Financial Analysis and Stakeholder Needs: Management Report

VerifiedAdded on 2022/12/14

|15

|4299

|108

Report

AI Summary

This report examines financial resource management, analyzing financial statements, financial ratios, and stakeholder information needs. The report begins with an introduction to resource management, emphasizing the importance of financial statements and ratios in evaluating a company's financial performance. It explores various financial statements, including income statements, balance sheets, and statements of cash flow, along with different types of financial ratios like liquidity, solvency, and profitability ratios. The main body of the report delves into interpreting specific financial ratios, such as gross profit, expense, and net profit ratios, providing insights into the company's performance. It further analyzes the financial information needs of different stakeholders, including board of directors, shareholders, banks, customers, creditors, and competitors, and how they use financial statements to make informed decisions. The report concludes by summarizing the key findings and emphasizing the importance of effective financial management for organizational success.

Managing financial resources

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Table of Contents.............................................................................................................................2

ASSIGNMENT 1.............................................................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Q1. Examining the various financial statements and financial ratios..........................................3

Q2. Interpreting certain financial ratios of the company.............................................................5

Q3. Analysing the financial information needs of different stakeholder.....................................7

CONCLUSION................................................................................................................................8

ASSIGNMENT 2.............................................................................................................................9

INTRODUCTION...........................................................................................................................9

MAIN BODY..................................................................................................................................9

Q2. Identifying the meaning of cost-plus approach and problem...............................................9

Q3. Identifying the financial ratios of the company..................................................................10

Q.4 Analysing the terms............................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

3

Table of Contents.............................................................................................................................2

ASSIGNMENT 1.............................................................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Q1. Examining the various financial statements and financial ratios..........................................3

Q2. Interpreting certain financial ratios of the company.............................................................5

Q3. Analysing the financial information needs of different stakeholder.....................................7

CONCLUSION................................................................................................................................8

ASSIGNMENT 2.............................................................................................................................9

INTRODUCTION...........................................................................................................................9

MAIN BODY..................................................................................................................................9

Q2. Identifying the meaning of cost-plus approach and problem...............................................9

Q3. Identifying the financial ratios of the company..................................................................10

Q.4 Analysing the terms............................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSIGNMENT 1

INTRODUCTION

Managing the resources refers to the regulating and operating the various types of resources in

the company and will lead to satisfaction among the employees and overall management. This

also termed as properly allocation of resources so that it can able to optimize the activities and

functions (Aidemark, 2001). This will going increase the effectiveness and will improve the

efficiency and enhance the production. This could be achieved by the reducing the wastages and

will going to increase the profit for the company. In this report it is being discussing about the

effectiveness of financial statements and different financial ratios and that will be useful for the

shareholder. Apart from that its evaluating the various types of ratios that is being used in the

company and interpret its performance. It is being analysed about the different types of financial

information that will be needed by the shareholder to take the informed decisions.

MAIN BODY

Q1. Examining the various financial statements and financial ratios

Financial statements are financial information that is portrait by the organisation to

evaluate the financial performance of the company at the end of the year. It shows the formal

records of all necessary financial transaction that used to take place in day-to-day operations to

maintain the efficiency. This is useful in taking important decision about the performance of the

organisation and further action that is taken by the top management. This is very important part

to make the financial statements of the company and formulating the profit. Following are types

of financial statements are as follows-

Income statements- This is financial information that helps in reporting the company’s

financial performance for specific period of time. This essential part of the company that

will is prepared by the accountant to analyse the income and expense during financial

year. This is used by many external users to assess the overall performance of the

organisation. Some of the components are as follows-

Revenue- It concern with the sales of goods and services that company generate or produced

profit during the specific period (Barsky and Marchant, 2000). This differs from the various

activities and involves many efforts to minimize the profit for the company.

4

INTRODUCTION

Managing the resources refers to the regulating and operating the various types of resources in

the company and will lead to satisfaction among the employees and overall management. This

also termed as properly allocation of resources so that it can able to optimize the activities and

functions (Aidemark, 2001). This will going increase the effectiveness and will improve the

efficiency and enhance the production. This could be achieved by the reducing the wastages and

will going to increase the profit for the company. In this report it is being discussing about the

effectiveness of financial statements and different financial ratios and that will be useful for the

shareholder. Apart from that its evaluating the various types of ratios that is being used in the

company and interpret its performance. It is being analysed about the different types of financial

information that will be needed by the shareholder to take the informed decisions.

MAIN BODY

Q1. Examining the various financial statements and financial ratios

Financial statements are financial information that is portrait by the organisation to

evaluate the financial performance of the company at the end of the year. It shows the formal

records of all necessary financial transaction that used to take place in day-to-day operations to

maintain the efficiency. This is useful in taking important decision about the performance of the

organisation and further action that is taken by the top management. This is very important part

to make the financial statements of the company and formulating the profit. Following are types

of financial statements are as follows-

Income statements- This is financial information that helps in reporting the company’s

financial performance for specific period of time. This essential part of the company that

will is prepared by the accountant to analyse the income and expense during financial

year. This is used by many external users to assess the overall performance of the

organisation. Some of the components are as follows-

Revenue- It concern with the sales of goods and services that company generate or produced

profit during the specific period (Barsky and Marchant, 2000). This differs from the various

activities and involves many efforts to minimize the profit for the company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit and loss- This is Net income that is obtained by the deducting the expenses and will occur

after the appropriate time. Profit is important part for the company as this indicate efficiency of

the company.

Expenses- This is called as cost of activities and operation that used to occur while

manufacturing or any other operational function. This could be administrative expenses, selling

expenses, promotion and advertising expenses (Beer and et.al, 1984).

Balance sheet- This called as the statement of financial position as it tells the position of

assets and liabilities at the end of accounting period. This is essential part of financial

statements where it helps the users to make the informed decisions about the financial

position. This is useful in analysing the efficiency and effectiveness in long term and

fulfil all important decision to achieve the goals and objectives of the company.

Statement of cash flow- This is financial statement that helps in aggregate data

regarding all cash inflows company receives from its ongoing operations and other

external investment sources. This also include all cash outflows its pay for business

activities and different investment during the period and gives an overview to the investor

and shareholder about the company. This will help in knowing the operational efficiency

of the management and help to take the informed decision. There are three different

sections of the cash flow such as Investing activity, operating activity and Financing

activities.

Ratio analysis- There are various pieces that gives financial information from the

financial statements of the business and evaluating the extremal and internal efficiency to

determine the profitability of the company. There are various ratios such as liquidity,

solvency and profitability ratio. This is important to understand the effectiveness of the

company. Some of the ratio are as follows-

Liquidity ratio- This measure the organisation to meet the obligation using the current

asset and current liability to make the timely payments and measure the short-term

efficiency. It can convert its assets into the cash and from that using the money to settle

any pending debts with more ease. Some of the example are Current ratio, Quick ratio

and cash ratio (Cardon and Stevens, 2004).

Solvency ratio- This measure the solvency and efficient viability and this compare the

debt level of the company according to the assets and annual earnings. Some of the

5

after the appropriate time. Profit is important part for the company as this indicate efficiency of

the company.

