Analysis of Sami Design Ltd. Job Costing and Overhead Allocation

VerifiedAdded on 2023/01/11

|11

|2518

|65

Homework Assignment

AI Summary

This assignment addresses job costing for Sami Design Ltd., a manufacturer of musical instruments. It begins by calculating the predetermined overhead rate and then completes a job cost sheet for a specific job. The solution includes preparing journal entries to record March's events, setting up le...

Manufacturing job

costing

costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

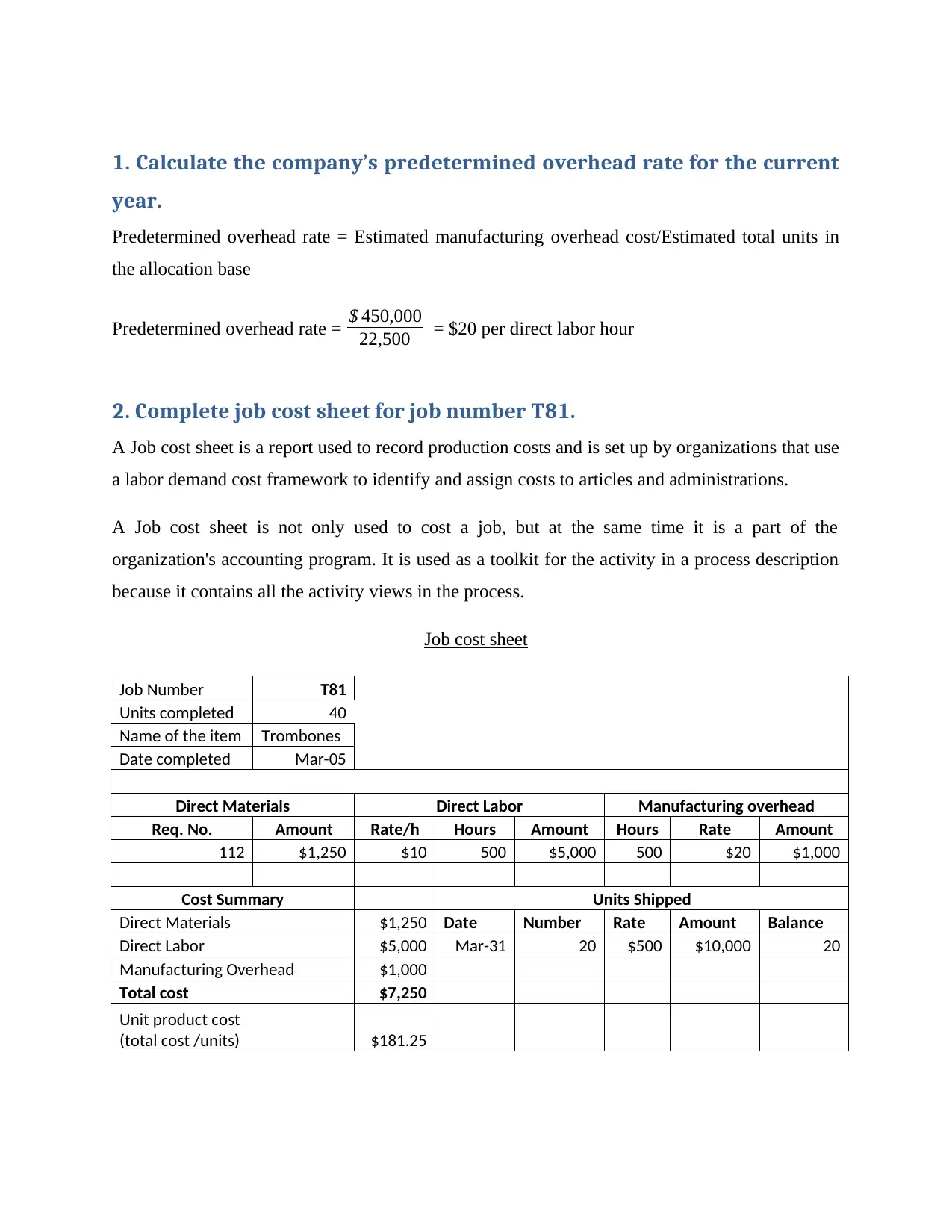

1. Calculate the company’s predetermined overhead rate for the current

year.

Predetermined overhead rate = Estimated manufacturing overhead cost/Estimated total units in

the allocation base

Predetermined overhead rate = $ 450,000

22,500 = $20 per direct labor hour

2. Complete job cost sheet for job number T81.

A Job cost sheet is a report used to record production costs and is set up by organizations that use

a labor demand cost framework to identify and assign costs to articles and administrations.

A Job cost sheet is not only used to cost a job, but at the same time it is a part of the

organization's accounting program. It is used as a toolkit for the activity in a process description

because it contains all the activity views in the process.

Job cost sheet

Job Number T81

Units completed 40

Name of the item Trombones

Date completed Mar-05

Direct Materials Direct Labor Manufacturing overhead

Req. No. Amount Rate/h Hours Amount Hours Rate Amount

112 $1,250 $10 500 $5,000 500 $20 $1,000

Cost Summary Units Shipped

Direct Materials $1,250 Date Number Rate Amount Balance

Direct Labor $5,000 Mar-31 20 $500 $10,000 20

Manufacturing Overhead $1,000

Total cost $7,250

Unit product cost

(total cost /units) $181.25

year.

Predetermined overhead rate = Estimated manufacturing overhead cost/Estimated total units in

the allocation base

Predetermined overhead rate = $ 450,000

22,500 = $20 per direct labor hour

2. Complete job cost sheet for job number T81.

A Job cost sheet is a report used to record production costs and is set up by organizations that use

a labor demand cost framework to identify and assign costs to articles and administrations.

A Job cost sheet is not only used to cost a job, but at the same time it is a part of the

organization's accounting program. It is used as a toolkit for the activity in a process description

because it contains all the activity views in the process.

