Audit Report: Analysis of Sheridan AV Financial Statements, 2019

VerifiedAdded on 2023/01/11

|15

|3661

|58

Report

AI Summary

This report provides an in-depth analysis of the Sheridan AV audit case study, examining key aspects such as client acceptance decisions, audit planning, preliminary risk assessment, and materiality calculations. The report details the inherent and control risks identified, alongside the audit procedures employed to evaluate the financial statements of Sheridan AV. The analysis covers various financial aspects, including non-current assets, revenue, and cash, highlighting the application of valuation, dual aspect, classification, and occurrence tests. The report is structured to reflect the stages of an audit, from initial client acceptance to risk assessment and the development of audit plans to mitigate identified risks. The conclusion summarizes the audit's findings and recommendations, providing a comprehensive overview of the audit process and its application in a real-world scenario.

Running head: MANGEMENT ACCOUNTING

MANGEMENT ACCOUNTING

Name of the Student:

Name of the University:

Author Note

MANGEMENT ACCOUNTING

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANGEMENT ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Client acceptance decision.....................................................................................................2

Audit planning........................................................................................................................4

Preliminarily risk assessment.................................................................................................6

Preliminarily materiality calculation......................................................................................6

Inherent risks..........................................................................................................................7

Control risk.............................................................................................................................8

Conclusion................................................................................................................................10

References and bibliography....................................................................................................11

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Client acceptance decision.....................................................................................................2

Audit planning........................................................................................................................4

Preliminarily risk assessment.................................................................................................6

Preliminarily materiality calculation......................................................................................6

Inherent risks..........................................................................................................................7

Control risk.............................................................................................................................8

Conclusion................................................................................................................................10

References and bibliography....................................................................................................11

2MANGEMENT ACCOUNTING

Introduction

The report is prepared to review the company named “Sheridan AV” in the audit

point of view. Sheridan AV is a retail and wholesale company of the electronic products. The

company is situated in the Brigstowe. The company is involved in the retail as well as the

wholesale of the electronic items based on the audio and visuals. The some key products of

the company are speakers, projectors, television, screens, audio -visual receiver, blue ray

players and same like. John Sheridan founded the company in 1971. The mission of the

company is to bring the absolute best in sound and vision for their customers. The company

is not focused to sell the huge product range but to provide the selected high quality product,

which give the flawless experience to the customers of the company.

Discussion

Client acceptance decision

The client acceptance decision is the process to accept the audit request offered by the

any company to the audit firm. The client acceptance the minimum five major issues that

must be addressed. The five major are as follows:-

Management Integrity: - the management integrity of the firm plays an important

role in the client acceptance decision of the audit firm. The management integrity

means that, whether the company is providing the meaningful disclosures and

representation of the data during the time of their operation and requirements (Hassan

2016). For example, the independent auditor, analyse the financial statements, which

are based on asserting the management operations from including an element in

financial report to reveals the information of that element. Here, the company provide

the proper information related to different financial terms as the neon- current asset,

payables, inventory and same like.

Introduction

The report is prepared to review the company named “Sheridan AV” in the audit

point of view. Sheridan AV is a retail and wholesale company of the electronic products. The

company is situated in the Brigstowe. The company is involved in the retail as well as the

wholesale of the electronic items based on the audio and visuals. The some key products of

the company are speakers, projectors, television, screens, audio -visual receiver, blue ray

players and same like. John Sheridan founded the company in 1971. The mission of the

company is to bring the absolute best in sound and vision for their customers. The company

is not focused to sell the huge product range but to provide the selected high quality product,

which give the flawless experience to the customers of the company.

Discussion

Client acceptance decision

The client acceptance decision is the process to accept the audit request offered by the

any company to the audit firm. The client acceptance the minimum five major issues that

must be addressed. The five major are as follows:-

Management Integrity: - the management integrity of the firm plays an important

role in the client acceptance decision of the audit firm. The management integrity

means that, whether the company is providing the meaningful disclosures and

representation of the data during the time of their operation and requirements (Hassan

2016). For example, the independent auditor, analyse the financial statements, which

are based on asserting the management operations from including an element in

financial report to reveals the information of that element. Here, the company provide

the proper information related to different financial terms as the neon- current asset,

payables, inventory and same like.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANGEMENT ACCOUNTING

Relationships with other professional: - the relation of the firm with the other

professional institutes and the companies also plays the important role in the decision

making to accept the client or not. If the company is highly reputed and have the good

relationship status with the other professional then it increases the audit firm to make

the decision to accept the audit request of the firm.