Expenses- This is called as cost of activities and operation that used to occur while

manufacturing or any other operational function. This could be administrative expenses, selling

expenses, promotion and advertising expenses (Beer and et.al, 1984).

Balance sheet- This called as the statement of financial position as it tells the position of

assets and liabilities at the end of accounting period. This is essential part of financial

statements where it helps the users to make the informed decisions about the financial

position. This is useful in analysing the efficiency and effectiveness in long term and

fulfil all important decision to achieve the goals and objectives of the company.

Statement of cash flow- This is financial statement that helps in aggregate data

regarding all cash inflows company receives from its ongoing operations and other

external investment sources. This also include all cash outflows its pay for business

activities and different investment during the period and gives an overview to the investor

and shareholder about the company. This will help in knowing the operational efficiency

of the management and help to take the informed decision. There are three different

sections of the cash flow such as Investing activity, operating activity and Financing

activities.

Ratio analysis- There are various pieces that gives financial information from the

financial statements of the business and evaluating the extremal and internal efficiency to

determine the profitability of the company. There are various ratios such as liquidity,

solvency and profitability ratio. This is important to understand the effectiveness of the

company. Some of the ratio are as follows-

Liquidity ratio- This measure the organisation to meet the obligation using the current

asset and current liability to make the timely payments and measure the short-term

efficiency. It can convert its assets into the cash and from that using the money to settle

any pending debts with more ease. Some of the example are Current ratio, Quick ratio

and cash ratio (Cardon and Stevens, 2004).

Solvency ratio- This measure the solvency and efficient viability and this compare the

debt level of the company according to the assets and annual earnings. Some of the

5

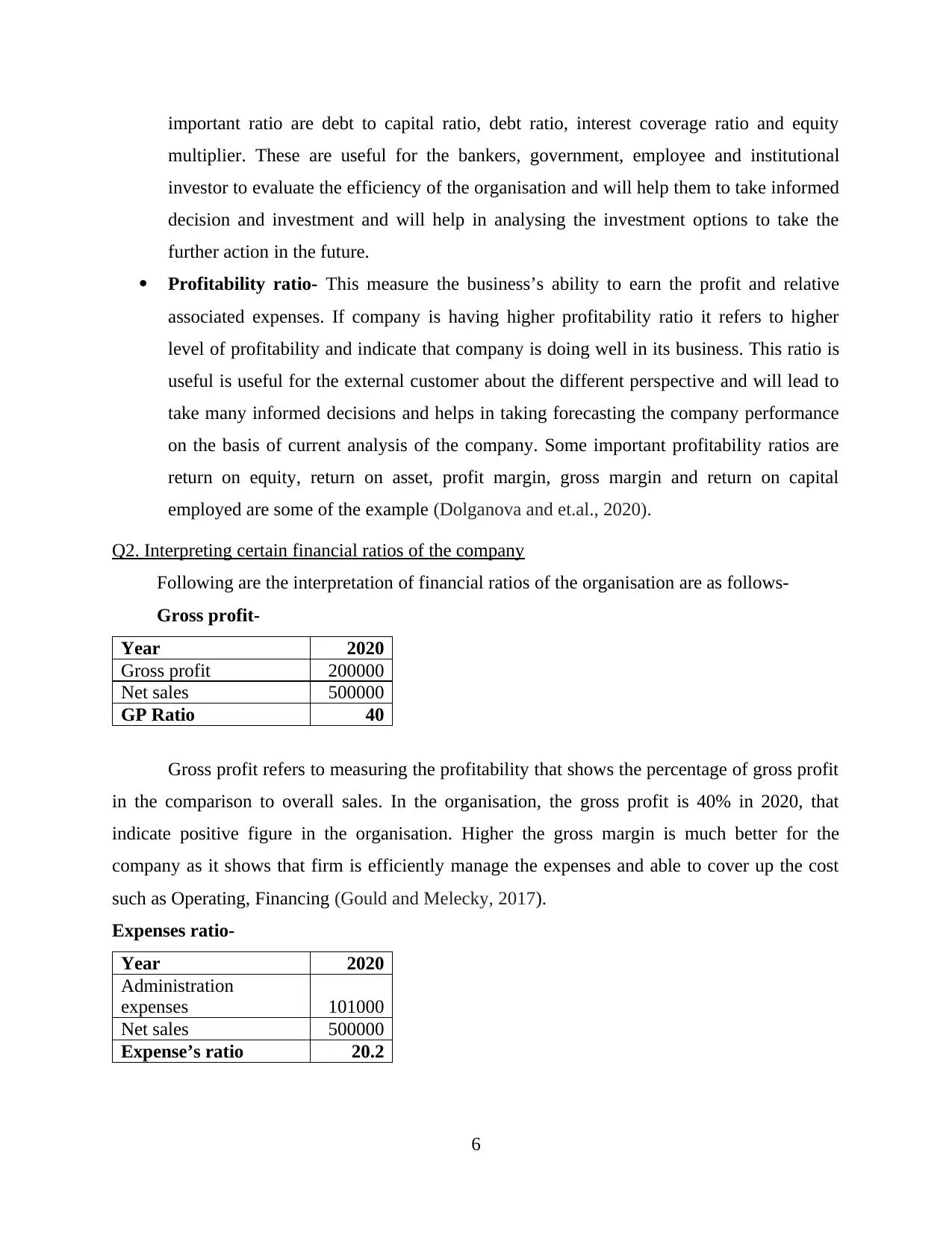

important ratio are debt to capital ratio, debt ratio, interest coverage ratio and equity

multiplier. These are useful for the bankers, government, employee and institutional

investor to evaluate the efficiency of the organisation and will help them to take informed

decision and investment and will help in analysing the investment options to take the

further action in the future.

Profitability ratio- This measure the business’s ability to earn the profit and relative

associated expenses. If company is having higher profitability ratio it refers to higher

level of profitability and indicate that company is doing well in its business. This ratio is

useful is useful for the external customer about the different perspective and will lead to

take many informed decisions and helps in taking forecasting the company performance

on the basis of current analysis of the company. Some important profitability ratios are

return on equity, return on asset, profit margin, gross margin and return on capital

employed are some of the example (Dolganova and et.al., 2020).

Q2. Interpreting certain financial ratios of the company

Following are the interpretation of financial ratios of the organisation are as follows-

Gross profit-

Year 2020

Gross profit 200000

Net sales 500000

GP Ratio 40

Gross profit refers to measuring the profitability that shows the percentage of gross profit

in the comparison to overall sales. In the organisation, the gross profit is 40% in 2020, that

indicate positive figure in the organisation. Higher the gross margin is much better for the

company as it shows that firm is efficiently manage the expenses and able to cover up the cost

such as Operating, Financing (Gould and Melecky, 2017).

Expenses ratio-

Year 2020

Administration

expenses 101000

Net sales 500000

Expense’s ratio 20.2

6

multiplier. These are useful for the bankers, government, employee and institutional

investor to evaluate the efficiency of the organisation and will help them to take informed

decision and investment and will help in analysing the investment options to take the

further action in the future.

