Report on Managing Financial Resources & Decisions for ACME Corp

VerifiedAdded on 2019/12/18

|13

|3813

|34

Report

AI Summary

This report examines the financial resource management strategies for ACME Corporation, a steel manufacturing company considering a factory in the UAE. The report investigates various capital sources, including debt, equity, retained earnings, and leasing, analyzing their implications and proposing an optimal capital structure. It delves into financial planning, budgeting, cost analysis, and investment appraisal techniques, such as payback period and Net Present Value (NPV), to assess project viability. The report also explores the impact of financial decisions on financial statements, including the income statement, balance sheet, and cash flow statement. Furthermore, the report provides interpretations of sales, production, and cash budgets, offering recommendations for cost reduction and improved financial performance. The analysis covers operational, managerial, and strategic financial decisions, providing a comprehensive overview of financial resource management within the context of a major capital investment project.

Managing Financial

Resources & decisions

1

Resources & decisions

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1....................................................................................................................................................3

1.2....................................................................................................................................................3

1.3....................................................................................................................................................3

TASK 2.................................................................................................................................................4

2.1....................................................................................................................................................4

2.2....................................................................................................................................................4

2.3....................................................................................................................................................4

2.4....................................................................................................................................................5

TASK 3.................................................................................................................................................5

3.1....................................................................................................................................................5

3.2....................................................................................................................................................6

3.3....................................................................................................................................................6

TASK 4.................................................................................................................................................6

4.1....................................................................................................................................................6

4.2....................................................................................................................................................6

4.3....................................................................................................................................................7

CONCLUSION....................................................................................................................................7

REFERENCES.....................................................................................................................................8

APPENDIX..........................................................................................................................................9

Appendix 1 Effective cost of interest...............................................................................................9

Appendix 2: Budgeting....................................................................................................................9

Appendix 3: Cost calculation.........................................................................................................10

Appendix 4 Investment appraisal..................................................................................................10

Appendix 5: Ratio analysis............................................................................................................10

2

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1....................................................................................................................................................3

1.2....................................................................................................................................................3

1.3....................................................................................................................................................3

TASK 2.................................................................................................................................................4

2.1....................................................................................................................................................4

2.2....................................................................................................................................................4

2.3....................................................................................................................................................4

2.4....................................................................................................................................................5

TASK 3.................................................................................................................................................5

3.1....................................................................................................................................................5

3.2....................................................................................................................................................6

3.3....................................................................................................................................................6

TASK 4.................................................................................................................................................6

4.1....................................................................................................................................................6

4.2....................................................................................................................................................6

4.3....................................................................................................................................................7

CONCLUSION....................................................................................................................................7

REFERENCES.....................................................................................................................................8

APPENDIX..........................................................................................................................................9

Appendix 1 Effective cost of interest...............................................................................................9

Appendix 2: Budgeting....................................................................................................................9

Appendix 3: Cost calculation.........................................................................................................10

Appendix 4 Investment appraisal..................................................................................................10

Appendix 5: Ratio analysis............................................................................................................10

2

INTRODUCTION

ACME Corporation is a Germany based steel manufacturing company which is considering

setting a factory in UAE at a projected cost of US$175m. Thus, this report will investigate different

capital sources by which it can meet their capital requirement and also use various financial tools

i.e. capital budgeting, forecasting, cost & pricing decisions for the viable decisions.

TASK 1

1.1

Debt: ACME Corporation can apply for the long-term loans from the financial institutions to

finance their expansion project in UAE at the applicable interest charges to acquire fixed assets

(Kumar and Rao, 2016).

Equity: In this, ACM can issue shares to the public and deliver stake in the business to the

investors for the procurement of fund to buy non-current assets. Issuing shares helps to generate

sufficient funds and finance the new project successfully; in return, ACME Corporation needs to

pay dividend to their shareholders.

Retained earnings: Available retained profits can be used by ACME to finance its pre-

operative expense & working capital need. The profits that is available or retained in the business

after the distribution of dividend to the investors, is called retained earnings which can be further

invested by ACME in the business itself to finance the new project.

Lease: Non-current assets can also be acquired on the lease wherein there is no need for the

company to purchase the assets through taking it on rental basis. Every year lease charges will pay

at the starting date till the contracted period in which, lessor charge some interest as a monetary

return.

1.2

Debt-borrowings provide tax benefits but it is too risky because under the financial

implication, fixed interest needs to be paid as per the loan amortization schedule. However, it

prevents the transfer of stake to the lenders at no dilution (Shibata and Nishihara, 2015). Loan

impose bankruptcy implications on the business, because in case of failure in repayment, lenders

have legal authority to dispose-off the security provided by borrower against loans and thereby get

back the loan amount. Unlike it, equity issue transfer controlling rights to the investors, thus,

dilution exists whereas financial implications include dividend payment. The monetary return to the

investors, dividend is not fixed and also not legally compulsory to pay it periodically. The dividend

a decision is taken by the firm based on the availability of return, competitor’s dividend and

3

ACME Corporation is a Germany based steel manufacturing company which is considering

setting a factory in UAE at a projected cost of US$175m. Thus, this report will investigate different

capital sources by which it can meet their capital requirement and also use various financial tools

i.e. capital budgeting, forecasting, cost & pricing decisions for the viable decisions.

TASK 1

1.1

Debt: ACME Corporation can apply for the long-term loans from the financial institutions to

finance their expansion project in UAE at the applicable interest charges to acquire fixed assets

(Kumar and Rao, 2016).

Equity: In this, ACM can issue shares to the public and deliver stake in the business to the

investors for the procurement of fund to buy non-current assets. Issuing shares helps to generate

sufficient funds and finance the new project successfully; in return, ACME Corporation needs to

pay dividend to their shareholders.

