Economic Analysis of Cash Rate and Financial Stability

VerifiedAdded on 2021/04/21

|18

|2930

|422

AI Summary

This assignment requires an analysis of the cash rate and its relationship with economic factors such as wage rates and inflation. It involves a discussion of the implications of the cash rate on employment growth and household spending, as well as its potential impact on retail sales and financial stability. The assignment aims to provide insights into the role of cash rate in maintaining economic stability and promoting sustainable growth.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MASTER OF PROFESSIONAL ACCOUNTING

Master of professional accounting

Name of the Student

Name of the University

Author Note

Master of professional accounting

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MASTER OF PROFESSIONAL ACCOUNTING

Table of Contents

Answer to question 1:.................................................................................................................3

Requirement a).......................................................................................................................3

Requirement b).......................................................................................................................3

Answer to question 2:.................................................................................................................5

Requirement a).......................................................................................................................5

Requirement b).......................................................................................................................5

Requirement c).......................................................................................................................6

Answer to question 3:.................................................................................................................7

Requirement a).......................................................................................................................7

Requirement b).......................................................................................................................7

Requirement c).......................................................................................................................8

Requirement d).......................................................................................................................8

Requirement e).......................................................................................................................9

Answer to question 4:.................................................................................................................9

Requirement a).......................................................................................................................9

Requirement b).....................................................................................................................10

Requirement c).....................................................................................................................10

Requirement d).....................................................................................................................10

Requirement e).....................................................................................................................11

Answer to question 5:...............................................................................................................11

Introduction:.........................................................................................................................11

MASTER OF PROFESSIONAL ACCOUNTING

Table of Contents

Answer to question 1:.................................................................................................................3

Requirement a).......................................................................................................................3

Requirement b).......................................................................................................................3

Answer to question 2:.................................................................................................................5

Requirement a).......................................................................................................................5

Requirement b).......................................................................................................................5

Requirement c).......................................................................................................................6

Answer to question 3:.................................................................................................................7

Requirement a).......................................................................................................................7

Requirement b).......................................................................................................................7

Requirement c).......................................................................................................................8

Requirement d).......................................................................................................................8

Requirement e).......................................................................................................................9

Answer to question 4:.................................................................................................................9

Requirement a).......................................................................................................................9

Requirement b).....................................................................................................................10

Requirement c).....................................................................................................................10

Requirement d).....................................................................................................................10

Requirement e).....................................................................................................................11

Answer to question 5:...............................................................................................................11

Introduction:.........................................................................................................................11

2

MASTER OF PROFESSIONAL ACCOUNTING

Discussion:...........................................................................................................................12

Conclusion:..........................................................................................................................14

References list:.........................................................................................................................15

MASTER OF PROFESSIONAL ACCOUNTING

Discussion:...........................................................................................................................12

Conclusion:..........................................................................................................................14

References list:.........................................................................................................................15