Risk association: - the level of risk associated with the firm also influenced the

decision making process of the audit firm to accept the decision of the firm (Habib

2015). Mostly, the high reputed companies with the lower risk attracts the audit firm

to accept the audit request. A prospective client involved in or about to be involved in

litigation can be very dangerous. This is particularly true if the work to be performed

by the cu may be involved in the litigation or in some other form of claim. Worse still

would be a lawsuit between the prospective client and another client of the CPA.

Here, the information revels by the Sheridan AV, shows there is not a high risk

associated with the firm as the company properly maintained and report its financial

information.

Technical competence: - the technical competence also affect the decision making

process of the audit firm. Like the size of the company, their operation, industry type

and likes (Knechel and Salterio 2016). The Sheridan AV is not a big company but big

enough to attract the company. As the some audit firms are specialized in the certain

field and only take the work of the same industry. Many prospective clients may be

subject to complex laws and regulations of several governments in different countries.

Financial stability and liquidity of the prospective client also are important. Stability

and liquidity can affect the CPA's choice of auditing procedures and the report

ultimately rendered. A prospective client with liquidity problems, an inability to meet

its financial obligations when they are due, large numbers of transactions with related

Relationships with other professional: - the relation of the firm with the other

professional institutes and the companies also plays the important role in the decision

making to accept the client or not. If the company is highly reputed and have the good

relationship status with the other professional then it increases the audit firm to make

the decision to accept the audit request of the firm.

Risk association: - the level of risk associated with the firm also influenced the

decision making process of the audit firm to accept the decision of the firm (Habib

2015). Mostly, the high reputed companies with the lower risk attracts the audit firm

to accept the audit request. A prospective client involved in or about to be involved in

litigation can be very dangerous. This is particularly true if the work to be performed

by the cu may be involved in the litigation or in some other form of claim. Worse still

would be a lawsuit between the prospective client and another client of the CPA.

Here, the information revels by the Sheridan AV, shows there is not a high risk

associated with the firm as the company properly maintained and report its financial

information.

Technical competence: - the technical competence also affect the decision making

process of the audit firm. Like the size of the company, their operation, industry type

and likes (Knechel and Salterio 2016). The Sheridan AV is not a big company but big

enough to attract the company. As the some audit firms are specialized in the certain

field and only take the work of the same industry. Many prospective clients may be

subject to complex laws and regulations of several governments in different countries.

Financial stability and liquidity of the prospective client also are important. Stability

and liquidity can affect the CPA's choice of auditing procedures and the report

ultimately rendered. A prospective client with liquidity problems, an inability to meet

its financial obligations when they are due, large numbers of transactions with related

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANGEMENT ACCOUNTING

parties, and dependence upon a single customer or a small group of customers should

be carefully considered prior to acceptance.

Professional fee: - the monetary factor also affect the decision making process of the

firm as the company. Generally, the high fee attract the auditor to accept the request

of the audit (Mock, Srivastava and Wright 2017). As the audit firm are also provide

audit services for the making profit the and the audit fee is there main source of

income. Adequate fees must be charged if a client acceptance decision is to attract and

retain competent personnel. Although profitability cannot be allowed to overshadow

integrity, profitability most assuredly must be considered if the CPA is to be

successful (Fortvingler 2016). The fee of the auditor must provide satisfaction to the

auditor in against the work done by the auditor.

Audit planning

The audit procedure is an activity used by the auditor to identify the quality of the

financial information by the clients. There are various procedure available to analyse and

examine the quality of the provided information (Kleinberg, Mullainathan and Raghavan

2016). The whole audit procedure is divided into the three parts that is planning, performing

and reporting.

In the audit planning is an important part of the audit as the all plan and procedure to

perform the audit and to identify the business risk is done in this part (Holmen, Haugen and

Ratvik 2017). The auditor try to identify the audit risk and solve them to the acceptable level.

