taken with reference to IRR.

5. This eases evaluating profitability aspect of new project and aids in making viable decisions.

6. It is useful for investing in short-term projects which lapses within short time frame

(Pivorienė, 2017).

Disadvantages

1. Major drawback of this method is that it does not consider time value of money which is

required while determining usefulness of project.

2. Cash flows from investment is required to evaluate properly effectiveness of project but is

ignored in this method.

3. It is not suitable to implement ARR method as it does not consider terminal value while

investing in the project.

4. It is not useful method for long-term projects and as such, viable decision cannot be made in

this aspect.

IRR

IRR is another effective method which provides rate of return on project over its useful

life. It is termed as discounting rate which assumes that present value of cash inflows will be

equal to cash outflows. In simple words, net present value of investment will become zero for the

project. Management can set minimum required investment rate by which project can be easily

assessed. If rate is more than minimum one, investment is accepted else rejected (Internal Rate

of Return (IRR), 2018).

Advantages

1. The main essence of this method is that it consider time value of money while assessing

project and as such, correct interpretation can be made.

2. It is easier to compute and derive outcome in effective manner.

3. Hurdle rate is ignored while calculating IRR of the project and as such, wrong determination

of investment decision is not possible.

3

4. It does not take cost of capital in account and as such, it provides better results.

5. This method gives priority to increase or maximising in shareholder's wealth.

6. IRR is used for ranking project options as it provides rate of return on various projects.

Disadvantages

1. Reinvestment rate is estimated for life of project which leads to inaccurate results regarding

profitability of new project.

2. Another disadvantage of IRR method is that computation is not easy and incorporates complex

calculations difficult for assessing usefulness of project (Ababneh, Shrafat and Zeglat, 2017).

3. IRR gives due importance only to profitability aspect but ignores recovery of investment in

near future.

4. IRR is not helpful for when there are two mutually projects and as such, interpretation cannot

be done.

5. It is unsuitable when size and term of two projects differ from each other which is the biggest

drawback of this method.

