Marks & Spencer's: Business Environment and Stakeholder Analysis

VerifiedAdded on 2023/06/10

|12

|3617

|419

Report

AI Summary

This report provides a comprehensive analysis of the business environment surrounding Marks & Spencer's, a prominent British multinational retailer. It delves into various aspects, starting with an overview of the company's background, legal structure (Public Limited Company), and its position within an oligopoly market structure. The report identifies and analyzes key stakeholders, including shareholders, and employs a stakeholder analysis process to prioritize their involvement. Furthermore, it utilizes PESTLE analysis to evaluate the political, economic, social, technological, legal, and environmental factors influencing the business. The report also highlights the importance of Porter's Five Forces model in assessing competitive strength and profitability within the industry, examining factors such as the bargaining power of customers and suppliers. Desklib offers a wide range of solved assignments and study tools for students.

Understanding the business environment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1...................................................................................................................................3

TASK 2...................................................................................................................................4

Task 3.....................................................................................................................................7

TASK-4..................................................................................................................................9

CONCLUSION..............................................................................................................................10

References .....................................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1...................................................................................................................................3

TASK 2...................................................................................................................................4

Task 3.....................................................................................................................................7

TASK-4..................................................................................................................................9

CONCLUSION..............................................................................................................................10

References .....................................................................................................................................11

INTRODUCTION

Business organisation is an entity formed by an individual or group of people in order to

attain more wealth in their ongoing life. Through this they are able to earn profit which can help

them to survive in the world by fulling basic needs. Their are various forms of business

organisation present from which an individual should select the most appropriate type in order to

run their business operation effectively and fluently. Due to this they can easily manage their

companies operation which can help them to create such products that can fulfil the needs of

their targeted audience. Furthermore, in this report the chosen organisation is Marks and

spencers which is one the biggest retail chain headquartered in United Kingdom. They provide

the large variety and differentiated fashionable products or services to their customer across the

world due to which they have build a strong market position in their industry. In this report

various aspects such as legal structure, market structure, pestle related to Marks and spencers is

been included in this report (Raum, Rawlings-Sanaei and Potter, 2021).

MAIN BODY

TASK 1

Marks and spencers in founded in the year 1884 and they became the first British

company to hit the revenue of 1 billion dollar. It is a British multinational company that have the

speciality in selling the cloths, beauty, home products and foods product. They deals in various

countries present across the globe. Marks and spencers currently have more than 959 stores in

UK, in which 615 stores only sells the food products to their customers. The management of this

company has collaborated with Ocado by which they are able to sell their food online to their

customers. The management of this company has adopt various advertising techniques in order

to convey the information of their products or services to their selected customer base. Marks

and Spencer's is a public limited company. This are the type of companies whose ownership is

organized through exchange of stocks present in their company. These are the company which

are listed on a stock exchange which helps an individual to acquire the share in their an specific

organisation. Public companies are formed under the legal structure formed in their region. The

objective of marks and spencers is to provide high quality and valuable products and services to

their customers. They always try to generate high quality , innovative and new products which

Business organisation is an entity formed by an individual or group of people in order to

attain more wealth in their ongoing life. Through this they are able to earn profit which can help

them to survive in the world by fulling basic needs. Their are various forms of business

organisation present from which an individual should select the most appropriate type in order to

run their business operation effectively and fluently. Due to this they can easily manage their

companies operation which can help them to create such products that can fulfil the needs of

their targeted audience. Furthermore, in this report the chosen organisation is Marks and

spencers which is one the biggest retail chain headquartered in United Kingdom. They provide

the large variety and differentiated fashionable products or services to their customer across the

world due to which they have build a strong market position in their industry. In this report

various aspects such as legal structure, market structure, pestle related to Marks and spencers is

been included in this report (Raum, Rawlings-Sanaei and Potter, 2021).

MAIN BODY

TASK 1

Marks and spencers in founded in the year 1884 and they became the first British

company to hit the revenue of 1 billion dollar. It is a British multinational company that have the

speciality in selling the cloths, beauty, home products and foods product. They deals in various

countries present across the globe. Marks and spencers currently have more than 959 stores in

UK, in which 615 stores only sells the food products to their customers. The management of this

company has collaborated with Ocado by which they are able to sell their food online to their

customers. The management of this company has adopt various advertising techniques in order

to convey the information of their products or services to their selected customer base. Marks

and Spencer's is a public limited company. This are the type of companies whose ownership is

organized through exchange of stocks present in their company. These are the company which

are listed on a stock exchange which helps an individual to acquire the share in their an specific

organisation. Public companies are formed under the legal structure formed in their region. The

objective of marks and spencers is to provide high quality and valuable products and services to

their customers. They always try to generate high quality , innovative and new products which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps them to maintain the strong position in the mind of their customers. Their vision is to stay

at the top by assuring the quality of their product which they are giving to their customers. Marks

and spencers follows the oligopoly market structure. It is one of the most famous British retailer

of clothing, food, household items which has more than 900 stores in 30 plus countries across the

globe. Market structure determines in which market an organisation should deal at low cost and

which customers are interested in their products and services. One of the most important

advantage of market structure is that it can assist an organisation that in what ways they can save

their funds present in their company (Alexander and Hjortsø, 2019).

TASK 2

STAKE HOLDERS

Stakeholders are those who are interested in the company and may influence or be influenced by

the company. The most important stakeholders in a typical company are their investors,

employees, customers, and suppliers. Stakeholders can be inside or outside the organization.