3

MASTER OF PROFESSIONAL ACCOUNTING

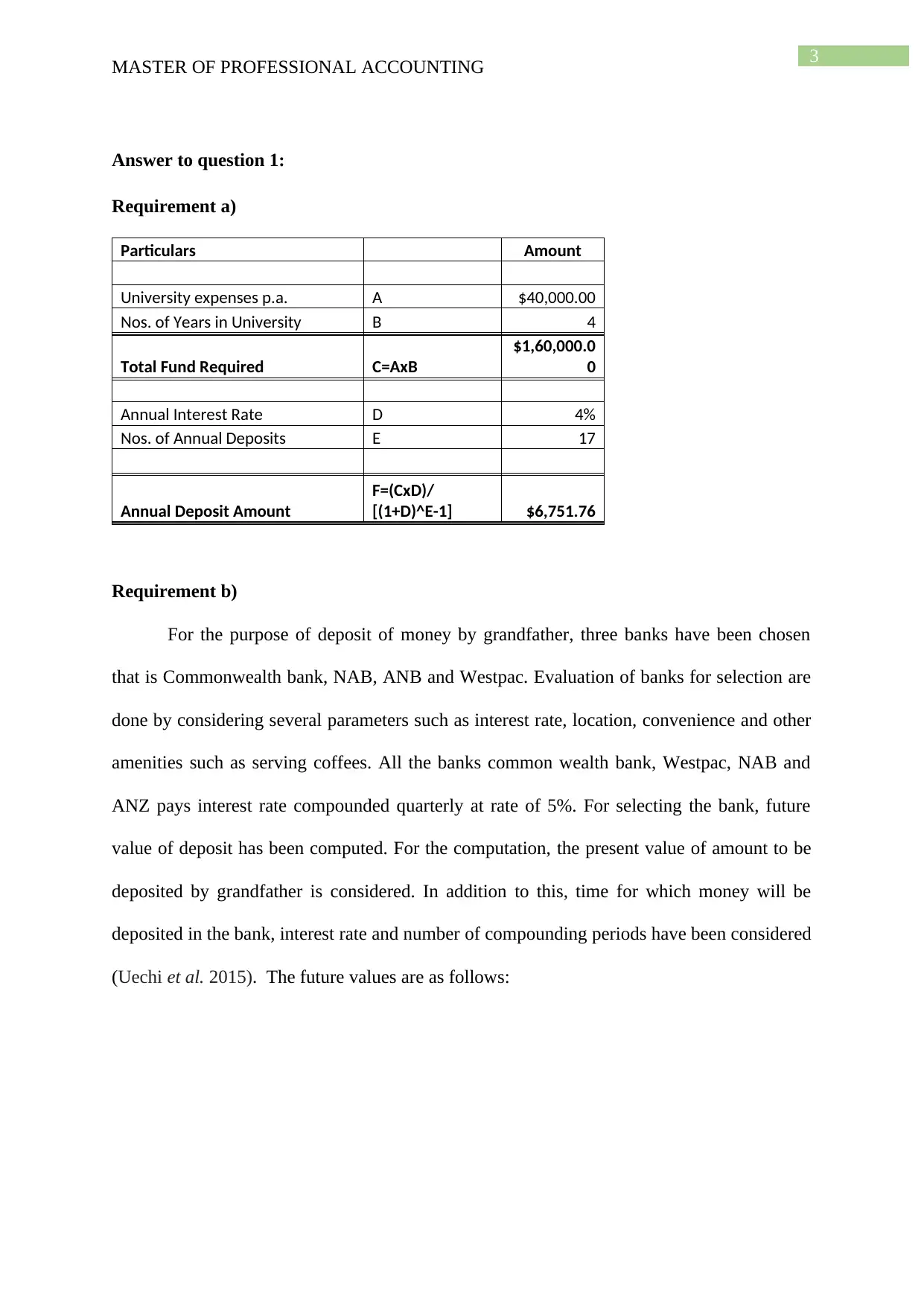

Answer to question 1:

Requirement a)

Particulars Amount

University expenses p.a. A $40,000.00

Nos. of Years in University B 4

Total Fund Required C=AxB

$1,60,000.0

0

Annual Interest Rate D 4%

Nos. of Annual Deposits E 17

Annual Deposit Amount

F=(CxD)/

[(1+D)^E-1] $6,751.76

Requirement b)

For the purpose of deposit of money by grandfather, three banks have been chosen

that is Commonwealth bank, NAB, ANB and Westpac. Evaluation of banks for selection are

done by considering several parameters such as interest rate, location, convenience and other

amenities such as serving coffees. All the banks common wealth bank, Westpac, NAB and

ANZ pays interest rate compounded quarterly at rate of 5%. For selecting the bank, future

value of deposit has been computed. For the computation, the present value of amount to be

deposited by grandfather is considered. In addition to this, time for which money will be

deposited in the bank, interest rate and number of compounding periods have been considered

(Uechi et al. 2015). The future values are as follows:

MASTER OF PROFESSIONAL ACCOUNTING

Answer to question 1:

Requirement a)

Particulars Amount

University expenses p.a. A $40,000.00

Nos. of Years in University B 4

Total Fund Required C=AxB

$1,60,000.0

0

Annual Interest Rate D 4%

Nos. of Annual Deposits E 17

Annual Deposit Amount

F=(CxD)/

[(1+D)^E-1] $6,751.76

Requirement b)

For the purpose of deposit of money by grandfather, three banks have been chosen

that is Commonwealth bank, NAB, ANB and Westpac. Evaluation of banks for selection are

done by considering several parameters such as interest rate, location, convenience and other

amenities such as serving coffees. All the banks common wealth bank, Westpac, NAB and

ANZ pays interest rate compounded quarterly at rate of 5%. For selecting the bank, future

value of deposit has been computed. For the computation, the present value of amount to be

deposited by grandfather is considered. In addition to this, time for which money will be

deposited in the bank, interest rate and number of compounding periods have been considered

(Uechi et al. 2015). The future values are as follows:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MASTER OF PROFESSIONAL ACCOUNTING

