HI5017 Managerial Accounting: Master Budget Analysis for Alpha HPA

VerifiedAdded on 2023/04/23

|23

|4406

|272

Report

AI Summary

This report provides an overview of the elements of a master budget, compares top-down and bottom-up budgeting approaches, and determines the most suitable approach for Alpha HPA Limited. It also develops a budgeted income statement for Alpha HPA Limited for 2019 based on the company's 2018 income statement data, analyzing the impacts of the projections made. The analysis concludes that a top-down budgeting approach is more favorable for Alpha HPA Limited as it supports effective management of business operations, and highlights the importance of a budgeted income statement for assessing the reasonableness of estimated financial outcomes.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The current report would provide a brief overview of the different elements of master

budget. The second section would focus on comparing the top-down and bottom-up

approach to the budget process and accordingly, the most suitable approach for Alpha HPA

Limited would be considered. Finally, the report would shed light on developing the

budgeted income statement for the concerned organisation for 2019 based on the actual

data disclosed in its income statement in 2018. From the analysis of bottom-up and top-

down budget approaches, the elements of the master budget could be prepared so that the

future operations of the business organisations could be supported adequately. By analysing

these two approaches, the top-down budget approach is deemed to be favourable for Alpha

HPA Limited, as it would aid the management of the organisation in conducting its business

operations effectively. With the help of budgeted income statement, it becomes easy to test

whether the estimated financial outcomes of an organisation seem to be reasonable.

Executive Summary:

The current report would provide a brief overview of the different elements of master

budget. The second section would focus on comparing the top-down and bottom-up

approach to the budget process and accordingly, the most suitable approach for Alpha HPA

Limited would be considered. Finally, the report would shed light on developing the

budgeted income statement for the concerned organisation for 2019 based on the actual

data disclosed in its income statement in 2018. From the analysis of bottom-up and top-

down budget approaches, the elements of the master budget could be prepared so that the

future operations of the business organisations could be supported adequately. By analysing

these two approaches, the top-down budget approach is deemed to be favourable for Alpha

HPA Limited, as it would aid the management of the organisation in conducting its business

operations effectively. With the help of budgeted income statement, it becomes easy to test

whether the estimated financial outcomes of an organisation seem to be reasonable.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:..............................................................................................................................3

a. Elements of the master budget:............................................................................................3

b. Comparison of top-down and bottom-up approach to the budget process:......................13

c. Budgeted income statement for 2019 for Alpha HPA Limited:...........................................15

d. Comparison of the actual and budgeted income statements:............................................16

Conclusion:...............................................................................................................................18

References:...............................................................................................................................20

Table of Contents

Introduction:..............................................................................................................................3

a. Elements of the master budget:............................................................................................3

b. Comparison of top-down and bottom-up approach to the budget process:......................13

c. Budgeted income statement for 2019 for Alpha HPA Limited:...........................................15

d. Comparison of the actual and budgeted income statements:............................................16

Conclusion:...............................................................................................................................18

References:...............................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

In the current era, all business organisations have to incur different types of costs

and this mandates the need for forming different types of budgets in order to keep track of

the actual and estimated expenses. In this context, Armitage, Webb and Glynn (2016)

advocated that a budget is a detailed future plan, which is usually denoted in formal

quantitative terms. Thus, budgets help in communicating the plan of the management

throughout the organisation. The aspect holds good for all ASX listed organisations and in

order to meet the purpose of this report, Alpha HPA Limited is taken into consideration. It is

an ASX listed organisation, which is involved in acquisition, exploration and mineral deposits

development in Australia and Indonesia (Collerinacobalt.com.au 2019).

This report would provide a brief overview of the different elements of master

budget. The second section would focus on comparing the top-down and bottom-up

approach to the budget process and accordingly, the most suitable approach for Alpha HPA

Limited would be considered. Finally, the report would shed light on developing the

budgeted income statement for the concerned organisation for 2019 based on the actual

data disclosed in its income statement in 2018 and accordingly, the impact of the changes

owing to the projections made would be analysed.

a. Elements of the master budget:

In the words of Barr and McClellan (2018), master budget is a plan developed to

manage the manufacturing and sales activities of an organisation for fulfilling profit and cash

flow objectives. In order to develop a successful master budget, the different elements of

the master budget need to be prepared in the initial stage accurately. In this way, master

Introduction:

In the current era, all business organisations have to incur different types of costs

and this mandates the need for forming different types of budgets in order to keep track of

the actual and estimated expenses. In this context, Armitage, Webb and Glynn (2016)

advocated that a budget is a detailed future plan, which is usually denoted in formal

quantitative terms. Thus, budgets help in communicating the plan of the management

throughout the organisation. The aspect holds good for all ASX listed organisations and in

order to meet the purpose of this report, Alpha HPA Limited is taken into consideration. It is

an ASX listed organisation, which is involved in acquisition, exploration and mineral deposits

development in Australia and Indonesia (Collerinacobalt.com.au 2019).

