Managing Financial Resources: Analysis of WBC Scenarios Report

VerifiedAdded on 2023/01/13

|10

|2699

|66

Report

AI Summary

This report provides an analysis of three business scenarios for Whizz Bang Corporation Ltd (WBC), a manufacturer of spare parts for heavy transport materials. The first scenario addresses capital acquisition, focusing on the replacement of worn-out equipment, emphasizing the need for detailed analysis, supplier selection, and appropriate financing. The second scenario examines a project proposal, including investment calculations using NPV, IRR, and payback methods, discussing their advantages and disadvantages, and recommending the NPV method. It also highlights the importance of considering organizational, social, and environmental factors. The third scenario discusses the Weighted Average Cost of Capital (WACC) for WBC, recommending against its use for project assessment due to its complexity and the preference for a project-focused cost of capital. The report concludes with a summary of the findings and provides recommendations for WBC's financial decision-making.

Managing Financial Resources

Assessment Task Three: Business Finance

Whizz Bang Corporation Ltd (WBC)

Assessment Task Three: Business Finance

Whizz Bang Corporation Ltd (WBC)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

This report discusses three business related scenarios for a company called Whizz Bang Corporation

Ltd (WBC). This company manufactures spare parts for heavy transport materials. It addresses all

three scenarios and analyses the requirements of the business depending on the analysis. The report

explains the necessary requirements of each of the scenarios.

The first scenario discusses the capital acquisition of a worn out equipment at WBC. A staff member

had requested an approval from the manager to replace a worm out equipment. Unfortunately, not

enough information was provided to the Manager, as it was assumed that the request would be

approved. This section describes information that needs to bee considered before replacing the item

due to the equipment being expensive. It is important to understand the reasons behind replacing

the worn out equipment which is discussed in this section.

The second scenario discusses the requirements of a project proposal. The manager has identified a

potential opportunity for the company and is required to understand the financial requirements to

implement the project. This includes the investment calculations of NPV, IRR and payback. It

discusses the advantages and disadvantages of using these investment methodologies and also

recommends which one would be better suited to understand the investment requirements to use

for the assessment of the proposed project. It also explains other factors to consider for assessing

the project proposal.

The third scenario provides information in regards to the Weighted Average Cost of Capital (WACC)

for WBC. This is defined as the company’s weighted average cost of capital which is assessed

depending on the organisation’s financial structure. It explains that this calculation method can

become complicated, which is why it is better not to use this pro the project proposal and

requirements.

The report then provides a conclusion, which gives a good summary and recommendations of the

information discussed in this report.

Table of Contents

1 | P a g e

This report discusses three business related scenarios for a company called Whizz Bang Corporation

Ltd (WBC). This company manufactures spare parts for heavy transport materials. It addresses all

three scenarios and analyses the requirements of the business depending on the analysis. The report

explains the necessary requirements of each of the scenarios.

The first scenario discusses the capital acquisition of a worn out equipment at WBC. A staff member

had requested an approval from the manager to replace a worm out equipment. Unfortunately, not

enough information was provided to the Manager, as it was assumed that the request would be

approved. This section describes information that needs to bee considered before replacing the item

due to the equipment being expensive. It is important to understand the reasons behind replacing

the worn out equipment which is discussed in this section.

The second scenario discusses the requirements of a project proposal. The manager has identified a

potential opportunity for the company and is required to understand the financial requirements to

implement the project. This includes the investment calculations of NPV, IRR and payback. It

discusses the advantages and disadvantages of using these investment methodologies and also

recommends which one would be better suited to understand the investment requirements to use

for the assessment of the proposed project. It also explains other factors to consider for assessing

the project proposal.

The third scenario provides information in regards to the Weighted Average Cost of Capital (WACC)

for WBC. This is defined as the company’s weighted average cost of capital which is assessed

depending on the organisation’s financial structure. It explains that this calculation method can

become complicated, which is why it is better not to use this pro the project proposal and

requirements.

The report then provides a conclusion, which gives a good summary and recommendations of the

information discussed in this report.

Table of Contents

1 | P a g e

Executive summary...............................................................................................................................1

Introduction..........................................................................................................................................3

Discussion.............................................................................................................................................3

Scenario 1: Capital acquisition...........................................................................................................3

Scenario 2: Project Proposal..............................................................................................................4

Scenario 3: Project Financing.............................................................................................................5

Conclusion.............................................................................................................................................6

References............................................................................................................................................7

Appendix 1............................................................................................................................................8

Appendix 2............................................................................................................................................8

Appendix 3............................................................................................................................................9

2 | P a g e

Introduction..........................................................................................................................................3

Discussion.............................................................................................................................................3

Scenario 1: Capital acquisition...........................................................................................................3

Scenario 2: Project Proposal..............................................................................................................4

Scenario 3: Project Financing.............................................................................................................5

Conclusion.............................................................................................................................................6

References............................................................................................................................................7

Appendix 1............................................................................................................................................8

Appendix 2............................................................................................................................................8

Appendix 3............................................................................................................................................9

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report explains three scenarios for an organisation called Whizz Bang Corporation Ltd (WBC).