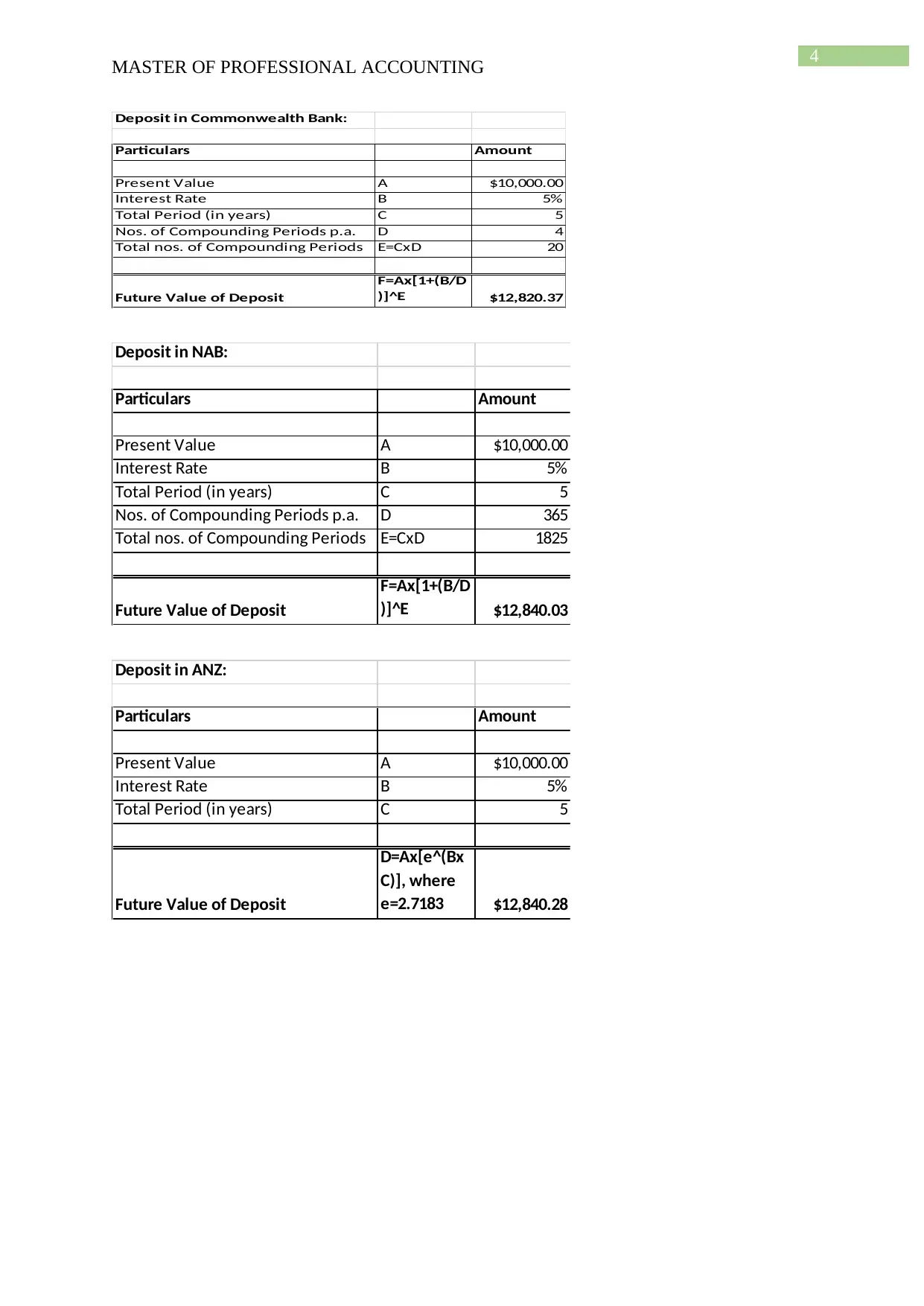

Deposit in Commonwealth Bank:

Particulars Amount

Present Value A $10,000.00

Interest Rate B 5%

Total Period (in years) C 5

Nos. of Compounding Periods p.a. D 4

Total nos. of Compounding Periods E=CxD 20

Future Value of Deposit

F=Ax[1+(B/D

)]^E $12,820.37

Deposit in NAB:

Particulars Amount

Present Value A $10,000.00

Interest Rate B 5%

Total Period (in years) C 5

Nos. of Compounding Periods p.a. D 365

Total nos. of Compounding Periods E=CxD 1825

Future Value of Deposit

F=Ax[1+(B/D

)]^E $12,840.03

Deposit in ANZ:

Particulars Amount

Present Value A $10,000.00

Interest Rate B 5%

Total Period (in years) C 5

Future Value of Deposit

D=Ax[e^(Bx

C)], where

e=2.7183 $12,840.28

MASTER OF PROFESSIONAL ACCOUNTING

Deposit in Commonwealth Bank:

Particulars Amount

Present Value A $10,000.00

Interest Rate B 5%

Total Period (in years) C 5

Nos. of Compounding Periods p.a. D 4

Total nos. of Compounding Periods E=CxD 20

Future Value of Deposit

F=Ax[1+(B/D

)]^E $12,820.37

Deposit in NAB:

Particulars Amount

Present Value A $10,000.00

Interest Rate B 5%

Total Period (in years) C 5

Nos. of Compounding Periods p.a. D 365

Total nos. of Compounding Periods E=CxD 1825

Future Value of Deposit

F=Ax[1+(B/D

)]^E $12,840.03

Deposit in ANZ:

Particulars Amount

Present Value A $10,000.00

Interest Rate B 5%

Total Period (in years) C 5

Future Value of Deposit

D=Ax[e^(Bx

C)], where

e=2.7183 $12,840.28

5

MASTER OF PROFESSIONAL ACCOUNTING

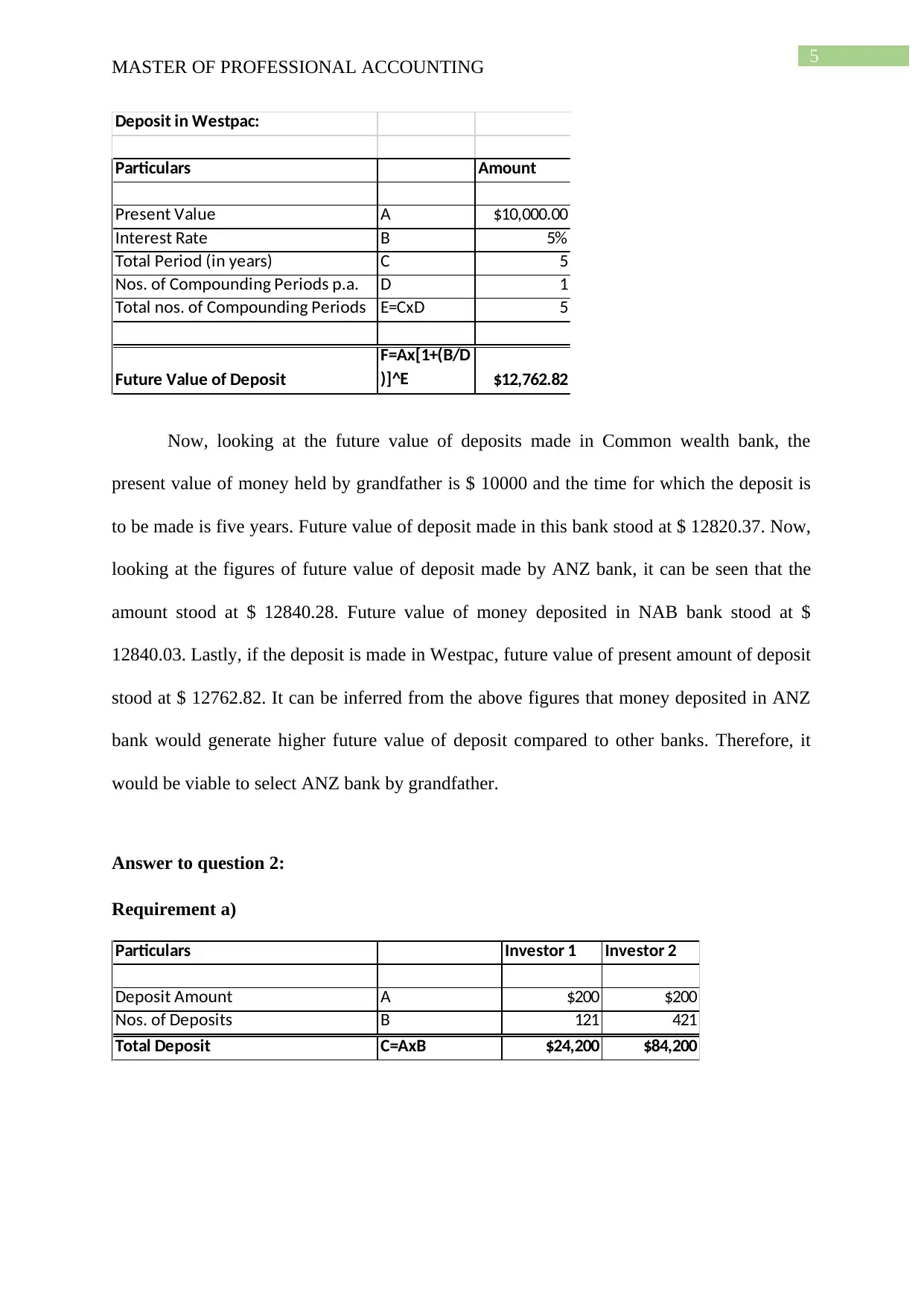

Deposit in Westpac:

Particulars Amount

Present Value A $10,000.00

Interest Rate B 5%

Total Period (in years) C 5

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 5

Future Value of Deposit

F=Ax[1+(B/D

)]^E $12,762.82

Now, looking at the future value of deposits made in Common wealth bank, the

present value of money held by grandfather is $ 10000 and the time for which the deposit is

to be made is five years. Future value of deposit made in this bank stood at $ 12820.37. Now,

looking at the figures of future value of deposit made by ANZ bank, it can be seen that the

amount stood at $ 12840.28. Future value of money deposited in NAB bank stood at $

12840.03. Lastly, if the deposit is made in Westpac, future value of present amount of deposit

stood at $ 12762.82. It can be inferred from the above figures that money deposited in ANZ

bank would generate higher future value of deposit compared to other banks. Therefore, it

would be viable to select ANZ bank by grandfather.

Answer to question 2:

Requirement a)

Particulars Investor 1 Investor 2

Deposit Amount A $200 $200

Nos. of Deposits B 121 421

Total Deposit C=AxB $24,200 $84,200

MASTER OF PROFESSIONAL ACCOUNTING

Deposit in Westpac:

Particulars Amount

Present Value A $10,000.00

Interest Rate B 5%

Total Period (in years) C 5

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 5

Future Value of Deposit

F=Ax[1+(B/D

)]^E $12,762.82

Now, looking at the future value of deposits made in Common wealth bank, the

present value of money held by grandfather is $ 10000 and the time for which the deposit is

to be made is five years. Future value of deposit made in this bank stood at $ 12820.37. Now,

looking at the figures of future value of deposit made by ANZ bank, it can be seen that the

amount stood at $ 12840.28. Future value of money deposited in NAB bank stood at $

12840.03. Lastly, if the deposit is made in Westpac, future value of present amount of deposit

stood at $ 12762.82. It can be inferred from the above figures that money deposited in ANZ

bank would generate higher future value of deposit compared to other banks. Therefore, it

would be viable to select ANZ bank by grandfather.

Answer to question 2:

Requirement a)

