ACC4029 - Operations & Finance: Strategic Analysis of Cucumber Ltd

VerifiedAdded on 2023/04/21

|12

|3548

|494

Report

AI Summary

This report evaluates Cucumber Ltd's expansion plans using capital investment techniques, analyzing four proposals and recommending the most suitable option. It discusses the role of management accounting, business plans, and budgets in operational effectiveness. A balanced scorecard is devel...

Managing Operations and Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report is undertaken to evaluate the case study of Cucumber Ltd on the basis of

information provided. It is a Smartphone company that is planning for gaining future expansion

in the next three eyras and is considering the execution of its expansion plan by selection of a

proposal from the four proposals provided with the use of capital investment techniques. It has

also discussed the role of business plan and budgets in examining the effectiveness of operation

for an organization. Also, it has developed and presented a balance scorecard on the basis of

information provided within the case.

2

This report is undertaken to evaluate the case study of Cucumber Ltd on the basis of

information provided. It is a Smartphone company that is planning for gaining future expansion

in the next three eyras and is considering the execution of its expansion plan by selection of a

proposal from the four proposals provided with the use of capital investment techniques. It has

also discussed the role of business plan and budgets in examining the effectiveness of operation

for an organization. Also, it has developed and presented a balance scorecard on the basis of

information provided within the case.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part 1: Role of Management accounting in the management process.............................................4

Part 2: Application of capital investment appraisal techniques in the case the organization..........6

Part 3: Importance of Business Plan and Budget in the case organization......................................8

Part 4: Critically discussion of the usefulness of Balanced Scorecard Approach and development

of Balance Scorecard for Cucumber Ltd.......................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part 1: Role of Management accounting in the management process.............................................4

Part 2: Application of capital investment appraisal techniques in the case the organization..........6

Part 3: Importance of Business Plan and Budget in the case organization......................................8

Part 4: Critically discussion of the usefulness of Balanced Scorecard Approach and development

of Balance Scorecard for Cucumber Ltd.......................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report is developed for carrying out an analysis of the case study of Cucumber Ltd, a

smart phone company, that is planning to expand its business in the future context. The analysis

is undertaken by examination of the role of management accounting process and adopting the sue

of capital investment appraisal techniques for selecting an adequate project for supporting

company future expansion pan, IT is followed by examining the role of business plan and budget

in operational management in the context of the case study. Lastly, the usefulness of balance

scorecard has been discussing along with its preparation for Cucumber Ltd on the basis of the

information presented within the case study.

Part 1: Role of Management accounting in the management process

Management accounting refers to the processes used for tracking the internal cost of

business processes that enables the management in taking decisions related to production and

other operational activities. It refers to the accounting processes that are undertaken by

management for identifying, measuring and interpreting the financial data gathered for the

purpose of planning and control. The role of management accounting is preparation and

presentation of relevant and useful financial data before the management for guiding in decision-

making process and achieving the stated organizational goals. It implies to integrating the use of

actual financial information and estimated data that assist managers to make decisions regarding

carrying out daily operations and planning for promoting the future organizational growth

(Ghanbari and Vaseli, 2015). The different management accounting tools that are used by the

business managers in managing and controlling the different operational activities are activity-

based costing, target costing, Kaizen costing, JIT, six sigma, total quality management and

others. The role of management accounting is becoming highly important within an organization

to enhance its operational efficiency. The use of budgeting and other control techniques in

management accounting enables in developing an understanding of the future target and goals to

be achieved and thus assisting the management in strategic planning.

The process of management accounting is significantly different from that of financial

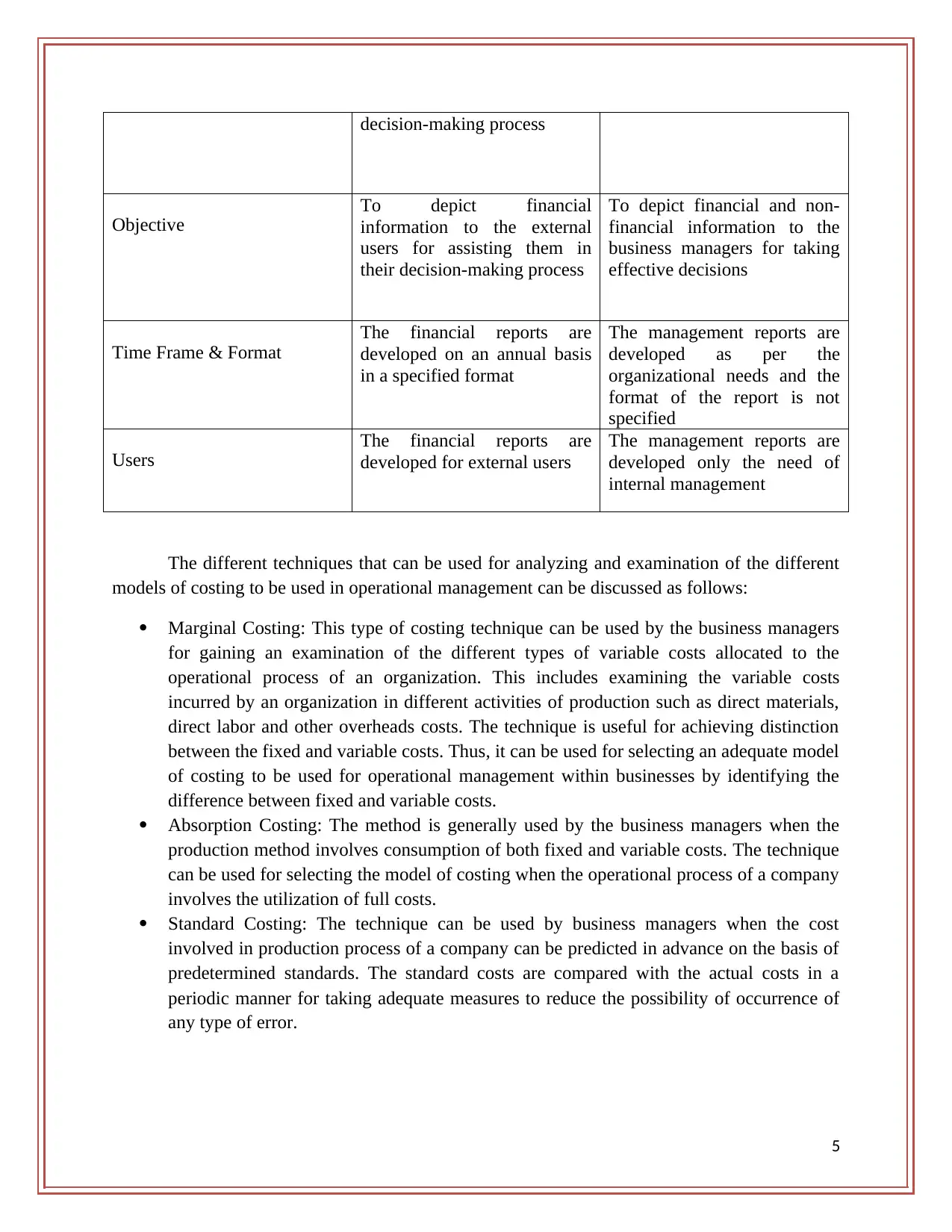

accounting and the basic differences between them can be depicted by the use of following table:

Comparison Basis Financial Accounting Management Accounting

Meaning The accounting system

emphasis on development and

presentation of financial

statement to the external users

of an organization for

providing the financial

information to assist in the

This accounting system refers

to developing and presenting

the financial information to

the managers for assisting

them to develop future

strategies and plan to promote

its growth and development

4

This report is developed for carrying out an analysis of the case study of Cucumber Ltd, a

smart phone company, that is planning to expand its business in the future context. The analysis

is undertaken by examination of the role of management accounting process and adopting the sue

of capital investment appraisal techniques for selecting an adequate project for supporting

company future expansion pan, IT is followed by examining the role of business plan and budget

in operational management in the context of the case study. Lastly, the usefulness of balance

scorecard has been discussing along with its preparation for Cucumber Ltd on the basis of the

information presented within the case study.

