Financial Resource Management Report for Business Finance Module

VerifiedAdded on 2019/12/03

|28

|7871

|243

Report

AI Summary

This report delves into the critical aspects of financial resource management, essential for the smooth operation of any enterprise. It begins with an introduction to the importance of financial planning and the various sources of finance available to businesses, including share capital, retained earnings, and bank loans, along with their respective advantages and disadvantages. The report then examines the implications of each source, such as legal considerations, potential for bankruptcy, and dilution of ownership. The analysis extends to short-term sources like cash management, hire purchase, and leasing. Furthermore, the report presents three case studies focusing on small business startups, large business expansions, and the acquisition of a medium-sized company, evaluating the most appropriate sources of finance for each scenario. The report also explores the cost of different finance sources, the importance of financial planning, and the information required for informed decision-making, including sample profit and loss accounts and balance sheets. Finally, the report addresses making financial decisions through formal written reports and evaluates the financial performance of businesses using tools like books of prime entry, providing a comprehensive overview of financial resource management.

MANAGING FINANCIAL

RESOURCES

1

RESOURCES

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ...............................................................................................................................3

TASK 1 UNDERSTANDING SOURCES OF FINANCE AVAILABLE TO BUSINESS .................3

Scenario 1.............................................................................................................................................3

Information pack for new and existing businesses which Identifies the sources of finance

available to business....................................................................................................................3

Implications of source of finance along with its advantage and disadvantage...........................5

Evaluating appropriate source of finance for business project...................................................7

M2: Appropriate source of finance for small business................................................................8

TASK 2 UNDERSTADING IMPLICATIONS OF FINANCE AS A RESOURCE.............................8

Scenario 1 ............................................................................................................................................8

2.1 Cost of different sources of finance......................................................................................8

2.2 Importance of financial planning..........................................................................................9

2.3 Types of information required for decision making..............................................................9

2.4 Sample profit and loss account and balance sheet with explanatory notes...........................9

TASK 3 MAKING FINANCIAL DECISIONS ................................................................................10

Scenario 1...........................................................................................................................................10

3.1 Findings and recommendations in formal written report ...................................................13

Scenario 2 .................................................................................................................................14

3.3 Written report to Directors..................................................................................................16

Scenario 3 ..........................................................................................................................................16

Scenario 4 ..........................................................................................................................................21

LO4 EVALUATING FINANCIAL PERFORMANCE OF BUSINESS ...........................................22

Scenario 1...........................................................................................................................................22

Scenario 2 ..........................................................................................................................................23

4.1 Books of prime entry...........................................................................................................23

Scenario 3...........................................................................................................................................24

CONCLUSION..................................................................................................................................24

REFERENCES...................................................................................................................................26

2

INTRODUCTION ...............................................................................................................................3

TASK 1 UNDERSTANDING SOURCES OF FINANCE AVAILABLE TO BUSINESS .................3

Scenario 1.............................................................................................................................................3

Information pack for new and existing businesses which Identifies the sources of finance

available to business....................................................................................................................3

Implications of source of finance along with its advantage and disadvantage...........................5

Evaluating appropriate source of finance for business project...................................................7

M2: Appropriate source of finance for small business................................................................8

TASK 2 UNDERSTADING IMPLICATIONS OF FINANCE AS A RESOURCE.............................8

Scenario 1 ............................................................................................................................................8

2.1 Cost of different sources of finance......................................................................................8

2.2 Importance of financial planning..........................................................................................9

2.3 Types of information required for decision making..............................................................9

2.4 Sample profit and loss account and balance sheet with explanatory notes...........................9

TASK 3 MAKING FINANCIAL DECISIONS ................................................................................10

Scenario 1...........................................................................................................................................10

3.1 Findings and recommendations in formal written report ...................................................13

Scenario 2 .................................................................................................................................14

3.3 Written report to Directors..................................................................................................16

Scenario 3 ..........................................................................................................................................16

Scenario 4 ..........................................................................................................................................21

LO4 EVALUATING FINANCIAL PERFORMANCE OF BUSINESS ...........................................22

Scenario 1...........................................................................................................................................22

Scenario 2 ..........................................................................................................................................23

4.1 Books of prime entry...........................................................................................................23

Scenario 3...........................................................................................................................................24

CONCLUSION..................................................................................................................................24

REFERENCES...................................................................................................................................26

2

INTRODUCTION

Management of financial resources is necessary in every organization and it is required for

smooth functioning of the enterprise. Further, every organization prepares different plans through

which finance can be managed in an appropriate manner. This allows business to focus on its key

activities and in turn boosts overall efficiency of the firm (Reid, 2003). Different sources of finance

are present which businesses can consider for satisfying its financial needs but it depends on every

organization which source to adopt so as to gain long term benefits with the help of this. To

consider implications of sources of finance is also necessary as through this appropriate decision

can be taken easily. The present study is being carried out by focusing on the range of finance

available to business along with its implications such as advantage, disadvantage etc. Apart from

this, three case study examples have been discussed in the report which involves small business

start up, large expansion etc.

TASK 1: UNDERSTANDING SOURCES OF FINANCE AVAILABLE TO

BUSINESS

SCENARIO 1

Information pack for new and existing businesses which Identifies the sources of finance available

to business

Different sources of finance are present in business with the help of which enterprise can

easily satisfy its financial needs. Selecting most appropriate financial source depends on the nature

of business, its size and type of operations being carried out in the company (Vereker, 2002).