WBC is a large organisation that specialises in manufacturing spare parts for heavy transport

materials. The report is to be presented to senior management for them to make executive

decisions in regards to all three scenarios that are discussed in detail.

Discussion

Scenario 1: Capital acquisition

Capital acquisition can be defined as a company that is purchasing of capital assets for business

purposes to be used for a log term basis, usually more than 12 months. In this scenario, the capital

asset is identified as a piece of equipment that is required for business operations. Other examples

of capital assets can be inventory, software, machinery, etc.

Capital acquisition of a corporation involves an in depth strategic analysis to confirm the effective

demand of the assets.

In this scenario, WBC is expecting to replace a worn out piece equipment which is understood to be

expensive. A detailed strategic analysis is not required if the cost of the replacement is insignificant

as the cost can be financed by the running capital of the organisation. However, the piece of

equipment that WBC is wanting to replace is considered to be expensive. In this situation, the capital

acquisition is the replacement of the worn out piece of equipment.

WBC should progress the capital acquisition analysis to ensure that the manager and the company is

making a cost effective outcome for the benefit of the business operations.

Requirement identification of the replacement

WBC should first of all consider the reason for the replacement of the worn out piece of equipment.

Detailed analysis is needed to be actioned. The equipment could have been worn out because it was

being used excessively and continuously There needs to be a consideration of the worn out item to

be re-used if it is repaired, taking into account the costs that might be involved in repairing and also

the maintenance the repaired equipment. Another aspect to be considered, is the maintenance cost

if WBC considers re-using the item compared to replacing the item in the long run. It can also be

assumed that if the item is re-used after it is fixed, regular maintenance may be required to ensure

its sustainability. This may become financially expensive to WBC in long term. Therefore, a proper

calculation should be made to understand the costs that would be involved in replacing or repairing

the item.

A proper assessment should be conducted to understand the cause for the worn out equipment.

There may not have been a structure or process to ensure that the equipment was maintained in the

first place by the maintenance team. In that case, corrective measures should be put in place to

report these issues to ensure future maintenance of equipment is conducted on a regular basis.

Choosing the supplier

3 | P a g e

This report explains three scenarios for an organisation called Whizz Bang Corporation Ltd (WBC).

WBC is a large organisation that specialises in manufacturing spare parts for heavy transport

materials. The report is to be presented to senior management for them to make executive

decisions in regards to all three scenarios that are discussed in detail.

Discussion

Scenario 1: Capital acquisition

Capital acquisition can be defined as a company that is purchasing of capital assets for business

purposes to be used for a log term basis, usually more than 12 months. In this scenario, the capital

asset is identified as a piece of equipment that is required for business operations. Other examples

of capital assets can be inventory, software, machinery, etc.

Capital acquisition of a corporation involves an in depth strategic analysis to confirm the effective

demand of the assets.

In this scenario, WBC is expecting to replace a worn out piece equipment which is understood to be

expensive. A detailed strategic analysis is not required if the cost of the replacement is insignificant

as the cost can be financed by the running capital of the organisation. However, the piece of

equipment that WBC is wanting to replace is considered to be expensive. In this situation, the capital

acquisition is the replacement of the worn out piece of equipment.

WBC should progress the capital acquisition analysis to ensure that the manager and the company is

making a cost effective outcome for the benefit of the business operations.

Requirement identification of the replacement

WBC should first of all consider the reason for the replacement of the worn out piece of equipment.

Detailed analysis is needed to be actioned. The equipment could have been worn out because it was

being used excessively and continuously There needs to be a consideration of the worn out item to

be re-used if it is repaired, taking into account the costs that might be involved in repairing and also

the maintenance the repaired equipment. Another aspect to be considered, is the maintenance cost

if WBC considers re-using the item compared to replacing the item in the long run. It can also be

assumed that if the item is re-used after it is fixed, regular maintenance may be required to ensure

its sustainability. This may become financially expensive to WBC in long term. Therefore, a proper

calculation should be made to understand the costs that would be involved in replacing or repairing

the item.

A proper assessment should be conducted to understand the cause for the worn out equipment.

There may not have been a structure or process to ensure that the equipment was maintained in the

first place by the maintenance team. In that case, corrective measures should be put in place to

report these issues to ensure future maintenance of equipment is conducted on a regular basis.

