Management Accounting: Techniques, Budgeting, Pricing, Costing, and Strategic Position

VerifiedAdded on 2023/01/10

|12

|2644

|24

AI Summary

This report discusses the usefulness of management accounting in evaluating business aspects and making crucial decisions. It covers microeconomic techniques, product costing, income statement using marginal and absorption costing, budgeting, pricing, costing, and strategic position. The report also compares different management accounting systems used by organizations to resolve financial problems.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................3

Microeconomic techniques.........................................................................................................3

Product costing............................................................................................................................4

Income statement using marginal and absorption costing..........................................................4

LO 3.................................................................................................................................................6

Budget.........................................................................................................................................6

Pricing.........................................................................................................................................7

Costing........................................................................................................................................8

Strategic Position........................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................3

Microeconomic techniques.........................................................................................................3

Product costing............................................................................................................................4

Income statement using marginal and absorption costing..........................................................4

LO 3.................................................................................................................................................6

Budget.........................................................................................................................................6

Pricing.........................................................................................................................................7

Costing........................................................................................................................................8

Strategic Position........................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is utilized by the organization for the purpose of evaluating the

various business aspect which are used by the business for the purpose of taking crucial business

decisions. This report presents about the usefulness of MA along with its techniques and

systems. It also covers the different planning tools for exercising budgetary control and ways

through which business can respond to its financial problems.

TASK 1

Covered in ppt.

TASK 2

Microeconomic techniques

Cost: It refers to money value that the company spent for the purpose of producing something. It

does not include the profit element (Collis and Hussey, 2017).

Different types of cost

Fixed cost: It is the periodic cost which remains stable irrespective of change in the level

of activity. At zero level of production, the fixed cost will incur.

Variable cost: This cost varies with the variation in the production volume. In case of no

production, the variable cost will be zero.

Cost allocation: It is the process of aggregating the cost and assigning it to the costs

objects. The cost object is the activity for which the cost is measured separately.

Cost analysis:

It used in comparing the cost with respect to the output which helps in taking decision

with respect to cost control.

Cost-volume profit

It is used to determine how the change in the cost and volume of the organization will

affect the company's operating income.

Flexible budgeting

Under this, the budget is very flexible as it adjusts with the change in the level of activity.

Thus, in between changes in the budget can be easily made.

Cost variances

It refers to the difference in the actual amount of the cost and the cost that was planned.

Management accounting is utilized by the organization for the purpose of evaluating the

various business aspect which are used by the business for the purpose of taking crucial business

decisions. This report presents about the usefulness of MA along with its techniques and

systems. It also covers the different planning tools for exercising budgetary control and ways

through which business can respond to its financial problems.

TASK 1

Covered in ppt.

TASK 2

Microeconomic techniques

Cost: It refers to money value that the company spent for the purpose of producing something. It

does not include the profit element (Collis and Hussey, 2017).

Different types of cost

Fixed cost: It is the periodic cost which remains stable irrespective of change in the level

of activity. At zero level of production, the fixed cost will incur.

Variable cost: This cost varies with the variation in the production volume. In case of no

production, the variable cost will be zero.

Cost allocation: It is the process of aggregating the cost and assigning it to the costs

objects. The cost object is the activity for which the cost is measured separately.

Cost analysis:

It used in comparing the cost with respect to the output which helps in taking decision

with respect to cost control.

Cost-volume profit

It is used to determine how the change in the cost and volume of the organization will

affect the company's operating income.

Flexible budgeting

Under this, the budget is very flexible as it adjusts with the change in the level of activity.

Thus, in between changes in the budget can be easily made.

Cost variances

It refers to the difference in the actual amount of the cost and the cost that was planned.