Further, to avoid unfavourable situations appropriate sources are adopted by the management which

enhances organizational performance in the market. Long and short/ medium term sources are

present in business but decision has to be taken which source has to adopt which is cheap and can

enhance profitability level. Different sources of finance present are as follows: Share capital: It is regarded as one of the most effective source of finance which usually

every organization considers. In order to satisfy financial needs business can issue equity

shares in the market through which large number of investors can be attracted. This source

of finance is generally suitable for businesses which are old and large. Companies which are

operating on wider platform can issue shares in the market and can easily raise additional

funds with the help of this (Weaver, 2012). By adopting this source it is possible for the

business to avoid unfavourable situations such as inadequacy of finance which can further

enhance overall reputation in the market which is one of the main objectives of firm behind

3

Management of financial resources is necessary in every organization and it is required for

smooth functioning of the enterprise. Further, every organization prepares different plans through

which finance can be managed in an appropriate manner. This allows business to focus on its key

activities and in turn boosts overall efficiency of the firm (Reid, 2003). Different sources of finance

are present which businesses can consider for satisfying its financial needs but it depends on every

organization which source to adopt so as to gain long term benefits with the help of this. To

consider implications of sources of finance is also necessary as through this appropriate decision

can be taken easily. The present study is being carried out by focusing on the range of finance

available to business along with its implications such as advantage, disadvantage etc. Apart from

this, three case study examples have been discussed in the report which involves small business

start up, large expansion etc.

TASK 1: UNDERSTANDING SOURCES OF FINANCE AVAILABLE TO

BUSINESS

SCENARIO 1

Information pack for new and existing businesses which Identifies the sources of finance available

to business

Different sources of finance are present in business with the help of which enterprise can

easily satisfy its financial needs. Selecting most appropriate financial source depends on the nature

of business, its size and type of operations being carried out in the company (Vereker, 2002).

Further, to avoid unfavourable situations appropriate sources are adopted by the management which

enhances organizational performance in the market. Long and short/ medium term sources are

present in business but decision has to be taken which source has to adopt which is cheap and can

enhance profitability level. Different sources of finance present are as follows: Share capital: It is regarded as one of the most effective source of finance which usually

every organization considers. In order to satisfy financial needs business can issue equity

shares in the market through which large number of investors can be attracted. This source

of finance is generally suitable for businesses which are old and large. Companies which are

operating on wider platform can issue shares in the market and can easily raise additional

funds with the help of this (Weaver, 2012). By adopting this source it is possible for the

business to avoid unfavourable situations such as inadequacy of finance which can further

enhance overall reputation in the market which is one of the main objectives of firm behind

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

carrying out operations in the market. Retained earnings: It is the next effective source of finance which business can easily

consider. Retained earnings are the amount saved by company in order to meet any

unforeseen contingency. This type of source can be easily considered by large sized

organizations that are having strong financial base and in turn this can easily satisfy

financial needs of the entity in the most efficient manner. This source is not applicable in

case of businesses that have been newly established in the market as their financial position

is regarded to be weak. Apart from this, one of the key attribute of using this source is that it

is cheap and amount can be easily obtained as per requirement of the firm (Norton and

Kelly, 2014).

Bank loan: Taking loan from financial institutions also supports organization in satisfying

its financial needs and in turn acts as a development tool. Further, various banks are present

in the market who can provide loan to company at a cheaper rate of interest. In order to

satisfy financial needs, company can compare interest rate of different banks and can obtain

funds from specific financial institution present in the market. It is considered as an effective

external source of finance and through these financial needs of entity can be satisfied easily.

This source is especially beneficial when organization takes expansion decision and it assist

in carrying out operations in an effective manner (Burgess, 2007).

So these are some of the long term sources of finance which business can easily consider as

per requirement of the management. Further, short term sources of finance are also present which

are as follows: Cash management: It is considered as an effective short term source of finance where

organization can manage its cash through proper planning (Mohsin, 2013). Through this

source organization can easily deal with the situation of inadequacy of finance and this can

be favourable for business in every possible manner. This source is beneficial for new

business start ups as through effective management of cash they can easily manage funds

which are necessary for the organization.

Hire purchase and leasing: Hire purchase is regarded as the agreement in which owner of

assets lets them on hire for regular instalments paid by the hirer. This short term source of

finance can be easily considered by small and large businesses. When leasing as a source of

finance is adopted then assets can be financed without actually having to buy them outright.

On the other hand, with the help of hire purchase firm can use an asset for fixed period in

return for regular payment (Shahrokhi, 2008). Therefore, this source of finance is also

considered to be effective for small and start up businesses in the market.

4

consider. Retained earnings are the amount saved by company in order to meet any

unforeseen contingency. This type of source can be easily considered by large sized

organizations that are having strong financial base and in turn this can easily satisfy

financial needs of the entity in the most efficient manner. This source is not applicable in

case of businesses that have been newly established in the market as their financial position

is regarded to be weak. Apart from this, one of the key attribute of using this source is that it

is cheap and amount can be easily obtained as per requirement of the firm (Norton and

Kelly, 2014).

Bank loan: Taking loan from financial institutions also supports organization in satisfying

its financial needs and in turn acts as a development tool. Further, various banks are present

in the market who can provide loan to company at a cheaper rate of interest. In order to

satisfy financial needs, company can compare interest rate of different banks and can obtain

funds from specific financial institution present in the market. It is considered as an effective

external source of finance and through these financial needs of entity can be satisfied easily.

This source is especially beneficial when organization takes expansion decision and it assist

in carrying out operations in an effective manner (Burgess, 2007).

So these are some of the long term sources of finance which business can easily consider as

per requirement of the management. Further, short term sources of finance are also present which

are as follows: Cash management: It is considered as an effective short term source of finance where

organization can manage its cash through proper planning (Mohsin, 2013). Through this

source organization can easily deal with the situation of inadequacy of finance and this can

be favourable for business in every possible manner. This source is beneficial for new

business start ups as through effective management of cash they can easily manage funds

which are necessary for the organization.

Hire purchase and leasing: Hire purchase is regarded as the agreement in which owner of

assets lets them on hire for regular instalments paid by the hirer. This short term source of

finance can be easily considered by small and large businesses. When leasing as a source of

finance is adopted then assets can be financed without actually having to buy them outright.