This is the constant function of the auditor in the entire auditing process of the auditor. The

auditor analyse the various accounting aspect of the Sheridan AV to identify the risk

associated with the sale system, purchase system, inventory, purchase and other important

aspect of financial terms. The auditor plans the timing, nature as well as the extent of the

parties, and dependence upon a single customer or a small group of customers should

be carefully considered prior to acceptance.

Professional fee: - the monetary factor also affect the decision making process of the

firm as the company. Generally, the high fee attract the auditor to accept the request

of the audit (Mock, Srivastava and Wright 2017). As the audit firm are also provide

audit services for the making profit the and the audit fee is there main source of

income. Adequate fees must be charged if a client acceptance decision is to attract and

retain competent personnel. Although profitability cannot be allowed to overshadow

integrity, profitability most assuredly must be considered if the CPA is to be

successful (Fortvingler 2016). The fee of the auditor must provide satisfaction to the

auditor in against the work done by the auditor.

Audit planning

The audit procedure is an activity used by the auditor to identify the quality of the

financial information by the clients. There are various procedure available to analyse and

examine the quality of the provided information (Kleinberg, Mullainathan and Raghavan

2016). The whole audit procedure is divided into the three parts that is planning, performing

and reporting.

In the audit planning is an important part of the audit as the all plan and procedure to

perform the audit and to identify the business risk is done in this part (Holmen, Haugen and

Ratvik 2017). The auditor try to identify the audit risk and solve them to the acceptable level.

This is the constant function of the auditor in the entire auditing process of the auditor. The

auditor analyse the various accounting aspect of the Sheridan AV to identify the risk

associated with the sale system, purchase system, inventory, purchase and other important

aspect of financial terms. The auditor plans the timing, nature as well as the extent of the

5MANGEMENT ACCOUNTING

supervision of the evolved team members and review work. The main importance or the

reason of the audit plan are as follows:-

The audit planning is very important to identify the area of the risk of the material

misstatements (Yoon, Hoogduin and Zhang 2015). The material misstatement means

the disclosure of the unfair information that effect the evaluating process of the

auditor. Here, the auditor plan the entire audit procedure for the Sheridan AV in the

basis of previous identified risks.

Secondly, it is important to develop the procedures to address the identified risks and

also to obtain the sufficient appropriate evidence of the identified material

misstatements.

The planning of the audit also helps the auditor to estimate the cost of the effort made

by the auditor while performing the audit of any firm (Leitch, 2016). This make sure

that the audit cost must be the reasonable for the audit firm as well as the client

company. In this, audit estimates the cost of audit for the Sheridan AV.

The audit planning also reduces the chances of the misunderstand between the audit

firm and the client company (Hines, et al. 2015). A proper planning helps the auditor

to be attentive whole time during the audit.

In context of new client matters, important issues involve with the company as mention

above. First, auditor considers any type of major issues with the with the company for which

the audit will perform. If the auditor found any issues, then it is a big problem for both the

client and the auditor as the auditor owes a duty of care to the clients (Bahr 2018). Secondly,

the auditor will consider the client’s overall financial status, as the client be able to continue

their operation in another year or not. Thirdly, as we all know that the auditing business is not

a charity work. It is also a business and hence auditors confirms that the client should pay the

reasonable audit fees to the audit firm. Finally, the audit firm contacts the former auditor of

supervision of the evolved team members and review work. The main importance or the

reason of the audit plan are as follows:-

The audit planning is very important to identify the area of the risk of the material

misstatements (Yoon, Hoogduin and Zhang 2015). The material misstatement means

the disclosure of the unfair information that effect the evaluating process of the

auditor. Here, the auditor plan the entire audit procedure for the Sheridan AV in the

basis of previous identified risks.

Secondly, it is important to develop the procedures to address the identified risks and

also to obtain the sufficient appropriate evidence of the identified material

misstatements.

The planning of the audit also helps the auditor to estimate the cost of the effort made

by the auditor while performing the audit of any firm (Leitch, 2016). This make sure

that the audit cost must be the reasonable for the audit firm as well as the client

company. In this, audit estimates the cost of audit for the Sheridan AV.

The audit planning also reduces the chances of the misunderstand between the audit

firm and the client company (Hines, et al. 2015). A proper planning helps the auditor

to be attentive whole time during the audit.