Retained earnings: Available retained profits can be used by ACME to finance its pre-

operative expense & working capital need. The profits that is available or retained in the business

after the distribution of dividend to the investors, is called retained earnings which can be further

invested by ACME in the business itself to finance the new project.

Lease: Non-current assets can also be acquired on the lease wherein there is no need for the

company to purchase the assets through taking it on rental basis. Every year lease charges will pay

at the starting date till the contracted period in which, lessor charge some interest as a monetary

return.

1.2

Debt-borrowings provide tax benefits but it is too risky because under the financial

implication, fixed interest needs to be paid as per the loan amortization schedule. However, it

prevents the transfer of stake to the lenders at no dilution (Shibata and Nishihara, 2015). Loan

impose bankruptcy implications on the business, because in case of failure in repayment, lenders

have legal authority to dispose-off the security provided by borrower against loans and thereby get

back the loan amount. Unlike it, equity issue transfer controlling rights to the investors, thus,

dilution exists whereas financial implications include dividend payment. The monetary return to the

investors, dividend is not fixed and also not legally compulsory to pay it periodically. The dividend

a decision is taken by the firm based on the availability of return, competitor’s dividend and

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

investors expectations as well. Besides this, equity also does not offer tax shields to the ACME and

needs to satisfy stock exchange rules and regulations. Interest is the cost of lease on which tax

shields are available which helps to reduce tax burden on entity.

1.3

Neither the collection of only debt nor equity is considered appropriate because of different

implications on the business. Therefore, ACME’s manager must consider a composition of both

borrowings & equity for satisfying their long-term capital need to finance their project in UAE by

proposing the following structure:

Sources of finance Financing

Amount (US

$m)

Debt borrowings (long-term) Plant and machinery 95

Retained profits Pre-operating expense & working capital 32

Shareholder equity Building, land & furniture and fixture 48

Total 175

As per the maximum D/E ratio to 1:1 which states that ACME can borrow maximum capital

at $125m & $55m but it will drive high financial burden due to excessive lending. However, by

collecting $95m and $80m via debt and equity, debt to equity ratio can be managed to 0.73 which is

considered acceptable because ACME has enough availability of profit which it can use to meet

interest payment.

TASK 2

2.1

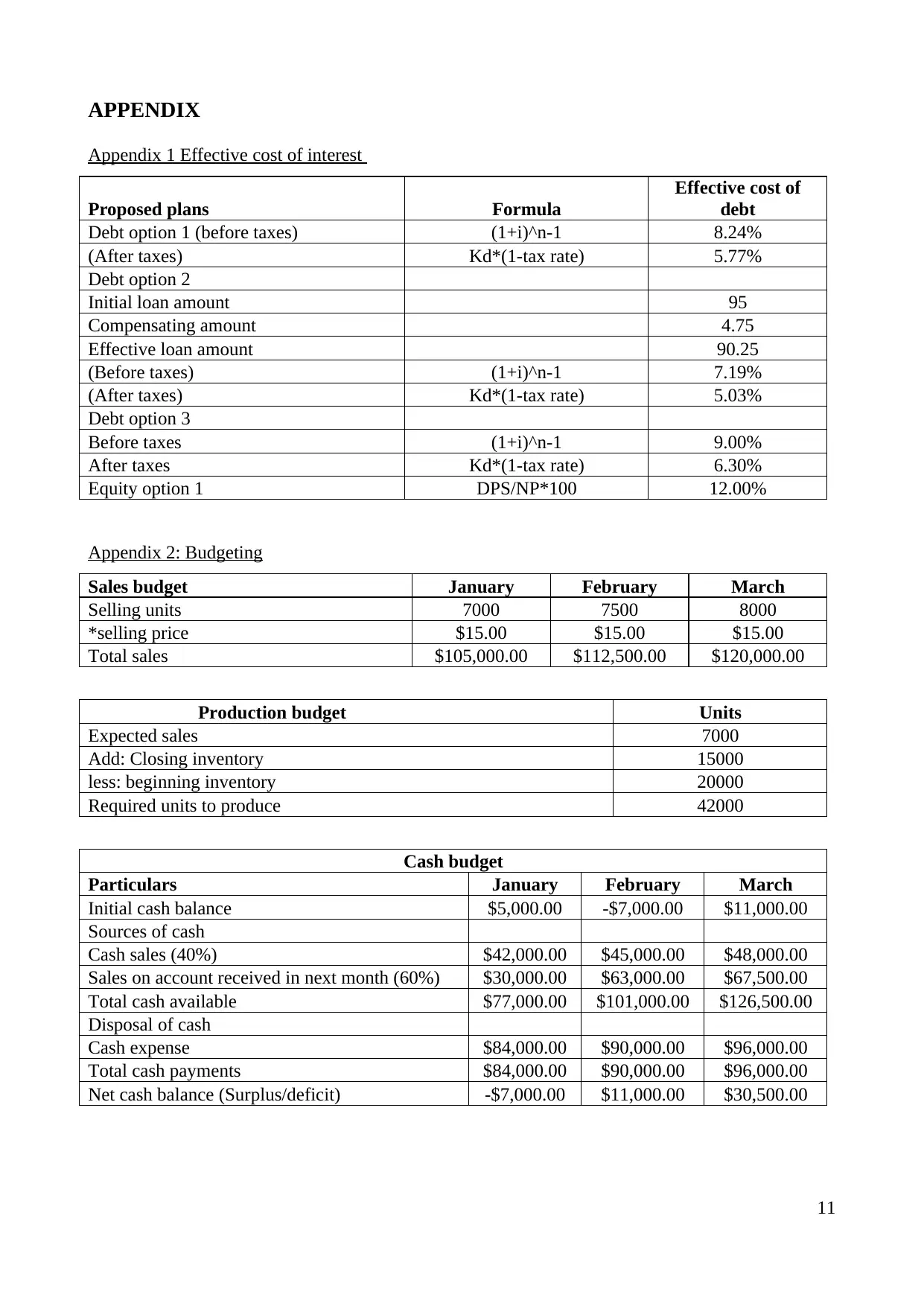

Appendix 1

Interest is the cost of debt and lease financing and leasing whereas on equity, dividend is the

financial cost (Malik, Field and Gorwood, 2016). As per the results, it is founded that under 1st, 2nd

and 3rd option, effective cost of debt has been derived to 5.77%, 5.03% & 6.30% respectively.