On the other hand, with the help of hire purchase firm can use an asset for fixed period in

return for regular payment (Shahrokhi, 2008). Therefore, this source of finance is also

considered to be effective for small and start up businesses in the market.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

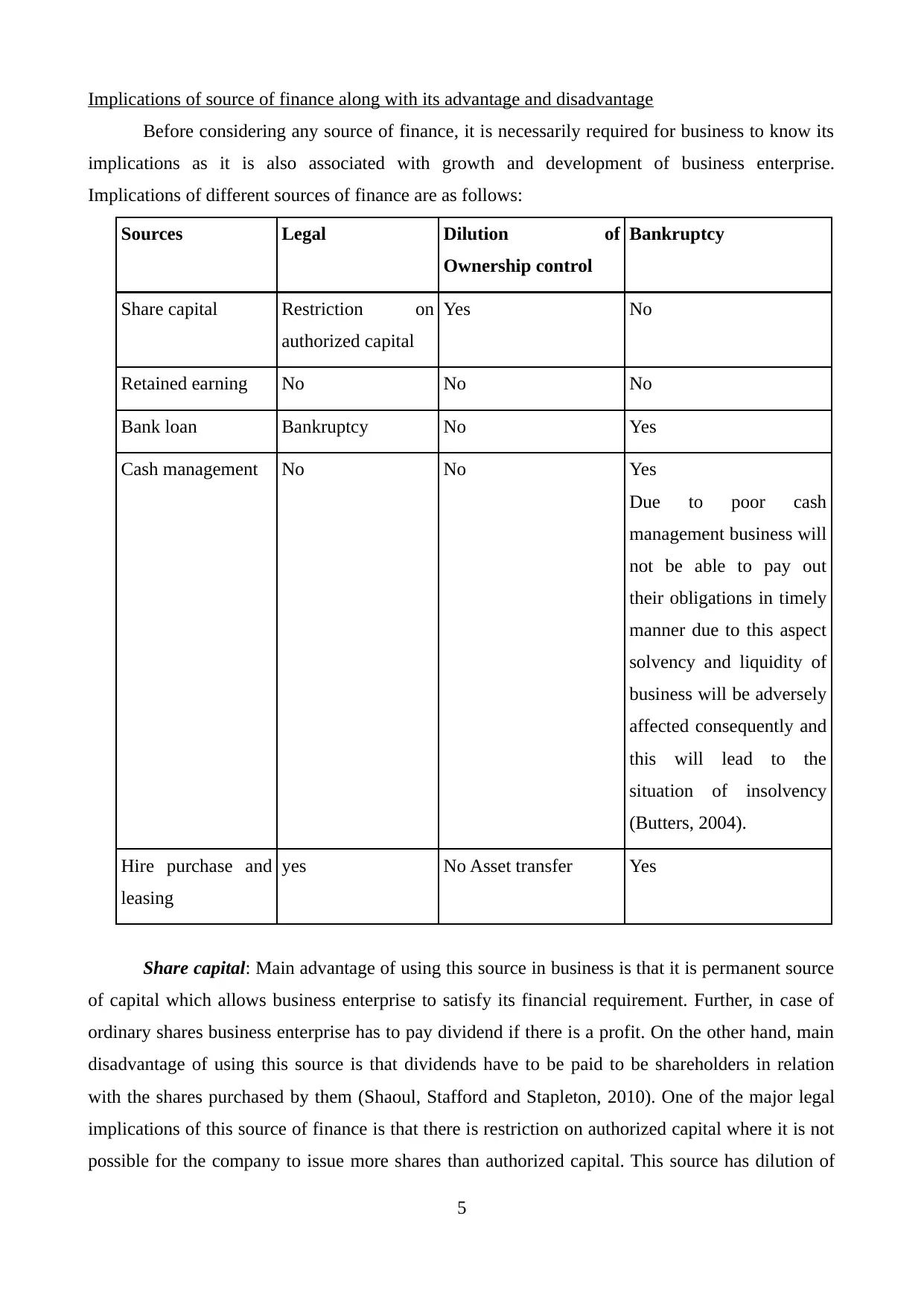

Implications of source of finance along with its advantage and disadvantage

Before considering any source of finance, it is necessarily required for business to know its

implications as it is also associated with growth and development of business enterprise.

Implications of different sources of finance are as follows:

Sources Legal Dilution of

Ownership control

Bankruptcy

Share capital Restriction on

authorized capital

Yes No

Retained earning No No No

Bank loan Bankruptcy No Yes

Cash management No No Yes

Due to poor cash

management business will

not be able to pay out

their obligations in timely

manner due to this aspect

solvency and liquidity of

business will be adversely

affected consequently and

this will lead to the

situation of insolvency

(Butters, 2004).

Hire purchase and

leasing

yes No Asset transfer Yes

Share capital: Main advantage of using this source in business is that it is permanent source

of capital which allows business enterprise to satisfy its financial requirement. Further, in case of

ordinary shares business enterprise has to pay dividend if there is a profit. On the other hand, main

disadvantage of using this source is that dividends have to be paid to be shareholders in relation

with the shares purchased by them (Shaoul, Stafford and Stapleton, 2010). One of the major legal

implications of this source of finance is that there is restriction on authorized capital where it is not

possible for the company to issue more shares than authorized capital. This source has dilution of

5

Before considering any source of finance, it is necessarily required for business to know its

implications as it is also associated with growth and development of business enterprise.

Implications of different sources of finance are as follows:

Sources Legal Dilution of

Ownership control

Bankruptcy

Share capital Restriction on

authorized capital

Yes No

Retained earning No No No

Bank loan Bankruptcy No Yes

Cash management No No Yes

Due to poor cash

management business will

not be able to pay out

their obligations in timely

manner due to this aspect

solvency and liquidity of

business will be adversely

affected consequently and

this will lead to the

situation of insolvency

(Butters, 2004).