Job cost sheet

Job Number T81

Units completed 40

Name of the item Trombones

Date completed Mar-05

Direct Materials Direct Labor Manufacturing overhead

Req. No. Amount Rate/h Hours Amount Hours Rate Amount

112 $1,250 $10 500 $5,000 500 $20 $1,000

Cost Summary Units Shipped

Direct Materials $1,250 Date Number Rate Amount Balance

Direct Labor $5,000 Mar-31 20 $500 $10,000 20

Manufacturing Overhead $1,000

Total cost $7,250

Unit product cost

(total cost /units) $181.25

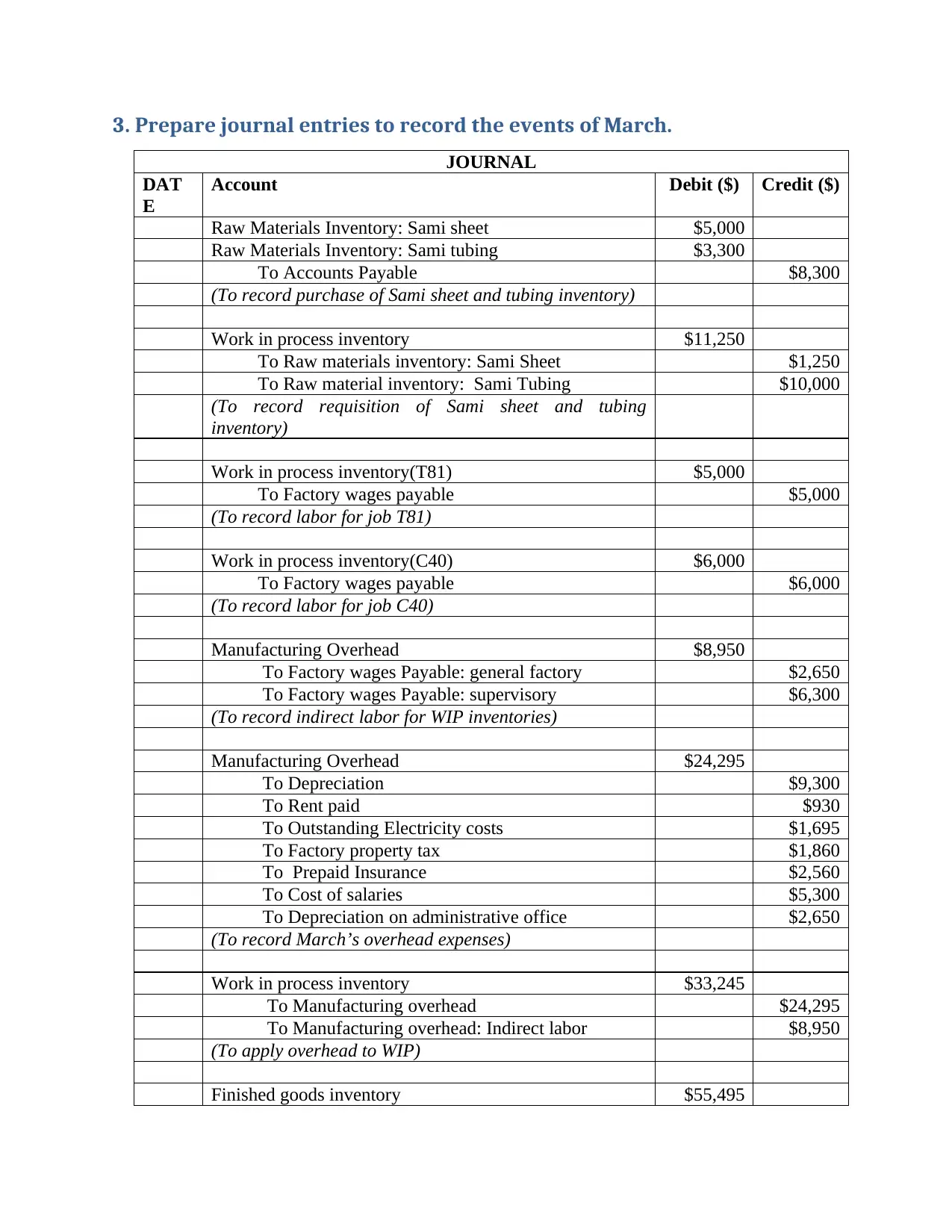

3. Prepare journal entries to record the events of March.

JOURNAL

DAT

E

Account Debit ($) Credit ($)

Raw Materials Inventory: Sami sheet $5,000

Raw Materials Inventory: Sami tubing $3,300

To Accounts Payable $8,300

(To record purchase of Sami sheet and tubing inventory)

Work in process inventory $11,250

To Raw materials inventory: Sami Sheet $1,250

To Raw material inventory: Sami Tubing $10,000

(To record requisition of Sami sheet and tubing

inventory)

Work in process inventory(T81) $5,000

To Factory wages payable $5,000

(To record labor for job T81)

Work in process inventory(C40) $6,000

To Factory wages payable $6,000

(To record labor for job C40)

Manufacturing Overhead $8,950

To Factory wages Payable: general factory $2,650

To Factory wages Payable: supervisory $6,300

(To record indirect labor for WIP inventories)

Manufacturing Overhead $24,295

To Depreciation $9,300

To Rent paid $930

To Outstanding Electricity costs $1,695

To Factory property tax $1,860

To Prepaid Insurance $2,560

To Cost of salaries $5,300

To Depreciation on administrative office $2,650

(To record March’s overhead expenses)

Work in process inventory $33,245

To Manufacturing overhead $24,295

To Manufacturing overhead: Indirect labor $8,950

(To apply overhead to WIP)

Finished goods inventory $55,495

JOURNAL

DAT

E

Account Debit ($) Credit ($)

Raw Materials Inventory: Sami sheet $5,000

Raw Materials Inventory: Sami tubing $3,300

To Accounts Payable $8,300

(To record purchase of Sami sheet and tubing inventory)

Work in process inventory $11,250

To Raw materials inventory: Sami Sheet $1,250

To Raw material inventory: Sami Tubing $10,000

(To record requisition of Sami sheet and tubing

inventory)

Work in process inventory(T81) $5,000

To Factory wages payable $5,000

(To record labor for job T81)

Work in process inventory(C40) $6,000

To Factory wages payable $6,000

(To record labor for job C40)

Manufacturing Overhead $8,950

To Factory wages Payable: general factory $2,650

To Factory wages Payable: supervisory $6,300

(To record indirect labor for WIP inventories)

Manufacturing Overhead $24,295

To Depreciation $9,300

To Rent paid $930

To Outstanding Electricity costs $1,695

To Factory property tax $1,860

To Prepaid Insurance $2,560

To Cost of salaries $5,300

To Depreciation on administrative office $2,650

(To record March’s overhead expenses)