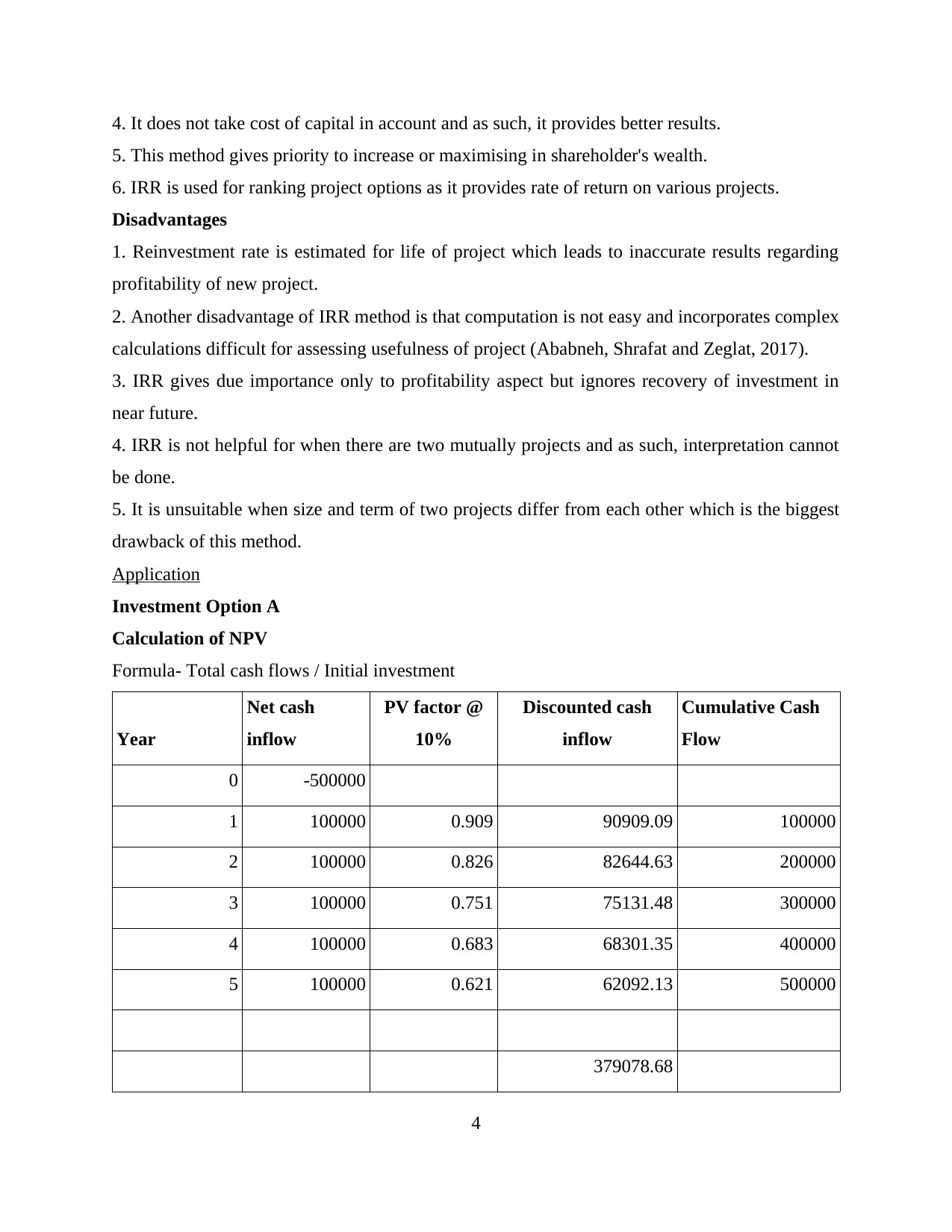

Application

Investment Option A

Calculation of NPV

Formula- Total cash flows / Initial investment

Year

Net cash

inflow

PV factor @

10%

Discounted cash

inflow

Cumulative Cash

Flow

0 -500000

1 100000 0.909 90909.09 100000

2 100000 0.826 82644.63 200000

3 100000 0.751 75131.48 300000

4 100000 0.683 68301.35 400000

5 100000 0.621 62092.13 500000

379078.68

4

5. This method gives priority to increase or maximising in shareholder's wealth.

6. IRR is used for ranking project options as it provides rate of return on various projects.

Disadvantages

1. Reinvestment rate is estimated for life of project which leads to inaccurate results regarding

profitability of new project.

2. Another disadvantage of IRR method is that computation is not easy and incorporates complex

calculations difficult for assessing usefulness of project (Ababneh, Shrafat and Zeglat, 2017).

3. IRR gives due importance only to profitability aspect but ignores recovery of investment in

near future.

4. IRR is not helpful for when there are two mutually projects and as such, interpretation cannot

be done.

5. It is unsuitable when size and term of two projects differ from each other which is the biggest

drawback of this method.