However, under the last option, ACME has been considering to receive funds through investment,

thus, there is no tax benefits associated on the same, hence, return rate will be the effective cost

derived to 12.00%. It is lowest in the second option thus, it is better to suggest ACME to use 2nd

debt option and remaining & remaining through equity to manage a balance in the CS.

2.2

Financial planning refers to the procurement of required funds and devising policies and

strategies for the efficient fund management for ensuring smooth functioning (Revell, 2016). It is

the process of identifying the proposed capital requirement of the business and design policies and

4

needs to satisfy stock exchange rules and regulations. Interest is the cost of lease on which tax

shields are available which helps to reduce tax burden on entity.

1.3

Neither the collection of only debt nor equity is considered appropriate because of different

implications on the business. Therefore, ACME’s manager must consider a composition of both

borrowings & equity for satisfying their long-term capital need to finance their project in UAE by

proposing the following structure:

Sources of finance Financing

Amount (US

$m)

Debt borrowings (long-term) Plant and machinery 95

Retained profits Pre-operating expense & working capital 32

Shareholder equity Building, land & furniture and fixture 48

Total 175

As per the maximum D/E ratio to 1:1 which states that ACME can borrow maximum capital

at $125m & $55m but it will drive high financial burden due to excessive lending. However, by

collecting $95m and $80m via debt and equity, debt to equity ratio can be managed to 0.73 which is

considered acceptable because ACME has enough availability of profit which it can use to meet

interest payment.

TASK 2

2.1

Appendix 1

Interest is the cost of debt and lease financing and leasing whereas on equity, dividend is the

financial cost (Malik, Field and Gorwood, 2016). As per the results, it is founded that under 1st, 2nd

and 3rd option, effective cost of debt has been derived to 5.77%, 5.03% & 6.30% respectively.

However, under the last option, ACME has been considering to receive funds through investment,

thus, there is no tax benefits associated on the same, hence, return rate will be the effective cost

derived to 12.00%. It is lowest in the second option thus, it is better to suggest ACME to use 2nd

debt option and remaining & remaining through equity to manage a balance in the CS.

2.2

Financial planning refers to the procurement of required funds and devising policies and

strategies for the efficient fund management for ensuring smooth functioning (Revell, 2016). It is

the process of identifying the proposed capital requirement of the business and design policies and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

plans accordingly to meet out the financial requirement of the entity.

Importance

1. Collection of required capital to finance the UAE project by gathering funds through designing

an efficient capital structure including debt borrowings and share capital to manage cost

2. Mitigate working capital, and long-term financial requirement

3. Managing business cost by designing rationalized cost curtailment strategies such as monitoring

and boost saving through effective management

4. Closure supervision & controlling encourage optimum utilization of funds at minimal wastage

5. Safeguard against possible financial risk & prospective consequences i.e. high cost of

borrowing, sudden fluctuation in demand and others

2.3

Operational: It includes regular activities and short-term decisions which are taken by

lower managerial level to make well informed decisions. They require results about operational

income, sales, expense and comparison of actual results with the targets to find out deviations to set

right decisions. For instance, marketing, credit collection policy and other decisions are taken at

operational level.

Managerial: At the managerial level, ACME’s middle level departments have to create

policies, plans, define hierarchy and make strategies for the acquisition of required sources,

allocation and optimum management (Finkler and et.al., 2016 ). They also monitor & supervise

regular staff activities to make on-time decisions and enhance results.

Strategic: It comprises business processes, practices and procedures which require

information regarding dynamic market environment, external conditions, business performance,

solvency and liquidity position and others so as to create the right strategies at the upper level

management. They set targets and make strategic plans to achieve the same such as long-term fund

gathering decisions to mange financial risk and others.

2.4

Interest is reported in income statement of the firm which in turn reduces the return. High

amount of debt as compared to equity will raise the long-term borrowings in the ACME’s liability

side and impose fixed burden. High financing cost will raise the monetary burden in income

statement and decline the yield also (Malik, Field and Gorwood, 2016). In the cash flow statement,

it will be recorded in the cash inflow/outflow from financing activities. Besides this, increasing tax

rate from 30% to 40% bring excessive tax obligations and decrease cash and net profit as well.

5

Importance

1. Collection of required capital to finance the UAE project by gathering funds through designing

an efficient capital structure including debt borrowings and share capital to manage cost

2. Mitigate working capital, and long-term financial requirement

3. Managing business cost by designing rationalized cost curtailment strategies such as monitoring

and boost saving through effective management

4. Closure supervision & controlling encourage optimum utilization of funds at minimal wastage

5. Safeguard against possible financial risk & prospective consequences i.e. high cost of

borrowing, sudden fluctuation in demand and others

2.3

Operational: It includes regular activities and short-term decisions which are taken by

lower managerial level to make well informed decisions. They require results about operational

income, sales, expense and comparison of actual results with the targets to find out deviations to set

right decisions. For instance, marketing, credit collection policy and other decisions are taken at

operational level.

Managerial: At the managerial level, ACME’s middle level departments have to create

policies, plans, define hierarchy and make strategies for the acquisition of required sources,

allocation and optimum management (Finkler and et.al., 2016 ). They also monitor & supervise

regular staff activities to make on-time decisions and enhance results.

Strategic: It comprises business processes, practices and procedures which require

information regarding dynamic market environment, external conditions, business performance,

solvency and liquidity position and others so as to create the right strategies at the upper level

management. They set targets and make strategic plans to achieve the same such as long-term fund

gathering decisions to mange financial risk and others.