Choosing the supplier

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Once it has been understood that the piece of equipment requires to be replaced and a new item

needs to be purchased, suppliers should then be contacted by the team member who initially put

through the request to replace the item. A quotation should be requested from all of the suppliers.

Once this is obtained, the manager should then make a decision as to which supplier to purchase the

item from depending on the costs and quality as this can be varied supplier to supplier. Therefore

the best price, keeping the best quality in mind needs to be considered when choosing the supplier.

Finance option for the capital acquisition

An appropriate finance method needs to be considered to establish the capital acquisition. WBC

should choose the most beneficial financial choice available. They need to decide if they will shift to

either equity financing or debt financing. It can utilise the company’s operating cash flows, however

it may be insufficient to satisfy the complete capital acquisition due to the high cost. Therefore, it

may be beneficial for the company to focus on debt financing, which means, it can burrow capital

from a third party on an agreed interest rate which will not impact the ownership of the equipment.

This decision needs to be taken by the manager and the company of WBC to ensure the finance

method that is chosen, meets the requirements of the organisation.

Scenario 2: Project Proposal

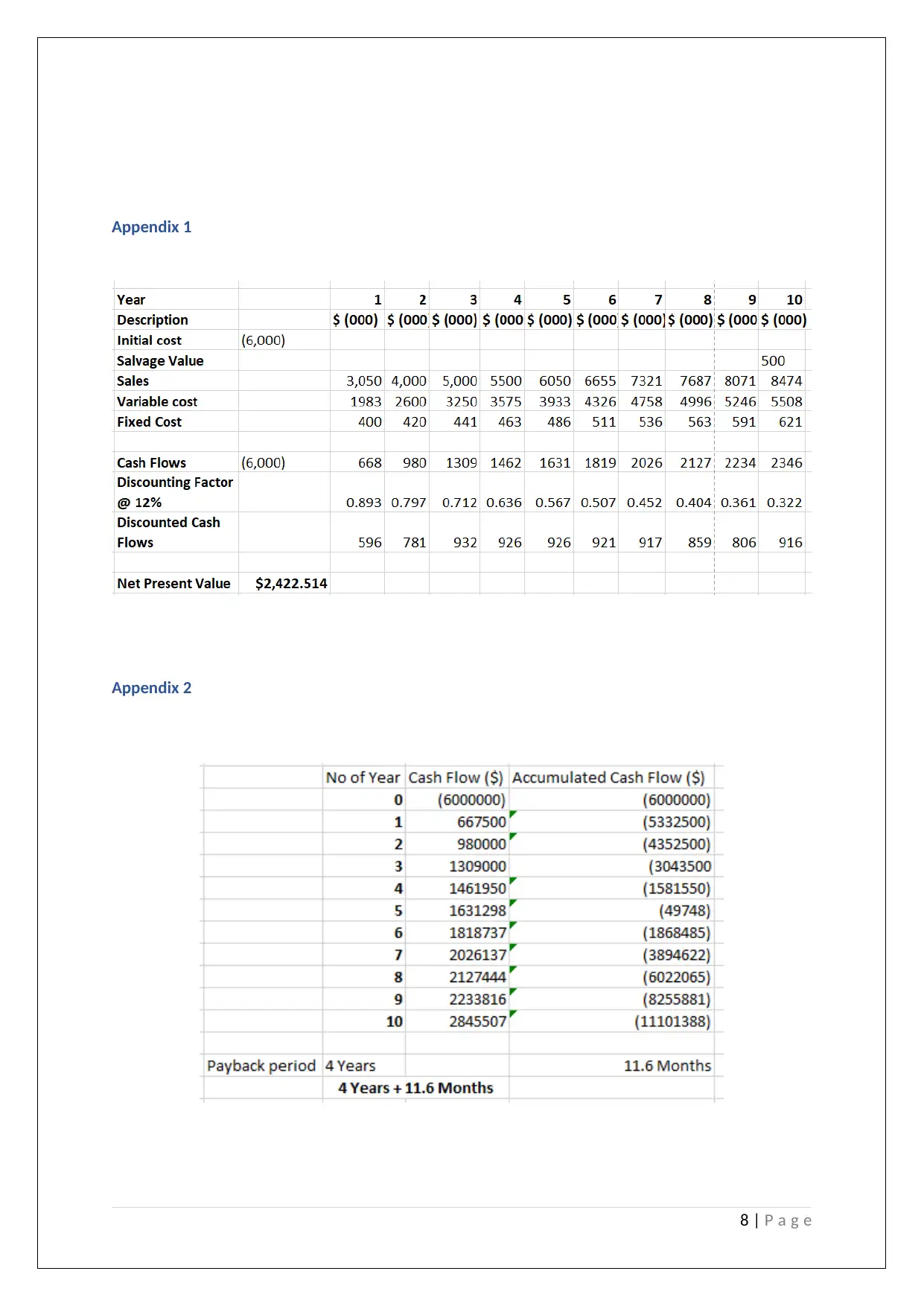

Net present value is used for comparing the present value of the cash inflow of an investment to the

amount invested today. Negative net present value shows a negative return on investment and a

positive NPV value reflects a good return on investment for the project. If the NPV value is zero, this

means that the project is under break even and it shows no return for the investor. In reference to

the calculation of NPV below for Whizz Bang Corporation Limited, it can be identified that there is a

positive NPV figure of $2,422,514, which means that the company is able to undergo the project

specified.