Application

Investment Option A

Calculation of NPV

Formula- Total cash flows / Initial investment

Year

Net cash

inflow

PV factor @

10%

Discounted cash

inflow

Cumulative Cash

Flow

0 -500000

1 100000 0.909 90909.09 100000

2 100000 0.826 82644.63 200000

3 100000 0.751 75131.48 300000

4 100000 0.683 68301.35 400000

5 100000 0.621 62092.13 500000

379078.68

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Initial

investment 500000

NPV -120921.32

Calculation of Payback period

Formula- Initial Investment / Average Payback

= 5 years

Calculation of ARR

Formula – Average Profit / Average Investment

Average Investment is taken as initial investment

= 70000 / 500000

= 14 %

Calculation of IRR

Formula- PV (Present Value) of cash flows – Initial Investment

= 0 %

Investment Option B

Calculation of NPV

Year

Net cash

inflow

PV factor @

10%

Discounted cash

inflow

Cumulative Cash

Flow

0 -500000

1 220000 0.909 200000 220000

2 240000 0.826 198347.11 460000

3 50000 0.751 37565.74 510000

4 70000 0.683 47810.94 580000

5 50000 0.621 31046.07 630000

514769.86

5

investment 500000

NPV -120921.32

Calculation of Payback period

Formula- Initial Investment / Average Payback

= 5 years

Calculation of ARR

Formula – Average Profit / Average Investment

Average Investment is taken as initial investment

= 70000 / 500000

= 14 %

Calculation of IRR

Formula- PV (Present Value) of cash flows – Initial Investment

= 0 %

Investment Option B

Calculation of NPV

Year

Net cash

inflow

PV factor @

10%

Discounted cash

inflow

Cumulative Cash

Flow

0 -500000

1 220000 0.909 200000 220000

2 240000 0.826 198347.11 460000

3 50000 0.751 37565.74 510000

4 70000 0.683 47810.94 580000

5 50000 0.621 31046.07 630000

514769.86

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Initial

investment 500000

NPV 14769.86

Calculation of Payback period

= 2 + (40000 / 50000)

