Market Equilibrium and Industry Changes: An In-Depth Economic Analysis

VerifiedAdded on 2023/06/11

|11

|1931

|306

Essay

AI Summary

This essay discusses market equilibrium, defined as the point where quantity demanded equals quantity supplied, and its role in determining industry dynamics. It examines how shifts in demand and supply impact market prices and quantities, referencing economic laws and examples such as the portable generator market during the Y2K scare and Microsoft's DOS licensing strategy. The essay further contrasts competitive, monopoly, and oligopoly market structures, highlighting how pricing strategies and the presence of substitutes influence equilibrium. It concludes by emphasizing the importance of understanding market equilibrium for investors and businesses to anticipate market changes, maximize profits, and make informed decisions about investment and pricing.

Running head: MARKET EQUILIBRIUM AND INDUSTRY CHANGES

Market Equilibrium and Industry Changes

Name of Student:

Name of University:

Author’s Note:

Market Equilibrium and Industry Changes

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MARKET EQUILIBRIUM AND INDUSTRY CHANGES

Executive Summary

Market equilibrium is the market clearing price and output which is measured by the amount of

output sellers are willing, able to sell and buyers are willing to buy. The equilibrium determines

the market in which a firm operates. The effect of equilibrium price and quantity is a key factor

for investors and managers to anticipate future costs and make plans accordingly. However, this

equilibrium is different according to industry and commodity type.

Executive Summary

Market equilibrium is the market clearing price and output which is measured by the amount of

output sellers are willing, able to sell and buyers are willing to buy. The equilibrium determines

the market in which a firm operates. The effect of equilibrium price and quantity is a key factor

for investors and managers to anticipate future costs and make plans accordingly. However, this

equilibrium is different according to industry and commodity type.

2MARKET EQUILIBRIUM AND INDUSTRY CHANGES

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Conclusion.......................................................................................................................................7

Reference List..................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Conclusion.......................................................................................................................................7

Reference List..................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MARKET EQUILIBRIUM AND INDUSTRY CHANGES

Introduction

Market equilibrium is the point where quantity demanded by the buyers equals to the

quantity supplied by the sellers at a particular price. The specified price is the market clearing

price because goods and services must be sold at that price with given amount of quantity. This

optimum equilibrium level is different according to industries. This is one of the most interesting

topics as market equilibrium has an important role to determine the type of industry in which a

firm operates. Industries transform themselves according to the demand and supply changes due

to market determined price and quantity. Industries and equilibrium level varies due to consumer

preference and availability of substitutes or complements (Cowell 2018).

Discussion

A market is a place where buyers and sellers meet and figure out the price of a product

along with the output level. According to the law of demand, demand for a commodity rises due

to fall in price and vice-versa, showing a negative relation (Karl 2019). Whereas, law of supply

says that with increase in price, supply goes up as selling goods are more profitable, showing a

positive relation. Thus, demand curve is downward sloping and supply curve is upward sloping.

The point where quantity demanded by consumers intersects with quantity supplied by sellers

gives equilibrium price. Let’s take an example.

Quantit

y Price of suppliers($) Price of consumers($)

1 32 6

2 30 8

3 28 10

4 26 12

5 25 16

6 24 18

7 23 19

8 20 20

Introduction

Market equilibrium is the point where quantity demanded by the buyers equals to the

quantity supplied by the sellers at a particular price. The specified price is the market clearing

price because goods and services must be sold at that price with given amount of quantity. This

optimum equilibrium level is different according to industries. This is one of the most interesting

topics as market equilibrium has an important role to determine the type of industry in which a

firm operates. Industries transform themselves according to the demand and supply changes due

to market determined price and quantity. Industries and equilibrium level varies due to consumer

preference and availability of substitutes or complements (Cowell 2018).

Discussion

A market is a place where buyers and sellers meet and figure out the price of a product

along with the output level. According to the law of demand, demand for a commodity rises due

to fall in price and vice-versa, showing a negative relation (Karl 2019). Whereas, law of supply

says that with increase in price, supply goes up as selling goods are more profitable, showing a

positive relation. Thus, demand curve is downward sloping and supply curve is upward sloping.

The point where quantity demanded by consumers intersects with quantity supplied by sellers

gives equilibrium price. Let’s take an example.