Hire purchase and

leasing

yes No Asset transfer Yes

Share capital: Main advantage of using this source in business is that it is permanent source

of capital which allows business enterprise to satisfy its financial requirement. Further, in case of

ordinary shares business enterprise has to pay dividend if there is a profit. On the other hand, main

disadvantage of using this source is that dividends have to be paid to be shareholders in relation

with the shares purchased by them (Shaoul, Stafford and Stapleton, 2010). One of the major legal

implications of this source of finance is that there is restriction on authorized capital where it is not

possible for the company to issue more shares than authorized capital. This source has dilution of

5

ownership where some rights are transferred to the investors of company along with right to take

decisions.

Retained earnings: Main advantage of using this source is that it is not required for business

to increase liability and there is no need to pay interest. But on the other hand, main disadvantage of

using this source is that it is not applicable in case of small businesses. Retained earnings as a

source of finance has no legal implication as it is type of internal source. Apart from this, condition

of bankruptcy is not applicable in case of retained earnings as source of finance (Danso and

Adomako, 2014).

Bank loan: Main advantage of using bank loan as a source of finance is that loan taken can

be easily procured; interest paid on bank loan is tax deductible expenditure. On the other hand, main

disadvantage of using this source is that excess borrowing can lead to decreased cash flow and some

financial institutions carry prepayment penalty. Legal implication of taking bank loan is that it leads

to bankruptcy as sometime it is possible that organization may not be able to repay the amount of

loan taken which has adverse impact on the enterprise. Further, dilution of ownership does not take

place in case of bank loan (Bokpin, 2010).

Cash management: It is one of the most effective internal sources of finance whose main

advantage is that it saves major expenses of the business and cash can be managed with the support

of management. On the other hand, main disadvantage of this source is that it becomes difficult to

determine the most effective way to manage cash within the organization. There are no legal

implications and dilution of ownership control issues associated with this source. Apart from this, in

case of bankruptcy due to poor cash management business will not be able to pay its obligations and

due to this aspect liquidity position of enterprise can be badly affected (Dittenhofer, 2001).

Hire purchase and leasing: Main advantage of adopting hire purchase and leasing as source

of finance is that business can take benefit by utilizing assets without purchasing it. Further, all the

responsibility linked with maintenance of assets is done by the leasing company. On the other hand,

main disadvantage of using this source is that total cost of leasing may exceed and it can be higher

than the purchase of asset. In case if organization is not able to make payment for the assets

acquired then it leads to bankruptcy. Further, the legal implication of this source is that ownership is

not transferred and organization is having right to use the assets (Ezeoha, 2011).

So, these are some of the advantage along with disadvantage of source of finance which

every organization has to consider so that its operations can be carried out in an effective manner.

Further, every source has some implications in the form of legal, bankruptcy and dilution of

ownership control. By considering all these implications, it is possible for business to satisfy its

6

decisions.

Retained earnings: Main advantage of using this source is that it is not required for business

to increase liability and there is no need to pay interest. But on the other hand, main disadvantage of

using this source is that it is not applicable in case of small businesses. Retained earnings as a

source of finance has no legal implication as it is type of internal source. Apart from this, condition

of bankruptcy is not applicable in case of retained earnings as source of finance (Danso and

Adomako, 2014).

Bank loan: Main advantage of using bank loan as a source of finance is that loan taken can

be easily procured; interest paid on bank loan is tax deductible expenditure. On the other hand, main

disadvantage of using this source is that excess borrowing can lead to decreased cash flow and some

financial institutions carry prepayment penalty. Legal implication of taking bank loan is that it leads

to bankruptcy as sometime it is possible that organization may not be able to repay the amount of

loan taken which has adverse impact on the enterprise. Further, dilution of ownership does not take

place in case of bank loan (Bokpin, 2010).

Cash management: It is one of the most effective internal sources of finance whose main

advantage is that it saves major expenses of the business and cash can be managed with the support

of management. On the other hand, main disadvantage of this source is that it becomes difficult to

determine the most effective way to manage cash within the organization. There are no legal

implications and dilution of ownership control issues associated with this source. Apart from this, in

case of bankruptcy due to poor cash management business will not be able to pay its obligations and

due to this aspect liquidity position of enterprise can be badly affected (Dittenhofer, 2001).

Hire purchase and leasing: Main advantage of adopting hire purchase and leasing as source

of finance is that business can take benefit by utilizing assets without purchasing it. Further, all the

responsibility linked with maintenance of assets is done by the leasing company. On the other hand,

main disadvantage of using this source is that total cost of leasing may exceed and it can be higher

than the purchase of asset. In case if organization is not able to make payment for the assets

acquired then it leads to bankruptcy. Further, the legal implication of this source is that ownership is

not transferred and organization is having right to use the assets (Ezeoha, 2011).

So, these are some of the advantage along with disadvantage of source of finance which

every organization has to consider so that its operations can be carried out in an effective manner.

Further, every source has some implications in the form of legal, bankruptcy and dilution of

ownership control. By considering all these implications, it is possible for business to satisfy its

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial needs in an efficient manner and it can act as development tool for the entity. Moreover,

selection of source of finance directly depends on the size, operations and overall nature of the

company which is also significant.

Evaluating appropriate source of finance for business project

Different sources of finance are present but it is required for management to determine the

best one through which financial needs of company can be satisfied easily. In the present scenario

three case study examples for businesses has been considered which involves small business start

up, large business expansion and small group of people who are looking to buy existing medium

sized company.

Small business start up: In case of small business start up it is feasible for business to use

bank loan as source of finance in order to purchase medium sized company. Further, this can easily

enhance liquidity position of the organization and in turn is fruitful for business (Fay, 2015).

Generally small businesses does not have sound liquidity position due to which taking loan from

banks at an cheaper rate of interest is beneficial for company and this can surely satisfy financial

requirement of the company. Main benefit of adopting this source is that it enhances liquidity

position of enterprise which is the main requirement of every company. Apart from this business has

to pay high amount in the form of interest to bank for the amount obtained which is one of the

major drawbacks of this source. Moreover, other sources of finance such as retained earnings and

issuing shares in the market are not at all appropriate for small business as their financial base is

considered to be weak and this does not allows management in accepting this source.