In context of new client matters, important issues involve with the company as mention

above. First, auditor considers any type of major issues with the with the company for which

the audit will perform. If the auditor found any issues, then it is a big problem for both the

client and the auditor as the auditor owes a duty of care to the clients (Bahr 2018). Secondly,

the auditor will consider the client’s overall financial status, as the client be able to continue

their operation in another year or not. Thirdly, as we all know that the auditing business is not

a charity work. It is also a business and hence auditors confirms that the client should pay the

reasonable audit fees to the audit firm. Finally, the audit firm contacts the former auditor of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANGEMENT ACCOUNTING

the company to ask the information about the specific issues that need attention related to the

client (Menon and Williams 2016). In the given case study, the auditor perform the several

testing to identify the business risk associated with the company. The main test that are used

in the provided case are valuation test, dual aspect test, classification test and occurrence test.

The auditor performs the valuation test, to determine the truthfulness of the

information provided by the firm. The valuation test tests the value of the different account

provided by the firm. The dual aspect test is the method of verification of any information. In

this, the auditor verifies the both the end of the transaction (Fan, Nagarajan and Smith 2015).

Classification test are used to ensure that the company is properly done the classification of

the different accounts while preparing the financial report or not. Lastly, the occurrence test

are those test that verifies the information of the company is actually occurred or not.

Preliminarily risk assessment

The preliminarily risk assessment is the process of identifying the risk associated with

the information provided by the client in the initial stage of the introduction. The preliminary

risk are those risks that are associated with the initial information provided by the company

or the identified the auditor in the earlier stage of the introduction (Mao, Ettredge and Stone

2019). This risk are generally identified at the time of the introduction phase when the auditor

try to understand or start knowing about the firm. Here, in this case, the initial risks identified

by the auditor at the time of knowing the firm is consider as the preliminary risk assessment.

Here, the report highlight various risk associated with the Sheridan AV. The maximum level

of the risk is associated with the non- current assets, Valuation of the inventory, purchasing

system of the firm, sale system of the firm, cash and revenue of the company (Khalil and

Mazboudi 2016). The auditor performs the various test in respect of the identified risk like

the classification test, dual aspect test and valuation test. These test also help the auditor to

provide and recommend the proper solution of the identified risk.

the company to ask the information about the specific issues that need attention related to the

client (Menon and Williams 2016). In the given case study, the auditor perform the several

testing to identify the business risk associated with the company. The main test that are used

in the provided case are valuation test, dual aspect test, classification test and occurrence test.

The auditor performs the valuation test, to determine the truthfulness of the

information provided by the firm. The valuation test tests the value of the different account

provided by the firm. The dual aspect test is the method of verification of any information. In

this, the auditor verifies the both the end of the transaction (Fan, Nagarajan and Smith 2015).

Classification test are used to ensure that the company is properly done the classification of

the different accounts while preparing the financial report or not. Lastly, the occurrence test

are those test that verifies the information of the company is actually occurred or not.

Preliminarily risk assessment

The preliminarily risk assessment is the process of identifying the risk associated with

the information provided by the client in the initial stage of the introduction. The preliminary

risk are those risks that are associated with the initial information provided by the company

or the identified the auditor in the earlier stage of the introduction (Mao, Ettredge and Stone

2019). This risk are generally identified at the time of the introduction phase when the auditor

try to understand or start knowing about the firm. Here, in this case, the initial risks identified

by the auditor at the time of knowing the firm is consider as the preliminary risk assessment.

Here, the report highlight various risk associated with the Sheridan AV. The maximum level

of the risk is associated with the non- current assets, Valuation of the inventory, purchasing

system of the firm, sale system of the firm, cash and revenue of the company (Khalil and

Mazboudi 2016). The auditor performs the various test in respect of the identified risk like

the classification test, dual aspect test and valuation test. These test also help the auditor to

provide and recommend the proper solution of the identified risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANGEMENT ACCOUNTING

Preliminarily materiality calculation

The preliminarily materiality calculation is the process of calculating the risk

associated with the initial information provided by the company to the auditor. The auditor

firstly, identifies the preliminarily risk and then start to collect the evidences of such risk.

