Market Structure in the Telecom Industry

VerifiedAdded on 2022/08/16

|14

|2862

|22

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

Market Structure of Telecommunication Industry

Name of the Student

Name of the University

Student ID

Market Structure of Telecommunication Industry

Name of the Student

Name of the University

Student ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

Executive Summary

The report discussed about the telecommunication industry of Australia, New Zealand and the

United Kingdom. By calculating the market concentration of the telecommunication industry in

the respective countries it is found that the industry in the concerned countries operate under

oligopoly market structure. Thus, the industry is exploitative in nature and caused loss in social

welfare and consumer surplus. The government of Australia has taken price policies to reduce

the inefficiency of eh market and is successful to some extent.

Executive Summary

The report discussed about the telecommunication industry of Australia, New Zealand and the

United Kingdom. By calculating the market concentration of the telecommunication industry in

the respective countries it is found that the industry in the concerned countries operate under

oligopoly market structure. Thus, the industry is exploitative in nature and caused loss in social

welfare and consumer surplus. The government of Australia has taken price policies to reduce

the inefficiency of eh market and is successful to some extent.

2MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

Table of Contents

Introduction......................................................................................................................................3

Market concentration in telecommunication industry.....................................................................3

Market structure of the telecommunication industry.......................................................................7

Government policies to control non-competitive Australian telecommunication industry...........10

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................3

Market concentration in telecommunication industry.....................................................................3

Market structure of the telecommunication industry.......................................................................7

Government policies to control non-competitive Australian telecommunication industry...........10

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

3MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

Introduction

Telecommunication industry is one of the important industry in the world. In different

countries, there are different telecommunication companies that operate and serve the entire

market. The main concern of this report is to study the telecommunication industry of Australia,

New Zealand and the United Kingdom. By studying the industry of the above mentioned

countries, the report finds the market structure the telecom companies of the respective countries

operate in. The report uses Herfindahl Hirschman Index to find the market concentration of the

telecommunication industries of the said countries and thereby confirms market structure of the

industries (De Vries et al., 2017) . Additionally, the report focuses further on the characteristics

of the markets structure in which the industry companies are operating in and thereby finds the

possible profit of the companies. It means that whether the companies are making loss, zero

economic profit or super normal profit. The discussion on the welfare of the producers,

consumers and society is one of the interests of this report. However, the effective governmental

policies and their consequences will be discussed that would curb the price of the

telecommunication industry in Australia if it is found that the industry in Australia is non-

competitive in nature. Therefore, the report discusses the different aspects of market structure of

the telecommunication industry in the above mentioned countries.

Market concentration in telecommunication industry

The market concentration in the telecommunication industry in Australia, the United

Kingdom and New Zealand can be estimated by the use of Herfindahl Hirschman Index (HHI).

For the calculation the given market shares of the companies operating in the broadband service

and mobile phone service segment of the industry in respective countries has been considered.

Introduction

Telecommunication industry is one of the important industry in the world. In different

countries, there are different telecommunication companies that operate and serve the entire

market. The main concern of this report is to study the telecommunication industry of Australia,

New Zealand and the United Kingdom. By studying the industry of the above mentioned

countries, the report finds the market structure the telecom companies of the respective countries

operate in. The report uses Herfindahl Hirschman Index to find the market concentration of the

telecommunication industries of the said countries and thereby confirms market structure of the

industries (De Vries et al., 2017) . Additionally, the report focuses further on the characteristics

of the markets structure in which the industry companies are operating in and thereby finds the

possible profit of the companies. It means that whether the companies are making loss, zero

economic profit or super normal profit. The discussion on the welfare of the producers,

consumers and society is one of the interests of this report. However, the effective governmental

policies and their consequences will be discussed that would curb the price of the

telecommunication industry in Australia if it is found that the industry in Australia is non-

competitive in nature. Therefore, the report discusses the different aspects of market structure of

the telecommunication industry in the above mentioned countries.

Market concentration in telecommunication industry

The market concentration in the telecommunication industry in Australia, the United

Kingdom and New Zealand can be estimated by the use of Herfindahl Hirschman Index (HHI).