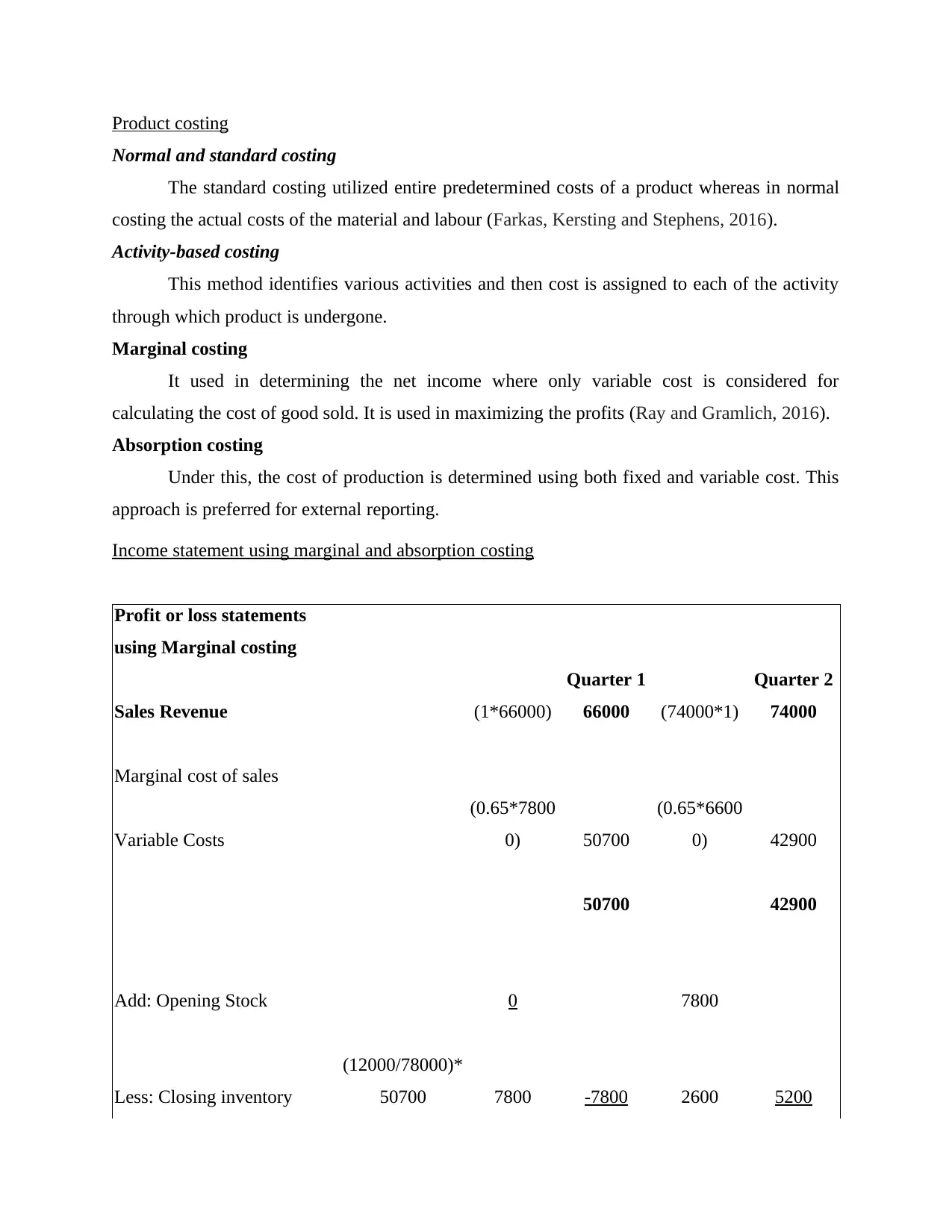

Product costing

Normal and standard costing

The standard costing utilized entire predetermined costs of a product whereas in normal

costing the actual costs of the material and labour (Farkas, Kersting and Stephens, 2016).

Activity-based costing

This method identifies various activities and then cost is assigned to each of the activity

through which product is undergone.

Marginal costing

It used in determining the net income where only variable cost is considered for

calculating the cost of good sold. It is used in maximizing the profits (Ray and Gramlich, 2016).

Absorption costing

Under this, the cost of production is determined using both fixed and variable cost. This

approach is preferred for external reporting.

Income statement using marginal and absorption costing

Profit or loss statements

using Marginal costing

Quarter 1 Quarter 2

Sales Revenue (1*66000) 66000 (74000*1) 74000

Marginal cost of sales

Variable Costs

(0.65*7800

0) 50700

(0.65*6600

0) 42900

50700 42900

Add: Opening Stock 0 7800

Less: Closing inventory

(12000/78000)*

50700 7800 -7800 2600 5200

Normal and standard costing

The standard costing utilized entire predetermined costs of a product whereas in normal

costing the actual costs of the material and labour (Farkas, Kersting and Stephens, 2016).

Activity-based costing

This method identifies various activities and then cost is assigned to each of the activity

through which product is undergone.

Marginal costing

It used in determining the net income where only variable cost is considered for

calculating the cost of good sold. It is used in maximizing the profits (Ray and Gramlich, 2016).

Absorption costing

Under this, the cost of production is determined using both fixed and variable cost. This

approach is preferred for external reporting.

