Financial Management Analysis and Recommendations Report

VerifiedAdded on 2020/02/17

|21

|5783

|62

Report

AI Summary

This report provides a comprehensive financial management analysis of Clariton Antiques Ltd, an unincorporated business specializing in antiques. It explores various sources of finance, including personal savings, bank loans, retained earnings, and venture capital, comparing the implications of internal and external funding. The report assesses the costs associated with different financing options, such as dividends and interest, and highlights the importance of financial planning, including budgeting and economic forecasting. It also examines unit cost and pricing decisions, investment decisions, and the components and formats of financial statements. Furthermore, the report includes a comparative analysis of financial ratios to evaluate the financial performance of Clariton Antiques Ltd. The report offers insights into making effective financial decisions and managing financial resources to ensure profitability and sustainability.

Managing Financial Resources

and Decisions

and Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Unincorporated and incorporated business and sources of finance.......................................3

1.2 Internal and external sources along with their implications..................................................4

1.3 Appropriate source of finance................................................................................................5

Task 2...............................................................................................................................................6

2.1 Cost of sources of finance......................................................................................................6

2.2 Importance of financial planning...........................................................................................7

2.3 Requirement of information for making effective decision...................................................8

2.4 Impact on financial statements..............................................................................................9

Task 3.............................................................................................................................................10

3.1 Cash budget..........................................................................................................................10

3.2 Unit cost and pricing decisions............................................................................................11

3.3 Investment decisions............................................................................................................11

Task 4.............................................................................................................................................14

4.1 Components of financial statements....................................................................................14

4.2 Formats of financial statements...........................................................................................14

4.3 Comparison of financial ratios.............................................................................................17

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Unincorporated and incorporated business and sources of finance.......................................3

1.2 Internal and external sources along with their implications..................................................4

1.3 Appropriate source of finance................................................................................................5

Task 2...............................................................................................................................................6

2.1 Cost of sources of finance......................................................................................................6

2.2 Importance of financial planning...........................................................................................7

2.3 Requirement of information for making effective decision...................................................8

2.4 Impact on financial statements..............................................................................................9

Task 3.............................................................................................................................................10

3.1 Cash budget..........................................................................................................................10

3.2 Unit cost and pricing decisions............................................................................................11

3.3 Investment decisions............................................................................................................11

Task 4.............................................................................................................................................14

4.1 Components of financial statements....................................................................................14

4.2 Formats of financial statements...........................................................................................14

4.3 Comparison of financial ratios.............................................................................................17

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

2

INTRODUCTION

Financial management is the methodology that is used by organization to make effective

control over its income, expenditures, assets and liabilities. Main agenda of managing cash at the

workplace is to maximize profit and ensure sustainability. Sound capital structure is the aim of

every corporation so that they can run their business well. It is only possible with the help of

effective financial management strategies (Zimmerman, 2015). Present report is based on

Clariton Antiques Ltd. Five years ago, five partners have invested their money and started an

unincorporated business of selling antiques items. Slowly it has developed its own reputation in

the industry and now, it has become one of the well-known brand names in London.

Study will discuss several sources of finance which can raise capital of the cited firm.

Venture capitalist and financial brokers are the two main sources where cost attached with these

sources will be analysed in this assignment. Economic forecasting and its importance in business

will be discussed in this report. Unit cost, NPV, ARR and PBP calculations will be done in this

study to find out the feasibility of projects. In addition to this, financial ratio of Clariton Antiques

Ltd will be illustrated in this report (Croce, Grilli and Murtinu, 2014).

TASK 1

1.1 Unincorporated and incorporated business and sources of finance

a) Unincorporated businesses

These are such entities which have no legal identification and their liabilities are limited.

Sole traders and partnership firms are the great examples of unincorporated business. These

organizations are not legally registered and owner or partners run business separately. Clariton

Antiques Ltd is working as unincorporated corporations. Sources of finance available to the

business are as follows: Personal saving: It is the main source of finance for unincorporated business like

Clariton Antiques Ltd. In this, owner or partners of the cited firm can invest their own

capital for the expansion of organization. It assists in keeping liability of the entity in

control because in this, partners need not to pay interest to any lender (Rubin, Aas and

Stead, 2015).

3

Financial management is the methodology that is used by organization to make effective

control over its income, expenditures, assets and liabilities. Main agenda of managing cash at the

workplace is to maximize profit and ensure sustainability. Sound capital structure is the aim of

every corporation so that they can run their business well. It is only possible with the help of

effective financial management strategies (Zimmerman, 2015). Present report is based on

Clariton Antiques Ltd. Five years ago, five partners have invested their money and started an

unincorporated business of selling antiques items. Slowly it has developed its own reputation in

the industry and now, it has become one of the well-known brand names in London.

Study will discuss several sources of finance which can raise capital of the cited firm.