Internal stakeholders are individuals whose interest in the company is based on direct

relationships such as employment, ownership, and investment. External stakeholders are those

who do not work directly with the company but are influenced in any way by the actions and

outcomes of the company. Suppliers, creditors, and public groups are considered external

stakeholders. A common problem with companies with a large number of stakeholders is that the

interests of different stakeholders may not be aligned. In fact, the interests can be in direct

conflict. For example, from a shareholder's perspective, a company's main goal is to maximize

profits and increase shareholder value. Labour costs are inevitable for most companies, and they

have tight control over these costs. Stakeholders are important for several reasons. These are

important to internal stakeholders because business operations depend on their ability to work

together toward business goals. External stakeholders, on the other hand, can indirectly impact

your business. For example, customers may change purchasing habits, suppliers may change

manufacturing and distribution practices, and governments may change legislation. Ultimately,

managing relationships with internal and external stakeholders is key to a company's long-term

success.

SHARE HOLDERS

Shareholders, also called shareholders, are individuals, companies, or institutions that

own at least a portion of a company's shares. Shareholders are essentially owners of the company

at the top by assuring the quality of their product which they are giving to their customers. Marks

and spencers follows the oligopoly market structure. It is one of the most famous British retailer

of clothing, food, household items which has more than 900 stores in 30 plus countries across the

globe. Market structure determines in which market an organisation should deal at low cost and

which customers are interested in their products and services. One of the most important

advantage of market structure is that it can assist an organisation that in what ways they can save

their funds present in their company (Alexander and Hjortsø, 2019).

TASK 2

STAKE HOLDERS

Stakeholders are those who are interested in the company and may influence or be influenced by

the company. The most important stakeholders in a typical company are their investors,

employees, customers, and suppliers. Stakeholders can be inside or outside the organization.

Internal stakeholders are individuals whose interest in the company is based on direct

relationships such as employment, ownership, and investment. External stakeholders are those

who do not work directly with the company but are influenced in any way by the actions and

outcomes of the company. Suppliers, creditors, and public groups are considered external

stakeholders. A common problem with companies with a large number of stakeholders is that the

interests of different stakeholders may not be aligned. In fact, the interests can be in direct

conflict. For example, from a shareholder's perspective, a company's main goal is to maximize

profits and increase shareholder value. Labour costs are inevitable for most companies, and they

have tight control over these costs. Stakeholders are important for several reasons. These are

important to internal stakeholders because business operations depend on their ability to work

together toward business goals. External stakeholders, on the other hand, can indirectly impact

your business. For example, customers may change purchasing habits, suppliers may change

manufacturing and distribution practices, and governments may change legislation. Ultimately,

managing relationships with internal and external stakeholders is key to a company's long-term

success.

SHARE HOLDERS

Shareholders, also called shareholders, are individuals, companies, or institutions that

own at least a portion of a company's shares. Shareholders are essentially owners of the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and therefore benefit from the success of the company. These rewards are offered in the form of

monetary gains paid as higher stock valuations or dividends. After that, the shareholders are

divided into two parts:-

Common shareholders- A common shareholder is a person who owns the common stock of a

company. They are the most common type of shareholder and have voting rights on issues that

affect the company. Because they control how the company operates, they have the right to file a

class action proceeding against the company for any misconduct that could harm the

organization.

Preferred shareholders- On the other hand, it is rare. Unlike ordinary shareholders, they own

some of the company's preferred stock and do not have voting rights or a voice in the company's

management. (Eskerod, and Larsen, 2018)

STAKE HORLDER ANALYSIS.

It is a systematic framework that helps an organization to identify, examine and prioritize

the entities that are directly affected by the business operations conducted by an organization.

Not everyone involved needs the same attention. Careful analysis helps organizations identify

stakeholders who support and oppose the project, how strongly they feel about the project, and

how much they can influence the outcome. This valuable information helps organizations make

decisions. Who and how much an organisation need to work with in the course of the project? By

concentrating efforts in this way, organizations do not waste time and resources unnecessarily. A

thorough stakeholder assessment helps organizations determine which types of communication

and messages are most successful. This allows organizations to minimize negative perceptions,

amplify positive impacts, and resolve conflicts before they escalate. Knowledge also helps the

management of company better to adjust their daily commitment to get the results an

organisation want.

STAKEHOLDER ANALYSIS PROCESS

Identify Stakeholders

The first phase of stakeholder involvement investigates potential third parties and

organizations. There may be different groups that are directly influenced by the Marks &

Spencer Management Initiative, have influence or power over their success, and are involved in

successful or unsuccessful completion. (Franco-Trigo and et.al., 2020).

monetary gains paid as higher stock valuations or dividends. After that, the shareholders are

divided into two parts:-

Common shareholders- A common shareholder is a person who owns the common stock of a

company. They are the most common type of shareholder and have voting rights on issues that

affect the company. Because they control how the company operates, they have the right to file a

class action proceeding against the company for any misconduct that could harm the

organization.

Preferred shareholders- On the other hand, it is rare. Unlike ordinary shareholders, they own

some of the company's preferred stock and do not have voting rights or a voice in the company's

management. (Eskerod, and Larsen, 2018)

STAKE HORLDER ANALYSIS.

It is a systematic framework that helps an organization to identify, examine and prioritize

the entities that are directly affected by the business operations conducted by an organization.

