Financial Planning and Decision Making for Sweet Menu Restaurant

VerifiedAdded on 2020/01/07

|16

|3955

|160

Report

AI Summary

This report provides a comprehensive analysis of financial resources and decision-making processes, focusing on the Sweet Menu restaurant and comparing it to the Blue Island restaurant. It begins by identifying and evaluating various sources of finance, including internal and external options such as sale of assets, retained profit, bank loans, and the issue of shares, along with their implications, costs, and suitability for the restaurant. The report also emphasizes the importance of financial planning and the information needs of different decision-makers, such as shareholders, employees, managers, government, and suppliers. A detailed analysis of the cash budget for Blue Island restaurant is presented to assess its financial position and cash flow management. Furthermore, the report includes a calculation of unit costs, an evaluation of the viability of different proposals, and a comparative analysis of financial statements, including ratio calculations, to determine the financial health of both companies. The report concludes with recommendations for improved financial management and decision-making.

MANAGING FINANCIAL

RESOURCES AND DECISION

RESOURCES AND DECISION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MANAGING FINANCIAL RESOURCES AND DECISION ......................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance ................................................................................................................1

1.2 Implication of sources of finance..........................................................................................2

1.3 Suitable sources of finance for Sweet Menu restaurant........................................................3

TASK 2............................................................................................................................................3

2.1 Cost of sources of finance.....................................................................................................3

2.2 Importance of financial planning to Sweet Menu restaurant................................................4

2.3 Information need by different decision maker......................................................................4

2.4 Impact of sources of finance on financial statements...........................................................5

TASK 3............................................................................................................................................6

3.1 Analyses of cash budget and necessary decisions.................................................................6

3.2 Calculation of Unit cost........................................................................................................6

3.3 Viability of two proposal .....................................................................................................8

TASK 4............................................................................................................................................9

4.1 Financial statements..............................................................................................................9

4.2 Financial statements prepared by different organisation....................................................10

4.3 Analyse of financial statements by calculating various ratios............................................10

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................13

MANAGING FINANCIAL RESOURCES AND DECISION ......................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance ................................................................................................................1

1.2 Implication of sources of finance..........................................................................................2

1.3 Suitable sources of finance for Sweet Menu restaurant........................................................3

TASK 2............................................................................................................................................3

2.1 Cost of sources of finance.....................................................................................................3

2.2 Importance of financial planning to Sweet Menu restaurant................................................4

2.3 Information need by different decision maker......................................................................4

2.4 Impact of sources of finance on financial statements...........................................................5

TASK 3............................................................................................................................................6

3.1 Analyses of cash budget and necessary decisions.................................................................6

3.2 Calculation of Unit cost........................................................................................................6

3.3 Viability of two proposal .....................................................................................................8

TASK 4............................................................................................................................................9

4.1 Financial statements..............................................................................................................9

4.2 Financial statements prepared by different organisation....................................................10

4.3 Analyse of financial statements by calculating various ratios............................................10

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................13

INTRODUCTION

Finance is the branch of economic that is mainly concerned the management, allocation

of resources and capital (Barnes and Pancost, 2010). Management of finance help the company

in maintaining a balance between inflow and outflow of cash that takes place within and outside

the business organisation. Moreover, in the following report two restaurant have been considered

(i.e Sweet Menu which is suited in Gants Hill of East London and the other is Blue Island

restaurant whose financial position has been compared).

In this report, various sources of finance has been identified for Sweet Menu restaurant

along with its implication. In addition to this, the cost that will be incurred by the company at the

time of using various sources. Along with this importance of financial planning of Sweet Menu

has also been discussed. In the following report, cash budget of Blue Island restaurant has been

analysed in order to find out its flow of cash. In addition, viability of the proposal given is

identified by using investment appraisal techniques. At last financial statements of both the

companies are analysed in order to conclude its financial position.

TASK 1

1.1 Sources of finance

INTERNAL SOURCES OF FINANCE

Sale of assets This is one of the beneficial method that can be used by Sweet Menu in order

to raise its capital. By using this method, restaurant will be raising funds by

selling out the old and obsolescent assets that is of no use.

Retained profit It is a part of profit that is kept by the company out of the revenue earned at

the end of the financial year. Retained profit is kept by the restaurant in order

overcome certain contingencies (Bhowmik and Saha, 2013).

EXTERNAL SOURCES OF FINANCE

Bank loan This can be said as one of the simplest method that can be used by Sweet

Menu in order to raise its capital. By using this method, company can

borrow funds from the bank for a predetermined time period by submitting

the collateral security.

Issue of shares This is another way through which Sweet Menu restaurant can raise large

1

Finance is the branch of economic that is mainly concerned the management, allocation

of resources and capital (Barnes and Pancost, 2010). Management of finance help the company

in maintaining a balance between inflow and outflow of cash that takes place within and outside

the business organisation. Moreover, in the following report two restaurant have been considered

(i.e Sweet Menu which is suited in Gants Hill of East London and the other is Blue Island

restaurant whose financial position has been compared).

In this report, various sources of finance has been identified for Sweet Menu restaurant

along with its implication. In addition to this, the cost that will be incurred by the company at the

time of using various sources. Along with this importance of financial planning of Sweet Menu

has also been discussed. In the following report, cash budget of Blue Island restaurant has been

analysed in order to find out its flow of cash. In addition, viability of the proposal given is

identified by using investment appraisal techniques. At last financial statements of both the

companies are analysed in order to conclude its financial position.

TASK 1

1.1 Sources of finance

INTERNAL SOURCES OF FINANCE

Sale of assets This is one of the beneficial method that can be used by Sweet Menu in order

to raise its capital. By using this method, restaurant will be raising funds by

selling out the old and obsolescent assets that is of no use.