Income statement using marginal and absorption costing

Profit or loss statements

using Marginal costing

Quarter 1 Quarter 2

Sales Revenue (1*66000) 66000 (74000*1) 74000

Marginal cost of sales

Variable Costs

(0.65*7800

0) 50700

(0.65*6600

0) 42900

50700 42900

Add: Opening Stock 0 7800

Less: Closing inventory

(12000/78000)*

50700 7800 -7800 2600 5200

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

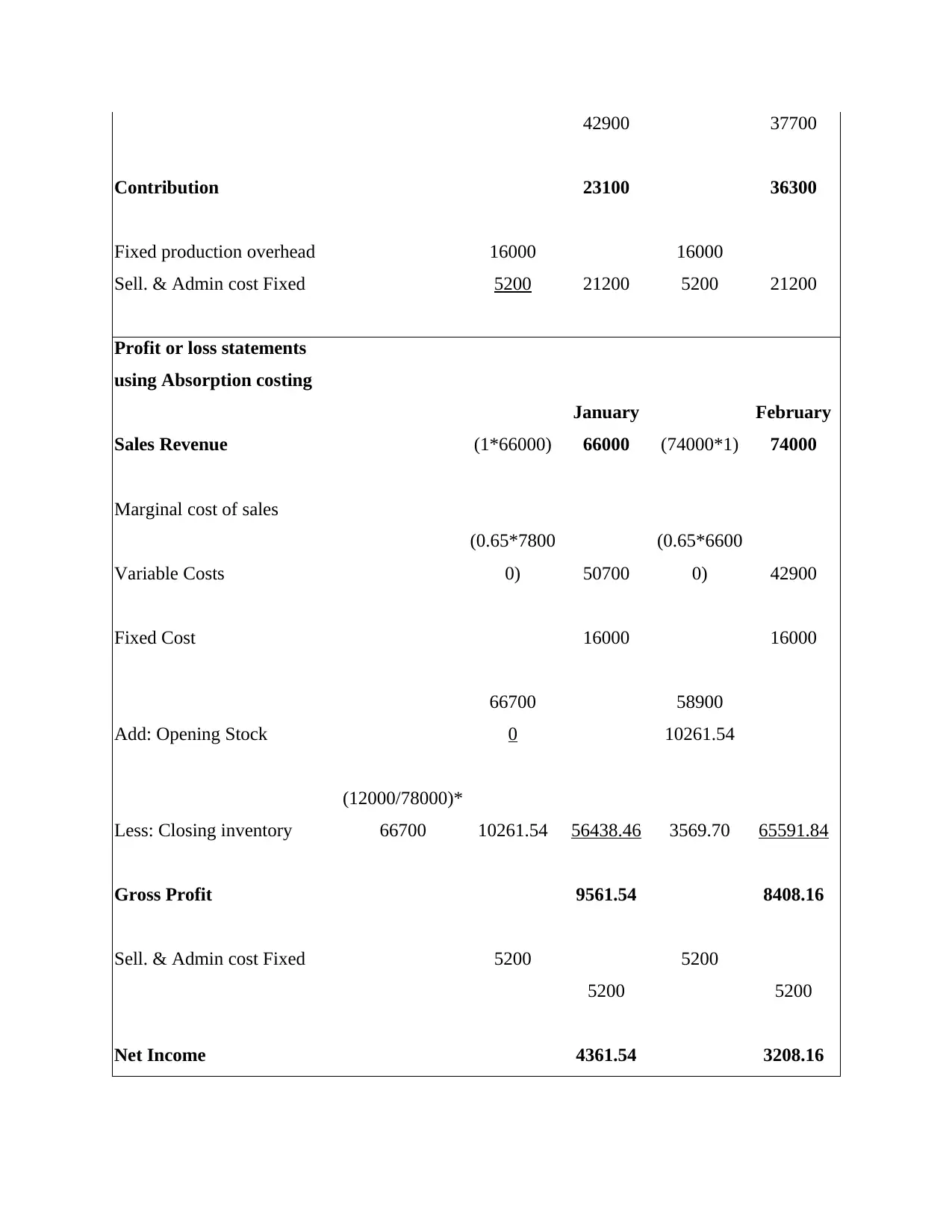

42900 37700

Contribution 23100 36300

Fixed production overhead 16000 16000

Sell. & Admin cost Fixed 5200 21200 5200 21200

Profit or loss statements

using Absorption costing

January February

Sales Revenue (1*66000) 66000 (74000*1) 74000

Marginal cost of sales

Variable Costs

(0.65*7800

0) 50700

(0.65*6600

0) 42900

Fixed Cost 16000 16000

66700 58900

Add: Opening Stock 0 10261.54

Less: Closing inventory

(12000/78000)*

66700 10261.54 56438.46 3569.70 65591.84

Gross Profit 9561.54 8408.16

Sell. & Admin cost Fixed 5200 5200

5200 5200

Net Income 4361.54 3208.16

Contribution 23100 36300

Fixed production overhead 16000 16000

Sell. & Admin cost Fixed 5200 21200 5200 21200

Profit or loss statements

using Absorption costing

January February

Sales Revenue (1*66000) 66000 (74000*1) 74000

Marginal cost of sales

Variable Costs

(0.65*7800

0) 50700

(0.65*6600

0) 42900

Fixed Cost 16000 16000

66700 58900

Add: Opening Stock 0 10261.54

Less: Closing inventory

(12000/78000)*

66700 10261.54 56438.46 3569.70 65591.84

Gross Profit 9561.54 8408.16

Sell. & Admin cost Fixed 5200 5200

5200 5200

Net Income 4361.54 3208.16

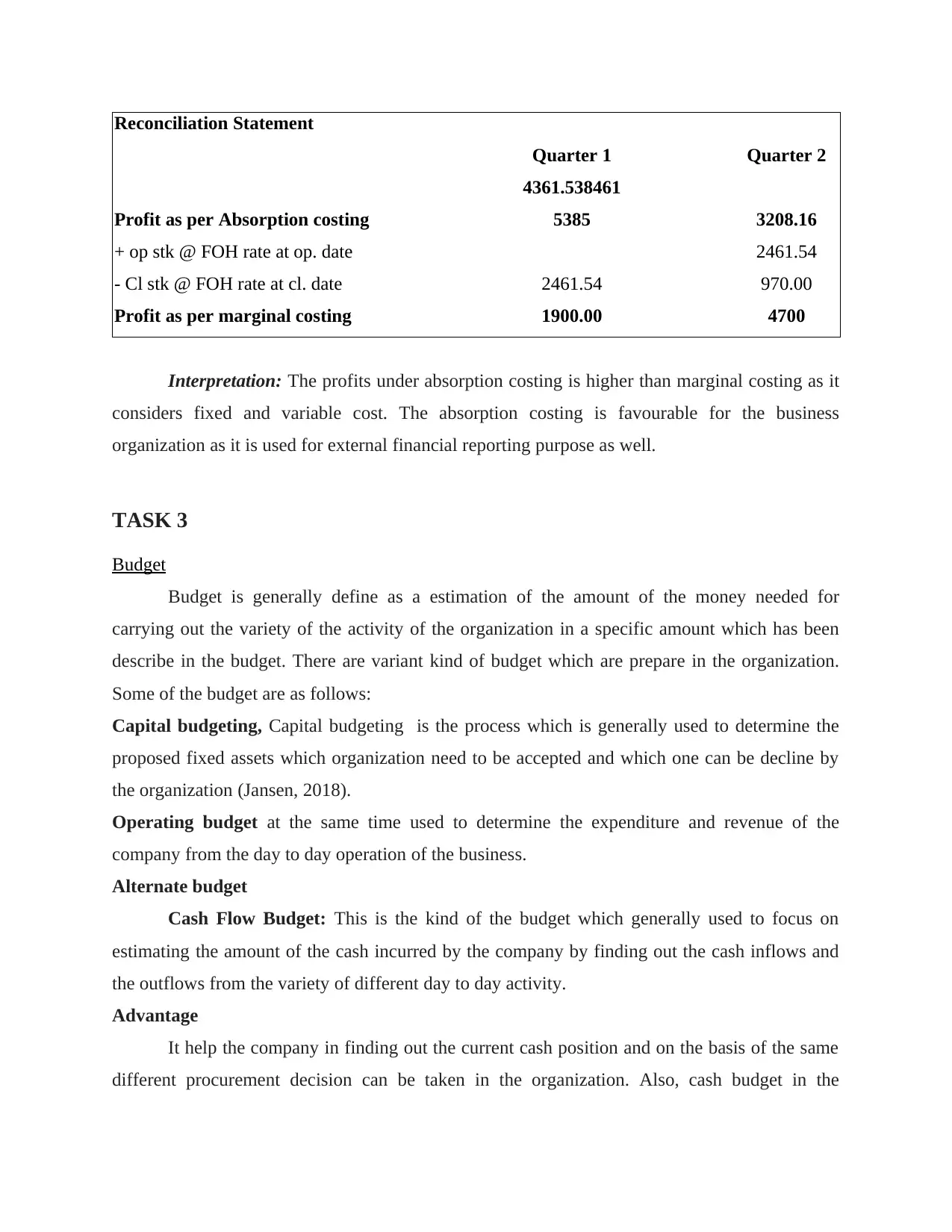

Reconciliation Statement

Quarter 1 Quarter 2

Profit as per Absorption costing

4361.538461

5385 3208.16

+ op stk @ FOH rate at op. date 2461.54

- Cl stk @ FOH rate at cl. date 2461.54 970.00

Profit as per marginal costing 1900.00 4700

Interpretation: The profits under absorption costing is higher than marginal costing as it

considers fixed and variable cost. The absorption costing is favourable for the business

organization as it is used for external financial reporting purpose as well.

TASK 3

Budget

Budget is generally define as a estimation of the amount of the money needed for

carrying out the variety of the activity of the organization in a specific amount which has been

describe in the budget. There are variant kind of budget which are prepare in the organization.

Some of the budget are as follows:

Capital budgeting, Capital budgeting is the process which is generally used to determine the

proposed fixed assets which organization need to be accepted and which one can be decline by

the organization (Jansen, 2018).

Operating budget at the same time used to determine the expenditure and revenue of the

company from the day to day operation of the business.

Alternate budget

Cash Flow Budget: This is the kind of the budget which generally used to focus on

estimating the amount of the cash incurred by the company by finding out the cash inflows and

the outflows from the variety of different day to day activity.

Advantage

It help the company in finding out the current cash position and on the basis of the same

different procurement decision can be taken in the organization. Also, cash budget in the

Quarter 1 Quarter 2

Profit as per Absorption costing

4361.538461

5385 3208.16

+ op stk @ FOH rate at op. date 2461.54

- Cl stk @ FOH rate at cl. date 2461.54 970.00

Profit as per marginal costing 1900.00 4700

Interpretation: The profits under absorption costing is higher than marginal costing as it

considers fixed and variable cost. The absorption costing is favourable for the business

organization as it is used for external financial reporting purpose as well.

TASK 3

Budget

Budget is generally define as a estimation of the amount of the money needed for

carrying out the variety of the activity of the organization in a specific amount which has been

describe in the budget. There are variant kind of budget which are prepare in the organization.

Some of the budget are as follows:

Capital budgeting, Capital budgeting is the process which is generally used to determine the

proposed fixed assets which organization need to be accepted and which one can be decline by

the organization (Jansen, 2018).

Operating budget at the same time used to determine the expenditure and revenue of the

company from the day to day operation of the business.

Alternate budget

Cash Flow Budget: This is the kind of the budget which generally used to focus on

estimating the amount of the cash incurred by the company by finding out the cash inflows and

the outflows from the variety of different day to day activity.

Advantage

It help the company in finding out the current cash position and on the basis of the same

different procurement decision can be taken in the organization. Also, cash budget in the

organization used to help the company at the time of taking any sort of the loan in the

organization.