Venture capitalist and financial brokers are the two main sources where cost attached with these

sources will be analysed in this assignment. Economic forecasting and its importance in business

will be discussed in this report. Unit cost, NPV, ARR and PBP calculations will be done in this

study to find out the feasibility of projects. In addition to this, financial ratio of Clariton Antiques

Ltd will be illustrated in this report (Croce, Grilli and Murtinu, 2014).

TASK 1

1.1 Unincorporated and incorporated business and sources of finance

a) Unincorporated businesses

These are such entities which have no legal identification and their liabilities are limited.

Sole traders and partnership firms are the great examples of unincorporated business. These

organizations are not legally registered and owner or partners run business separately. Clariton

Antiques Ltd is working as unincorporated corporations. Sources of finance available to the

business are as follows: Personal saving: It is the main source of finance for unincorporated business like

Clariton Antiques Ltd. In this, owner or partners of the cited firm can invest their own

capital for the expansion of organization. It assists in keeping liability of the entity in

control because in this, partners need not to pay interest to any lender (Rubin, Aas and

Stead, 2015).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank loan: It is another source of finance available to Clariton Antique Ltd where cited

firm can borrow money for fixed period from financial institutions. Bank usually charges

interest on lending amount but it is low and affordable by the borrower. Owner of

company needs to give security. It may be in the form of personal guarantee. This source

of finance can increase cash inflow in the organization and support in accomplishing the

aim of cited firm.

b) Incorporated business:

These are the legally structured entities who have to follow norms of international

accounting standards. In such type of organizations, person is not liable for the debt of company.

It can get benefit of tax and owner can generate income by selling its stock in the markets.

Sources of finance for incorporated business are maintained as below: Retained earnings: It is an important economic source that raises the capital of company.

It is the internal source or can be termed as profit of entity (Deshpandé and et.al., 2013).

Management of organization uses these funds for further development of the firms as no

economic cost is associated with it. So, it can be a good source of finance for the

enterprises.

Venture capital: There are many capitalists who invest their money in the startup

business to gain higher returns. They invest a huge amount so that entity can expand its

operations and generate a good amount of income. But, in this, owner has to involve them

in board meetings and they can influence the decision of company.

1.2 Internal and external sources along with their implications

a) Internal sources

These are the funds which are generated by business internally. Company’s own fund can

be utilized by the management for further development (Pe'er, and Keil, 2013). Retained earnings: It is the net profit of entity after paying dividend to its shareholders.

This is a long term source of finance and in this, Clariton Antiques Ltd needs not to repay

this amount. So, no economic implications are associated with these funds. Along with

that, it does not create financial burden on the entity. In addition to this, as firm does not

issue any equity thus, ownership needs not to be shared with any investors. Thus,

4

firm can borrow money for fixed period from financial institutions. Bank usually charges

interest on lending amount but it is low and affordable by the borrower. Owner of

company needs to give security. It may be in the form of personal guarantee. This source

of finance can increase cash inflow in the organization and support in accomplishing the

aim of cited firm.

b) Incorporated business:

These are the legally structured entities who have to follow norms of international

accounting standards. In such type of organizations, person is not liable for the debt of company.

It can get benefit of tax and owner can generate income by selling its stock in the markets.

Sources of finance for incorporated business are maintained as below: Retained earnings: It is an important economic source that raises the capital of company.

It is the internal source or can be termed as profit of entity (Deshpandé and et.al., 2013).

Management of organization uses these funds for further development of the firms as no

economic cost is associated with it. So, it can be a good source of finance for the

enterprises.

Venture capital: There are many capitalists who invest their money in the startup

business to gain higher returns. They invest a huge amount so that entity can expand its

operations and generate a good amount of income. But, in this, owner has to involve them

in board meetings and they can influence the decision of company.

1.2 Internal and external sources along with their implications

a) Internal sources

These are the funds which are generated by business internally. Company’s own fund can

be utilized by the management for further development (Pe'er, and Keil, 2013). Retained earnings: It is the net profit of entity after paying dividend to its shareholders.

This is a long term source of finance and in this, Clariton Antiques Ltd needs not to repay

this amount. So, no economic implications are associated with these funds. Along with

that, it does not create financial burden on the entity. In addition to this, as firm does not

issue any equity thus, ownership needs not to be shared with any investors. Thus,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ownership and control remains the same, they do not get diluted. Owner can take his own

decision without any influence of third party. No legal complications have to be faced by

partners and therefore, no legal implications are attached with the same (Pinkwart and

Proksch, 2014).

Sales of assets: To generate the cash, Clariton Antiques Ltd can sell its assets in the

market that will increase cash inflow which can be used by the cited firm to acquire

building in Birmingham for opening its another branch. It is short term finance and no

need to repay it. So, economic implications are associated with the sale of assets. When

company sells its inventories then it has to make legal agreement with the purchaser

which is a legal implication of this source of finance. But, in this, cited firm needs not to

share its ownership and also, controlling power remains in the hands of entrepreneur.