Particulars Investor 1 Investor 2

Deposit Amount A $200 $200

Nos. of Deposits B 121 421

Total Deposit C=AxB $24,200 $84,200

6

MASTER OF PROFESSIONAL ACCOUNTING

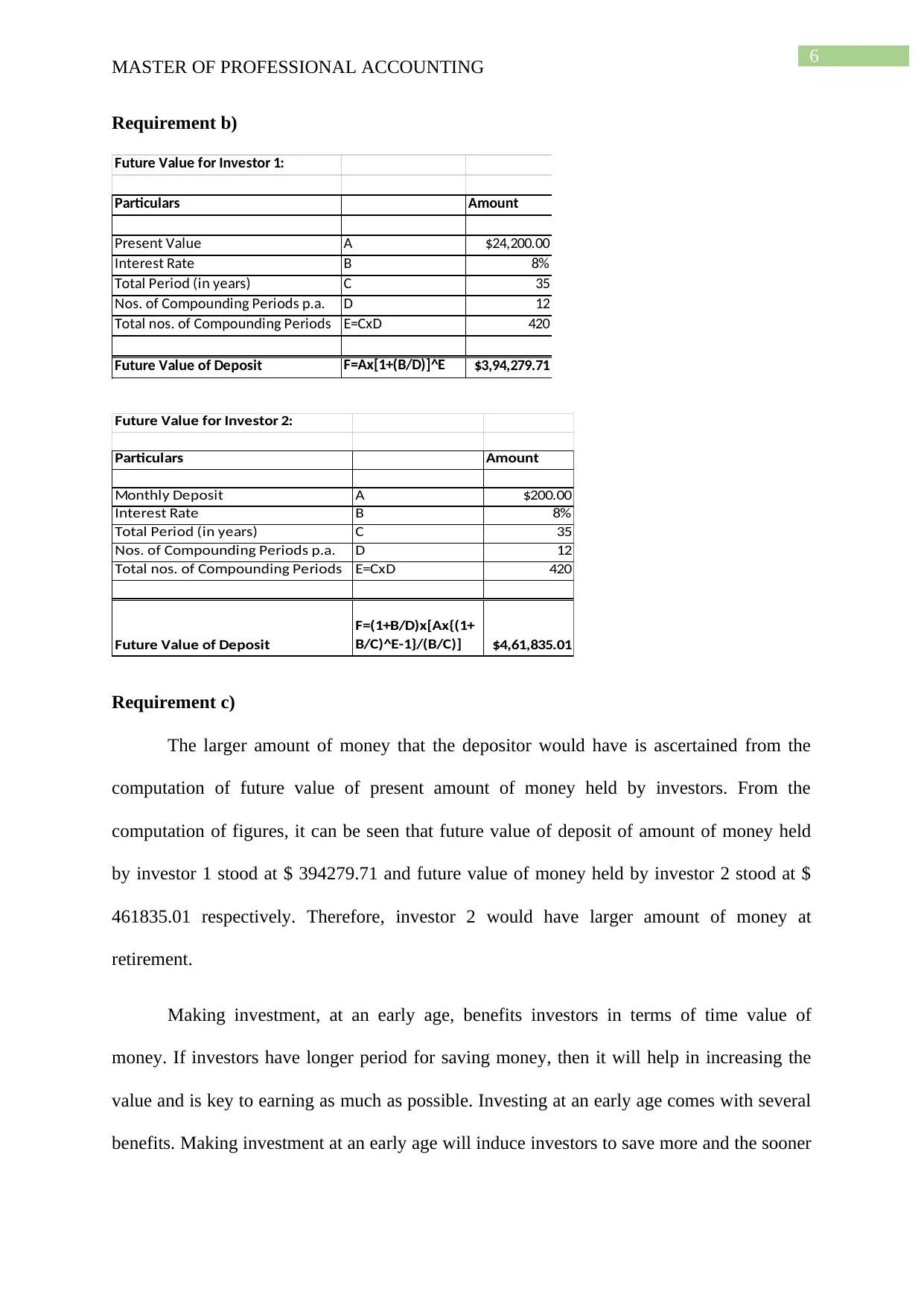

Requirement b)

Future Value for Investor 1:

Particulars Amount

Present Value A $24,200.00

Interest Rate B 8%

Total Period (in years) C 35

Nos. of Compounding Periods p.a. D 12

Total nos. of Compounding Periods E=CxD 420

Future Value of Deposit F=Ax[1+(B/D)]^E $3,94,279.71

Future Value for Investor 2:

Particulars Amount

Monthly Deposit A $200.00

Interest Rate B 8%

Total Period (in years) C 35

Nos. of Compounding Periods p.a. D 12

Total nos. of Compounding Periods E=CxD 420

Future Value of Deposit

F=(1+B/D)x[Ax{(1+

B/C)^E-1}/(B/C)] $4,61,835.01

Requirement c)

The larger amount of money that the depositor would have is ascertained from the

computation of future value of present amount of money held by investors. From the

computation of figures, it can be seen that future value of deposit of amount of money held

by investor 1 stood at $ 394279.71 and future value of money held by investor 2 stood at $

461835.01 respectively. Therefore, investor 2 would have larger amount of money at

retirement.

Making investment, at an early age, benefits investors in terms of time value of

money. If investors have longer period for saving money, then it will help in increasing the

value and is key to earning as much as possible. Investing at an early age comes with several

benefits. Making investment at an early age will induce investors to save more and the sooner

MASTER OF PROFESSIONAL ACCOUNTING

Requirement b)

Future Value for Investor 1:

Particulars Amount

Present Value A $24,200.00

Interest Rate B 8%

Total Period (in years) C 35

Nos. of Compounding Periods p.a. D 12

Total nos. of Compounding Periods E=CxD 420

Future Value of Deposit F=Ax[1+(B/D)]^E $3,94,279.71

Future Value for Investor 2:

Particulars Amount

Monthly Deposit A $200.00

Interest Rate B 8%

Total Period (in years) C 35

Nos. of Compounding Periods p.a. D 12

Total nos. of Compounding Periods E=CxD 420

Future Value of Deposit

F=(1+B/D)x[Ax{(1+

B/C)^E-1}/(B/C)] $4,61,835.01

Requirement c)

The larger amount of money that the depositor would have is ascertained from the

computation of future value of present amount of money held by investors. From the

computation of figures, it can be seen that future value of deposit of amount of money held

by investor 1 stood at $ 394279.71 and future value of money held by investor 2 stood at $

461835.01 respectively. Therefore, investor 2 would have larger amount of money at

retirement.