This report would provide a brief overview of the different elements of master

budget. The second section would focus on comparing the top-down and bottom-up

approach to the budget process and accordingly, the most suitable approach for Alpha HPA

Limited would be considered. Finally, the report would shed light on developing the

budgeted income statement for the concerned organisation for 2019 based on the actual

data disclosed in its income statement in 2018 and accordingly, the impact of the changes

owing to the projections made would be analysed.

a. Elements of the master budget:

In the words of Barr and McClellan (2018), master budget is a plan developed to

manage the manufacturing and sales activities of an organisation for fulfilling profit and cash

flow objectives. In order to develop a successful master budget, the different elements of

the master budget need to be prepared in the initial stage accurately. In this way, master

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

budget is deemed to be realistic; however, it is not complacent. The master is generally

represented in either monthly or quarterly format and thus, it covers the full accounting

year of an organisation. More precisely, a master budget acts the tool of central planning

that a management team utilises in directing the activities of an organisation along with

judging the performance of various responsibility centres. It is necessary for the top

management in reviewing various iterations of the master budget along with including

modifications until a budget is arrived at for accomplishing the desired outcomes (Baiman

2014). The master budget consists of a number of elements, which are illustrated in the

form of a figure as follows:

Figure 1: Various components of the master budget

(Source: Noreen, Brewer and Garrison 2014)

The above elements in the figure are discussed briefly as follows:

budget is deemed to be realistic; however, it is not complacent. The master is generally

represented in either monthly or quarterly format and thus, it covers the full accounting

year of an organisation. More precisely, a master budget acts the tool of central planning

that a management team utilises in directing the activities of an organisation along with

judging the performance of various responsibility centres. It is necessary for the top

management in reviewing various iterations of the master budget along with including

modifications until a budget is arrived at for accomplishing the desired outcomes (Baiman

2014). The master budget consists of a number of elements, which are illustrated in the

form of a figure as follows:

Figure 1: Various components of the master budget

(Source: Noreen, Brewer and Garrison 2014)

The above elements in the figure are discussed briefly as follows:

5MANAGERIAL ACCOUNTING

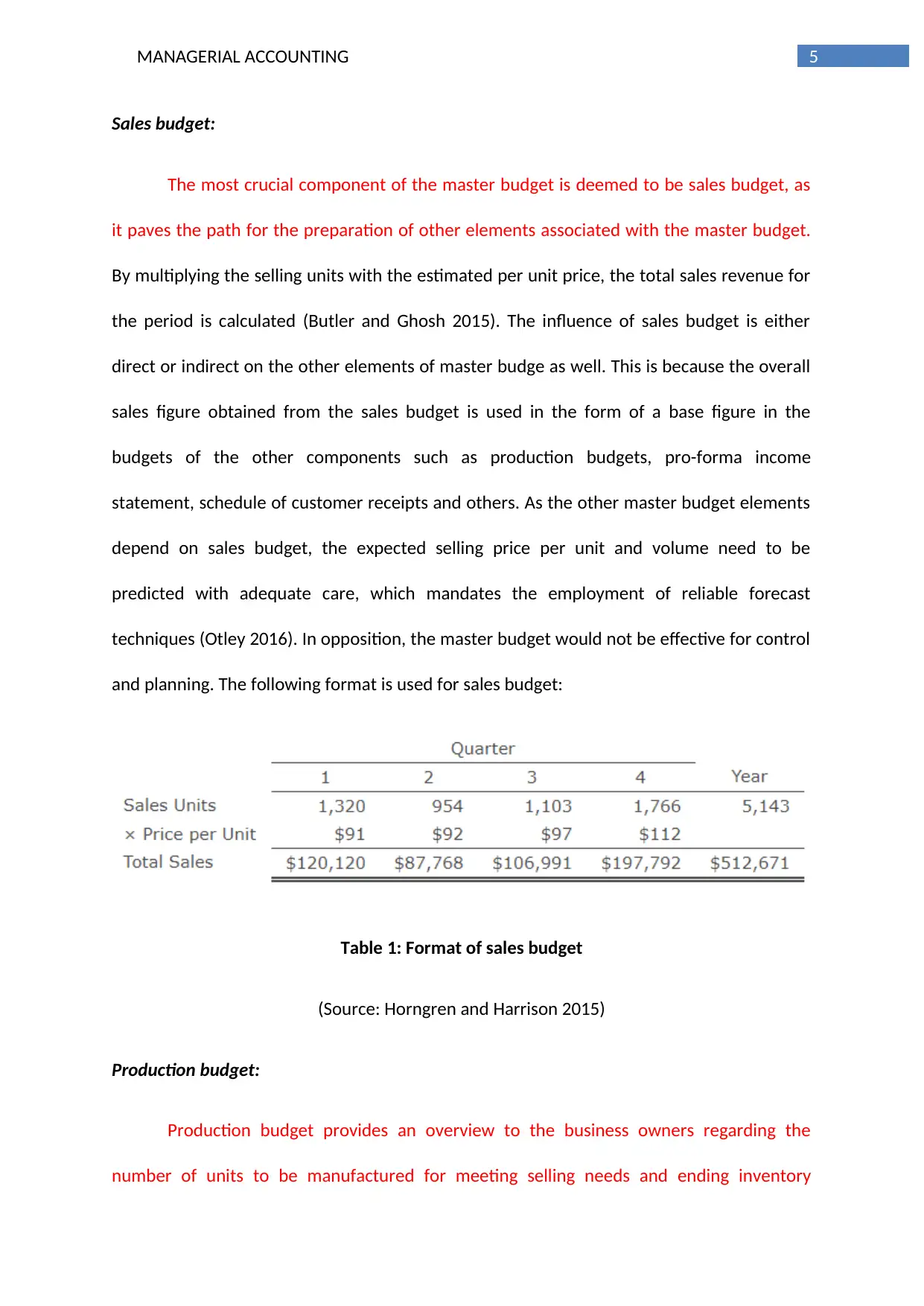

Sales budget:

The most crucial component of the master budget is deemed to be sales budget, as

it paves the path for the preparation of other elements associated with the master budget.