Retained profit It is a part of profit that is kept by the company out of the revenue earned at

the end of the financial year. Retained profit is kept by the restaurant in order

overcome certain contingencies (Bhowmik and Saha, 2013).

EXTERNAL SOURCES OF FINANCE

Bank loan This can be said as one of the simplest method that can be used by Sweet

Menu in order to raise its capital. By using this method, company can

borrow funds from the bank for a predetermined time period by submitting

the collateral security.

Issue of shares This is another way through which Sweet Menu restaurant can raise large

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount of capital within a short period of time. In this method, firm issue

shares to the general public and collect funds from them which they may not

require to pay back.

1.2 Implication of sources of finance

Sources Legal aspects Cost Suitability

Sale of assets Sweet menu restaurant

is required to take

legal procedure into

consideration at the

time of selling assets.

By using this method,

Sweet Menu can be

able to meet its

financial needs but at

the same time assets of

the company will also

decrease.

This method is suitable

for meeting short term

requirements. Because

business is required to

follow a set limit by

the board of directors

in regard to the sale of

assets.

Retained profit As the law, every

organisation is

required to keep

certain amount of

profit as a reserves

with them. In lieu of

which Sweet menu

restaurant will be able

to overcome

uncertainty.

By using this source

Sweet Menu will be

able to meet its

financial needs at that

particular time

(Brigham and Daves,

2012). But afterwards

they may not be able

to overcome

uncertainty that can

occur in future.

This source is suitable

for the Sweet Menu

restaurant in order to

overcome uncertainty.

In addition, this

method can also be

used by the company

to expand its business

unit.

Bank loan If Sweet Menu is not

able to repay the

amount of loan taken

by them from bank

than in that case bank

Debt of the company

may increase if they

move on with this

method because

company is required to

This method is suitable

for expanding the

business units.

2

shares to the general public and collect funds from them which they may not

require to pay back.

1.2 Implication of sources of finance

Sources Legal aspects Cost Suitability

Sale of assets Sweet menu restaurant

is required to take

legal procedure into

consideration at the

time of selling assets.

By using this method,

Sweet Menu can be

able to meet its

financial needs but at

the same time assets of

the company will also

decrease.

This method is suitable

for meeting short term

requirements. Because

business is required to

follow a set limit by

the board of directors

in regard to the sale of

assets.

Retained profit As the law, every

organisation is

required to keep

certain amount of

profit as a reserves

with them. In lieu of

which Sweet menu

restaurant will be able

to overcome

uncertainty.

By using this source

Sweet Menu will be

able to meet its

financial needs at that

particular time

(Brigham and Daves,

2012). But afterwards

they may not be able

to overcome

uncertainty that can

occur in future.

This source is suitable

for the Sweet Menu

restaurant in order to

overcome uncertainty.

In addition, this

method can also be

used by the company

to expand its business

unit.

Bank loan If Sweet Menu is not

able to repay the

amount of loan taken

by them from bank

than in that case bank

Debt of the company

may increase if they

move on with this

method because

company is required to

This method is suitable

for expanding the

business units.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

has the right to cease

the assets of the

company.

pay high interest rate

to bank.

Issue of shares If company issues the

shares then they are

required to give voting

rights to the

shareholders. In

addition to this

company is also

required to pay

dividend.

Sweet Menu restaurant

is required to pay

dividend to the

individual to whom

they have issued the

shares.

This is also one of the

best method that can

be used by the

company in order to

start up a new business

or to expand it.

1.3 Suitable sources of finance for Sweet Menu restaurant

In accordance to the above implication it can be suggested that Sweet Menu

restaurant should move onto Bank loan, As it is one of the best methods that can be used by the

Sweet Menu to expand the business bank are always ready to provide loan to the companies in

order to meet their financial requirement (Cetorelli and Strahan, 2006). Bank charges, rate of

interest on the loan given by them but the amount of interest is less as compared to any other

financial institutions.

By using this source Sweet Menu is able to avail tax benefits. In addition to this,

restaurant is not required to repay the whole amount of loan at a time, they can repay it as per

there requirement. Payment in instalment reduces the financial burden of the business.

TASK 2

2.1 Cost of sources of finance

Sweet Menu restaurant has taken into consideration the two source to expand its business.

They have preferred to use bank loan and retained profit as sources to raise their finance level.

But in order avail these sources, corporation is required to bear financial and opportunities cost.

Both these cost creates an impact on profitability and growth of the company.

3

the assets of the

company.

pay high interest rate

to bank.

Issue of shares If company issues the

shares then they are

required to give voting

rights to the

shareholders. In

addition to this

company is also

required to pay

dividend.

Sweet Menu restaurant

is required to pay

dividend to the

individual to whom

they have issued the

shares.

This is also one of the

best method that can

be used by the

company in order to

start up a new business

or to expand it.

1.3 Suitable sources of finance for Sweet Menu restaurant

In accordance to the above implication it can be suggested that Sweet Menu

restaurant should move onto Bank loan, As it is one of the best methods that can be used by the

Sweet Menu to expand the business bank are always ready to provide loan to the companies in

order to meet their financial requirement (Cetorelli and Strahan, 2006). Bank charges, rate of

interest on the loan given by them but the amount of interest is less as compared to any other

financial institutions.

By using this source Sweet Menu is able to avail tax benefits. In addition to this,

restaurant is not required to repay the whole amount of loan at a time, they can repay it as per

there requirement. Payment in instalment reduces the financial burden of the business.

TASK 2

2.1 Cost of sources of finance

Sweet Menu restaurant has taken into consideration the two source to expand its business.

