Financial Ratio Analysis Report: Jones Ltd vs Millet Ltd

VerifiedAdded on 2023/01/18

|13

|2490

|73

Report

AI Summary

This report presents a comprehensive financial analysis, focusing on the performance comparison of Jones Ltd and Millet Ltd through various financial ratios such as operating profit margin, return on shareholders' funds, return on equity, inventory turnover, quick ratio, gearing ratio, interest coverage ratio, and dividend cover ratio. The analysis includes a detailed computation and assessment of these ratios, offering insights into each company's financial health and efficiency. Additionally, the report delves into the limitations of financial ratios in decision-making. Furthermore, the report includes a detailed job cost card for Benns Ltd, covering cost classifications (direct, indirect, variable, and fixed costs), and recommending the selection of the best quote to the finance manager based on the cost analysis. The report culminates in a recommendation regarding investment decisions and the importance of accurate cost estimations for profitability.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

a. Computation of ratio...............................................................................................................1

b. assessing the performance and comparing both the companies .............................................2

c. Analysing limitation of the financial ratios in the process of decision making......................4

Task 2...............................................................................................................................................5

a. Determining the types of cost classification in manufacturing goods and the services .........5

b. Preparing job cost card ...........................................................................................................6

c. Recommending selection of best quote to the finance manager.............................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

a. Computation of ratio...............................................................................................................1

b. assessing the performance and comparing both the companies .............................................2

c. Analysing limitation of the financial ratios in the process of decision making......................4

Task 2...............................................................................................................................................5

a. Determining the types of cost classification in manufacturing goods and the services .........5

b. Preparing job cost card ...........................................................................................................6

c. Recommending selection of best quote to the finance manager.............................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Management of the financial resources includes the details of the money available to the business for making expenses in form

of the cash, credit lines and the liquid securities. Prior to entering into the business, an organization requires to secure enough financial

resources for the purpose of achieving operational efficiency and effectiveness in promoting its success. The present study is based on

ratio analysis of Jones Ltd and Millet Ltd that depicts the financial performance and position of the company. Furthermore, it includes

framing of job cost records for Benns Ltd that produces bespoke furniture’s.

Task 1

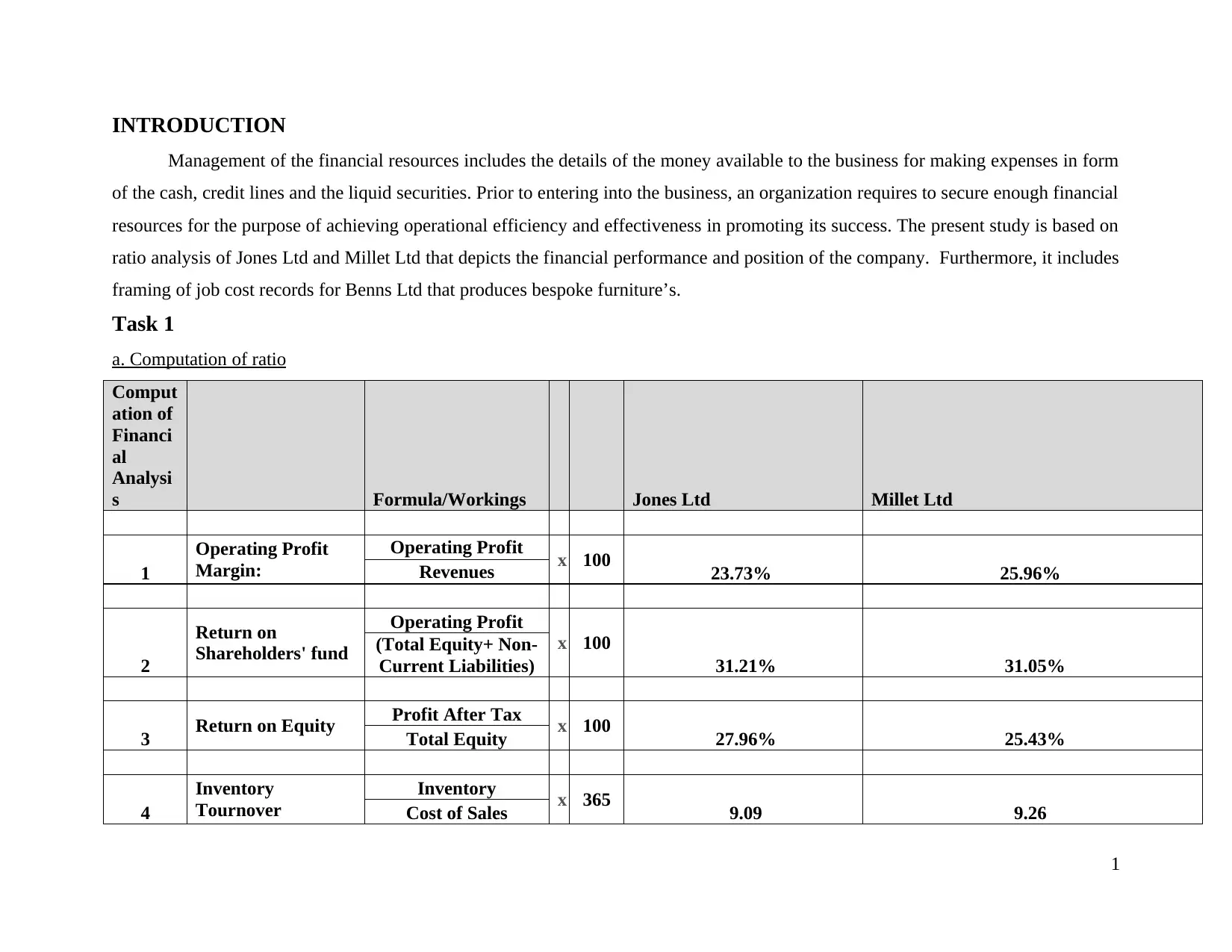

a. Computation of ratio

Comput

ation of

Financi

al

Analysi

s Formula/Workings Jones Ltd Millet Ltd

1

Operating Profit

Margin:

Operating Profit x 100 23.73% 25.96%Revenues

2

Return on

Shareholders' fund

Operating Profit

x 100

31.21% 31.05%

(Total Equity+ Non-

Current Liabilities)

3 Return on Equity Profit After Tax x 100 27.96% 25.43%Total Equity

4

Inventory

Tournover

Inventory x 365 9.09 9.26Cost of Sales

1

Management of the financial resources includes the details of the money available to the business for making expenses in form

of the cash, credit lines and the liquid securities. Prior to entering into the business, an organization requires to secure enough financial

resources for the purpose of achieving operational efficiency and effectiveness in promoting its success. The present study is based on

ratio analysis of Jones Ltd and Millet Ltd that depicts the financial performance and position of the company. Furthermore, it includes

framing of job cost records for Benns Ltd that produces bespoke furniture’s.

Task 1

a. Computation of ratio

Comput

ation of

Financi

al

Analysi

s Formula/Workings Jones Ltd Millet Ltd

1

Operating Profit

Margin:

Operating Profit x 100 23.73% 25.96%Revenues

2

Return on

Shareholders' fund

Operating Profit

x 100

31.21% 31.05%

(Total Equity+ Non-

Current Liabilities)

3 Return on Equity Profit After Tax x 100 27.96% 25.43%Total Equity

4

Inventory

Tournover

Inventory x 365 9.09 9.26Cost of Sales

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

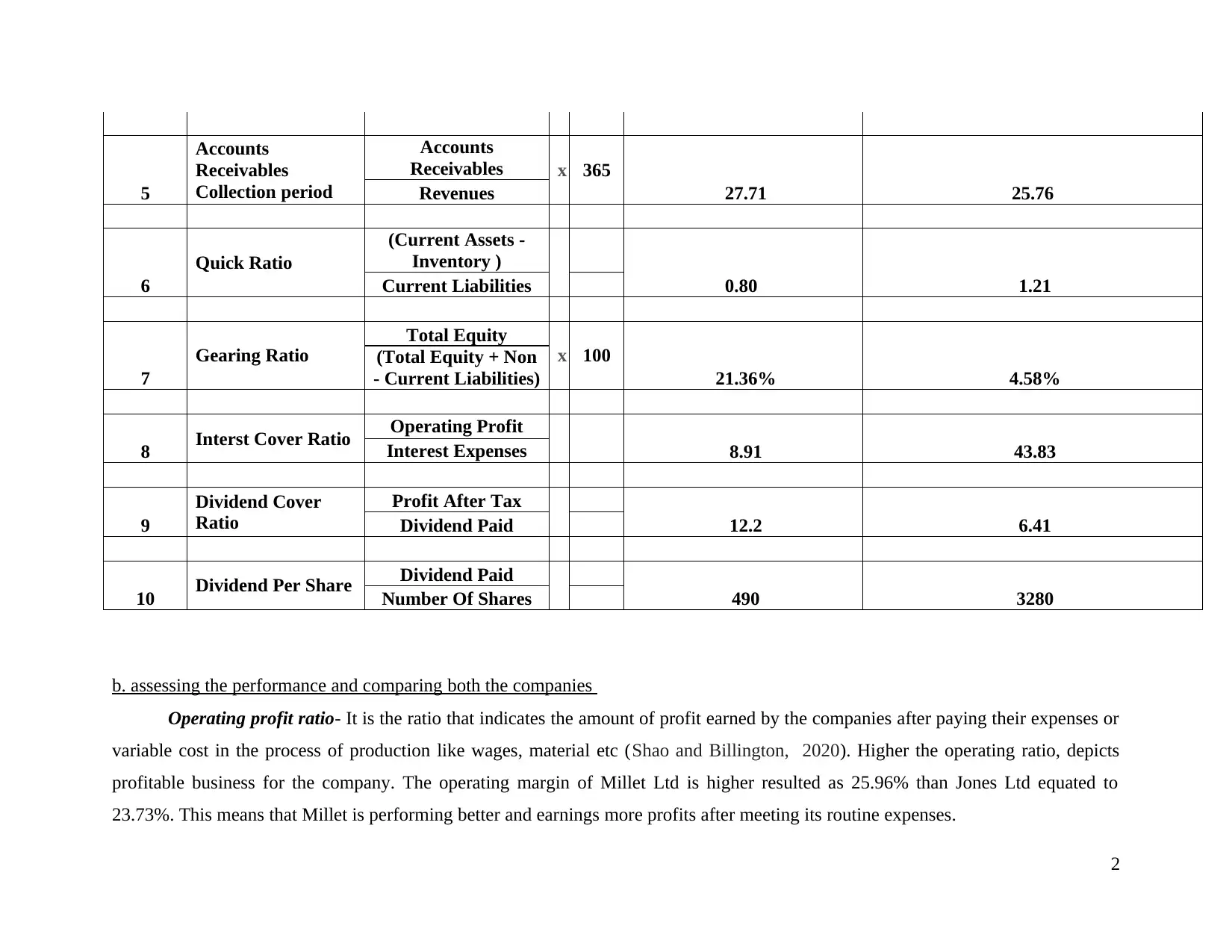

5

Accounts

Receivables

Collection period

Accounts

Receivables x 365

27.71 25.76Revenues

6

Quick Ratio

(Current Assets -

Inventory )