B) External sources

These are such funds which are borrowed by the external market and it is necessary to

repay the same on time. Bank loan: It is the main external financial source but in this, borrower has to pay interest

on it and rate of interest may be fixed or variable. This is an economic implication for

Clariton Antiques Ltd (Ambrose, Cordell and Ma, 2015). Bank can demand security that

is another economic cost. Apart from this, financial institutions make a legal agreement

with the borrower so that if person do not pay installment then he would get legal rights

to sell its properties to recover the complete loan amount. In this, ownership and

controlling power remains the same and owner needs not to share it with lenders.

Equity share: Dividend is the economic implication of this source. Clariton Antique Ltd

needs to pay dividend to its equity partners. They have to follow regulations before

opting this source of finance. Apart from this, in the equity share, owner has to share

ownership with the equity holders and they can influence the decision of organization

(Deffains-Crapsky and Sudolska, 2014).

1.3 Appropriate source of finance

As Clariton Antiques Ltd is engaged in the selling of antique items. In this, it has to buy

products from the suppliers and have to resale it in the market. For expanding business, cited

5

decision without any influence of third party. No legal complications have to be faced by

partners and therefore, no legal implications are attached with the same (Pinkwart and

Proksch, 2014).

Sales of assets: To generate the cash, Clariton Antiques Ltd can sell its assets in the

market that will increase cash inflow which can be used by the cited firm to acquire

building in Birmingham for opening its another branch. It is short term finance and no

need to repay it. So, economic implications are associated with the sale of assets. When

company sells its inventories then it has to make legal agreement with the purchaser

which is a legal implication of this source of finance. But, in this, cited firm needs not to

share its ownership and also, controlling power remains in the hands of entrepreneur.

B) External sources

These are such funds which are borrowed by the external market and it is necessary to

repay the same on time. Bank loan: It is the main external financial source but in this, borrower has to pay interest

on it and rate of interest may be fixed or variable. This is an economic implication for

Clariton Antiques Ltd (Ambrose, Cordell and Ma, 2015). Bank can demand security that

is another economic cost. Apart from this, financial institutions make a legal agreement

with the borrower so that if person do not pay installment then he would get legal rights

to sell its properties to recover the complete loan amount. In this, ownership and

controlling power remains the same and owner needs not to share it with lenders.

Equity share: Dividend is the economic implication of this source. Clariton Antique Ltd

needs to pay dividend to its equity partners. They have to follow regulations before

opting this source of finance. Apart from this, in the equity share, owner has to share

ownership with the equity holders and they can influence the decision of organization

(Deffains-Crapsky and Sudolska, 2014).

1.3 Appropriate source of finance

As Clariton Antiques Ltd is engaged in the selling of antique items. In this, it has to buy

products from the suppliers and have to resale it in the market. For expanding business, cited

5

firm needs funds but it is important to look upon the cost and implications before selecting any

source of finance. Bank loan can be the best way of raising funds of Clariton Antiques Ltd. In

this, owner needs not to share controlling power with the lender and so, all important decisions

can be made by them individually without any interruption. Repayment schedule is simple and

affordable for the cited firm. Apart from this, interest rates of bank is low for startup firms and it

can get tax benefit on the same (Bessen and Meurer, 2013). So, it can be an appropriate source of

finance for the organization.

Retained earnings is another source which can raise the capital of entity. As it is an

internal source of finance so, there is no need to repay it as own capital can be used for further

development or expansion of the business. No much legal formalities are needed to be followed

and controlling power is the main benefit of this source. Apart from that, in this source of

finance, no dilution of ownership takes place.

TASK 2

2.1 Cost of sources of finance

Cost of raising funds can be measured by two ways; equity and debt. Cost of debt can be

explained as amount which is to be paid by organization on its debt. Whereas equity financing is

hose sources in which firm has to share ownership against funds. It is attached with equity shares

type of sources whereas bank loan is the great example of debt financing. As Clariton Antiques

Ltd has been just approached by “ We Finance Limited:. It is venture capitalists and is

demanding 20% stake in the business against its investment (Mayordomo, Peña and Schwartz,

2014). Financial brokers are another persons those who can arrange funds for the organization.

They take commission and arrange bank loan for the borrower. Both these sources are essential

and can increase capital of the company. Cost of these are explained as below:

a) Dividends:

If Clariton Antiques Ltd goes with venture capital then it will have to bear this cost. As it

is very important to give dividend to capitalist and involve them in decision making process.