Profitability ratio- This measure the business’s ability to earn the profit and relative

associated expenses. If company is having higher profitability ratio it refers to higher

level of profitability and indicate that company is doing well in its business. This ratio is

useful is useful for the external customer about the different perspective and will lead to

take many informed decisions and helps in taking forecasting the company performance

on the basis of current analysis of the company. Some important profitability ratios are

return on equity, return on asset, profit margin, gross margin and return on capital

employed are some of the example (Dolganova and et.al., 2020).

Q2. Interpreting certain financial ratios of the company

Following are the interpretation of financial ratios of the organisation are as follows-

Gross profit-

Year 2020

Gross profit 200000

Net sales 500000

GP Ratio 40

Gross profit refers to measuring the profitability that shows the percentage of gross profit

in the comparison to overall sales. In the organisation, the gross profit is 40% in 2020, that

indicate positive figure in the organisation. Higher the gross margin is much better for the

company as it shows that firm is efficiently manage the expenses and able to cover up the cost

such as Operating, Financing (Gould and Melecky, 2017).

Expenses ratio-

Year 2020

Administration

expenses 101000

Net sales 500000

Expense’s ratio 20.2

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

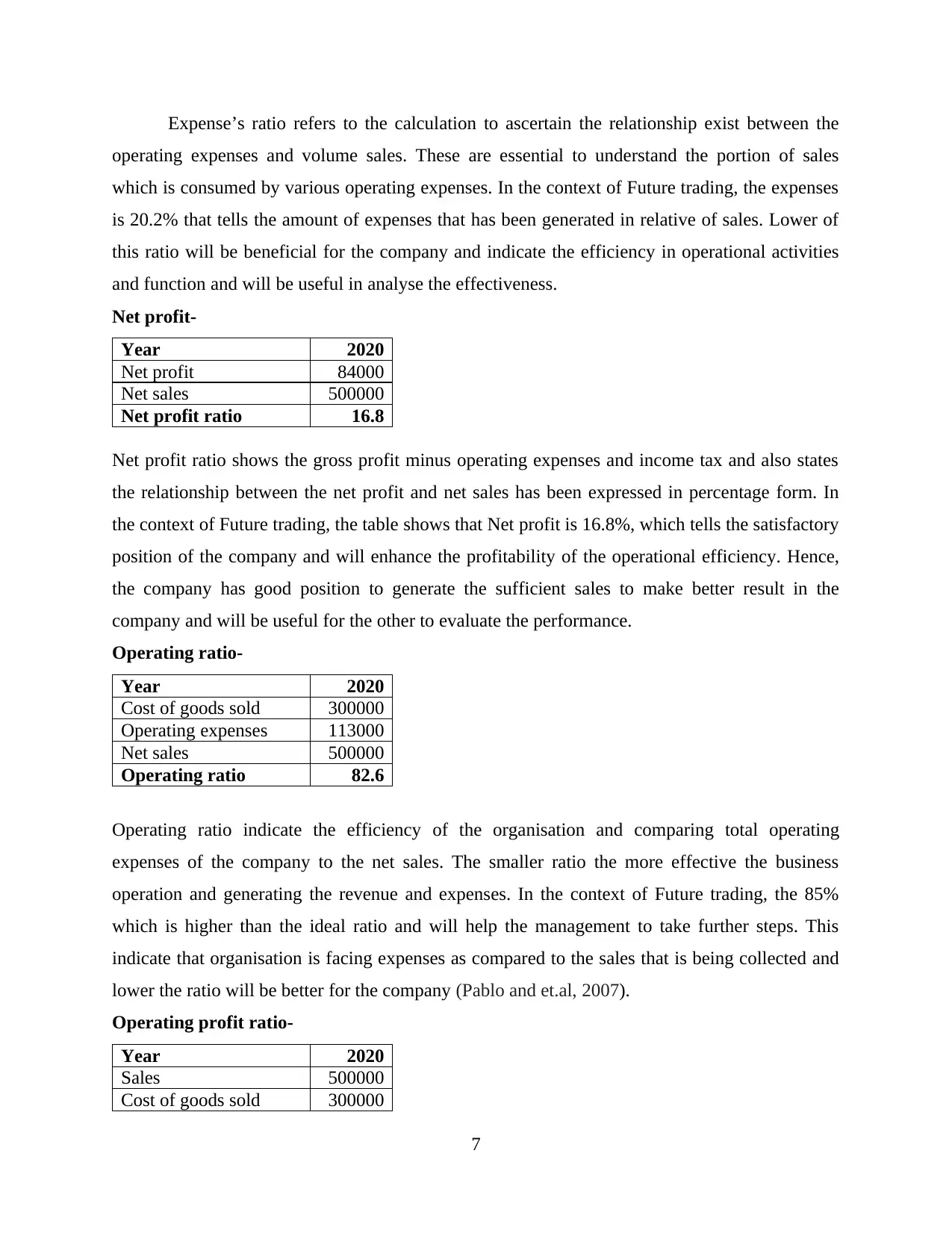

Expense’s ratio refers to the calculation to ascertain the relationship exist between the

operating expenses and volume sales. These are essential to understand the portion of sales

which is consumed by various operating expenses. In the context of Future trading, the expenses

is 20.2% that tells the amount of expenses that has been generated in relative of sales. Lower of

this ratio will be beneficial for the company and indicate the efficiency in operational activities

and function and will be useful in analyse the effectiveness.

Net profit-

Year 2020

Net profit 84000

Net sales 500000

Net profit ratio 16.8

Net profit ratio shows the gross profit minus operating expenses and income tax and also states

the relationship between the net profit and net sales has been expressed in percentage form. In

the context of Future trading, the table shows that Net profit is 16.8%, which tells the satisfactory

position of the company and will enhance the profitability of the operational efficiency. Hence,

the company has good position to generate the sufficient sales to make better result in the

company and will be useful for the other to evaluate the performance.

Operating ratio-

Year 2020

Cost of goods sold 300000

Operating expenses 113000

Net sales 500000

Operating ratio 82.6

Operating ratio indicate the efficiency of the organisation and comparing total operating

expenses of the company to the net sales. The smaller ratio the more effective the business

operation and generating the revenue and expenses. In the context of Future trading, the 85%

which is higher than the ideal ratio and will help the management to take further steps. This

indicate that organisation is facing expenses as compared to the sales that is being collected and

lower the ratio will be better for the company (Pablo and et.al, 2007).

Operating profit ratio-

Year 2020

Sales 500000

Cost of goods sold 300000

7

operating expenses and volume sales. These are essential to understand the portion of sales

which is consumed by various operating expenses. In the context of Future trading, the expenses

is 20.2% that tells the amount of expenses that has been generated in relative of sales. Lower of

this ratio will be beneficial for the company and indicate the efficiency in operational activities

and function and will be useful in analyse the effectiveness.

Net profit-

Year 2020

Net profit 84000

Net sales 500000

Net profit ratio 16.8

Net profit ratio shows the gross profit minus operating expenses and income tax and also states

the relationship between the net profit and net sales has been expressed in percentage form. In

the context of Future trading, the table shows that Net profit is 16.8%, which tells the satisfactory

position of the company and will enhance the profitability of the operational efficiency. Hence,

the company has good position to generate the sufficient sales to make better result in the

company and will be useful for the other to evaluate the performance.

