Management Accounting Systems and Reports in Excite Entertainment Ltd

VerifiedAdded on 2023/01/18

|16

|4608

|77

AI Summary

This article discusses the management accounting systems and reports used in Excite Entertainment Ltd, including inventory management, cost accounting, job costing, and various managerial accounting reports. It also evaluates the integration of these systems within the company's operational processes.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...............................................................................................................3

TASK 1 ..............................................................................................................................3

Section (A)......................................................................................................................3

Section (B)......................................................................................................................5

TASK 2...............................................................................................................................8

TASK 3.............................................................................................................................10

Section (A) ...................................................................................................................10

TASK 4.............................................................................................................................12

Section (B)....................................................................................................................12

Calculations:....................................................................................................................13

CONCLUSION.................................................................................................................14

REFERENCES................................................................................................................15

INTRODUCTION...............................................................................................................3

TASK 1 ..............................................................................................................................3

Section (A)......................................................................................................................3

Section (B)......................................................................................................................5

TASK 2...............................................................................................................................8

TASK 3.............................................................................................................................10

Section (A) ...................................................................................................................10

TASK 4.............................................................................................................................12

Section (B)....................................................................................................................12

Calculations:....................................................................................................................13

CONCLUSION.................................................................................................................14

REFERENCES................................................................................................................15

INTRODUCTION

The management accounting is a systematic accounting approach which is

assigned in process of gathering financial and non financial data of business entities in

order to prepare internal reports (O’Grady, Morlidge and Rouse, 2016). These reports

are widely used by different kinds of department of business entities for better

management of various kind of activities and operations. The basic aim of project report

is to demonstrate understanding about detailed concept of MA. The project report is

based on Excite entertainment limited company which operates in entertainment sector.

The company is located in United Kingdom. The project report covers about different

kinds of management accounting systems (MAS), MA reports and budgets. Along with

role of various kind of MAS is demonstrated under the project report in detailed manner.

TASK 1

Section (A)

(a) Comparison between MA and financial accounting:

Basis MA Financial accounting

Data gathered In this accounting both kinds of

data is gathered by accountants

including monetary and non

monetary.

On the other hand, in this

accounting only monetary data is

gathered.

Outcome This accounting is being applied by

business entities in order to

produce internal reports that help to

managers.

While this accounting is applied

by companies for preparation of

financial statements.

Presentation of

reports

Under this accounting internal

reports are presented only to the

internal stakeholders.

On the other hand, under this

accounting financial statements

are presented both to internal

and external stakeholders.

The management accounting is a systematic accounting approach which is

assigned in process of gathering financial and non financial data of business entities in

order to prepare internal reports (O’Grady, Morlidge and Rouse, 2016). These reports

are widely used by different kinds of department of business entities for better

management of various kind of activities and operations. The basic aim of project report

is to demonstrate understanding about detailed concept of MA. The project report is

based on Excite entertainment limited company which operates in entertainment sector.

The company is located in United Kingdom. The project report covers about different

kinds of management accounting systems (MAS), MA reports and budgets. Along with

role of various kind of MAS is demonstrated under the project report in detailed manner.

TASK 1

Section (A)

(a) Comparison between MA and financial accounting:

Basis MA Financial accounting

Data gathered In this accounting both kinds of

data is gathered by accountants

including monetary and non

monetary.

On the other hand, in this

accounting only monetary data is

gathered.

Outcome This accounting is being applied by

business entities in order to

produce internal reports that help to

managers.

While this accounting is applied

by companies for preparation of

financial statements.

Presentation of

reports

Under this accounting internal

reports are presented only to the

internal stakeholders.

On the other hand, under this

accounting financial statements

are presented both to internal

and external stakeholders.

(b) Cost accounting system-It is an accounting system that is associated with keeping a

detailed record of incurred cost in different operations. With the use of it companies can

aware about actual financial position, this is so because under it actual cost is

compared with estimated cost. Basically, this accounting system is essential for finance

department of companies because with the use of it they prepare the financial plan as

well as allocate the financial resources into activities. Under this accounting system

below mentioned costs are included that are as followings:

Direct cost- Direct costs are costs that are accountable specifically to a cost

entity. Several overhead costs that can be solely attributed to a project could also

be categorized as direct costs (Ahrens and Khalifa, 2015).

Indirect cost- Indirect costs are costs that can not be accounted for directly by a

cost item. Indirect costs may vary or be solved. Indirect costs involve costs

related to regime, personnel and safety.

Such as in the context of selected company, Excite entertainment limited their financial

team use this accounting system that help them in keeping cost minimum. As well as in

proper allocation of available funds into different kind of activities of production.

(c) Inventory management system- In this accounting system of MA, the inventory of

companies is managed in an effective manner. Along with it traces the cost which

occurs in process of storing goods in warehouses and stores. The key objective of this

system is to create balance between the demand and supply of goods of companies.

Along with it is essential for organisations for providing time to time report about stored

material in the warehouses so that they can take decisions about acquiring new material

as well as production. Herein, the aspect of above Excite entertainment limited, they

implement this accounting system. Due to this accounting system they get able to track

the record of material of organising the events such as music system, display system

etc. As well as their department take decision for purchasing newer equipments as per

the available quantity in the warehouses.

(d) Job costing system- It has been defined as a type of accounting system that is

related to the allocating the production cost of a particular unit of output (Burritt and

detailed record of incurred cost in different operations. With the use of it companies can

aware about actual financial position, this is so because under it actual cost is

compared with estimated cost. Basically, this accounting system is essential for finance

department of companies because with the use of it they prepare the financial plan as

well as allocate the financial resources into activities. Under this accounting system

below mentioned costs are included that are as followings:

Direct cost- Direct costs are costs that are accountable specifically to a cost

entity. Several overhead costs that can be solely attributed to a project could also

be categorized as direct costs (Ahrens and Khalifa, 2015).

Indirect cost- Indirect costs are costs that can not be accounted for directly by a

cost item. Indirect costs may vary or be solved. Indirect costs involve costs

related to regime, personnel and safety.

Such as in the context of selected company, Excite entertainment limited their financial

team use this accounting system that help them in keeping cost minimum. As well as in

proper allocation of available funds into different kind of activities of production.

(c) Inventory management system- In this accounting system of MA, the inventory of

companies is managed in an effective manner. Along with it traces the cost which

occurs in process of storing goods in warehouses and stores. The key objective of this

system is to create balance between the demand and supply of goods of companies.

Along with it is essential for organisations for providing time to time report about stored

material in the warehouses so that they can take decisions about acquiring new material

as well as production. Herein, the aspect of above Excite entertainment limited, they

implement this accounting system. Due to this accounting system they get able to track

the record of material of organising the events such as music system, display system

etc. As well as their department take decision for purchasing newer equipments as per

the available quantity in the warehouses.

(d) Job costing system- It has been defined as a type of accounting system that is

related to the allocating the production cost of a particular unit of output (Burritt and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Christ, 2017). Basically, this accounting system is crucial for those companies in which

portfolio of products is larger and their cost is different from each other. So it is essential

for ascertain of cost, loss, profits of each job. Herein, the context of above Excite

entertainment limited company they use it because their portfolio of equipments is vital.

This helps them in effective evaluation of each activity's cost. As well as their managers

assess the cost of each individual activity in process of organising any kinds of events

at global or local level.