Making investment, at an early age, benefits investors in terms of time value of

money. If investors have longer period for saving money, then it will help in increasing the

value and is key to earning as much as possible. Investing at an early age comes with several

benefits. Making investment at an early age will induce investors to save more and the sooner

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MASTER OF PROFESSIONAL ACCOUNTING

will be the interest received and dividend amount that will be added to the principal amount

of investment. A habit of saving is developed and enables investors to reap the benefits of the

magical concepts of compound interest (Hanna et al. 2016). Investors will be capable of

making smart investment decision at an early age. They would be capable of taking higher

risks and higher risks are associated with higher rate of return. For covering regular

household, expenses and other medical expenses, there should be enough retirement corpus.

Investors are able to inculcate financial decisions if they have the habit of making investment

at an earlier age and keeping their expenses in check by prioritizing investment over

purchase. All the lessons that investors learn from making earlier investment will reward

them in the long-run. Imposing restraint and having financial discipline articulated in earlier

age will lead to a better financial position (Atkinson et al. 2015).

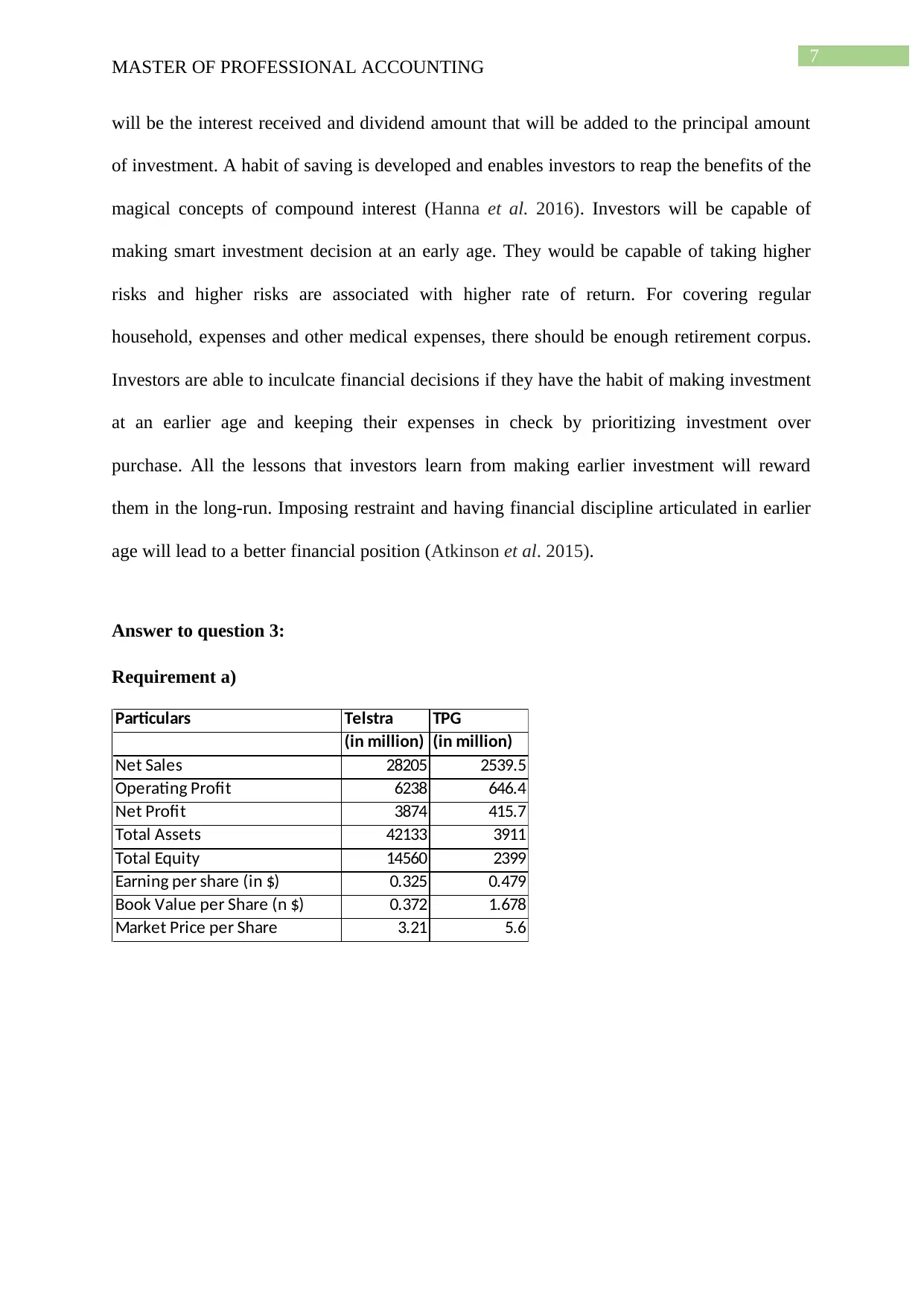

Answer to question 3:

Requirement a)

Particulars Telstra TPG

(in million) (in million)

Net Sales 28205 2539.5

Operating Profit 6238 646.4

Net Profit 3874 415.7

Total Assets 42133 3911

Total Equity 14560 2399

Earning per share (in $) 0.325 0.479

Book Value per Share (n $) 0.372 1.678

Market Price per Share 3.21 5.6

MASTER OF PROFESSIONAL ACCOUNTING

will be the interest received and dividend amount that will be added to the principal amount

of investment. A habit of saving is developed and enables investors to reap the benefits of the

magical concepts of compound interest (Hanna et al. 2016). Investors will be capable of

making smart investment decision at an early age. They would be capable of taking higher

risks and higher risks are associated with higher rate of return. For covering regular

household, expenses and other medical expenses, there should be enough retirement corpus.