Work in process inventory $33,245

To Manufacturing overhead $24,295

To Manufacturing overhead: Indirect labor $8,950

(To apply overhead to WIP)

Finished goods inventory $55,495

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To WIP: Material $11,250

To WIP: Direct Labor $11,000

To WIP: Manufacturing overhead $33,245

(To transfer work in process to finished goods)

Cost of goods sold $55,495

To finished goods $55,495

(To transfer finished goods to cost of goods sold)

Accounts receivable $10,000

To Sales $10,000

(To record the sale of the goods)

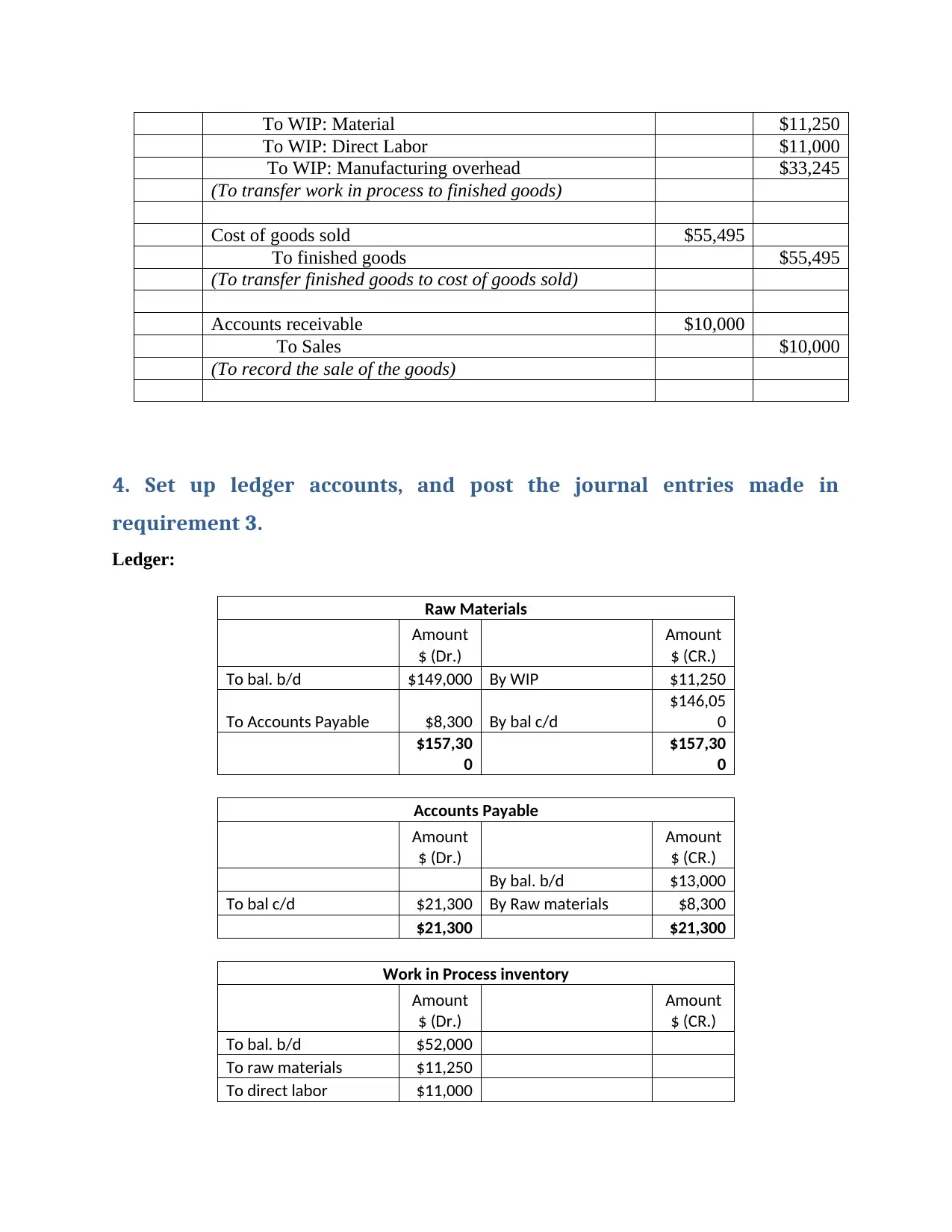

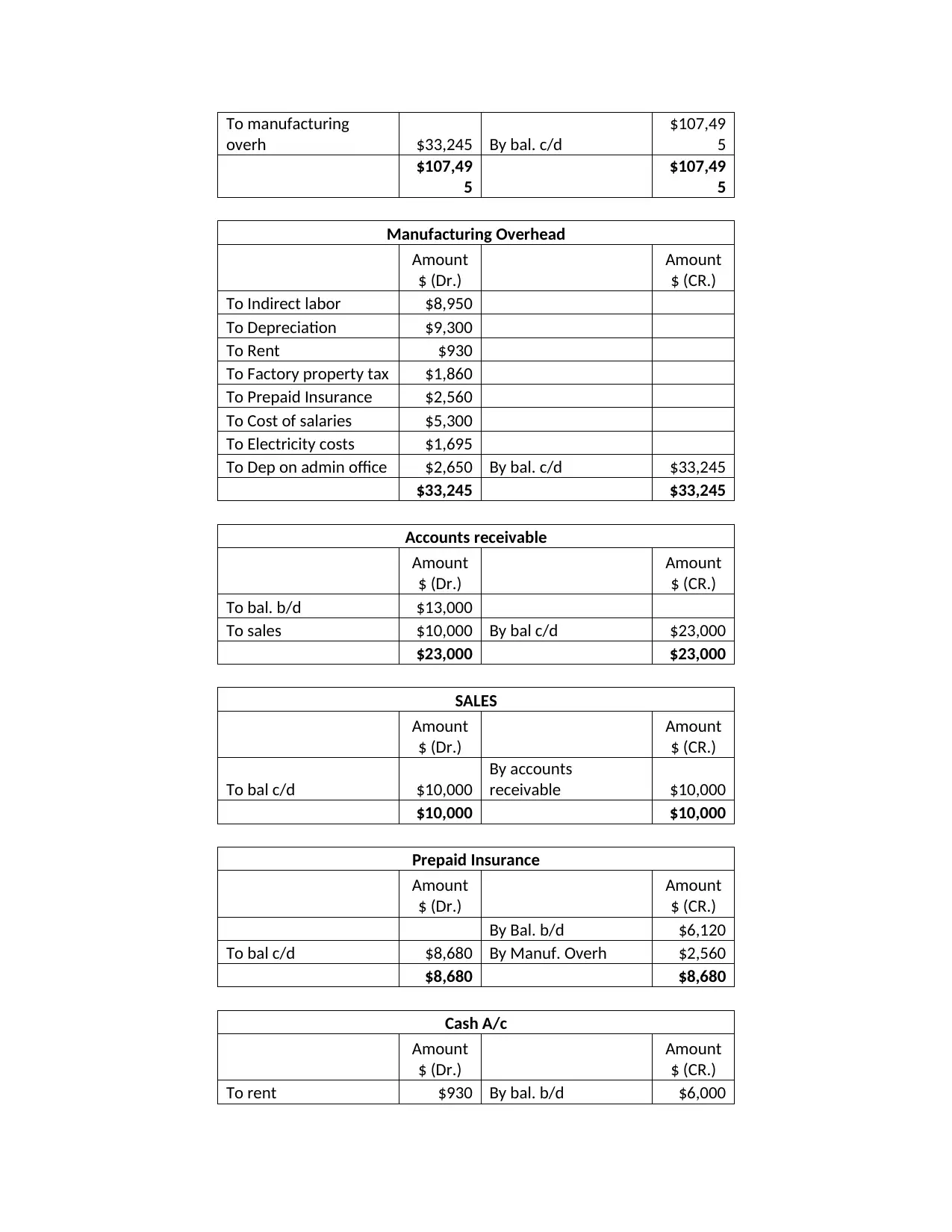

4. Set up ledger accounts, and post the journal entries made in

requirement 3.

Ledger:

Raw Materials

Amount

$ (Dr.)

Amount

$ (CR.)

To bal. b/d $149,000 By WIP $11,250

To Accounts Payable $8,300 By bal c/d

$146,05

0

$157,30

0

$157,30

0

Accounts Payable

Amount

$ (Dr.)

Amount

$ (CR.)

By bal. b/d $13,000

To bal c/d $21,300 By Raw materials $8,300

$21,300 $21,300

Work in Process inventory

Amount

$ (Dr.)

Amount

$ (CR.)

To bal. b/d $52,000

To raw materials $11,250

To direct labor $11,000

To WIP: Direct Labor $11,000

To WIP: Manufacturing overhead $33,245

(To transfer work in process to finished goods)

Cost of goods sold $55,495

To finished goods $55,495

(To transfer finished goods to cost of goods sold)

Accounts receivable $10,000

To Sales $10,000

(To record the sale of the goods)

4. Set up ledger accounts, and post the journal entries made in

requirement 3.

Ledger:

Raw Materials

Amount

$ (Dr.)

Amount

$ (CR.)

To bal. b/d $149,000 By WIP $11,250

To Accounts Payable $8,300 By bal c/d

$146,05

0

$157,30

0

$157,30

0

Accounts Payable

Amount

$ (Dr.)

Amount

$ (CR.)

By bal. b/d $13,000

To bal c/d $21,300 By Raw materials $8,300