NPV calculation - Assumptions

As there is no cash effect, depreciation has not been considered

Research cost has been considered as a sunk cost

As only the cash flow is considered, therefore tax has not been considered

12% is used for the cost of capital

Payback period

Payback period is defined as the duration of time that is taken to recuperate the project’s initial

investment. The payback period for Whizz Bang Corporation Limited is calculated at four years and

just over eleven and a half months (4 years and 11.6 months).

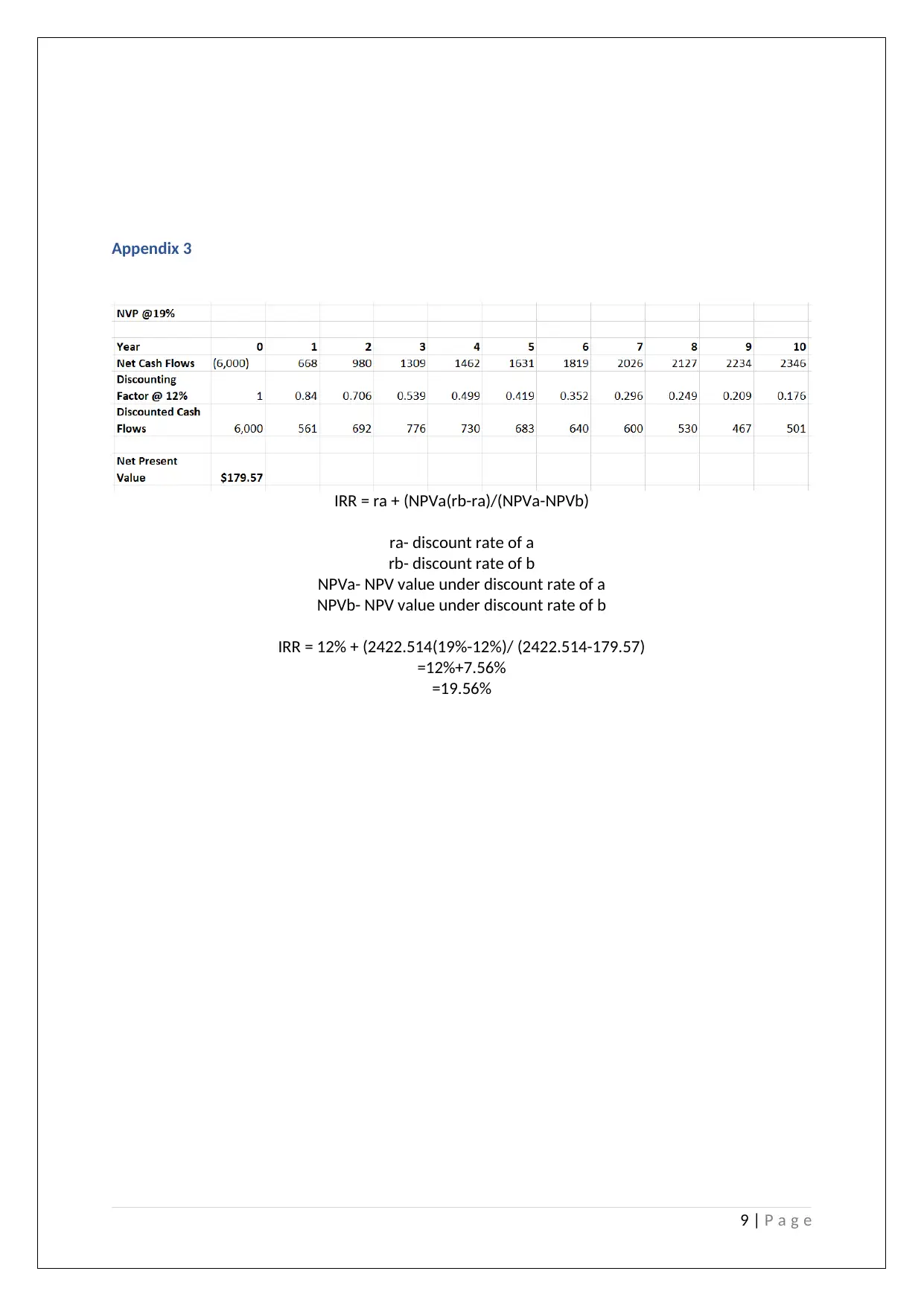

Internal Rate of Return (IRR)