Not everyone involved needs the same attention. Careful analysis helps organizations identify

stakeholders who support and oppose the project, how strongly they feel about the project, and

how much they can influence the outcome. This valuable information helps organizations make

decisions. Who and how much an organisation need to work with in the course of the project? By

concentrating efforts in this way, organizations do not waste time and resources unnecessarily. A

thorough stakeholder assessment helps organizations determine which types of communication

and messages are most successful. This allows organizations to minimize negative perceptions,

amplify positive impacts, and resolve conflicts before they escalate. Knowledge also helps the

management of company better to adjust their daily commitment to get the results an

organisation want.

STAKEHOLDER ANALYSIS PROCESS

Identify Stakeholders

The first phase of stakeholder involvement investigates potential third parties and

organizations. There may be different groups that are directly influenced by the Marks &

Spencer Management Initiative, have influence or power over their success, and are involved in

successful or unsuccessful completion. (Franco-Trigo and et.al., 2020).

Study Stakeholder

Once the potential stakeholders have been identified, the organization needs to do some

research. Start online research to identify organization's mission, how the management of

organization overlaps with its goals, organization's reputation, level of activity and public profile,

key touchpoints, and more. In addition to online information, it also helps the management of the

company to reach out to others directly over the phone to gain insights that may not be available

online.

Prioritize stakeholder

After a better understanding of the stakeholder ecosystem, the next step is to prioritize the

general public. There are several criteria for classifying or classifying stakeholders, and some of

the common groups used by Proof are:

Relevance – Do they share similar interests and goals?

Visibility – Are they active publicly, and in the right circles?

Credibility – Do they have a strong reputation and legitimacy?

Influence – Do they have the ear of companies audience, and the audience’s influencers

and decision-makers?

Reach – Are they active in the jurisdictions that matter to the company– i.e., nationally,

regionally, locally?

Contact Stakeholder

At last, after the management of Marks and spencers is able to identifies, researched and

prioritize their most valuable stakeholder, then the final stage in this process is to examine the

area in their business where they have more interest. By using various tools and information

techniques the management of the company is able to identify the interest level by which they

can build such kind of process that can highly involve the stakeholder in the business

organisation. For this stage, an organisation should appoint highly educated and skilled

employees that can properly convey the message to the present stakeholders.

Once the potential stakeholders have been identified, the organization needs to do some

research. Start online research to identify organization's mission, how the management of

organization overlaps with its goals, organization's reputation, level of activity and public profile,

key touchpoints, and more. In addition to online information, it also helps the management of the

company to reach out to others directly over the phone to gain insights that may not be available

online.

Prioritize stakeholder

After a better understanding of the stakeholder ecosystem, the next step is to prioritize the

general public. There are several criteria for classifying or classifying stakeholders, and some of

the common groups used by Proof are:

Relevance – Do they share similar interests and goals?

Visibility – Are they active publicly, and in the right circles?

Credibility – Do they have a strong reputation and legitimacy?

Influence – Do they have the ear of companies audience, and the audience’s influencers

and decision-makers?

Reach – Are they active in the jurisdictions that matter to the company– i.e., nationally,

regionally, locally?

Contact Stakeholder

At last, after the management of Marks and spencers is able to identifies, researched and

prioritize their most valuable stakeholder, then the final stage in this process is to examine the

area in their business where they have more interest. By using various tools and information

techniques the management of the company is able to identify the interest level by which they

can build such kind of process that can highly involve the stakeholder in the business

organisation. For this stage, an organisation should appoint highly educated and skilled

employees that can properly convey the message to the present stakeholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