0.80 1.21Current Liabilities

7

Gearing Ratio

Total Equity

x 100

21.36% 4.58%

(Total Equity + Non

- Current Liabilities)

8 Interst Cover Ratio Operating Profit

8.91 43.83Interest Expenses

9

Dividend Cover

Ratio

Profit After Tax

12.2 6.41Dividend Paid

10 Dividend Per Share Dividend Paid

490 3280Number Of Shares

b. assessing the performance and comparing both the companies

Operating profit ratio- It is the ratio that indicates the amount of profit earned by the companies after paying their expenses or

variable cost in the process of production like wages, material etc (Shao and Billington, 2020). Higher the operating ratio, depicts

profitable business for the company. The operating margin of Millet Ltd is higher resulted as 25.96% than Jones Ltd equated to

23.73%. This means that Millet is performing better and earnings more profits after meeting its routine expenses.

2

Accounts

Receivables

Collection period

Accounts

Receivables x 365

27.71 25.76Revenues

6

Quick Ratio

(Current Assets -

Inventory )

0.80 1.21Current Liabilities

7

Gearing Ratio

Total Equity

x 100

21.36% 4.58%

(Total Equity + Non

- Current Liabilities)

8 Interst Cover Ratio Operating Profit

8.91 43.83Interest Expenses

9

Dividend Cover

Ratio

Profit After Tax

12.2 6.41Dividend Paid

10 Dividend Per Share Dividend Paid

490 3280Number Of Shares

b. assessing the performance and comparing both the companies

Operating profit ratio- It is the ratio that indicates the amount of profit earned by the companies after paying their expenses or

variable cost in the process of production like wages, material etc (Shao and Billington, 2020). Higher the operating ratio, depicts

profitable business for the company. The operating margin of Millet Ltd is higher resulted as 25.96% than Jones Ltd equated to

23.73%. This means that Millet is performing better and earnings more profits after meeting its routine expenses.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Return on shareholders funds- This ratio reflects the proportion of money returned to owners of an enterprise in percentage

value that they had been invested in their business (Netreba and et.al., 2018). Greater the percentage means more amount of the money

is returned to the stakeholder or investor. The ratio of Jones and Millet evaluated as 31.21% & 31.05% which clearly indicates that

both the company is facilitating good amount of returns to their respective investors.

Return on equity- It referred as the profitability ratio that measures an ability of the company in generating the profits from the

investment made by their shareholders. Higher the ratio of return on equity indicates better performance of the company (Jiang and

et.al., 2019). As the ROE of Jones Ltd is higher or better equating to 27.96% as compared to Millet Ltd resulting as 25.43%. This

reflects better returns gained by Jones on its shareholders investment.

Inventory turnover ratio- It means number of times an entity's average inventory is been sold during the account period. High

ratio indicated a fast moving inventory and the low ratio reflects obsolete or the slow moving stock (Almohamad and et.al., 2018). The

ITR ratio of both the companies accounted as 9.09 and 9.26 which does not show a large difference that means Jones and Millet both

convert their inventory into cash as 9 times.

Accounts receivable days- This shows the number of days customers or the debtors of the firm takes in paying off their

receivables (Peng and et.al., 2017). The customers of Jones takes 27.71 days in making payment on the goods purchased by them

whereas, debtors of Millet takes 25.76 days for paying their invoices. This depicts that trade debtors of Millet are taking less time than

customers of Jones in making their dues clear so it shows better performance of the Jones.

Quick ratio- It is the ratio that acts as an indicator of the short run liquidity position of the company that measures an ability of

the firm for meeting their short term liabilities with the use of their major liquid assets (Yang and et.al., 2018). It has been stated that a

quick ratio higher than 1 reflects company is having sufficient quick assets for paying off their current obligations. As quick ratio of

Millet resulted greater than 1 that is 1.21 but ratio of Jones equates to 0.80, this clearly indicates that Millet is capable of the meeting

its short term obligations effectively with their immediate assets than Jones.

3

value that they had been invested in their business (Netreba and et.al., 2018). Greater the percentage means more amount of the money

is returned to the stakeholder or investor. The ratio of Jones and Millet evaluated as 31.21% & 31.05% which clearly indicates that

both the company is facilitating good amount of returns to their respective investors.

Return on equity- It referred as the profitability ratio that measures an ability of the company in generating the profits from the

investment made by their shareholders. Higher the ratio of return on equity indicates better performance of the company (Jiang and

et.al., 2019). As the ROE of Jones Ltd is higher or better equating to 27.96% as compared to Millet Ltd resulting as 25.43%. This

reflects better returns gained by Jones on its shareholders investment.

Inventory turnover ratio- It means number of times an entity's average inventory is been sold during the account period. High

ratio indicated a fast moving inventory and the low ratio reflects obsolete or the slow moving stock (Almohamad and et.al., 2018). The

ITR ratio of both the companies accounted as 9.09 and 9.26 which does not show a large difference that means Jones and Millet both

convert their inventory into cash as 9 times.