That is legal right of the investor to get divided, but due to this financial burden of the company

can get enhanced. That is cost of venture capital source, 20% stake very high which can increase

expenditure of the cited firm.

b) Interest:

6

source of finance. Bank loan can be the best way of raising funds of Clariton Antiques Ltd. In

this, owner needs not to share controlling power with the lender and so, all important decisions

can be made by them individually without any interruption. Repayment schedule is simple and

affordable for the cited firm. Apart from this, interest rates of bank is low for startup firms and it

can get tax benefit on the same (Bessen and Meurer, 2013). So, it can be an appropriate source of

finance for the organization.

Retained earnings is another source which can raise the capital of entity. As it is an

internal source of finance so, there is no need to repay it as own capital can be used for further

development or expansion of the business. No much legal formalities are needed to be followed

and controlling power is the main benefit of this source. Apart from that, in this source of

finance, no dilution of ownership takes place.

TASK 2

2.1 Cost of sources of finance

Cost of raising funds can be measured by two ways; equity and debt. Cost of debt can be

explained as amount which is to be paid by organization on its debt. Whereas equity financing is

hose sources in which firm has to share ownership against funds. It is attached with equity shares

type of sources whereas bank loan is the great example of debt financing. As Clariton Antiques

Ltd has been just approached by “ We Finance Limited:. It is venture capitalists and is

demanding 20% stake in the business against its investment (Mayordomo, Peña and Schwartz,

2014). Financial brokers are another persons those who can arrange funds for the organization.

They take commission and arrange bank loan for the borrower. Both these sources are essential

and can increase capital of the company. Cost of these are explained as below:

a) Dividends:

If Clariton Antiques Ltd goes with venture capital then it will have to bear this cost. As it

is very important to give dividend to capitalist and involve them in decision making process.

That is legal right of the investor to get divided, but due to this financial burden of the company

can get enhanced. That is cost of venture capital source, 20% stake very high which can increase

expenditure of the cited firm.

b) Interest:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As if Clariton Antiques Ltd goes with bank loan through financial brokers then this cost

would be applied. In this cited firm needs to pay annual interest to bank that increases long term

liability of the company (Ubel, Abernethy and Zafar, 2013). Interest is cost for the entity and can

reduce net profit of the corporation. Apart from this 1% brokerage can be considered as cost of

the organization. For instance Clariton Antiques Ltd is taking loan of £10,00,000 and bank

interest rate is 2% annual then cost would be:

= £1000000*2% + £10,00,000*1%

= £20000 + £10000

= £30000 cost of interest if cited firm takes loan from financial institutes.

c) Tax:

Clariton Antiques Ltd will have to pay tax on its income, that would considered as cost of

the entity. For instance recent tax rate is 30% then cost would be:

= £10,00,000* (1-0.3)*2%

= £14000 + 1% brokerage

= £14000+ £10000

= £15000

2.2 Importance of financial planning

It is the process through which entities can determine future capital requirements and can

control over its costs. Economic forecasting is the tool which assists in taking proper investment

decisions and managing cash well in the workplace. It is very important for ensuring adequacy of

funds in the organization. Apart from this future uncertain events can be forecasted by the firms

easily thus risk can be minimized (RAHDAN, MIRHASHEMI and DEHKORDI, 2014). It acts

as monitor and check the financial activities of the company and compare it with actual revenues.

It is essential in making coordination between various business functions such as sales and

production so that overall cost can be controlled by the owner.

a) Budgeting: It is one of the main element and important factor that can influence entire

business operations. Budget is the itemized summary of overall expenditure and income of the

organization. It can help in analysing the future of the business. It is an invaluable tool through

which manages can prioritize its spending and manage their cash well. With the help of financial

planning budget can be prepared effectively (Axelson and et.al, 2013). It helps to look upon the

7

would be applied. In this cited firm needs to pay annual interest to bank that increases long term

liability of the company (Ubel, Abernethy and Zafar, 2013). Interest is cost for the entity and can

reduce net profit of the corporation. Apart from this 1% brokerage can be considered as cost of

the organization. For instance Clariton Antiques Ltd is taking loan of £10,00,000 and bank

interest rate is 2% annual then cost would be:

= £1000000*2% + £10,00,000*1%

= £20000 + £10000

= £30000 cost of interest if cited firm takes loan from financial institutes.

c) Tax:

Clariton Antiques Ltd will have to pay tax on its income, that would considered as cost of

the entity. For instance recent tax rate is 30% then cost would be:

= £10,00,000* (1-0.3)*2%

= £14000 + 1% brokerage

= £14000+ £10000

= £15000

2.2 Importance of financial planning

It is the process through which entities can determine future capital requirements and can

control over its costs. Economic forecasting is the tool which assists in taking proper investment

decisions and managing cash well in the workplace. It is very important for ensuring adequacy of

funds in the organization. Apart from this future uncertain events can be forecasted by the firms

easily thus risk can be minimized (RAHDAN, MIRHASHEMI and DEHKORDI, 2014). It acts

as monitor and check the financial activities of the company and compare it with actual revenues.