The internal rate of return (IRR) is useful to estimate the effectiveness of possible investments. This

method allows the NPV of cash flows equivalent to zero for a particular project. Usually, the higher a

project’s IRR is, the more suitable it is to be conducted. According to the IRR calculation (appendix

3), it is shown that the value of the IRR is 19.56%, which is higher for Whizz Bang Corporation

Limited than the price of capital value of 12% for the project. From this observation, one can state

that WBC can accept and proceed with the proposed project.

Advantages & disadvantages of the methodology mentioned above (NPV, IRR & Payback)

4 | P a g e

needs to be purchased, suppliers should then be contacted by the team member who initially put

through the request to replace the item. A quotation should be requested from all of the suppliers.

Once this is obtained, the manager should then make a decision as to which supplier to purchase the

item from depending on the costs and quality as this can be varied supplier to supplier. Therefore

the best price, keeping the best quality in mind needs to be considered when choosing the supplier.

Finance option for the capital acquisition

An appropriate finance method needs to be considered to establish the capital acquisition. WBC

should choose the most beneficial financial choice available. They need to decide if they will shift to

either equity financing or debt financing. It can utilise the company’s operating cash flows, however

it may be insufficient to satisfy the complete capital acquisition due to the high cost. Therefore, it

may be beneficial for the company to focus on debt financing, which means, it can burrow capital

from a third party on an agreed interest rate which will not impact the ownership of the equipment.

This decision needs to be taken by the manager and the company of WBC to ensure the finance

method that is chosen, meets the requirements of the organisation.

Scenario 2: Project Proposal

Net present value is used for comparing the present value of the cash inflow of an investment to the

amount invested today. Negative net present value shows a negative return on investment and a

positive NPV value reflects a good return on investment for the project. If the NPV value is zero, this

means that the project is under break even and it shows no return for the investor. In reference to

the calculation of NPV below for Whizz Bang Corporation Limited, it can be identified that there is a

positive NPV figure of $2,422,514, which means that the company is able to undergo the project

specified.

NPV calculation - Assumptions

As there is no cash effect, depreciation has not been considered

Research cost has been considered as a sunk cost

As only the cash flow is considered, therefore tax has not been considered

12% is used for the cost of capital

Payback period

Payback period is defined as the duration of time that is taken to recuperate the project’s initial

investment. The payback period for Whizz Bang Corporation Limited is calculated at four years and

just over eleven and a half months (4 years and 11.6 months).

Internal Rate of Return (IRR)

The internal rate of return (IRR) is useful to estimate the effectiveness of possible investments. This

method allows the NPV of cash flows equivalent to zero for a particular project. Usually, the higher a

project’s IRR is, the more suitable it is to be conducted. According to the IRR calculation (appendix

3), it is shown that the value of the IRR is 19.56%, which is higher for Whizz Bang Corporation

Limited than the price of capital value of 12% for the project. From this observation, one can state

that WBC can accept and proceed with the proposed project.

Advantages & disadvantages of the methodology mentioned above (NPV, IRR & Payback)

4 | P a g e

In contrast to the IRR method, where the net cash flows are re-invested on an increased rate than

the current market rate as it includes the project’s profit, the NPV method allows the net cash flows

to be re-invested at the current market rate. It is crucial to understand that the NPV method gives

and absolute value and the IRR gives a relative measurement. It is more understandable and

relevant to projects using an absolute vale. Therefore the NPV method would be more relevant.

In the payback method, the convenience and understanding of the calculation is a lot higher than

IRR. Using the payback method, it can reduce any risk and have more certainty in regards to the

running of the project. The IRR method considers all the generated cash flows in the project which

can be a disadvantage for this methodology. It only selects the less uncertain and high risk projects,

which can mean that profitable projects night get avoided or ignored.

Having an understanding of the three methodologies discussed above, it can be evaluated that the

NPV calculation method is much more relevant and reliable for the project.

Other matters to consider for the proposed project

Some of the Financial factors have been discussed above for when assessing the requirements and

investments of the proposed project. However, non-financial factors also need to be considered

when assessing the requirements and recommendations of a project. The following factors need to

be considered as well:

Organisational Factors

The current organsational strategy should be assessed with the proposed investment. For example,

if WBC has a strategy to expand its business further or increases its market share later, it can impact

the proposed project, therefore would need to be considered when assessing the investment of the

project.