Accounts receivable days- This shows the number of days customers or the debtors of the firm takes in paying off their

receivables (Peng and et.al., 2017). The customers of Jones takes 27.71 days in making payment on the goods purchased by them

whereas, debtors of Millet takes 25.76 days for paying their invoices. This depicts that trade debtors of Millet are taking less time than

customers of Jones in making their dues clear so it shows better performance of the Jones.

Quick ratio- It is the ratio that acts as an indicator of the short run liquidity position of the company that measures an ability of

the firm for meeting their short term liabilities with the use of their major liquid assets (Yang and et.al., 2018). It has been stated that a

quick ratio higher than 1 reflects company is having sufficient quick assets for paying off their current obligations. As quick ratio of

Millet resulted greater than 1 that is 1.21 but ratio of Jones equates to 0.80, this clearly indicates that Millet is capable of the meeting

its short term obligations effectively with their immediate assets than Jones.

3

Gearing ratio- It is kind of financial ratio that compares the debt of the company in relation to different financial metrics like

total equity. It is counted as the measure of leverage position of the company that is the level of the liabilities present in the capital

structure of an entity that are interest bearing (Cleophas and Zwinderman, 2019). A gearing ration in between 25-50% is said as good

and reflects optimum for the well-established corporations. With respect to the evaluation it has been presented that gearing ratio of

Jones is much better than millet because its ratio resulted as 21.36% which is close to optimum ratio. However, Millet's gearing ratio

attained as 4.58% which reflects a bad leverage position of the company.

Interest coverage ratio- It is the measures that states for number of times the company can make its interest obligation through

its earnings. High ratio is considered to be better because it shows that an entity is having enough profits for paying their interest

expenses while low ratio indicates low profitability (Papista and et.al., 2018). The ICR of Millet is better as its ratio is higher with a

greater value that is 43.83 as its interest obligation are very low as compared to Jones Ltd resulting a ratio as 8.91.

Dividend coverage ratio- This ratio indicates capacity of an enterprise in paying off their dividends from the profit attributable

to their shareholders. A dividend coverage of the 3 implied that company is having enough earnings in paying off their dividends.

Jones has good capability in making the payment of dividend through their profits as its ratio is greater that is 12.2 as compared to

Millet equates to 6.41.

Dividend per share- The value of DPS of Millet is higher because the amount of annual dividends of Millet is greater than

Jones resulting as 3280 and 490. This shows the better position and performance of Millet as compared to Jones.

Overall the performance of Jones is better than Millet as its profitability ratios, gearing ratio and efficiency ratio are higher

than Millet so fro earning better returns, Benns Ltd must make investment in Jones Ltd.

c. Analysing limitation of the financial ratios in the process of decision making

Financial analysis tends to be useful as it highlights the relationship between different items in the final reports. There are

several limitations associated with financial ratios that are as follows-

4

total equity. It is counted as the measure of leverage position of the company that is the level of the liabilities present in the capital

structure of an entity that are interest bearing (Cleophas and Zwinderman, 2019). A gearing ration in between 25-50% is said as good

and reflects optimum for the well-established corporations. With respect to the evaluation it has been presented that gearing ratio of

Jones is much better than millet because its ratio resulted as 21.36% which is close to optimum ratio. However, Millet's gearing ratio

attained as 4.58% which reflects a bad leverage position of the company.

Interest coverage ratio- It is the measures that states for number of times the company can make its interest obligation through

its earnings. High ratio is considered to be better because it shows that an entity is having enough profits for paying their interest

expenses while low ratio indicates low profitability (Papista and et.al., 2018). The ICR of Millet is better as its ratio is higher with a

greater value that is 43.83 as its interest obligation are very low as compared to Jones Ltd resulting a ratio as 8.91.

Dividend coverage ratio- This ratio indicates capacity of an enterprise in paying off their dividends from the profit attributable

to their shareholders. A dividend coverage of the 3 implied that company is having enough earnings in paying off their dividends.

Jones has good capability in making the payment of dividend through their profits as its ratio is greater that is 12.2 as compared to

Millet equates to 6.41.

Dividend per share- The value of DPS of Millet is higher because the amount of annual dividends of Millet is greater than

Jones resulting as 3280 and 490. This shows the better position and performance of Millet as compared to Jones.

Overall the performance of Jones is better than Millet as its profitability ratios, gearing ratio and efficiency ratio are higher

than Millet so fro earning better returns, Benns Ltd must make investment in Jones Ltd.

c. Analysing limitation of the financial ratios in the process of decision making

Financial analysis tends to be useful as it highlights the relationship between different items in the final reports. There are

several limitations associated with financial ratios that are as follows-

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial ratios are evaluated on the basis of accounting figures that are been provided in the final statements of the

company (Zhang and et.al., 2017). As the accounting figures contains deficiencies, estimations and subjected to

manipulation so ratios drawn from it are not counted as useful in order to infer accurate and reliable conclusions.

It comprises of comparability problem as different company employs or chooses different methods of accounting, that

in turn causes problem in making appropriate comparison in key relationships.

In some cases, inflation might limit the utility of the financial ratios as because of inflation, historical based final

reports and the accounting figures does not shows present value figures. Therefore, accounting ratios computed

contains distortions and becomes deceptive over the years.

Accounting ratios are not considered as totally dependable and it should be utilised after facilitating the due weight to

the general economic conditions, position of the firm, industry situation, size of the company and product diversity

which in turn makes the corporation entirely dissimilar and impact calculation of the financial ratios.

