Financial Analysis and Corporate Governance of Marks & Spencer Plc

VerifiedAdded on 2023/06/12

|18

|3922

|53

Report

AI Summary

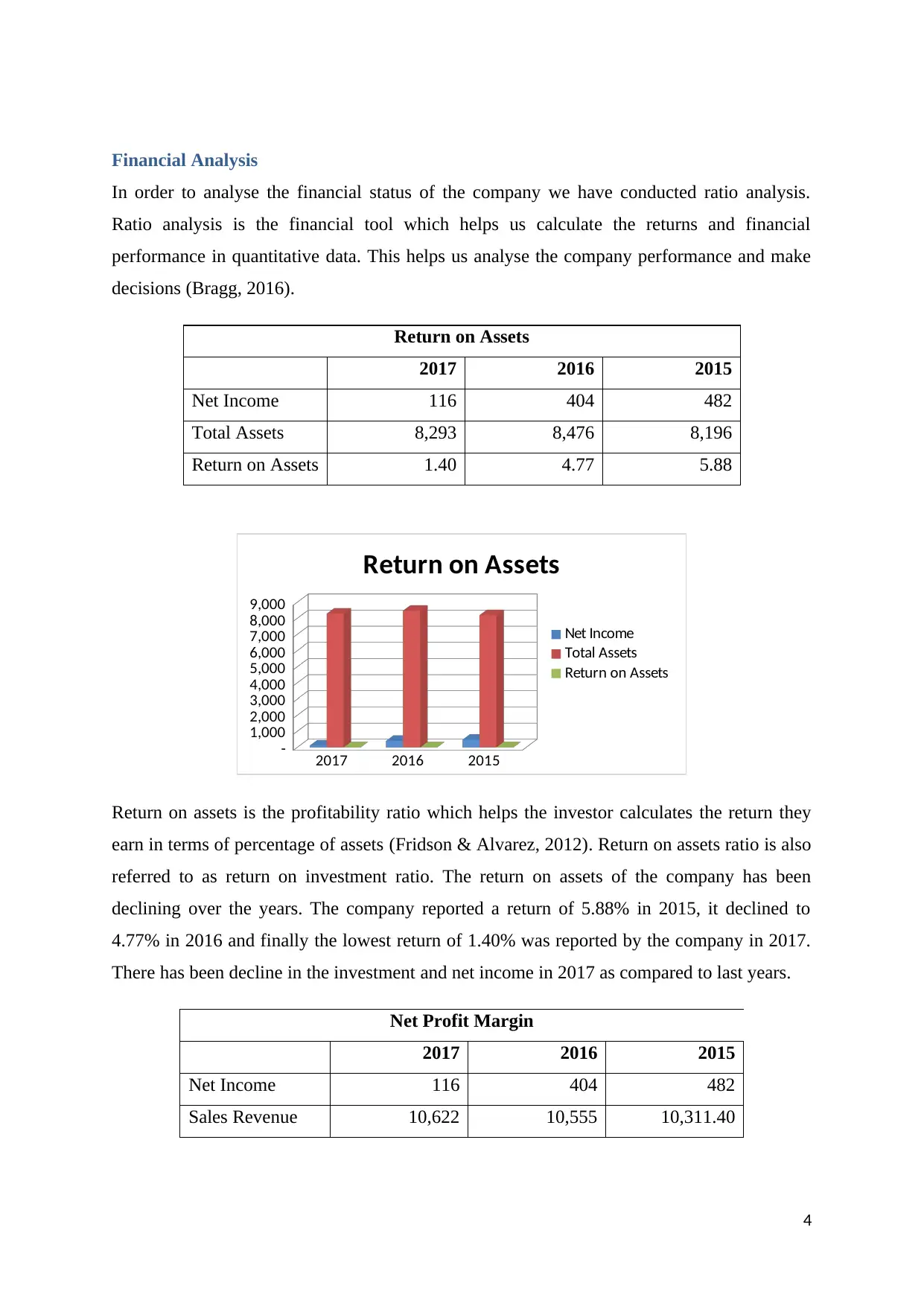

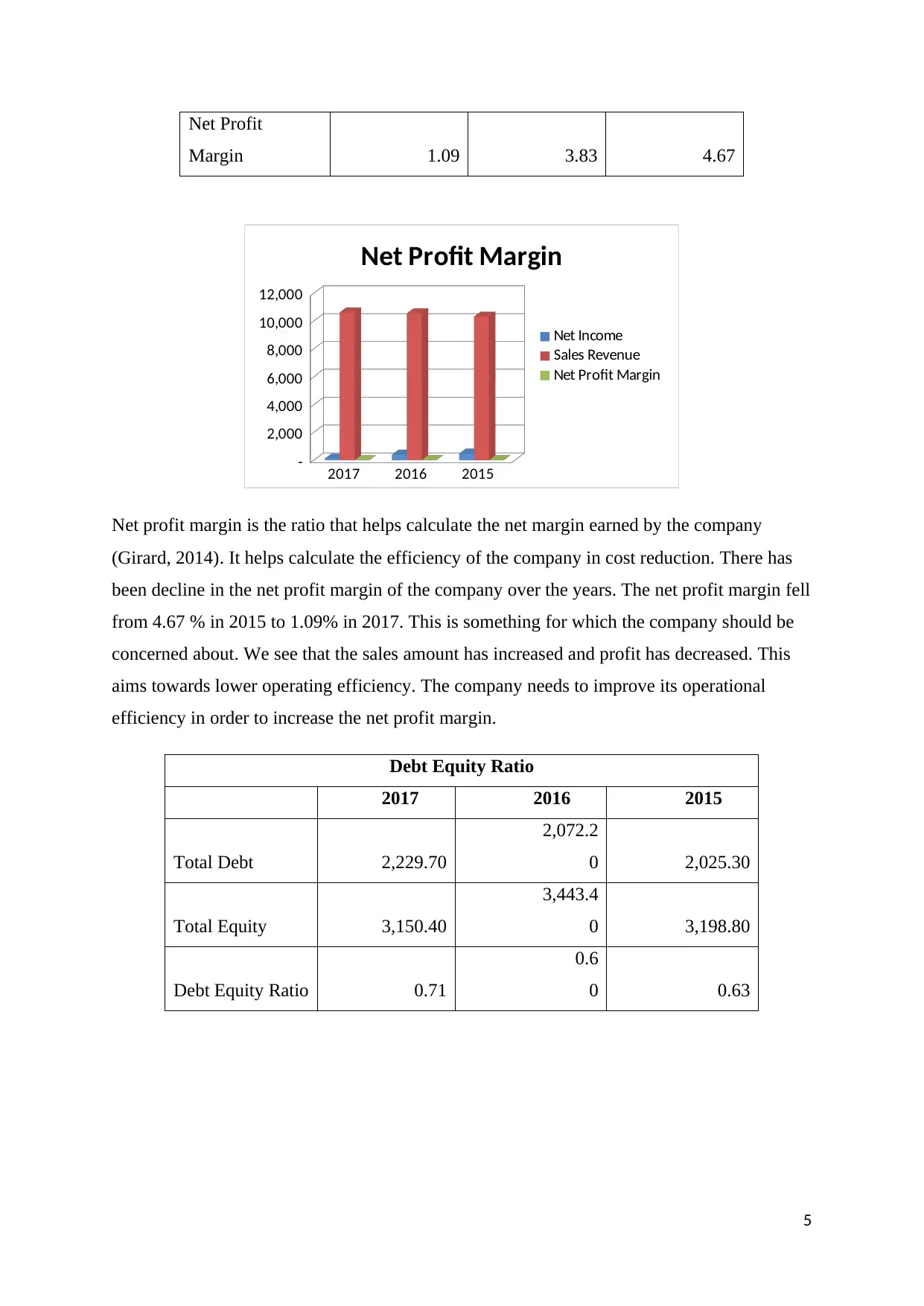

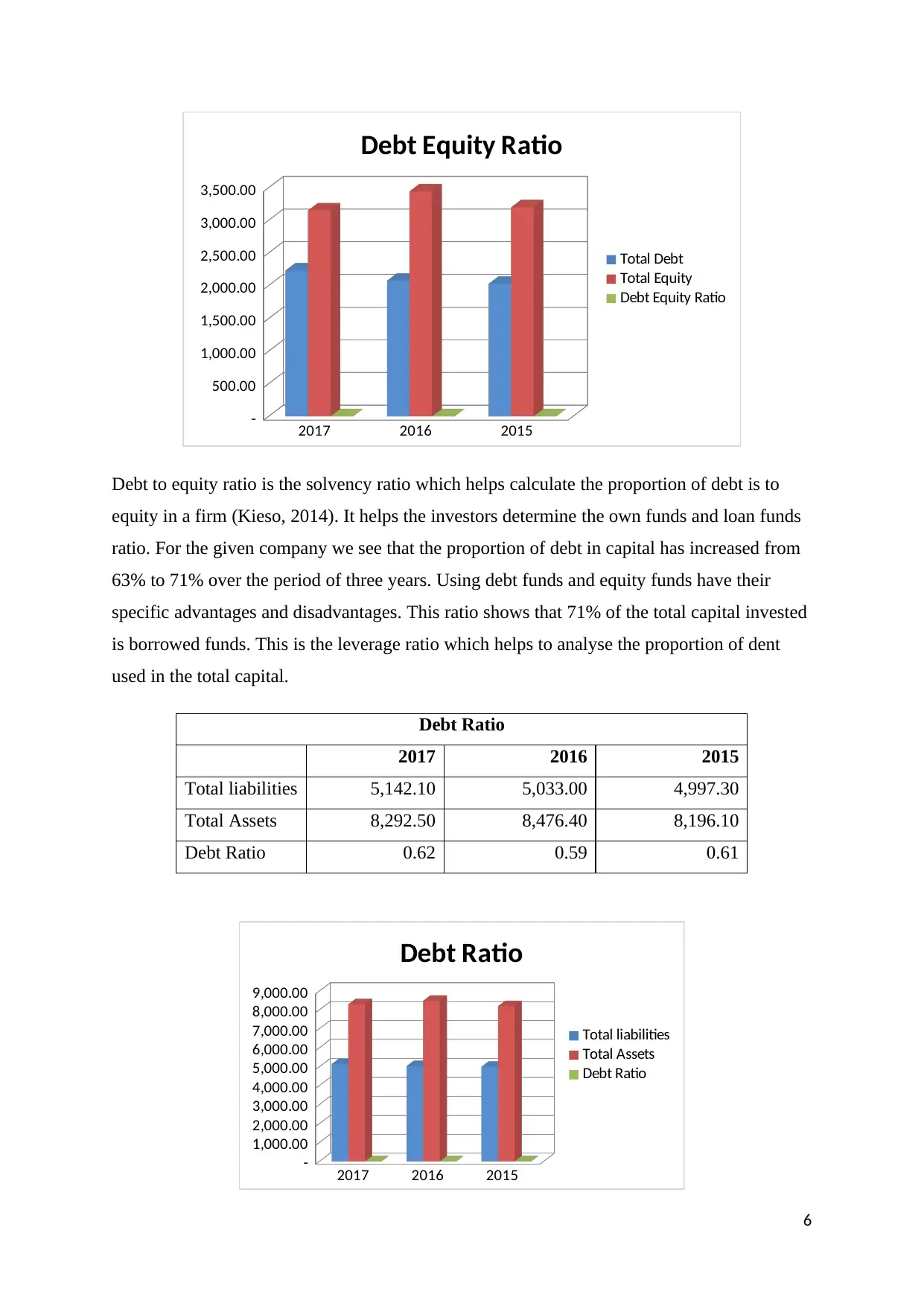

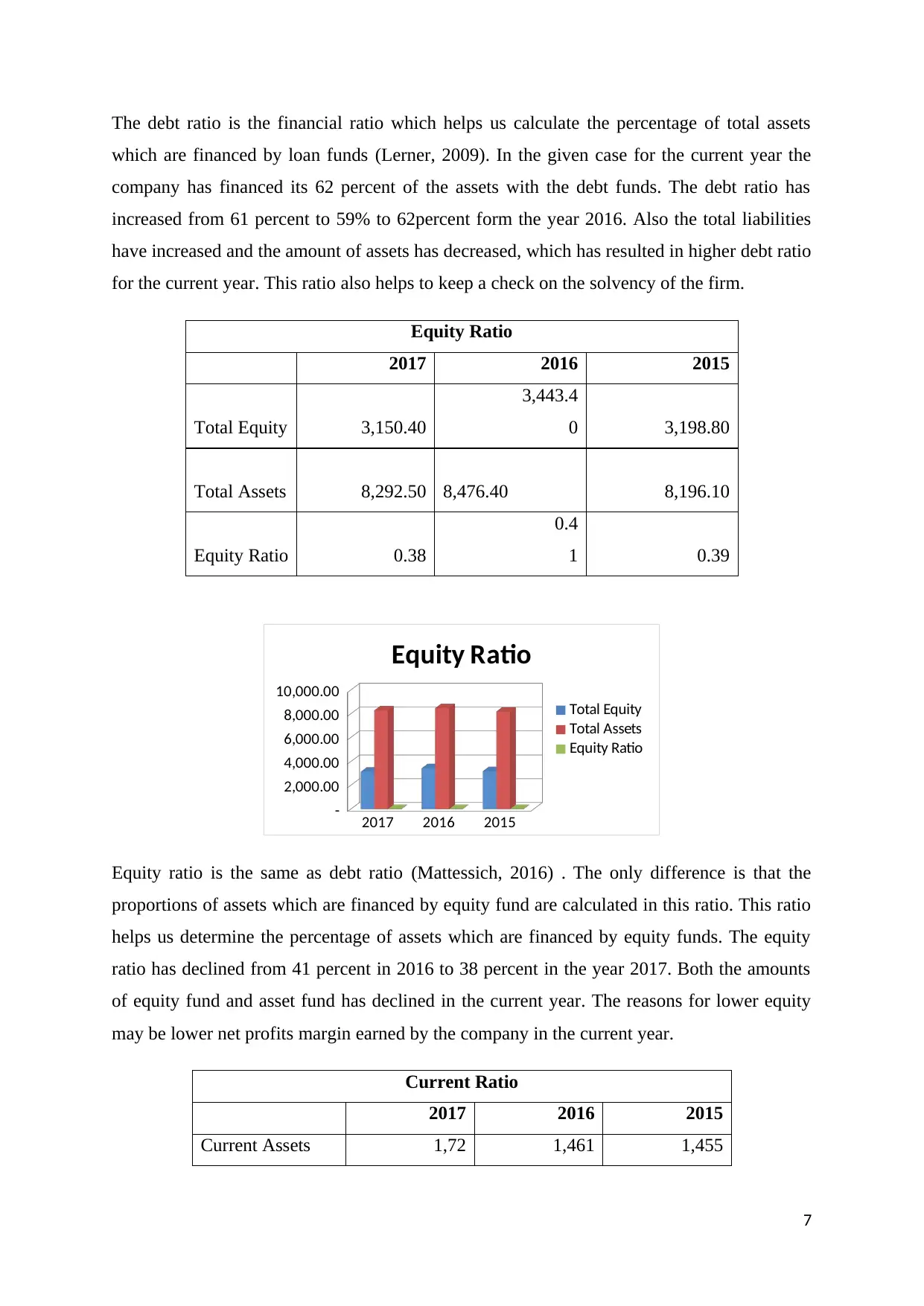