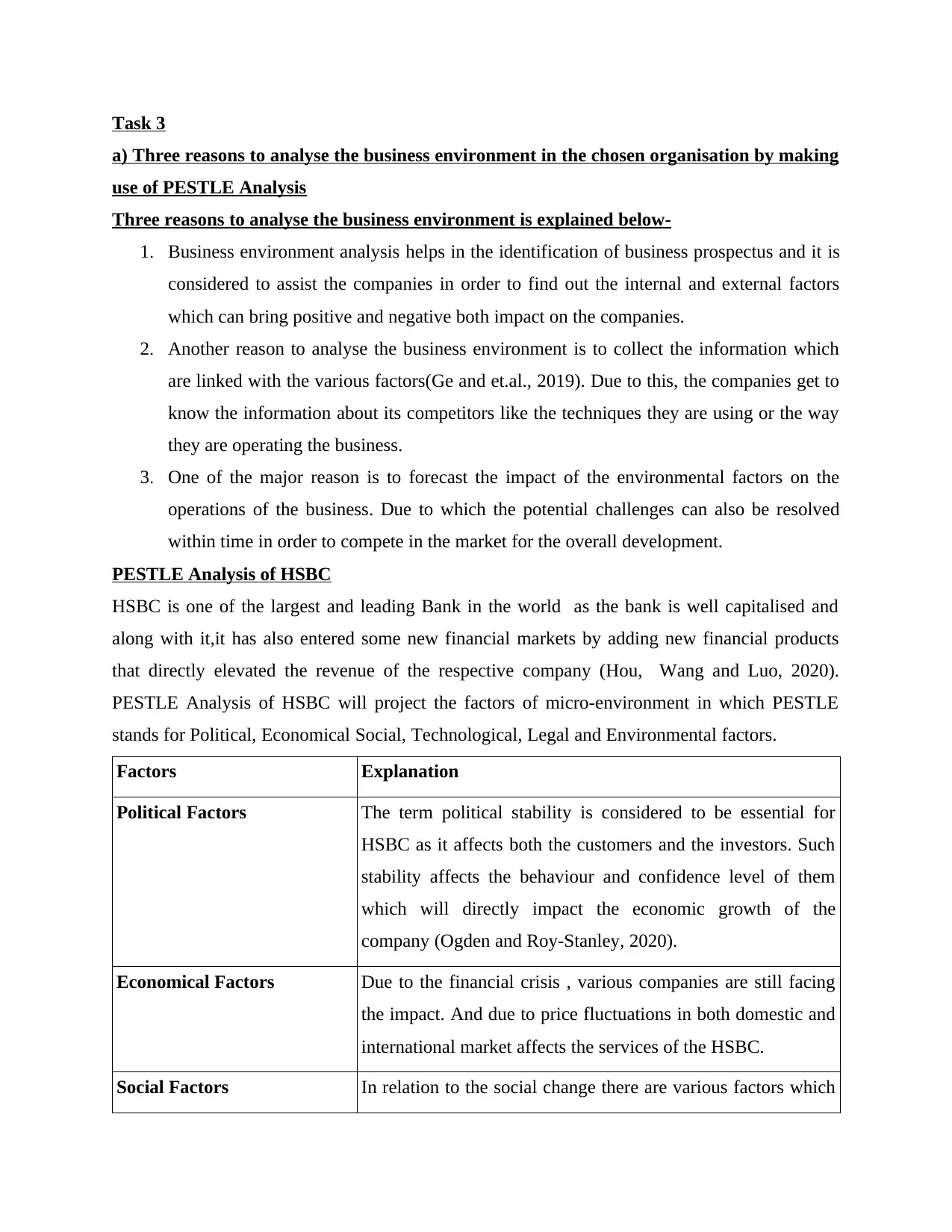

Task 3

a) Three reasons to analyse the business environment in the chosen organisation by making

use of PESTLE Analysis

Three reasons to analyse the business environment is explained below-

1. Business environment analysis helps in the identification of business prospectus and it is

considered to assist the companies in order to find out the internal and external factors

which can bring positive and negative both impact on the companies.

2. Another reason to analyse the business environment is to collect the information which

are linked with the various factors(Ge and et.al., 2019). Due to this, the companies get to

know the information about its competitors like the techniques they are using or the way

they are operating the business.

3. One of the major reason is to forecast the impact of the environmental factors on the

operations of the business. Due to which the potential challenges can also be resolved

within time in order to compete in the market for the overall development.

PESTLE Analysis of HSBC

HSBC is one of the largest and leading Bank in the world as the bank is well capitalised and

along with it,it has also entered some new financial markets by adding new financial products

that directly elevated the revenue of the respective company (Hou, Wang and Luo, 2020).

PESTLE Analysis of HSBC will project the factors of micro-environment in which PESTLE

stands for Political, Economical Social, Technological, Legal and Environmental factors.

Factors Explanation

Political Factors The term political stability is considered to be essential for

HSBC as it affects both the customers and the investors. Such

stability affects the behaviour and confidence level of them

which will directly impact the economic growth of the

company (Ogden and Roy-Stanley, 2020).

Economical Factors Due to the financial crisis , various companies are still facing

the impact. And due to price fluctuations in both domestic and

international market affects the services of the HSBC.

