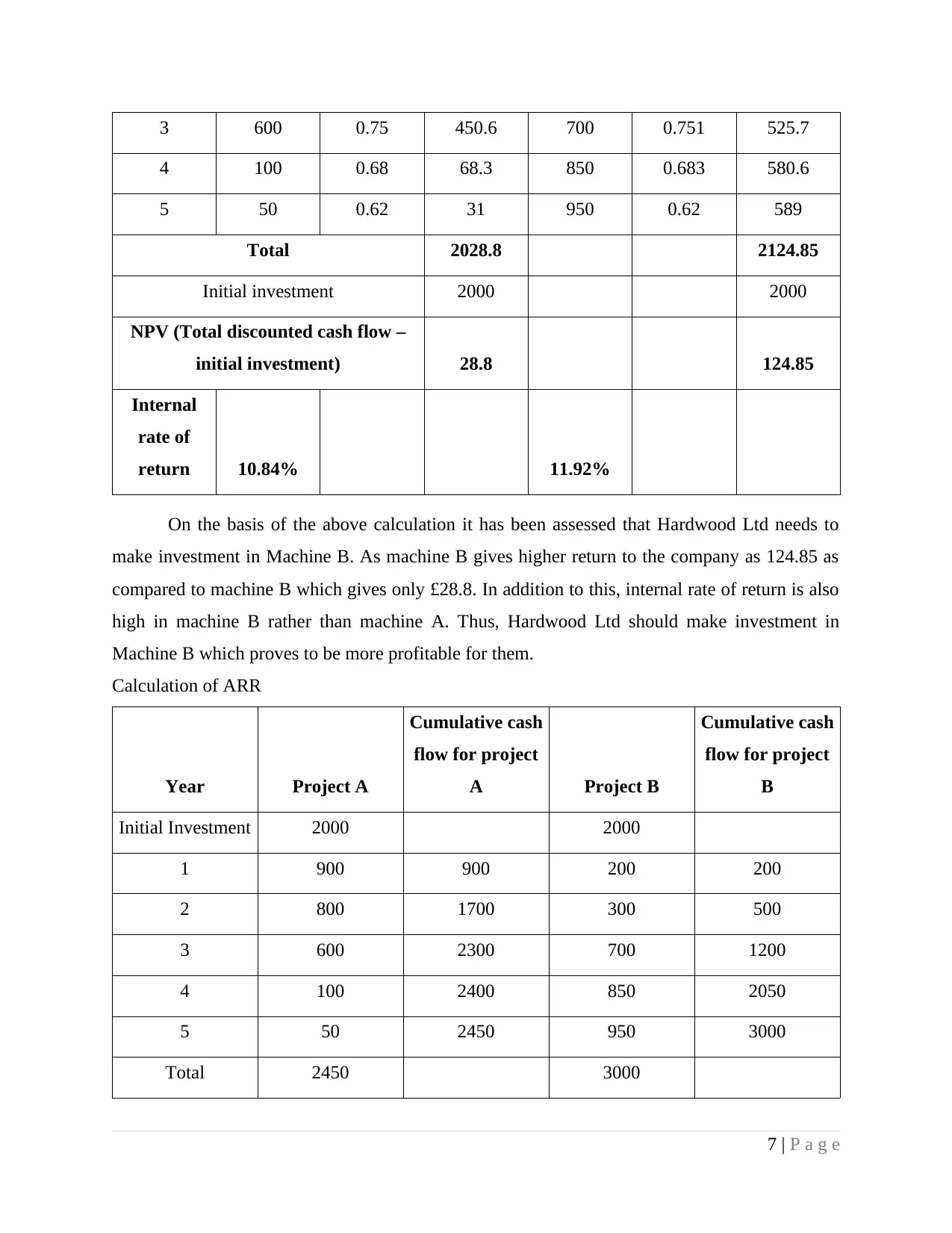

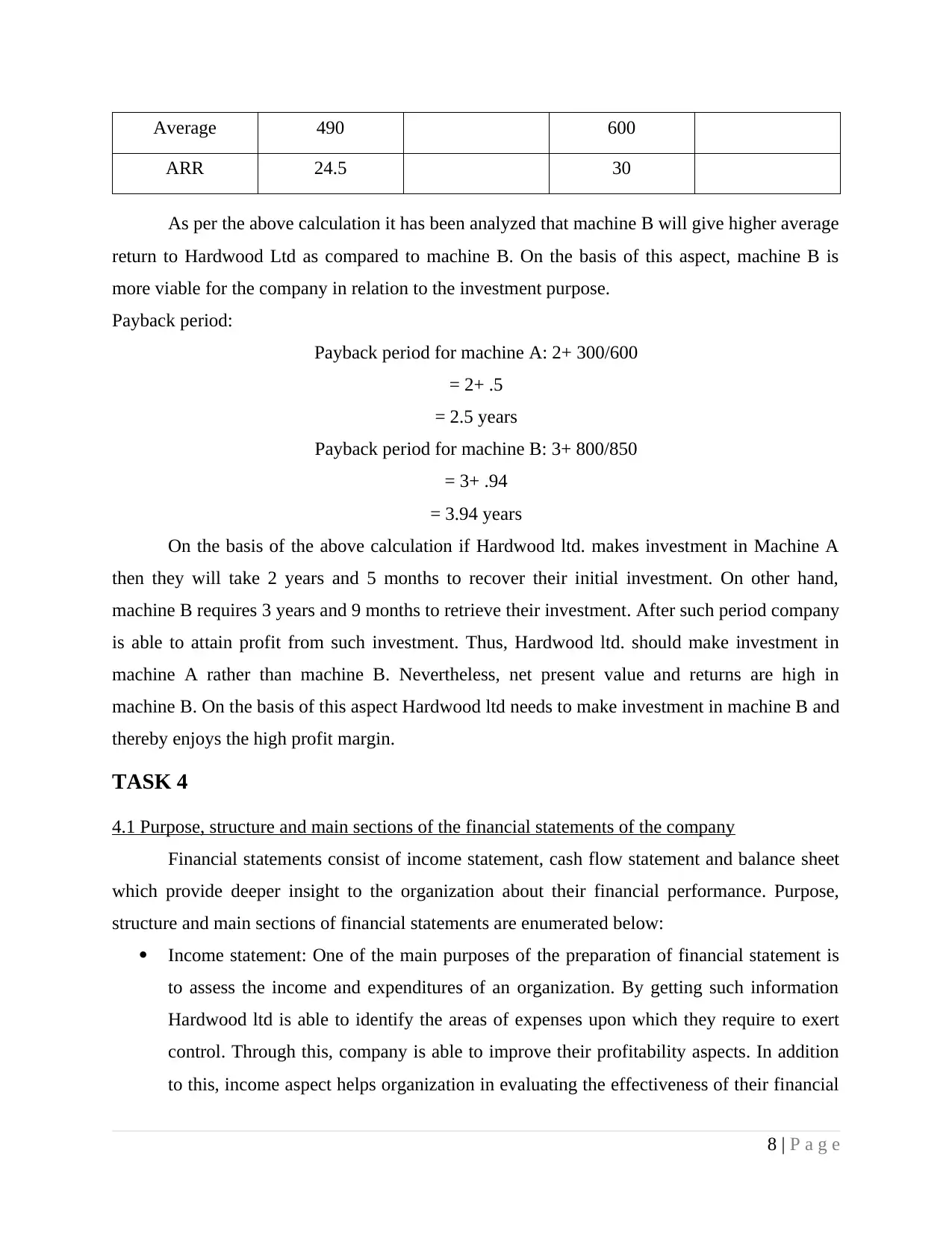

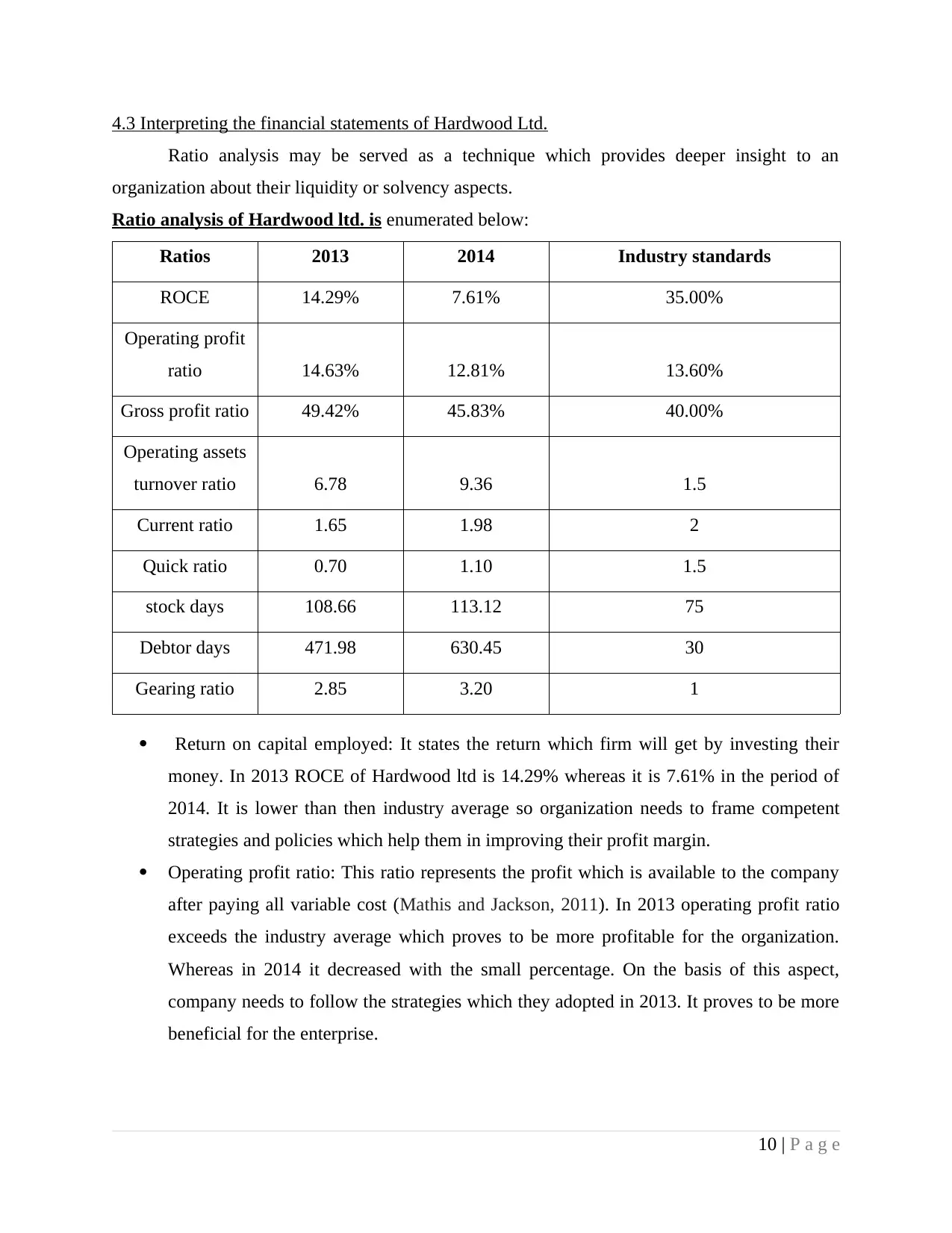

This assignment analyzes the financial performance of Hardwood Ltd. over two years, using various financial ratios such as return on capital employed (ROCE), operating profit ratio, gross profit ratio, operating assets turnover ratio, current ratio, quick ratio, and gearing ratio. The results show that ROCE decreased in 2014 compared to 2013, indicating a need for the company to frame competent strategies to improve its profit margin. Operating profit ratio exceeded the industry average in 2013 but decreased slightly in 2014. Gross profit ratio was higher than the industry average, reflecting sound policies and strategies. Operating assets turnover ratio was near the industry average, indicating optimal use of assets. Current ratio aligned with the industry average, showing sufficient liquidity to meet financial obligations. Quick ratio exceeded the ideal ratio in 2014, suggesting investment opportunities. Stock days were more than the industry average, indicating a need to improve sales. Gearing ratio was higher than the industry average, suggesting reducing dependence on debt for financing. The conclusion is that Hardwood Ltd. should consider taking out a bank loan to fulfill financial needs and invest in machine B.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)