$21,300 $21,300

Work in Process inventory

Amount

$ (Dr.)

Amount

$ (CR.)

To bal. b/d $52,000

To raw materials $11,250

To direct labor $11,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To manufacturing

overh $33,245 By bal. c/d

$107,49

5

$107,49

5

$107,49

5

Manufacturing Overhead

Amount

$ (Dr.)

Amount

$ (CR.)

To Indirect labor $8,950

To Depreciation $9,300

To Rent $930

To Factory property tax $1,860

To Prepaid Insurance $2,560

To Cost of salaries $5,300

To Electricity costs $1,695

To Dep on admin office $2,650 By bal. c/d $33,245

$33,245 $33,245

Accounts receivable

Amount

$ (Dr.)

Amount

$ (CR.)

To bal. b/d $13,000

To sales $10,000 By bal c/d $23,000

$23,000 $23,000

SALES

Amount

$ (Dr.)

Amount

$ (CR.)

To bal c/d $10,000

By accounts

receivable $10,000

$10,000 $10,000

Prepaid Insurance

Amount

$ (Dr.)

Amount

$ (CR.)

By Bal. b/d $6,120

To bal c/d $8,680 By Manuf. Overh $2,560

$8,680 $8,680

Cash A/c

Amount

$ (Dr.)

Amount

$ (CR.)

To rent $930 By bal. b/d $6,000

overh $33,245 By bal. c/d

$107,49

5

$107,49

5

$107,49

5

Manufacturing Overhead

Amount

$ (Dr.)

Amount

$ (CR.)

To Indirect labor $8,950

To Depreciation $9,300

To Rent $930

To Factory property tax $1,860

To Prepaid Insurance $2,560

To Cost of salaries $5,300

To Electricity costs $1,695

To Dep on admin office $2,650 By bal. c/d $33,245

$33,245 $33,245

Accounts receivable

Amount

$ (Dr.)

Amount

$ (CR.)

To bal. b/d $13,000

To sales $10,000 By bal c/d $23,000

$23,000 $23,000

SALES

Amount

$ (Dr.)

Amount

$ (CR.)

To bal c/d $10,000

By accounts

receivable $10,000

$10,000 $10,000

Prepaid Insurance

Amount

$ (Dr.)

Amount

$ (CR.)

By Bal. b/d $6,120

To bal c/d $8,680 By Manuf. Overh $2,560

$8,680 $8,680

Cash A/c

Amount

$ (Dr.)

Amount

$ (CR.)