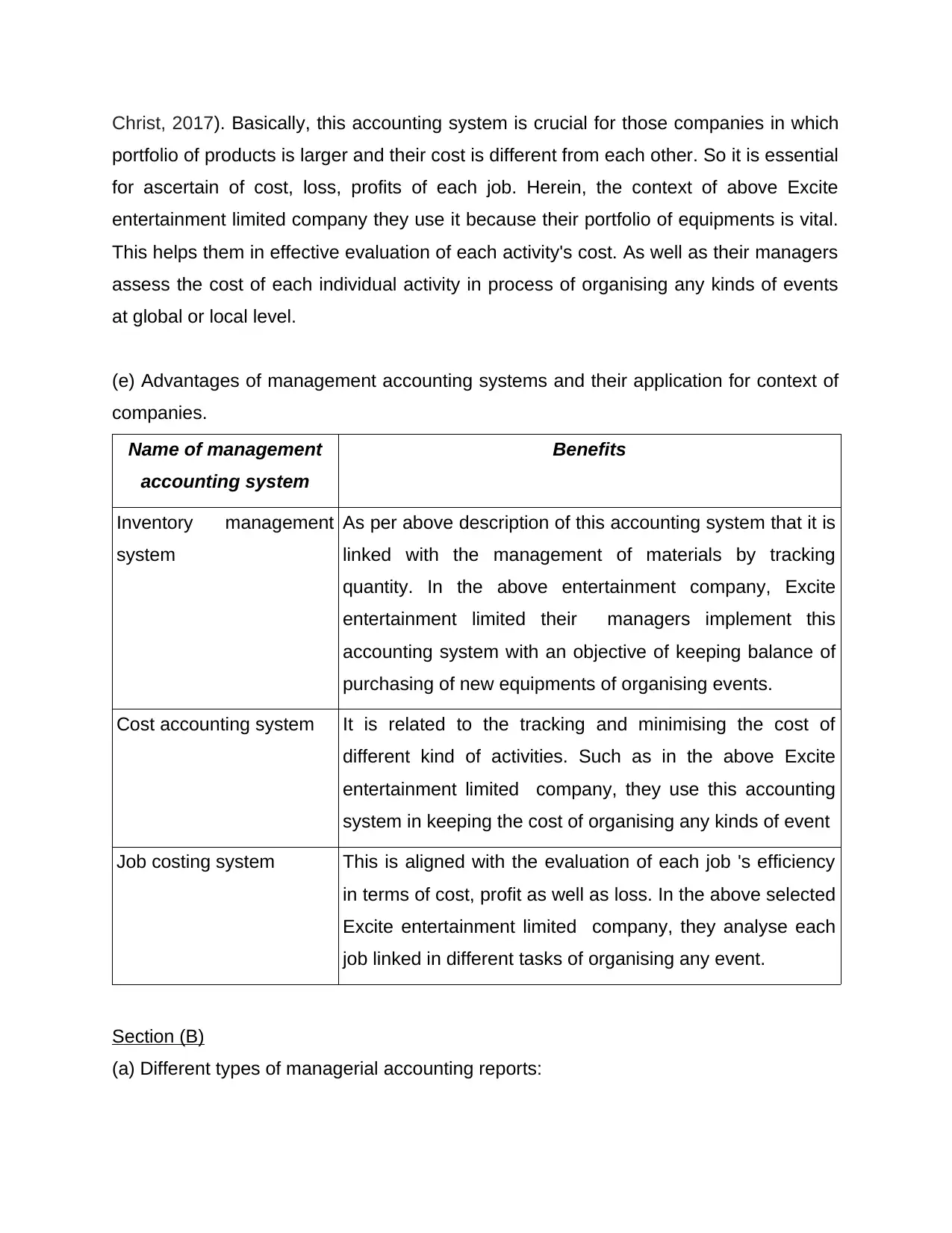

(e) Advantages of management accounting systems and their application for context of

companies.

Name of management

accounting system

Benefits

Inventory management

system

As per above description of this accounting system that it is

linked with the management of materials by tracking

quantity. In the above entertainment company, Excite

entertainment limited their managers implement this

accounting system with an objective of keeping balance of

purchasing of new equipments of organising events.

Cost accounting system It is related to the tracking and minimising the cost of

different kind of activities. Such as in the above Excite

entertainment limited company, they use this accounting

system in keeping the cost of organising any kinds of event

Job costing system This is aligned with the evaluation of each job 's efficiency

in terms of cost, profit as well as loss. In the above selected

Excite entertainment limited company, they analyse each

job linked in different tasks of organising any event.

Section (B)

(a) Different types of managerial accounting reports:

portfolio of products is larger and their cost is different from each other. So it is essential

for ascertain of cost, loss, profits of each job. Herein, the context of above Excite

entertainment limited company they use it because their portfolio of equipments is vital.

This helps them in effective evaluation of each activity's cost. As well as their managers

assess the cost of each individual activity in process of organising any kinds of events

at global or local level.

(e) Advantages of management accounting systems and their application for context of

companies.

Name of management

accounting system

Benefits

Inventory management

system

As per above description of this accounting system that it is

linked with the management of materials by tracking

quantity. In the above entertainment company, Excite

entertainment limited their managers implement this

accounting system with an objective of keeping balance of

purchasing of new equipments of organising events.

Cost accounting system It is related to the tracking and minimising the cost of

different kind of activities. Such as in the above Excite

entertainment limited company, they use this accounting

system in keeping the cost of organising any kinds of event

Job costing system This is aligned with the evaluation of each job 's efficiency

in terms of cost, profit as well as loss. In the above selected

Excite entertainment limited company, they analyse each

job linked in different tasks of organising any event.

Section (B)

(a) Different types of managerial accounting reports:

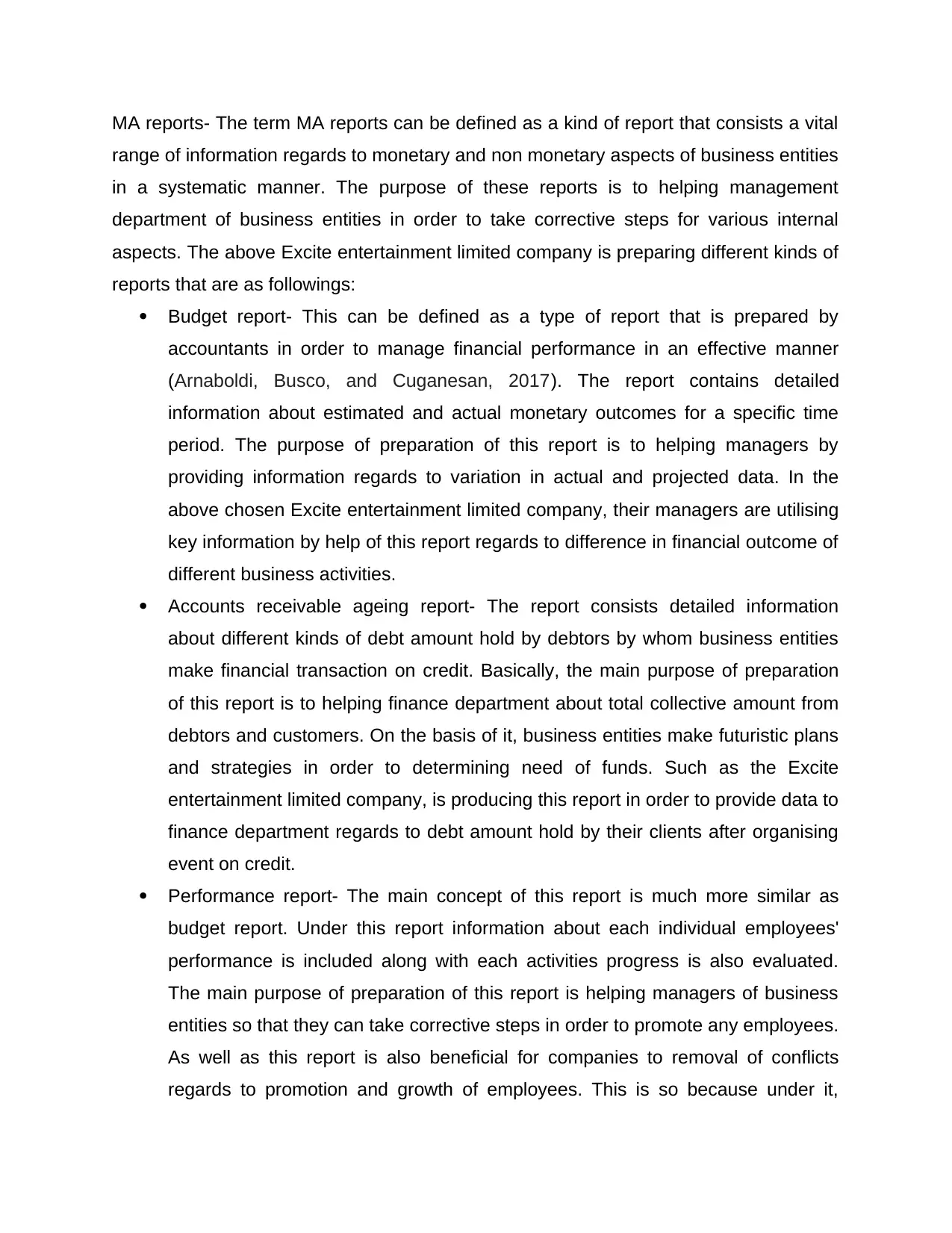

MA reports- The term MA reports can be defined as a kind of report that consists a vital

range of information regards to monetary and non monetary aspects of business entities

in a systematic manner. The purpose of these reports is to helping management

department of business entities in order to take corrective steps for various internal

aspects. The above Excite entertainment limited company is preparing different kinds of

reports that are as followings:

Budget report- This can be defined as a type of report that is prepared by

accountants in order to manage financial performance in an effective manner

(Arnaboldi, Busco, and Cuganesan, 2017). The report contains detailed

information about estimated and actual monetary outcomes for a specific time

period. The purpose of preparation of this report is to helping managers by

providing information regards to variation in actual and projected data. In the

above chosen Excite entertainment limited company, their managers are utilising

key information by help of this report regards to difference in financial outcome of

different business activities.

Accounts receivable ageing report- The report consists detailed information

about different kinds of debt amount hold by debtors by whom business entities

make financial transaction on credit. Basically, the main purpose of preparation

of this report is to helping finance department about total collective amount from

debtors and customers. On the basis of it, business entities make futuristic plans

and strategies in order to determining need of funds. Such as the Excite

entertainment limited company, is producing this report in order to provide data to

finance department regards to debt amount hold by their clients after organising

event on credit.

Performance report- The main concept of this report is much more similar as

budget report. Under this report information about each individual employees'

performance is included along with each activities progress is also evaluated.

The main purpose of preparation of this report is helping managers of business

entities so that they can take corrective steps in order to promote any employees.

As well as this report is also beneficial for companies to removal of conflicts

regards to promotion and growth of employees. This is so because under it,

range of information regards to monetary and non monetary aspects of business entities

in a systematic manner. The purpose of these reports is to helping management

department of business entities in order to take corrective steps for various internal

aspects. The above Excite entertainment limited company is preparing different kinds of

reports that are as followings:

Budget report- This can be defined as a type of report that is prepared by

accountants in order to manage financial performance in an effective manner

(Arnaboldi, Busco, and Cuganesan, 2017). The report contains detailed

information about estimated and actual monetary outcomes for a specific time

period. The purpose of preparation of this report is to helping managers by

providing information regards to variation in actual and projected data. In the

above chosen Excite entertainment limited company, their managers are utilising

key information by help of this report regards to difference in financial outcome of

different business activities.

Accounts receivable ageing report- The report consists detailed information

about different kinds of debt amount hold by debtors by whom business entities

make financial transaction on credit. Basically, the main purpose of preparation

of this report is to helping finance department about total collective amount from

debtors and customers. On the basis of it, business entities make futuristic plans

and strategies in order to determining need of funds. Such as the Excite

entertainment limited company, is producing this report in order to provide data to

finance department regards to debt amount hold by their clients after organising

event on credit.

Performance report- The main concept of this report is much more similar as

budget report. Under this report information about each individual employees'

performance is included along with each activities progress is also evaluated.

The main purpose of preparation of this report is helping managers of business

entities so that they can take corrective steps in order to promote any employees.

As well as this report is also beneficial for companies to removal of conflicts

regards to promotion and growth of employees. This is so because under it,

employees are promoted on the basis of their actual performance. Such as in the

aspect of above Excite entertainment limited company, their manager are using

this report for promoting their employees on the basis of their actual

performance.

Stock report- This report is being prepared by accountants by aligning inventory

management system (Hopper and Wickramasinghe, 2015). In this report,

information regards to all types of stock is included. In broad manner this report

includes statistical data about quantity of raw material, finished goods etc. Under

it, information is included only after proper valuation using various kinds of

techniques. The above, Excite entertainment limited company is using this report

to help their store manager in order to evaluate how much quantity of equipments

are stored in their warehouses for organising any types of events.

(b) Explanation about why information presented should be accurate, relevant to the

user, reliable up to date and timely.

This is important for business entities to keep the information accurate and

relevant because of following reasons:

Accurate- The accounting information should be accurate without containing any

error. It is so because if accounting information will be correct then it will be

easier to management department to take right actions in order to formulate

strategies.

Updated- Another feature of accounting information is that these should be

updated on a regular basis so that accountants can become aware about

changes in monetary aspects.

Timely- As well as another importance of good accounting information is that the

presentation of reports should be on time (Ofileanu, 2015). This is so because if

information will not be published on time then it can be difficult for managers to

prepare further plans on right time.

aspect of above Excite entertainment limited company, their manager are using

this report for promoting their employees on the basis of their actual

performance.

Stock report- This report is being prepared by accountants by aligning inventory

management system (Hopper and Wickramasinghe, 2015). In this report,

information regards to all types of stock is included. In broad manner this report

includes statistical data about quantity of raw material, finished goods etc. Under

it, information is included only after proper valuation using various kinds of

techniques. The above, Excite entertainment limited company is using this report

to help their store manager in order to evaluate how much quantity of equipments

are stored in their warehouses for organising any types of events.

(b) Explanation about why information presented should be accurate, relevant to the

user, reliable up to date and timely.

This is important for business entities to keep the information accurate and

relevant because of following reasons:

Accurate- The accounting information should be accurate without containing any

error. It is so because if accounting information will be correct then it will be

easier to management department to take right actions in order to formulate

strategies.

Updated- Another feature of accounting information is that these should be

updated on a regular basis so that accountants can become aware about

changes in monetary aspects.

Timely- As well as another importance of good accounting information is that the

presentation of reports should be on time (Ofileanu, 2015). This is so because if

information will not be published on time then it can be difficult for managers to

prepare further plans on right time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(c) Critically evaluation of way in which management accounting systems and

management accounting reporting should be integrated within Excite Entertainment Ltd

Operational processes.

In the current business scenario, it is essential to interrelate different

departments with each other so that higher success can be achieved. Such as in the

Excite Entertainment Ltd company, their finance department is linked with cost

accounting system so that they can take maximum use of available resources (Hoque,

2018). As well as job order costing department is also aligned with this department.

Apart from it, the MA reports are also linked with departments such as performance

report is integrated to management department so that they can take decision about

progress and performance of their employees. Thus, as per the above description this

can be stated that MAS and MA reports are linked to process of Excite Entertainment

Ltd company.