Quantit

y Price of suppliers($) Price of consumers($)

1 32 6

2 30 8

3 28 10

4 26 12

5 25 16

6 24 18

7 23 19

8 20 20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MARKET EQUILIBRIUM AND INDUSTRY CHANGES

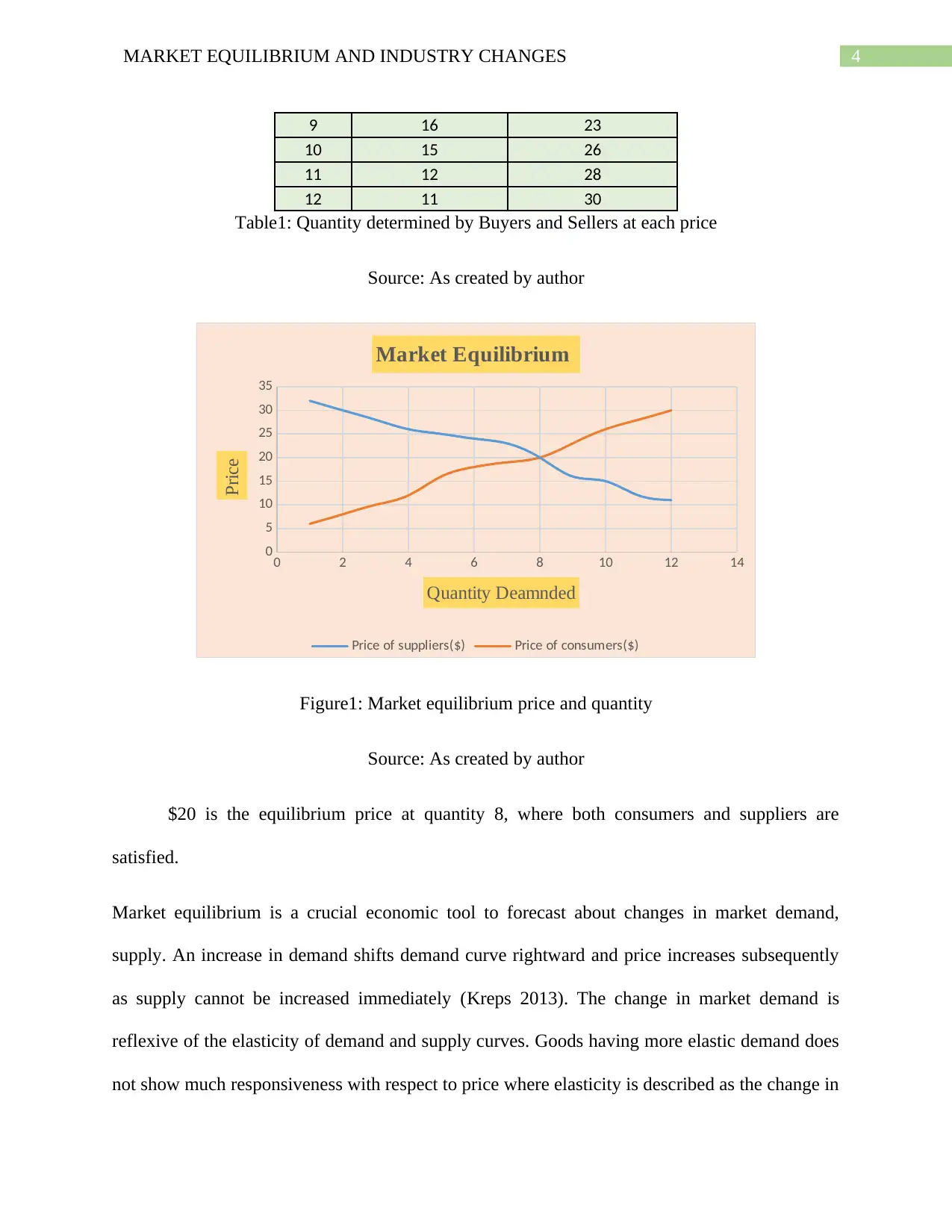

9 16 23

10 15 26

11 12 28

12 11 30

Table1: Quantity determined by Buyers and Sellers at each price

Source: As created by author

0 2 4 6 8 10 12 14

0

5

10

15

20

25

30

35

Market Equilibrium

Price of suppliers($) Price of consumers($)

Quantity Deamnded

Price

Figure1: Market equilibrium price and quantity

Source: As created by author

$20 is the equilibrium price at quantity 8, where both consumers and suppliers are

satisfied.