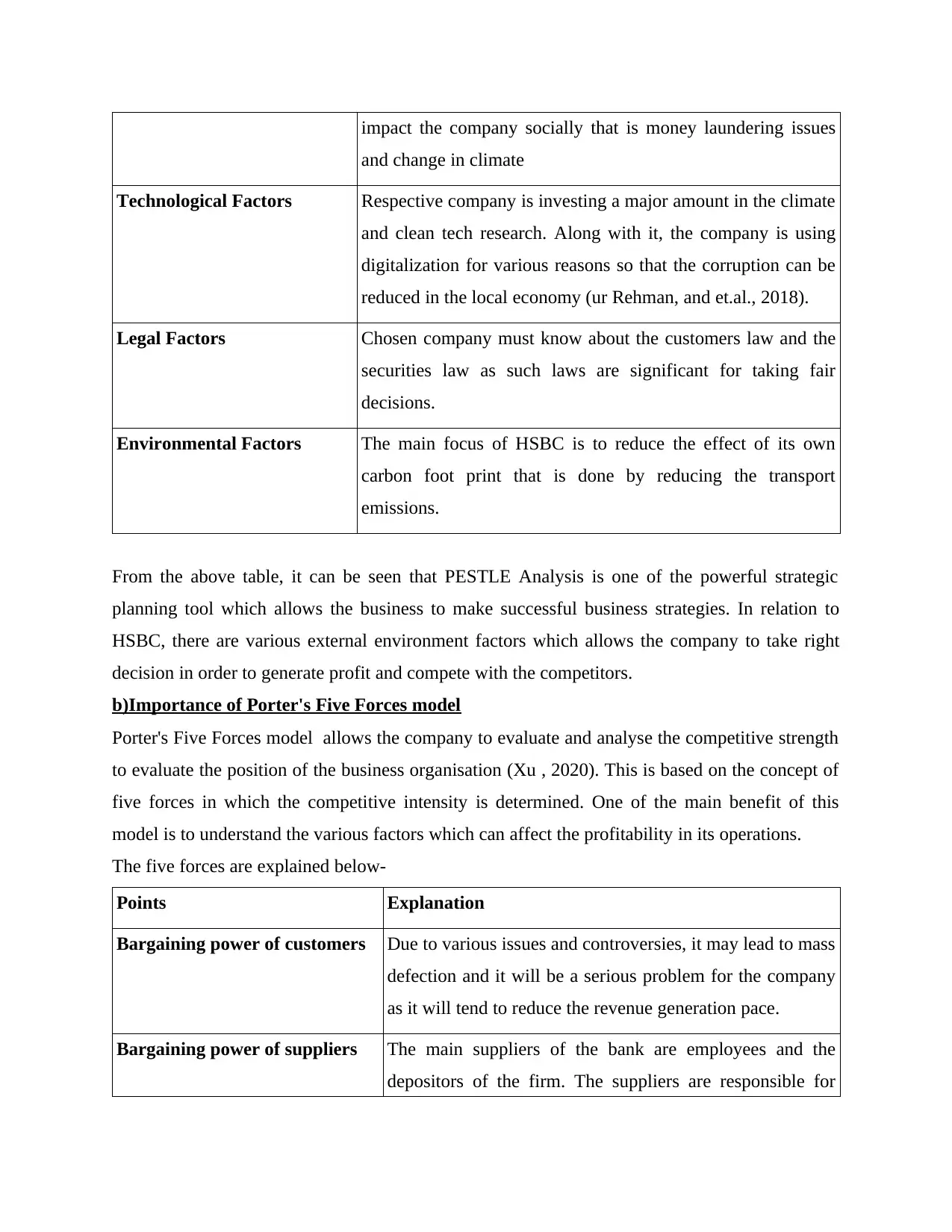

Social Factors In relation to the social change there are various factors which

a) Three reasons to analyse the business environment in the chosen organisation by making

use of PESTLE Analysis

Three reasons to analyse the business environment is explained below-

1. Business environment analysis helps in the identification of business prospectus and it is

considered to assist the companies in order to find out the internal and external factors

which can bring positive and negative both impact on the companies.

2. Another reason to analyse the business environment is to collect the information which

are linked with the various factors(Ge and et.al., 2019). Due to this, the companies get to

know the information about its competitors like the techniques they are using or the way

they are operating the business.

3. One of the major reason is to forecast the impact of the environmental factors on the

operations of the business. Due to which the potential challenges can also be resolved

within time in order to compete in the market for the overall development.

PESTLE Analysis of HSBC

HSBC is one of the largest and leading Bank in the world as the bank is well capitalised and

along with it,it has also entered some new financial markets by adding new financial products

that directly elevated the revenue of the respective company (Hou, Wang and Luo, 2020).

PESTLE Analysis of HSBC will project the factors of micro-environment in which PESTLE

stands for Political, Economical Social, Technological, Legal and Environmental factors.

Factors Explanation

Political Factors The term political stability is considered to be essential for

HSBC as it affects both the customers and the investors. Such

stability affects the behaviour and confidence level of them

which will directly impact the economic growth of the

company (Ogden and Roy-Stanley, 2020).

Economical Factors Due to the financial crisis , various companies are still facing

the impact. And due to price fluctuations in both domestic and

international market affects the services of the HSBC.

Social Factors In relation to the social change there are various factors which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

impact the company socially that is money laundering issues

and change in climate

Technological Factors Respective company is investing a major amount in the climate

and clean tech research. Along with it, the company is using

digitalization for various reasons so that the corruption can be

reduced in the local economy (ur Rehman, and et.al., 2018).

Legal Factors Chosen company must know about the customers law and the

securities law as such laws are significant for taking fair

decisions.

Environmental Factors The main focus of HSBC is to reduce the effect of its own

carbon foot print that is done by reducing the transport

emissions.

From the above table, it can be seen that PESTLE Analysis is one of the powerful strategic

planning tool which allows the business to make successful business strategies. In relation to

HSBC, there are various external environment factors which allows the company to take right

decision in order to generate profit and compete with the competitors.

b)Importance of Porter's Five Forces model

Porter's Five Forces model allows the company to evaluate and analyse the competitive strength

to evaluate the position of the business organisation (Xu , 2020). This is based on the concept of

five forces in which the competitive intensity is determined. One of the main benefit of this

model is to understand the various factors which can affect the profitability in its operations.

The five forces are explained below-

Points Explanation

Bargaining power of customers Due to various issues and controversies, it may lead to mass

defection and it will be a serious problem for the company

as it will tend to reduce the revenue generation pace.