2.4

Interest is reported in income statement of the firm which in turn reduces the return. High

amount of debt as compared to equity will raise the long-term borrowings in the ACME’s liability

side and impose fixed burden. High financing cost will raise the monetary burden in income

statement and decline the yield also (Malik, Field and Gorwood, 2016). In the cash flow statement,

it will be recorded in the cash inflow/outflow from financing activities. Besides this, increasing tax

rate from 30% to 40% bring excessive tax obligations and decrease cash and net profit as well.

5

Further, dividend is deducted from the net profit to find out the balance of profit available thus, if

investor pushes ACME to pay more return then it will decline the retained profits and cash balance

in the balance sheet. However, on the other side, amount collected through share capital will be

reported under equity capital head of balance sheet and in the statement of cash flow, it will be the

part of financing activities. Besides this, long-term lease is reported in the long-term liability of the

balance sheet.

TASK 3

3.1

Appendix 2

Interpretation: Sales budget of ACME Corporation founded that expected turnover for the

first quarter will be $105,000, $112,500 & $120,000 respectively. It indicates that ACME

Corporation will generate growing sales over the budgeted period but it will be increase at declined

rate of 7.14% and 6.67% respectively.

Interpretation: Production budget identify the number of units that is required to tbe

produce by ACME Corporation to meet out its consumer demand. In order to satisfy the market

demand, ACME’s production department has to produce 42000 units to offer required quantum of

products to the clients.

Interpretation: Cash budget reflects that ACME’s sales policy is based on 40% cash basis

sales and remaining 60% on credit for 1 month duration. In total, the expected cash receipts for first

three month are computed to $77,000, $101,000 & $126,500 respectively. In contrast, disposal of

cash has been derived to $84,000, $90,000 & $96,000; thus, per unit expenses remain fixed to $12.

In first month, it reported shortfall of $7,000 and thereafter surplus balance worth $11,000 &

$30,500 respectively.

Recommendation:

Reduction in cost and overheads to $12/unit by cost-curtailment & tighten controlling &

supervision (Kim and et.al., 2016)

Effective advertisement, promotional campaign, marketing, attractive discount offers

Granting less credit period to receivables and boost sales on cash basis helps to generate

cash quickly in the business

3.2

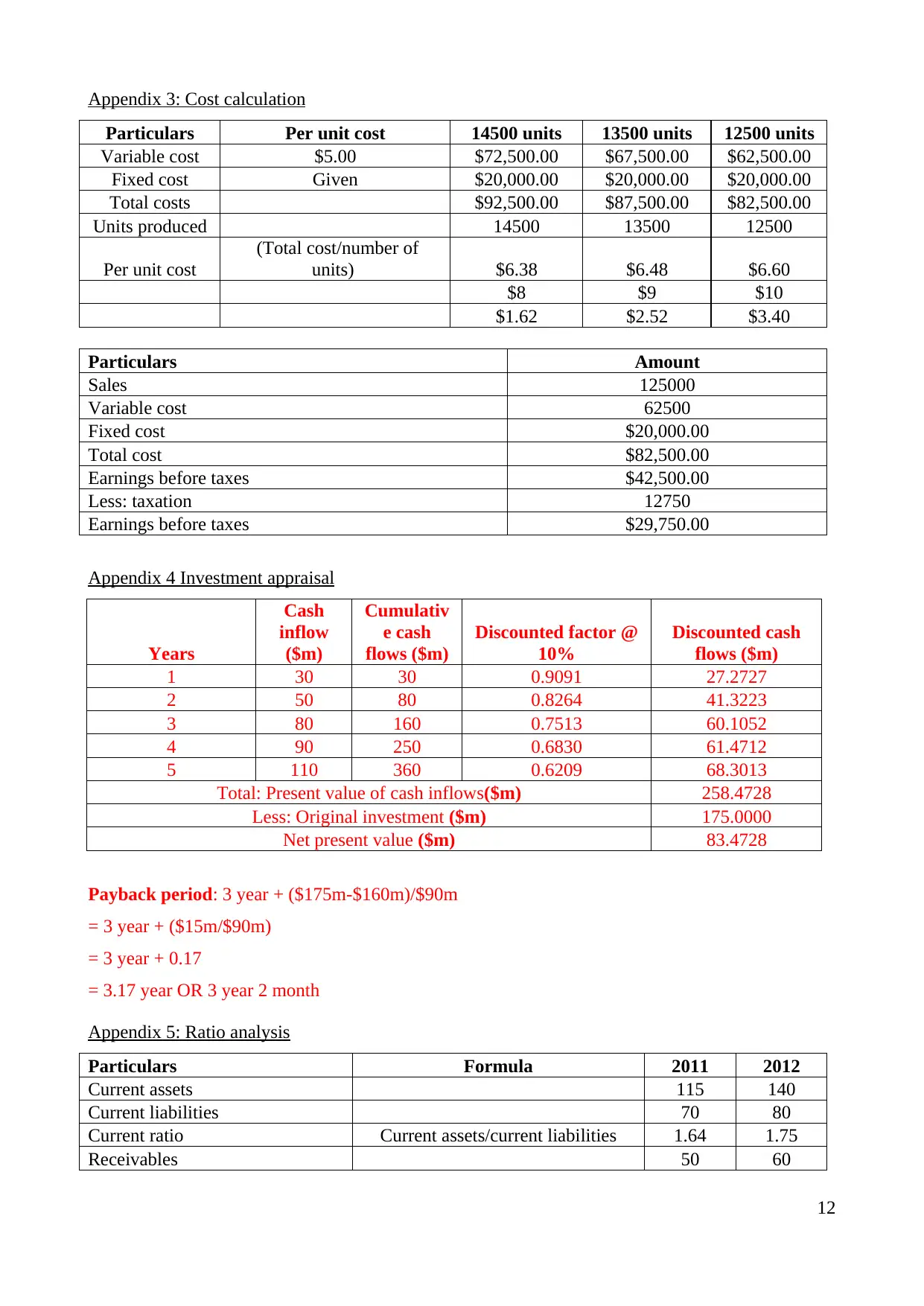

Appendix 3

Total costs = Total fixed cost + total variable cost

Units costs = Total cost/Number of units produced

6

investor pushes ACME to pay more return then it will decline the retained profits and cash balance

in the balance sheet. However, on the other side, amount collected through share capital will be

reported under equity capital head of balance sheet and in the statement of cash flow, it will be the

part of financing activities. Besides this, long-term lease is reported in the long-term liability of the

balance sheet.