By multiplying the selling units with the estimated per unit price, the total sales revenue for

the period is calculated (Butler and Ghosh 2015). The influence of sales budget is either

direct or indirect on the other elements of master budge as well. This is because the overall

sales figure obtained from the sales budget is used in the form of a base figure in the

budgets of the other components such as production budgets, pro-forma income

statement, schedule of customer receipts and others. As the other master budget elements

depend on sales budget, the expected selling price per unit and volume need to be

predicted with adequate care, which mandates the employment of reliable forecast

techniques (Otley 2016). In opposition, the master budget would not be effective for control

and planning. The following format is used for sales budget:

Table 1: Format of sales budget

(Source: Horngren and Harrison 2015)

Production budget:

Production budget provides an overview to the business owners regarding the

number of units to be manufactured for meeting selling needs and ending inventory

Sales budget:

The most crucial component of the master budget is deemed to be sales budget, as

it paves the path for the preparation of other elements associated with the master budget.

By multiplying the selling units with the estimated per unit price, the total sales revenue for

the period is calculated (Butler and Ghosh 2015). The influence of sales budget is either

direct or indirect on the other elements of master budge as well. This is because the overall

sales figure obtained from the sales budget is used in the form of a base figure in the

budgets of the other components such as production budgets, pro-forma income

statement, schedule of customer receipts and others. As the other master budget elements

depend on sales budget, the expected selling price per unit and volume need to be

predicted with adequate care, which mandates the employment of reliable forecast

techniques (Otley 2016). In opposition, the master budget would not be effective for control

and planning. The following format is used for sales budget:

Table 1: Format of sales budget

(Source: Horngren and Harrison 2015)

Production budget:

Production budget provides an overview to the business owners regarding the

number of units to be manufactured for meeting selling needs and ending inventory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

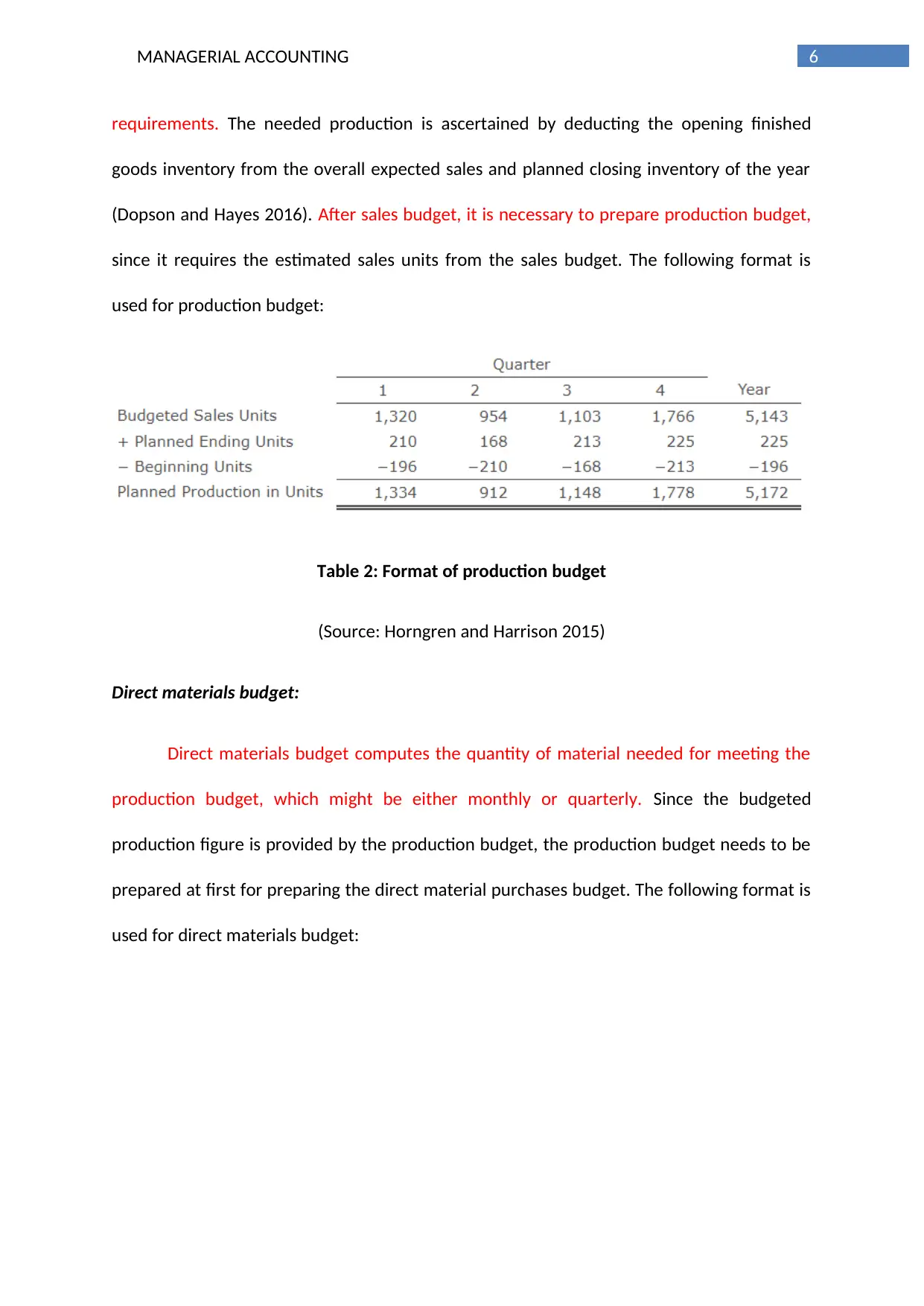

requirements. The needed production is ascertained by deducting the opening finished

goods inventory from the overall expected sales and planned closing inventory of the year