They have preferred to use bank loan and retained profit as sources to raise their finance level.

But in order avail these sources, corporation is required to bear financial and opportunities cost.

Both these cost creates an impact on profitability and growth of the company.

3

Opportunities cost: - Opportunity cost is the cost that needs to be incurred by the

company at the time of selection of one best alternative against another (Chandra, 2011). For

instance, if they move on retained profit than in this case company may not be able to pay

dividend to its shareholder at the time of loss. In addition to this, Sweet Menu restaurant may not

be able to overcome any of its uncertainties that can occur in future.

Financial cost: - Bank and other financial institution changes high rate of interest on the

funds given by them in order to increase its financial assistance. This in turn reduces the

financial cost of the company. Along with interest, Sweet Menu is also required to repay the

amount of money borrowed by them. Moreover, this affects the liquidity and profitability ratio of

the firm.

2.2 Importance of financial planning to Sweet Menu restaurant

Financial planning is the activity which assist Sweet Menu restaurant to make various

necessary decisions in order to generate more profit and move the business towards growth.

Some of the importance of financial plannings are listed below:-

Financial planning of all the activities in advance help the Sweet Menu restaurant to

utilize the available resources upto full extend. Wastage of resources can also reduce.

This in turn will help to avoid the condition of surplus and deficits (Dontoh, Ronen and

Sarath, 2008).Economic planning in advance will assist the Sweet menu to anticipate its

future sales and growth. In addition to this, business entity will be able to forecast its

financial requirement that can occurs in future.

Planning of all the activities in advance will aid the Sweet menu to properly coordinate

all the activities that are taking place within an organisation. In lieu of this company will

be have the deeper knowledge of the funds that are required by each and every

department.

2.3 Information need by different decision maker

Shareholders: - Shareholder are the one who invest in the company with an aim of

generating high rate of return on investment. These shareholder prefer financial statements of the

company in order to determine whether they should spend their saving in the business or not

(Eccles and Holt, 2005).

4

company at the time of selection of one best alternative against another (Chandra, 2011). For

instance, if they move on retained profit than in this case company may not be able to pay

dividend to its shareholder at the time of loss. In addition to this, Sweet Menu restaurant may not

be able to overcome any of its uncertainties that can occur in future.

Financial cost: - Bank and other financial institution changes high rate of interest on the

funds given by them in order to increase its financial assistance. This in turn reduces the

financial cost of the company. Along with interest, Sweet Menu is also required to repay the

amount of money borrowed by them. Moreover, this affects the liquidity and profitability ratio of

the firm.

2.2 Importance of financial planning to Sweet Menu restaurant

Financial planning is the activity which assist Sweet Menu restaurant to make various

necessary decisions in order to generate more profit and move the business towards growth.

Some of the importance of financial plannings are listed below:-

Financial planning of all the activities in advance help the Sweet Menu restaurant to

utilize the available resources upto full extend. Wastage of resources can also reduce.

This in turn will help to avoid the condition of surplus and deficits (Dontoh, Ronen and

Sarath, 2008).Economic planning in advance will assist the Sweet menu to anticipate its

future sales and growth. In addition to this, business entity will be able to forecast its

financial requirement that can occurs in future.

Planning of all the activities in advance will aid the Sweet menu to properly coordinate

all the activities that are taking place within an organisation. In lieu of this company will

be have the deeper knowledge of the funds that are required by each and every

department.

2.3 Information need by different decision maker

Shareholders: - Shareholder are the one who invest in the company with an aim of

generating high rate of return on investment. These shareholder prefer financial statements of the

company in order to determine whether they should spend their saving in the business or not

(Eccles and Holt, 2005).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employees: - Employees are the one who work for the betterment of the company. They

only want that the firm should pay them fair wages. In lieu of this, prefer to see the income

statements of the company.

Manager: - Managers works for the development of the company (Vitez, 2014). They

take into consideration all the financial statements in order to develop various strategies for the

growth of the enterprise.

Government: - They are the one who work for the welfare and betterment of the society.

They prefer financial statements in order to analyse the economic position of the company and to

calculate the amount of tax needed to be paid bythem.

Suppliers: - They are the one who supply raw material to the firm. They simply want that

company should make payment to them on time of the goods supplied by them. In lieu of this,

they opt to see the income statements and balance sheet of the business.

2.4 Impact of sources of finance on financial statements

Sale of assets: - Entry of sale of assets will be made at the assets side of the balance sheet

and the same amount will be deducted from particular asset (Hursti and Maula, 2007). In

addition to this entry of profit earned or loss suffered by the company at the time of selling the

asset, will be recorded in profit and loss account.

Retained profit: - Entry of reserve kept by the company as retained profit which will be

made on equity side of the balance sheet under the head of share capital.

Bank loan: - Entry of bank loan will be made under the head of current liability in

balance sheet. Because bank loan is debt for the company. In addition to this interest paid by

them against the bank loan will be recorded at debit side of income statement.

Issue of shares: - Entry of issuing equity shares will be made under the head of share

capital in balance sheet (Sabău, 2013). Along with this entry of dividend paid to the shareholders

will be recorded at debit side of the income statement.

TASK 3

3.1 Analyses of cash budget and necessary decisions

5

only want that the firm should pay them fair wages. In lieu of this, prefer to see the income

statements of the company.

Manager: - Managers works for the development of the company (Vitez, 2014). They

take into consideration all the financial statements in order to develop various strategies for the

growth of the enterprise.

Government: - They are the one who work for the welfare and betterment of the society.

They prefer financial statements in order to analyse the economic position of the company and to

calculate the amount of tax needed to be paid bythem.