After, collecting the evidence of the preliminarily risk, the auditor calculate the level of risk

associated with the information and the areas of such risk (Lai and Chen 2015). The

materiality calculation helps the auditor to meet the preliminarily risk and reduce the level of

such risk to the certain acceptable risk. This kind of the risk and the process of meeting it is

performed by the auditor in the planning and performing phase of the audit. In the given case

study the auditor perform the preliminarily materiality calculation by collecting the various

financial information of the company and documents of the Sheridan AV. The auditor collect

the financial report of the company, all purchase vouchers and sell vouchers, records of the

inventories and other details related to the cash transaction of the firm for the last year.

Inherent risks

The inherent risks are those risks of material misstatement in the financial statements

arising due to the error of omission or due to the factors other than the failure of control. In

simple words, the inherent risks are those risk which are associated with the financial

information of the company and generally rises due to the error of omission. The error of

omission occurs when the accountant of the firm fully omitted the transaction from the

accounting book. In the given case study the following are the main inherent risk are

identified by the auditor. Here, the main inherent risk identified by the auditor are non-

current asset, revenue and cash. The above stated three areas has the highest risk of material

misstatement as based on the control performance of the company (Knechel and Salterio

2016). To address this risks the auditor analyse the financial report of the company, all

Preliminarily materiality calculation

The preliminarily materiality calculation is the process of calculating the risk

associated with the initial information provided by the company to the auditor. The auditor

firstly, identifies the preliminarily risk and then start to collect the evidences of such risk.

After, collecting the evidence of the preliminarily risk, the auditor calculate the level of risk

associated with the information and the areas of such risk (Lai and Chen 2015). The

materiality calculation helps the auditor to meet the preliminarily risk and reduce the level of

such risk to the certain acceptable risk. This kind of the risk and the process of meeting it is

performed by the auditor in the planning and performing phase of the audit. In the given case

study the auditor perform the preliminarily materiality calculation by collecting the various

financial information of the company and documents of the Sheridan AV. The auditor collect

the financial report of the company, all purchase vouchers and sell vouchers, records of the

inventories and other details related to the cash transaction of the firm for the last year.

Inherent risks

The inherent risks are those risks of material misstatement in the financial statements

arising due to the error of omission or due to the factors other than the failure of control. In

simple words, the inherent risks are those risk which are associated with the financial

information of the company and generally rises due to the error of omission. The error of

omission occurs when the accountant of the firm fully omitted the transaction from the

accounting book. In the given case study the following are the main inherent risk are

identified by the auditor. Here, the main inherent risk identified by the auditor are non-

current asset, revenue and cash. The above stated three areas has the highest risk of material

misstatement as based on the control performance of the company (Knechel and Salterio

2016). To address this risks the auditor analyse the financial report of the company, all