Part 1: Role of Management accounting in the management process

Management accounting refers to the processes used for tracking the internal cost of

business processes that enables the management in taking decisions related to production and

other operational activities. It refers to the accounting processes that are undertaken by

management for identifying, measuring and interpreting the financial data gathered for the

purpose of planning and control. The role of management accounting is preparation and

presentation of relevant and useful financial data before the management for guiding in decision-

making process and achieving the stated organizational goals. It implies to integrating the use of

actual financial information and estimated data that assist managers to make decisions regarding

carrying out daily operations and planning for promoting the future organizational growth

(Ghanbari and Vaseli, 2015). The different management accounting tools that are used by the

business managers in managing and controlling the different operational activities are activity-

based costing, target costing, Kaizen costing, JIT, six sigma, total quality management and

others. The role of management accounting is becoming highly important within an organization

to enhance its operational efficiency. The use of budgeting and other control techniques in

management accounting enables in developing an understanding of the future target and goals to

be achieved and thus assisting the management in strategic planning.

The process of management accounting is significantly different from that of financial

accounting and the basic differences between them can be depicted by the use of following table:

Comparison Basis Financial Accounting Management Accounting

Meaning The accounting system

emphasis on development and

presentation of financial

statement to the external users

of an organization for

providing the financial

information to assist in the

This accounting system refers

to developing and presenting

the financial information to

the managers for assisting

them to develop future

strategies and plan to promote

its growth and development

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decision-making process

Objective

To depict financial

information to the external

users for assisting them in

their decision-making process

To depict financial and non-

financial information to the

business managers for taking

effective decisions

Time Frame & Format

The financial reports are

developed on an annual basis

in a specified format

The management reports are

developed as per the

organizational needs and the

format of the report is not

specified

Users

The financial reports are

developed for external users

The management reports are

developed only the need of

internal management

The different techniques that can be used for analyzing and examination of the different

models of costing to be used in operational management can be discussed as follows:

Marginal Costing: This type of costing technique can be used by the business managers

for gaining an examination of the different types of variable costs allocated to the

operational process of an organization. This includes examining the variable costs

incurred by an organization in different activities of production such as direct materials,

direct labor and other overheads costs. The technique is useful for achieving distinction

between the fixed and variable costs. Thus, it can be used for selecting an adequate model

of costing to be used for operational management within businesses by identifying the

difference between fixed and variable costs.

Absorption Costing: The method is generally used by the business managers when the

production method involves consumption of both fixed and variable costs. The technique

can be used for selecting the model of costing when the operational process of a company

involves the utilization of full costs.

Standard Costing: The technique can be used by business managers when the cost

involved in production process of a company can be predicted in advance on the basis of

predetermined standards. The standard costs are compared with the actual costs in a

periodic manner for taking adequate measures to reduce the possibility of occurrence of

any type of error.

5

Objective

To depict financial

information to the external

users for assisting them in

their decision-making process

To depict financial and non-

financial information to the

business managers for taking

effective decisions

Time Frame & Format

The financial reports are

developed on an annual basis

in a specified format

The management reports are

developed as per the

organizational needs and the

format of the report is not

specified

Users

The financial reports are

developed for external users

The management reports are

developed only the need of

internal management

The different techniques that can be used for analyzing and examination of the different

models of costing to be used in operational management can be discussed as follows:

Marginal Costing: This type of costing technique can be used by the business managers

for gaining an examination of the different types of variable costs allocated to the

operational process of an organization. This includes examining the variable costs

incurred by an organization in different activities of production such as direct materials,

direct labor and other overheads costs. The technique is useful for achieving distinction

between the fixed and variable costs. Thus, it can be used for selecting an adequate model

of costing to be used for operational management within businesses by identifying the

difference between fixed and variable costs.

Absorption Costing: The method is generally used by the business managers when the

production method involves consumption of both fixed and variable costs. The technique

can be used for selecting the model of costing when the operational process of a company

involves the utilization of full costs.

Standard Costing: The technique can be used by business managers when the cost

involved in production process of a company can be predicted in advance on the basis of

predetermined standards. The standard costs are compared with the actual costs in a

periodic manner for taking adequate measures to reduce the possibility of occurrence of

any type of error.