TASK 2

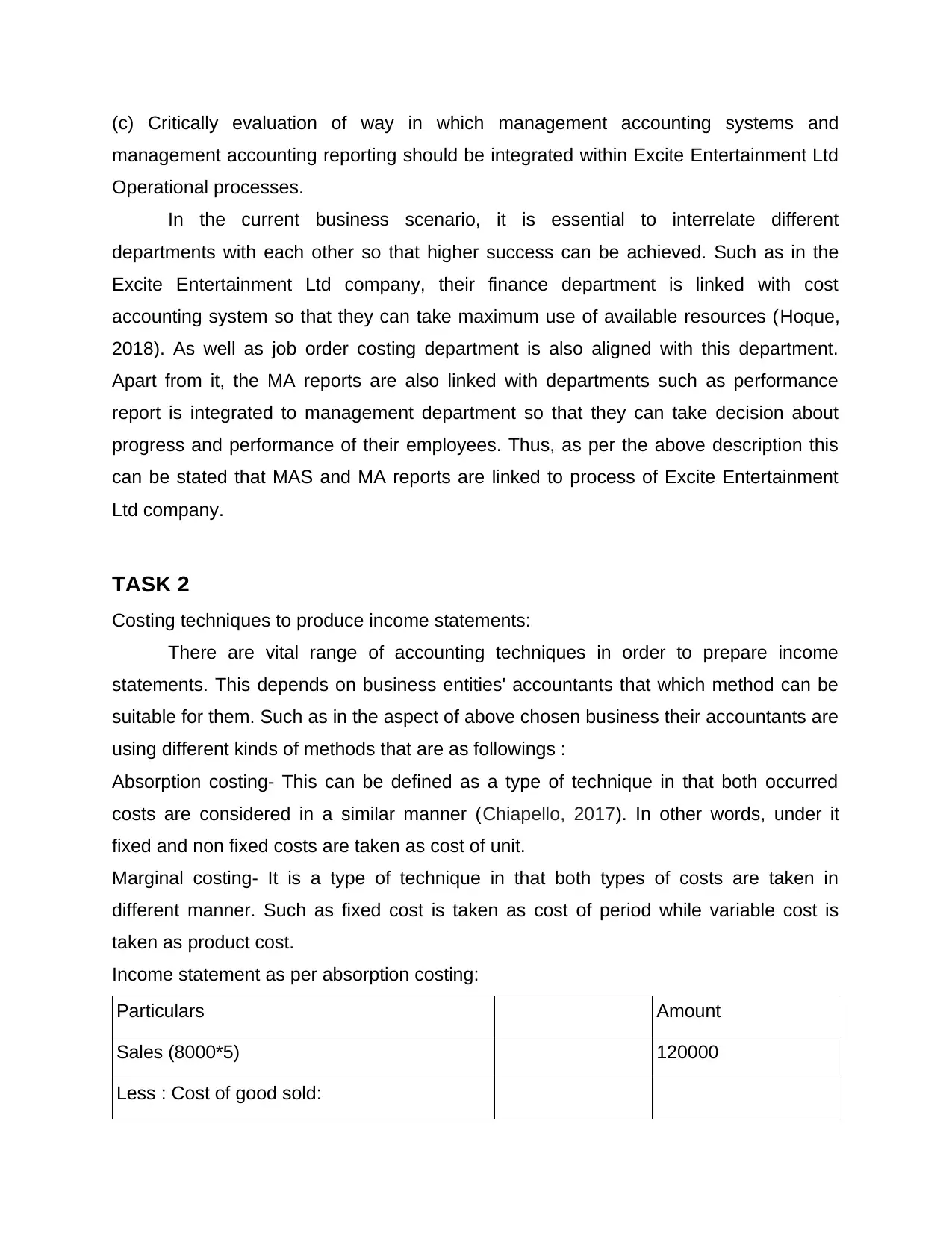

Costing techniques to produce income statements:

There are vital range of accounting techniques in order to prepare income

statements. This depends on business entities' accountants that which method can be

suitable for them. Such as in the aspect of above chosen business their accountants are

using different kinds of methods that are as followings :

Absorption costing- This can be defined as a type of technique in that both occurred

costs are considered in a similar manner (Chiapello, 2017). In other words, under it

fixed and non fixed costs are taken as cost of unit.

Marginal costing- It is a type of technique in that both types of costs are taken in

different manner. Such as fixed cost is taken as cost of period while variable cost is

taken as product cost.

Income statement as per absorption costing:

Particulars Amount

Sales (8000*5) 120000

Less : Cost of good sold:

management accounting reporting should be integrated within Excite Entertainment Ltd

Operational processes.

In the current business scenario, it is essential to interrelate different

departments with each other so that higher success can be achieved. Such as in the

Excite Entertainment Ltd company, their finance department is linked with cost

accounting system so that they can take maximum use of available resources (Hoque,

2018). As well as job order costing department is also aligned with this department.

Apart from it, the MA reports are also linked with departments such as performance

report is integrated to management department so that they can take decision about

progress and performance of their employees. Thus, as per the above description this

can be stated that MAS and MA reports are linked to process of Excite Entertainment

Ltd company.

TASK 2

Costing techniques to produce income statements:

There are vital range of accounting techniques in order to prepare income

statements. This depends on business entities' accountants that which method can be

suitable for them. Such as in the aspect of above chosen business their accountants are

using different kinds of methods that are as followings :

Absorption costing- This can be defined as a type of technique in that both occurred

costs are considered in a similar manner (Chiapello, 2017). In other words, under it

fixed and non fixed costs are taken as cost of unit.

Marginal costing- It is a type of technique in that both types of costs are taken in

different manner. Such as fixed cost is taken as cost of period while variable cost is

taken as product cost.