It is essential in making coordination between various business functions such as sales and

production so that overall cost can be controlled by the owner.

a) Budgeting: It is one of the main element and important factor that can influence entire

business operations. Budget is the itemized summary of overall expenditure and income of the

organization. It can help in analysing the future of the business. It is an invaluable tool through

which manages can prioritize its spending and manage their cash well. With the help of financial

planning budget can be prepared effectively (Axelson and et.al, 2013). It helps to look upon the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

additional expenditure and impact of decisions on cash inflow. So owner of Clariton Antiques

Ltd can formulate proper strategies to manage its cash in the organization, by this way shortage

or surplus both activities will not take place in the business unit.

b) Implication of failure to finance adequately: many times wrong decisions can harm

the business performances to great extent. With the help of economic forecasting owner of

Clariton Antiques Ltd will be able to take proper economic decisions which can reduce risk of

failure. By this way company will be able to manage its stock well as per the demand of

customers, there would not be surplus stock of antiques in the inventory (Tadesse, 2014).

c) Over trading: As Clariton Antiques Ltd is engaged in the selling of antiques items, it

is essential for the cited firm to identify the demand and order goods as per the demand.

Financial planning helps in minimizing the issues of over trading. By this way cash inflow in the

entity can get raised to great extent and unnecessary wastage can be minimized.

2.3 Requirement of information for making effective decision

Financial information helps in making economic decision in the organization. Details

related to balance sheet, assets & liabilities, sales & purchase, expenditure, profit history are

major details which are necessary to know by the person (Almarri and Blackwell, 2014).

a) The Partners:

Clariton Antiques Ltd has been started by four partners, they all have put their money for

the development of the organization. Before investing their money they need to know about

market requirement, liabilities, solvency ratio, inventory turn over ratio, gearing ratio. By this

way they will be able to make effective decisions of investment. This information helps them in

forecasting returns on their invested amount.

b) Venture Capitalist:

“We Finance Limited” has approached to Clariton Antiques for investment, they need

information about profit history, previous liabilities, assists value, gearing ratio, dividend policy.

Capacity to generate income, market worth etc. With the helps of these details capitalist will be

able to make accurate decision.

c) Finance Broker:

They are the person those who are linked with the banks and they arrange loan for the

company (Venables, Laird and Overman, 2014). They need information like repay capacity,

8

Ltd can formulate proper strategies to manage its cash in the organization, by this way shortage

or surplus both activities will not take place in the business unit.

b) Implication of failure to finance adequately: many times wrong decisions can harm

the business performances to great extent. With the help of economic forecasting owner of

Clariton Antiques Ltd will be able to take proper economic decisions which can reduce risk of

failure. By this way company will be able to manage its stock well as per the demand of

customers, there would not be surplus stock of antiques in the inventory (Tadesse, 2014).

c) Over trading: As Clariton Antiques Ltd is engaged in the selling of antiques items, it

is essential for the cited firm to identify the demand and order goods as per the demand.

Financial planning helps in minimizing the issues of over trading. By this way cash inflow in the

entity can get raised to great extent and unnecessary wastage can be minimized.

2.3 Requirement of information for making effective decision

Financial information helps in making economic decision in the organization. Details

related to balance sheet, assets & liabilities, sales & purchase, expenditure, profit history are

major details which are necessary to know by the person (Almarri and Blackwell, 2014).

a) The Partners:

Clariton Antiques Ltd has been started by four partners, they all have put their money for

the development of the organization. Before investing their money they need to know about

market requirement, liabilities, solvency ratio, inventory turn over ratio, gearing ratio. By this

way they will be able to make effective decisions of investment. This information helps them in

forecasting returns on their invested amount.

b) Venture Capitalist:

“We Finance Limited” has approached to Clariton Antiques for investment, they need

information about profit history, previous liabilities, assists value, gearing ratio, dividend policy.

Capacity to generate income, market worth etc. With the helps of these details capitalist will be

able to make accurate decision.

c) Finance Broker:

They are the person those who are linked with the banks and they arrange loan for the

company (Venables, Laird and Overman, 2014). They need information like repay capacity,

8

previous liabilities, solvency ratio, profitability ratio, credit history of owner and partners, market

worth of the firm etc. By this way broker will be able to decide whether to grand loan to the cited

firm of not.

2.4 Impact on financial statements

If Clariton Antique Ltd goes with venture capitalism and finance broker then both these

will impact on the financial statement of the cited firm.

a) Venture capitalist:

As “We Finance limited” is demanding 20% stake in the business, that can increase

expenditure of the organization to great extent. This spending will reflect in the income

statement of the company. Apart from this dividend is necessary to be paid to the shareholders.