Suppliers: - They are the one who supply raw material to the firm. They simply want that

company should make payment to them on time of the goods supplied by them. In lieu of this,

they opt to see the income statements and balance sheet of the business.

2.4 Impact of sources of finance on financial statements

Sale of assets: - Entry of sale of assets will be made at the assets side of the balance sheet

and the same amount will be deducted from particular asset (Hursti and Maula, 2007). In

addition to this entry of profit earned or loss suffered by the company at the time of selling the

asset, will be recorded in profit and loss account.

Retained profit: - Entry of reserve kept by the company as retained profit which will be

made on equity side of the balance sheet under the head of share capital.

Bank loan: - Entry of bank loan will be made under the head of current liability in

balance sheet. Because bank loan is debt for the company. In addition to this interest paid by

them against the bank loan will be recorded at debit side of income statement.

Issue of shares: - Entry of issuing equity shares will be made under the head of share

capital in balance sheet (Sabău, 2013). Along with this entry of dividend paid to the shareholders

will be recorded at debit side of the income statement.

TASK 3

3.1 Analyses of cash budget and necessary decisions

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

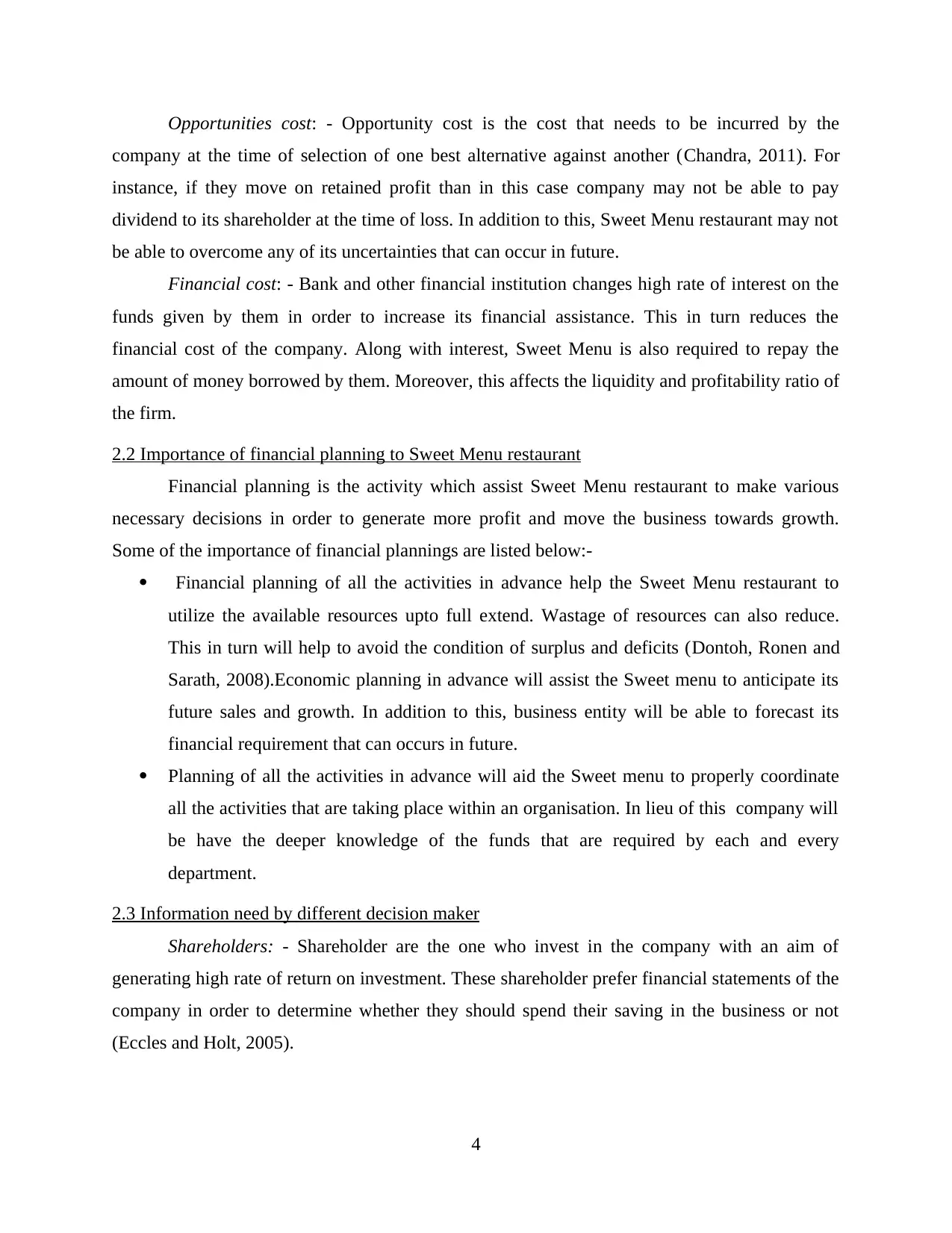

From the following analysis it can be concluded that financial position of Blue Island

restaurant is not good. Its flow of cash is constantly changing. It is seen that in the month of

September and December expenses made by the company were more than its income earned.

Firm income for both the months was 15000 and 20000 respectively while on the other hand

expenses made by the company were 40850 and 24280 which is almost double to that of the

income earned. Likewise, income earned by the business in the month October and November

was 15500 and 18000 respectively which is more than the expenses made by them. Its

expenditures for this month is 11630 and 13230 respectively.

This in turn point out that Blue Island is not able to negotiate its financial resources

properly. The main cause behind this could be that company is able to prepare various strategies

in order to maintain a balance between flows of cash. Therefore, at last it is suggested that in

order to overcome this problem, company should develop various strategies in an effective

manner.