Operating ratio-

Year 2020

Cost of goods sold 300000

Operating expenses 113000

Net sales 500000

Operating ratio 82.6

Operating ratio indicate the efficiency of the organisation and comparing total operating

expenses of the company to the net sales. The smaller ratio the more effective the business

operation and generating the revenue and expenses. In the context of Future trading, the 85%

which is higher than the ideal ratio and will help the management to take further steps. This

indicate that organisation is facing expenses as compared to the sales that is being collected and

lower the ratio will be better for the company (Pablo and et.al, 2007).

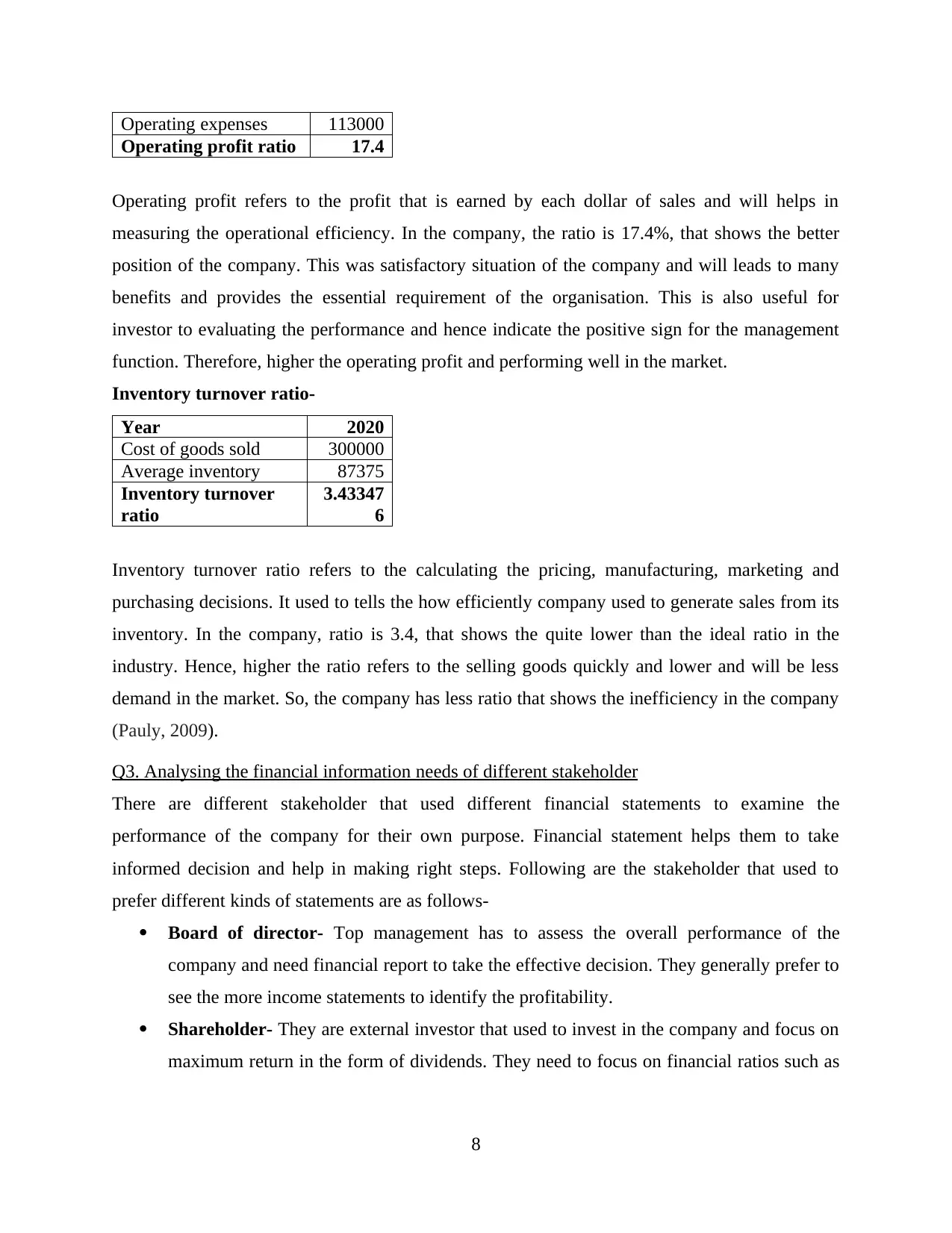

Operating profit ratio-

Year 2020

Sales 500000

Cost of goods sold 300000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating expenses 113000

Operating profit ratio 17.4

Operating profit refers to the profit that is earned by each dollar of sales and will helps in

measuring the operational efficiency. In the company, the ratio is 17.4%, that shows the better

position of the company. This was satisfactory situation of the company and will leads to many

benefits and provides the essential requirement of the organisation. This is also useful for

investor to evaluating the performance and hence indicate the positive sign for the management

function. Therefore, higher the operating profit and performing well in the market.

Inventory turnover ratio-

Year 2020

Cost of goods sold 300000

Average inventory 87375

Inventory turnover

ratio

3.43347

6

Inventory turnover ratio refers to the calculating the pricing, manufacturing, marketing and

purchasing decisions. It used to tells the how efficiently company used to generate sales from its

inventory. In the company, ratio is 3.4, that shows the quite lower than the ideal ratio in the

industry. Hence, higher the ratio refers to the selling goods quickly and lower and will be less

demand in the market. So, the company has less ratio that shows the inefficiency in the company

(Pauly, 2009).

Q3. Analysing the financial information needs of different stakeholder

There are different stakeholder that used different financial statements to examine the

performance of the company for their own purpose. Financial statement helps them to take

informed decision and help in making right steps. Following are the stakeholder that used to

prefer different kinds of statements are as follows-

Board of director- Top management has to assess the overall performance of the

company and need financial report to take the effective decision. They generally prefer to

see the more income statements to identify the profitability.

Shareholder- They are external investor that used to invest in the company and focus on

maximum return in the form of dividends. They need to focus on financial ratios such as

8

Operating profit ratio 17.4

Operating profit refers to the profit that is earned by each dollar of sales and will helps in

measuring the operational efficiency. In the company, the ratio is 17.4%, that shows the better

position of the company. This was satisfactory situation of the company and will leads to many

benefits and provides the essential requirement of the organisation. This is also useful for

investor to evaluating the performance and hence indicate the positive sign for the management

function. Therefore, higher the operating profit and performing well in the market.

Inventory turnover ratio-

Year 2020

Cost of goods sold 300000

Average inventory 87375

Inventory turnover

ratio

3.43347

6

Inventory turnover ratio refers to the calculating the pricing, manufacturing, marketing and

purchasing decisions. It used to tells the how efficiently company used to generate sales from its

inventory. In the company, ratio is 3.4, that shows the quite lower than the ideal ratio in the

industry. Hence, higher the ratio refers to the selling goods quickly and lower and will be less

demand in the market. So, the company has less ratio that shows the inefficiency in the company

(Pauly, 2009).