Large business expansion: For large business expansion appropriate source of finance is

retained earnings as through this finance can be easily obtained with the help of internal source.

Further, finance obtained by management can support in purchasing existing medium sized

company. This can surely support business in taking expansion decision where financial needs of

enterprise can be satisfied easily (Norton and Kelly, 2014). Need of large business expansion is to

purchase existing medium sized organization for which internal source is most appropriate as it can

easily assist in acquiring large finance keeping in view overall aim of the company. Generally it is

well known fact that in case of large businesses their financial base is quite strong due to which they

can easily utilize overall funds saved so as to meet any unfavourable situations.

Small group of people: The most appropriate source of finance for small group of people is

cash management as individuals can plan different things and can take corrective actions so as to

manage cash in appropriate manner. Further, main benefit of adopting this source to the business is

that financial requirements can be satisfied internally and it can save major expenses. Basic need of

business operated by small group of people is to purchase medium sized company already operating

7

selection of source of finance directly depends on the size, operations and overall nature of the

company which is also significant.

Evaluating appropriate source of finance for business project

Different sources of finance are present but it is required for management to determine the

best one through which financial needs of company can be satisfied easily. In the present scenario

three case study examples for businesses has been considered which involves small business start

up, large business expansion and small group of people who are looking to buy existing medium

sized company.

Small business start up: In case of small business start up it is feasible for business to use

bank loan as source of finance in order to purchase medium sized company. Further, this can easily

enhance liquidity position of the organization and in turn is fruitful for business (Fay, 2015).

Generally small businesses does not have sound liquidity position due to which taking loan from

banks at an cheaper rate of interest is beneficial for company and this can surely satisfy financial

requirement of the company. Main benefit of adopting this source is that it enhances liquidity

position of enterprise which is the main requirement of every company. Apart from this business has

to pay high amount in the form of interest to bank for the amount obtained which is one of the

major drawbacks of this source. Moreover, other sources of finance such as retained earnings and

issuing shares in the market are not at all appropriate for small business as their financial base is

considered to be weak and this does not allows management in accepting this source.

Large business expansion: For large business expansion appropriate source of finance is

retained earnings as through this finance can be easily obtained with the help of internal source.

Further, finance obtained by management can support in purchasing existing medium sized

company. This can surely support business in taking expansion decision where financial needs of

enterprise can be satisfied easily (Norton and Kelly, 2014). Need of large business expansion is to

purchase existing medium sized organization for which internal source is most appropriate as it can

easily assist in acquiring large finance keeping in view overall aim of the company. Generally it is

well known fact that in case of large businesses their financial base is quite strong due to which they

can easily utilize overall funds saved so as to meet any unfavourable situations.

Small group of people: The most appropriate source of finance for small group of people is

cash management as individuals can plan different things and can take corrective actions so as to

manage cash in appropriate manner. Further, main benefit of adopting this source to the business is

that financial requirements can be satisfied internally and it can save major expenses. Basic need of

business operated by small group of people is to purchase medium sized company already operating

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in the market (Mohsin, 2013). So, this need can be only satisfied only when cash management

techniques are adopted so as to manage funds of the business in effective manner. Main advantage

of using cash management techniques to business is that it supports in dealing with the situation of

inadequacy of funds and enhances overall performance of firm in the market. Through proper cash

management liquidity position of company can be improved to an extent and it can provide base to

business enterprise in every possible manner.

M2: Appropriate source of finance for small business

For small business enterprise taking bank loan is one of the most appropriate source of

finance as through this organization can enhance its liquidity position. Generally businesses

operating on smaller platform have weak financial position and in such condition it is preferable to

take loan from financial institutions at a cheaper rate of interest. This source is considered as best

for company as through this management can easily satisfy its financial requirement and in turn

situation such as inadequacy of funds can be easily avoided. But on the other hand, it can increase

expenditure level of business as company has to pay interest to bank for the amount obtained. Apart

from this savings of small businesses are not adequate due to which it is not possible to implement

financial decisions by using retained earnings as source of finance (Dittenhofer, 2001). Therefore, in

this way taking loan from financial institution is appropriate for small business and can assist in

implementing the financial plan. On the other hand, before considering any source of finance it is

necessary for management to consider its pros and cons so that source considered may not

adversely affect business enterprise. Sometime it can be possible that organization is not able to pay

the interest amount to bank for the loan taken and due to this reason it is necessary to ensure well in

advance regarding the source which can be considered for satisfying financial needs of business.

TASK 2: UNDERSTADING IMPLICATIONS OF FINANCE AS A RESOURCE

SCENARIO 1

2.1 Cost of different sources of finance

In order to select the most appropriate source of finance it is necessary for management to

identify its cost as through this organization can easily utilize its financial resources in effective

manner. Further, cost of considering bank loan as a source of finance is payment of interest which

business enterprise has to pay in large amount in the form of interest for the amount obtained. So,

this increases expenditure level of the firm as management has to bear this cost. At the time when

any business obtains loan from bank then management has to bear interest cost on the same and it

has to be paid on monthly basis (Montier, 2010). Due to presence of this type of cost, expenditure

8

techniques are adopted so as to manage funds of the business in effective manner. Main advantage

of using cash management techniques to business is that it supports in dealing with the situation of

inadequacy of funds and enhances overall performance of firm in the market. Through proper cash

management liquidity position of company can be improved to an extent and it can provide base to

business enterprise in every possible manner.