Market equilibrium is a crucial economic tool to forecast about changes in market demand,

supply. An increase in demand shifts demand curve rightward and price increases subsequently

as supply cannot be increased immediately (Kreps 2013). The change in market demand is

reflexive of the elasticity of demand and supply curves. Goods having more elastic demand does

not show much responsiveness with respect to price where elasticity is described as the change in

9 16 23

10 15 26

11 12 28

12 11 30

Table1: Quantity determined by Buyers and Sellers at each price

Source: As created by author

0 2 4 6 8 10 12 14

0

5

10

15

20

25

30

35

Market Equilibrium

Price of suppliers($) Price of consumers($)

Quantity Deamnded

Price

Figure1: Market equilibrium price and quantity

Source: As created by author

$20 is the equilibrium price at quantity 8, where both consumers and suppliers are

satisfied.

Market equilibrium is a crucial economic tool to forecast about changes in market demand,

supply. An increase in demand shifts demand curve rightward and price increases subsequently

as supply cannot be increased immediately (Kreps 2013). The change in market demand is

reflexive of the elasticity of demand and supply curves. Goods having more elastic demand does

not show much responsiveness with respect to price where elasticity is described as the change in

5MARKET EQUILIBRIUM AND INDUSTRY CHANGES

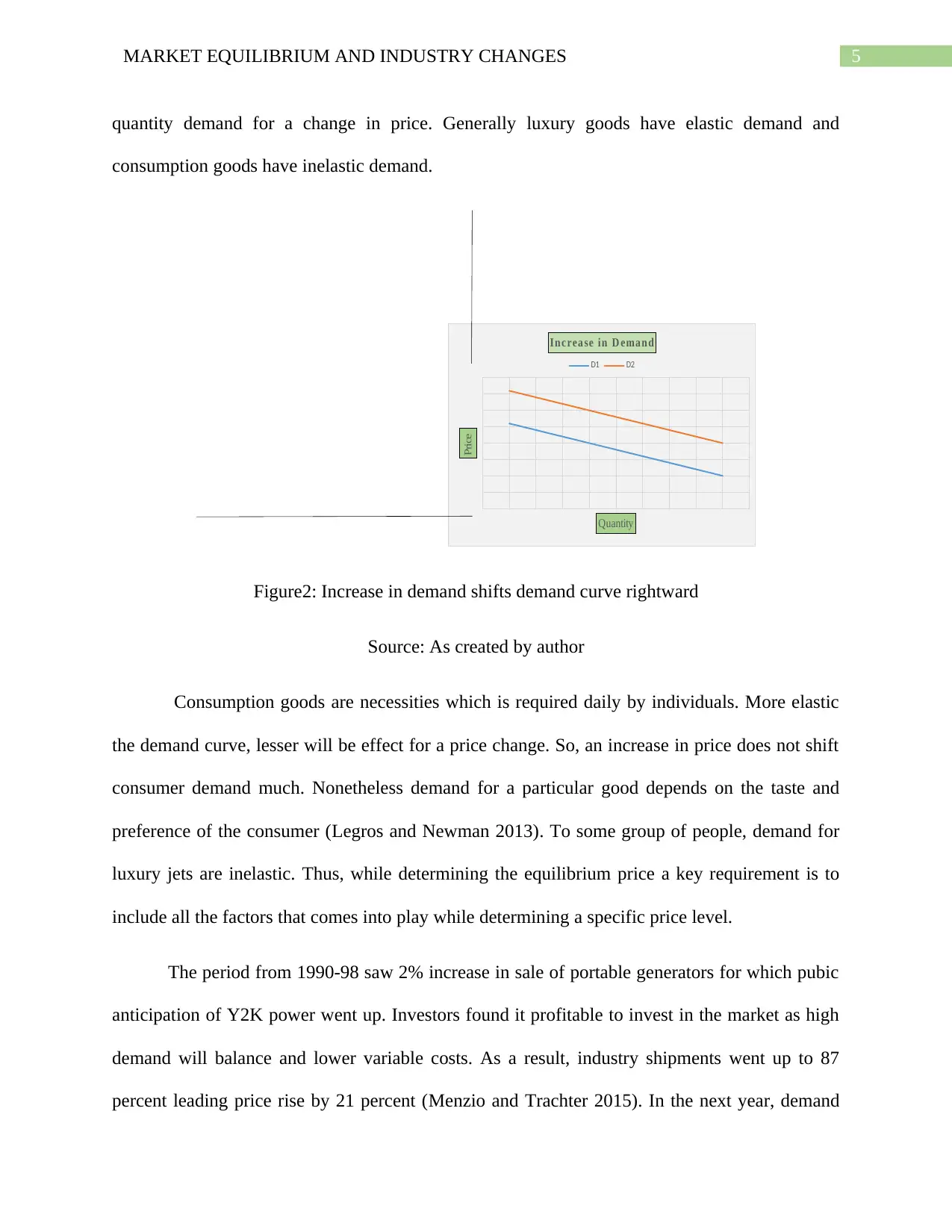

quantity demand for a change in price. Generally luxury goods have elastic demand and

consumption goods have inelastic demand.

Inc rea se in D eman d

D1 D2

Quantity

Price

Figure2: Increase in demand shifts demand curve rightward

Source: As created by author

Consumption goods are necessities which is required daily by individuals. More elastic

the demand curve, lesser will be effect for a price change. So, an increase in price does not shift

consumer demand much. Nonetheless demand for a particular good depends on the taste and

preference of the consumer (Legros and Newman 2013). To some group of people, demand for

luxury jets are inelastic. Thus, while determining the equilibrium price a key requirement is to

include all the factors that comes into play while determining a specific price level.

The period from 1990-98 saw 2% increase in sale of portable generators for which pubic

anticipation of Y2K power went up. Investors found it profitable to invest in the market as high

demand will balance and lower variable costs. As a result, industry shipments went up to 87

percent leading price rise by 21 percent (Menzio and Trachter 2015). In the next year, demand

quantity demand for a change in price. Generally luxury goods have elastic demand and

consumption goods have inelastic demand.

Inc rea se in D eman d

D1 D2

Quantity

Price

Figure2: Increase in demand shifts demand curve rightward

Source: As created by author

Consumption goods are necessities which is required daily by individuals. More elastic

the demand curve, lesser will be effect for a price change. So, an increase in price does not shift

consumer demand much. Nonetheless demand for a particular good depends on the taste and