5

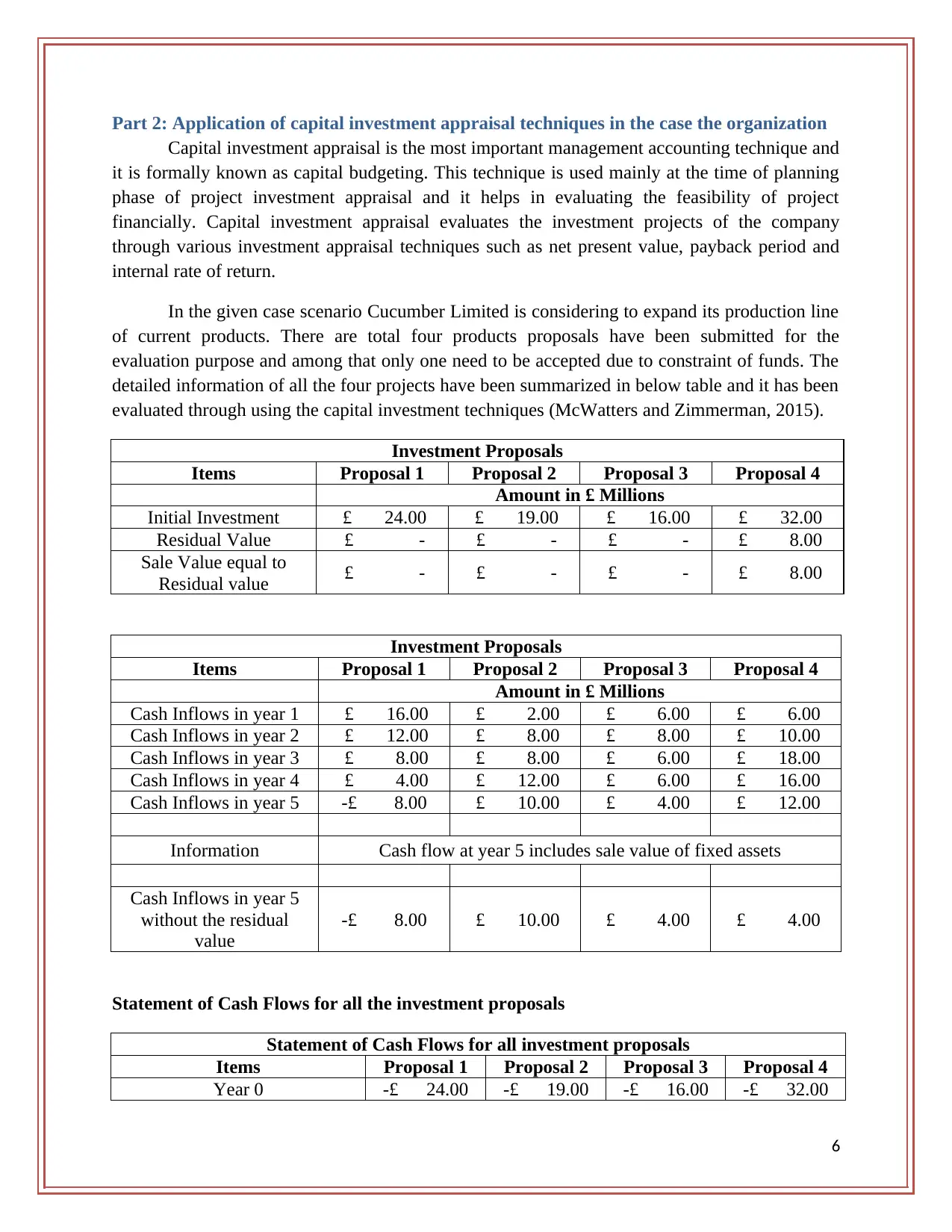

Part 2: Application of capital investment appraisal techniques in the case the organization

Capital investment appraisal is the most important management accounting technique and

it is formally known as capital budgeting. This technique is used mainly at the time of planning

phase of project investment appraisal and it helps in evaluating the feasibility of project

financially. Capital investment appraisal evaluates the investment projects of the company

through various investment appraisal techniques such as net present value, payback period and

internal rate of return.

In the given case scenario Cucumber Limited is considering to expand its production line

of current products. There are total four products proposals have been submitted for the

evaluation purpose and among that only one need to be accepted due to constraint of funds. The

detailed information of all the four projects have been summarized in below table and it has been

evaluated through using the capital investment techniques (McWatters and Zimmerman, 2015).

Investment Proposals

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Amount in £ Millions

Initial Investment £ 24.00 £ 19.00 £ 16.00 £ 32.00

Residual Value £ - £ - £ - £ 8.00

Sale Value equal to

Residual value £ - £ - £ - £ 8.00

Investment Proposals

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Amount in £ Millions

Cash Inflows in year 1 £ 16.00 £ 2.00 £ 6.00 £ 6.00

Cash Inflows in year 2 £ 12.00 £ 8.00 £ 8.00 £ 10.00

Cash Inflows in year 3 £ 8.00 £ 8.00 £ 6.00 £ 18.00

Cash Inflows in year 4 £ 4.00 £ 12.00 £ 6.00 £ 16.00

Cash Inflows in year 5 -£ 8.00 £ 10.00 £ 4.00 £ 12.00

Information Cash flow at year 5 includes sale value of fixed assets

Cash Inflows in year 5

without the residual

value

-£ 8.00 £ 10.00 £ 4.00 £ 4.00

Statement of Cash Flows for all the investment proposals

Statement of Cash Flows for all investment proposals

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

6

Capital investment appraisal is the most important management accounting technique and

it is formally known as capital budgeting. This technique is used mainly at the time of planning

phase of project investment appraisal and it helps in evaluating the feasibility of project

financially. Capital investment appraisal evaluates the investment projects of the company

through various investment appraisal techniques such as net present value, payback period and

internal rate of return.

In the given case scenario Cucumber Limited is considering to expand its production line

of current products. There are total four products proposals have been submitted for the

evaluation purpose and among that only one need to be accepted due to constraint of funds. The

detailed information of all the four projects have been summarized in below table and it has been

evaluated through using the capital investment techniques (McWatters and Zimmerman, 2015).