Disadvantage

It can manipulate the interest of the employee as employee can change the level of

interest by seeing the surplus of cash in the organization (Malina, 2018).

Production budget: It is type of the budget which is generally prepare in the

organization to track the amount of the product which has been produce in the organization, this

budget is generally made on the basis of the sales budget of the company. As sales budget are

prepare on basis of production budget.

Advantage

This budget in the organization used to help the company in setting up the basis on the

basis of the same different budget are form such as sales budget and cash flow budget in the

organization.

Disadvantages

If the budget which is prepare in the organization is inappropriate it generally used to

create the variety of the different type of the issue for the organization (Mack and Goretzki,

2017). As production is important task and if there is some sort of incorporation of production

budget then it used to impact the efficiency of variety of the task which has been performed.

Zero Based budgeting: It is the type of the budget in the organization which used to not

consider the past at the time of preparing the budget in the organization. As in this type of the

budget all the time the budget is generally started from the zero in the organization.

Advantage

This sort of the budget in the organization used to increases the chances of finding out the

appropriate outcome. Reason behind the same is identified that it help the organization in

improving the element which was neglected at the time of constructing the budget in the past.

Disadvantage

Disadvantage of this type of the budget is that it is very time consuming as compare to

the other form of the budget (Messner, 2016).

Behavioural budget

organization.

Disadvantage

It can manipulate the interest of the employee as employee can change the level of

interest by seeing the surplus of cash in the organization (Malina, 2018).

Production budget: It is type of the budget which is generally prepare in the

organization to track the amount of the product which has been produce in the organization, this

budget is generally made on the basis of the sales budget of the company. As sales budget are

prepare on basis of production budget.

Advantage

This budget in the organization used to help the company in setting up the basis on the

basis of the same different budget are form such as sales budget and cash flow budget in the

organization.

Disadvantages

If the budget which is prepare in the organization is inappropriate it generally used to

create the variety of the different type of the issue for the organization (Mack and Goretzki,

2017). As production is important task and if there is some sort of incorporation of production

budget then it used to impact the efficiency of variety of the task which has been performed.

Zero Based budgeting: It is the type of the budget in the organization which used to not

consider the past at the time of preparing the budget in the organization. As in this type of the

budget all the time the budget is generally started from the zero in the organization.

Advantage

This sort of the budget in the organization used to increases the chances of finding out the

appropriate outcome. Reason behind the same is identified that it help the organization in

improving the element which was neglected at the time of constructing the budget in the past.

Disadvantage

Disadvantage of this type of the budget is that it is very time consuming as compare to

the other form of the budget (Messner, 2016).

Behavioural budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Manager who is participating in the process of budget making has to make sure that they used to

be fair to the business and also used to take the honest decision as any bias decision in the

process of budget making will create good sort of the issue for the firm to overcome.

Pricing

Pricing strategy

Prime furniture used to use the skimming pricing method, in which rate of different

product are kept low at initial stage and after seeing the response rate of the product are generally

increased (Mills, 2018).

Competitor pricing

Competitor in the market used to determine the price of the product by generally adding

the profit margin of the company with the cost which has been incurred by the organization in

producing the product of the company in the market.

Supply and demand consideration

At the time of setting up the price of variety of the different product supply and demand

are also consider. As if demand of the company product is high that profit margin is kept high.

At the same time if supply is high profit margin is kept low (Maskell and et.al., 2016).

Costing

Costing system

Actual costing is system which used the direct cost such as direct cost and actual qualities

used in production to determine the cost of specific products..

Normal costing at the same time is the system which is generally used in the derivation of

costing. In this actual cost is used with the exception of manufacturing overhead.

Standard costing system is generally used to standard cost which is budgeted or the

estimated cost for a single unit of product.

Difference in cost

Reason behind the difference is that all the costing system used to consider different basis of

calculation. As job costing used to consider the cost of carrying out job. Process costing used to

consider the cost of process. Batch costing used to consider the batch and contract costing used t

consider the contract.

be fair to the business and also used to take the honest decision as any bias decision in the

process of budget making will create good sort of the issue for the firm to overcome.

Pricing

Pricing strategy

Prime furniture used to use the skimming pricing method, in which rate of different

product are kept low at initial stage and after seeing the response rate of the product are generally

increased (Mills, 2018).

Competitor pricing

Competitor in the market used to determine the price of the product by generally adding

the profit margin of the company with the cost which has been incurred by the organization in

producing the product of the company in the market.

Supply and demand consideration

At the time of setting up the price of variety of the different product supply and demand

are also consider. As if demand of the company product is high that profit margin is kept high.

At the same time if supply is high profit margin is kept low (Maskell and et.al., 2016).

Costing

Costing system

Actual costing is system which used the direct cost such as direct cost and actual qualities

used in production to determine the cost of specific products..

Normal costing at the same time is the system which is generally used in the derivation of

costing. In this actual cost is used with the exception of manufacturing overhead.

Standard costing system is generally used to standard cost which is budgeted or the

estimated cost for a single unit of product.

Difference in cost

Reason behind the difference is that all the costing system used to consider different basis of

calculation. As job costing used to consider the cost of carrying out job. Process costing used to

consider the cost of process. Batch costing used to consider the batch and contract costing used t

consider the contract.