For the calculation the given market shares of the companies operating in the broadband service

and mobile phone service segment of the industry in respective countries has been considered.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

Broadband Services market concentration

Australia

The companies that operate in the broadband service segment of the telecommunication

industry in the country are Telstra, Optus, iiNet, TPG and other. Therefore, market concentration

of this segment of the industry is given as

HHI =(Telstra)2 +(Optus)2+(iiNet )2+(TPG)2 +(Other)2

¿ , HHI =( 41)2+(14)2 +(15)2 +(12)2 +(18)2

¿ , HHI=1681+196+225+144 +324

¿ , HHI =2570

New Zealand

The companies that operate in the broadband service segment of the telecommunication

industry in the country are Spark, Vodafone, Calipus, Orcone and other. Therefore, market

concentration of this segment of the industry is given as

HHI =(Spark )2 +( Vodafone)2 +(Calipus)2+(Orcone )2 +(Other )2

¿ , HHI =( 49)2+(32)2+(8)2 +(5)2 +(6)2

¿ , HHI =2401+1024+64 +25+36

¿ , HHI =3550

Broadband Services market concentration

Australia

The companies that operate in the broadband service segment of the telecommunication

industry in the country are Telstra, Optus, iiNet, TPG and other. Therefore, market concentration

of this segment of the industry is given as

HHI =(Telstra)2 +(Optus)2+(iiNet )2+(TPG)2 +(Other)2

¿ , HHI =( 41)2+(14)2 +(15)2 +(12)2 +(18)2

¿ , HHI=1681+196+225+144 +324

¿ , HHI =2570

New Zealand

The companies that operate in the broadband service segment of the telecommunication

industry in the country are Spark, Vodafone, Calipus, Orcone and other. Therefore, market

concentration of this segment of the industry is given as

HHI =(Spark )2 +( Vodafone)2 +(Calipus)2+(Orcone )2 +(Other )2

¿ , HHI =( 49)2+(32)2+(8)2 +(5)2 +(6)2

¿ , HHI =2401+1024+64 +25+36

¿ , HHI =3550

5MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

The United Kingdom

The companies that operate in the broadband service segment of the telecommunication

industry in the country are BT, Virgin Media, Sky, Talk Talk and other. Therefore, market

concentration of this segment of the industry is given as

HHI=(BT )2 +(Virgin Media)2 +(Sky)2 +(Talk Talk )2+(Other )2

¿ , HHI =( 31)2 +(20)2 +(20)2 +(15)2+(13)2

¿ , HHI =961+ 400+400+225+ 169

¿ , HHI=2155

From the above calculations, it can be observed that market concentration in broadband

segment in New Zealand is the highest with value 3550 whereas in the United Kingdom is the

lowest (Bos et al., 2017). The HHI of both the New Zealand and Australia are above 2500 and

that indicates the market concentration in these two countries are considerable high and the

market structure is of oligopoly. In case of the United Kingdom the market concentration is

lower than 2500 but it is also of oligopoly in nature.

Mobile phone Services market concentration

Australia

Telstra, Optus, Vodafone and other are the companies that operate in the mobile phone

service segment in the telecommunication industry of Australia. Therefore, market concentration

in the mobile phone service segment is given as

The United Kingdom

The companies that operate in the broadband service segment of the telecommunication

industry in the country are BT, Virgin Media, Sky, Talk Talk and other. Therefore, market

concentration of this segment of the industry is given as

HHI=(BT )2 +(Virgin Media)2 +(Sky)2 +(Talk Talk )2+(Other )2

¿ , HHI =( 31)2 +(20)2 +(20)2 +(15)2+(13)2

¿ , HHI =961+ 400+400+225+ 169

¿ , HHI=2155

From the above calculations, it can be observed that market concentration in broadband

segment in New Zealand is the highest with value 3550 whereas in the United Kingdom is the

lowest (Bos et al., 2017). The HHI of both the New Zealand and Australia are above 2500 and

that indicates the market concentration in these two countries are considerable high and the

market structure is of oligopoly. In case of the United Kingdom the market concentration is

lower than 2500 but it is also of oligopoly in nature.