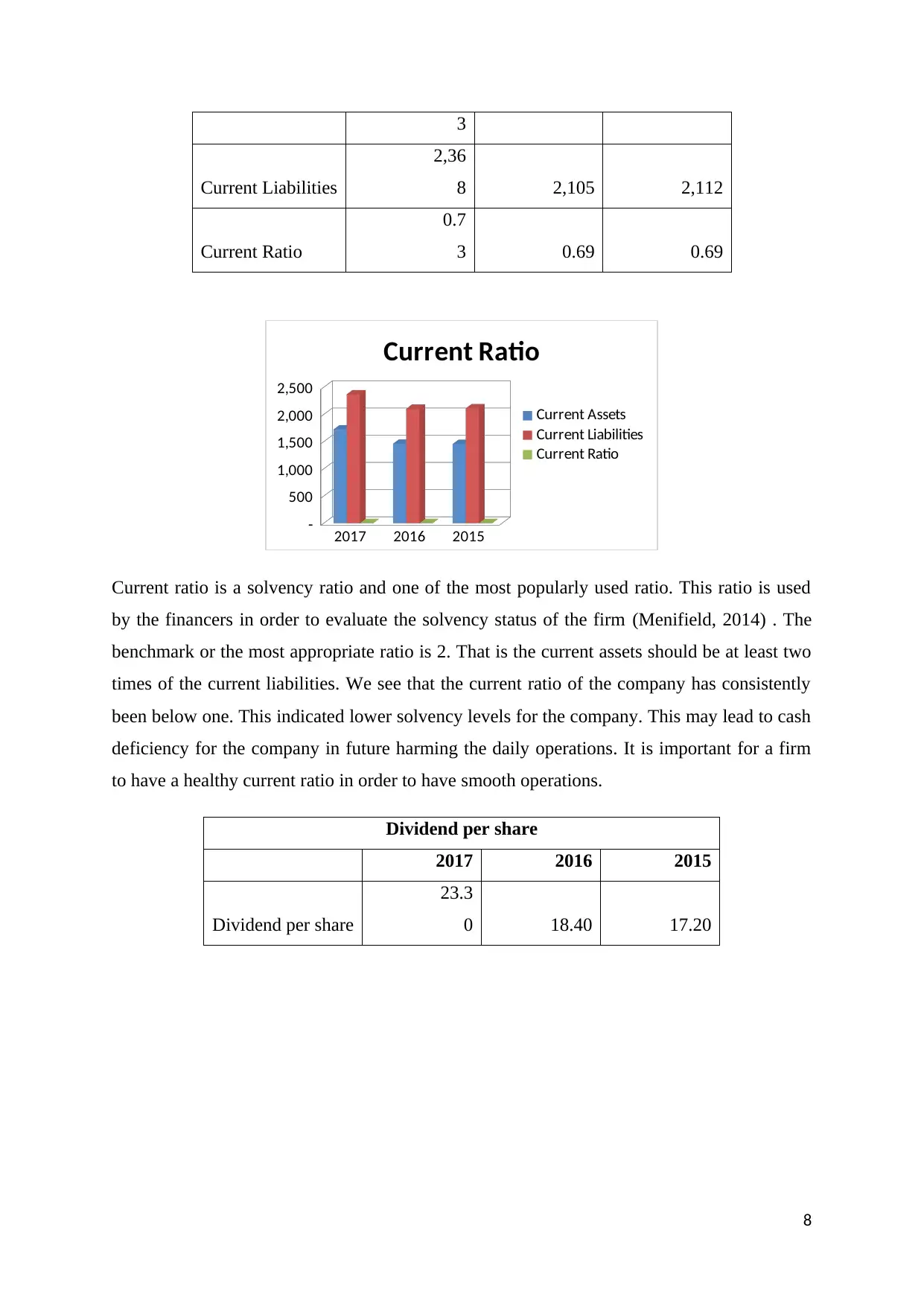

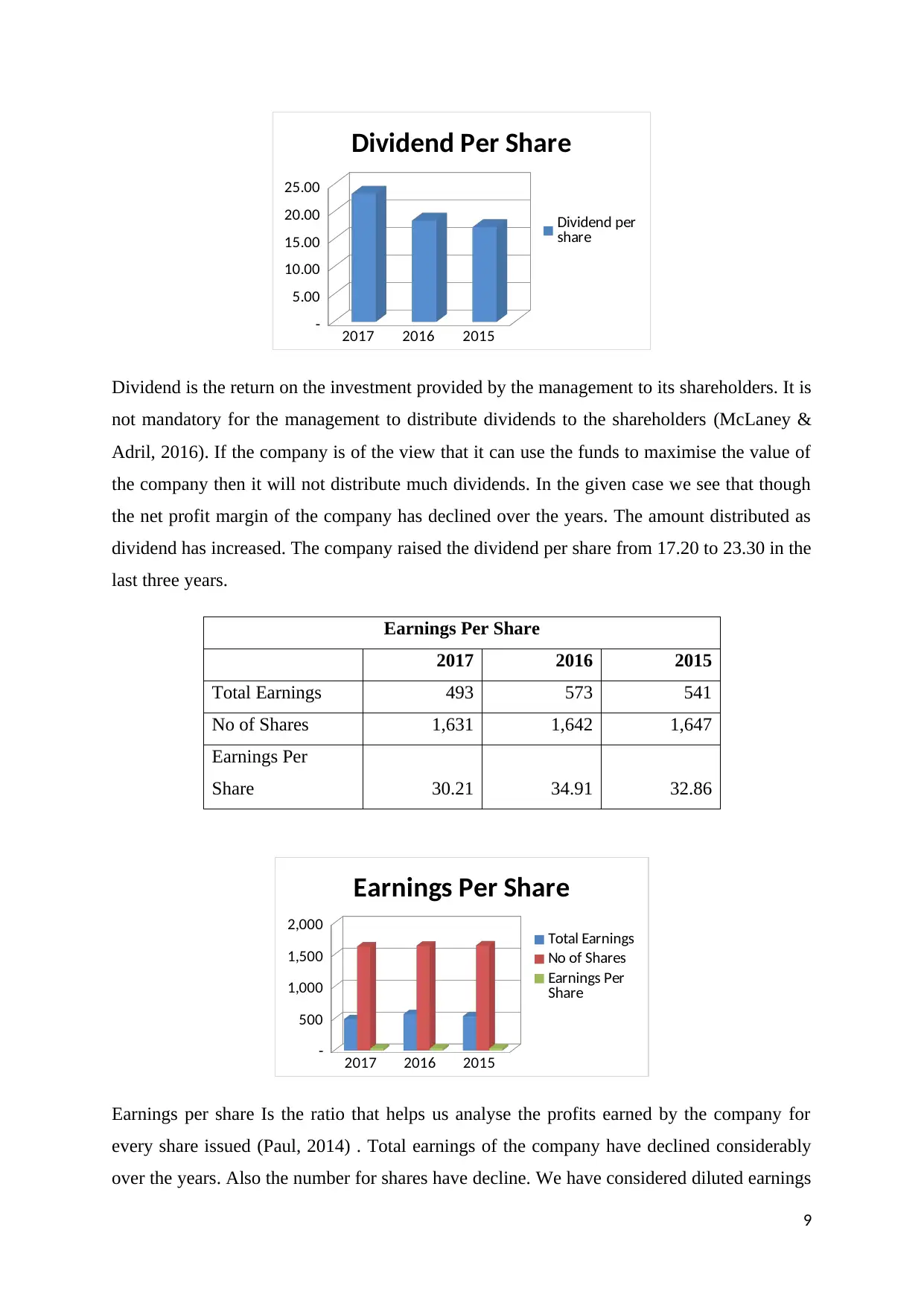

This report provides a comprehensive financial analysis of Marks & Spencer Plc, a leading British brand, using ratio analysis to evaluate the company's financial performance from 2015 to 2017. Key ratios such as Return on Assets, Net Profit Margin, Debt Equity Ratio, Debt Ratio, Equity Ratio, and Current Ratio are analyzed to assess profitability, solvency, and operational efficiency. The report identifies a decline in several key financial metrics, particularly in 2017, and attributes this to decreased revenues from the clothing line. In addition to quantitative analysis, the report discusses qualitative factors affecting the company's future performance, including its business model, competitive advantages, management strategies, relationships with third parties, and corporate governance practices. The analysis also considers the impact of declining market capitalization on shareholder wealth, concluding that while the company's standalone performance in the current year is reasonable, the overall trend indicates a need for improved operational efficiency and strategic adjustments to enhance profitability and shareholder value. This document is available on Desklib, a platform offering a wide range of study resources including past papers and solved assignments to support students in their academic endeavors.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.