So that would increase liabilities of the firm and will impact on the balance sheet of the firm. But

as they invest much amount in the business thus, capital side gets strong that show in the balance

sheet of the firm. Cash inflow get increases that impact on the cash flow statement of the

organization. So it can be said that venture capitalist impact on the all three main financial

statements of the company (Vesty and Oliver, 2014).

b) Finance Broker

Brokers are the mediators between bank and company. If Clariton Antique Ltd goes with

this source then owner of the firm will have to pay interest and brokerage to the broker. That will

be considered as expenses of the entity and will impact on the profit and loss account in the

expenditure side. Whenever, organization takes any loan from financial institutions then its long

term liabilities get increased. That impact on the liability side of balance sheet. On other hand

capital of the firm get increased thus it impacts positive on the assets side of balance sheet. It

increases cash inflow but interest charges and brokerage can be count as expenses or cash

outflow. So it will impact on the cash flow statement of the firm (Cost Per Unit, 2017).

TASK 3

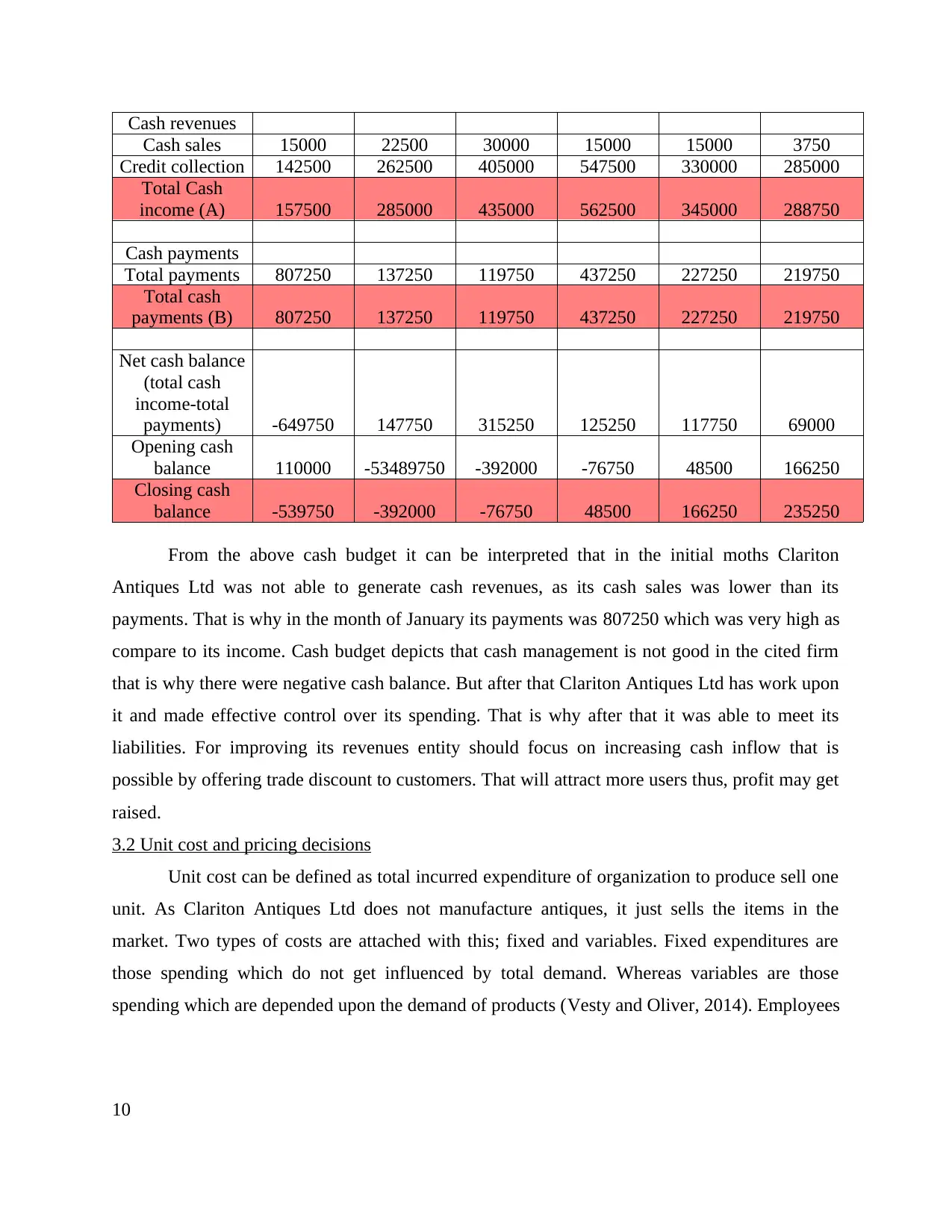

3.1 Cash budget

Cash budget is the tool through which firm can ensure adequacy of funds in the

organization (Cost Per Unit, 2017). It can be explained as review of cash inflow and outflow so

that proper strategies can be made by the managers to control over excess expenses.