Investment Proposals

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Amount in £ Millions

Initial Investment £ 24.00 £ 19.00 £ 16.00 £ 32.00

Residual Value £ - £ - £ - £ 8.00

Sale Value equal to

Residual value £ - £ - £ - £ 8.00

Investment Proposals

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Amount in £ Millions

Cash Inflows in year 1 £ 16.00 £ 2.00 £ 6.00 £ 6.00

Cash Inflows in year 2 £ 12.00 £ 8.00 £ 8.00 £ 10.00

Cash Inflows in year 3 £ 8.00 £ 8.00 £ 6.00 £ 18.00

Cash Inflows in year 4 £ 4.00 £ 12.00 £ 6.00 £ 16.00

Cash Inflows in year 5 -£ 8.00 £ 10.00 £ 4.00 £ 12.00

Information Cash flow at year 5 includes sale value of fixed assets

Cash Inflows in year 5

without the residual

value

-£ 8.00 £ 10.00 £ 4.00 £ 4.00

Statement of Cash Flows for all the investment proposals

Statement of Cash Flows for all investment proposals

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

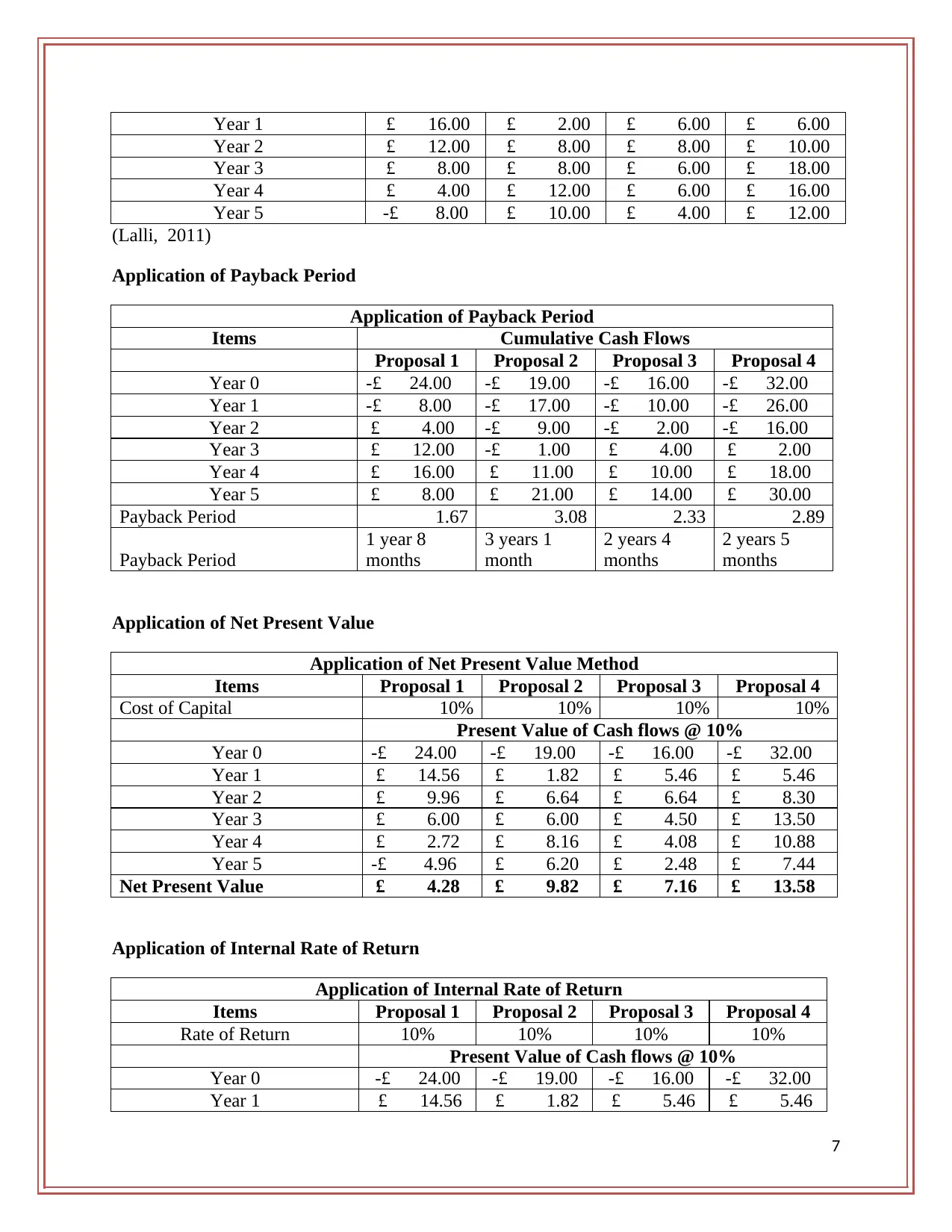

Year 1 £ 16.00 £ 2.00 £ 6.00 £ 6.00

Year 2 £ 12.00 £ 8.00 £ 8.00 £ 10.00

Year 3 £ 8.00 £ 8.00 £ 6.00 £ 18.00

Year 4 £ 4.00 £ 12.00 £ 6.00 £ 16.00

Year 5 -£ 8.00 £ 10.00 £ 4.00 £ 12.00

(Lalli, 2011)

Application of Payback Period

Application of Payback Period

Items Cumulative Cash Flows

Proposal 1 Proposal 2 Proposal 3 Proposal 4

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

Year 1 -£ 8.00 -£ 17.00 -£ 10.00 -£ 26.00

Year 2 £ 4.00 -£ 9.00 -£ 2.00 -£ 16.00

Year 3 £ 12.00 -£ 1.00 £ 4.00 £ 2.00

Year 4 £ 16.00 £ 11.00 £ 10.00 £ 18.00

Year 5 £ 8.00 £ 21.00 £ 14.00 £ 30.00

Payback Period 1.67 3.08 2.33 2.89

Payback Period

1 year 8

months

3 years 1

month

2 years 4

months

2 years 5

months

Application of Net Present Value

Application of Net Present Value Method

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Cost of Capital 10% 10% 10% 10%

Present Value of Cash flows @ 10%

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

Year 1 £ 14.56 £ 1.82 £ 5.46 £ 5.46

Year 2 £ 9.96 £ 6.64 £ 6.64 £ 8.30

Year 3 £ 6.00 £ 6.00 £ 4.50 £ 13.50

Year 4 £ 2.72 £ 8.16 £ 4.08 £ 10.88

Year 5 -£ 4.96 £ 6.20 £ 2.48 £ 7.44

Net Present Value £ 4.28 £ 9.82 £ 7.16 £ 13.58

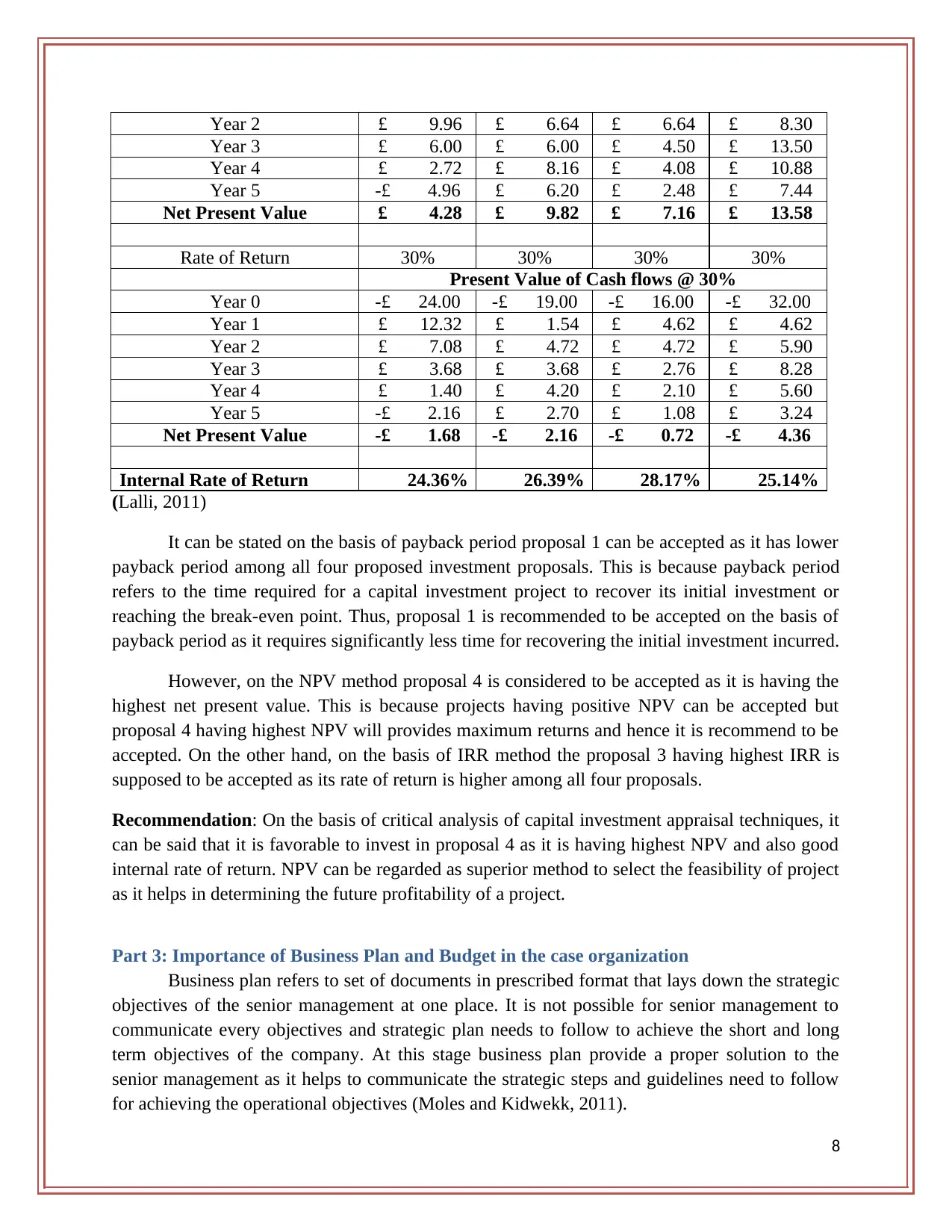

Application of Internal Rate of Return

Application of Internal Rate of Return

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Rate of Return 10% 10% 10% 10%