M2: Appropriate source of finance for small business

For small business enterprise taking bank loan is one of the most appropriate source of

finance as through this organization can enhance its liquidity position. Generally businesses

operating on smaller platform have weak financial position and in such condition it is preferable to

take loan from financial institutions at a cheaper rate of interest. This source is considered as best

for company as through this management can easily satisfy its financial requirement and in turn

situation such as inadequacy of funds can be easily avoided. But on the other hand, it can increase

expenditure level of business as company has to pay interest to bank for the amount obtained. Apart

from this savings of small businesses are not adequate due to which it is not possible to implement

financial decisions by using retained earnings as source of finance (Dittenhofer, 2001). Therefore, in

this way taking loan from financial institution is appropriate for small business and can assist in

implementing the financial plan. On the other hand, before considering any source of finance it is

necessary for management to consider its pros and cons so that source considered may not

adversely affect business enterprise. Sometime it can be possible that organization is not able to pay

the interest amount to bank for the loan taken and due to this reason it is necessary to ensure well in

advance regarding the source which can be considered for satisfying financial needs of business.

TASK 2: UNDERSTADING IMPLICATIONS OF FINANCE AS A RESOURCE

SCENARIO 1

2.1 Cost of different sources of finance

In order to select the most appropriate source of finance it is necessary for management to

identify its cost as through this organization can easily utilize its financial resources in effective

manner. Further, cost of considering bank loan as a source of finance is payment of interest which

business enterprise has to pay in large amount in the form of interest for the amount obtained. So,

this increases expenditure level of the firm as management has to bear this cost. At the time when

any business obtains loan from bank then management has to bear interest cost on the same and it

has to be paid on monthly basis (Montier, 2010). Due to presence of this type of cost, expenditure

8

level of business enhances and in turn, overall cost increases. Moreover, in case when shares are

issued by company in the market then major cost is linked with payment of dividend to its investors

(James, Leavel and Mainam, 2002). Dividend cost also enhances expenditure level of the

organization where it is necessary to provide dividend to the investors. Further, it is a well known

fact that every shareholder expects some sort of return and for every business, it is necessary to

satisfy such need. For satisfying financial needs of business, each and every source is beneficial but

it is necessary to determine well in advance the actual cost of sources of finance. On the other hand,

when retained earnings are considered as a source of finance then company has to bear opportunity

cost as firm uses opportunity of investing in one profitable project. Opportunity cost is regarded as

the loss of other alternatives when one alternative is being chosen by business. Therefore, this cost

has to be beard by business in case when one project is selected and other one is rejected.

2.2 Importance of financial planning

Financial planning plays most important role in organization as through this it becomes easy

for business enterprise to utilize financial resources in efficient manner. Further, for local businesses

financial planning is must as through this it is possible for business to remove instability along with

uncertainty associated with the organization (Montier, 2010). Moreover, planning is directly linked

with estimation of funds required for conducting business operations and building various policies

which are associated with the financial operations of the entity. It also assist in policy formation,

setting of objectives, budget and other type of procedure through which financial operations of the

organization can be carried out in effective manner. Apart from this, for local businesses it is must

for management to determine the basic difference in outflow and inflow of cash in order to know

financial stability of enterprise. Further, business can obtain idea regarding its overall performance

in the market through proper financial planning. Thus, proper financial planning is must for

business and it supports in accomplishment of long term goals along with objectives (Siano,

Kitchen and Confetto, 2010).

Through presence of appropriate financial planning, it is possible for the organization to

invest funds in right project as comparison can be done in between different projects and this

directly increases the business efficiency (Mohsin, 2013). Further, it supports in operational

activities where success along with the failure of production and distribution relies on financial

decisions taken. In short, through proper planning, it is possible to indulge into the key activities

which supports in optimum utilization of finance and assist in coordination. Further, it is possible

for business to link present with the future and provide base to company in accomplishment of long

term goals and objectives.

9

issued by company in the market then major cost is linked with payment of dividend to its investors

(James, Leavel and Mainam, 2002). Dividend cost also enhances expenditure level of the

organization where it is necessary to provide dividend to the investors. Further, it is a well known

fact that every shareholder expects some sort of return and for every business, it is necessary to

satisfy such need. For satisfying financial needs of business, each and every source is beneficial but

it is necessary to determine well in advance the actual cost of sources of finance. On the other hand,

when retained earnings are considered as a source of finance then company has to bear opportunity

cost as firm uses opportunity of investing in one profitable project. Opportunity cost is regarded as

the loss of other alternatives when one alternative is being chosen by business. Therefore, this cost

has to be beard by business in case when one project is selected and other one is rejected.

2.2 Importance of financial planning

Financial planning plays most important role in organization as through this it becomes easy

for business enterprise to utilize financial resources in efficient manner. Further, for local businesses

financial planning is must as through this it is possible for business to remove instability along with

uncertainty associated with the organization (Montier, 2010). Moreover, planning is directly linked

with estimation of funds required for conducting business operations and building various policies

which are associated with the financial operations of the entity. It also assist in policy formation,

setting of objectives, budget and other type of procedure through which financial operations of the

organization can be carried out in effective manner. Apart from this, for local businesses it is must

for management to determine the basic difference in outflow and inflow of cash in order to know

financial stability of enterprise. Further, business can obtain idea regarding its overall performance

in the market through proper financial planning. Thus, proper financial planning is must for

business and it supports in accomplishment of long term goals along with objectives (Siano,

Kitchen and Confetto, 2010).

Through presence of appropriate financial planning, it is possible for the organization to

invest funds in right project as comparison can be done in between different projects and this

directly increases the business efficiency (Mohsin, 2013). Further, it supports in operational

activities where success along with the failure of production and distribution relies on financial

decisions taken. In short, through proper planning, it is possible to indulge into the key activities

which supports in optimum utilization of finance and assist in coordination. Further, it is possible

for business to link present with the future and provide base to company in accomplishment of long

term goals and objectives.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.3 Types of information required for decision making

Different type of information is required by financial department of organization and these

assist managers in taking appropriate decisions. Further, different type of financial statements is

prepared such as profit and loss account, income statement, balance sheet etc. Through all these

statements crucial information can be obtained easily linked with assets and liabilities of the

business enterprise (Mumford, Schultz and Osburn, 2001). Further, information linked with sale and

purchase supports in preparing different type of trading accounts with potential customers and

supplies. Information linked with payment of wages and purchasing assets is also provided. Further,

presence of appropriate financial information supports organization in taking different type of

decisions which are associated with enhancing profitability level, investing in new project, reducing

overall cost, selecting source of finance etc. On the other hand past record present linked with

financial performance assist in enhancing current performance. Moreover, budgets are analysed so

as to know the major difference in actual and expected results.