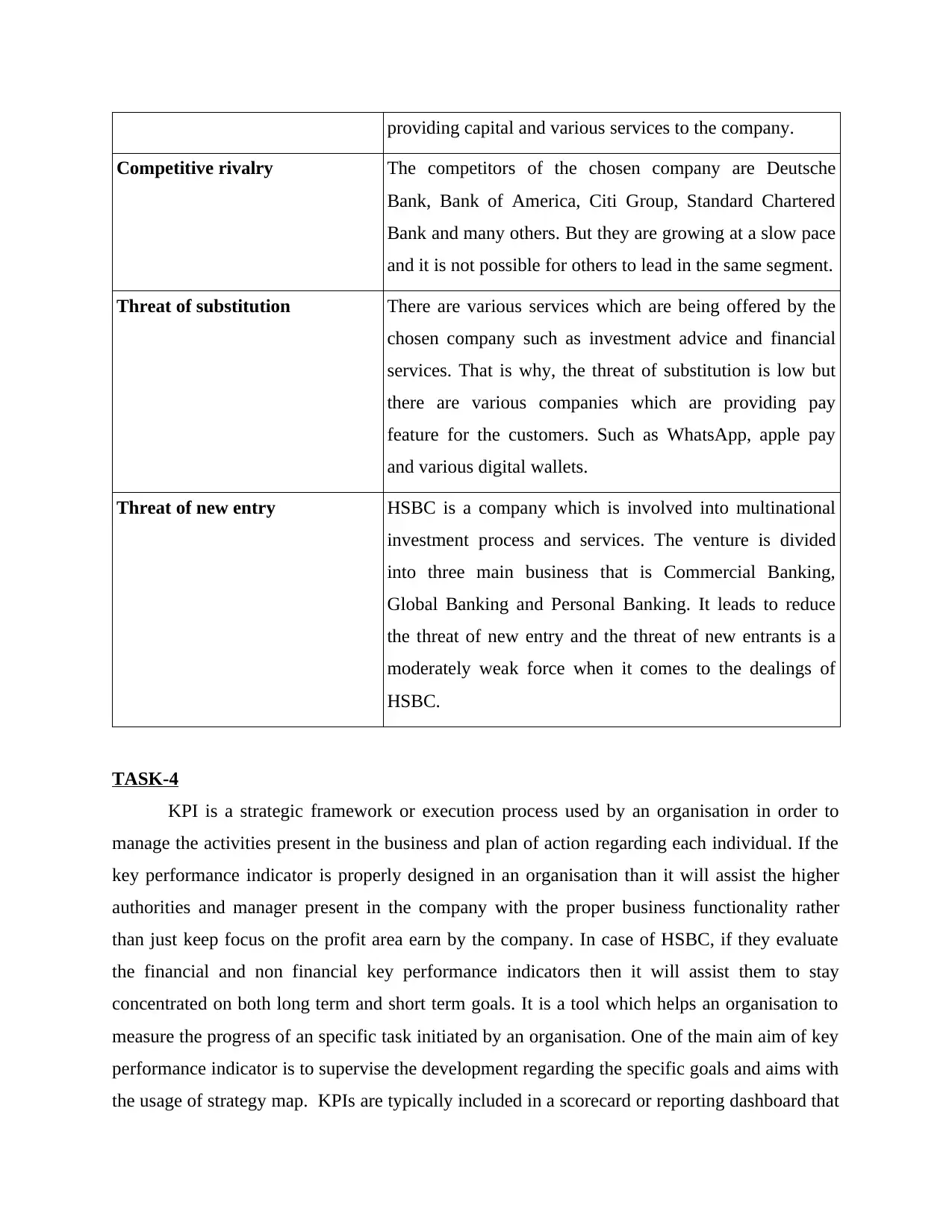

Bargaining power of suppliers The main suppliers of the bank are employees and the

depositors of the firm. The suppliers are responsible for

and change in climate

Technological Factors Respective company is investing a major amount in the climate

and clean tech research. Along with it, the company is using

digitalization for various reasons so that the corruption can be

reduced in the local economy (ur Rehman, and et.al., 2018).

Legal Factors Chosen company must know about the customers law and the

securities law as such laws are significant for taking fair

decisions.

Environmental Factors The main focus of HSBC is to reduce the effect of its own

carbon foot print that is done by reducing the transport

emissions.

From the above table, it can be seen that PESTLE Analysis is one of the powerful strategic

planning tool which allows the business to make successful business strategies. In relation to

HSBC, there are various external environment factors which allows the company to take right

decision in order to generate profit and compete with the competitors.

b)Importance of Porter's Five Forces model

Porter's Five Forces model allows the company to evaluate and analyse the competitive strength

to evaluate the position of the business organisation (Xu , 2020). This is based on the concept of

five forces in which the competitive intensity is determined. One of the main benefit of this

model is to understand the various factors which can affect the profitability in its operations.

The five forces are explained below-

Points Explanation

Bargaining power of customers Due to various issues and controversies, it may lead to mass

defection and it will be a serious problem for the company

as it will tend to reduce the revenue generation pace.

Bargaining power of suppliers The main suppliers of the bank are employees and the

depositors of the firm. The suppliers are responsible for

providing capital and various services to the company.

Competitive rivalry The competitors of the chosen company are Deutsche

Bank, Bank of America, Citi Group, Standard Chartered

Bank and many others. But they are growing at a slow pace

and it is not possible for others to lead in the same segment.

Threat of substitution There are various services which are being offered by the

chosen company such as investment advice and financial

services. That is why, the threat of substitution is low but

there are various companies which are providing pay

feature for the customers. Such as WhatsApp, apple pay

and various digital wallets.

Threat of new entry HSBC is a company which is involved into multinational

investment process and services. The venture is divided

into three main business that is Commercial Banking,

Global Banking and Personal Banking. It leads to reduce

the threat of new entry and the threat of new entrants is a

moderately weak force when it comes to the dealings of

HSBC.

TASK-4

KPI is a strategic framework or execution process used by an organisation in order to

manage the activities present in the business and plan of action regarding each individual. If the

key performance indicator is properly designed in an organisation than it will assist the higher

authorities and manager present in the company with the proper business functionality rather

than just keep focus on the profit area earn by the company. In case of HSBC, if they evaluate

the financial and non financial key performance indicators then it will assist them to stay

concentrated on both long term and short term goals. It is a tool which helps an organisation to

measure the progress of an specific task initiated by an organisation. One of the main aim of key

performance indicator is to supervise the development regarding the specific goals and aims with

the usage of strategy map. KPIs are typically included in a scorecard or reporting dashboard that

Competitive rivalry The competitors of the chosen company are Deutsche

Bank, Bank of America, Citi Group, Standard Chartered

Bank and many others. But they are growing at a slow pace

and it is not possible for others to lead in the same segment.