Present Value of Cash flows @ 10%

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

Year 1 £ 14.56 £ 1.82 £ 5.46 £ 5.46

7

Year 2 £ 12.00 £ 8.00 £ 8.00 £ 10.00

Year 3 £ 8.00 £ 8.00 £ 6.00 £ 18.00

Year 4 £ 4.00 £ 12.00 £ 6.00 £ 16.00

Year 5 -£ 8.00 £ 10.00 £ 4.00 £ 12.00

(Lalli, 2011)

Application of Payback Period

Application of Payback Period

Items Cumulative Cash Flows

Proposal 1 Proposal 2 Proposal 3 Proposal 4

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

Year 1 -£ 8.00 -£ 17.00 -£ 10.00 -£ 26.00

Year 2 £ 4.00 -£ 9.00 -£ 2.00 -£ 16.00

Year 3 £ 12.00 -£ 1.00 £ 4.00 £ 2.00

Year 4 £ 16.00 £ 11.00 £ 10.00 £ 18.00

Year 5 £ 8.00 £ 21.00 £ 14.00 £ 30.00

Payback Period 1.67 3.08 2.33 2.89

Payback Period

1 year 8

months

3 years 1

month

2 years 4

months

2 years 5

months

Application of Net Present Value

Application of Net Present Value Method

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Cost of Capital 10% 10% 10% 10%

Present Value of Cash flows @ 10%

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

Year 1 £ 14.56 £ 1.82 £ 5.46 £ 5.46

Year 2 £ 9.96 £ 6.64 £ 6.64 £ 8.30

Year 3 £ 6.00 £ 6.00 £ 4.50 £ 13.50

Year 4 £ 2.72 £ 8.16 £ 4.08 £ 10.88

Year 5 -£ 4.96 £ 6.20 £ 2.48 £ 7.44

Net Present Value £ 4.28 £ 9.82 £ 7.16 £ 13.58

Application of Internal Rate of Return

Application of Internal Rate of Return

Items Proposal 1 Proposal 2 Proposal 3 Proposal 4

Rate of Return 10% 10% 10% 10%

Present Value of Cash flows @ 10%

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

Year 1 £ 14.56 £ 1.82 £ 5.46 £ 5.46

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Year 2 £ 9.96 £ 6.64 £ 6.64 £ 8.30

Year 3 £ 6.00 £ 6.00 £ 4.50 £ 13.50

Year 4 £ 2.72 £ 8.16 £ 4.08 £ 10.88

Year 5 -£ 4.96 £ 6.20 £ 2.48 £ 7.44

Net Present Value £ 4.28 £ 9.82 £ 7.16 £ 13.58

Rate of Return 30% 30% 30% 30%

Present Value of Cash flows @ 30%

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

Year 1 £ 12.32 £ 1.54 £ 4.62 £ 4.62

Year 2 £ 7.08 £ 4.72 £ 4.72 £ 5.90

Year 3 £ 3.68 £ 3.68 £ 2.76 £ 8.28

Year 4 £ 1.40 £ 4.20 £ 2.10 £ 5.60

Year 5 -£ 2.16 £ 2.70 £ 1.08 £ 3.24

Net Present Value -£ 1.68 -£ 2.16 -£ 0.72 -£ 4.36

Internal Rate of Return 24.36% 26.39% 28.17% 25.14%

(Lalli, 2011)

It can be stated on the basis of payback period proposal 1 can be accepted as it has lower

payback period among all four proposed investment proposals. This is because payback period

refers to the time required for a capital investment project to recover its initial investment or

reaching the break-even point. Thus, proposal 1 is recommended to be accepted on the basis of

payback period as it requires significantly less time for recovering the initial investment incurred.

However, on the NPV method proposal 4 is considered to be accepted as it is having the

highest net present value. This is because projects having positive NPV can be accepted but

proposal 4 having highest NPV will provides maximum returns and hence it is recommend to be

accepted. On the other hand, on the basis of IRR method the proposal 3 having highest IRR is

supposed to be accepted as its rate of return is higher among all four proposals.

Recommendation: On the basis of critical analysis of capital investment appraisal techniques, it

can be said that it is favorable to invest in proposal 4 as it is having highest NPV and also good

internal rate of return. NPV can be regarded as superior method to select the feasibility of project

as it helps in determining the future profitability of a project.

Part 3: Importance of Business Plan and Budget in the case organization

Business plan refers to set of documents in prescribed format that lays down the strategic

objectives of the senior management at one place. It is not possible for senior management to

communicate every objectives and strategic plan needs to follow to achieve the short and long

term objectives of the company. At this stage business plan provide a proper solution to the

senior management as it helps to communicate the strategic steps and guidelines need to follow

for achieving the operational objectives (Moles and Kidwekk, 2011).

8

Year 3 £ 6.00 £ 6.00 £ 4.50 £ 13.50

Year 4 £ 2.72 £ 8.16 £ 4.08 £ 10.88

Year 5 -£ 4.96 £ 6.20 £ 2.48 £ 7.44

Net Present Value £ 4.28 £ 9.82 £ 7.16 £ 13.58

Rate of Return 30% 30% 30% 30%

Present Value of Cash flows @ 30%

Year 0 -£ 24.00 -£ 19.00 -£ 16.00 -£ 32.00

Year 1 £ 12.32 £ 1.54 £ 4.62 £ 4.62

Year 2 £ 7.08 £ 4.72 £ 4.72 £ 5.90

Year 3 £ 3.68 £ 3.68 £ 2.76 £ 8.28

Year 4 £ 1.40 £ 4.20 £ 2.10 £ 5.60

Year 5 -£ 2.16 £ 2.70 £ 1.08 £ 3.24

Net Present Value -£ 1.68 -£ 2.16 -£ 0.72 -£ 4.36

Internal Rate of Return 24.36% 26.39% 28.17% 25.14%

(Lalli, 2011)

It can be stated on the basis of payback period proposal 1 can be accepted as it has lower

payback period among all four proposed investment proposals. This is because payback period

refers to the time required for a capital investment project to recover its initial investment or

reaching the break-even point. Thus, proposal 1 is recommended to be accepted on the basis of

payback period as it requires significantly less time for recovering the initial investment incurred.

However, on the NPV method proposal 4 is considered to be accepted as it is having the

highest net present value. This is because projects having positive NPV can be accepted but

proposal 4 having highest NPV will provides maximum returns and hence it is recommend to be

accepted. On the other hand, on the basis of IRR method the proposal 3 having highest IRR is

supposed to be accepted as its rate of return is higher among all four proposals.