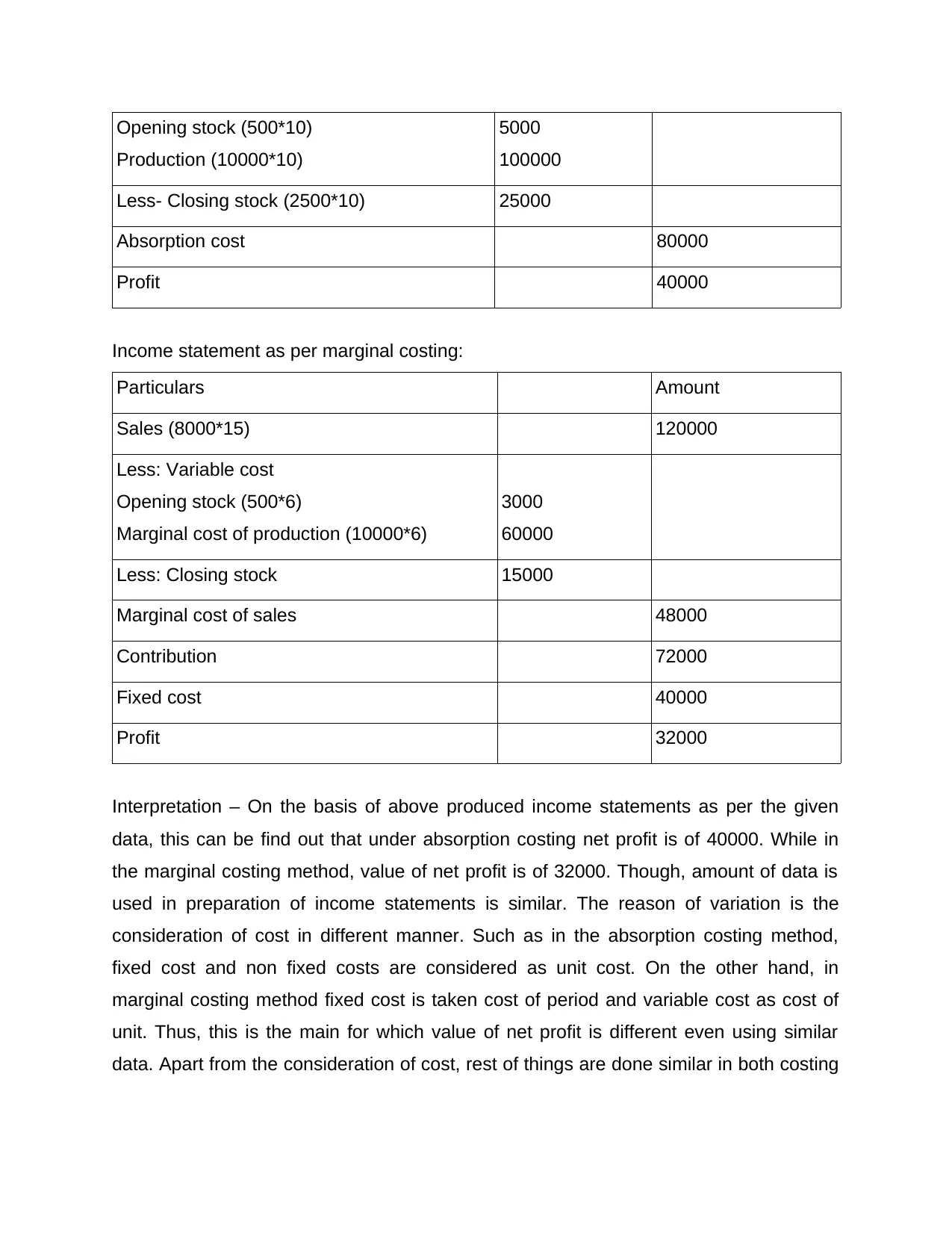

Income statement as per absorption costing:

Particulars Amount

Sales (8000*5) 120000

Less : Cost of good sold:

Opening stock (500*10)

Production (10000*10)

5000

100000

Less- Closing stock (2500*10) 25000

Absorption cost 80000

Profit 40000

Income statement as per marginal costing:

Particulars Amount

Sales (8000*15) 120000

Less: Variable cost

Opening stock (500*6)

Marginal cost of production (10000*6)

3000

60000

Less: Closing stock 15000

Marginal cost of sales 48000

Contribution 72000

Fixed cost 40000

Profit 32000

Interpretation – On the basis of above produced income statements as per the given

data, this can be find out that under absorption costing net profit is of 40000. While in

the marginal costing method, value of net profit is of 32000. Though, amount of data is

used in preparation of income statements is similar. The reason of variation is the

consideration of cost in different manner. Such as in the absorption costing method,

fixed cost and non fixed costs are considered as unit cost. On the other hand, in

marginal costing method fixed cost is taken cost of period and variable cost as cost of

unit. Thus, this is the main for which value of net profit is different even using similar

data. Apart from the consideration of cost, rest of things are done similar in both costing

Production (10000*10)

5000

100000

Less- Closing stock (2500*10) 25000

Absorption cost 80000

Profit 40000

Income statement as per marginal costing:

Particulars Amount

Sales (8000*15) 120000

Less: Variable cost

Opening stock (500*6)

Marginal cost of production (10000*6)

3000

60000

Less: Closing stock 15000

Marginal cost of sales 48000

Contribution 72000

Fixed cost 40000

Profit 32000

Interpretation – On the basis of above produced income statements as per the given

data, this can be find out that under absorption costing net profit is of 40000. While in

the marginal costing method, value of net profit is of 32000. Though, amount of data is

used in preparation of income statements is similar. The reason of variation is the

consideration of cost in different manner. Such as in the absorption costing method,

fixed cost and non fixed costs are considered as unit cost. On the other hand, in

marginal costing method fixed cost is taken cost of period and variable cost as cost of

unit. Thus, this is the main for which value of net profit is different even using similar

data. Apart from the consideration of cost, rest of things are done similar in both costing

methods. Like value of sales is similar under absorption and marginal costing that is of

120000.

Advise to management:

On the basis of produced results by help of absorption and marginal costing, this

can be find out that both techniques are producing different results and analysis of

these techniques is done below:

Absorption costing:

Advantage-

This technique is beneficial for business entities in order to track the profits in

more effective manner.

As well as under this costing all kinds of costs are considered as unit cost that

makes enable the consumption of total cost.

Disadvantage-

One of the key disadvantage of this technique is that it does not help in

enhancement of operational efficiency.

As well as this is not beneficial for making comparison of product lines.

Marginal costing:

Advantage-

This costing technique is useful for business entities in order to dividing cost in a

separate manner (Seal and Mattimoe, 2016).

As well as this costing has the nature of remaining same irrespective of volume

of production.

Disadvantage-

The key drawback of this costing technique is that it ignores time element.

As well as it is difficult to analyse the overhead in an effective manner.

So, as per the above analysis this can be analysed that above absorption costing

technique seem better to use. This is so because under it both costs are taken in a

similar manner.

120000.

Advise to management:

On the basis of produced results by help of absorption and marginal costing, this

can be find out that both techniques are producing different results and analysis of

these techniques is done below:

Absorption costing:

Advantage-

This technique is beneficial for business entities in order to track the profits in

more effective manner.

As well as under this costing all kinds of costs are considered as unit cost that

makes enable the consumption of total cost.

Disadvantage-

One of the key disadvantage of this technique is that it does not help in

enhancement of operational efficiency.

As well as this is not beneficial for making comparison of product lines.

Marginal costing:

Advantage-

This costing technique is useful for business entities in order to dividing cost in a

separate manner (Seal and Mattimoe, 2016).

As well as this costing has the nature of remaining same irrespective of volume

of production.

Disadvantage-

The key drawback of this costing technique is that it ignores time element.

As well as it is difficult to analyse the overhead in an effective manner.

So, as per the above analysis this can be analysed that above absorption costing

technique seem better to use. This is so because under it both costs are taken in a

similar manner.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TASK 3

Section (A)

Different types of planning tools of budgetary control.

Budgetary control- This can be defined as a kind of performance management

technique in that goals are set by managers by help of different kinds of budgets. The

main objective of this approach is that keeping an extra sight of eye over various types

of financing activities. Such as in the context of above Excite Entertainment Ltd

company, they are using different kinds of planning tools of budgetary control and some

of them are demonstrated below in such manner:

Cash budget – This is a kinds of budget that consists detailed information

regards to activities of cash which cause as in and outflow of cash (Jacobs,

2016). The objective of preparation of this budget is to helping finance

department in order to assess key information about in and out flow of cash. In

the aspect of above chosen Excite Entertainment Ltd company, their managers

are using key information by help of this budget about allocation of cash.

Advantages- One of they benefit of this budget is that this is suitable for companies in

order to manage the performance regards to cash management.

Disadvantage- This budget is not suitable for those business entities in which

transactions of cash is done at a large parameter.

Zero based budget- This is a type of budget that is prepared in a completely

different manner in which financing activities are projected on the basis of proper

research. The objective of this budget is that to provide accuracy in financial

activities of business activities. In the absence of this budget, it can be difficult to

business entities to manage over all performance of various aspects. In the

context of above Excite Entertainment Ltd company, their managers are using

this budget in order to control overall expenditure in an effective manner. It has

some advantages and disadvantages that are as followings:

Advantages- This budget is suitable for business entities in order to provide accuracy

and consistency in financial activities.

Section (A)

Different types of planning tools of budgetary control.

Budgetary control- This can be defined as a kind of performance management

technique in that goals are set by managers by help of different kinds of budgets. The

main objective of this approach is that keeping an extra sight of eye over various types

of financing activities. Such as in the context of above Excite Entertainment Ltd

company, they are using different kinds of planning tools of budgetary control and some

of them are demonstrated below in such manner:

Cash budget – This is a kinds of budget that consists detailed information

regards to activities of cash which cause as in and outflow of cash (Jacobs,

2016). The objective of preparation of this budget is to helping finance

department in order to assess key information about in and out flow of cash. In

the aspect of above chosen Excite Entertainment Ltd company, their managers

are using key information by help of this budget about allocation of cash.

Advantages- One of they benefit of this budget is that this is suitable for companies in

order to manage the performance regards to cash management.

Disadvantage- This budget is not suitable for those business entities in which

transactions of cash is done at a large parameter.