Threat of substitution There are various services which are being offered by the

chosen company such as investment advice and financial

services. That is why, the threat of substitution is low but

there are various companies which are providing pay

feature for the customers. Such as WhatsApp, apple pay

and various digital wallets.

Threat of new entry HSBC is a company which is involved into multinational

investment process and services. The venture is divided

into three main business that is Commercial Banking,

Global Banking and Personal Banking. It leads to reduce

the threat of new entry and the threat of new entrants is a

moderately weak force when it comes to the dealings of

HSBC.

TASK-4

KPI is a strategic framework or execution process used by an organisation in order to

manage the activities present in the business and plan of action regarding each individual. If the

key performance indicator is properly designed in an organisation than it will assist the higher

authorities and manager present in the company with the proper business functionality rather

than just keep focus on the profit area earn by the company. In case of HSBC, if they evaluate

the financial and non financial key performance indicators then it will assist them to stay

concentrated on both long term and short term goals. It is a tool which helps an organisation to

measure the progress of an specific task initiated by an organisation. One of the main aim of key

performance indicator is to supervise the development regarding the specific goals and aims with

the usage of strategy map. KPIs are typically included in a scorecard or reporting dashboard that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

allows senior management, the board of directors, or other stakeholders to focus on the metrics

deemed most important to a company's success. Financial metrics are typically based on income

statement or balance sheet

components and may also report changes in revenue growth or expense categories. Non-financial

KPIs are other metrics used to evaluate activities that an organization considers important to the

achievement of its strategic goals. Typical non-financial KPIs include customer relationships,

employees, operations, quality, cycle times, and metrics related to a company's supply chain or

pipeline. Some people prefer to use the term "external finance" rather than "non-finance." This

suggests that all actions that contribute to an organization's success are ultimately financial. In

addition to financial and non-financial, other common classifications of performance indicators

are quantitative and qualitative. Fast or slow; short-term or long-term; input, output, or process

indicator, etc. KPI development is an overall strategic management process that connects an

organization's overall mission, vision, strategy, and its short-term and long-term goals to specific

strategic business goals and the projects or initiatives that support them. Must be part of. .. An

important first step in this process is to understand your organization's value drivers and the core

activities and competencies that underpin their value proposition. (Flew and Lim, 2019).

CONCLUSION

From the above report it has been concluded that, an organisation should always select a

appropriate and effective business structure in order to run their business operation fluently and

smoothly. Furthermore, in this report the chosen organisation is Marks and Spencer's which is a

multinational company located in various region of the world. Later on in this report information

regarding M&S such as their legal structure, shareholders, stakeholders are been included in this

report. At last, the key performance indicators related to financial and non-financial measures

which can HSBC in the future development is a part of this report.

deemed most important to a company's success. Financial metrics are typically based on income

statement or balance sheet

components and may also report changes in revenue growth or expense categories. Non-financial

KPIs are other metrics used to evaluate activities that an organization considers important to the

achievement of its strategic goals. Typical non-financial KPIs include customer relationships,

employees, operations, quality, cycle times, and metrics related to a company's supply chain or

pipeline. Some people prefer to use the term "external finance" rather than "non-finance." This

suggests that all actions that contribute to an organization's success are ultimately financial. In

addition to financial and non-financial, other common classifications of performance indicators

are quantitative and qualitative. Fast or slow; short-term or long-term; input, output, or process

indicator, etc. KPI development is an overall strategic management process that connects an

organization's overall mission, vision, strategy, and its short-term and long-term goals to specific

strategic business goals and the projects or initiatives that support them. Must be part of. .. An

important first step in this process is to understand your organization's value drivers and the core

activities and competencies that underpin their value proposition. (Flew and Lim, 2019).

CONCLUSION

From the above report it has been concluded that, an organisation should always select a

appropriate and effective business structure in order to run their business operation fluently and

smoothly. Furthermore, in this report the chosen organisation is Marks and Spencer's which is a

multinational company located in various region of the world. Later on in this report information

regarding M&S such as their legal structure, shareholders, stakeholders are been included in this

report. At last, the key performance indicators related to financial and non-financial measures

which can HSBC in the future development is a part of this report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journals

Alexander, I.K. and Hjortsø, C.N., 2019. Sources of complexity in participatory curriculum

development: an activity system and stakeholder analysis approach to the analyses of tensions

and contradictions. Higher Education, 77(2), pp.301-322.

Eskerod, P. and Larsen, T., 2018. Advancing project stakeholder analysis by the concept

‘shadows of the context’. International Journal of Project Management, 36(1), pp.161-169.

Flew, T. and Lim, T., 2019. Assessing policy I: Stakeholder analysis. In The Palgrave handbook

of methods for media policy research (pp. 541-555). Palgrave Macmillan, Cham.

Franco-Trigo, L., Fernandez-Llimos, F., Martínez-Martínez, F., Benrimoj, S.I. and Sabater-

Hernández, D., 2020. Stakeholder analysis in health innovation planning processes: a systematic

scoping review. Health Policy, 124(10), pp.1083-1099.