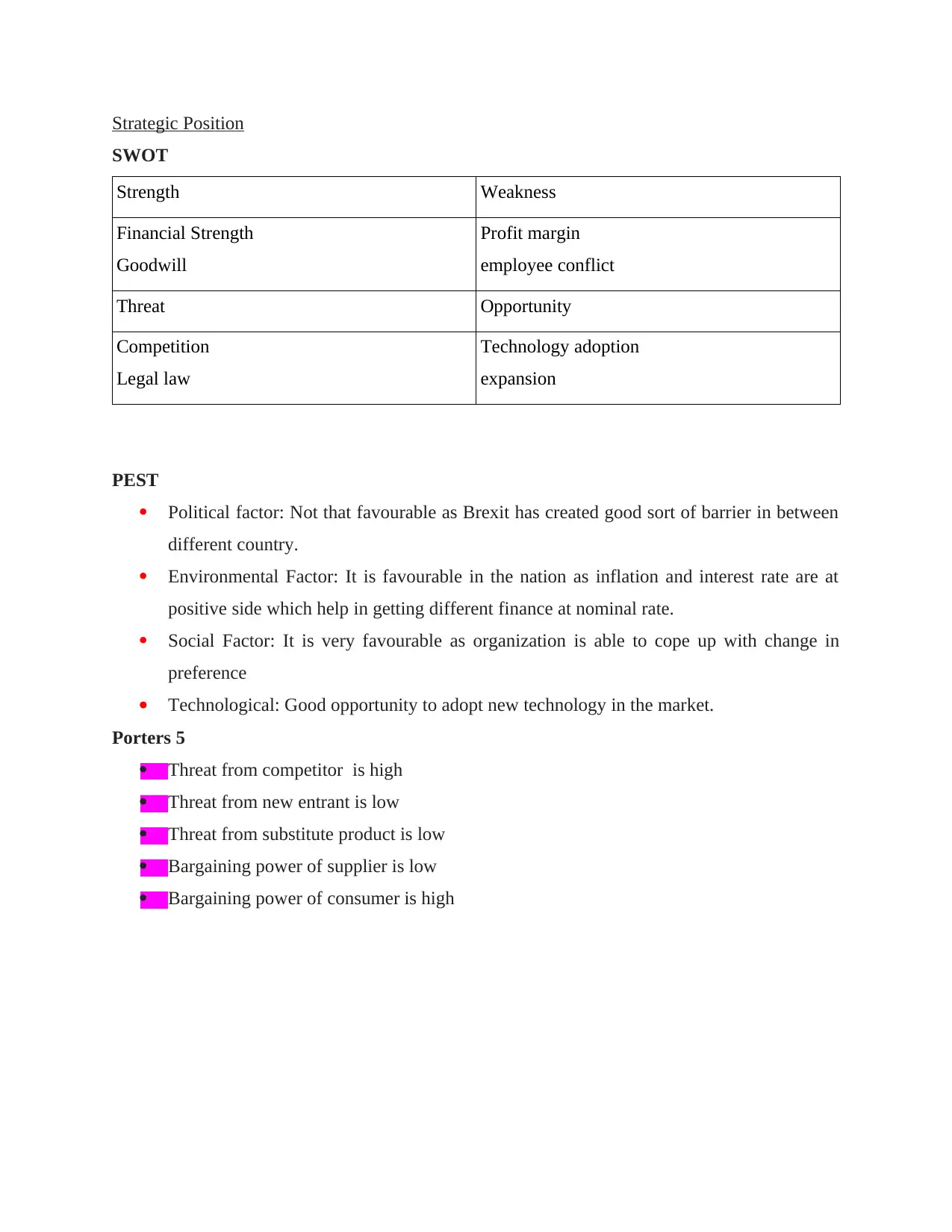

Strategic Position

SWOT

Strength Weakness

Financial Strength

Goodwill

Profit margin

employee conflict

Threat Opportunity

Competition

Legal law

Technology adoption

expansion

PEST

Political factor: Not that favourable as Brexit has created good sort of barrier in between

different country.

Environmental Factor: It is favourable in the nation as inflation and interest rate are at

positive side which help in getting different finance at nominal rate.

Social Factor: It is very favourable as organization is able to cope up with change in

preference

Technological: Good opportunity to adopt new technology in the market.

Porters 5

Threat from competitor is high

Threat from new entrant is low

Threat from substitute product is low

Bargaining power of supplier is low

Bargaining power of consumer is high

SWOT

Strength Weakness

Financial Strength

Goodwill

Profit margin

employee conflict

Threat Opportunity

Competition

Legal law

Technology adoption

expansion

PEST

Political factor: Not that favourable as Brexit has created good sort of barrier in between

different country.

Environmental Factor: It is favourable in the nation as inflation and interest rate are at

positive side which help in getting different finance at nominal rate.

Social Factor: It is very favourable as organization is able to cope up with change in

preference

Technological: Good opportunity to adopt new technology in the market.