Social & Environmental factors

The impact on the environment needs to be considered when assessing the requirements of the

project. For example, there needs to be appropriate disposal methods in place to ensure that the

company avoids any social or environment issues that may arise during project implementation.

WBC also need to consider any emission tests, quality tests and other important tests required to

ensure that they are following any required rules and regulations in relation to the environmental

factors of the country that it is operating in.

Scenario 3: Project Financing

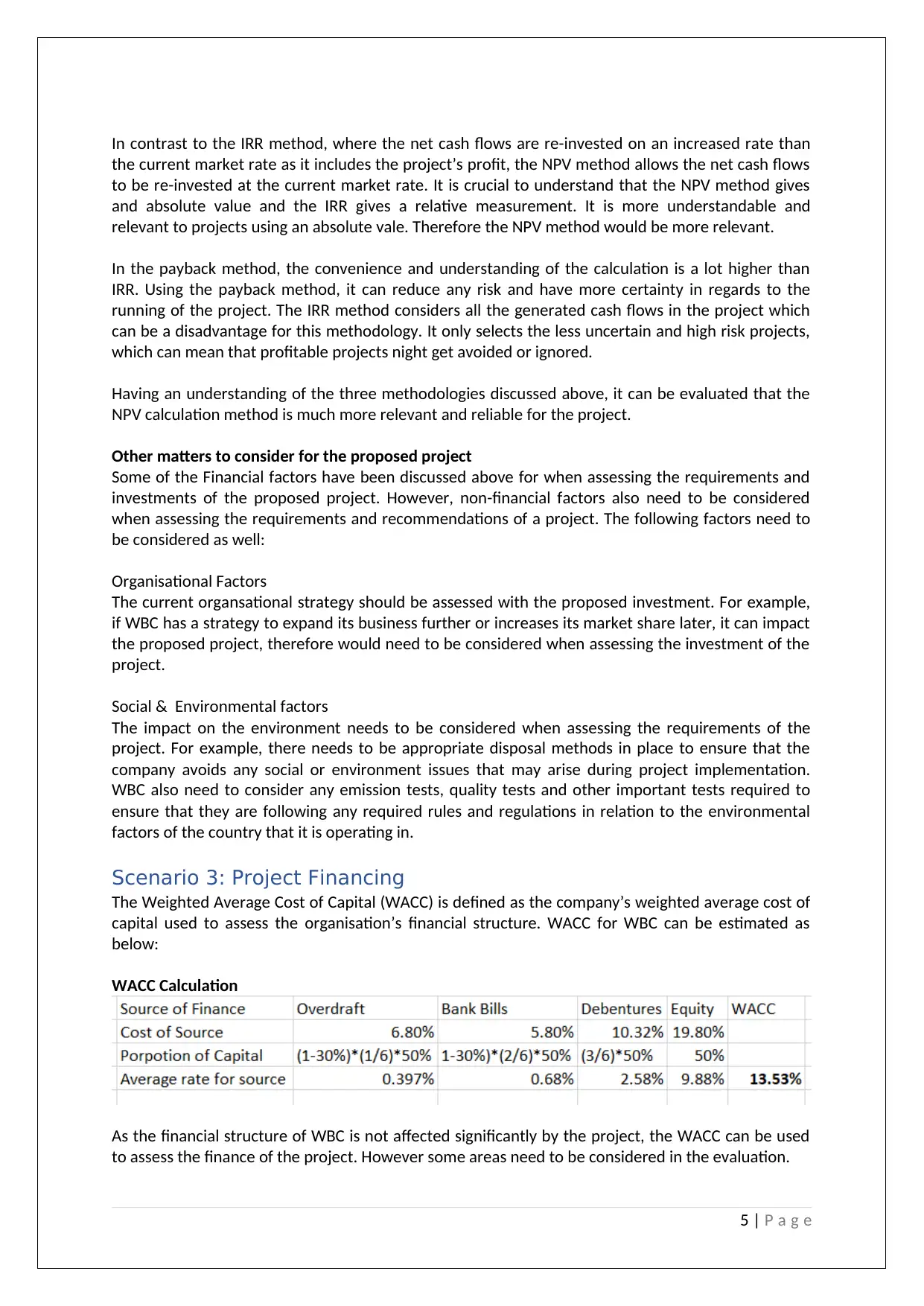

The Weighted Average Cost of Capital (WACC) is defined as the company’s weighted average cost of

capital used to assess the organisation’s financial structure. WACC for WBC can be estimated as

below:

WACC Calculation

As the financial structure of WBC is not affected significantly by the project, the WACC can be used

to assess the finance of the project. However some areas need to be considered in the evaluation.