Zero based budget- This is a type of budget that is prepared in a completely

different manner in which financing activities are projected on the basis of proper

research. The objective of this budget is that to provide accuracy in financial

activities of business activities. In the absence of this budget, it can be difficult to

business entities to manage over all performance of various aspects. In the

context of above Excite Entertainment Ltd company, their managers are using

this budget in order to control overall expenditure in an effective manner. It has

some advantages and disadvantages that are as followings:

Advantages- This budget is suitable for business entities in order to provide accuracy

and consistency in financial activities.

Disadvantage- One of the key drawback of this budget is that it is not affordable for all

kinds of business entities. Specially for small businesses who can not afford cost of

preparation of this budget.

Sales budget- It is a type of budget that is prepared by accountants in order to

trace activities of sales units in an effective manner (Lobianco, Caurla and

Barkaoui, 2016). The budget consists information regarding to quantity of

possible units that can be sold out during a particular time period. In addition, this

budget consists information about total possible amount of revenues that can be

generated by selling of vital range of outputs. In the aspect of Excite

Entertainment Ltd company, they prepare this budget in order to estimate

number of events that can be performed by them. This has some advantages

and disadvantages that are as followings:

Advantages- This budget is beneficial for companies in order to track the progress

regards to total units of outputs that can be sold out.

Disadvantage- It is not beneficial for companies in the case when any financial crises

occurs inside of business.

Role of planning tools in order to sort out the issues.

In the aspect of overcoming from financial issues, different kinds of budgets play

a significant role ( Chandler, 2017). This is so because budgets consists information

about all possible monetary transactions. On the basis of it, this becomes easier for

finance managers to keep an extra sight of eye over monetary transactions. Such as in

the aspect of above Excite Entertainment Ltd company, they are using different kinds of

budgets such as ZBB, cash budget etc. in order to overcome the issue of

mismanagement of total expenditures.

TASK 4

Section (B)

Comparison of ways in which MAS is used to sort out the issues.

kinds of business entities. Specially for small businesses who can not afford cost of

preparation of this budget.

Sales budget- It is a type of budget that is prepared by accountants in order to

trace activities of sales units in an effective manner (Lobianco, Caurla and

Barkaoui, 2016). The budget consists information regarding to quantity of

possible units that can be sold out during a particular time period. In addition, this

budget consists information about total possible amount of revenues that can be

generated by selling of vital range of outputs. In the aspect of Excite

Entertainment Ltd company, they prepare this budget in order to estimate

number of events that can be performed by them. This has some advantages

and disadvantages that are as followings:

Advantages- This budget is beneficial for companies in order to track the progress

regards to total units of outputs that can be sold out.

Disadvantage- It is not beneficial for companies in the case when any financial crises

occurs inside of business.

Role of planning tools in order to sort out the issues.

In the aspect of overcoming from financial issues, different kinds of budgets play

a significant role ( Chandler, 2017). This is so because budgets consists information

about all possible monetary transactions. On the basis of it, this becomes easier for

finance managers to keep an extra sight of eye over monetary transactions. Such as in

the aspect of above Excite Entertainment Ltd company, they are using different kinds of

budgets such as ZBB, cash budget etc. in order to overcome the issue of

mismanagement of total expenditures.

TASK 4

Section (B)

Comparison of ways in which MAS is used to sort out the issues.

Monetary issue - It can be characterized as a problem because businesses do not have

sufficient funds for execute various types of activities. In the aspect of business entities,

there are vital range of financial issues that are demonstrated below in such manner :

Higher expenses- This is a kind of financial problem in which the profits of

businesses decreases by a huge gap as time goes by while spending increases

significantly (Schmidt, Götze and Sygulla, 2015). Because of this, companies are

dealing with the problem of lack of financial resources. Such as in the aspect of

above Excite Entertainment Ltd company chosen business entity they are facing

this monetary issue.

Lack of sales revenues - It is an economic issue in which the transaction value of

sales of corporations begins to decline. As a result, companies total amount of

funds start to decrease and they are beaten by competitors.

Identifying monetary issue:

Benchmarking- It is a method in which the financial dimensions of firms are

compared with competitive business organizations in order to find a real problem

(Farrell and Gallagher, 2015). This method is being used by administrators in the

above-mentioned organization to find actual monetary problem.

KPI - This is a way to manage monetary and anti-financial output. Under it, all

activities that generate more revenue and expenditures relative to projected

goals are outlined.

Budgetary targets- Comparing actual income & expenditure with estimated

objectives is done within this technique so that errors can be found.

Financial governance- It can be characterized as a structured method of efficiently

collecting analysing and handling financial information in order to manage financial

issues (Gray and Alles, 2015).

It could be used as a way to avoid money issues as it comprises of all a

corporate entity's financial documents and on the basis of which companies can find

alternatives to work out the issues. Such for financial management, due to additional

information on all economic factors, it serves as a control tool for businesses.

sufficient funds for execute various types of activities. In the aspect of business entities,

there are vital range of financial issues that are demonstrated below in such manner :

Higher expenses- This is a kind of financial problem in which the profits of

businesses decreases by a huge gap as time goes by while spending increases

significantly (Schmidt, Götze and Sygulla, 2015). Because of this, companies are

dealing with the problem of lack of financial resources. Such as in the aspect of

above Excite Entertainment Ltd company chosen business entity they are facing

this monetary issue.

Lack of sales revenues - It is an economic issue in which the transaction value of

sales of corporations begins to decline. As a result, companies total amount of

funds start to decrease and they are beaten by competitors.

Identifying monetary issue:

Benchmarking- It is a method in which the financial dimensions of firms are

compared with competitive business organizations in order to find a real problem

(Farrell and Gallagher, 2015). This method is being used by administrators in the

above-mentioned organization to find actual monetary problem.

KPI - This is a way to manage monetary and anti-financial output. Under it, all

activities that generate more revenue and expenditures relative to projected

goals are outlined.

Budgetary targets- Comparing actual income & expenditure with estimated

objectives is done within this technique so that errors can be found.

Financial governance- It can be characterized as a structured method of efficiently

collecting analysing and handling financial information in order to manage financial

issues (Gray and Alles, 2015).

It could be used as a way to avoid money issues as it comprises of all a

corporate entity's financial documents and on the basis of which companies can find

alternatives to work out the issues. Such for financial management, due to additional

information on all economic factors, it serves as a control tool for businesses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