Various methods of calculating influences utility of the accounting ratios and various concepts that are been used in

identifying denominator and the numerator in the specific accounting ratio does not assist in drawing the reliable

conclusions in the identical situations.

Task 2

a. Determining the types of cost classification in manufacturing goods and the services

The cost is classified in this study based on elements, function and behaviour that are as follows-

Direct cost- It means the cost that is been directly mark up to specific cost like raw material, e labour cost involving operating

expenses and the other related cost.

Indirect cost- It refers to the cost that does relate directly with a department or the unit and could not be tracked for a particular

product (Papista and et.al., 2018).

5

company (Zhang and et.al., 2017). As the accounting figures contains deficiencies, estimations and subjected to

manipulation so ratios drawn from it are not counted as useful in order to infer accurate and reliable conclusions.

It comprises of comparability problem as different company employs or chooses different methods of accounting, that

in turn causes problem in making appropriate comparison in key relationships.

In some cases, inflation might limit the utility of the financial ratios as because of inflation, historical based final

reports and the accounting figures does not shows present value figures. Therefore, accounting ratios computed

contains distortions and becomes deceptive over the years.

Accounting ratios are not considered as totally dependable and it should be utilised after facilitating the due weight to

the general economic conditions, position of the firm, industry situation, size of the company and product diversity

which in turn makes the corporation entirely dissimilar and impact calculation of the financial ratios.

Various methods of calculating influences utility of the accounting ratios and various concepts that are been used in

identifying denominator and the numerator in the specific accounting ratio does not assist in drawing the reliable

conclusions in the identical situations.

Task 2

a. Determining the types of cost classification in manufacturing goods and the services

The cost is classified in this study based on elements, function and behaviour that are as follows-

Direct cost- It means the cost that is been directly mark up to specific cost like raw material, e labour cost involving operating

expenses and the other related cost.

Indirect cost- It refers to the cost that does relate directly with a department or the unit and could not be tracked for a particular

product (Papista and et.al., 2018).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

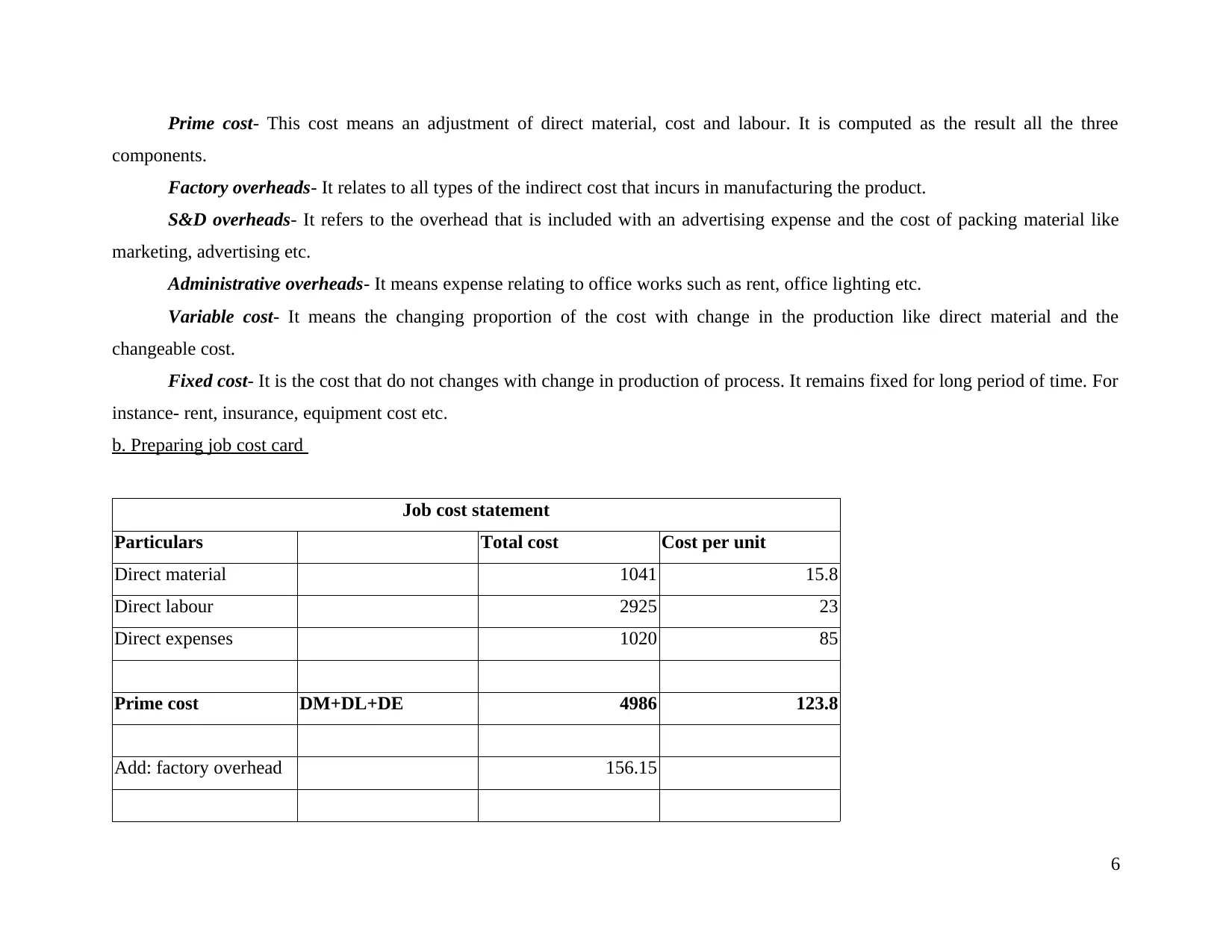

Prime cost- This cost means an adjustment of direct material, cost and labour. It is computed as the result all the three

components.