(Dopson and Hayes 2016). After sales budget, it is necessary to prepare production budget,

since it requires the estimated sales units from the sales budget. The following format is

used for production budget:

Table 2: Format of production budget

(Source: Horngren and Harrison 2015)

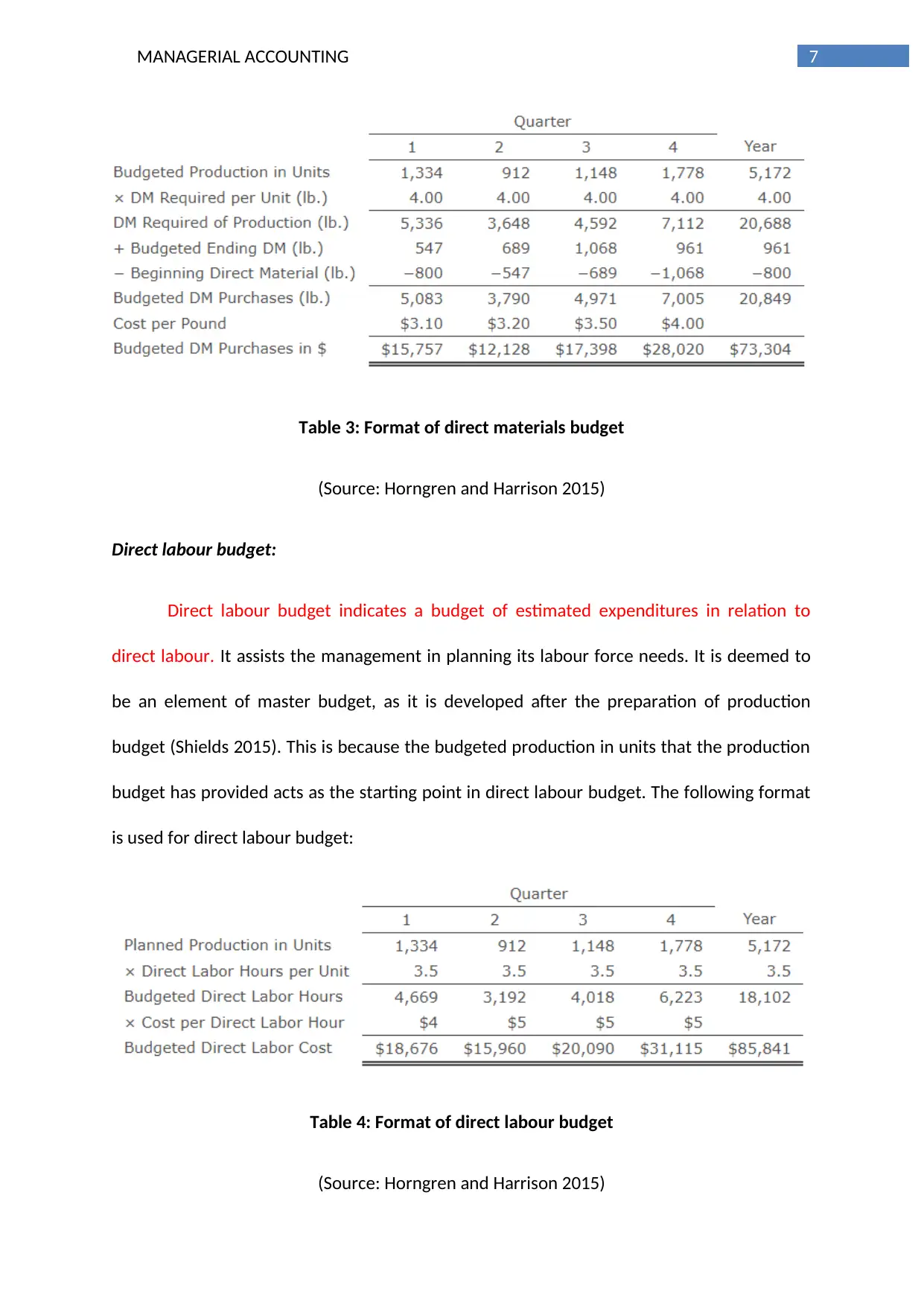

Direct materials budget:

Direct materials budget computes the quantity of material needed for meeting the

production budget, which might be either monthly or quarterly. Since the budgeted

production figure is provided by the production budget, the production budget needs to be

prepared at first for preparing the direct material purchases budget. The following format is

used for direct materials budget:

requirements. The needed production is ascertained by deducting the opening finished

goods inventory from the overall expected sales and planned closing inventory of the year

(Dopson and Hayes 2016). After sales budget, it is necessary to prepare production budget,

since it requires the estimated sales units from the sales budget. The following format is

used for production budget:

Table 2: Format of production budget

(Source: Horngren and Harrison 2015)

Direct materials budget:

Direct materials budget computes the quantity of material needed for meeting the

production budget, which might be either monthly or quarterly. Since the budgeted

production figure is provided by the production budget, the production budget needs to be

prepared at first for preparing the direct material purchases budget. The following format is

used for direct materials budget:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

Table 3: Format of direct materials budget

(Source: Horngren and Harrison 2015)

Direct labour budget:

Direct labour budget indicates a budget of estimated expenditures in relation to

direct labour. It assists the management in planning its labour force needs. It is deemed to

be an element of master budget, as it is developed after the preparation of production

budget (Shields 2015). This is because the budgeted production in units that the production

budget has provided acts as the starting point in direct labour budget. The following format

is used for direct labour budget:

Table 4: Format of direct labour budget

(Source: Horngren and Harrison 2015)

Table 3: Format of direct materials budget

(Source: Horngren and Harrison 2015)

Direct labour budget:

Direct labour budget indicates a budget of estimated expenditures in relation to

direct labour. It assists the management in planning its labour force needs. It is deemed to

be an element of master budget, as it is developed after the preparation of production

budget (Shields 2015). This is because the budgeted production in units that the production

budget has provided acts as the starting point in direct labour budget. The following format

is used for direct labour budget:

Table 4: Format of direct labour budget

(Source: Horngren and Harrison 2015)

8MANAGERIAL ACCOUNTING

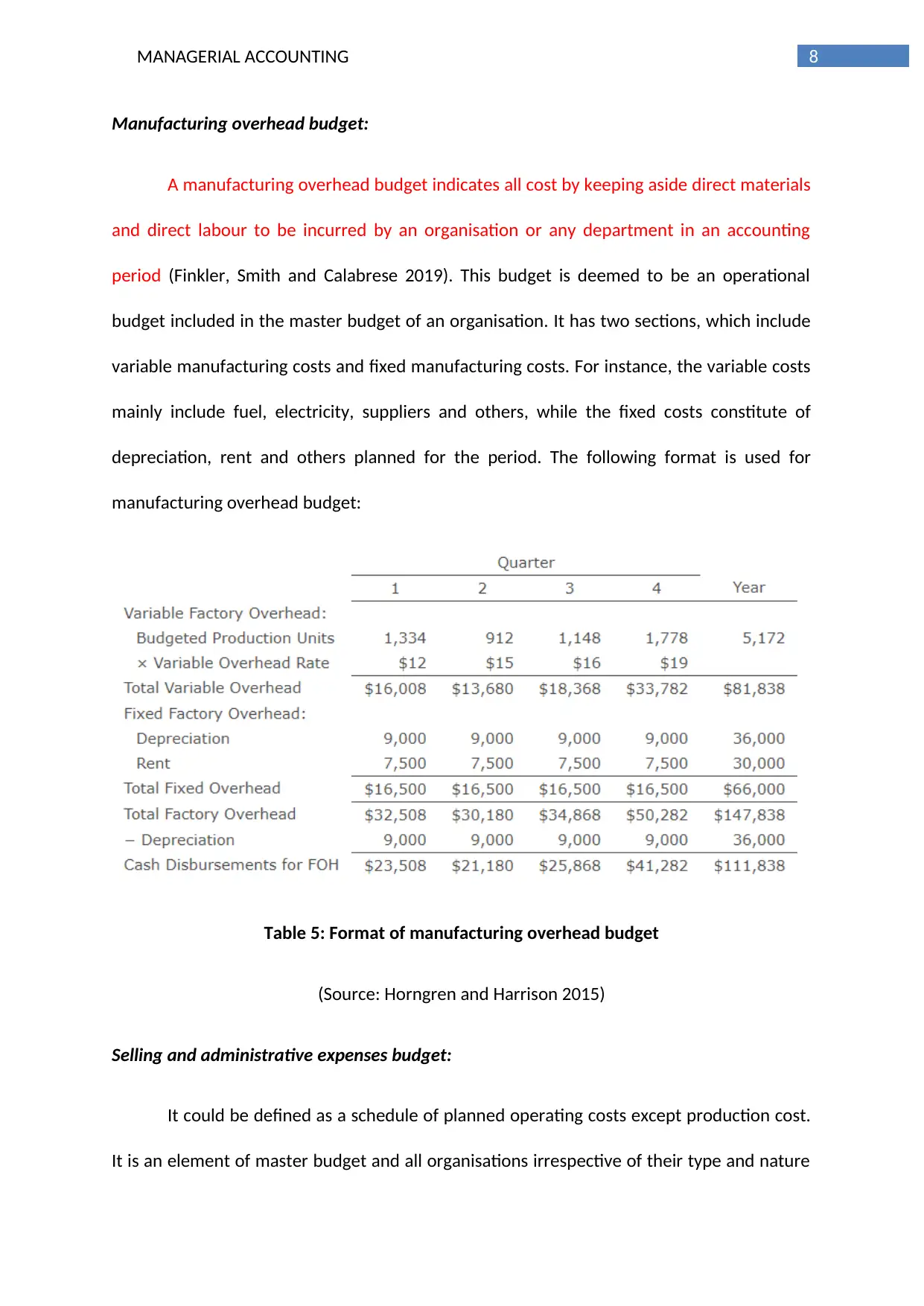

Manufacturing overhead budget:

A manufacturing overhead budget indicates all cost by keeping aside direct materials

and direct labour to be incurred by an organisation or any department in an accounting

period (Finkler, Smith and Calabrese 2019). This budget is deemed to be an operational

budget included in the master budget of an organisation. It has two sections, which include

variable manufacturing costs and fixed manufacturing costs. For instance, the variable costs

mainly include fuel, electricity, suppliers and others, while the fixed costs constitute of

depreciation, rent and others planned for the period. The following format is used for

manufacturing overhead budget:

Table 5: Format of manufacturing overhead budget

(Source: Horngren and Harrison 2015)