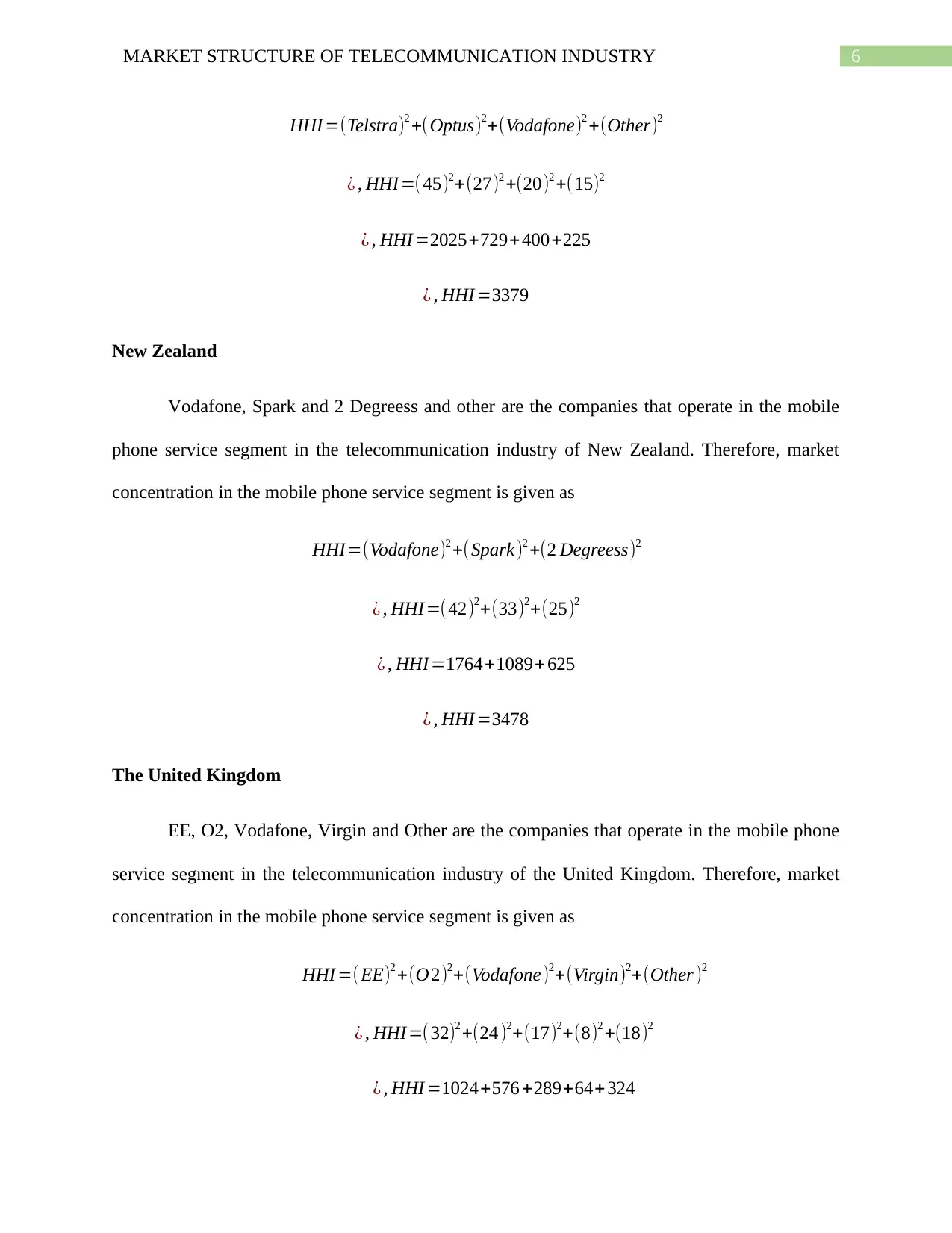

Mobile phone Services market concentration

Australia

Telstra, Optus, Vodafone and other are the companies that operate in the mobile phone

service segment in the telecommunication industry of Australia. Therefore, market concentration

in the mobile phone service segment is given as

6MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

HHI =(Telstra)2 +(Optus)2+(Vodafone)2 +(Other)2

¿ , HHI =(45)2+(27)2 +(20)2 +(15)2

¿ , HHI =2025+729+400+225

¿ , HHI =3379

New Zealand

Vodafone, Spark and 2 Degreess and other are the companies that operate in the mobile

phone service segment in the telecommunication industry of New Zealand. Therefore, market

concentration in the mobile phone service segment is given as

HHI =(Vodafone)2 +( Spark )2 +(2 Degreess)2

¿ , HHI=(42)2+(33)2+(25)2

¿ , HHI=1764+1089+ 625

¿ , HHI =3478

The United Kingdom

EE, O2, Vodafone, Virgin and Other are the companies that operate in the mobile phone

service segment in the telecommunication industry of the United Kingdom. Therefore, market

concentration in the mobile phone service segment is given as

HHI =( EE)2 +(O2)2+(Vodafone)2+(Virgin)2+(Other )2

¿ , HHI =( 32)2 +(24 )2+(17)2+(8)2 +(18)2

¿ , HHI =1024+576 +289+64+ 324

HHI =(Telstra)2 +(Optus)2+(Vodafone)2 +(Other)2

¿ , HHI =(45)2+(27)2 +(20)2 +(15)2

¿ , HHI =2025+729+400+225

¿ , HHI =3379

New Zealand

Vodafone, Spark and 2 Degreess and other are the companies that operate in the mobile

phone service segment in the telecommunication industry of New Zealand. Therefore, market