5 | P a g e

the current market rate as it includes the project’s profit, the NPV method allows the net cash flows

to be re-invested at the current market rate. It is crucial to understand that the NPV method gives

and absolute value and the IRR gives a relative measurement. It is more understandable and

relevant to projects using an absolute vale. Therefore the NPV method would be more relevant.

In the payback method, the convenience and understanding of the calculation is a lot higher than

IRR. Using the payback method, it can reduce any risk and have more certainty in regards to the

running of the project. The IRR method considers all the generated cash flows in the project which

can be a disadvantage for this methodology. It only selects the less uncertain and high risk projects,

which can mean that profitable projects night get avoided or ignored.

Having an understanding of the three methodologies discussed above, it can be evaluated that the

NPV calculation method is much more relevant and reliable for the project.

Other matters to consider for the proposed project

Some of the Financial factors have been discussed above for when assessing the requirements and

investments of the proposed project. However, non-financial factors also need to be considered

when assessing the requirements and recommendations of a project. The following factors need to

be considered as well:

Organisational Factors

The current organsational strategy should be assessed with the proposed investment. For example,

if WBC has a strategy to expand its business further or increases its market share later, it can impact

the proposed project, therefore would need to be considered when assessing the investment of the

project.

Social & Environmental factors

The impact on the environment needs to be considered when assessing the requirements of the

project. For example, there needs to be appropriate disposal methods in place to ensure that the

company avoids any social or environment issues that may arise during project implementation.

WBC also need to consider any emission tests, quality tests and other important tests required to

ensure that they are following any required rules and regulations in relation to the environmental

factors of the country that it is operating in.

Scenario 3: Project Financing

The Weighted Average Cost of Capital (WACC) is defined as the company’s weighted average cost of

capital used to assess the organisation’s financial structure. WACC for WBC can be estimated as

below:

WACC Calculation

As the financial structure of WBC is not affected significantly by the project, the WACC can be used

to assess the finance of the project. However some areas need to be considered in the evaluation.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The WACC will not show the real cost of capital which WBC is exposed to as the financial structure

will change when any project is implemented. The WACC is analysed according to the present

market rate that is available. However, it needs to be considered that due to the industry risk

exposure and the economic fluctuation, the market rate can be changed. As the calculation for

WACC is very complicated, it can also change the figures and may increase the risk for business

continuity.

It is therefore recommended for WBC to consider the project focused Cost of capital to assess the

proposed project. Therefore, it will not be beneficial for WBC to use WACC calculation to evaluate

the proposed project as It is more appropriate for them to use the project particular cost of capital.

Conclusion

This report explains three scenarios in detail for WBC. The first scenario explains the requirements of

the replacement of a worn out equipment that WBC owns. This section would assist the manager to

decide whether the item should be replaced or repaired, depending of factors such as cost, need,

how quickly the company would need the item, etc. The second scenario describes the project

requirement of a potential opportunity for WBC. The outcome of the analysis in this scenario was

that the company was able to progress with the proposed project for the implementation of the new

opportunity. The third scenario discusses the calculation of the Weighted Average Cost of Capital

(WACC) for WBC and whether this method can be used to assess the project mentioned in this

scenario and if there are any restrictions.

6 | P a g e

will change when any project is implemented. The WACC is analysed according to the present

market rate that is available. However, it needs to be considered that due to the industry risk

exposure and the economic fluctuation, the market rate can be changed. As the calculation for

WACC is very complicated, it can also change the figures and may increase the risk for business

continuity.

It is therefore recommended for WBC to consider the project focused Cost of capital to assess the

proposed project. Therefore, it will not be beneficial for WBC to use WACC calculation to evaluate

the proposed project as It is more appropriate for them to use the project particular cost of capital.

Conclusion

This report explains three scenarios in detail for WBC. The first scenario explains the requirements of

the replacement of a worn out equipment that WBC owns. This section would assist the manager to

decide whether the item should be replaced or repaired, depending of factors such as cost, need,

how quickly the company would need the item, etc. The second scenario describes the project

requirement of a potential opportunity for WBC. The outcome of the analysis in this scenario was

that the company was able to progress with the proposed project for the implementation of the new

opportunity. The third scenario discusses the calculation of the Weighted Average Cost of Capital

(WACC) for WBC and whether this method can be used to assess the project mentioned in this

scenario and if there are any restrictions.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Chapter 10 in Birt, J., Chalmers, K., Maloney, S., Oliver, J., 2014. Accounting: Business Reporting for

Decision Making, 5th ed. John Wiley and Sons, Milton, Australia.