TASK 3

3.1

Appendix 2

Interpretation: Sales budget of ACME Corporation founded that expected turnover for the

first quarter will be $105,000, $112,500 & $120,000 respectively. It indicates that ACME

Corporation will generate growing sales over the budgeted period but it will be increase at declined

rate of 7.14% and 6.67% respectively.

Interpretation: Production budget identify the number of units that is required to tbe

produce by ACME Corporation to meet out its consumer demand. In order to satisfy the market

demand, ACME’s production department has to produce 42000 units to offer required quantum of

products to the clients.

Interpretation: Cash budget reflects that ACME’s sales policy is based on 40% cash basis

sales and remaining 60% on credit for 1 month duration. In total, the expected cash receipts for first

three month are computed to $77,000, $101,000 & $126,500 respectively. In contrast, disposal of

cash has been derived to $84,000, $90,000 & $96,000; thus, per unit expenses remain fixed to $12.

In first month, it reported shortfall of $7,000 and thereafter surplus balance worth $11,000 &

$30,500 respectively.

Recommendation:

Reduction in cost and overheads to $12/unit by cost-curtailment & tighten controlling &

supervision (Kim and et.al., 2016)

Effective advertisement, promotional campaign, marketing, attractive discount offers

Granting less credit period to receivables and boost sales on cash basis helps to generate

cash quickly in the business

3.2

Appendix 3

Total costs = Total fixed cost + total variable cost

Units costs = Total cost/Number of units produced

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

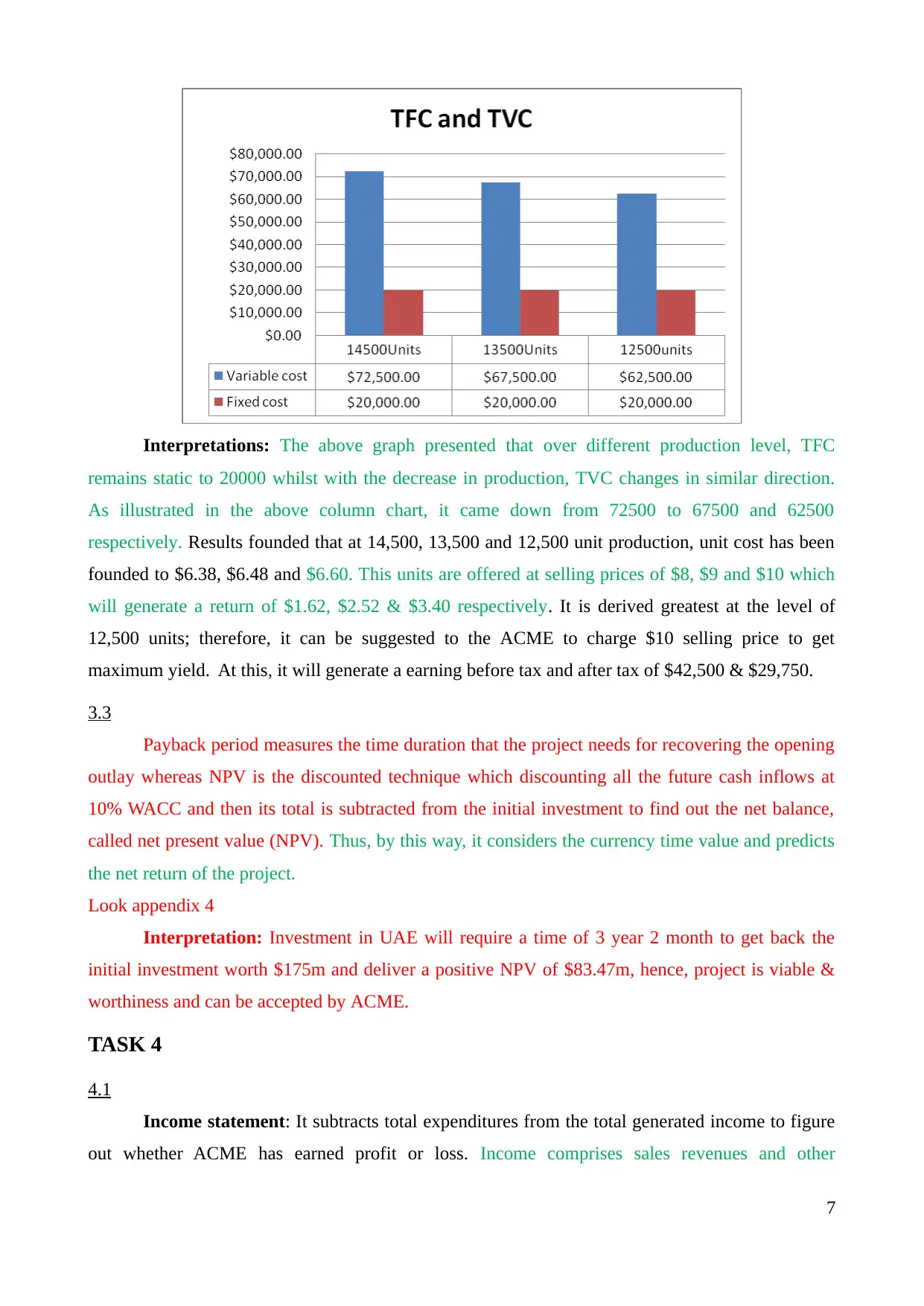

Interpretations: The above graph presented that over different production level, TFC

remains static to 20000 whilst with the decrease in production, TVC changes in similar direction.