Particulars January (£) February (£) March (£) April (£) May (£) June (£)

9

worth of the firm etc. By this way broker will be able to decide whether to grand loan to the cited

firm of not.

2.4 Impact on financial statements

If Clariton Antique Ltd goes with venture capitalism and finance broker then both these

will impact on the financial statement of the cited firm.

a) Venture capitalist:

As “We Finance limited” is demanding 20% stake in the business, that can increase

expenditure of the organization to great extent. This spending will reflect in the income

statement of the company. Apart from this dividend is necessary to be paid to the shareholders.

So that would increase liabilities of the firm and will impact on the balance sheet of the firm. But

as they invest much amount in the business thus, capital side gets strong that show in the balance

sheet of the firm. Cash inflow get increases that impact on the cash flow statement of the

organization. So it can be said that venture capitalist impact on the all three main financial

statements of the company (Vesty and Oliver, 2014).

b) Finance Broker

Brokers are the mediators between bank and company. If Clariton Antique Ltd goes with

this source then owner of the firm will have to pay interest and brokerage to the broker. That will

be considered as expenses of the entity and will impact on the profit and loss account in the

expenditure side. Whenever, organization takes any loan from financial institutions then its long

term liabilities get increased. That impact on the liability side of balance sheet. On other hand

capital of the firm get increased thus it impacts positive on the assets side of balance sheet. It

increases cash inflow but interest charges and brokerage can be count as expenses or cash

outflow. So it will impact on the cash flow statement of the firm (Cost Per Unit, 2017).

TASK 3

3.1 Cash budget

Cash budget is the tool through which firm can ensure adequacy of funds in the

organization (Cost Per Unit, 2017). It can be explained as review of cash inflow and outflow so

that proper strategies can be made by the managers to control over excess expenses.

Particulars January (£) February (£) March (£) April (£) May (£) June (£)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash revenues

Cash sales 15000 22500 30000 15000 15000 3750

Credit collection 142500 262500 405000 547500 330000 285000

Total Cash

income (A) 157500 285000 435000 562500 345000 288750

Cash payments

Total payments 807250 137250 119750 437250 227250 219750

Total cash

payments (B) 807250 137250 119750 437250 227250 219750

Net cash balance

(total cash

income-total

payments) -649750 147750 315250 125250 117750 69000

Opening cash

balance 110000 -53489750 -392000 -76750 48500 166250

Closing cash

balance -539750 -392000 -76750 48500 166250 235250

From the above cash budget it can be interpreted that in the initial moths Clariton

Antiques Ltd was not able to generate cash revenues, as its cash sales was lower than its

payments. That is why in the month of January its payments was 807250 which was very high as

compare to its income. Cash budget depicts that cash management is not good in the cited firm

that is why there were negative cash balance. But after that Clariton Antiques Ltd has work upon

it and made effective control over its spending. That is why after that it was able to meet its

liabilities. For improving its revenues entity should focus on increasing cash inflow that is

possible by offering trade discount to customers. That will attract more users thus, profit may get

raised.

3.2 Unit cost and pricing decisions

Unit cost can be defined as total incurred expenditure of organization to produce sell one

unit. As Clariton Antiques Ltd does not manufacture antiques, it just sells the items in the

market. Two types of costs are attached with this; fixed and variables. Fixed expenditures are

those spending which do not get influenced by total demand. Whereas variables are those

spending which are depended upon the demand of products (Vesty and Oliver, 2014). Employees

10

Cash sales 15000 22500 30000 15000 15000 3750

Credit collection 142500 262500 405000 547500 330000 285000

Total Cash

income (A) 157500 285000 435000 562500 345000 288750

Cash payments

Total payments 807250 137250 119750 437250 227250 219750

Total cash

payments (B) 807250 137250 119750 437250 227250 219750

Net cash balance

(total cash

income-total

payments) -649750 147750 315250 125250 117750 69000

Opening cash

balance 110000 -53489750 -392000 -76750 48500 166250

Closing cash

balance -539750 -392000 -76750 48500 166250 235250

From the above cash budget it can be interpreted that in the initial moths Clariton

Antiques Ltd was not able to generate cash revenues, as its cash sales was lower than its

payments. That is why in the month of January its payments was 807250 which was very high as

compare to its income. Cash budget depicts that cash management is not good in the cited firm

that is why there were negative cash balance. But after that Clariton Antiques Ltd has work upon

it and made effective control over its spending. That is why after that it was able to meet its

liabilities. For improving its revenues entity should focus on increasing cash inflow that is

possible by offering trade discount to customers. That will attract more users thus, profit may get

raised.