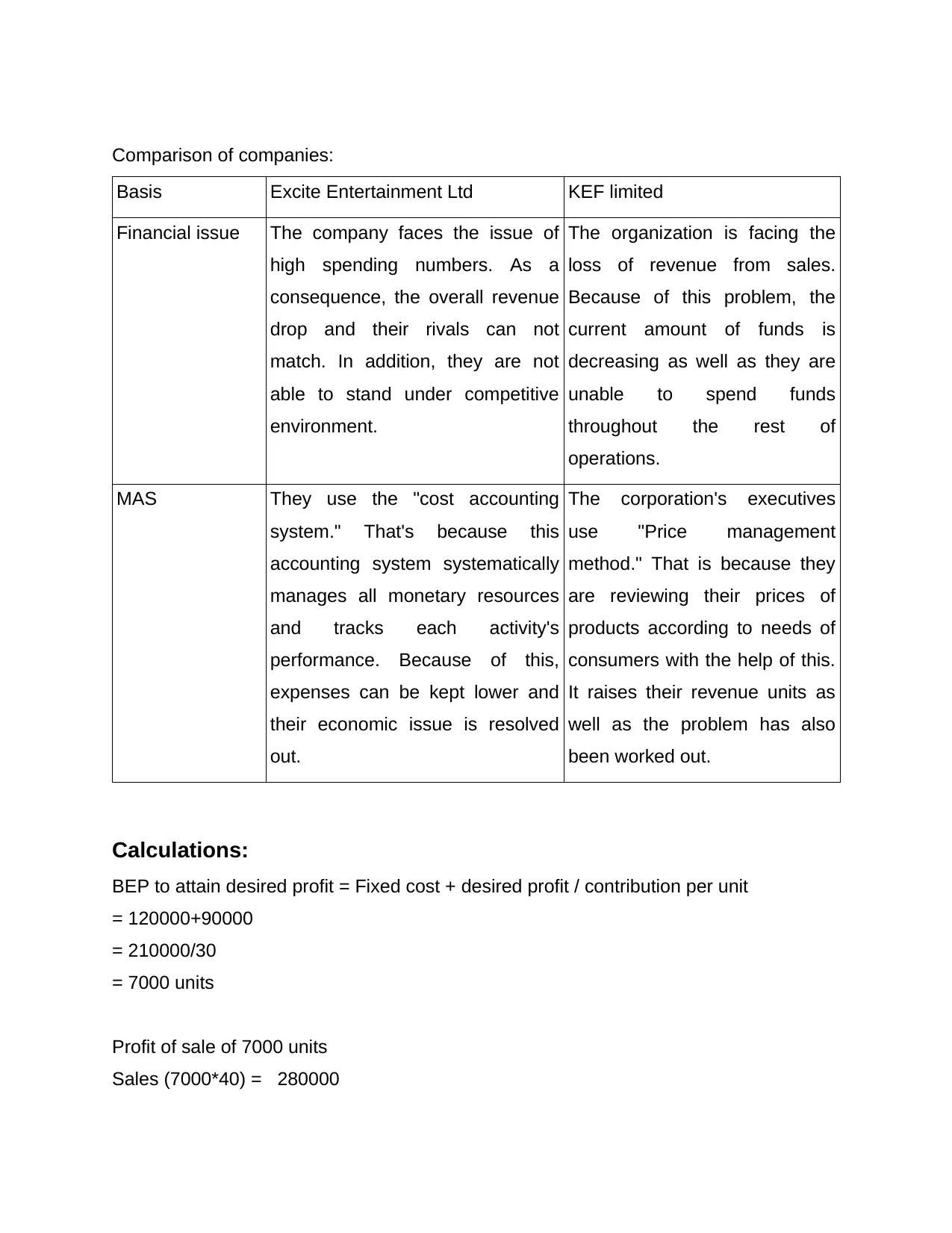

Comparison of companies:

Basis Excite Entertainment Ltd KEF limited

Financial issue The company faces the issue of

high spending numbers. As a

consequence, the overall revenue

drop and their rivals can not

match. In addition, they are not

able to stand under competitive

environment.

The organization is facing the

loss of revenue from sales.

Because of this problem, the

current amount of funds is

decreasing as well as they are

unable to spend funds

throughout the rest of

operations.

MAS They use the "cost accounting

system." That's because this

accounting system systematically

manages all monetary resources

and tracks each activity's

performance. Because of this,

expenses can be kept lower and

their economic issue is resolved

out.

The corporation's executives

use "Price management

method." That is because they

are reviewing their prices of

products according to needs of

consumers with the help of this.

It raises their revenue units as

well as the problem has also

been worked out.

Calculations:

BEP to attain desired profit = Fixed cost + desired profit / contribution per unit

= 120000+90000

= 210000/30

= 7000 units

Profit of sale of 7000 units

Sales (7000*40) = 280000

Basis Excite Entertainment Ltd KEF limited

Financial issue The company faces the issue of

high spending numbers. As a

consequence, the overall revenue

drop and their rivals can not

match. In addition, they are not

able to stand under competitive

environment.

The organization is facing the

loss of revenue from sales.

Because of this problem, the

current amount of funds is

decreasing as well as they are

unable to spend funds

throughout the rest of

operations.

MAS They use the "cost accounting

system." That's because this

accounting system systematically

manages all monetary resources

and tracks each activity's

performance. Because of this,

expenses can be kept lower and

their economic issue is resolved

out.

The corporation's executives

use "Price management

method." That is because they

are reviewing their prices of

products according to needs of

consumers with the help of this.

It raises their revenue units as

well as the problem has also

been worked out.

Calculations:

BEP to attain desired profit = Fixed cost + desired profit / contribution per unit

= 120000+90000

= 210000/30

= 7000 units

Profit of sale of 7000 units

Sales (7000*40) = 280000

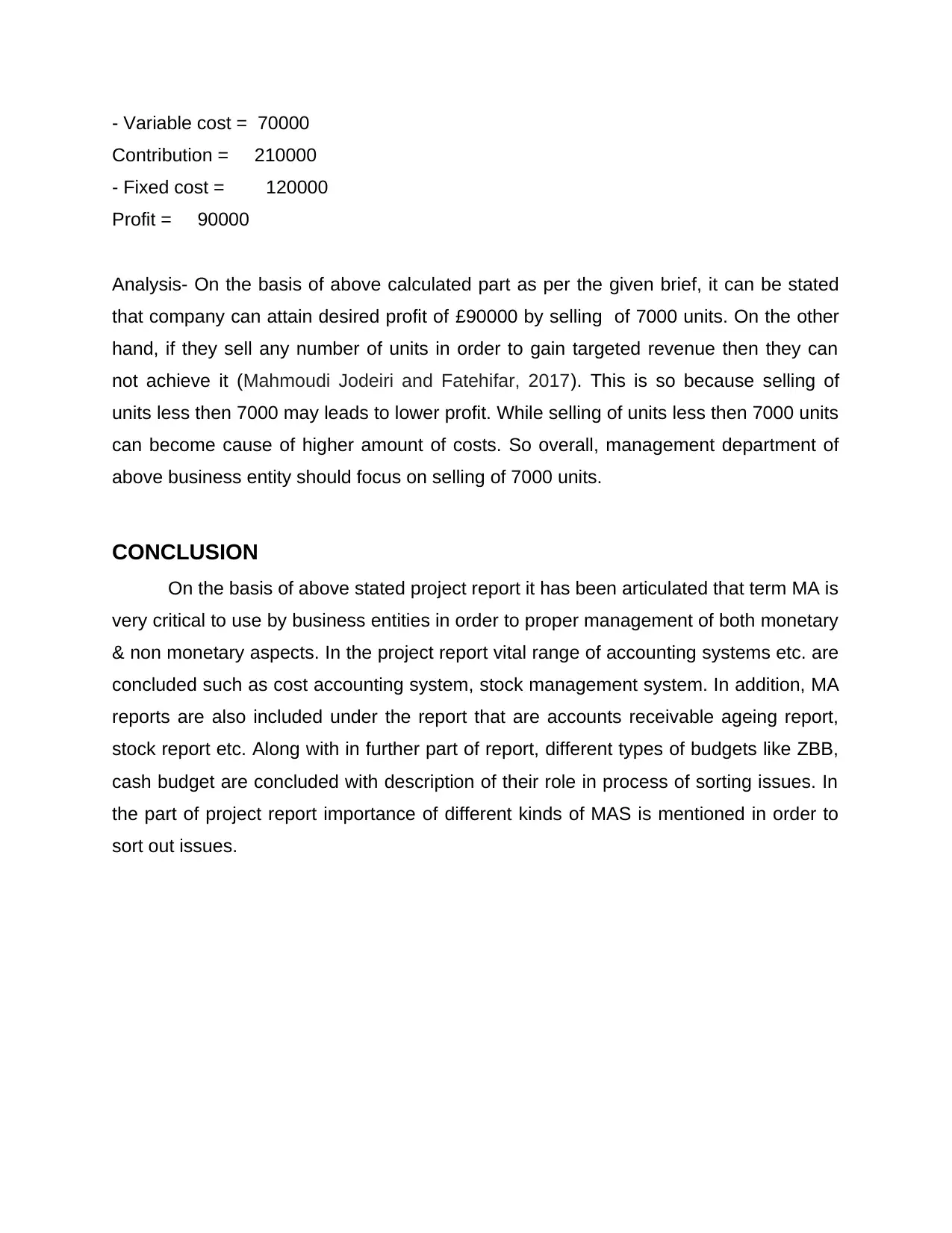

- Variable cost = 70000

Contribution = 210000

- Fixed cost = 120000

Profit = 90000

Analysis- On the basis of above calculated part as per the given brief, it can be stated

that company can attain desired profit of £90000 by selling of 7000 units. On the other

hand, if they sell any number of units in order to gain targeted revenue then they can

not achieve it (Mahmoudi Jodeiri and Fatehifar, 2017). This is so because selling of

units less then 7000 may leads to lower profit. While selling of units less then 7000 units

can become cause of higher amount of costs. So overall, management department of

above business entity should focus on selling of 7000 units.