As illustrated in the above column chart, it came down from 72500 to 67500 and 62500

respectively. Results founded that at 14,500, 13,500 and 12,500 unit production, unit cost has been

founded to $6.38, $6.48 and $6.60. This units are offered at selling prices of $8, $9 and $10 which

will generate a return of $1.62, $2.52 & $3.40 respectively. It is derived greatest at the level of

12,500 units; therefore, it can be suggested to the ACME to charge $10 selling price to get

maximum yield. At this, it will generate a earning before tax and after tax of $42,500 & $29,750.

3.3

Payback period measures the time duration that the project needs for recovering the opening

outlay whereas NPV is the discounted technique which discounting all the future cash inflows at

10% WACC and then its total is subtracted from the initial investment to find out the net balance,

called net present value (NPV). Thus, by this way, it considers the currency time value and predicts

the net return of the project.

Look appendix 4

Interpretation: Investment in UAE will require a time of 3 year 2 month to get back the

initial investment worth $175m and deliver a positive NPV of $83.47m, hence, project is viable &

worthiness and can be accepted by ACME.

TASK 4

4.1

Income statement: It subtracts total expenditures from the total generated income to figure

out whether ACME has earned profit or loss. Income comprises sales revenues and other

7

remains static to 20000 whilst with the decrease in production, TVC changes in similar direction.

As illustrated in the above column chart, it came down from 72500 to 67500 and 62500

respectively. Results founded that at 14,500, 13,500 and 12,500 unit production, unit cost has been

founded to $6.38, $6.48 and $6.60. This units are offered at selling prices of $8, $9 and $10 which

will generate a return of $1.62, $2.52 & $3.40 respectively. It is derived greatest at the level of

12,500 units; therefore, it can be suggested to the ACME to charge $10 selling price to get

maximum yield. At this, it will generate a earning before tax and after tax of $42,500 & $29,750.

3.3

Payback period measures the time duration that the project needs for recovering the opening

outlay whereas NPV is the discounted technique which discounting all the future cash inflows at

10% WACC and then its total is subtracted from the initial investment to find out the net balance,

called net present value (NPV). Thus, by this way, it considers the currency time value and predicts

the net return of the project.

Look appendix 4

Interpretation: Investment in UAE will require a time of 3 year 2 month to get back the

initial investment worth $175m and deliver a positive NPV of $83.47m, hence, project is viable &

worthiness and can be accepted by ACME.

TASK 4

4.1

Income statement: It subtracts total expenditures from the total generated income to figure

out whether ACME has earned profit or loss. Income comprises sales revenues and other

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operational revenues whereas expenses include sales, general & administration cost, interest, taxes

and others. In this, only operational transactions are recorded following accrual accounting concept.

Gross profit/loss: Sales – cost of sale

Net profit/loss: Total revenues – Total expenditures

Balance sheet: It indicates a true financial picture by reporting current assets (receivables,

cash etc.), current liabilities (payables, short-term debt), long-term assets (property and plant) and

non-current liabilities (debt) and excess of total assets over liabilities is reported as investor equity

(Malik, Field and Gorwood, 2016). Its target aim is to determine the financial position or health of

the enterprise by finding solvency position, liquidity status and efficiency as well.

Cash flow statement: It reports cash inflow & its disposal from operational (regular

merchandising), financing (debt and equity) and investing (buy and sell of fixed assets) activities to

figure out the ending cash. It helps to determine the detailed reasons behind changes in the net cash

position at two distinctive balance sheet dates.

4.2

Sole proprietor reports owner’s capital in the balance sheet whereas; partnership showcase

all the partner’s closing capital which is figured out by preparing partners capital account. Unlike

this, companies like ACME Corporation do not need to construct such account and investors equity

capital is presented in capital section which financed its assets (Kaplan and Atkinson, 2015).

Moreover, company prepare their annual account in a standard format following international

financial reporting standard (IFRS) & IAS. Further, sole trader do not prepare P&L appropriation

a/c whereas partners prepare it for the distribution of return, interest on capital, loan & drawings &

other just following the principles without any agreed or specified format. Unlike it, ACME

prepares SOFP, SOCI and SOCF in an agreed format for ensuring greater transparency.

4.3

Appendix 5

Current ratio: In 2012, ACME’s CR gone up from 1.64:1 to 1.75:1 due to 21.74% YOY

growth in CA above than YOY growth in CL by 14.29% reflects strong liquidity position. Little bit

increase in CA can assist ACME to achieve idle ratio of 2:1 and improve the liquidity position.

Accounts receivables: It improved from 1.60 times to 1.67 times show quicker conversion

of receivables into cash for the having adequate cash in the business. Company must make policies

like credit collection policies to generate cash promptly from the debtors and thereby manage cash

position.

Time to interest ratio: It dropped from 6 to 4.33 times due to higher interest reflects that

8

and others. In this, only operational transactions are recorded following accrual accounting concept.

Gross profit/loss: Sales – cost of sale

Net profit/loss: Total revenues – Total expenditures

Balance sheet: It indicates a true financial picture by reporting current assets (receivables,

cash etc.), current liabilities (payables, short-term debt), long-term assets (property and plant) and

non-current liabilities (debt) and excess of total assets over liabilities is reported as investor equity

(Malik, Field and Gorwood, 2016). Its target aim is to determine the financial position or health of

the enterprise by finding solvency position, liquidity status and efficiency as well.