8MANGEMENT ACCOUNTING

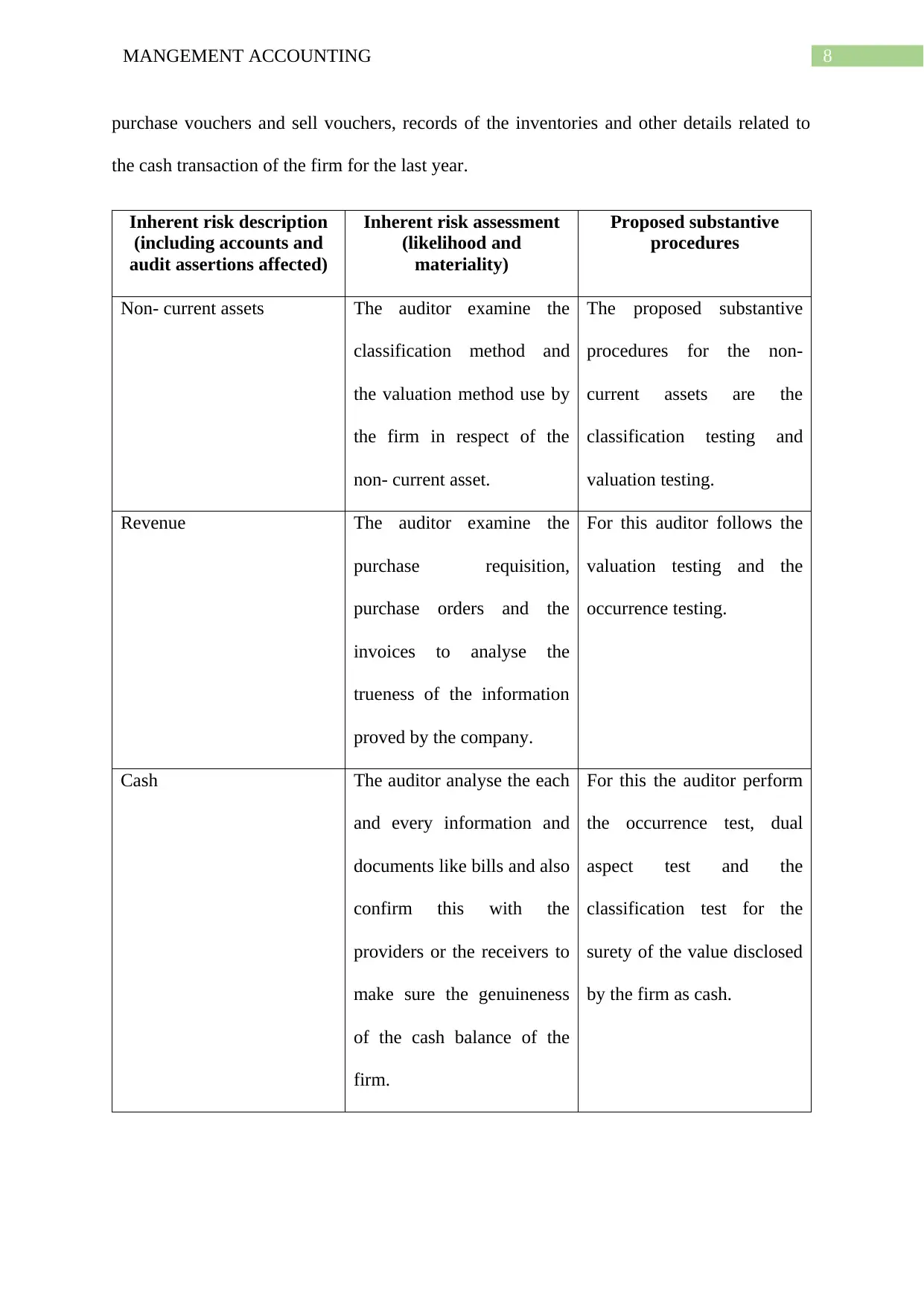

purchase vouchers and sell vouchers, records of the inventories and other details related to

the cash transaction of the firm for the last year.

Inherent risk description

(including accounts and

audit assertions affected)

Inherent risk assessment

(likelihood and

materiality)

Proposed substantive

procedures

Non- current assets The auditor examine the

classification method and

the valuation method use by

the firm in respect of the

non- current asset.

The proposed substantive

procedures for the non-

current assets are the

classification testing and

valuation testing.

Revenue The auditor examine the

purchase requisition,

purchase orders and the

invoices to analyse the

trueness of the information

proved by the company.

For this auditor follows the

valuation testing and the

occurrence testing.

Cash The auditor analyse the each

and every information and

documents like bills and also

confirm this with the

providers or the receivers to

make sure the genuineness

of the cash balance of the

firm.

For this the auditor perform

the occurrence test, dual

aspect test and the

classification test for the

surety of the value disclosed

by the firm as cash.

purchase vouchers and sell vouchers, records of the inventories and other details related to

the cash transaction of the firm for the last year.

Inherent risk description

(including accounts and

audit assertions affected)

Inherent risk assessment

(likelihood and

materiality)

Proposed substantive

procedures

Non- current assets The auditor examine the

classification method and

the valuation method use by

the firm in respect of the

non- current asset.

The proposed substantive

procedures for the non-

current assets are the

classification testing and

valuation testing.

Revenue The auditor examine the

purchase requisition,

purchase orders and the

invoices to analyse the

trueness of the information

proved by the company.

For this auditor follows the

valuation testing and the

occurrence testing.

Cash The auditor analyse the each

and every information and

documents like bills and also

confirm this with the

providers or the receivers to

make sure the genuineness

of the cash balance of the

firm.