Porters 5

Threat from competitor is high

Threat from new entrant is low

Threat from substitute product is low

Bargaining power of supplier is low

Bargaining power of consumer is high

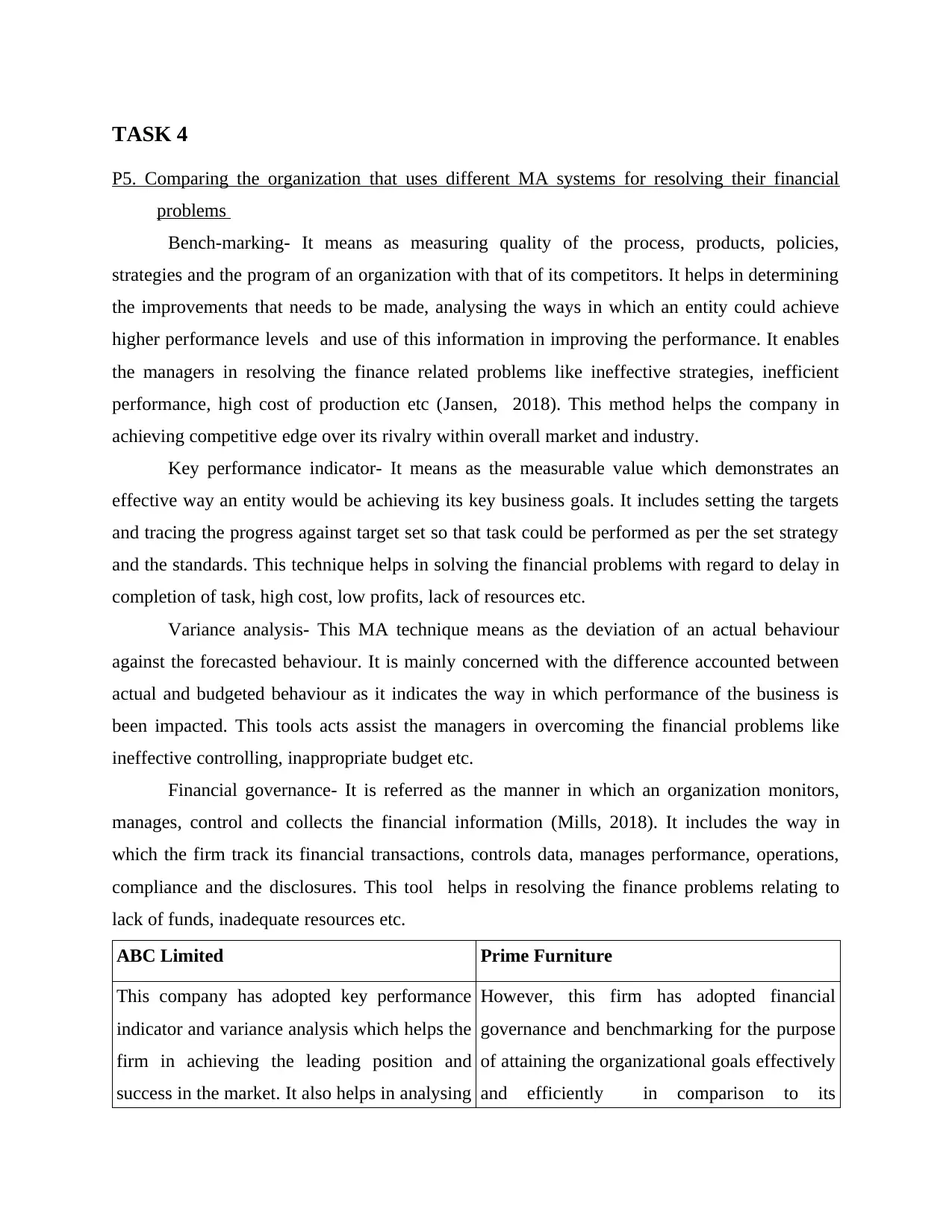

TASK 4

P5. Comparing the organization that uses different MA systems for resolving their financial

problems

Bench-marking- It means as measuring quality of the process, products, policies,

strategies and the program of an organization with that of its competitors. It helps in determining

the improvements that needs to be made, analysing the ways in which an entity could achieve

higher performance levels and use of this information in improving the performance. It enables

the managers in resolving the finance related problems like ineffective strategies, inefficient

performance, high cost of production etc (Jansen, 2018). This method helps the company in

achieving competitive edge over its rivalry within overall market and industry.

Key performance indicator- It means as the measurable value which demonstrates an

effective way an entity would be achieving its key business goals. It includes setting the targets

and tracing the progress against target set so that task could be performed as per the set strategy

and the standards. This technique helps in solving the financial problems with regard to delay in

completion of task, high cost, low profits, lack of resources etc.

Variance analysis- This MA technique means as the deviation of an actual behaviour

against the forecasted behaviour. It is mainly concerned with the difference accounted between

actual and budgeted behaviour as it indicates the way in which performance of the business is

been impacted. This tools acts assist the managers in overcoming the financial problems like

ineffective controlling, inappropriate budget etc.

Financial governance- It is referred as the manner in which an organization monitors,

manages, control and collects the financial information (Mills, 2018). It includes the way in

which the firm track its financial transactions, controls data, manages performance, operations,

compliance and the disclosures. This tool helps in resolving the finance problems relating to

lack of funds, inadequate resources etc.