Q3. Analysing the financial information needs of different stakeholder

There are different stakeholder that used different financial statements to examine the

performance of the company for their own purpose. Financial statement helps them to take

informed decision and help in making right steps. Following are the stakeholder that used to

prefer different kinds of statements are as follows-

Board of director- Top management has to assess the overall performance of the

company and need financial report to take the effective decision. They generally prefer to

see the more income statements to identify the profitability.

Shareholder- They are external investor that used to invest in the company and focus on

maximum return in the form of dividends. They need to focus on financial ratios such as

8

operating profit ratio, dividend pay out ratio and analyse the income statements to

determine the net profit of the organisation (Row and Popiel, 1987).

Banks- These are extremely interested in the company and make sure that company able

to afford the loans and other obligations. The need to take the appropriate steps before

granting them loans and must evaluate the operational efficiency. It generally helps in

evaluating the effectiveness of the organisation for that need to consider the cash flow of

the company and calculate the acid ratio that helps in evaluating the liabilities and their

current assets.

Customer- They were interested in the company’s continuous into the future as secure

source of supply and sales price increase. They show efforts when company able to

perform well in the market and will need to assess the income statements and balance

sheet of the organisation (Schoonraad, N., 2005).

Creditors- They are interested in the company to know the liquidity and efficiency of the

organisation so that it can pay regular for its purchase from them and for that they can

keep eye on the cash position of company. They need to analyse financial statements

such as balance sheet and other important statements. They need to understand the

effectiveness and operational profitability and for that it measure average payment period

to payable expressed in days.

Competitor- They also interested in financial result of the organisation to see whether its

performing better or worse than its own. To analyse cost and expense that helps in

evaluate the balance sheet and cash flow statement.

CONCLUSION

From the above report it is concluded that managing the resources will help in managing

overall efficiently of the organisation and which is more beneficial for the company. This is

important to understand the performance. Apart from that it being determine the different

stakeholder to assess the performance of the firm.

9

determine the net profit of the organisation (Row and Popiel, 1987).

Banks- These are extremely interested in the company and make sure that company able

to afford the loans and other obligations. The need to take the appropriate steps before

granting them loans and must evaluate the operational efficiency. It generally helps in

evaluating the effectiveness of the organisation for that need to consider the cash flow of

the company and calculate the acid ratio that helps in evaluating the liabilities and their

current assets.

Customer- They were interested in the company’s continuous into the future as secure

source of supply and sales price increase. They show efforts when company able to

perform well in the market and will need to assess the income statements and balance

sheet of the organisation (Schoonraad, N., 2005).

Creditors- They are interested in the company to know the liquidity and efficiency of the

organisation so that it can pay regular for its purchase from them and for that they can

keep eye on the cash position of company. They need to analyse financial statements

such as balance sheet and other important statements. They need to understand the

effectiveness and operational profitability and for that it measure average payment period

to payable expressed in days.

Competitor- They also interested in financial result of the organisation to see whether its

performing better or worse than its own. To analyse cost and expense that helps in

evaluate the balance sheet and cash flow statement.

CONCLUSION

From the above report it is concluded that managing the resources will help in managing

overall efficiently of the organisation and which is more beneficial for the company. This is

important to understand the performance. Apart from that it being determine the different

stakeholder to assess the performance of the firm.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSIGNMENT 2

INTRODUCTION

In this report it is being determine the effectiveness of the organisation and need to

understand the meaning of cost-plus pricing and problems of using this approach in the

company and discussing the importance. Apart from that evaluating some ratios is being

analysed to take effective decision in the company.

MAIN BODY

Q2. Identifying the meaning of cost-plus approach and problem

Cost plus approach also called markup pricing it is like practice by the organisation to determine

the cost of product to the company and then adding some percentage on the top of that price to

evaluate the selling price to the customer. This is simple cost-based pricing strategy to set the

price for certain goods and services. Makeup percentage is added to the total cost to assess the

cost to offer the product and services and helps in finding the accuracy of cost that is being used

in the management. This method is not acceptable for deriving the exact price of product that is

to be sold in the competitive market and it does not factor in the price charged by the

competitors.

Some of the problems are there while using this approach-

Limiting price segmentation- This basically reduce the ability to price to certain

segments of the market. This also put the limits on the limitation on innovation and that

leads to reduce the creativity and distinct that put into to sell the goods and services

(Snell, Morris and Bohlander, 2015).

Lacks market orientation- The main problem is that it does not gives market orientation

and that lacks the efficiency and effectiveness in the company. Price is basically set

without targeted the customer to perceive the product as good value at that point of time.

It create the problem in solving the issue of performing well in the market and will leads

to problem.

Production inconsistency- This also functional problem that understand the cost which

is rarely static and leads to moving target or risk variability in profit margin. However,

10

INTRODUCTION

In this report it is being determine the effectiveness of the organisation and need to

understand the meaning of cost-plus pricing and problems of using this approach in the

company and discussing the importance. Apart from that evaluating some ratios is being

analysed to take effective decision in the company.

MAIN BODY

Q2. Identifying the meaning of cost-plus approach and problem

Cost plus approach also called markup pricing it is like practice by the organisation to determine

the cost of product to the company and then adding some percentage on the top of that price to

evaluate the selling price to the customer. This is simple cost-based pricing strategy to set the

price for certain goods and services. Makeup percentage is added to the total cost to assess the

cost to offer the product and services and helps in finding the accuracy of cost that is being used

in the management. This method is not acceptable for deriving the exact price of product that is

to be sold in the competitive market and it does not factor in the price charged by the

competitors.

Some of the problems are there while using this approach-

Limiting price segmentation- This basically reduce the ability to price to certain

segments of the market. This also put the limits on the limitation on innovation and that

leads to reduce the creativity and distinct that put into to sell the goods and services

(Snell, Morris and Bohlander, 2015).

Lacks market orientation- The main problem is that it does not gives market orientation

and that lacks the efficiency and effectiveness in the company. Price is basically set

without targeted the customer to perceive the product as good value at that point of time.

It create the problem in solving the issue of performing well in the market and will leads

to problem.

Production inconsistency- This also functional problem that understand the cost which

is rarely static and leads to moving target or risk variability in profit margin. However,

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

material used in the product may become more expensive or harder to get and will lower

the gross margin of the company effectiveness.