Ge, L., Li, H., Liu, J. and Zhou, A., 2019, June. Temporal graph convolutional networks for

traffic speed prediction considering external factors. In 2019 20th IEEE International Conference

on Mobile Data Management (MDM) (pp. 234-242). IEEE.

Hou, J., Wang, C. and Luo, S., 2020. How to improve the competiveness of distributed energy

resources in China with blockchain technology. Technological Forecasting and Social

Change, 151, p.119744.

Ogden, J. and Roy-Stanley, C., 2020. How do children make food choices? Using a think-aloud

method to explore the role of internal and external factors on eating behaviour. Appetite, 147,

p.104551.

Raum, S., Rawlings-Sanaei, F. and Potter, C., 2021. A web content-based method of stakeholder

analysis: The case of forestry in the context of natural resource management. Journal of

Environmental Management, 300, p.113733.

ur Rehman, Z., Khan, S.A., Khan, A. and Rahman, A., 2018. Internal factors, external factors

and bank profitability. Sarhad Journal of Management Sciences, 4(2), pp.246-259.

Xu, J., 2020. The growth and internationalisation of global and Chinese banks: The cases of

HSBC and ICBC (Doctoral dissertation, University of Cambridge).

Rossi, F., Barth, J.R. and Cebula, R.J., 2018. Do shareholder coalitions affect agency costs?

Evidence from Italian-listed companies. Research in International Business and Finance, 46,

pp.181-200.

Du, S., Ma, L. and Li, Z., 2022. Non-family shareholder governance and corporate risk-taking:

Evidence from Chinese family-controlled businesses. Journal of Business Research, 145, pp.156-

170.

Tokbolat, Y., Le, H. and Thompson, S., 2021. Corporate diversification, refocusing and

shareholder voting. International Review of Financial Analysis, 78, p.101924.

Moore, M.T., 2018. Shareholder primacy, labour and the historic ambivalence of UK company

law. In Research handbook on the history of corporate and company law. Edward Elgar

Publishing.

Hirose, R. and McCauley, D., 2022. The risks and impacts of nuclear decommissioning:

Stakeholder reflections on the UK nuclear industry. Energy Policy, 164, p.112862.

Graham, S., 2020. The influence of external and internal stakeholder pressures on the

implementation of upstream environmental supply chain practices. Business & Society, 59(2),

pp.351-383.

Books and Journals

Alexander, I.K. and Hjortsø, C.N., 2019. Sources of complexity in participatory curriculum

development: an activity system and stakeholder analysis approach to the analyses of tensions

and contradictions. Higher Education, 77(2), pp.301-322.

Eskerod, P. and Larsen, T., 2018. Advancing project stakeholder analysis by the concept

‘shadows of the context’. International Journal of Project Management, 36(1), pp.161-169.

Flew, T. and Lim, T., 2019. Assessing policy I: Stakeholder analysis. In The Palgrave handbook

of methods for media policy research (pp. 541-555). Palgrave Macmillan, Cham.

Franco-Trigo, L., Fernandez-Llimos, F., Martínez-Martínez, F., Benrimoj, S.I. and Sabater-

Hernández, D., 2020. Stakeholder analysis in health innovation planning processes: a systematic

scoping review. Health Policy, 124(10), pp.1083-1099.

Ge, L., Li, H., Liu, J. and Zhou, A., 2019, June. Temporal graph convolutional networks for

traffic speed prediction considering external factors. In 2019 20th IEEE International Conference

on Mobile Data Management (MDM) (pp. 234-242). IEEE.

Hou, J., Wang, C. and Luo, S., 2020. How to improve the competiveness of distributed energy

resources in China with blockchain technology. Technological Forecasting and Social

Change, 151, p.119744.

Ogden, J. and Roy-Stanley, C., 2020. How do children make food choices? Using a think-aloud

method to explore the role of internal and external factors on eating behaviour. Appetite, 147,

p.104551.

Raum, S., Rawlings-Sanaei, F. and Potter, C., 2021. A web content-based method of stakeholder

analysis: The case of forestry in the context of natural resource management. Journal of

Environmental Management, 300, p.113733.

ur Rehman, Z., Khan, S.A., Khan, A. and Rahman, A., 2018. Internal factors, external factors

and bank profitability. Sarhad Journal of Management Sciences, 4(2), pp.246-259.

Xu, J., 2020. The growth and internationalisation of global and Chinese banks: The cases of

HSBC and ICBC (Doctoral dissertation, University of Cambridge).

Rossi, F., Barth, J.R. and Cebula, R.J., 2018. Do shareholder coalitions affect agency costs?

Evidence from Italian-listed companies. Research in International Business and Finance, 46,

pp.181-200.

Du, S., Ma, L. and Li, Z., 2022. Non-family shareholder governance and corporate risk-taking:

Evidence from Chinese family-controlled businesses. Journal of Business Research, 145, pp.156-

170.

Tokbolat, Y., Le, H. and Thompson, S., 2021. Corporate diversification, refocusing and

shareholder voting. International Review of Financial Analysis, 78, p.101924.

Moore, M.T., 2018. Shareholder primacy, labour and the historic ambivalence of UK company

law. In Research handbook on the history of corporate and company law. Edward Elgar

Publishing.

Hirose, R. and McCauley, D., 2022. The risks and impacts of nuclear decommissioning:

Stakeholder reflections on the UK nuclear industry. Energy Policy, 164, p.112862.

Graham, S., 2020. The influence of external and internal stakeholder pressures on the

implementation of upstream environmental supply chain practices. Business & Society, 59(2),

pp.351-383.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.