concentration in the mobile phone service segment is given as

HHI =(Vodafone)2 +( Spark )2 +(2 Degreess)2

¿ , HHI=(42)2+(33)2+(25)2

¿ , HHI=1764+1089+ 625

¿ , HHI =3478

The United Kingdom

EE, O2, Vodafone, Virgin and Other are the companies that operate in the mobile phone

service segment in the telecommunication industry of the United Kingdom. Therefore, market

concentration in the mobile phone service segment is given as

HHI =( EE)2 +(O2)2+(Vodafone)2+(Virgin)2+(Other )2

¿ , HHI =( 32)2 +(24 )2+(17)2+(8)2 +(18)2

¿ , HHI =1024+576 +289+64+ 324

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

¿ , HHI =2277

The above calculations regarding market concentration of mobile phone service segment

of telecommunication industry in Australia, New Zealand and the United Kingdom show that in

all the three countries the structure of market of the segment is oligopoly nature (Brezina et al.,

2016). However, it should be noted that market concentration in Australia and New Zealand is

much higher than that of the United Kingdom.

Market structure of the telecommunication industry

In the previous section, the market concentration of the two segment, that is broadband

and mobile phone service segments of the telecommunication industry of the Australia, New

Zealand and the United Kingdom has been calculated and it is found that both the segments in all

the three countries are of oligopoly in nature (Lipsky et al., 2018). Apart from market

concentration, it has been observed that the firms operating in the industry are few in number.

Thus, it can be strongly stated that the companies operating in the telecommunication industry in

all the three countries have substantial market power. However, companies in the United

Kingdom has comparatively lower market power than the other two (Azar & Vives, 2019). In

oligopoly market structure, there are huge fixed cost associated and thus high constraints to entry

and exit exist in the market. The companies in this markets structure are price setter and the since

there are numerous buyers, the buyers are the price takers. The demand curve faced by the

companies in this market structure is downward sloping and the profit maximizing output is

decided where marginal revenue (MR) equals marginal cost (MC) (Adams & Williams 2019).

However, unlike perfectly competitive market structure price is not determined at MR=MC. The

demand curve is well above MR=MC point and the price is determined from the demand curve at

the level of profit maximizing output. Thus, it is evident that the price of the telecommunication

¿ , HHI =2277

The above calculations regarding market concentration of mobile phone service segment

of telecommunication industry in Australia, New Zealand and the United Kingdom show that in

all the three countries the structure of market of the segment is oligopoly nature (Brezina et al.,

2016). However, it should be noted that market concentration in Australia and New Zealand is

much higher than that of the United Kingdom.

Market structure of the telecommunication industry

In the previous section, the market concentration of the two segment, that is broadband

and mobile phone service segments of the telecommunication industry of the Australia, New

Zealand and the United Kingdom has been calculated and it is found that both the segments in all

the three countries are of oligopoly in nature (Lipsky et al., 2018). Apart from market

concentration, it has been observed that the firms operating in the industry are few in number.

Thus, it can be strongly stated that the companies operating in the telecommunication industry in

all the three countries have substantial market power. However, companies in the United

Kingdom has comparatively lower market power than the other two (Azar & Vives, 2019). In

oligopoly market structure, there are huge fixed cost associated and thus high constraints to entry

and exit exist in the market. The companies in this markets structure are price setter and the since

there are numerous buyers, the buyers are the price takers. The demand curve faced by the

companies in this market structure is downward sloping and the profit maximizing output is

decided where marginal revenue (MR) equals marginal cost (MC) (Adams & Williams 2019).

However, unlike perfectly competitive market structure price is not determined at MR=MC. The

demand curve is well above MR=MC point and the price is determined from the demand curve at

the level of profit maximizing output. Thus, it is evident that the price of the telecommunication

8MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

industry in the given countries is higher than the price in perfectly competitive market (Colombo,

2019). It is known from the market theory of microeconomics that in perfect competition

companies earn zero economic profit, which is termed as normal profit too. Thus, in oligopoly

telecommunication industry the firms are positive economic profit or super normal profit

(Gomez-Martinez, Onderstal & Sonnemans, 2016). However, the super normal profit earned by

the companies operating in the telecommunication industry is lower than a company that

operates under a monopoly structure. In contrary, the companies in the telecommunication

industry can earn super normal profit equal to a monopoly company if the companies in the

industry collude that is cooperate with each other and set price accordingly (Bradshaw, Linneker

& Overton, 2017). Hence, under this case of collusion companies in the oligopoly

telecommunication industry will be able to charge price as high as possible and thereby earns