For this the auditor perform

the occurrence test, dual

aspect test and the

classification test for the

surety of the value disclosed

by the firm as cash.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANGEMENT ACCOUNTING

Control risk

The control risks are those risks of a material misstatement in the financial statements

arising due to absence or failure in the operation of relevant controls of the entity. In simple

words, the control risks are material misstatement of the financial information generally

arises due the improper control function performed by the management of the firm. The

management must perform their control function to prevent this kind of risk and safe the

company and other stakeholder of the company from the malfunction and the frauds. Thee

auditor identified the purchasing system of the company, selling system of the company and

the method used by the company to value the inventories as the highest risk associated area

off the given company. To address this risk and to bring it into the acceptable level, the

auditor collect, analyse and examine the various accounting details and information of the

company. The auditor analyse the annual report of the firm for the last year (Knechel 2017).

The auditor also examine the different methods used by the management of the firm, the

policies and procedure of the management to perform the control function in the business

operations of the firm.

Control risks (including

accounts and audit

assertions affected)

Control risk assessment

(likelihood and

materiality)

Proposed internal controls

Sales System High For this the management of

the company need to hire

proper knowledgeable

accountant who has the

ability to perform the control

function for the company to

reduce the material

Control risk

The control risks are those risks of a material misstatement in the financial statements

arising due to absence or failure in the operation of relevant controls of the entity. In simple

words, the control risks are material misstatement of the financial information generally

arises due the improper control function performed by the management of the firm. The

management must perform their control function to prevent this kind of risk and safe the

company and other stakeholder of the company from the malfunction and the frauds. Thee

auditor identified the purchasing system of the company, selling system of the company and

the method used by the company to value the inventories as the highest risk associated area

off the given company. To address this risk and to bring it into the acceptable level, the

auditor collect, analyse and examine the various accounting details and information of the

company. The auditor analyse the annual report of the firm for the last year (Knechel 2017).

The auditor also examine the different methods used by the management of the firm, the

policies and procedure of the management to perform the control function in the business

operations of the firm.

Control risks (including

accounts and audit

assertions affected)

Control risk assessment

(likelihood and

materiality)

Proposed internal controls

Sales System High For this the management of

the company need to hire

proper knowledgeable

accountant who has the

ability to perform the control

function for the company to

reduce the material

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANGEMENT ACCOUNTING

misstatement.

Purchase system High The management of the firm

need to maintain the proper

purchasing system in the

operation of the firm. The

management also need to

review the performance of

the purchase system adopted

by the firm and make timely

changes in the system if

required.

Inventory valuation system High For this management need to

perform their control

function properly. The

management need to verify

the valuation of the

inventory in dual aspect

valuation procedure. Along

with the timely reviewing of

the results and

performances.

Conclusion

The paper concludes that the Sheridan AV is a retail and whole- sale company of the

electronics products. The client acceptance decision of the audit firm is affected by the

misstatement.

Purchase system High The management of the firm

need to maintain the proper

purchasing system in the

operation of the firm. The

management also need to

review the performance of

the purchase system adopted

by the firm and make timely

changes in the system if

required.

Inventory valuation system High For this management need to

perform their control

function properly. The

management need to verify

the valuation of the

inventory in dual aspect

valuation procedure. Along

with the timely reviewing of

the results and

performances.

Conclusion

The paper concludes that the Sheridan AV is a retail and whole- sale company of the

electronics products. The client acceptance decision of the audit firm is affected by the

11MANGEMENT ACCOUNTING

management integrity of the company, professional relationship of the firm with the other,

technical ascertains, risk association and the professional fee. The audit plan for the provided

company is to examine the various high- risk associated information provided by the firm by

performing the various tests like occurrence test, dual aspect test, classification test and

valuation test. Further, the report concludes that the highest inherent risk associated areas of

the company are cash, revenue and non- current assets. While, the highest control risk

associated areas of the company are the purchasing system of the company, selling system of

the company and the method used by the company to value the inventories. The auditor use

various test to identify them and policy and procedures to minimise the associated risk to the

certain acceptable level.

management integrity of the company, professional relationship of the firm with the other,

technical ascertains, risk association and the professional fee. The audit plan for the provided

company is to examine the various high- risk associated information provided by the firm by

performing the various tests like occurrence test, dual aspect test, classification test and

valuation test. Further, the report concludes that the highest inherent risk associated areas of

the company are cash, revenue and non- current assets. While, the highest control risk

associated areas of the company are the purchasing system of the company, selling system of

the company and the method used by the company to value the inventories. The auditor use

various test to identify them and policy and procedures to minimise the associated risk to the

certain acceptable level.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.