Investors are able to inculcate financial decisions if they have the habit of making investment

at an earlier age and keeping their expenses in check by prioritizing investment over

purchase. All the lessons that investors learn from making earlier investment will reward

them in the long-run. Imposing restraint and having financial discipline articulated in earlier

age will lead to a better financial position (Atkinson et al. 2015).

Answer to question 3:

Requirement a)

Particulars Telstra TPG

(in million) (in million)

Net Sales 28205 2539.5

Operating Profit 6238 646.4

Net Profit 3874 415.7

Total Assets 42133 3911

Total Equity 14560 2399

Earning per share (in $) 0.325 0.479

Book Value per Share (n $) 0.372 1.678

Market Price per Share 3.21 5.6

8

MASTER OF PROFESSIONAL ACCOUNTING

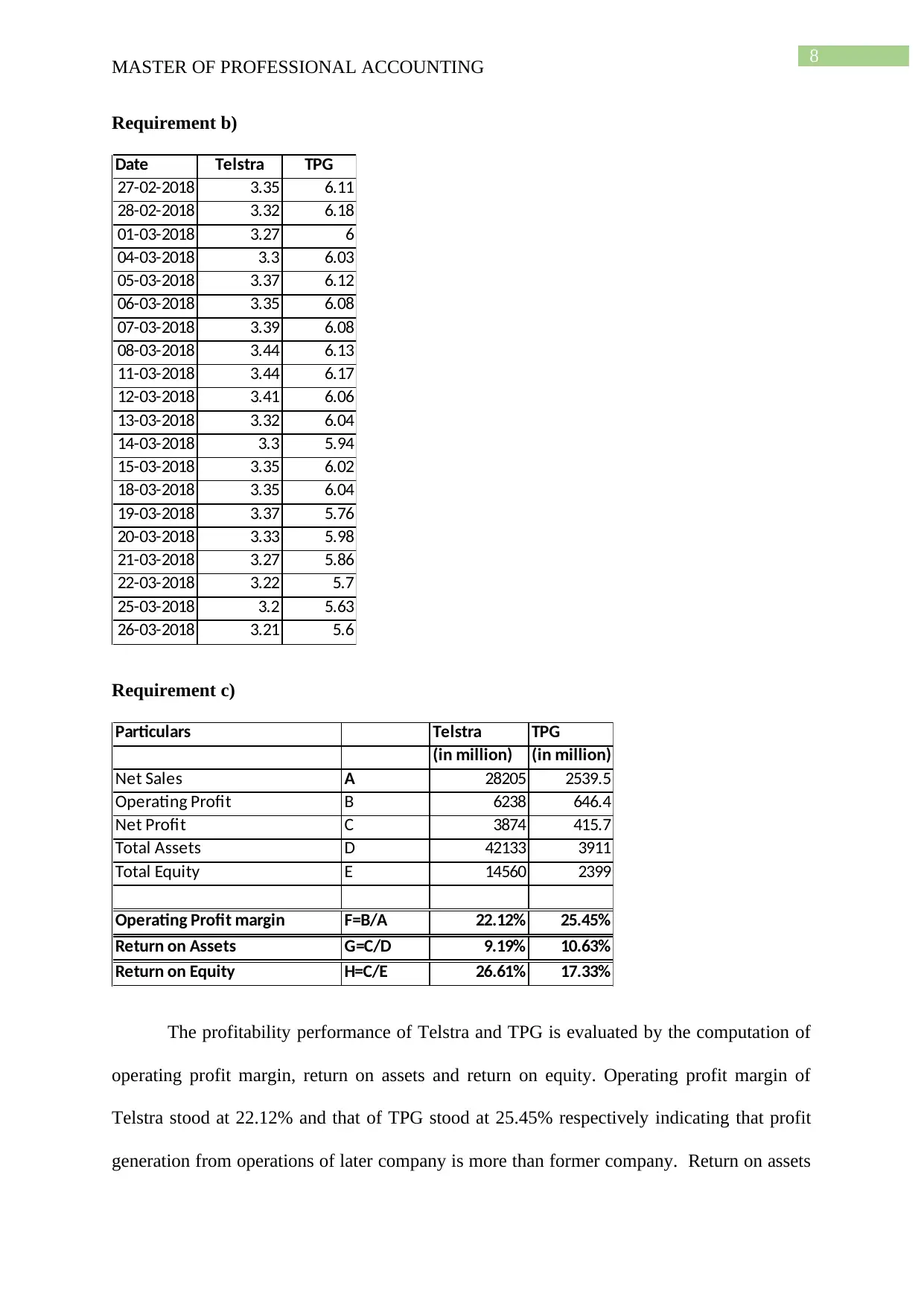

Requirement b)

Date Telstra TPG

27-02-2018 3.35 6.11

28-02-2018 3.32 6.18

01-03-2018 3.27 6

04-03-2018 3.3 6.03

05-03-2018 3.37 6.12

06-03-2018 3.35 6.08

07-03-2018 3.39 6.08

08-03-2018 3.44 6.13

11-03-2018 3.44 6.17

12-03-2018 3.41 6.06

13-03-2018 3.32 6.04

14-03-2018 3.3 5.94

15-03-2018 3.35 6.02

18-03-2018 3.35 6.04

19-03-2018 3.37 5.76

20-03-2018 3.33 5.98

21-03-2018 3.27 5.86

22-03-2018 3.22 5.7

25-03-2018 3.2 5.63

26-03-2018 3.21 5.6

Requirement c)

Particulars Telstra TPG

(in million) (in million)