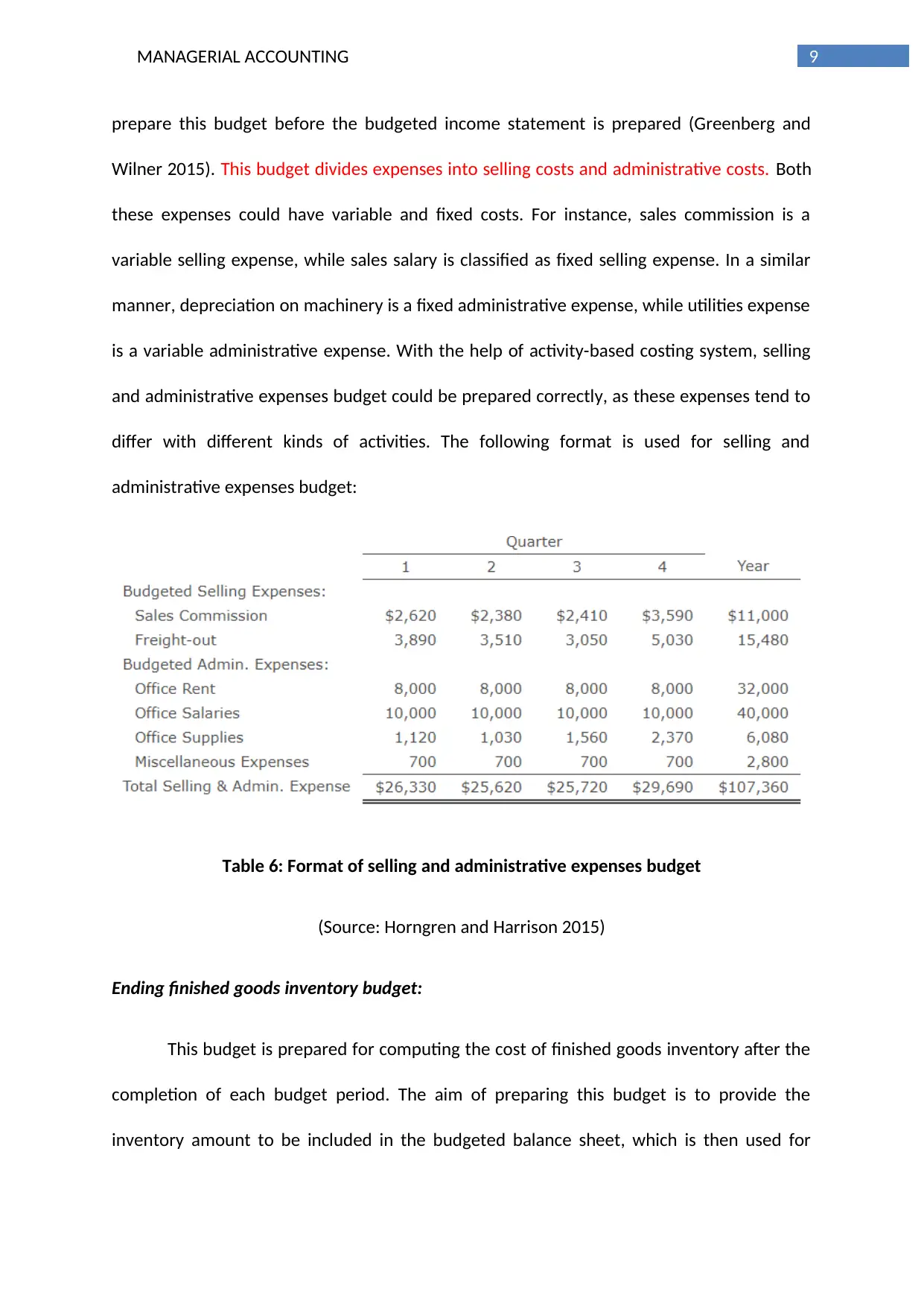

Selling and administrative expenses budget:

It could be defined as a schedule of planned operating costs except production cost.

It is an element of master budget and all organisations irrespective of their type and nature

Manufacturing overhead budget:

A manufacturing overhead budget indicates all cost by keeping aside direct materials

and direct labour to be incurred by an organisation or any department in an accounting

period (Finkler, Smith and Calabrese 2019). This budget is deemed to be an operational

budget included in the master budget of an organisation. It has two sections, which include

variable manufacturing costs and fixed manufacturing costs. For instance, the variable costs

mainly include fuel, electricity, suppliers and others, while the fixed costs constitute of

depreciation, rent and others planned for the period. The following format is used for

manufacturing overhead budget:

Table 5: Format of manufacturing overhead budget

(Source: Horngren and Harrison 2015)

Selling and administrative expenses budget:

It could be defined as a schedule of planned operating costs except production cost.

It is an element of master budget and all organisations irrespective of their type and nature

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

prepare this budget before the budgeted income statement is prepared (Greenberg and

Wilner 2015). This budget divides expenses into selling costs and administrative costs. Both

these expenses could have variable and fixed costs. For instance, sales commission is a

variable selling expense, while sales salary is classified as fixed selling expense. In a similar

manner, depreciation on machinery is a fixed administrative expense, while utilities expense

is a variable administrative expense. With the help of activity-based costing system, selling

and administrative expenses budget could be prepared correctly, as these expenses tend to

differ with different kinds of activities. The following format is used for selling and

administrative expenses budget:

Table 6: Format of selling and administrative expenses budget

(Source: Horngren and Harrison 2015)

Ending finished goods inventory budget:

This budget is prepared for computing the cost of finished goods inventory after the

completion of each budget period. The aim of preparing this budget is to provide the

inventory amount to be included in the budgeted balance sheet, which is then used for

prepare this budget before the budgeted income statement is prepared (Greenberg and

Wilner 2015). This budget divides expenses into selling costs and administrative costs. Both

these expenses could have variable and fixed costs. For instance, sales commission is a

variable selling expense, while sales salary is classified as fixed selling expense. In a similar

manner, depreciation on machinery is a fixed administrative expense, while utilities expense

is a variable administrative expense. With the help of activity-based costing system, selling

and administrative expenses budget could be prepared correctly, as these expenses tend to

differ with different kinds of activities. The following format is used for selling and

administrative expenses budget:

Table 6: Format of selling and administrative expenses budget

(Source: Horngren and Harrison 2015)

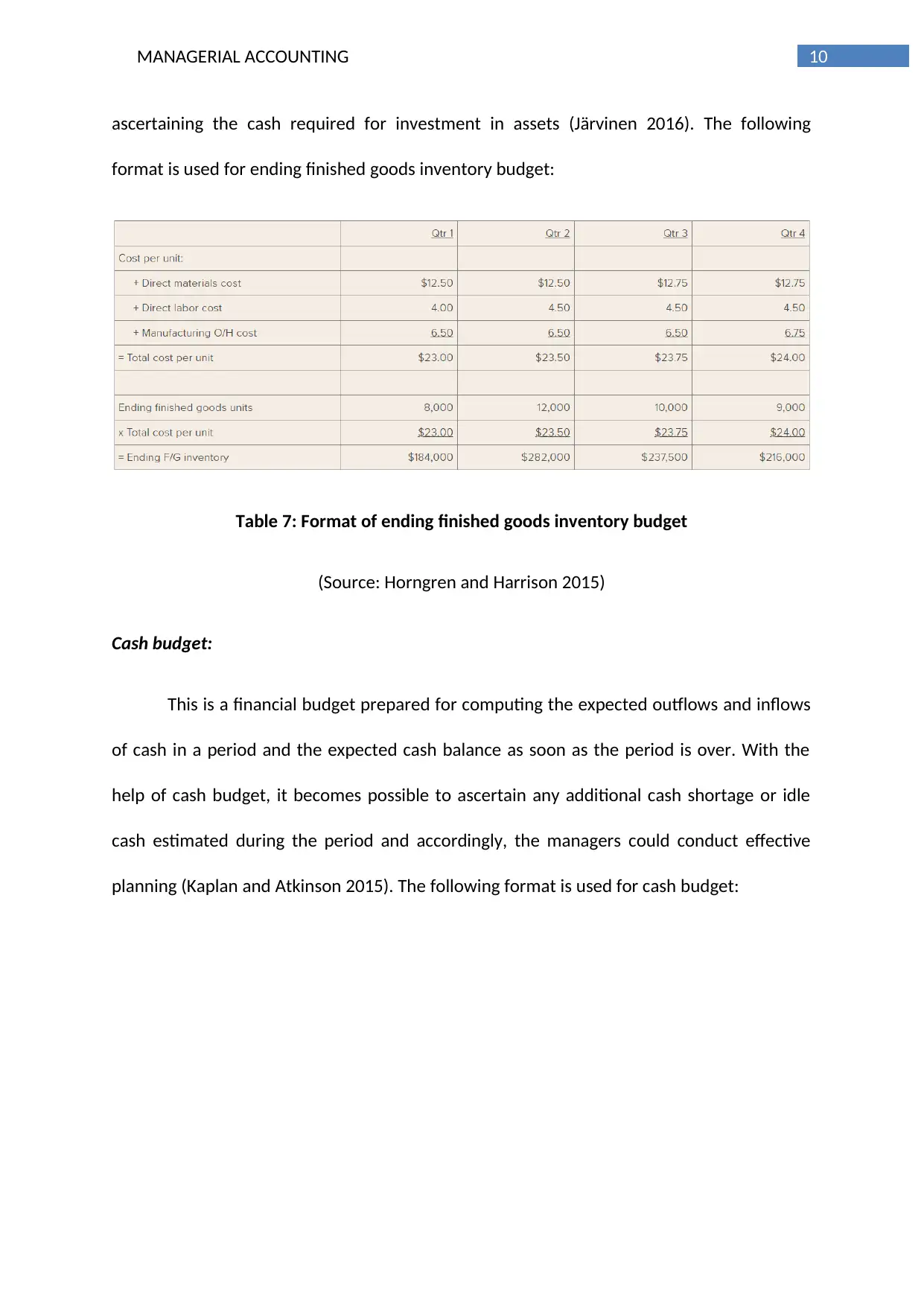

Ending finished goods inventory budget:

This budget is prepared for computing the cost of finished goods inventory after the

completion of each budget period. The aim of preparing this budget is to provide the

inventory amount to be included in the budgeted balance sheet, which is then used for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

ascertaining the cash required for investment in assets (Järvinen 2016). The following

format is used for ending finished goods inventory budget:

Table 7: Format of ending finished goods inventory budget

(Source: Horngren and Harrison 2015)