preference of the consumer (Legros and Newman 2013). To some group of people, demand for

luxury jets are inelastic. Thus, while determining the equilibrium price a key requirement is to

include all the factors that comes into play while determining a specific price level.

The period from 1990-98 saw 2% increase in sale of portable generators for which pubic

anticipation of Y2K power went up. Investors found it profitable to invest in the market as high

demand will balance and lower variable costs. As a result, industry shipments went up to 87

percent leading price rise by 21 percent (Menzio and Trachter 2015). In the next year, demand

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MARKET EQUILIBRIUM AND INDUSTRY CHANGES

fell sharply and the company was liable for bankruptcy. This gives a clear picture how investors

must anticipate the outcomes depending on economic laws and market equilibrium price

otherwise will lead to fall in revenues procuring to losses. When Microsoft developed its

operating system DOS, it licensed the system with other manufacturers so as to decrease the

price of the software. Microsoft responded by keeping a lower price and encouraged share and

growth of the software. This resulted in a rise in demand with a fixed price and created huge

profits (Profit= Revenue-Cost).

A good with more number of substitutes have a competitive market structure such that

each firm takes the price as given. This is because consumers can shift their preference if a

producer charges a higher price due to availability of infinite sellers. Industries in competitive

markets follow competitive based pricing model such that neither sellers nor buyers have

influence over the market price (Mankiw 2014). Industries add up their fixed cost on top and

then determine the variable cost depending on the number of quantities to be delivered. Any

firm can enter and leave from the market. So, by keeping the price same, industries can avoid the

trial, errors and risk of new pricing.

The strategy of firms is to grab markets share by keeping low price to gain maximum

profits from investments (Powell 2019). There is no requirement for the firms to bear risks as

competitors already know about the potentialities and inefficiencies as prices lead by them did

not lead to bankruptcy. In converse to that firms sell at a high price in order to create brand value

by keeping inefficient price which allows firms to attain economic equilibrium. One big example

is the retail industry where millions of sales take place every day and retailers act accordingly to

reach stabilize market price.

fell sharply and the company was liable for bankruptcy. This gives a clear picture how investors

must anticipate the outcomes depending on economic laws and market equilibrium price

otherwise will lead to fall in revenues procuring to losses. When Microsoft developed its

operating system DOS, it licensed the system with other manufacturers so as to decrease the

price of the software. Microsoft responded by keeping a lower price and encouraged share and

growth of the software. This resulted in a rise in demand with a fixed price and created huge

profits (Profit= Revenue-Cost).