Factory overheads- It relates to all types of the indirect cost that incurs in manufacturing the product.

S&D overheads- It refers to the overhead that is included with an advertising expense and the cost of packing material like

marketing, advertising etc.

Administrative overheads- It means expense relating to office works such as rent, office lighting etc.

Variable cost- It means the changing proportion of the cost with change in the production like direct material and the

changeable cost.

Fixed cost- It is the cost that do not changes with change in production of process. It remains fixed for long period of time. For

instance- rent, insurance, equipment cost etc.

b. Preparing job cost card

Job cost statement

Particulars Total cost Cost per unit

Direct material 1041 15.8

Direct labour 2925 23

Direct expenses 1020 85

Prime cost DM+DL+DE 4986 123.8

Add: factory overhead 156.15

6

components.

Factory overheads- It relates to all types of the indirect cost that incurs in manufacturing the product.

S&D overheads- It refers to the overhead that is included with an advertising expense and the cost of packing material like

marketing, advertising etc.

Administrative overheads- It means expense relating to office works such as rent, office lighting etc.

Variable cost- It means the changing proportion of the cost with change in the production like direct material and the

changeable cost.

Fixed cost- It is the cost that do not changes with change in production of process. It remains fixed for long period of time. For

instance- rent, insurance, equipment cost etc.

b. Preparing job cost card

Job cost statement

Particulars Total cost Cost per unit

Direct material 1041 15.8

Direct labour 2925 23

Direct expenses 1020 85

Prime cost DM+DL+DE 4986 123.8

Add: factory overhead 156.15

6

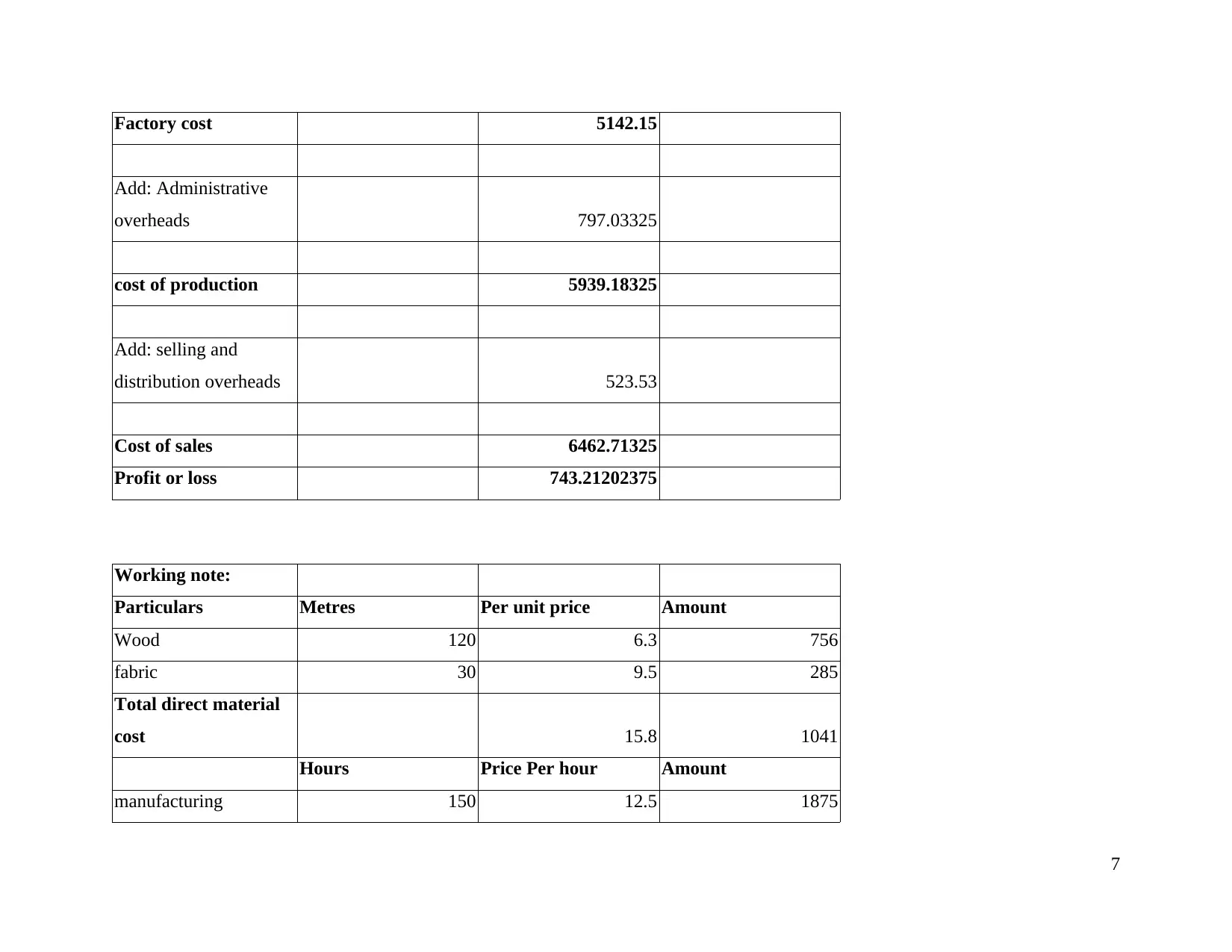

Factory cost 5142.15

Add: Administrative

overheads 797.03325

cost of production 5939.18325

Add: selling and

distribution overheads 523.53

Cost of sales 6462.71325

Profit or loss 743.21202375

Working note:

Particulars Metres Per unit price Amount

Wood 120 6.3 756

fabric 30 9.5 285

Total direct material

cost 15.8 1041

Hours Price Per hour Amount

manufacturing 150 12.5 1875

7

Add: Administrative

overheads 797.03325

cost of production 5939.18325

Add: selling and

distribution overheads 523.53

Cost of sales 6462.71325

Profit or loss 743.21202375

Working note:

Particulars Metres Per unit price Amount

Wood 120 6.3 756

fabric 30 9.5 285

Total direct material

cost 15.8 1041

Hours Price Per hour Amount

manufacturing 150 12.5 1875

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

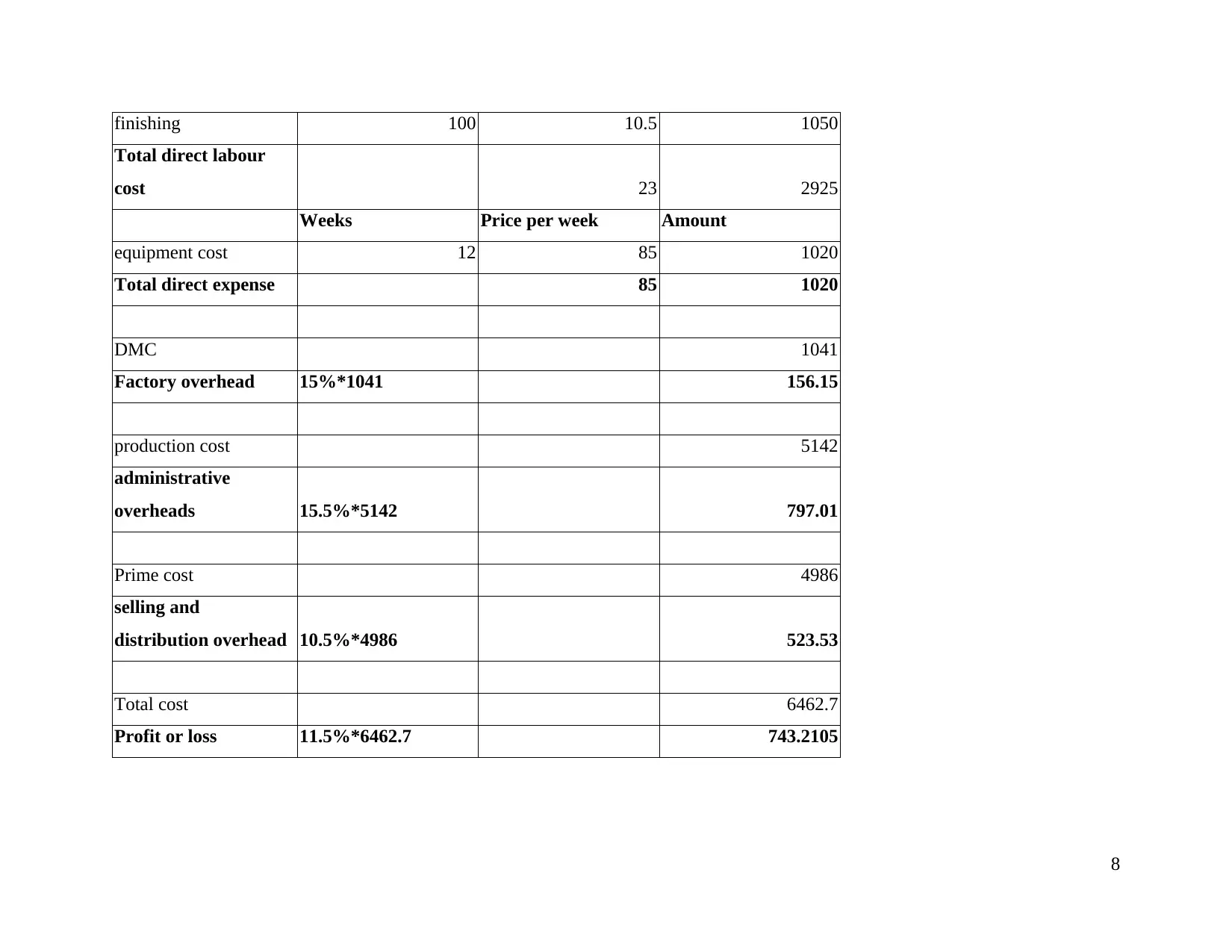

finishing 100 10.5 1050

Total direct labour

cost 23 2925

Weeks Price per week Amount

equipment cost 12 85 1020

Total direct expense 85 1020

DMC 1041

Factory overhead 15%*1041 156.15

production cost 5142

administrative

overheads 15.5%*5142 797.01

Prime cost 4986

selling and

distribution overhead 10.5%*4986 523.53

Total cost 6462.7

Profit or loss 11.5%*6462.7 743.2105

8

Total direct labour

cost 23 2925

Weeks Price per week Amount

equipment cost 12 85 1020

Total direct expense 85 1020

DMC 1041

Factory overhead 15%*1041 156.15

production cost 5142

administrative

overheads 15.5%*5142 797.01

Prime cost 4986

selling and

distribution overhead 10.5%*4986 523.53

Total cost 6462.7

Profit or loss 11.5%*6462.7 743.2105

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. Recommending selection of best quote to the finance manager

From the above evaluation it has been analysed that as the cost of sales resulting as 6460.7 after adding up all the cost. This

shows that finance manager must accept the quote of £7,450.99 from its customers as it will be a profitable proposal because after

deducting the estimated cost of 6460 from 7450, profit is gained of 988 by an enterprise. Therefore, cost report helps in identifying

accurate anticipations of the cost so that manager can compute accurate profitability that a company could be able to generate in the

future after meeting all of its expenses.