3.2 Unit cost and pricing decisions

Unit cost can be defined as total incurred expenditure of organization to produce sell one

unit. As Clariton Antiques Ltd does not manufacture antiques, it just sells the items in the

market. Two types of costs are attached with this; fixed and variables. Fixed expenditures are

those spending which do not get influenced by total demand. Whereas variables are those

spending which are depended upon the demand of products (Vesty and Oliver, 2014). Employees

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

salaries, rent of premises etc. are considered as fixed disbursement, transportation cost, utility

bills are variable costs of the Clariton Antique Ltd.

Unit cost= Fixed + variable costs / total produced units

For instance cited firm wants to purchase 5000 units of antique items, salaries paid to workers

are £15000, rent £10500, transportation cost £18000 and utility bills are £17000 then unit cost

would be:

Unit cost = [(15000+10500)+ (18000+17000)]/5000

Unit cost = £12.1

Pricing decision:

With the help of unit cost selling price can be calculated easily. Selling price= unit cost+

unit cost* profit percentage

For instance Clariton Antiques Ltd wants to earn 20% profit then calculation will b edone

as following:

= £12.1+ £12.1*20%

= £14.52 So it can be said that if cited firm keeps selling price of antiques £14.52 then it would

be able to generate 20% on its investments.

3.3 Investment decisions

Investment appraisal techniques are those methods through which an entity can take its

decision of investment and can identify feasibility of the projects (Investment appraisal, 2016).

Net present value (NPV): It is the method which compare present investment value with future

returns.

It is very effective tool through which firm can identify generation of income from the

project. As it focuses on risk factor so Clariton Antiques Ltd will be able to get high return on its

investment. But discounting factors are assumed by this firm so there may be high difference

between actual and expected figures.

11

bills are variable costs of the Clariton Antique Ltd.

Unit cost= Fixed + variable costs / total produced units

For instance cited firm wants to purchase 5000 units of antique items, salaries paid to workers

are £15000, rent £10500, transportation cost £18000 and utility bills are £17000 then unit cost

would be:

Unit cost = [(15000+10500)+ (18000+17000)]/5000

Unit cost = £12.1

Pricing decision:

With the help of unit cost selling price can be calculated easily. Selling price= unit cost+

unit cost* profit percentage

For instance Clariton Antiques Ltd wants to earn 20% profit then calculation will b edone

as following:

= £12.1+ £12.1*20%

= £14.52 So it can be said that if cited firm keeps selling price of antiques £14.52 then it would

be able to generate 20% on its investments.

3.3 Investment decisions

Investment appraisal techniques are those methods through which an entity can take its

decision of investment and can identify feasibility of the projects (Investment appraisal, 2016).

Net present value (NPV): It is the method which compare present investment value with future

returns.

It is very effective tool through which firm can identify generation of income from the

project. As it focuses on risk factor so Clariton Antiques Ltd will be able to get high return on its

investment. But discounting factors are assumed by this firm so there may be high difference

between actual and expected figures.

11

Investment 1 PV @ 14% Present value Investment 2

PV @

14%

Present

value

£m £m £m £m

Initial

investment 8.6 4.4

1 1.6 0.877 1 0.8 0.877 1

2 2.8 0.769 2 1.4 0.769 1

3 3.4 0.675 2 2 0.675 1

4 3.6 0.592 2 2.4 0.592 1

5 4 0.519 2 2.3 0.519 1

6 4.2 0.456 2 2.6 0.456 1

Total 12 7

NPV 3.38 2.53

So it can be interpreted that investment in project 2 would be good for the Clariton

Antiques Ltd, as in this it would be able to generate good income soon.

Average rate of returns (ARR):

It is the technique that helps to identify the profit percentage on investment.

ARR (%) = Total revenue / no. of year / Initial cost *100. It is easy to calculate and by this way

manager of cited firm can compare the results effectively. But it does not emphases on time

values so some times results may be differed from expectation (Vesty and Oliver, 2014).

Investment 1 Investment 2

£m £m

Initial investment 8.6 4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

Total 19.6 11.5

12

PV @

14%

Present

value

£m £m £m £m

Initial

investment 8.6 4.4

1 1.6 0.877 1 0.8 0.877 1

2 2.8 0.769 2 1.4 0.769 1

3 3.4 0.675 2 2 0.675 1

4 3.6 0.592 2 2.4 0.592 1

5 4 0.519 2 2.3 0.519 1

6 4.2 0.456 2 2.6 0.456 1

Total 12 7

NPV 3.38 2.53

So it can be interpreted that investment in project 2 would be good for the Clariton

Antiques Ltd, as in this it would be able to generate good income soon.

Average rate of returns (ARR):

It is the technique that helps to identify the profit percentage on investment.

ARR (%) = Total revenue / no. of year / Initial cost *100. It is easy to calculate and by this way

manager of cited firm can compare the results effectively. But it does not emphases on time

values so some times results may be differed from expectation (Vesty and Oliver, 2014).

Investment 1 Investment 2

£m £m

Initial investment 8.6 4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

Total 19.6 11.5

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.