Management of the organization requires information regarding financial position of

enterprise on the basis of which it can be known whether business is performing up to the mark or

not. On the basis of profitability information, expansion decision is taken and it assists organization

in carrying out overall operations in an effective manner (Mumford, Schultz and Osburn, 2001).

Further, shareholders of business require information regarding liquidity and profitability position

of business through which it is possible to know the capability of organization in providing

dividend to them on time and as per their requirement. Moreover, suppliers of business require

information regarding profitability on the basis of which they can take decision whether to supply

them goods as per their requirement or not.

10

Different type of information is required by financial department of organization and these

assist managers in taking appropriate decisions. Further, different type of financial statements is

prepared such as profit and loss account, income statement, balance sheet etc. Through all these

statements crucial information can be obtained easily linked with assets and liabilities of the

business enterprise (Mumford, Schultz and Osburn, 2001). Further, information linked with sale and

purchase supports in preparing different type of trading accounts with potential customers and

supplies. Information linked with payment of wages and purchasing assets is also provided. Further,

presence of appropriate financial information supports organization in taking different type of

decisions which are associated with enhancing profitability level, investing in new project, reducing

overall cost, selecting source of finance etc. On the other hand past record present linked with

financial performance assist in enhancing current performance. Moreover, budgets are analysed so

as to know the major difference in actual and expected results.

Management of the organization requires information regarding financial position of

enterprise on the basis of which it can be known whether business is performing up to the mark or

not. On the basis of profitability information, expansion decision is taken and it assists organization

in carrying out overall operations in an effective manner (Mumford, Schultz and Osburn, 2001).

Further, shareholders of business require information regarding liquidity and profitability position

of business through which it is possible to know the capability of organization in providing

dividend to them on time and as per their requirement. Moreover, suppliers of business require

information regarding profitability on the basis of which they can take decision whether to supply

them goods as per their requirement or not.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