CONCLUSION

By summing up the above report, it is been identified that performance of Jones Ltd is better than Millet Ltd as its gearing,

profitability, leverage and efficiency ratios are showing better results. The job cost report helps Benns Ltd in making adequate

estimation of the expenses and the income that will be generated from its business activities and in selecting the best order which helps

in generating larger returns and low cost.

9

From the above evaluation it has been analysed that as the cost of sales resulting as 6460.7 after adding up all the cost. This

shows that finance manager must accept the quote of £7,450.99 from its customers as it will be a profitable proposal because after

deducting the estimated cost of 6460 from 7450, profit is gained of 988 by an enterprise. Therefore, cost report helps in identifying

accurate anticipations of the cost so that manager can compute accurate profitability that a company could be able to generate in the

future after meeting all of its expenses.

CONCLUSION

By summing up the above report, it is been identified that performance of Jones Ltd is better than Millet Ltd as its gearing,

profitability, leverage and efficiency ratios are showing better results. The job cost report helps Benns Ltd in making adequate

estimation of the expenses and the income that will be generated from its business activities and in selecting the best order which helps

in generating larger returns and low cost.

9

REFERENCES

Books and Journals

Almohamad, T.A. and et.al., 2018. Simultaneous determination of modulation types and signal-to-noise ratios using feature-based

approach. IEEE access. 6. pp.9262-9271.

Cleophas, T. J. and Zwinderman, A. H., 2019. Benefit Risk Ratios. In Analysis of Safety Data of Drug Trials (pp. 129-134). Springer,

Cham.

Jiang, F. and et.al., 2019. Anti-corrosion behaviors of epoxy composite coatings enhanced via graphene oxide with different aspect

ratios. Progress in Organic Coatings. 127. pp.70-79.

Netreba, A. and et.al., 2018. Restoration of the protons spatial distribution for different types ratios of the biological

tissues. Molecular Crystals and Liquid Crystals. 673(1). pp.97-108.

Papista, E. and et.al., 2018. Types of value and cost in consumer–green brands relationship and loyalty behaviour. Journal of

Consumer Behaviour. 17(1). pp.e101-e113.

Peng, X. and et.al., 2017. Different responses of terrestrial C, N, and P pools and C/N/P ratios to P, NP, and NPK addition: a meta-

analysis. Water, Air, & Soil Pollution. 228(6). p.197.

Shao, Y. and Billington, S. L., 2020. Flexural performance of steel-reinforced engineered cementitious composites with different

reinforcing ratios and steel types. Construction and Building Materials. 231. p.117159.

Yang, Z. and et.al., 2018. Relationships between product ratios in ambimodal pericyclic reactions and bond lengths in transition

structures. Journal of the American Chemical Society. 140(8). pp.3061-3067.

Zhang, Z. L. and et.al., 2017. Cost-Sensitive back-propagation neural networks with binarization techniques in addressing multi-class

problems and non-competent classifiers. Applied Soft Computing. 56. pp.357-367.

10

Books and Journals

Almohamad, T.A. and et.al., 2018. Simultaneous determination of modulation types and signal-to-noise ratios using feature-based

approach. IEEE access. 6. pp.9262-9271.

Cleophas, T. J. and Zwinderman, A. H., 2019. Benefit Risk Ratios. In Analysis of Safety Data of Drug Trials (pp. 129-134). Springer,

Cham.

Jiang, F. and et.al., 2019. Anti-corrosion behaviors of epoxy composite coatings enhanced via graphene oxide with different aspect

ratios. Progress in Organic Coatings. 127. pp.70-79.

Netreba, A. and et.al., 2018. Restoration of the protons spatial distribution for different types ratios of the biological

tissues. Molecular Crystals and Liquid Crystals. 673(1). pp.97-108.

Papista, E. and et.al., 2018. Types of value and cost in consumer–green brands relationship and loyalty behaviour. Journal of

Consumer Behaviour. 17(1). pp.e101-e113.

Peng, X. and et.al., 2017. Different responses of terrestrial C, N, and P pools and C/N/P ratios to P, NP, and NPK addition: a meta-

analysis. Water, Air, & Soil Pollution. 228(6). p.197.

Shao, Y. and Billington, S. L., 2020. Flexural performance of steel-reinforced engineered cementitious composites with different

reinforcing ratios and steel types. Construction and Building Materials. 231. p.117159.

Yang, Z. and et.al., 2018. Relationships between product ratios in ambimodal pericyclic reactions and bond lengths in transition

structures. Journal of the American Chemical Society. 140(8). pp.3061-3067.

Zhang, Z. L. and et.al., 2017. Cost-Sensitive back-propagation neural networks with binarization techniques in addressing multi-class

problems and non-competent classifiers. Applied Soft Computing. 56. pp.357-367.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.