ABC Limited Prime Furniture

This company has adopted key performance

indicator and variance analysis which helps the

firm in achieving the leading position and

success in the market. It also helps in analysing

However, this firm has adopted financial

governance and benchmarking for the purpose

of attaining the organizational goals effectively

and efficiently in comparison to its

P5. Comparing the organization that uses different MA systems for resolving their financial

problems

Bench-marking- It means as measuring quality of the process, products, policies,

strategies and the program of an organization with that of its competitors. It helps in determining

the improvements that needs to be made, analysing the ways in which an entity could achieve

higher performance levels and use of this information in improving the performance. It enables

the managers in resolving the finance related problems like ineffective strategies, inefficient

performance, high cost of production etc (Jansen, 2018). This method helps the company in

achieving competitive edge over its rivalry within overall market and industry.

Key performance indicator- It means as the measurable value which demonstrates an

effective way an entity would be achieving its key business goals. It includes setting the targets

and tracing the progress against target set so that task could be performed as per the set strategy

and the standards. This technique helps in solving the financial problems with regard to delay in

completion of task, high cost, low profits, lack of resources etc.

Variance analysis- This MA technique means as the deviation of an actual behaviour

against the forecasted behaviour. It is mainly concerned with the difference accounted between

actual and budgeted behaviour as it indicates the way in which performance of the business is

been impacted. This tools acts assist the managers in overcoming the financial problems like

ineffective controlling, inappropriate budget etc.

Financial governance- It is referred as the manner in which an organization monitors,

manages, control and collects the financial information (Mills, 2018). It includes the way in

which the firm track its financial transactions, controls data, manages performance, operations,

compliance and the disclosures. This tool helps in resolving the finance problems relating to

lack of funds, inadequate resources etc.

ABC Limited Prime Furniture

This company has adopted key performance

indicator and variance analysis which helps the

firm in achieving the leading position and

success in the market. It also helps in analysing

However, this firm has adopted financial

governance and benchmarking for the purpose

of attaining the organizational goals effectively

and efficiently in comparison to its

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the gap present between the actual and the

budgeted performance.

competitors and track its financial

performance.

Features of effective management accountant

Management accountant is considered as an important person in each aspect of an entity

who plays crucial role in framing policy & fixing the procedures, preparing budgets, determining

future action course. He must have an ability to grasp the views or perception of the management

on quick basis and should have the detailed knowledge about the principles of the management.

He also has an ability for thinking & exchanging the opinions with the top executives regarding

issues that emphasize on growth & profitability of an enterprise (Ray and Gramlich, 2016). The

accountant guides the workers in relation to performing the specific task and must also have the

responsibility to resolve the financial problems or any other kind of problem which is been faced

by the staff within the premises.

budgeted performance.

competitors and track its financial

performance.

Features of effective management accountant

Management accountant is considered as an important person in each aspect of an entity

who plays crucial role in framing policy & fixing the procedures, preparing budgets, determining

future action course. He must have an ability to grasp the views or perception of the management

on quick basis and should have the detailed knowledge about the principles of the management.

He also has an ability for thinking & exchanging the opinions with the top executives regarding

issues that emphasize on growth & profitability of an enterprise (Ray and Gramlich, 2016). The

accountant guides the workers in relation to performing the specific task and must also have the

responsibility to resolve the financial problems or any other kind of problem which is been faced

by the staff within the premises.

REFERENCES

Books and Journals

Jansen, E. P., 2018. Bridging the gap between theory and practice in management accounting:

Reviewing the literature to shape interventions. Accounting, Auditing & Accountability

Journal. 31(5). pp.1486-1509.

Mack, S. and Goretzki, L., 2017. How management accountants exert influence on managers–a

micro-level analysis of management accountants’ influence tactics in budgetary control

meetings. Qualitative Research in Accounting & Management.14(3). pp.328-362.

Malina, M. A. ed., 2018. Advances in management accounting. Emerald Publishing Limited.

Maskell and et.al., 2016. Practical lean accounting: a proven system for measuring and

managing the lean enterprise. Productivity Press.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Mills, D., 2018. Financial Reporting: A Case Study Analysis (Doctoral dissertation, The

University of Mississippi).

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education. 35.

pp.56-68.

Ray, K. and Gramlich, J., 2016. Reconciling full-cost and marginal-cost pricing. Journal of

Management Accounting Research. 28(1). pp.27-37.

Books and Journals

Jansen, E. P., 2018. Bridging the gap between theory and practice in management accounting:

Reviewing the literature to shape interventions. Accounting, Auditing & Accountability

Journal. 31(5). pp.1486-1509.

Mack, S. and Goretzki, L., 2017. How management accountants exert influence on managers–a

micro-level analysis of management accountants’ influence tactics in budgetary control

meetings. Qualitative Research in Accounting & Management.14(3). pp.328-362.

Malina, M. A. ed., 2018. Advances in management accounting. Emerald Publishing Limited.

Maskell and et.al., 2016. Practical lean accounting: a proven system for measuring and

managing the lean enterprise. Productivity Press.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Mills, D., 2018. Financial Reporting: A Case Study Analysis (Doctoral dissertation, The

University of Mississippi).

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education. 35.

pp.56-68.

Ray, K. and Gramlich, J., 2016. Reconciling full-cost and marginal-cost pricing. Journal of

Management Accounting Research. 28(1). pp.27-37.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.