3.2 Calculation of Unit cost

Unit cost is per unit cost of the product that is incurred by the company at the time of

manufacturing (Mayer, Schoors and Yafeh, 2005).

Calculation of unit cost is as follows:-

6

Illustration 1: chart showing the inflow and outflow of cash

restaurant is not good. Its flow of cash is constantly changing. It is seen that in the month of

September and December expenses made by the company were more than its income earned.

Firm income for both the months was 15000 and 20000 respectively while on the other hand

expenses made by the company were 40850 and 24280 which is almost double to that of the

income earned. Likewise, income earned by the business in the month October and November

was 15500 and 18000 respectively which is more than the expenses made by them. Its

expenditures for this month is 11630 and 13230 respectively.

This in turn point out that Blue Island is not able to negotiate its financial resources

properly. The main cause behind this could be that company is able to prepare various strategies

in order to maintain a balance between flows of cash. Therefore, at last it is suggested that in

order to overcome this problem, company should develop various strategies in an effective

manner.

3.2 Calculation of Unit cost

Unit cost is per unit cost of the product that is incurred by the company at the time of

manufacturing (Mayer, Schoors and Yafeh, 2005).

Calculation of unit cost is as follows:-

6

Illustration 1: chart showing the inflow and outflow of cash

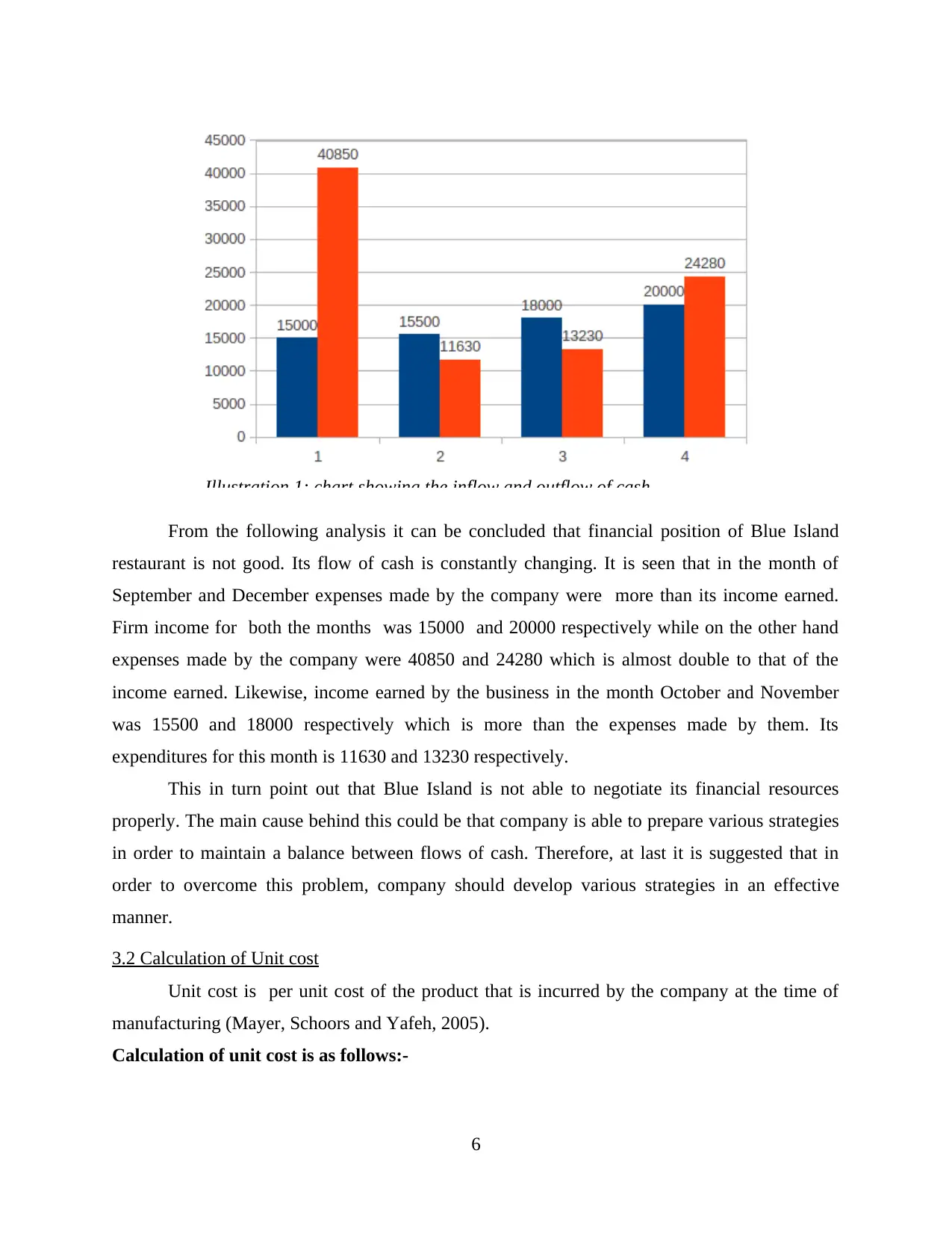

Unit cost = Direct cost per unit +Indirect cost per unitDirect costs or variable cost: streak(s) =

3Vegetables (v) = 1.5 Labour (l) = 3.5

(Total S+V+L = 8)

Indirect cost or fix cost=2 (overhead)

Mark-up =40%

Cost = 100%

Mark up = 40%

Selling price = 140%

Name of Units Costs (In £)