Q3. Identifying the financial ratios of the company

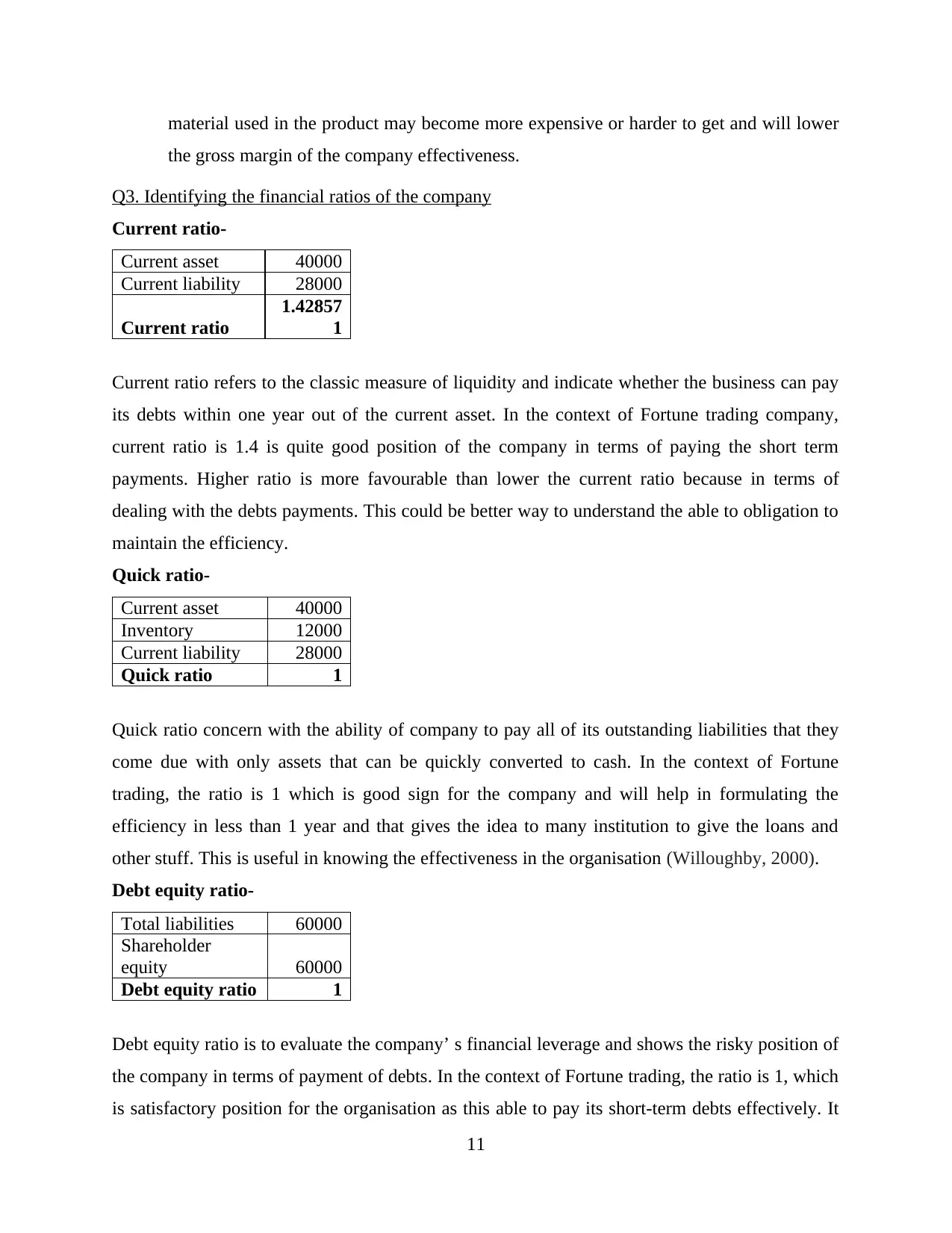

Current ratio-

Current asset 40000

Current liability 28000

Current ratio

1.42857

1

Current ratio refers to the classic measure of liquidity and indicate whether the business can pay

its debts within one year out of the current asset. In the context of Fortune trading company,

current ratio is 1.4 is quite good position of the company in terms of paying the short term

payments. Higher ratio is more favourable than lower the current ratio because in terms of

dealing with the debts payments. This could be better way to understand the able to obligation to

maintain the efficiency.

Quick ratio-

Current asset 40000

Inventory 12000

Current liability 28000

Quick ratio 1

Quick ratio concern with the ability of company to pay all of its outstanding liabilities that they

come due with only assets that can be quickly converted to cash. In the context of Fortune

trading, the ratio is 1 which is good sign for the company and will help in formulating the

efficiency in less than 1 year and that gives the idea to many institution to give the loans and

other stuff. This is useful in knowing the effectiveness in the organisation (Willoughby, 2000).

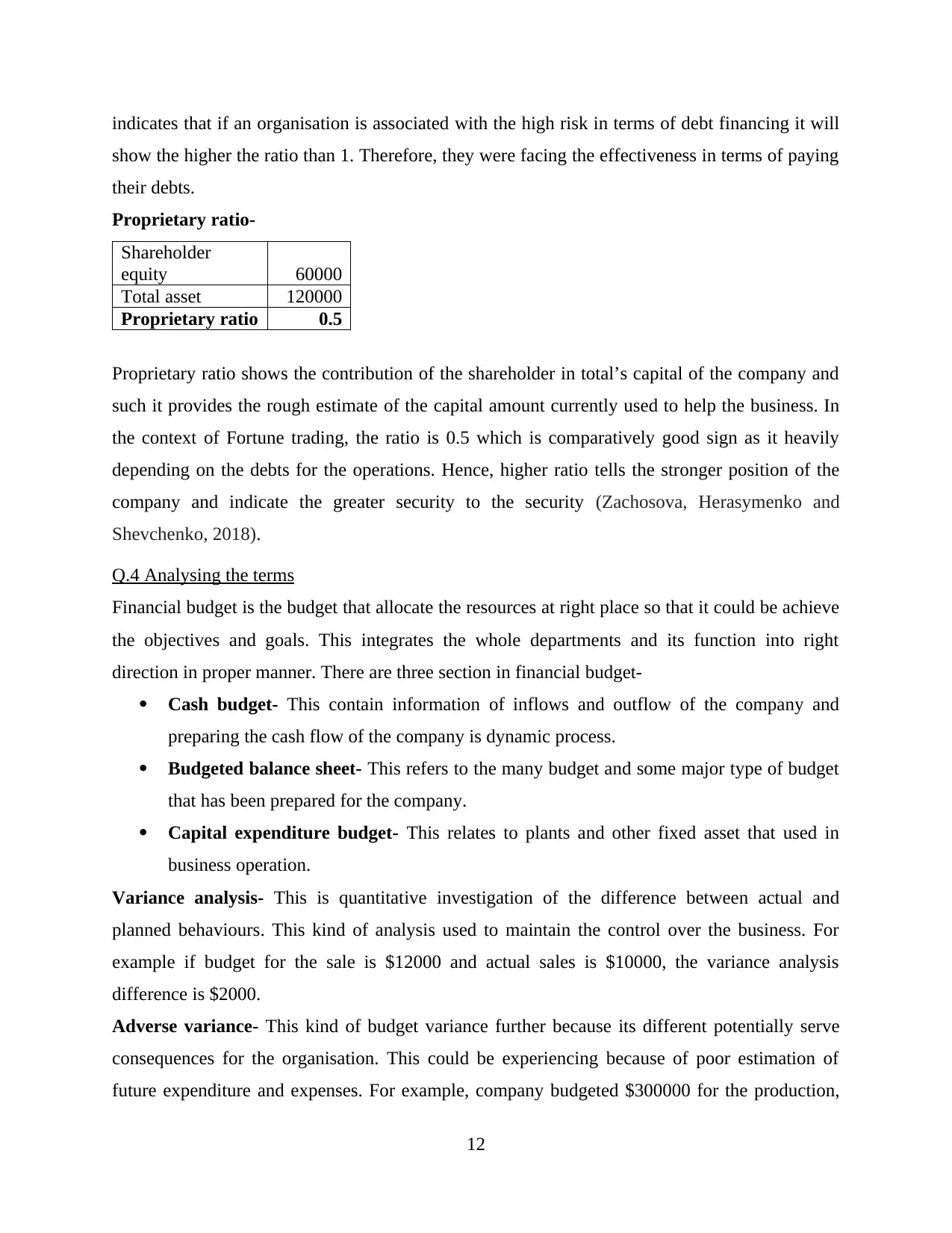

Debt equity ratio-

Total liabilities 60000

Shareholder

equity 60000

Debt equity ratio 1

Debt equity ratio is to evaluate the company’ s financial leverage and shows the risky position of

the company in terms of payment of debts. In the context of Fortune trading, the ratio is 1, which

is satisfactory position for the organisation as this able to pay its short-term debts effectively. It

11

the gross margin of the company effectiveness.