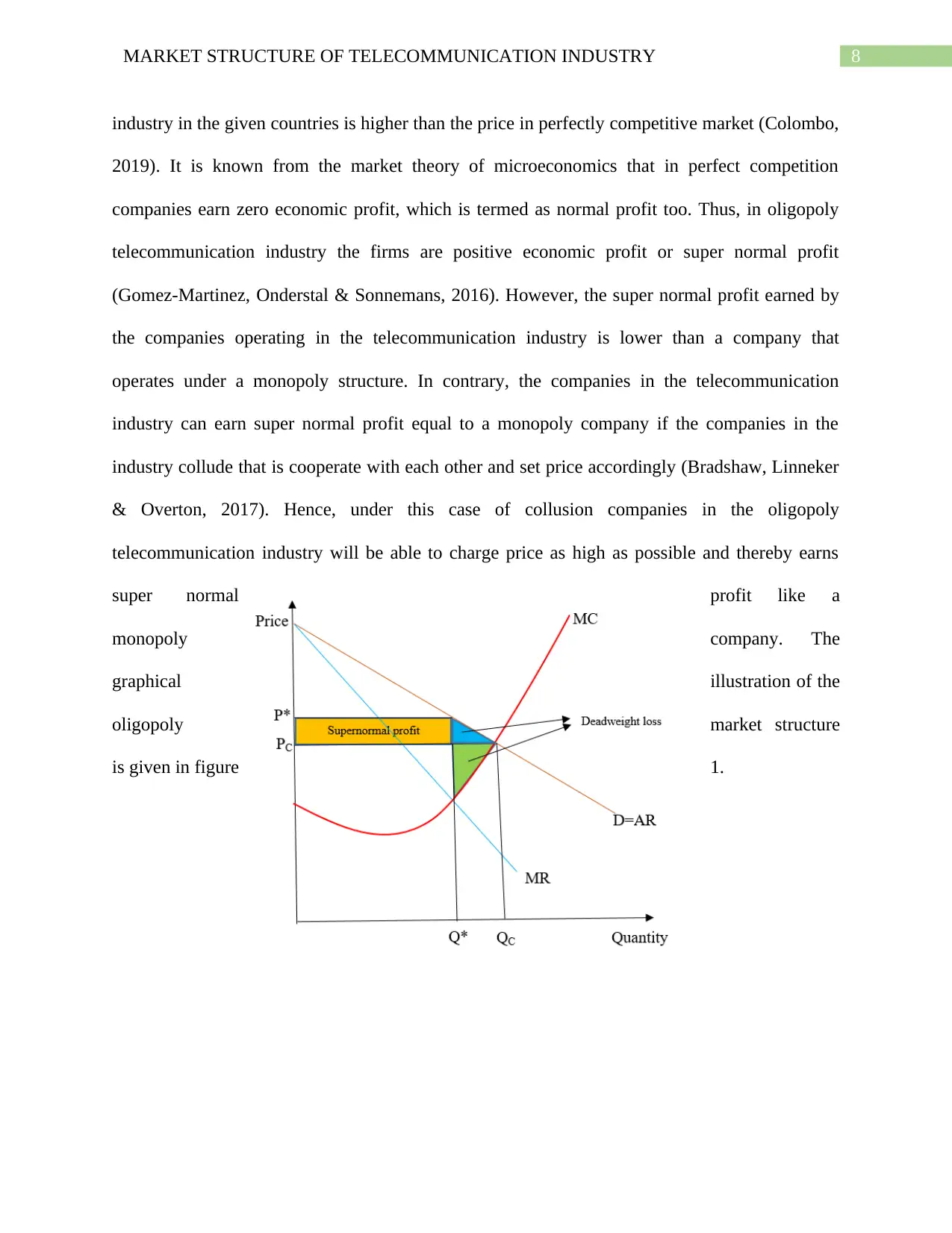

super normal profit like a

monopoly company. The

graphical illustration of the

oligopoly market structure

is given in figure 1.

industry in the given countries is higher than the price in perfectly competitive market (Colombo,

2019). It is known from the market theory of microeconomics that in perfect competition

companies earn zero economic profit, which is termed as normal profit too. Thus, in oligopoly

telecommunication industry the firms are positive economic profit or super normal profit

(Gomez-Martinez, Onderstal & Sonnemans, 2016). However, the super normal profit earned by

the companies operating in the telecommunication industry is lower than a company that

operates under a monopoly structure. In contrary, the companies in the telecommunication

industry can earn super normal profit equal to a monopoly company if the companies in the

industry collude that is cooperate with each other and set price accordingly (Bradshaw, Linneker

& Overton, 2017). Hence, under this case of collusion companies in the oligopoly

telecommunication industry will be able to charge price as high as possible and thereby earns

super normal profit like a

monopoly company. The

graphical illustration of the

oligopoly market structure

is given in figure 1.

9MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

Figure 1: Oligopoly market

Source: (Created by the Author)

In figure 1, it can be observed that QC and PC are the quantity and price respectively at the

equilibrium at competitive market structure (Cohen, Perakis & Thraves, 2017). On the other

hand, Q* and P* are the quantity and price respectively at equilibrium in oligopoly market. The

yellow shaded region is super normal profit earned by the companies operating in the

telecommunication industry.

Winners and Losers

It is evident from the figure 1 that under perfectly competitive market companies earn

zero economic profit but when the he market structure takes the form of oligopoly the n the price

of eth products increase from PC to P*. Due to this increased price due to difference in market

structure the profit of the companies operating in the industry increases and earn super normal

profit equivalent to the yellow shaded region (Butera et al., 2019). However, owing to earn more

the producers has to sacrifice a part of surplus given as green triangle region as shown in the

figure. The area of the yellow shaded rectangle is large than the area of green shaded triangle.

Therefore, in total under oligopoly market even after sacrificing a part of producer surplus the

companies earn more (Hutchison, 2017). However, the lost surplus is a loss of surplus as

deadweight loss. From the perspective of consumers end, it can be observed that the consumers

lost a large portion of their surplus. The amount of consumer surplus lost is given as yellow

shaded region and blue colored triangle. Additionally, the blue triangle is the total loss in

consumer surplus and is the loss in welfare called as deadweight loss. Therefore, green and blue

Figure 1: Oligopoly market

Source: (Created by the Author)

In figure 1, it can be observed that QC and PC are the quantity and price respectively at the

equilibrium at competitive market structure (Cohen, Perakis & Thraves, 2017). On the other

hand, Q* and P* are the quantity and price respectively at equilibrium in oligopoly market. The

yellow shaded region is super normal profit earned by the companies operating in the

telecommunication industry.

Winners and Losers

It is evident from the figure 1 that under perfectly competitive market companies earn

zero economic profit but when the he market structure takes the form of oligopoly the n the price

of eth products increase from PC to P*. Due to this increased price due to difference in market

structure the profit of the companies operating in the industry increases and earn super normal

profit equivalent to the yellow shaded region (Butera et al., 2019). However, owing to earn more

the producers has to sacrifice a part of surplus given as green triangle region as shown in the

figure. The area of the yellow shaded rectangle is large than the area of green shaded triangle.

Therefore, in total under oligopoly market even after sacrificing a part of producer surplus the

companies earn more (Hutchison, 2017). However, the lost surplus is a loss of surplus as

deadweight loss. From the perspective of consumers end, it can be observed that the consumers

lost a large portion of their surplus. The amount of consumer surplus lost is given as yellow

shaded region and blue colored triangle. Additionally, the blue triangle is the total loss in

consumer surplus and is the loss in welfare called as deadweight loss. Therefore, green and blue

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

triangles show that under oligopoly market structure of telecommunication industry there is

existence of deadweight loss. Therefore, it is evident the winners are the producers of the

telecommunication industry that is the companies that operate in the industry (Zeuthen, 2018).

On the other hand, the losers in the industry are consumers and the society. For consumers there

is significant loss in surplus and for society, there is loss too shown as deadweight loss in the

figure. Therefore, oligopoly market is more product centric than consumers.

Government policies to control non-competitive Australian telecommunication industry

The government of Australia has found that the telecommunication industry is of

oligopoly market structure and thus charges price higher than perfectly competitive market and

thereby exploits consumers (Doda, 2016). Therefore, to curb the exploitative nature of the

industry and to reduce price the government is taking price policies in order to control the

telecommunication industry of the country. Suppose, the government imposes price ceiling in the

telecommunication industry at the price level equivalent to perfectly competitive market price

PC. Due to this imposition of price ceiling, the amount received by the companies in the industry

is reduced and subsequently, the loss in consumer surplus and social welfare is retrieved (Wu,

2017). However, there is loss in producer surplus which could not be recovered and lost as

deadweight loss. Therefore, it is evident that government policies are to some extent are effective

since they has not caused any further loss in surplus but rather mitigated a significant amount of

welfare loss. At price ceiling, the companies that are operating will be producing the same

amount as they were under oligopoly price because the output is given by the profit maximizing

condition MR=MC (Tremblay & Tremblay, 2019). Hence, it has been observed that after

imposition of price ceiling by the government, there is reduction in price to the level of perfect

competition but quantity traded in the market has not increased a bit and remained at the same

triangles show that under oligopoly market structure of telecommunication industry there is

existence of deadweight loss. Therefore, it is evident the winners are the producers of the

telecommunication industry that is the companies that operate in the industry (Zeuthen, 2018).