Steak(direct) 3

Vegetables and other ingredients(direct) 1.5

labour(direct) 3.5

Overheads (indirect) 2

Total Costs 10

Mark Up (40%) 4

VAT (20%) 2.8

Price to charge customer 16.8

Currently changing 16

VAT

Price exclusive VAT (Net) = 100%

VAT = 20%

Selling price inclusive (gross) =120%

Food cost percentage= Total costs of ingredients/sales price

Food cost percentage = Total costs of ingredients/Sale prices

Food cost percentage = 10£/16.8 £*100

Food cost percentage = 59.52%

Loss percentage on sales = Loss/sales prices*100

Loss percentage on sales = 6.8£/16.8£*100

7

3Vegetables (v) = 1.5 Labour (l) = 3.5

(Total S+V+L = 8)

Indirect cost or fix cost=2 (overhead)

Mark-up =40%

Cost = 100%

Mark up = 40%

Selling price = 140%

Name of Units Costs (In £)

Steak(direct) 3

Vegetables and other ingredients(direct) 1.5

labour(direct) 3.5

Overheads (indirect) 2

Total Costs 10

Mark Up (40%) 4

VAT (20%) 2.8

Price to charge customer 16.8

Currently changing 16

VAT

Price exclusive VAT (Net) = 100%

VAT = 20%

Selling price inclusive (gross) =120%

Food cost percentage= Total costs of ingredients/sales price

Food cost percentage = Total costs of ingredients/Sale prices

Food cost percentage = 10£/16.8 £*100

Food cost percentage = 59.52%

Loss percentage on sales = Loss/sales prices*100

Loss percentage on sales = 6.8£/16.8£*100

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

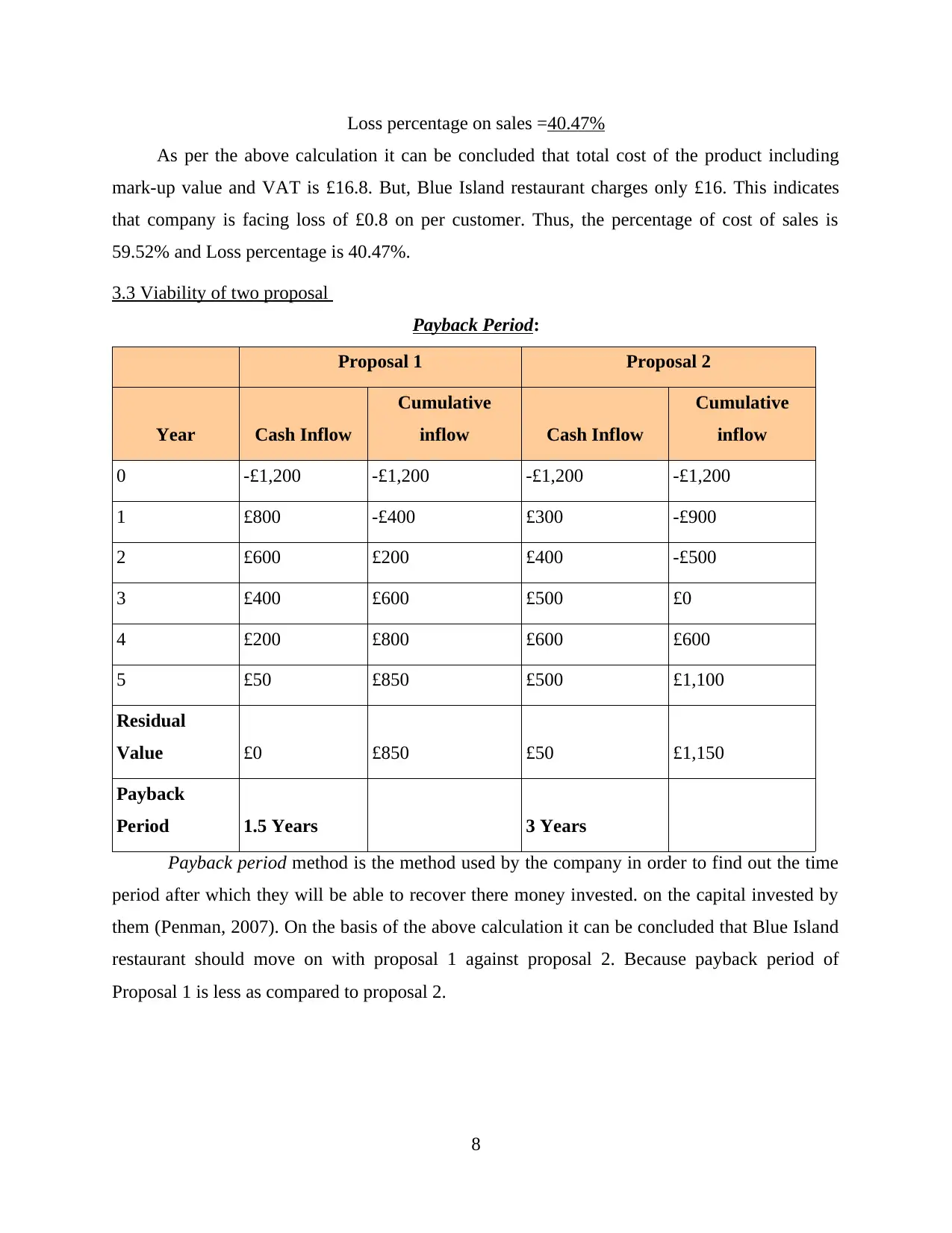

Loss percentage on sales =40.47%

As per the above calculation it can be concluded that total cost of the product including

mark-up value and VAT is £16.8. But, Blue Island restaurant charges only £16. This indicates

that company is facing loss of £0.8 on per customer. Thus, the percentage of cost of sales is

59.52% and Loss percentage is 40.47%.