CONCLUSION

On the basis of above stated project report it has been articulated that term MA is

very critical to use by business entities in order to proper management of both monetary

& non monetary aspects. In the project report vital range of accounting systems etc. are

concluded such as cost accounting system, stock management system. In addition, MA

reports are also included under the report that are accounts receivable ageing report,

stock report etc. Along with in further part of report, different types of budgets like ZBB,

cash budget are concluded with description of their role in process of sorting issues. In

the part of project report importance of different kinds of MAS is mentioned in order to

sort out issues.

Contribution = 210000

- Fixed cost = 120000

Profit = 90000

Analysis- On the basis of above calculated part as per the given brief, it can be stated

that company can attain desired profit of £90000 by selling of 7000 units. On the other

hand, if they sell any number of units in order to gain targeted revenue then they can

not achieve it (Mahmoudi Jodeiri and Fatehifar, 2017). This is so because selling of

units less then 7000 may leads to lower profit. While selling of units less then 7000 units

can become cause of higher amount of costs. So overall, management department of

above business entity should focus on selling of 7000 units.

CONCLUSION

On the basis of above stated project report it has been articulated that term MA is

very critical to use by business entities in order to proper management of both monetary

& non monetary aspects. In the project report vital range of accounting systems etc. are

concluded such as cost accounting system, stock management system. In addition, MA

reports are also included under the report that are accounts receivable ageing report,

stock report etc. Along with in further part of report, different types of budgets like ZBB,

cash budget are concluded with description of their role in process of sorting issues. In

the part of project report importance of different kinds of MAS is mentioned in order to

sort out issues.

REFERENCES

Books and journals:

O’Grady, W., Morlidge, S. and Rouse, P., 2016. Evaluating the completeness and

effectiveness of management control systems with cybernetic

tools. Management Accounting Research. 33. pp.1-15.

Ahrens, T. and Khalifa, R., 2015. The impact of regulation on management control:

Compliance as a strategic response to institutional logics of university

accreditation. Qualitative Research in Accounting & Management. 12(2).

pp.106-126.

Burritt, R .L. and Christ, K. L., 2017. The need for monetary information within corporate

water accounting. Journal of environmental management. 201. pp.72-81.

Arnaboldi, M., Busco, C. and Cuganesan, S., 2017. Accounting, accountability, social

media and big data: revolution or hype?. Accounting, auditing & accountability

journal. 30(4). pp.762-776.

Hopper, T., Ashraf, J., Uddin, S. and Wickramasinghe, D., 2015. Social theorisation of

accounting. The Routledge Companion to Financial Accounting Theory,

London: Routledge. pp.452-471.

Ofileanu, D., 2015. Considerations Regarding Lean Approach Within Management

Accounting. Ovidius University Annals, Series Economic Sciences. 15(2).

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Chiapello, E., 2017. Critical accounting research and neoliberalism. Critical

Perspectives on Accounting. 43. pp.47-64.

Seal, W. and Mattimoe, R., 2016. The role of narrative in developing management

control knowledge from fieldwork: A pragmatic constructivist

perspective. Qualitative Research in Accounting & Management. 13(3). pp.330-

349.

Jacobs, K., 2016. Theorising interdisciplinary public sector accounting

research. Financial Accountability & Management. 32(4). pp.469-488.

Chandler, J., 2017. Questioning the new public management. Routledge.

Farrell, M. and Gallagher, R., 2015. The valuation implications of enterprise risk

management maturity. Journal of Risk and Insurance. 82(3). pp.625-657.

Gray, G .L. and Alles, M., 2015. Data fracking strategy: Why management accountants

need it. Management Accounting Quarterly. 16(3).

Mahmoudi, E., Jodeiri, N. and Fatehifar, E., 2017. Implementation of material flow cost

accounting for efficiency improvement in wastewater treatment unit of Tabriz oil

refining company. Journal of cleaner production. 165. pp.530-536.

Schmidt, A., Götze, U. and Sygulla, R., 2015. Extending the scope of Material Flow

Cost Accounting–methodical refinements and use case. Journal of Cleaner

Production. 108. pp.1320-1332.

Lobianco, A., Delacote, P., Caurla, S. and Barkaoui, A., 2016. Accounting for active

management and risk attitude in forest sector models. Environmental Modeling

& Assessment. 21(3). pp.391-405.

Books and journals:

O’Grady, W., Morlidge, S. and Rouse, P., 2016. Evaluating the completeness and

effectiveness of management control systems with cybernetic

tools. Management Accounting Research. 33. pp.1-15.

Ahrens, T. and Khalifa, R., 2015. The impact of regulation on management control:

Compliance as a strategic response to institutional logics of university

accreditation. Qualitative Research in Accounting & Management. 12(2).

pp.106-126.

Burritt, R .L. and Christ, K. L., 2017. The need for monetary information within corporate

water accounting. Journal of environmental management. 201. pp.72-81.

Arnaboldi, M., Busco, C. and Cuganesan, S., 2017. Accounting, accountability, social

media and big data: revolution or hype?. Accounting, auditing & accountability

journal. 30(4). pp.762-776.

Hopper, T., Ashraf, J., Uddin, S. and Wickramasinghe, D., 2015. Social theorisation of

accounting. The Routledge Companion to Financial Accounting Theory,

London: Routledge. pp.452-471.

Ofileanu, D., 2015. Considerations Regarding Lean Approach Within Management

Accounting. Ovidius University Annals, Series Economic Sciences. 15(2).

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Chiapello, E., 2017. Critical accounting research and neoliberalism. Critical

Perspectives on Accounting. 43. pp.47-64.

Seal, W. and Mattimoe, R., 2016. The role of narrative in developing management

control knowledge from fieldwork: A pragmatic constructivist

perspective. Qualitative Research in Accounting & Management. 13(3). pp.330-

349.

Jacobs, K., 2016. Theorising interdisciplinary public sector accounting

research. Financial Accountability & Management. 32(4). pp.469-488.

Chandler, J., 2017. Questioning the new public management. Routledge.

Farrell, M. and Gallagher, R., 2015. The valuation implications of enterprise risk

management maturity. Journal of Risk and Insurance. 82(3). pp.625-657.

Gray, G .L. and Alles, M., 2015. Data fracking strategy: Why management accountants

need it. Management Accounting Quarterly. 16(3).

Mahmoudi, E., Jodeiri, N. and Fatehifar, E., 2017. Implementation of material flow cost

accounting for efficiency improvement in wastewater treatment unit of Tabriz oil

refining company. Journal of cleaner production. 165. pp.530-536.

Schmidt, A., Götze, U. and Sygulla, R., 2015. Extending the scope of Material Flow

Cost Accounting–methodical refinements and use case. Journal of Cleaner

Production. 108. pp.1320-1332.

Lobianco, A., Delacote, P., Caurla, S. and Barkaoui, A., 2016. Accounting for active

management and risk attitude in forest sector models. Environmental Modeling

& Assessment. 21(3). pp.391-405.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.