Billing Boats AS: Detailed Financial Analysis and Profit Projections

VerifiedAdded on 2020/02/03

|5

|617

|176

Report

AI Summary

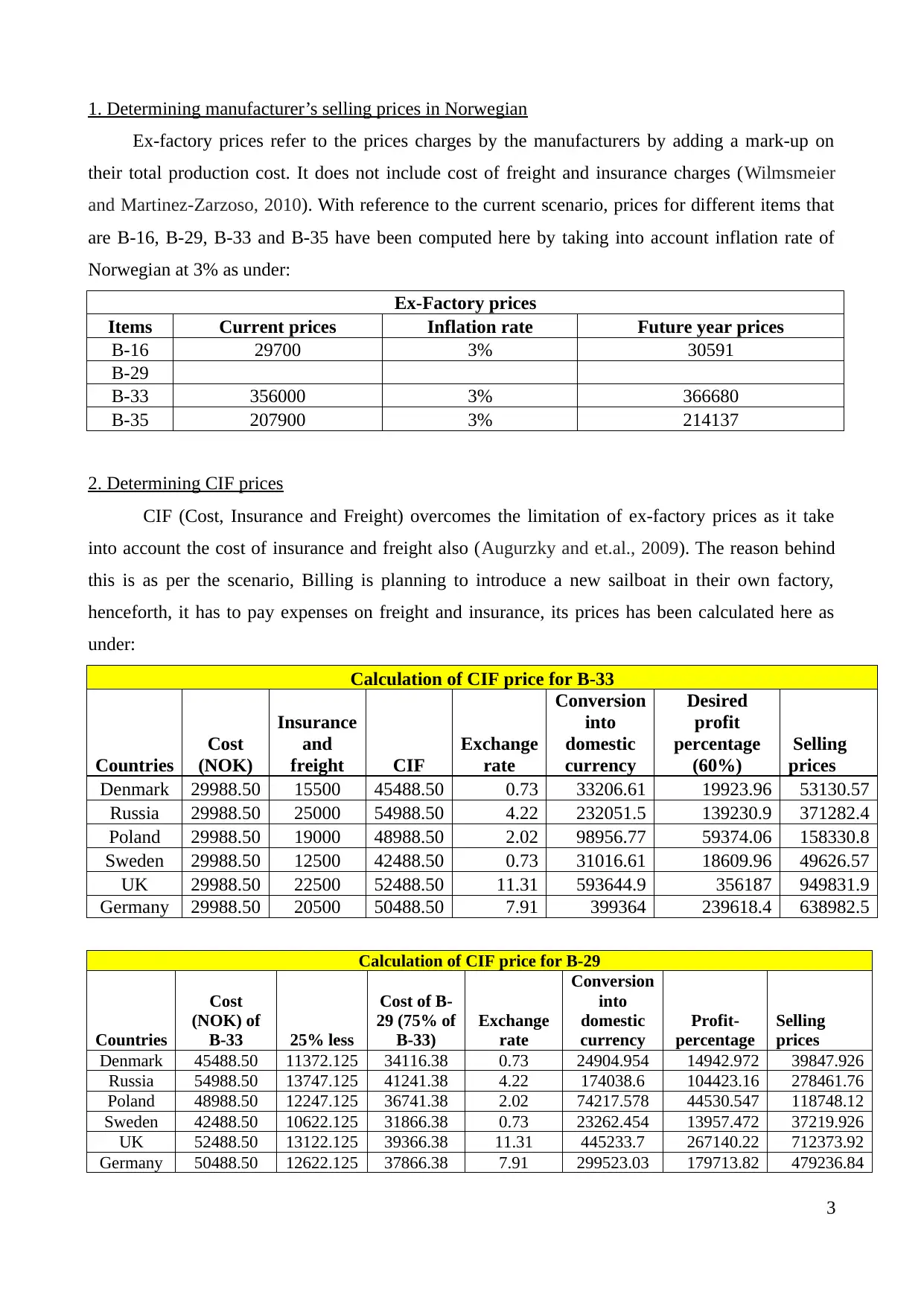

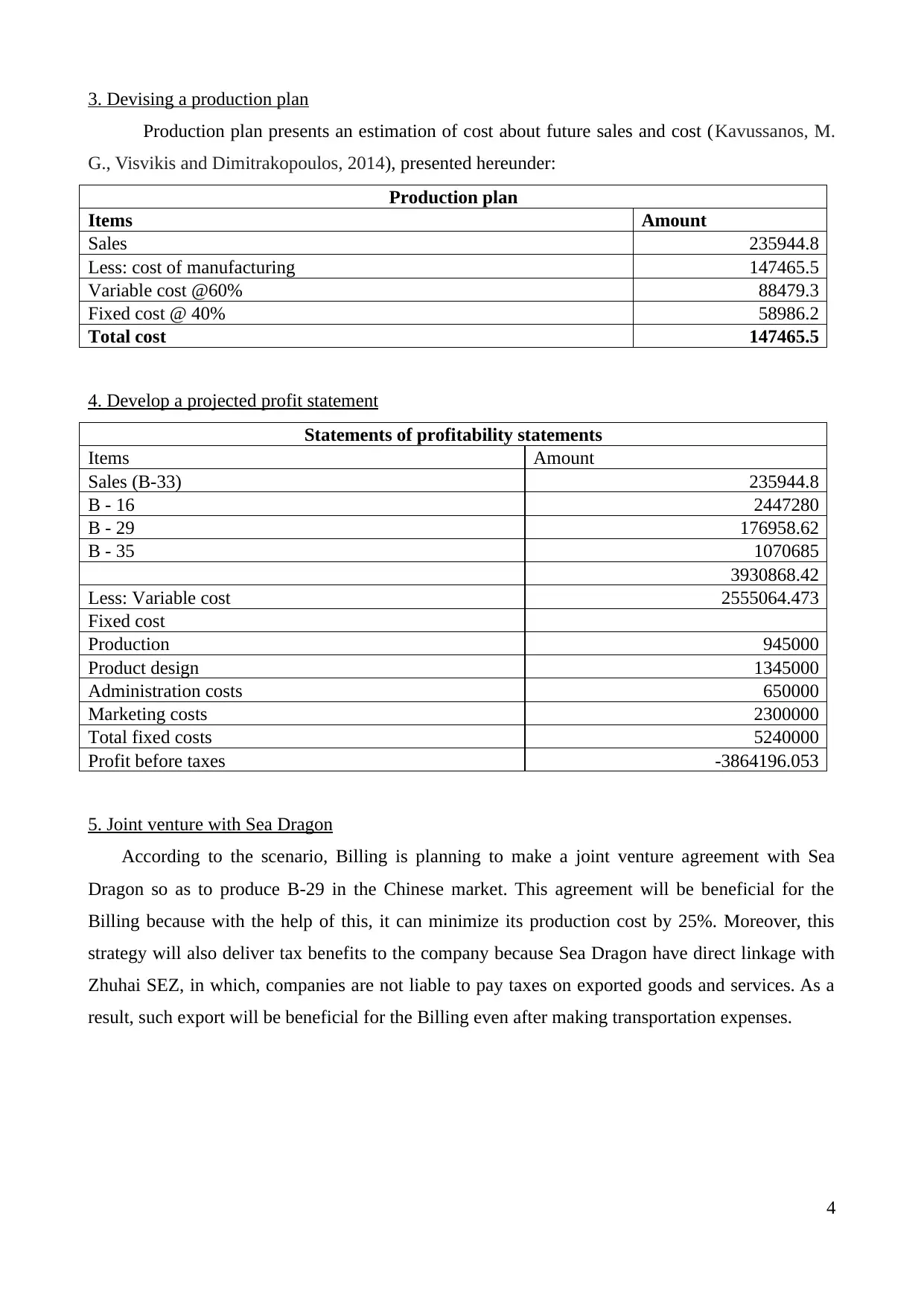

This report provides a financial analysis of Billing Boats AS, focusing on key aspects such as determining manufacturer's selling prices (ex-factory prices) in Norwegian currency, calculating CIF (Cost, Insurance, and Freight) prices, and devising a production plan. The analysis includes calculations of future year prices considering an inflation rate, along with the components of CIF prices. A projected profit statement is developed, outlining sales, variable and fixed costs, and resulting profit or loss before taxes. Furthermore, the report explores a potential joint venture with Sea Dragon, highlighting the benefits of reduced production costs and tax advantages through access to the Zhuhai SEZ. The report uses cited references to support the financial analyses and strategic recommendations.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.