Business dictionary, ‘net present value (NPV)’ Business dictionary, 2019, viewed on 22 Sep, 2019,

Available at http://www.businessdictionary.com/definition/net-present-value-NPV.html

Hart, M, ‘Net Present Value (NPV)’, Explained in 400 Words or Less’, HubSpot, 2019, viewed on

viewed on 22 Sep 2019, Available at https://blog.hubspot.com/sales/net-present-value

Kenton, W, ‘Net Present Value (NPV)’, Invetopedia, 25 July, 2019, viewed on 22 Sep 2019, Available

at https://www.investopedia.com/terms/n/npv.asp

Hayes, A, ‘Internal Rate of Return – IRR’, Jun 25, 2019, viewed on 22 Sep 2019, Available at

https://www.investopedia.com/terms/i/irr.asp

Raszkiewicz, O, ‘Explained: How to Calculate eighted Average Cost of Capital (WACC) in Valuation’

Raskfinance, Annual Report’, viewed on 22 Sep 2019, Available at

https://www.raskfinance.com/2018/07/16/explained-how-to-calculate-weighted-average-cost-of-

capital-wacc-in-valuation/

Accounting For Management, ‘Payback Method’ Accounting For Management, 2012-2018, viewed

on 22 Sep 2019, Available at https://www.accountingformanagement.org/payback-method/

Gallo, A, ‘A Refresher on Payback Method’, Harvard Business Review, Apr 18, 216, viewed on 22 Sep

2019, Available at https://hbr.org/2016/04/a-refresher-on-payback-method

Investing Answers, ‘Internal Rate of Return (IRR)’, Investing Answers, 2019, viewed on 22 Sep 2019,

Available at https://investinganswers.com/dictionary/i/internal-rate-return-irr

Guide, ‘Investment appraisal techniques, NiBusinessInfo, viewed on 22 Sep 2019, Available at

https://www.nibusinessinfo.co.uk/content/non-financial-factors-investment-appraisal

7 | P a g e

Chapter 10 in Birt, J., Chalmers, K., Maloney, S., Oliver, J., 2014. Accounting: Business Reporting for

Decision Making, 5th ed. John Wiley and Sons, Milton, Australia.

Business dictionary, ‘net present value (NPV)’ Business dictionary, 2019, viewed on 22 Sep, 2019,

Available at http://www.businessdictionary.com/definition/net-present-value-NPV.html

Hart, M, ‘Net Present Value (NPV)’, Explained in 400 Words or Less’, HubSpot, 2019, viewed on

viewed on 22 Sep 2019, Available at https://blog.hubspot.com/sales/net-present-value

Kenton, W, ‘Net Present Value (NPV)’, Invetopedia, 25 July, 2019, viewed on 22 Sep 2019, Available

at https://www.investopedia.com/terms/n/npv.asp

Hayes, A, ‘Internal Rate of Return – IRR’, Jun 25, 2019, viewed on 22 Sep 2019, Available at

https://www.investopedia.com/terms/i/irr.asp

Raszkiewicz, O, ‘Explained: How to Calculate eighted Average Cost of Capital (WACC) in Valuation’

Raskfinance, Annual Report’, viewed on 22 Sep 2019, Available at

https://www.raskfinance.com/2018/07/16/explained-how-to-calculate-weighted-average-cost-of-

capital-wacc-in-valuation/

Accounting For Management, ‘Payback Method’ Accounting For Management, 2012-2018, viewed

on 22 Sep 2019, Available at https://www.accountingformanagement.org/payback-method/

Gallo, A, ‘A Refresher on Payback Method’, Harvard Business Review, Apr 18, 216, viewed on 22 Sep

2019, Available at https://hbr.org/2016/04/a-refresher-on-payback-method

Investing Answers, ‘Internal Rate of Return (IRR)’, Investing Answers, 2019, viewed on 22 Sep 2019,

Available at https://investinganswers.com/dictionary/i/internal-rate-return-irr

Guide, ‘Investment appraisal techniques, NiBusinessInfo, viewed on 22 Sep 2019, Available at

https://www.nibusinessinfo.co.uk/content/non-financial-factors-investment-appraisal

7 | P a g e

Appendix 1

Appendix 2

8 | P a g e

Appendix 2

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appendix 3

IRR = ra + (NPVa(rb-ra)/(NPVa-NPVb)

ra- discount rate of a

rb- discount rate of b

NPVa- NPV value under discount rate of a

NPVb- NPV value under discount rate of b

IRR = 12% + (2422.514(19%-12%)/ (2422.514-179.57)

=12%+7.56%

=19.56%

9 | P a g e

IRR = ra + (NPVa(rb-ra)/(NPVa-NPVb)

ra- discount rate of a

rb- discount rate of b

NPVa- NPV value under discount rate of a

NPVb- NPV value under discount rate of b

IRR = 12% + (2422.514(19%-12%)/ (2422.514-179.57)

=12%+7.56%

=19.56%

9 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.