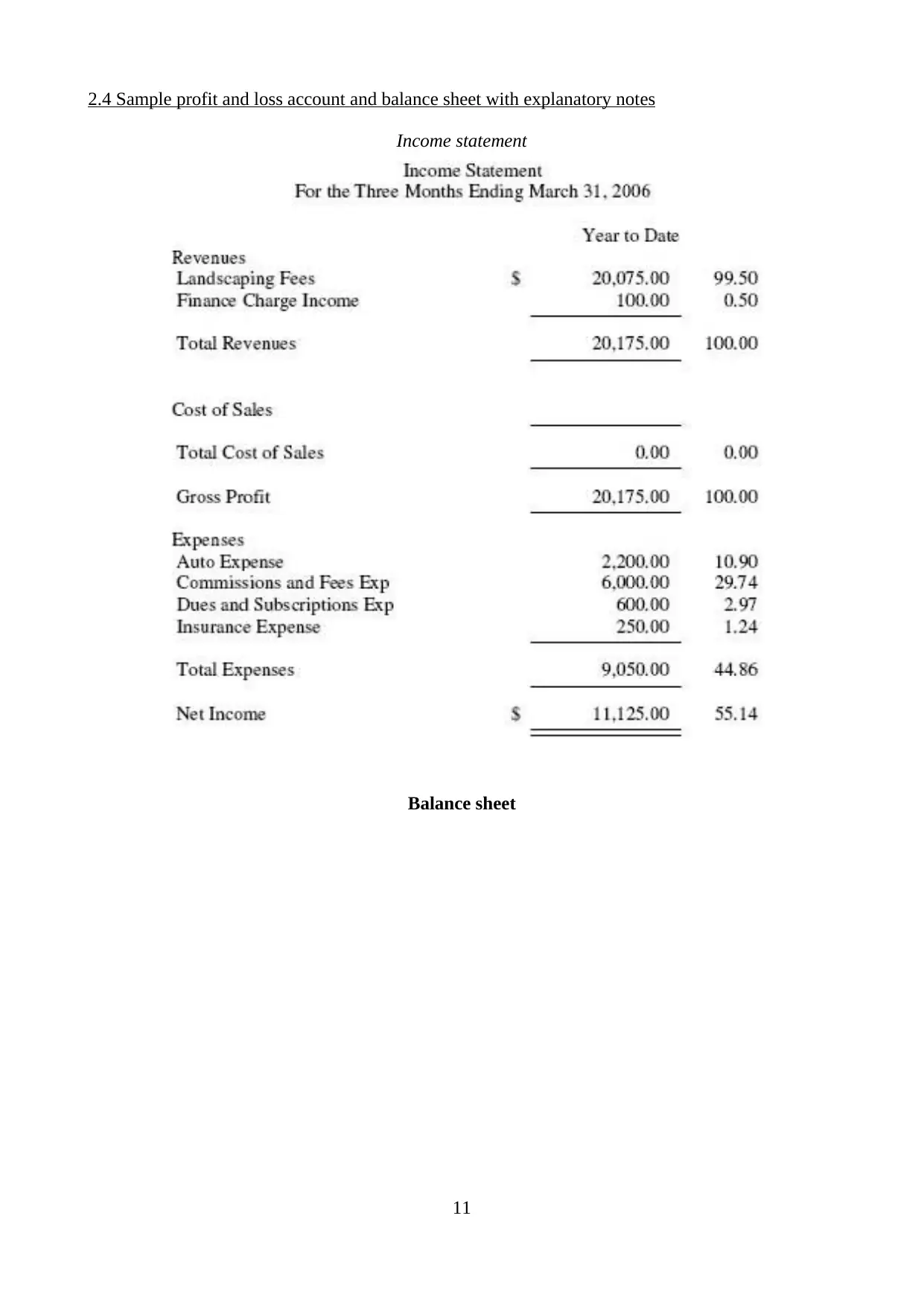

2.4 Sample profit and loss account and balance sheet with explanatory notes

Income statement

Balance sheet

11

Income statement

Balance sheet

11

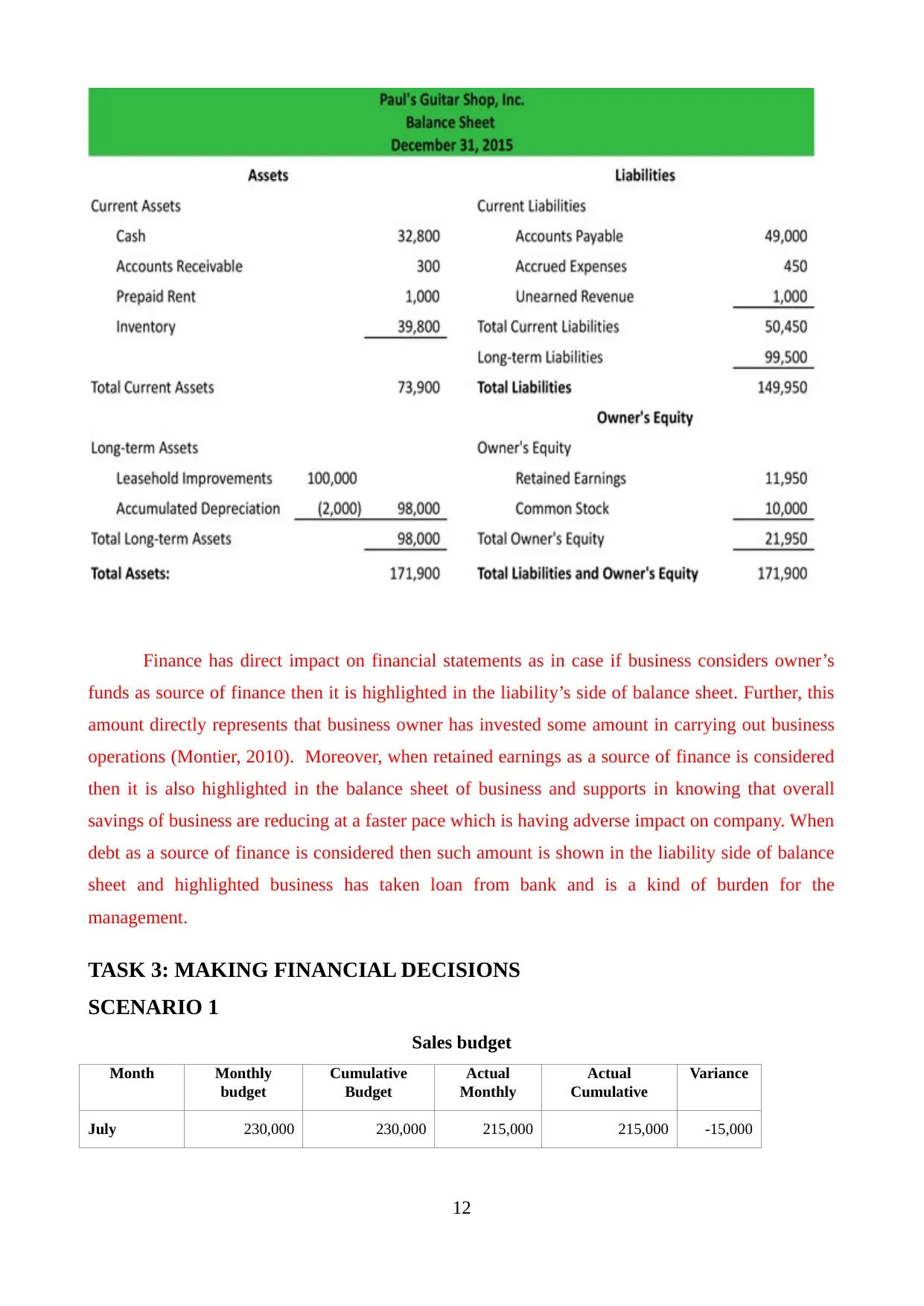

Finance has direct impact on financial statements as in case if business considers owner’s

funds as source of finance then it is highlighted in the liability’s side of balance sheet. Further, this

amount directly represents that business owner has invested some amount in carrying out business

operations (Montier, 2010). Moreover, when retained earnings as a source of finance is considered

then it is also highlighted in the balance sheet of business and supports in knowing that overall

savings of business are reducing at a faster pace which is having adverse impact on company. When

debt as a source of finance is considered then such amount is shown in the liability side of balance

sheet and highlighted business has taken loan from bank and is a kind of burden for the

management.

TASK 3: MAKING FINANCIAL DECISIONS

SCENARIO 1

Sales budget

Month Monthly

budget

Cumulative

Budget

Actual

Monthly

Actual

Cumulative

Variance

July 230,000 230,000 215,000 215,000 -15,000

12

funds as source of finance then it is highlighted in the liability’s side of balance sheet. Further, this

amount directly represents that business owner has invested some amount in carrying out business

operations (Montier, 2010). Moreover, when retained earnings as a source of finance is considered

then it is also highlighted in the balance sheet of business and supports in knowing that overall

savings of business are reducing at a faster pace which is having adverse impact on company. When

debt as a source of finance is considered then such amount is shown in the liability side of balance

sheet and highlighted business has taken loan from bank and is a kind of burden for the

management.

TASK 3: MAKING FINANCIAL DECISIONS

SCENARIO 1

Sales budget

Month Monthly

budget

Cumulative

Budget

Actual

Monthly

Actual

Cumulative

Variance

July 230,000 230,000 215,000 215,000 -15,000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.