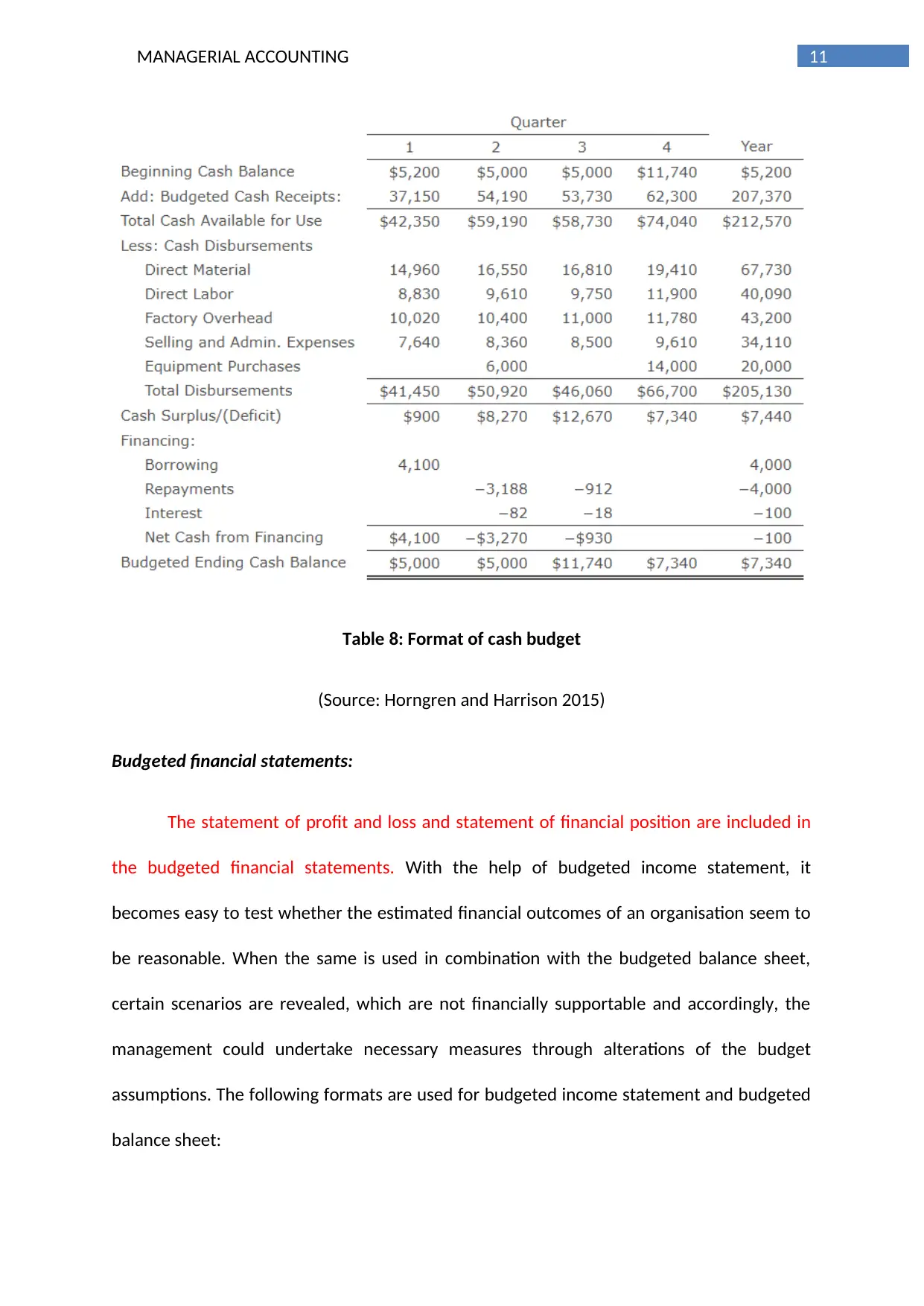

Cash budget:

This is a financial budget prepared for computing the expected outflows and inflows

of cash in a period and the expected cash balance as soon as the period is over. With the

help of cash budget, it becomes possible to ascertain any additional cash shortage or idle

cash estimated during the period and accordingly, the managers could conduct effective

planning (Kaplan and Atkinson 2015). The following format is used for cash budget:

ascertaining the cash required for investment in assets (Järvinen 2016). The following

format is used for ending finished goods inventory budget:

Table 7: Format of ending finished goods inventory budget

(Source: Horngren and Harrison 2015)

Cash budget:

This is a financial budget prepared for computing the expected outflows and inflows

of cash in a period and the expected cash balance as soon as the period is over. With the

help of cash budget, it becomes possible to ascertain any additional cash shortage or idle

cash estimated during the period and accordingly, the managers could conduct effective

planning (Kaplan and Atkinson 2015). The following format is used for cash budget:

11MANAGERIAL ACCOUNTING

Table 8: Format of cash budget

(Source: Horngren and Harrison 2015)

Budgeted financial statements:

The statement of profit and loss and statement of financial position are included in

the budgeted financial statements. With the help of budgeted income statement, it

becomes easy to test whether the estimated financial outcomes of an organisation seem to

be reasonable. When the same is used in combination with the budgeted balance sheet,

certain scenarios are revealed, which are not financially supportable and accordingly, the

management could undertake necessary measures through alterations of the budget

assumptions. The following formats are used for budgeted income statement and budgeted

balance sheet:

Table 8: Format of cash budget

(Source: Horngren and Harrison 2015)

Budgeted financial statements:

The statement of profit and loss and statement of financial position are included in

the budgeted financial statements. With the help of budgeted income statement, it

becomes easy to test whether the estimated financial outcomes of an organisation seem to

be reasonable. When the same is used in combination with the budgeted balance sheet,

certain scenarios are revealed, which are not financially supportable and accordingly, the

management could undertake necessary measures through alterations of the budget

assumptions. The following formats are used for budgeted income statement and budgeted

balance sheet:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.