Q3. Identifying the financial ratios of the company

Current ratio-

Current asset 40000

Current liability 28000

Current ratio

1.42857

1

Current ratio refers to the classic measure of liquidity and indicate whether the business can pay

its debts within one year out of the current asset. In the context of Fortune trading company,

current ratio is 1.4 is quite good position of the company in terms of paying the short term

payments. Higher ratio is more favourable than lower the current ratio because in terms of

dealing with the debts payments. This could be better way to understand the able to obligation to

maintain the efficiency.

Quick ratio-

Current asset 40000

Inventory 12000

Current liability 28000

Quick ratio 1

Quick ratio concern with the ability of company to pay all of its outstanding liabilities that they

come due with only assets that can be quickly converted to cash. In the context of Fortune

trading, the ratio is 1 which is good sign for the company and will help in formulating the

efficiency in less than 1 year and that gives the idea to many institution to give the loans and

other stuff. This is useful in knowing the effectiveness in the organisation (Willoughby, 2000).

Debt equity ratio-

Total liabilities 60000

Shareholder

equity 60000

Debt equity ratio 1

Debt equity ratio is to evaluate the company’ s financial leverage and shows the risky position of

the company in terms of payment of debts. In the context of Fortune trading, the ratio is 1, which

is satisfactory position for the organisation as this able to pay its short-term debts effectively. It

11

indicates that if an organisation is associated with the high risk in terms of debt financing it will

show the higher the ratio than 1. Therefore, they were facing the effectiveness in terms of paying

their debts.

Proprietary ratio-

Shareholder

equity 60000

Total asset 120000

Proprietary ratio 0.5

Proprietary ratio shows the contribution of the shareholder in total’s capital of the company and

such it provides the rough estimate of the capital amount currently used to help the business. In

the context of Fortune trading, the ratio is 0.5 which is comparatively good sign as it heavily

depending on the debts for the operations. Hence, higher ratio tells the stronger position of the

company and indicate the greater security to the security (Zachosova, Herasymenko and

Shevchenko, 2018).

Q.4 Analysing the terms

Financial budget is the budget that allocate the resources at right place so that it could be achieve

the objectives and goals. This integrates the whole departments and its function into right

direction in proper manner. There are three section in financial budget-

Cash budget- This contain information of inflows and outflow of the company and

preparing the cash flow of the company is dynamic process.

Budgeted balance sheet- This refers to the many budget and some major type of budget

that has been prepared for the company.

Capital expenditure budget- This relates to plants and other fixed asset that used in

business operation.

Variance analysis- This is quantitative investigation of the difference between actual and

planned behaviours. This kind of analysis used to maintain the control over the business. For

example if budget for the sale is $12000 and actual sales is $10000, the variance analysis

difference is $2000.

Adverse variance- This kind of budget variance further because its different potentially serve

consequences for the organisation. This could be experiencing because of poor estimation of

future expenditure and expenses. For example, company budgeted $300000 for the production,

12

show the higher the ratio than 1. Therefore, they were facing the effectiveness in terms of paying

their debts.

Proprietary ratio-

Shareholder

equity 60000

Total asset 120000

Proprietary ratio 0.5

Proprietary ratio shows the contribution of the shareholder in total’s capital of the company and

such it provides the rough estimate of the capital amount currently used to help the business. In

the context of Fortune trading, the ratio is 0.5 which is comparatively good sign as it heavily

depending on the debts for the operations. Hence, higher ratio tells the stronger position of the

company and indicate the greater security to the security (Zachosova, Herasymenko and

Shevchenko, 2018).

Q.4 Analysing the terms

Financial budget is the budget that allocate the resources at right place so that it could be achieve

the objectives and goals. This integrates the whole departments and its function into right

direction in proper manner. There are three section in financial budget-

Cash budget- This contain information of inflows and outflow of the company and

preparing the cash flow of the company is dynamic process.

Budgeted balance sheet- This refers to the many budget and some major type of budget

that has been prepared for the company.

Capital expenditure budget- This relates to plants and other fixed asset that used in

business operation.

Variance analysis- This is quantitative investigation of the difference between actual and

planned behaviours. This kind of analysis used to maintain the control over the business. For

example if budget for the sale is $12000 and actual sales is $10000, the variance analysis

difference is $2000.

Adverse variance- This kind of budget variance further because its different potentially serve

consequences for the organisation. This could be experiencing because of poor estimation of

future expenditure and expenses. For example, company budgeted $300000 for the production,

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

marketing for the business. It include labour, ink and cardstock. So, final amount was $325000.

This refers to the adverse budget variance of $25000.

Favourable variances- Variances should be indicated exactly as favourable when revenue

comes in higher than budgeted or when expenses are lower than expected. The result will be

greater income than original forecasted. This basically occurs when cost to produce something is

less than budgeted cost. For example, if supplies expenses budgeted to $40000 but actual

supplies expenses ends up being $30000, then $10000 variances is favourable because having the

fewer expenses than were budgeted that was good for the position of company. This basically

indicated the positive mark to the business operations and will helps in understanding company

variances (Kut, Pramborg and Smolarski, 2007).

Positive variances- This usually takes happens to relate with the favourable variance and almost

same meaning about the term. This is essential to make the important decision according the

budget when used to form for future circumstances to make important steps in fear future. For

example, if company budget $20000 for an expense and spends $16000 from the budget. The

surplus of $4000 or called as the positive expense’s variances. This is will be beneficial for the

organisation to attain surplus amount so that it could use this amount in other way where it

needed and hence will be useful.

Negative variance- This happens where ‘actual’ is less than ‘planned’ or budgeted and would be

when raw material cost is less then expected, hence sales were sales than predicted and labour

cost were below the budgeted figure. For an example, if budgeted expenses were less than

predicted which is $300000 but the actual cost that will occur is $350000, so the negative

expenses were $50000 or 25%. Hence this create problem for the company in near future to

make anu budget and at the time forecast. So, to reduce that it need to be determine properly to

avoid the negative variance in the business operations.

Direct labour variances- This concern with the difference between the standard cost production

and actual cost in production. There are two types of labour variance also that used function

differently. For an example, the actual hours of direct labour at standard rate equals to $43200,

standard cost of direct labour comes to $48000. To calculate the direct labour variance, subtract

the actual hours of direct labour at standard rate ($43200) from the actual cost of direct labour

($46800) to receive the $3600 unfavourable variance.