Cash flow statement: It reports cash inflow & its disposal from operational (regular

merchandising), financing (debt and equity) and investing (buy and sell of fixed assets) activities to

figure out the ending cash. It helps to determine the detailed reasons behind changes in the net cash

position at two distinctive balance sheet dates.

4.2

Sole proprietor reports owner’s capital in the balance sheet whereas; partnership showcase

all the partner’s closing capital which is figured out by preparing partners capital account. Unlike

this, companies like ACME Corporation do not need to construct such account and investors equity

capital is presented in capital section which financed its assets (Kaplan and Atkinson, 2015).

Moreover, company prepare their annual account in a standard format following international

financial reporting standard (IFRS) & IAS. Further, sole trader do not prepare P&L appropriation

a/c whereas partners prepare it for the distribution of return, interest on capital, loan & drawings &

other just following the principles without any agreed or specified format. Unlike it, ACME

prepares SOFP, SOCI and SOCF in an agreed format for ensuring greater transparency.

4.3

Appendix 5

Current ratio: In 2012, ACME’s CR gone up from 1.64:1 to 1.75:1 due to 21.74% YOY

growth in CA above than YOY growth in CL by 14.29% reflects strong liquidity position. Little bit

increase in CA can assist ACME to achieve idle ratio of 2:1 and improve the liquidity position.

Accounts receivables: It improved from 1.60 times to 1.67 times show quicker conversion

of receivables into cash for the having adequate cash in the business. Company must make policies

like credit collection policies to generate cash promptly from the debtors and thereby manage cash

position.

Time to interest ratio: It dropped from 6 to 4.33 times due to higher interest reflects that

8

firm do not has excessive return to meet timely payment of interest on debt. It suggests the business

to focus on profit maximization by sales increase and control over costs, so that, it can financially

strong and able to take additional borrowings.

ROE: It goes up from 12.73% to 13.33% due to better return as it gone up by 14.29% in

2012 demonstrates good return on equity (Kim and et.al., 2016). Increased net earnings in this year

by 14.29% are the reason behind high ROE which satisfy investors.

EPS: In 2012, ACME’s investor gained higher return on each holding to 0.32 due to better

yield at given number of shares.

Dividend payout ratio: It has been grown from 0.29 to 0.38 times which reflects that

ACME distributed higher dividend to their investors out of their earnings.

CONCLUSION

Report concluded that ACME must use a composition of debt & equity to finance its UAE

project and manage effectively their financing activities through monetary planning. Besides this,

cash budget founded that credit policy must be amended to drive in more cash sales and decrease

credit sales from 60%. Capital budgeting identified that project is viable and worthy hence, ACME

must invest 175m. Lastly, performance analysis founded that ACME’s operational performance and

financial position has been improved in 2012.

9

to focus on profit maximization by sales increase and control over costs, so that, it can financially

strong and able to take additional borrowings.

ROE: It goes up from 12.73% to 13.33% due to better return as it gone up by 14.29% in

2012 demonstrates good return on equity (Kim and et.al., 2016). Increased net earnings in this year

by 14.29% are the reason behind high ROE which satisfy investors.

EPS: In 2012, ACME’s investor gained higher return on each holding to 0.32 due to better

yield at given number of shares.

Dividend payout ratio: It has been grown from 0.29 to 0.38 times which reflects that

ACME distributed higher dividend to their investors out of their earnings.

CONCLUSION

Report concluded that ACME must use a composition of debt & equity to finance its UAE

project and manage effectively their financing activities through monetary planning. Besides this,

cash budget founded that credit policy must be amended to drive in more cash sales and decrease

credit sales from 60%. Capital budgeting identified that project is viable and worthy hence, ACME

must invest 175m. Lastly, performance analysis founded that ACME’s operational performance and

financial position has been improved in 2012.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Kim, J.B. and et.al., 2016. Financial statement comparability and expected crash risk. Journal of

Accounting and Economics. 61(2). pp. 294-312.

Finkler, S. A. and et.al., 2016. Financial management for public, health, and not-for-profit

organizations. CQ Press.

Revell, J., 2016. The recent evolution of financial systems. Springer.

Shibata, T. and Nishihara, M., 2015. Investment timing, debt structure, and financing

constraints. European Journal of Operational Research. 241(2). pp. 513-526.

Kumar, K. K. and Rao, P. B., 2016. A Book Review of “Strategic Financial Management: Managing

for Value Creation” by Dr. Prasanna Chandra. Indian Journal of Finance. 10(12). pp. 56-64.

Malik, A., Field, C. and Gorwood, P., 2016. Managing financial resources in healthcare

settings. Psychiatry in Practice: Education, Experience, and Expertise. pp.45-69.

10

Books and Journals

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Kim, J.B. and et.al., 2016. Financial statement comparability and expected crash risk. Journal of

Accounting and Economics. 61(2). pp. 294-312.

Finkler, S. A. and et.al., 2016. Financial management for public, health, and not-for-profit

organizations. CQ Press.

Revell, J., 2016. The recent evolution of financial systems. Springer.

Shibata, T. and Nishihara, M., 2015. Investment timing, debt structure, and financing

constraints. European Journal of Operational Research. 241(2). pp. 513-526.

Kumar, K. K. and Rao, P. B., 2016. A Book Review of “Strategic Financial Management: Managing

for Value Creation” by Dr. Prasanna Chandra. Indian Journal of Finance. 10(12). pp. 56-64.