= 2 + 0.8

= 2.8 years

Calculation of ARR

= 50000 / 500000

= 10 %

Calculation of IRR

= 11.58 %

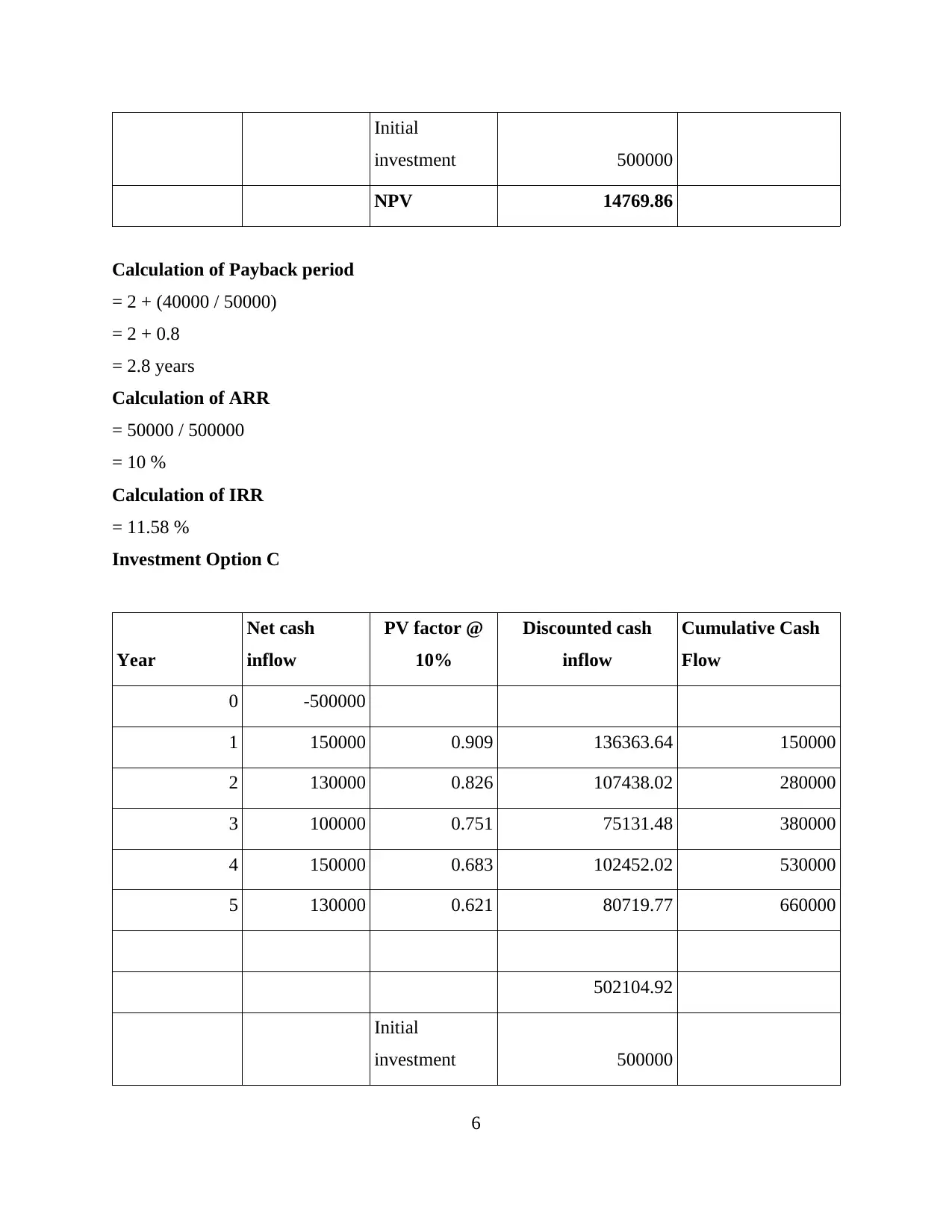

Investment Option C

Year

Net cash

inflow

PV factor @

10%

Discounted cash

inflow

Cumulative Cash

Flow

0 -500000

1 150000 0.909 136363.64 150000

2 130000 0.826 107438.02 280000

3 100000 0.751 75131.48 380000

4 150000 0.683 102452.02 530000

5 130000 0.621 80719.77 660000

502104.92

Initial

investment 500000

6

investment 500000

NPV 14769.86

Calculation of Payback period

= 2 + (40000 / 50000)

= 2 + 0.8

= 2.8 years

Calculation of ARR

= 50000 / 500000

= 10 %

Calculation of IRR

= 11.58 %

Investment Option C

Year

Net cash

inflow

PV factor @

10%

Discounted cash

inflow

Cumulative Cash

Flow

0 -500000

1 150000 0.909 136363.64 150000

2 130000 0.826 107438.02 280000

3 100000 0.751 75131.48 380000

4 150000 0.683 102452.02 530000

5 130000 0.621 80719.77 660000

502104.92

Initial

investment 500000

6

NPV 2104.92

Calculation of Payback period

= 3 + 120000 / 150000

= 3 + 0.8

= 3.8 years

Calculation of ARR

= 25000 / 500000

= 5 %

Calculation of IRR

= 10.17 %

Findings

The investment appraisal techniques are calculated which shows various options to be

selected by Victoria Babies Ltd so that it may expand its operations. There are three options

which are available to company to choose the best among them. Starting from option A which is

expanding existing plant with implementing bigger machines. It can be found out that this option

is not good one to chose as it has lower NPV which is considered for evaluating effective

outcome of the project. It can be interpreted that NPV is -120921 which implies that there is

negative aspect in case of this technique (Kolawale and Grace, 2017). It is not suitable for

company as NPV should in be positive value. On the other hand, payback period is 5 years

which means that company cannot recover initial investment amount before 5 years. This is not

recommended as shorter payback period is suggested for the betterment of the organisation.

Apart from this, IRR is 0 % which implies that there will be no adequate rate of return that will

be yield by investing in this project of implementing bigger machines. However, ARR is 14 %

which is good. But it is recommended that investment should not be done in this project by the

company as desired results will not be accomplished.

Investment option B is related to building new production plant in UK itself. By

analysing investment appraisal techniques, it can be said that company should invest in the same

as good profitability will be generated by it. This is evident from calculation of NPV which is

14729.86 and it implies that NPV is positive and will provide good profits to Victoria Babies

7

Calculation of Payback period

= 3 + 120000 / 150000

= 3 + 0.8

= 3.8 years

Calculation of ARR

= 25000 / 500000

= 5 %

Calculation of IRR

= 10.17 %

Findings

The investment appraisal techniques are calculated which shows various options to be

selected by Victoria Babies Ltd so that it may expand its operations. There are three options

which are available to company to choose the best among them. Starting from option A which is

expanding existing plant with implementing bigger machines. It can be found out that this option

is not good one to chose as it has lower NPV which is considered for evaluating effective

outcome of the project. It can be interpreted that NPV is -120921 which implies that there is

negative aspect in case of this technique (Kolawale and Grace, 2017). It is not suitable for

company as NPV should in be positive value. On the other hand, payback period is 5 years

which means that company cannot recover initial investment amount before 5 years. This is not

recommended as shorter payback period is suggested for the betterment of the organisation.