13

This refers to the adverse budget variance of $25000.

Favourable variances- Variances should be indicated exactly as favourable when revenue

comes in higher than budgeted or when expenses are lower than expected. The result will be

greater income than original forecasted. This basically occurs when cost to produce something is

less than budgeted cost. For example, if supplies expenses budgeted to $40000 but actual

supplies expenses ends up being $30000, then $10000 variances is favourable because having the

fewer expenses than were budgeted that was good for the position of company. This basically

indicated the positive mark to the business operations and will helps in understanding company

variances (Kut, Pramborg and Smolarski, 2007).

Positive variances- This usually takes happens to relate with the favourable variance and almost

same meaning about the term. This is essential to make the important decision according the

budget when used to form for future circumstances to make important steps in fear future. For

example, if company budget $20000 for an expense and spends $16000 from the budget. The

surplus of $4000 or called as the positive expense’s variances. This is will be beneficial for the

organisation to attain surplus amount so that it could use this amount in other way where it

needed and hence will be useful.

Negative variance- This happens where ‘actual’ is less than ‘planned’ or budgeted and would be

when raw material cost is less then expected, hence sales were sales than predicted and labour

cost were below the budgeted figure. For an example, if budgeted expenses were less than

predicted which is $300000 but the actual cost that will occur is $350000, so the negative

expenses were $50000 or 25%. Hence this create problem for the company in near future to

make anu budget and at the time forecast. So, to reduce that it need to be determine properly to

avoid the negative variance in the business operations.

Direct labour variances- This concern with the difference between the standard cost production

and actual cost in production. There are two types of labour variance also that used function

differently. For an example, the actual hours of direct labour at standard rate equals to $43200,

standard cost of direct labour comes to $48000. To calculate the direct labour variance, subtract

the actual hours of direct labour at standard rate ($43200) from the actual cost of direct labour

($46800) to receive the $3600 unfavourable variance.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it is concluded that every organisation has to regulate and maintain

their resources effectively to achieve the efficiency in long term operations. This will also going

to increase the overall performance of the company and hence enhance the productivity. It is

being discussed in this report about the cost-plus pricing in the company and its benefits to the

management and also evaluating its problem that used to face while implementing this. Apart

from that discussed certain ratios and their impact in the firm such as Profitability ratio, Solvency

ratio, Efficient ratio and also analyse some terms used in the company.

14

From the above report it is concluded that every organisation has to regulate and maintain

their resources effectively to achieve the efficiency in long term operations. This will also going

to increase the overall performance of the company and hence enhance the productivity. It is

being discussed in this report about the cost-plus pricing in the company and its benefits to the

management and also evaluating its problem that used to face while implementing this. Apart

from that discussed certain ratios and their impact in the firm such as Profitability ratio, Solvency

ratio, Efficient ratio and also analyse some terms used in the company.

14

REFERENCES

Books and Journal

Aidemark, L. G., 2001. Managed health care perspectives: a study of management accounting

reforms on managing financial difficulties in a health care organization. European

Accounting Review. 10(3). pp.545-560.

Barsky, N. P. and Marchant, G., 2000. The most valuable resource-measuring and managing

intellectual capital. Strategic Finance. 81(8). p.58.

Beer, M. and et.al, 1984. Managing human assets. Simon and Schuster.

Cardon, M. S. and Stevens, C. E., 2004. Managing human resources in small organizations:

What do we know?. Human resource management review. 14(3). pp.295-323.

Dolganova, Y. and et.al., 2020, December. State financial resources as a tool for managing

sustainable development of territories. In E3S Web of Conferences (Vol. 208, p. 08015).

Gould, D. M. and Melecky, M., 2017. Risks and returns: Managing financial trade-offs for

inclusive growth in Europe and Central Asia. The World Bank.

Kut, C., Pramborg, B. and Smolarski, J., 2007. Managing financial risk and uncertainty: The case

of venture capital and buy‐out funds. Global business and organizational

excellence. 26(2). pp.53-64.

Pablo, A. L. and et.al, 2007. Identifying, enabling and managing dynamic capabilities in the

public sector. Journal of management studies. 44(5). pp.687-708.

Pauly, L. W., 2009. Managing financial emergencies in an integrating

world. Globalizations. 6(3). pp.353-364.

Row, A. and Popiel, P. A., 1987. Managing financial adjustment in middle-income countries.

World Bank.

Schoonraad, N., 2005. Managing financial communication: Towards a conceptual

model (Doctoral dissertation, University of Pretoria).

Snell, S., Morris, S. and Bohlander, G. W., 2015. Managing human resources. Cengage

Learning.

Willoughby, C., 2000. Singapore's experience in managing motorization and its relevance to

other countries.

Zachosova, N., Herasymenko, O. and Shevchenko, А., 2018. Risks and possibilities of the effect

of financial inclusion on managing the financial security at the macro level. Investment

Management & Financial Innovations. 15(4). p.304.

15

Books and Journal

Aidemark, L. G., 2001. Managed health care perspectives: a study of management accounting

reforms on managing financial difficulties in a health care organization. European

Accounting Review. 10(3). pp.545-560.

Barsky, N. P. and Marchant, G., 2000. The most valuable resource-measuring and managing

intellectual capital. Strategic Finance. 81(8). p.58.

Beer, M. and et.al, 1984. Managing human assets. Simon and Schuster.

Cardon, M. S. and Stevens, C. E., 2004. Managing human resources in small organizations:

What do we know?. Human resource management review. 14(3). pp.295-323.

Dolganova, Y. and et.al., 2020, December. State financial resources as a tool for managing

sustainable development of territories. In E3S Web of Conferences (Vol. 208, p. 08015).

Gould, D. M. and Melecky, M., 2017. Risks and returns: Managing financial trade-offs for

inclusive growth in Europe and Central Asia. The World Bank.

Kut, C., Pramborg, B. and Smolarski, J., 2007. Managing financial risk and uncertainty: The case

of venture capital and buy‐out funds. Global business and organizational

excellence. 26(2). pp.53-64.

Pablo, A. L. and et.al, 2007. Identifying, enabling and managing dynamic capabilities in the

public sector. Journal of management studies. 44(5). pp.687-708.

Pauly, L. W., 2009. Managing financial emergencies in an integrating

world. Globalizations. 6(3). pp.353-364.

Row, A. and Popiel, P. A., 1987. Managing financial adjustment in middle-income countries.

World Bank.

Schoonraad, N., 2005. Managing financial communication: Towards a conceptual

model (Doctoral dissertation, University of Pretoria).

Snell, S., Morris, S. and Bohlander, G. W., 2015. Managing human resources. Cengage

Learning.

Willoughby, C., 2000. Singapore's experience in managing motorization and its relevance to

other countries.

Zachosova, N., Herasymenko, O. and Shevchenko, А., 2018. Risks and possibilities of the effect

of financial inclusion on managing the financial security at the macro level. Investment

Management & Financial Innovations. 15(4). p.304.

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.