To rent $930 By bal. b/d $6,000

To bal c/d $5,070

$6,000 $6,000

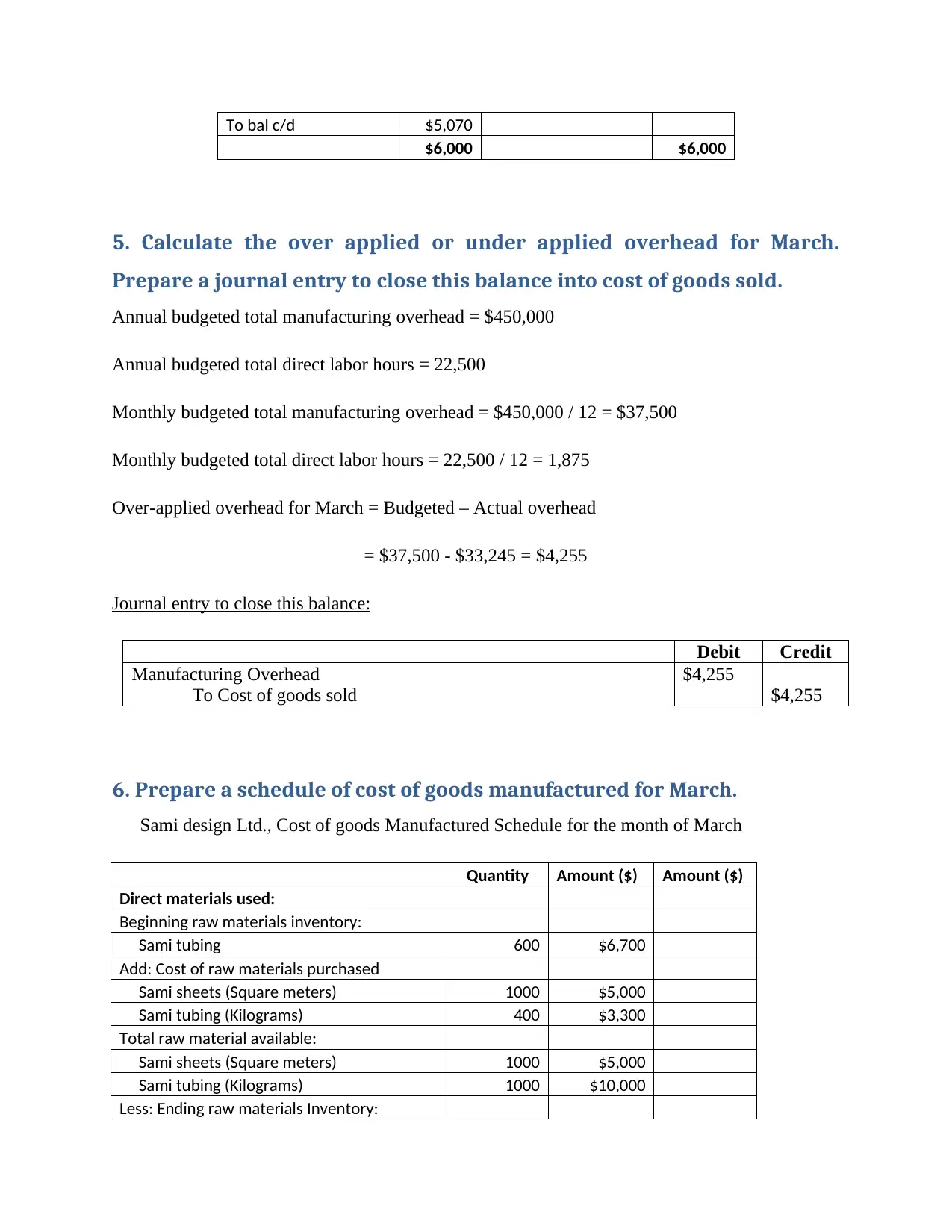

5. Calculate the over applied or under applied overhead for March.

Prepare a journal entry to close this balance into cost of goods sold.

Annual budgeted total manufacturing overhead = $450,000

Annual budgeted total direct labor hours = 22,500

Monthly budgeted total manufacturing overhead = $450,000 / 12 = $37,500

Monthly budgeted total direct labor hours = 22,500 / 12 = 1,875

Over-applied overhead for March = Budgeted – Actual overhead

= $37,500 - $33,245 = $4,255

Journal entry to close this balance:

Debit Credit

Manufacturing Overhead

To Cost of goods sold

$4,255

$4,255

6. Prepare a schedule of cost of goods manufactured for March.

Sami design Ltd., Cost of goods Manufactured Schedule for the month of March

Quantity Amount ($) Amount ($)

Direct materials used:

Beginning raw materials inventory:

Sami tubing 600 $6,700

Add: Cost of raw materials purchased

Sami sheets (Square meters) 1000 $5,000

Sami tubing (Kilograms) 400 $3,300

Total raw material available:

Sami sheets (Square meters) 1000 $5,000

Sami tubing (Kilograms) 1000 $10,000

Less: Ending raw materials Inventory:

$6,000 $6,000

5. Calculate the over applied or under applied overhead for March.

Prepare a journal entry to close this balance into cost of goods sold.

Annual budgeted total manufacturing overhead = $450,000

Annual budgeted total direct labor hours = 22,500

Monthly budgeted total manufacturing overhead = $450,000 / 12 = $37,500

Monthly budgeted total direct labor hours = 22,500 / 12 = 1,875

Over-applied overhead for March = Budgeted – Actual overhead

= $37,500 - $33,245 = $4,255

Journal entry to close this balance:

Debit Credit

Manufacturing Overhead

To Cost of goods sold

$4,255

$4,255

6. Prepare a schedule of cost of goods manufactured for March.

Sami design Ltd., Cost of goods Manufactured Schedule for the month of March

Quantity Amount ($) Amount ($)

Direct materials used:

Beginning raw materials inventory:

Sami tubing 600 $6,700

Add: Cost of raw materials purchased

Sami sheets (Square meters) 1000 $5,000

Sami tubing (Kilograms) 400 $3,300

Total raw material available:

Sami sheets (Square meters) 1000 $5,000

Sami tubing (Kilograms) 1000 $10,000

Less: Ending raw materials Inventory:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