Malik, A., Field, C. and Gorwood, P., 2016. Managing financial resources in healthcare

settings. Psychiatry in Practice: Education, Experience, and Expertise. pp.45-69.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Appendix 1 Effective cost of interest

Proposed plans Formula

Effective cost of

debt

Debt option 1 (before taxes) (1+i)^n-1 8.24%

(After taxes) Kd*(1-tax rate) 5.77%

Debt option 2

Initial loan amount 95

Compensating amount 4.75

Effective loan amount 90.25

(Before taxes) (1+i)^n-1 7.19%

(After taxes) Kd*(1-tax rate) 5.03%

Debt option 3

Before taxes (1+i)^n-1 9.00%

After taxes Kd*(1-tax rate) 6.30%

Equity option 1 DPS/NP*100 12.00%

Appendix 2: Budgeting

Sales budget January February March

Selling units 7000 7500 8000

*selling price $15.00 $15.00 $15.00

Total sales $105,000.00 $112,500.00 $120,000.00

Production budget Units

Expected sales 7000

Add: Closing inventory 15000

less: beginning inventory 20000

Required units to produce 42000

Cash budget

Particulars January February March

Initial cash balance $5,000.00 -$7,000.00 $11,000.00

Sources of cash

Cash sales (40%) $42,000.00 $45,000.00 $48,000.00

Sales on account received in next month (60%) $30,000.00 $63,000.00 $67,500.00

Total cash available $77,000.00 $101,000.00 $126,500.00

Disposal of cash

Cash expense $84,000.00 $90,000.00 $96,000.00

Total cash payments $84,000.00 $90,000.00 $96,000.00

Net cash balance (Surplus/deficit) -$7,000.00 $11,000.00 $30,500.00

11

Appendix 1 Effective cost of interest

Proposed plans Formula

Effective cost of

debt

Debt option 1 (before taxes) (1+i)^n-1 8.24%

(After taxes) Kd*(1-tax rate) 5.77%

Debt option 2

Initial loan amount 95

Compensating amount 4.75

Effective loan amount 90.25

(Before taxes) (1+i)^n-1 7.19%

(After taxes) Kd*(1-tax rate) 5.03%

Debt option 3

Before taxes (1+i)^n-1 9.00%

After taxes Kd*(1-tax rate) 6.30%

Equity option 1 DPS/NP*100 12.00%

Appendix 2: Budgeting

Sales budget January February March

Selling units 7000 7500 8000

*selling price $15.00 $15.00 $15.00

Total sales $105,000.00 $112,500.00 $120,000.00

Production budget Units

Expected sales 7000

Add: Closing inventory 15000

less: beginning inventory 20000

Required units to produce 42000

Cash budget

Particulars January February March

Initial cash balance $5,000.00 -$7,000.00 $11,000.00

Sources of cash

Cash sales (40%) $42,000.00 $45,000.00 $48,000.00

Sales on account received in next month (60%) $30,000.00 $63,000.00 $67,500.00

Total cash available $77,000.00 $101,000.00 $126,500.00

Disposal of cash

Cash expense $84,000.00 $90,000.00 $96,000.00

Total cash payments $84,000.00 $90,000.00 $96,000.00

Net cash balance (Surplus/deficit) -$7,000.00 $11,000.00 $30,500.00

11

Appendix 3: Cost calculation

Particulars Per unit cost 14500 units 13500 units 12500 units

Variable cost $5.00 $72,500.00 $67,500.00 $62,500.00

Fixed cost Given $20,000.00 $20,000.00 $20,000.00

Total costs $92,500.00 $87,500.00 $82,500.00

Units produced 14500 13500 12500

Per unit cost

(Total cost/number of

units) $6.38 $6.48 $6.60

$8 $9 $10

$1.62 $2.52 $3.40

Particulars Amount

Sales 125000

Variable cost 62500

Fixed cost $20,000.00

Total cost $82,500.00

Earnings before taxes $42,500.00

Less: taxation 12750

Earnings before taxes $29,750.00

Appendix 4 Investment appraisal

Years

Cash

inflow

($m)

Cumulativ

e cash

flows ($m)

Discounted factor @

10%

Discounted cash

flows ($m)

1 30 30 0.9091 27.2727

2 50 80 0.8264 41.3223

3 80 160 0.7513 60.1052

4 90 250 0.6830 61.4712

5 110 360 0.6209 68.3013

Total: Present value of cash inflows($m) 258.4728

Less: Original investment ($m) 175.0000

Net present value ($m) 83.4728

Payback period: 3 year + ($175m-$160m)/$90m

= 3 year + ($15m/$90m)

= 3 year + 0.17

= 3.17 year OR 3 year 2 month

Appendix 5: Ratio analysis

Particulars Formula 2011 2012

Current assets 115 140

Current liabilities 70 80

Current ratio Current assets/current liabilities 1.64 1.75

Receivables 50 60

12

Particulars Per unit cost 14500 units 13500 units 12500 units

Variable cost $5.00 $72,500.00 $67,500.00 $62,500.00

Fixed cost Given $20,000.00 $20,000.00 $20,000.00

Total costs $92,500.00 $87,500.00 $82,500.00

Units produced 14500 13500 12500

Per unit cost

(Total cost/number of

units) $6.38 $6.48 $6.60

$8 $9 $10

$1.62 $2.52 $3.40

Particulars Amount

Sales 125000

Variable cost 62500

Fixed cost $20,000.00

Total cost $82,500.00

Earnings before taxes $42,500.00

Less: taxation 12750

Earnings before taxes $29,750.00

Appendix 4 Investment appraisal

Years

Cash

inflow

($m)

Cumulativ

e cash

flows ($m)

Discounted factor @

10%

Discounted cash

flows ($m)

1 30 30 0.9091 27.2727

2 50 80 0.8264 41.3223

3 80 160 0.7513 60.1052

4 90 250 0.6830 61.4712

5 110 360 0.6209 68.3013

Total: Present value of cash inflows($m) 258.4728

Less: Original investment ($m) 175.0000

Net present value ($m) 83.4728

Payback period: 3 year + ($175m-$160m)/$90m

= 3 year + ($15m/$90m)

= 3 year + 0.17

= 3.17 year OR 3 year 2 month

Appendix 5: Ratio analysis

Particulars Formula 2011 2012

Current assets 115 140

Current liabilities 70 80

Current ratio Current assets/current liabilities 1.64 1.75

Receivables 50 60

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.