3.3 Viability of two proposal

Payback Period:

Proposal 1 Proposal 2

Year Cash Inflow

Cumulative

inflow Cash Inflow

Cumulative

inflow

0 -£1,200 -£1,200 -£1,200 -£1,200

1 £800 -£400 £300 -£900

2 £600 £200 £400 -£500

3 £400 £600 £500 £0

4 £200 £800 £600 £600

5 £50 £850 £500 £1,100

Residual

Value £0 £850 £50 £1,150

Payback

Period 1.5 Years 3 Years

Payback period method is the method used by the company in order to find out the time

period after which they will be able to recover there money invested. on the capital invested by

them (Penman, 2007). On the basis of the above calculation it can be concluded that Blue Island

restaurant should move on with proposal 1 against proposal 2. Because payback period of

Proposal 1 is less as compared to proposal 2.

8

As per the above calculation it can be concluded that total cost of the product including

mark-up value and VAT is £16.8. But, Blue Island restaurant charges only £16. This indicates

that company is facing loss of £0.8 on per customer. Thus, the percentage of cost of sales is

59.52% and Loss percentage is 40.47%.

3.3 Viability of two proposal

Payback Period:

Proposal 1 Proposal 2

Year Cash Inflow

Cumulative

inflow Cash Inflow

Cumulative

inflow

0 -£1,200 -£1,200 -£1,200 -£1,200

1 £800 -£400 £300 -£900

2 £600 £200 £400 -£500

3 £400 £600 £500 £0

4 £200 £800 £600 £600

5 £50 £850 £500 £1,100

Residual

Value £0 £850 £50 £1,150

Payback

Period 1.5 Years 3 Years

Payback period method is the method used by the company in order to find out the time

period after which they will be able to recover there money invested. on the capital invested by

them (Penman, 2007). On the basis of the above calculation it can be concluded that Blue Island

restaurant should move on with proposal 1 against proposal 2. Because payback period of

Proposal 1 is less as compared to proposal 2.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

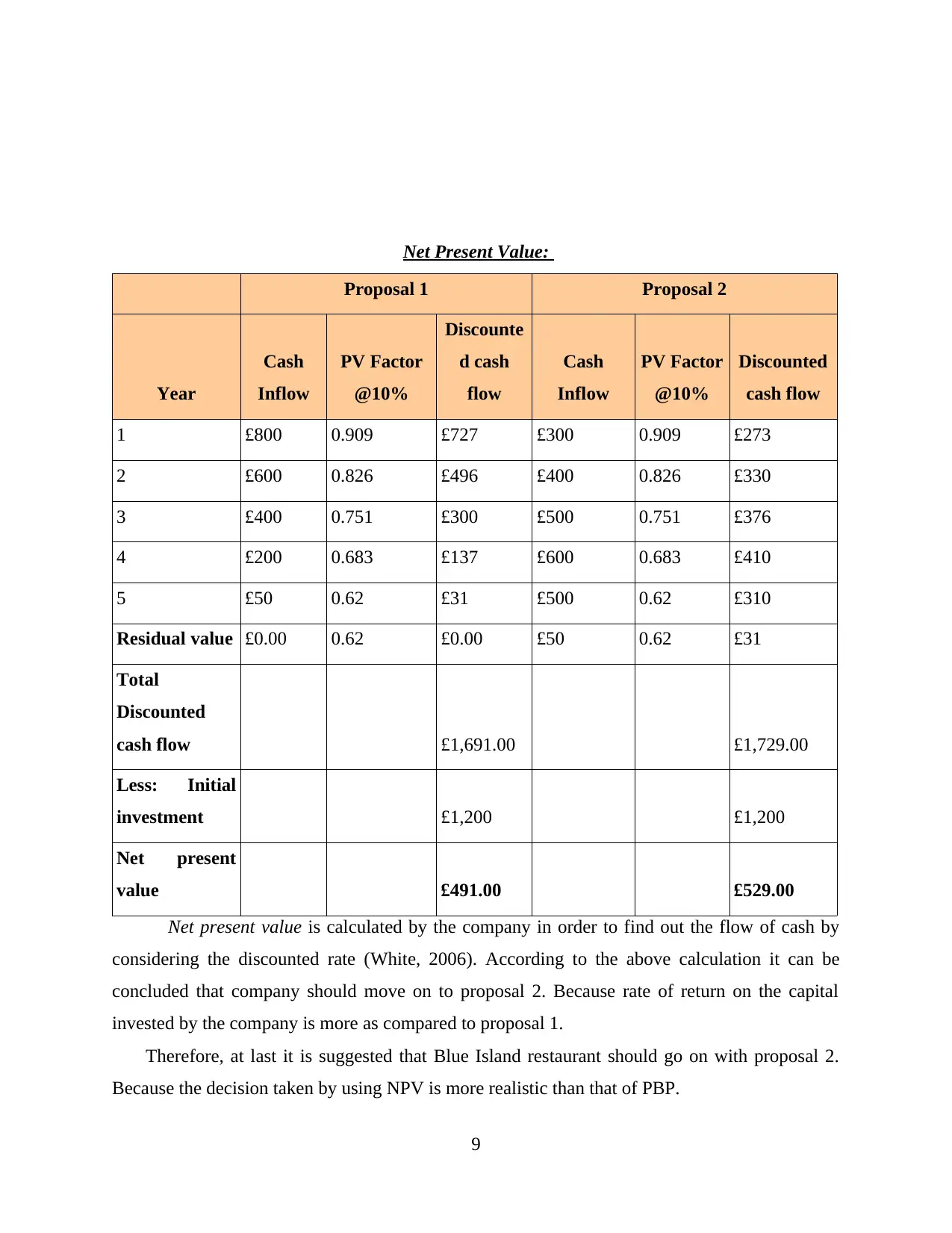

Net Present Value:

Proposal 1 Proposal 2

Year

Cash

Inflow

PV Factor

@10%

Discounte

d cash

flow

Cash

Inflow

PV Factor

@10%

Discounted

cash flow

1 £800 0.909 £727 £300 0.909 £273

2 £600 0.826 £496 £400 0.826 £330

3 £400 0.751 £300 £500 0.751 £376

4 £200 0.683 £137 £600 0.683 £410

5 £50 0.62 £31 £500 0.62 £310

Residual value £0.00 0.62 £0.00 £50 0.62 £31

Total

Discounted

cash flow £1,691.00 £1,729.00

Less: Initial

investment £1,200 £1,200

Net present

value £491.00 £529.00

Net present value is calculated by the company in order to find out the flow of cash by

considering the discounted rate (White, 2006). According to the above calculation it can be

concluded that company should move on to proposal 2. Because rate of return on the capital

invested by the company is more as compared to proposal 1.

Therefore, at last it is suggested that Blue Island restaurant should go on with proposal 2.

Because the decision taken by using NPV is more realistic than that of PBP.

9

Proposal 1 Proposal 2

Year

Cash

Inflow

PV Factor

@10%

Discounte

d cash

flow

Cash

Inflow

PV Factor

@10%

Discounted

cash flow

1 £800 0.909 £727 £300 0.909 £273

2 £600 0.826 £496 £400 0.826 £330

3 £400 0.751 £300 £500 0.751 £376

4 £200 0.683 £137 £600 0.683 £410

5 £50 0.62 £31 £500 0.62 £310

Residual value £0.00 0.62 £0.00 £50 0.62 £31

Total

Discounted

cash flow £1,691.00 £1,729.00

Less: Initial

investment £1,200 £1,200

Net present

value £491.00 £529.00

Net present value is calculated by the company in order to find out the flow of cash by

considering the discounted rate (White, 2006). According to the above calculation it can be

concluded that company should move on to proposal 2. Because rate of return on the capital

invested by the company is more as compared to proposal 1.

Therefore, at last it is suggested that Blue Island restaurant should go on with proposal 2.

Because the decision taken by using NPV is more realistic than that of PBP.

9

TASK 4

4.1 Financial statements

Income statements: - This statement is prepared by the company in order to analyse the

income earned and expenses made by them during thet financial year. It is further divided into

two parts (Peterson and Fabozzi, 2012). One is income side which is also known as credit side

which includes interest earned, dividend received etc. whereas another side is expense side that

contains Salary, rent, interest paid etc.

Balance Sheet: - This is prepared by the company in order to find out its financial

position at the accounting year. In this statements assets and liabilities of the company are

recorded. Assets side includes machinery, furniture, cash etc. and liabilities side comprises of

issue of shares, bank loan etc.

Cash flow statements: - This statement is prepared by the company in order to analyses

its inflow and outflow of cash. It is further divided into three activities (i.e. operating, investing

and financial activity).

4.2 Financial statements prepared by different organisation

Limited company: - Limited company are those which are listed on the stock exchange.

These organisation are required to prepare all financial statements. In addition to this they are

also required to issue there monetary statements to the general public.

Partnership firm: - Partnership firm are the organisations that are formed by making an

agreement between two or more parties at the time of starting new business (Tulsian, 2002).

These organisation are also required to maintain all financial statements. Along with this they are

also required to prepare partner's capital account.

Sole traders: - Sole trader’s organisation is the one which is owned and controlled by

asingle individual. These organisation are simply required to prepare receipt and payment

account in order to analyse the income earned and expenses made by the company during that

financial year.

4.3 Analyse of financial statements by calculating various ratios

Ratios Formula

Sweet Menu

Restaurant

Blue Island

Restaurant

PROFITABILITY RATIO

10

4.1 Financial statements

Income statements: - This statement is prepared by the company in order to analyse the

income earned and expenses made by them during thet financial year. It is further divided into

two parts (Peterson and Fabozzi, 2012). One is income side which is also known as credit side

which includes interest earned, dividend received etc. whereas another side is expense side that

contains Salary, rent, interest paid etc.

Balance Sheet: - This is prepared by the company in order to find out its financial

position at the accounting year. In this statements assets and liabilities of the company are

recorded. Assets side includes machinery, furniture, cash etc. and liabilities side comprises of

issue of shares, bank loan etc.

Cash flow statements: - This statement is prepared by the company in order to analyses

its inflow and outflow of cash. It is further divided into three activities (i.e. operating, investing

and financial activity).

4.2 Financial statements prepared by different organisation

Limited company: - Limited company are those which are listed on the stock exchange.

These organisation are required to prepare all financial statements. In addition to this they are

also required to issue there monetary statements to the general public.

Partnership firm: - Partnership firm are the organisations that are formed by making an

agreement between two or more parties at the time of starting new business (Tulsian, 2002).

These organisation are also required to maintain all financial statements. Along with this they are

also required to prepare partner's capital account.

Sole traders: - Sole trader’s organisation is the one which is owned and controlled by

asingle individual. These organisation are simply required to prepare receipt and payment

account in order to analyse the income earned and expenses made by the company during that

financial year.

4.3 Analyse of financial statements by calculating various ratios

Ratios Formula

Sweet Menu

Restaurant

Blue Island

Restaurant

PROFITABILITY RATIO

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.