A good with more number of substitutes have a competitive market structure such that

each firm takes the price as given. This is because consumers can shift their preference if a

producer charges a higher price due to availability of infinite sellers. Industries in competitive

markets follow competitive based pricing model such that neither sellers nor buyers have

influence over the market price (Mankiw 2014). Industries add up their fixed cost on top and

then determine the variable cost depending on the number of quantities to be delivered. Any

firm can enter and leave from the market. So, by keeping the price same, industries can avoid the

trial, errors and risk of new pricing.

The strategy of firms is to grab markets share by keeping low price to gain maximum

profits from investments (Powell 2019). There is no requirement for the firms to bear risks as

competitors already know about the potentialities and inefficiencies as prices lead by them did

not lead to bankruptcy. In converse to that firms sell at a high price in order to create brand value

by keeping inefficient price which allows firms to attain economic equilibrium. One big example

is the retail industry where millions of sales take place every day and retailers act accordingly to

reach stabilize market price.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MARKET EQUILIBRIUM AND INDUSTRY CHANGES

In markets where there is no substitutes and there is only a single seller in the industry,

market fall under monopoly structure. The sole seller is known as the market maker. The

equilibrium price in this sector is generally set high pricing strategy to get biggest returns on

investment. Monopolies gather maximum profits as new barriers cannot enter market due to

entry barriers, absence of huge inputs and need to governments support (Schneider 2013).

Electricity sector extracts maximum profits as consumers has no other option than to use it.

If market maker sells at the competitive price level, maker will end up with zero

economic profits. The demand curve is inelastic compared to that of competitive firms. Although

monopolies are efficient due to rise in average prices, yet in long run higher price will attract

more entrants and customers can easily shift their preferences. This equilibrium price can be set

by a collection of firms who dominate the industry. Such firms fall under oligopoly market

structure where few firms sell differentiated products which does not have substitutes (Spulber

2017).

Conclusion

Prices are the primary way of communication between buyers and sellers as buyers

resolve their willingness to pay and sellers to sell. The high price makes selling profitable in the

short run. Yet after some time, demand falls and price decreases. This cycle continues and this is

how equilibrium is obtained. However, increase in supply lowers price due to excess output in

opposition to demand and shifts supply curve towards right. While setting the price, firms always

takes into consideration of the production, labor, manufacture and input costs. Firms always tries

to build efficient techniques to reduce the production cost and increase the efficiency level per

unit output. The aim of industries is to maximize profits at a lower cost. Industries generally sets

In markets where there is no substitutes and there is only a single seller in the industry,

market fall under monopoly structure. The sole seller is known as the market maker. The

equilibrium price in this sector is generally set high pricing strategy to get biggest returns on

investment. Monopolies gather maximum profits as new barriers cannot enter market due to

entry barriers, absence of huge inputs and need to governments support (Schneider 2013).

Electricity sector extracts maximum profits as consumers has no other option than to use it.

If market maker sells at the competitive price level, maker will end up with zero

economic profits. The demand curve is inelastic compared to that of competitive firms. Although

monopolies are efficient due to rise in average prices, yet in long run higher price will attract

more entrants and customers can easily shift their preferences. This equilibrium price can be set

by a collection of firms who dominate the industry. Such firms fall under oligopoly market

structure where few firms sell differentiated products which does not have substitutes (Spulber

2017).

Conclusion

Prices are the primary way of communication between buyers and sellers as buyers

resolve their willingness to pay and sellers to sell. The high price makes selling profitable in the

short run. Yet after some time, demand falls and price decreases. This cycle continues and this is

how equilibrium is obtained. However, increase in supply lowers price due to excess output in

opposition to demand and shifts supply curve towards right. While setting the price, firms always

takes into consideration of the production, labor, manufacture and input costs. Firms always tries

to build efficient techniques to reduce the production cost and increase the efficiency level per

unit output. The aim of industries is to maximize profits at a lower cost. Industries generally sets

8MARKET EQUILIBRIUM AND INDUSTRY CHANGES

price above the cost incurred. Now, how much this pricing effects the industries, is dependent on

the market type.