Recommendation: On the basis of critical analysis of capital investment appraisal techniques, it

can be said that it is favorable to invest in proposal 4 as it is having highest NPV and also good

internal rate of return. NPV can be regarded as superior method to select the feasibility of project

as it helps in determining the future profitability of a project.

Part 3: Importance of Business Plan and Budget in the case organization

Business plan refers to set of documents in prescribed format that lays down the strategic

objectives of the senior management at one place. It is not possible for senior management to

communicate every objectives and strategic plan needs to follow to achieve the short and long

term objectives of the company. At this stage business plan provide a proper solution to the

senior management as it helps to communicate the strategic steps and guidelines need to follow

for achieving the operational objectives (Moles and Kidwekk, 2011).

8

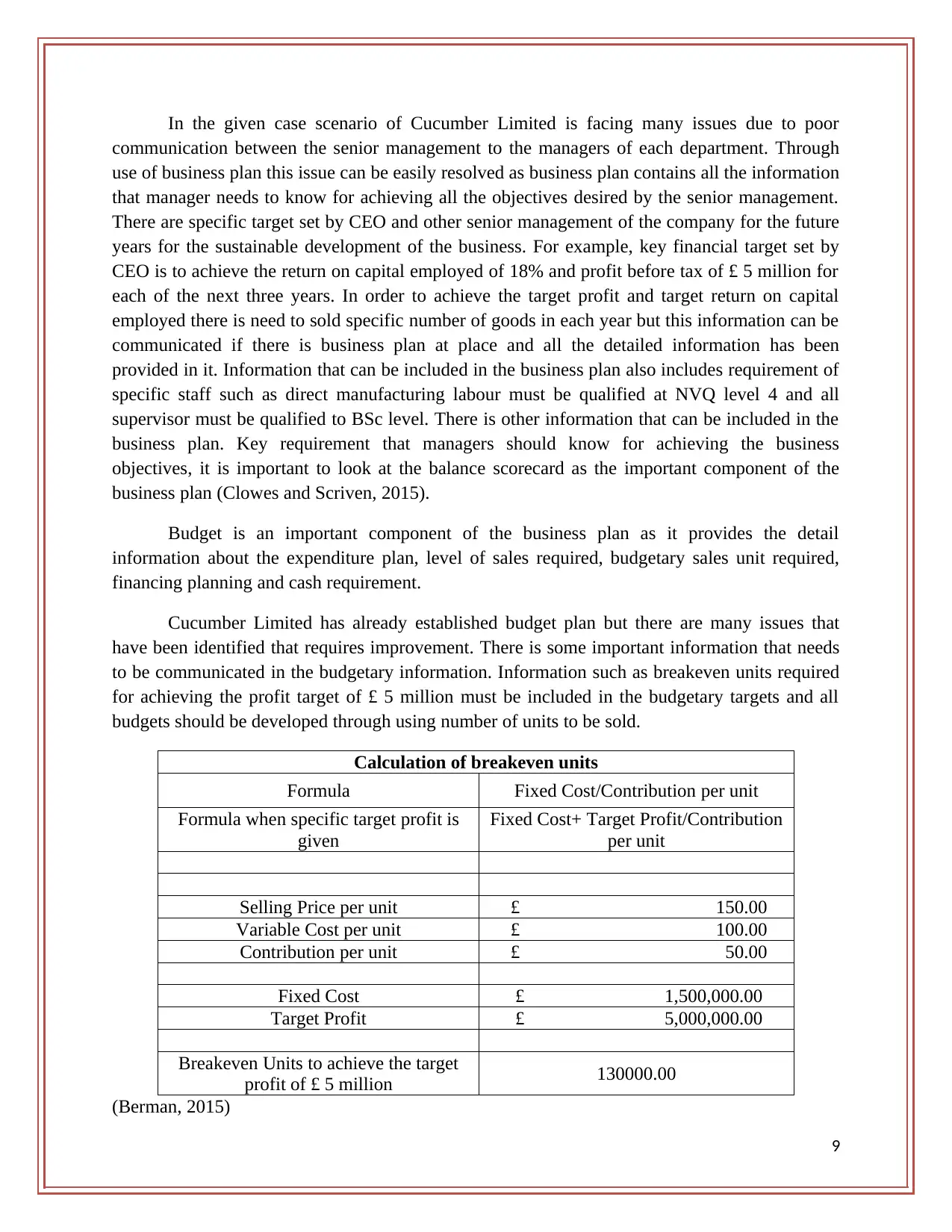

In the given case scenario of Cucumber Limited is facing many issues due to poor

communication between the senior management to the managers of each department. Through

use of business plan this issue can be easily resolved as business plan contains all the information

that manager needs to know for achieving all the objectives desired by the senior management.

There are specific target set by CEO and other senior management of the company for the future

years for the sustainable development of the business. For example, key financial target set by

CEO is to achieve the return on capital employed of 18% and profit before tax of £ 5 million for

each of the next three years. In order to achieve the target profit and target return on capital

employed there is need to sold specific number of goods in each year but this information can be

communicated if there is business plan at place and all the detailed information has been

provided in it. Information that can be included in the business plan also includes requirement of

specific staff such as direct manufacturing labour must be qualified at NVQ level 4 and all

supervisor must be qualified to BSc level. There is other information that can be included in the

business plan. Key requirement that managers should know for achieving the business

objectives, it is important to look at the balance scorecard as the important component of the

business plan (Clowes and Scriven, 2015).

Budget is an important component of the business plan as it provides the detail

information about the expenditure plan, level of sales required, budgetary sales unit required,

financing planning and cash requirement.

Cucumber Limited has already established budget plan but there are many issues that

have been identified that requires improvement. There is some important information that needs

to be communicated in the budgetary information. Information such as breakeven units required

for achieving the profit target of £ 5 million must be included in the budgetary targets and all

budgets should be developed through using number of units to be sold.

Calculation of breakeven units

Formula Fixed Cost/Contribution per unit

Formula when specific target profit is

given

Fixed Cost+ Target Profit/Contribution

per unit

Selling Price per unit £ 150.00

Variable Cost per unit £ 100.00

Contribution per unit £ 50.00

Fixed Cost £ 1,500,000.00

Target Profit £ 5,000,000.00

Breakeven Units to achieve the target

profit of £ 5 million 130000.00

(Berman, 2015)

9

communication between the senior management to the managers of each department. Through

use of business plan this issue can be easily resolved as business plan contains all the information

that manager needs to know for achieving all the objectives desired by the senior management.

There are specific target set by CEO and other senior management of the company for the future

years for the sustainable development of the business. For example, key financial target set by

CEO is to achieve the return on capital employed of 18% and profit before tax of £ 5 million for

each of the next three years. In order to achieve the target profit and target return on capital

employed there is need to sold specific number of goods in each year but this information can be

communicated if there is business plan at place and all the detailed information has been

provided in it. Information that can be included in the business plan also includes requirement of

specific staff such as direct manufacturing labour must be qualified at NVQ level 4 and all

supervisor must be qualified to BSc level. There is other information that can be included in the

business plan. Key requirement that managers should know for achieving the business

objectives, it is important to look at the balance scorecard as the important component of the

business plan (Clowes and Scriven, 2015).