On the other hand, the losers in the industry are consumers and the society. For consumers there

is significant loss in surplus and for society, there is loss too shown as deadweight loss in the

figure. Therefore, oligopoly market is more product centric than consumers.

Government policies to control non-competitive Australian telecommunication industry

The government of Australia has found that the telecommunication industry is of

oligopoly market structure and thus charges price higher than perfectly competitive market and

thereby exploits consumers (Doda, 2016). Therefore, to curb the exploitative nature of the

industry and to reduce price the government is taking price policies in order to control the

telecommunication industry of the country. Suppose, the government imposes price ceiling in the

telecommunication industry at the price level equivalent to perfectly competitive market price

PC. Due to this imposition of price ceiling, the amount received by the companies in the industry

is reduced and subsequently, the loss in consumer surplus and social welfare is retrieved (Wu,

2017). However, there is loss in producer surplus which could not be recovered and lost as

deadweight loss. Therefore, it is evident that government policies are to some extent are effective

since they has not caused any further loss in surplus but rather mitigated a significant amount of

welfare loss. At price ceiling, the companies that are operating will be producing the same

amount as they were under oligopoly price because the output is given by the profit maximizing

condition MR=MC (Tremblay & Tremblay, 2019). Hence, it has been observed that after

imposition of price ceiling by the government, there is reduction in price to the level of perfect

competition but quantity traded in the market has not increased a bit and remained at the same

11MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

level as it was under oligopoly market structure. Therefore, the government policy of price

ceiling is not perfectly effective to bring back the entire lost surplus.

Conclusion

The above discussion regarding the market structure of the telecommunication industry in

Australia, New Zealand and the United Kingdom leads to the conclusion that the industry in all

of the concerned countries are highly concentrated with few firms operating in the

telecommunication industry in the respective countries. Thus, the market concentration showed

that the industry is of oligopolistic in nature in all the three countries. The companies in the

industry charges high price and earns super normal profit. In addition to that, it is noticed that the

companies would be become capable earning profit equivalent to the super normal profit earned

by a monopoly firm if the companies collude with each other and charge a single high price.

Therefore, it has been observed from the further analysis that under the market structure of the

industry the companies gain but the consumers and the society faces loss in surplus. Thus, to

mitigate the problem the government of Australia intervened and implemented price solution

which is able to mitigate the loss of consumers and society but failed to recover the loss faced by

the companies and the there is no increase in quantity supplied in the market.

level as it was under oligopoly market structure. Therefore, the government policy of price

ceiling is not perfectly effective to bring back the entire lost surplus.

Conclusion

The above discussion regarding the market structure of the telecommunication industry in

Australia, New Zealand and the United Kingdom leads to the conclusion that the industry in all

of the concerned countries are highly concentrated with few firms operating in the

telecommunication industry in the respective countries. Thus, the market concentration showed

that the industry is of oligopolistic in nature in all the three countries. The companies in the

industry charges high price and earns super normal profit. In addition to that, it is noticed that the

companies would be become capable earning profit equivalent to the super normal profit earned

by a monopoly firm if the companies collude with each other and charge a single high price.

Therefore, it has been observed from the further analysis that under the market structure of the

industry the companies gain but the consumers and the society faces loss in surplus. Thus, to

mitigate the problem the government of Australia intervened and implemented price solution

which is able to mitigate the loss of consumers and society but failed to recover the loss faced by

the companies and the there is no increase in quantity supplied in the market.

12MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

Reference

Adams, B., & Williams, K. R. (2019). Zone pricing in retail oligopoly. American Economic

Journal: Microeconomics, 11(1), 124-56.

Azar, J., & Vives, X. (2019). General Equilibrium Oligopoly and Ownership

Structure. Available at SSRN 3501611.

Bos, J. W., Chan, Y. L., Kolari, J. W., & Yuan, J. (2017). Competition, concentration and critical

mass: why the Herfindahl–Hirschman Index is a biased competition measure.

In Handbook of Competition in Banking and Finance. Edward Elgar Publishing.

Bradshaw, S., Linneker, B., & Overton, L. (2017). Extractive industries as sites of supernormal

profits and supernormal patriarchy?. Gender & Development, 25(3), 439-454.

Brezina, I., Pekár, J., Čičková, Z., & Reiff, M. (2016). Herfindahl–Hirschman index level of

concentration values modification and analysis of their change. Central European journal

of operations research, 24(1), 49-72.

Butera, L., Metcalfe, R., Morrison, W., & Taubinsky, D. (2019). The deadweight loss of social

recognition (No. w25637). National Bureau of Economic Research.