The analysis of equilibrium price helps investors to understand the market structure and

whether investment is profitable. The anticipation of the effects of shifts in demand and supply

gives a good prospective for business to attain the maximum benefit. Competitive markets set a

similar price and continue to gather profits as the firms have all the information available.

Whereas risk factor is higher in monopoly market based industries even though the profits are

high due to high equilibrium price.

price above the cost incurred. Now, how much this pricing effects the industries, is dependent on

the market type.

The analysis of equilibrium price helps investors to understand the market structure and

whether investment is profitable. The anticipation of the effects of shifts in demand and supply

gives a good prospective for business to attain the maximum benefit. Competitive markets set a

similar price and continue to gather profits as the firms have all the information available.

Whereas risk factor is higher in monopoly market based industries even though the profits are

high due to high equilibrium price.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MARKET EQUILIBRIUM AND INDUSTRY CHANGES

Reference List

Cowell, F., 2018. Microeconomics: principles and analysis. Oxford University Press.

Ivanov, M., 2013. Information revelation in competitive markets. Economic Theory, 52(1),

pp.337-365.

Karl, E., CASE, F., OSTER, R. and SHARON, E., 2019. PRINCIPLES OF

MICROECONOMICS. Pearson. Alipranti, M., Milliou, C. and Petrakis, E., 2014. Price vs.

quantity competition in a vertically related market. Economics Letters, 124(1), pp.122-126.

Anshelevich, E. and Sekar, S., 2015, December. Price competition in networked markets: How

do monopolies impact social welfare. In International Conference on Web and Internet

Economics (pp. 16-30). Springer, Berlin, Heidelberg.

Kreps, D.M., 2013. Microeconomic foundations I: choice and competitive markets (Vol. 1).

Princeton university press.

Legros, P. and Newman, A.F., 2013. A price theory of vertical and lateral integration. The

Quarterly Journal of Economics, 128(2), pp.725-770.

Mankiw, N.G., 2014. Principles of economics. Cengage Learning.

Menzio, G. and Trachter, N., 2015. Equilibrium price dispersion with sequential search. Journal

of Economic Theory, 160, pp.188-215.

Powell, M., 2019. Productivity and credibility in industry equilibrium. The RAND Journal of

Economics, 50(1), pp.121-146.

Schneider, E., 2013. Pricing and equilibrium. Routledge.

Reference List

Cowell, F., 2018. Microeconomics: principles and analysis. Oxford University Press.

Ivanov, M., 2013. Information revelation in competitive markets. Economic Theory, 52(1),

pp.337-365.

Karl, E., CASE, F., OSTER, R. and SHARON, E., 2019. PRINCIPLES OF

MICROECONOMICS. Pearson. Alipranti, M., Milliou, C. and Petrakis, E., 2014. Price vs.

quantity competition in a vertically related market. Economics Letters, 124(1), pp.122-126.

Anshelevich, E. and Sekar, S., 2015, December. Price competition in networked markets: How

do monopolies impact social welfare. In International Conference on Web and Internet

Economics (pp. 16-30). Springer, Berlin, Heidelberg.

Kreps, D.M., 2013. Microeconomic foundations I: choice and competitive markets (Vol. 1).

Princeton university press.

Legros, P. and Newman, A.F., 2013. A price theory of vertical and lateral integration. The

Quarterly Journal of Economics, 128(2), pp.725-770.

Mankiw, N.G., 2014. Principles of economics. Cengage Learning.

Menzio, G. and Trachter, N., 2015. Equilibrium price dispersion with sequential search. Journal

of Economic Theory, 160, pp.188-215.

Powell, M., 2019. Productivity and credibility in industry equilibrium. The RAND Journal of

Economics, 50(1), pp.121-146.

Schneider, E., 2013. Pricing and equilibrium. Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MARKET EQUILIBRIUM AND INDUSTRY CHANGES

Spulber, D.F., 2017. Complementary monopolies and bargaining. The Journal of Law and

Economics, 60(1), pp.29-74.

Spulber, D.F., 2017. Complementary monopolies and bargaining. The Journal of Law and

Economics, 60(1), pp.29-74.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.