Budget is an important component of the business plan as it provides the detail

information about the expenditure plan, level of sales required, budgetary sales unit required,

financing planning and cash requirement.

Cucumber Limited has already established budget plan but there are many issues that

have been identified that requires improvement. There is some important information that needs

to be communicated in the budgetary information. Information such as breakeven units required

for achieving the profit target of £ 5 million must be included in the budgetary targets and all

budgets should be developed through using number of units to be sold.

Calculation of breakeven units

Formula Fixed Cost/Contribution per unit

Formula when specific target profit is

given

Fixed Cost+ Target Profit/Contribution

per unit

Selling Price per unit £ 150.00

Variable Cost per unit £ 100.00

Contribution per unit £ 50.00

Fixed Cost £ 1,500,000.00

Target Profit £ 5,000,000.00

Breakeven Units to achieve the target

profit of £ 5 million 130000.00

(Berman, 2015)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Areas need to be improved in budgetary control process:

It is required to provide the variance report on 1 st day of next month for which report has

been prepared. For example, for month of September, report must be given on 1st

October.

Variance report must be adjusted for number of units sold in respective month

Below is the correct variance report for the September month:

Productive Activity Budget Budget Actual Variance

3000 4000

4,000

units

Costs £ £ £ %

Materials 31000 41333.33 39000 2333.33 Favorable 8%

Supplies 11000 14666.67 12500 2166.67 Favorable 20%

Direct Labour 9000 12000.00 9500 2500.00 Favorable 28%

Indirect labour 5000 6666.67 5200 1466.67 Favorable 29%

Depreciation 2000 2000.00 2000 0.00 0%

0.00

Share of Sales costs 2500 3333.33 2800 533.33 Favorable 21%

0.00

Apportioned overhead 10000 13333.33 15000 -1666.67 Adverse -17%

Total 70500 93333.33 86000 7333.33 Favorable 10%

(Adler, 2013)

Part 4: Critically discussion of the usefulness of Balanced Scorecard Approach and

development of Balance Scorecard for Cucumber Ltd

The Balance Scorecard (BSC) is regarded as a strategic planning and management tool

that can be used by businesses for measuring and monitoring their progress towards the

achievement of the strategic targets. It evaluates the performance of an organization on the basis

of four perspectives, that are, financial, customer, internal business and learning and growth

perspectives. The BSC approach can be used by organizations for developing the long-term

strategic goals and aligning them with short-term strategic plans. The business organizations can

develop their key performance indicators on the basis of strategic goals and objectives created

with the use of BSC approach. The businesses adopting the use of this management tool are also

bale to develop and report higher quality of information to the management for aiding their

decision-making. It can also enable the businesses to improve the transparency and reliability

within their management reports and ensuring that information provided is trustworthy for

developing the strategic plans of future business growth and development. It can also be

regarded as an effective way for visualizing the financial as well as non-financial performance of

a company before the senior management people and developing the long-term strategic goals.

10

It is required to provide the variance report on 1 st day of next month for which report has

been prepared. For example, for month of September, report must be given on 1st

October.

Variance report must be adjusted for number of units sold in respective month

Below is the correct variance report for the September month:

Productive Activity Budget Budget Actual Variance

3000 4000

4,000

units

Costs £ £ £ %

Materials 31000 41333.33 39000 2333.33 Favorable 8%

Supplies 11000 14666.67 12500 2166.67 Favorable 20%

Direct Labour 9000 12000.00 9500 2500.00 Favorable 28%

Indirect labour 5000 6666.67 5200 1466.67 Favorable 29%

Depreciation 2000 2000.00 2000 0.00 0%

0.00

Share of Sales costs 2500 3333.33 2800 533.33 Favorable 21%

0.00

Apportioned overhead 10000 13333.33 15000 -1666.67 Adverse -17%

Total 70500 93333.33 86000 7333.33 Favorable 10%

(Adler, 2013)

Part 4: Critically discussion of the usefulness of Balanced Scorecard Approach and

development of Balance Scorecard for Cucumber Ltd

The Balance Scorecard (BSC) is regarded as a strategic planning and management tool

that can be used by businesses for measuring and monitoring their progress towards the

achievement of the strategic targets. It evaluates the performance of an organization on the basis

of four perspectives, that are, financial, customer, internal business and learning and growth

perspectives. The BSC approach can be used by organizations for developing the long-term

strategic goals and aligning them with short-term strategic plans. The business organizations can

develop their key performance indicators on the basis of strategic goals and objectives created

with the use of BSC approach. The businesses adopting the use of this management tool are also

bale to develop and report higher quality of information to the management for aiding their

decision-making. It can also enable the businesses to improve the transparency and reliability

within their management reports and ensuring that information provided is trustworthy for

developing the strategic plans of future business growth and development. It can also be

regarded as an effective way for visualizing the financial as well as non-financial performance of

a company before the senior management people and developing the long-term strategic goals.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