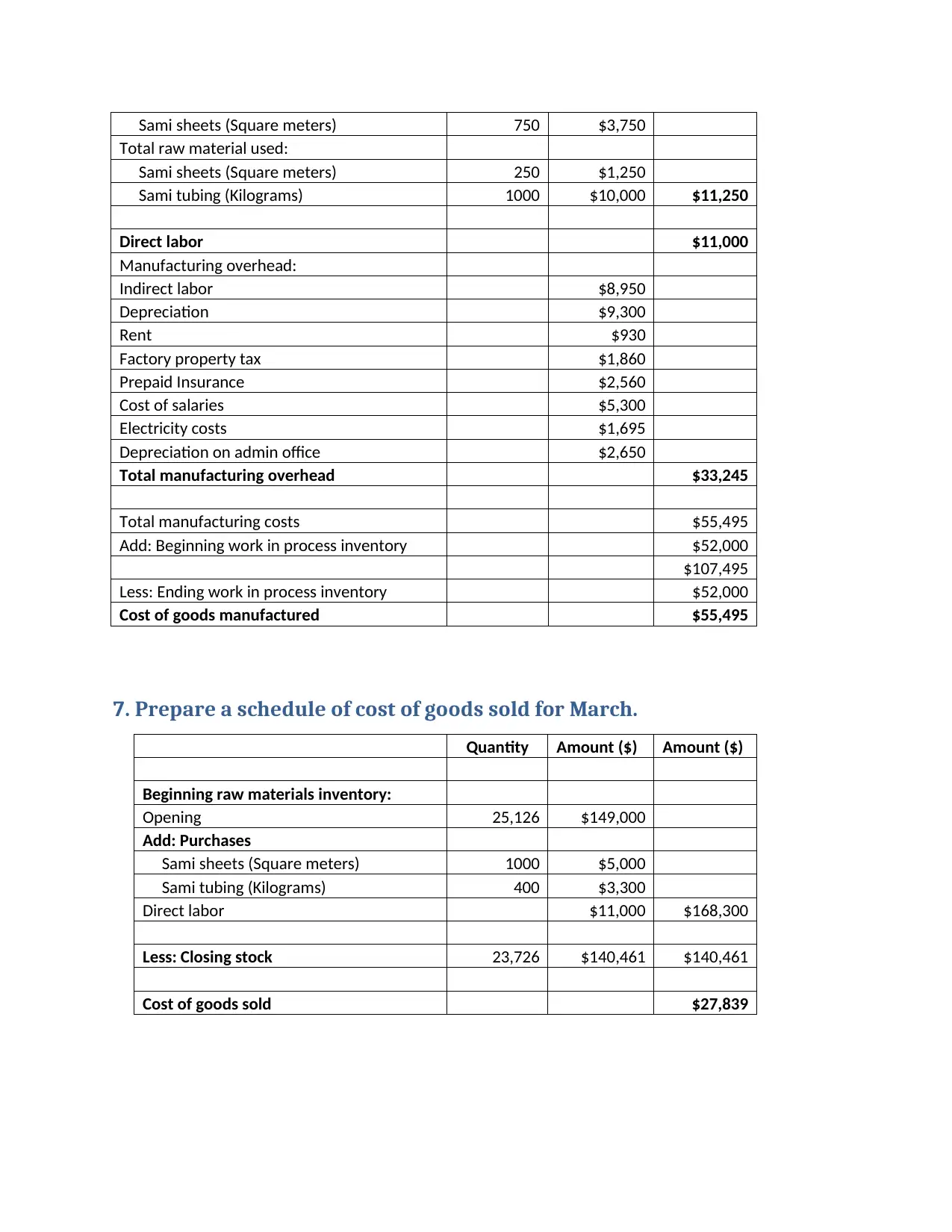

Sami sheets (Square meters) 750 $3,750

Total raw material used:

Sami sheets (Square meters) 250 $1,250

Sami tubing (Kilograms) 1000 $10,000 $11,250

Direct labor $11,000

Manufacturing overhead:

Indirect labor $8,950

Depreciation $9,300

Rent $930

Factory property tax $1,860

Prepaid Insurance $2,560

Cost of salaries $5,300

Electricity costs $1,695

Depreciation on admin office $2,650

Total manufacturing overhead $33,245

Total manufacturing costs $55,495

Add: Beginning work in process inventory $52,000

$107,495

Less: Ending work in process inventory $52,000

Cost of goods manufactured $55,495

7. Prepare a schedule of cost of goods sold for March.

Quantity Amount ($) Amount ($)

Beginning raw materials inventory:

Opening 25,126 $149,000

Add: Purchases

Sami sheets (Square meters) 1000 $5,000

Sami tubing (Kilograms) 400 $3,300

Direct labor $11,000 $168,300

Less: Closing stock 23,726 $140,461 $140,461

Cost of goods sold $27,839

Total raw material used:

Sami sheets (Square meters) 250 $1,250

Sami tubing (Kilograms) 1000 $10,000 $11,250

Direct labor $11,000

Manufacturing overhead:

Indirect labor $8,950

Depreciation $9,300

Rent $930

Factory property tax $1,860

Prepaid Insurance $2,560

Cost of salaries $5,300

Electricity costs $1,695

Depreciation on admin office $2,650

Total manufacturing overhead $33,245

Total manufacturing costs $55,495

Add: Beginning work in process inventory $52,000

$107,495

Less: Ending work in process inventory $52,000

Cost of goods manufactured $55,495

7. Prepare a schedule of cost of goods sold for March.

Quantity Amount ($) Amount ($)

Beginning raw materials inventory:

Opening 25,126 $149,000

Add: Purchases

Sami sheets (Square meters) 1000 $5,000

Sami tubing (Kilograms) 400 $3,300

Direct labor $11,000 $168,300

Less: Closing stock 23,726 $140,461 $140,461

Cost of goods sold $27,839

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

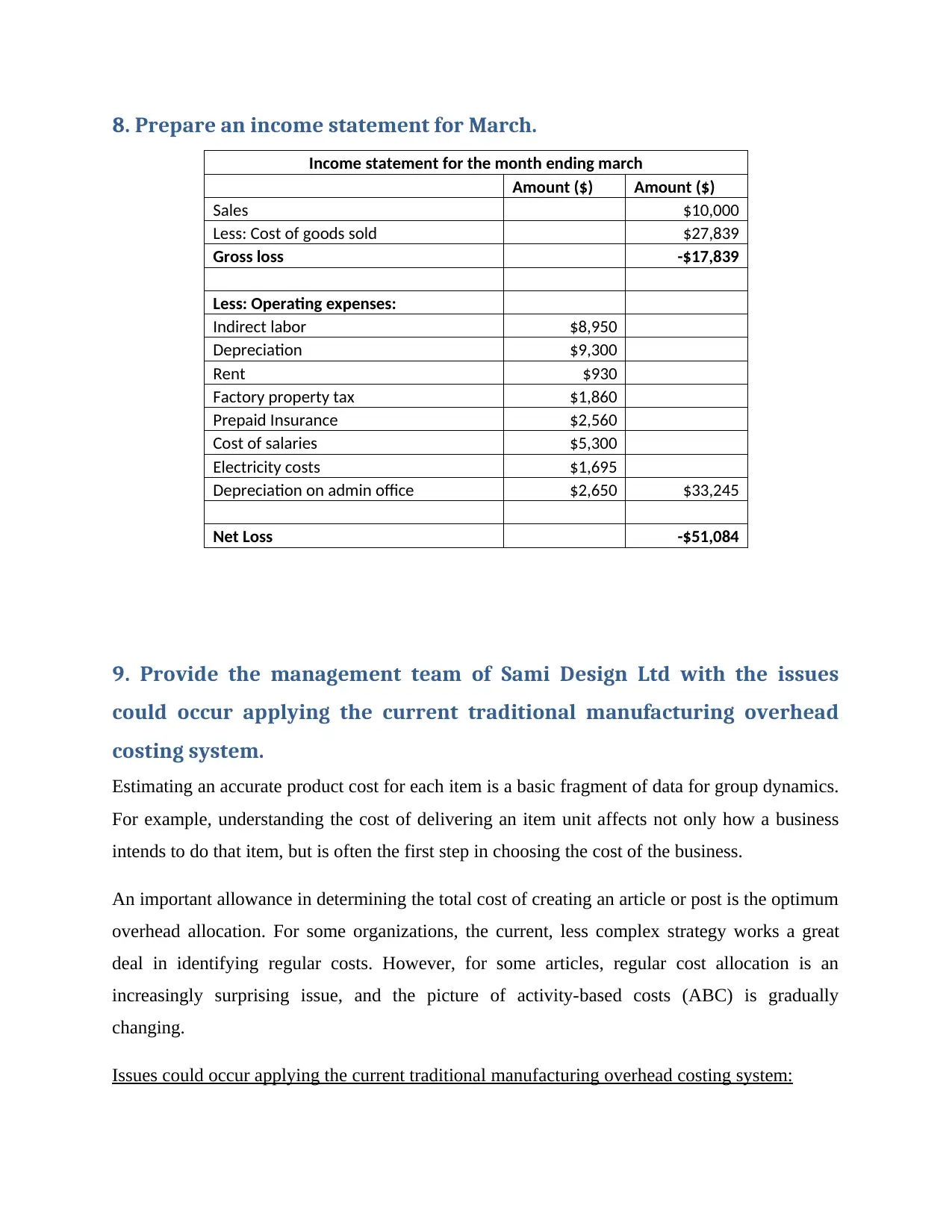

8. Prepare an income statement for March.

Income statement for the month ending march

Amount ($) Amount ($)

Sales $10,000

Less: Cost of goods sold $27,839

Gross loss -$17,839

Less: Operating expenses:

Indirect labor $8,950

Depreciation $9,300

Rent $930

Factory property tax $1,860

Prepaid Insurance $2,560

Cost of salaries $5,300

Electricity costs $1,695

Depreciation on admin office $2,650 $33,245

Net Loss -$51,084

9. Provide the management team of Sami Design Ltd with the issues

could occur applying the current traditional manufacturing overhead

costing system.

Estimating an accurate product cost for each item is a basic fragment of data for group dynamics.

For example, understanding the cost of delivering an item unit affects not only how a business

intends to do that item, but is often the first step in choosing the cost of the business.

An important allowance in determining the total cost of creating an article or post is the optimum

overhead allocation. For some organizations, the current, less complex strategy works a great

deal in identifying regular costs. However, for some articles, regular cost allocation is an

increasingly surprising issue, and the picture of activity-based costs (ABC) is gradually

changing.

Issues could occur applying the current traditional manufacturing overhead costing system:

Income statement for the month ending march

Amount ($) Amount ($)

Sales $10,000

Less: Cost of goods sold $27,839

Gross loss -$17,839

Less: Operating expenses:

Indirect labor $8,950

Depreciation $9,300

Rent $930

Factory property tax $1,860

Prepaid Insurance $2,560

Cost of salaries $5,300

Electricity costs $1,695

Depreciation on admin office $2,650 $33,245

Net Loss -$51,084

9. Provide the management team of Sami Design Ltd with the issues

could occur applying the current traditional manufacturing overhead

costing system.

Estimating an accurate product cost for each item is a basic fragment of data for group dynamics.

For example, understanding the cost of delivering an item unit affects not only how a business

intends to do that item, but is often the first step in choosing the cost of the business.

An important allowance in determining the total cost of creating an article or post is the optimum

overhead allocation. For some organizations, the current, less complex strategy works a great

deal in identifying regular costs. However, for some articles, regular cost allocation is an

increasingly surprising issue, and the picture of activity-based costs (ABC) is gradually

changing.

Issues could occur applying the current traditional manufacturing overhead costing system:

Organizations need cost frameworks to meet three essential capacities: stock valuation for

detailed cash related purposes, operational control for performance and profit evaluation and cost

estimation of individual items. It has been observed that no single framework can adequately

respond to the demands posed by the various elements of the expenditure frameworks. While

primary capacity appears to be satisfactorily satisfied with traditional cost frameworks, these

frameworks have not been able to clarify what the workshop manager should do to track costs to

improve performance and these frameworks generally reduce the costs of articles for vital and

promotional purposes, especially in excessively high contexts.

The current cost frameworks require that cost elements (articles or administrations) cost

resources and in this way these frameworks are perceived as creating costs. For this situation, it

is difficult to track costs, despite the fact that an organization can simply keep track of what is

being done (exercises) and the costs will change later. Be that as it may, in normal cost contexts,

the basic idea will be that costs can be analyzed, but given that most administrators have found

the way, it is more difficult to keep track of costs.

The normal cost frameworks for the most part use direct work or other bases of volume

specifications for cost purposes and in this way these bases occasionally reflect the actual

conditions and linking of the logical results between overhead and cost items cost. Likewise,

conventional cost frameworks are more interested in hierarchical references than in the actual

approach. These frameworks are basically set up (cost adjustment as indicated by a classification

structure) and the methodology seen is completely absent. From this we can understand that the

organized approach of the standard cost frameworks does not provide assistance for the

circulation of resources and the improvement of processes. After some time this can trigger

unnecessary connections and under-exploitation.

detailed cash related purposes, operational control for performance and profit evaluation and cost

estimation of individual items. It has been observed that no single framework can adequately

respond to the demands posed by the various elements of the expenditure frameworks. While

primary capacity appears to be satisfactorily satisfied with traditional cost frameworks, these

frameworks have not been able to clarify what the workshop manager should do to track costs to

improve performance and these frameworks generally reduce the costs of articles for vital and

promotional purposes, especially in excessively high contexts.