Cohen, M., Perakis, G., & Thraves, C. (2017). Consumer Surplus Under Demand

Uncertainty. Available at SSRN 3035992.

Colombo, S. (2016). Mixed oligopolies and collusion. Journal of Economics, 118(2), 167-184.

De Vries, G., Pennings, E., Block, J. H., & Fisch, C. (2017). Trademark or patent? The effects of

market concentration, customer type and venture capital financing on start-ups’ initial IP

applications. Industry and Innovation, 24(4), 325-345.

Reference

Adams, B., & Williams, K. R. (2019). Zone pricing in retail oligopoly. American Economic

Journal: Microeconomics, 11(1), 124-56.

Azar, J., & Vives, X. (2019). General Equilibrium Oligopoly and Ownership

Structure. Available at SSRN 3501611.

Bos, J. W., Chan, Y. L., Kolari, J. W., & Yuan, J. (2017). Competition, concentration and critical

mass: why the Herfindahl–Hirschman Index is a biased competition measure.

In Handbook of Competition in Banking and Finance. Edward Elgar Publishing.

Bradshaw, S., Linneker, B., & Overton, L. (2017). Extractive industries as sites of supernormal

profits and supernormal patriarchy?. Gender & Development, 25(3), 439-454.

Brezina, I., Pekár, J., Čičková, Z., & Reiff, M. (2016). Herfindahl–Hirschman index level of

concentration values modification and analysis of their change. Central European journal

of operations research, 24(1), 49-72.

Butera, L., Metcalfe, R., Morrison, W., & Taubinsky, D. (2019). The deadweight loss of social

recognition (No. w25637). National Bureau of Economic Research.

Cohen, M., Perakis, G., & Thraves, C. (2017). Consumer Surplus Under Demand

Uncertainty. Available at SSRN 3035992.

Colombo, S. (2016). Mixed oligopolies and collusion. Journal of Economics, 118(2), 167-184.

De Vries, G., Pennings, E., Block, J. H., & Fisch, C. (2017). Trademark or patent? The effects of

market concentration, customer type and venture capital financing on start-ups’ initial IP

applications. Industry and Innovation, 24(4), 325-345.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MARKET STRUCTURE OF TELECOMMUNICATION INDUSTRY

Doda, B. (2016). How to price carbon in good times… and bad!. Wiley Interdisciplinary

Reviews: Climate Change, 7(1), 135-144.

Gomez-Martinez, F., Onderstal, S., & Sonnemans, J. (2016). Firm-specific information and

explicit collusion in experimental oligopolies. European Economic Review, 82, 132-141.

Hutchinson, E. (2017). 3.4 Building Supply and Producer Surplus. Principles of

Microeconomics.

Lipsky, T., Wright, J. D., Ginsburg, D. H., & Yun, J. M. (2018). The United States Federal Trade

Commission Hearings on Competition and Consumer Protection in the 21st Century,

Hearing on Concentration and Competitiveness in the US Economy, Comment of the

Global Antitrust Institute, Antonin Scalia Law School, George Mason University. George

Mason Law & Economics Research Paper, (18-25).

Tremblay, C. H., & Tremblay, V. J. (2019). Oligopoly Games And The Cournot–Bertrand

Model: A Survey. Journal of Economic Surveys, 33(5), 1555-1577.

Wu, C. (2017). Strategic aspects of oligopolistic vertical integration. Elsevier.

Zeuthen, F. (2018). Problems of monopoly and economic warfare. Routledge.

Doda, B. (2016). How to price carbon in good times… and bad!. Wiley Interdisciplinary

Reviews: Climate Change, 7(1), 135-144.

Gomez-Martinez, F., Onderstal, S., & Sonnemans, J. (2016). Firm-specific information and

explicit collusion in experimental oligopolies. European Economic Review, 82, 132-141.

Hutchinson, E. (2017). 3.4 Building Supply and Producer Surplus. Principles of

Microeconomics.

Lipsky, T., Wright, J. D., Ginsburg, D. H., & Yun, J. M. (2018). The United States Federal Trade

Commission Hearings on Competition and Consumer Protection in the 21st Century,

Hearing on Concentration and Competitiveness in the US Economy, Comment of the

Global Antitrust Institute, Antonin Scalia Law School, George Mason University. George

Mason Law & Economics Research Paper, (18-25).

Tremblay, C. H., & Tremblay, V. J. (2019). Oligopoly Games And The Cournot–Bertrand

Model: A Survey. Journal of Economic Surveys, 33(5), 1555-1577.

Wu, C. (2017). Strategic aspects of oligopolistic vertical integration. Elsevier.

Zeuthen, F. (2018). Problems of monopoly and economic warfare. Routledge.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.