Apart from this, IRR is 0 % which implies that there will be no adequate rate of return that will

be yield by investing in this project of implementing bigger machines. However, ARR is 14 %

which is good. But it is recommended that investment should not be done in this project by the

company as desired results will not be accomplished.

Investment option B is related to building new production plant in UK itself. By

analysing investment appraisal techniques, it can be said that company should invest in the same

as good profitability will be generated by it. This is evident from calculation of NPV which is

14729.86 and it implies that NPV is positive and will provide good profits to Victoria Babies

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ltd. It has more NPV and it should be adopted as per this method. On the other hand, payback

period is 2.8 years which is less than compared to other options. It implies that initial investment

amount will be yield in shorter period which is better for investors to get results within short time

span. Apart from this, IRR is 11.58 % which is higher. This means that company should opt for

this investment option as better results are provided in it. Next comes ARR which is 10 %

implies that accounting profit will be generated in effective manner by investing in this project.

Investment option C is related to international expansion to existing plant in China. It can

be interpreted that investment in the project should not be made (Atari and Prause, 2017). This is

because NPV is less in this project which is just 2104.92. It implies that NPV is less than

compared to other options. It is recommended that Higher NPV should be selected and in this

aspect, option B is suitable. Besides this, payback period is 3.8 years which means that it will

take longer time to yield adequate results. While, IRR ARR are 10.17 % and 5 % which is low

than other options. Thus, it can found out that Victoria Babies Ltd should invest in the

investment option B which is related to expansion of plant in UK as all the investment appraisal

techniques are in favour of the same. It will be beneficial for the firm to achieve goals.

CONCLUSION

Hereby it can be concluded that capital budgeting techniques plays important role in the

company while selecting and evaluating good project out of available projects. Victoria Babies

Ltd should select investment option B which yields adequate results to it in the best possible

way. It will garner good quantum of profits in the long run with much ease.

8

period is 2.8 years which is less than compared to other options. It implies that initial investment

amount will be yield in shorter period which is better for investors to get results within short time

span. Apart from this, IRR is 11.58 % which is higher. This means that company should opt for

this investment option as better results are provided in it. Next comes ARR which is 10 %

implies that accounting profit will be generated in effective manner by investing in this project.

Investment option C is related to international expansion to existing plant in China. It can

be interpreted that investment in the project should not be made (Atari and Prause, 2017). This is

because NPV is less in this project which is just 2104.92. It implies that NPV is less than

compared to other options. It is recommended that Higher NPV should be selected and in this

aspect, option B is suitable. Besides this, payback period is 3.8 years which means that it will

take longer time to yield adequate results. While, IRR ARR are 10.17 % and 5 % which is low

than other options. Thus, it can found out that Victoria Babies Ltd should invest in the

investment option B which is related to expansion of plant in UK as all the investment appraisal

techniques are in favour of the same. It will be beneficial for the firm to achieve goals.

CONCLUSION

Hereby it can be concluded that capital budgeting techniques plays important role in the

company while selecting and evaluating good project out of available projects. Victoria Babies

Ltd should select investment option B which yields adequate results to it in the best possible

way. It will garner good quantum of profits in the long run with much ease.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ababneh, H., Shrafat, F. and Zeglat, D., 2017. Approaching information system evaluation

methodology and techniques: a comprehensive review. International Journal of

Business Information Systems. 24(1). pp.1-30.

Atari, S. and Prause, G., 2017, October. Risk assessment of emission abatement technologies for

clean shipping. InInternational Conference on Reliability and Statistics in

Transportation and Communication (pp. 93-101). Springer, Cham.

9

Books and Journals

Ababneh, H., Shrafat, F. and Zeglat, D., 2017. Approaching information system evaluation

methodology and techniques: a comprehensive review. International Journal of

Business Information Systems. 24(1). pp.1-30.

Atari, S. and Prause, G., 2017, October. Risk assessment of emission abatement technologies for

clean shipping. InInternational Conference on Reliability and Statistics in

Transportation and Communication (pp. 93-101). Springer, Cham.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.