The current cost frameworks require that cost elements (articles or administrations) cost

resources and in this way these frameworks are perceived as creating costs. For this situation, it

is difficult to track costs, despite the fact that an organization can simply keep track of what is

being done (exercises) and the costs will change later. Be that as it may, in normal cost contexts,

the basic idea will be that costs can be analyzed, but given that most administrators have found

the way, it is more difficult to keep track of costs.

The normal cost frameworks for the most part use direct work or other bases of volume

specifications for cost purposes and in this way these bases occasionally reflect the actual

conditions and linking of the logical results between overhead and cost items cost. Likewise,

conventional cost frameworks are more interested in hierarchical references than in the actual

approach. These frameworks are basically set up (cost adjustment as indicated by a classification

structure) and the methodology seen is completely absent. From this we can understand that the

organized approach of the standard cost frameworks does not provide assistance for the

circulation of resources and the improvement of processes. After some time this can trigger

unnecessary connections and under-exploitation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10. Analyze and describe the benefits of replacing Activity Base Costing

(ABC).

The difference between the standard approach (using a cost driver) and the ABC strategy (using

different cost drivers) is more striking than the simple cost drivers. When direct labor is a major

part of the cost of the item, overhead costs are generally determined by a cost factor, which

works immediately or machine hours; the usual way will pay these expenses dearly. When

innovation is a large share of the cost of the item, the general costs are usually driven by

different drivers, so the use of several cost drivers in the ABC strategy takes into account the

increasing satisfaction of the product 'Exceeding the regular costs. .

ABC's rise was due to its three components:

Changes to the cost structures of organizations, which means the expansion of regular

costs is reversed by the immediate decline in labor and material costs;

Hands-on behavior within organizations is improving, with leaders never aware of the

connections between their areas of expertise;

In the presence of fourth-century social databases and dialects.

In this way, ABC was born as a framework to solve the problem with detailed cost data for

requests for actions by individual articles, administrations, customers, and channels. At present it

is generally understood that ABC is not as "special" as its supporters, it may seem to have

diminished in some respect and it can be believed that it goes back to times previously before the

joke related.

In any case, it can be assumed that the ABC effect is amplified, after the impressive result of

Lost Appropriateness and the specialized work of the cut-off stage. In this approach, ABC itself

progressed and moved from being fixed to getting the "right costs" for the articles, focusing on

co-planning all exercises associations in the best possible way. In this appearance, ABC became

Activity-Based Regulation (ABM), which, as a structure, can undoubtedly give us the power to

overcome a dense object.

(ABC).

The difference between the standard approach (using a cost driver) and the ABC strategy (using

different cost drivers) is more striking than the simple cost drivers. When direct labor is a major

part of the cost of the item, overhead costs are generally determined by a cost factor, which

works immediately or machine hours; the usual way will pay these expenses dearly. When

innovation is a large share of the cost of the item, the general costs are usually driven by

different drivers, so the use of several cost drivers in the ABC strategy takes into account the

increasing satisfaction of the product 'Exceeding the regular costs. .

ABC's rise was due to its three components:

Changes to the cost structures of organizations, which means the expansion of regular

costs is reversed by the immediate decline in labor and material costs;

Hands-on behavior within organizations is improving, with leaders never aware of the

connections between their areas of expertise;

In the presence of fourth-century social databases and dialects.

In this way, ABC was born as a framework to solve the problem with detailed cost data for

requests for actions by individual articles, administrations, customers, and channels. At present it

is generally understood that ABC is not as "special" as its supporters, it may seem to have

diminished in some respect and it can be believed that it goes back to times previously before the

joke related.

In any case, it can be assumed that the ABC effect is amplified, after the impressive result of

Lost Appropriateness and the specialized work of the cut-off stage. In this approach, ABC itself

progressed and moved from being fixed to getting the "right costs" for the articles, focusing on

co-planning all exercises associations in the best possible way. In this appearance, ABC became

Activity-Based Regulation (ABM), which, as a structure, can undoubtedly give us the power to

overcome a dense object.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The ABC frameworks group the costs according to the various resources used to make the article

more accurate, they cost more to use and, in this way, usually not the strategy they are the best.

Managers need to consider each framework and how it works within their society.

Benefits of applying ABC based costing includes:

There are several pools overhead and each has its own exciting movement portion. This

provides progressively accurate rates for the use of regular costs, but puts aside more

efforts to realize and bring in higher spending.

The circulation bases (i.e. the rotation constants) change continuously from those used in

the standard specification. Several cost pools allow the board to impose costs under

comparable drivers and consider cost drivers beyond the mill operating cycle or machine

time. This leads to an increasingly precise level of environmental advocacy.

Action levels may consider the level of movement to a minimum rather than the intended

level of activity.

Both non-production costs and manufacturing costs can be attributed to the product. The main

basis in naming costs is the link between cost and item. In the event that costs increase as the size

of the object increases, it is displayed as part of an overhead.

Switching from the standard assignment method to ABC's costs is not as simple as forcing the

directors to simply follow the new picture to the producers. Often there are problems that begin

with the persuasion of producers that will bring benefits and that should be linked to the new

framework.

more accurate, they cost more to use and, in this way, usually not the strategy they are the best.

Managers need to consider each framework and how it works within their society.

Benefits of applying ABC based costing includes:

There are several pools overhead and each has its own exciting movement portion. This

provides progressively accurate rates for the use of regular costs, but puts aside more

efforts to realize and bring in higher spending.

The circulation bases (i.e. the rotation constants) change continuously from those used in

the standard specification. Several cost pools allow the board to impose costs under

comparable drivers and consider cost drivers beyond the mill operating cycle or machine

time. This leads to an increasingly precise level of environmental advocacy.

Action levels may consider the level of movement to a minimum rather than the intended

level of activity.

Both non-production costs and manufacturing costs can be attributed to the product. The main

basis in naming costs is the link between cost and item. In the event that costs increase as the size

of the object increases, it is displayed as part of an overhead.

Switching from the standard assignment method to ABC's costs is not as simple as forcing the

directors to simply follow the new picture to the producers. Often there are problems that begin

with the persuasion of producers that will bring benefits and that should be linked to the new

framework.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.