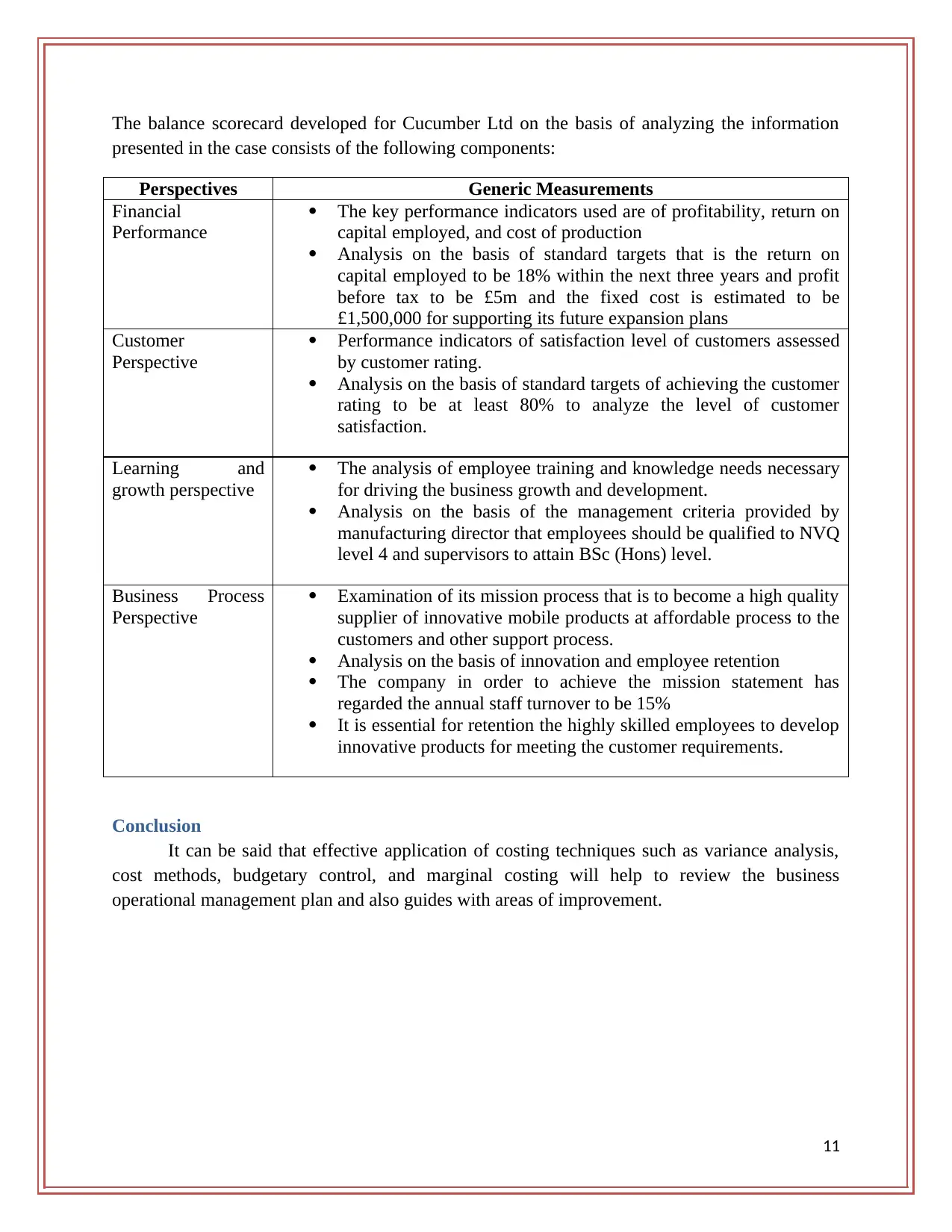

The balance scorecard developed for Cucumber Ltd on the basis of analyzing the information

presented in the case consists of the following components:

Perspectives Generic Measurements

Financial

Performance

The key performance indicators used are of profitability, return on

capital employed, and cost of production

Analysis on the basis of standard targets that is the return on

capital employed to be 18% within the next three years and profit

before tax to be £5m and the fixed cost is estimated to be

£1,500,000 for supporting its future expansion plans

Customer

Perspective

Performance indicators of satisfaction level of customers assessed

by customer rating.

Analysis on the basis of standard targets of achieving the customer

rating to be at least 80% to analyze the level of customer

satisfaction.

Learning and

growth perspective

The analysis of employee training and knowledge needs necessary

for driving the business growth and development.

Analysis on the basis of the management criteria provided by

manufacturing director that employees should be qualified to NVQ

level 4 and supervisors to attain BSc (Hons) level.

Business Process

Perspective

Examination of its mission process that is to become a high quality

supplier of innovative mobile products at affordable process to the

customers and other support process.

Analysis on the basis of innovation and employee retention

The company in order to achieve the mission statement has

regarded the annual staff turnover to be 15%

It is essential for retention the highly skilled employees to develop

innovative products for meeting the customer requirements.

Conclusion

It can be said that effective application of costing techniques such as variance analysis,

cost methods, budgetary control, and marginal costing will help to review the business

operational management plan and also guides with areas of improvement.

11

presented in the case consists of the following components:

Perspectives Generic Measurements

Financial

Performance

The key performance indicators used are of profitability, return on

capital employed, and cost of production

Analysis on the basis of standard targets that is the return on

capital employed to be 18% within the next three years and profit

before tax to be £5m and the fixed cost is estimated to be

£1,500,000 for supporting its future expansion plans

Customer

Perspective

Performance indicators of satisfaction level of customers assessed

by customer rating.

Analysis on the basis of standard targets of achieving the customer

rating to be at least 80% to analyze the level of customer

satisfaction.

Learning and

growth perspective

The analysis of employee training and knowledge needs necessary

for driving the business growth and development.

Analysis on the basis of the management criteria provided by

manufacturing director that employees should be qualified to NVQ

level 4 and supervisors to attain BSc (Hons) level.

Business Process

Perspective

Examination of its mission process that is to become a high quality

supplier of innovative mobile products at affordable process to the

customers and other support process.

Analysis on the basis of innovation and employee retention

The company in order to achieve the mission statement has

regarded the annual staff turnover to be 15%

It is essential for retention the highly skilled employees to develop

innovative products for meeting the customer requirements.

Conclusion

It can be said that effective application of costing techniques such as variance analysis,

cost methods, budgetary control, and marginal costing will help to review the business

operational management plan and also guides with areas of improvement.

11

References

Adler, R. 2013. Management Accounting. UK: Routledge.

Berman, K. 2015. Financial Planning, Budgeting, and Forecasting: Financial Intelligence

Collection. UK: Harvard Business Review Press.

Clowes, R. and Scriven, V. 2015. Budgeting: A Practical Approach. Pearson Higher Education

AU.

Lalli, W. 2011. Handbook of Budgeting. US: John Wiley & Sons.

McWatters, C., and Zimmerman, J. 2015. Management Accounting in a Dynamic Environment.

UK: Routledge.

Moles, P. and Kidwekk, D. 2011. Corporate finance. US: John Wiley &sons.

Rasmussen, N. et al. 2013. Process Improvement for Effective Budgeting and Financial

Reporting. US: John Wiley & Sons.

Scheller-Kreinsen, D. and Geissler, A. 2017. The ABC of DRGs. Euro Observer 11(4), pp. 1-5.

Shim, J.K., Siegel, J.G. and Shim, A.L. 2011. Budgeting Basics and Beyond. US: John Wiley &

Sons.

Tănase, G.L. 2013. An Overall Analysis of Participatory Budgeting: Advantages and Essential

Factors for an Effective Implementation in Economic Entities. Journal of Eastern Europe

Research in Business and Economics.

Vanderbeck, E. 2012. Principles of Cost Accounting. Cengage Learning.

12

Adler, R. 2013. Management Accounting. UK: Routledge.

Berman, K. 2015. Financial Planning, Budgeting, and Forecasting: Financial Intelligence

Collection. UK: Harvard Business Review Press.

Clowes, R. and Scriven, V. 2015. Budgeting: A Practical Approach. Pearson Higher Education

AU.

Lalli, W. 2011. Handbook of Budgeting. US: John Wiley & Sons.

McWatters, C., and Zimmerman, J. 2015. Management Accounting in a Dynamic Environment.

UK: Routledge.

Moles, P. and Kidwekk, D. 2011. Corporate finance. US: John Wiley &sons.

Rasmussen, N. et al. 2013. Process Improvement for Effective Budgeting and Financial

Reporting. US: John Wiley & Sons.

Scheller-Kreinsen, D. and Geissler, A. 2017. The ABC of DRGs. Euro Observer 11(4), pp. 1-5.

Shim, J.K., Siegel, J.G. and Shim, A.L. 2011. Budgeting Basics and Beyond. US: John Wiley &

Sons.

Tănase, G.L. 2013. An Overall Analysis of Participatory Budgeting: Advantages and Essential

Factors for an Effective Implementation in Economic Entities. Journal of Eastern Europe

Research in Business and Economics.

Vanderbeck, E. 2012. Principles of Cost Accounting. Cengage Learning.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.