Net Sales A 28205 2539.5

Operating Profit B 6238 646.4

Net Profit C 3874 415.7

Total Assets D 42133 3911

Total Equity E 14560 2399

Operating Profit margin F=B/A 22.12% 25.45%

Return on Assets G=C/D 9.19% 10.63%

Return on Equity H=C/E 26.61% 17.33%

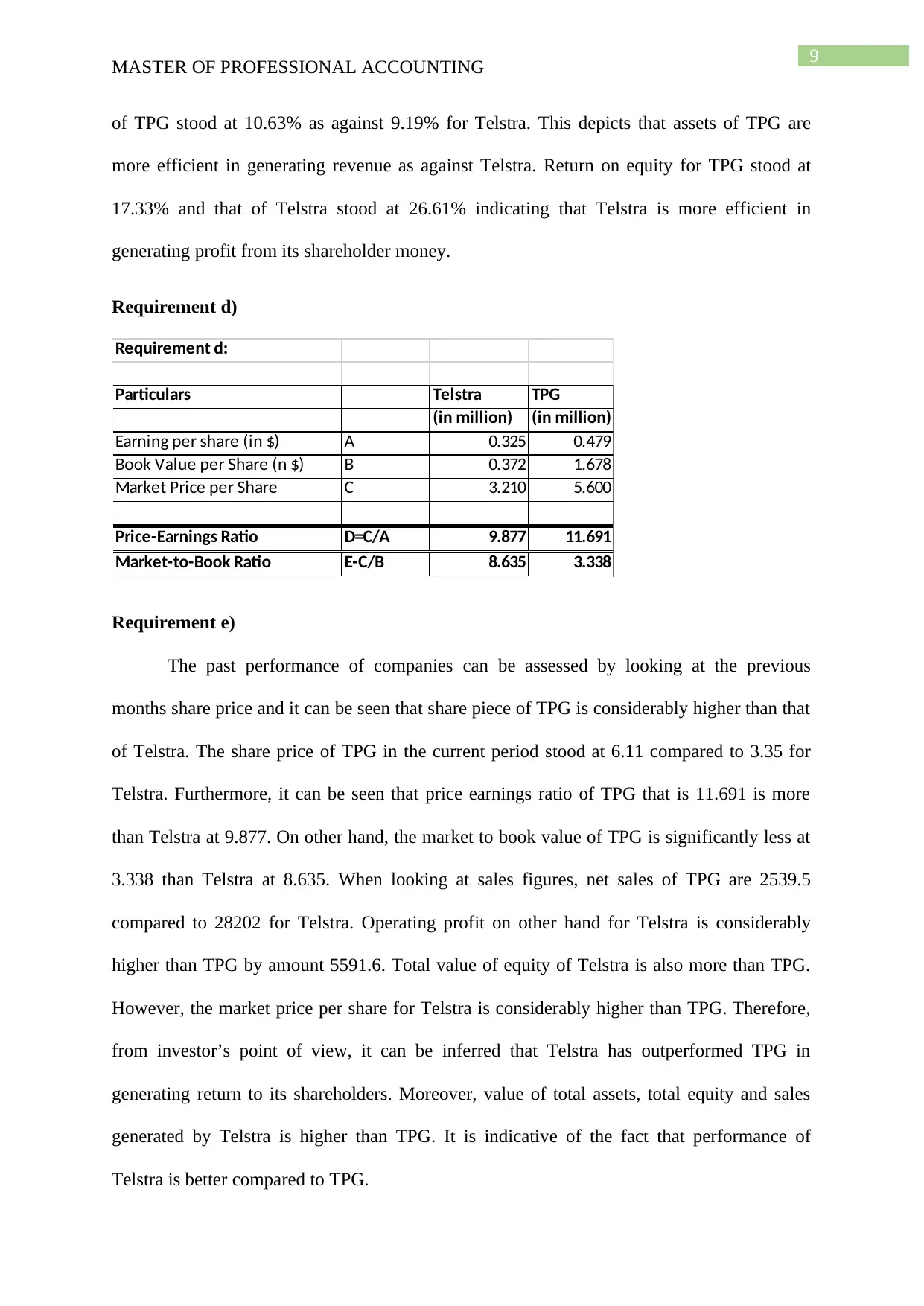

The profitability performance of Telstra and TPG is evaluated by the computation of

operating profit margin, return on assets and return on equity. Operating profit margin of

Telstra stood at 22.12% and that of TPG stood at 25.45% respectively indicating that profit

generation from operations of later company is more than former company. Return on assets

MASTER OF PROFESSIONAL ACCOUNTING

Requirement b)

Date Telstra TPG

27-02-2018 3.35 6.11

28-02-2018 3.32 6.18

01-03-2018 3.27 6

04-03-2018 3.3 6.03

05-03-2018 3.37 6.12

06-03-2018 3.35 6.08

07-03-2018 3.39 6.08

08-03-2018 3.44 6.13

11-03-2018 3.44 6.17

12-03-2018 3.41 6.06

13-03-2018 3.32 6.04

14-03-2018 3.3 5.94

15-03-2018 3.35 6.02

18-03-2018 3.35 6.04

19-03-2018 3.37 5.76

20-03-2018 3.33 5.98

21-03-2018 3.27 5.86

22-03-2018 3.22 5.7

25-03-2018 3.2 5.63

26-03-2018 3.21 5.6

Requirement c)

Particulars Telstra TPG

(in million) (in million)

Net Sales A 28205 2539.5

Operating Profit B 6238 646.4

Net Profit C 3874 415.7

Total Assets D 42133 3911

Total Equity E 14560 2399

Operating Profit margin F=B/A 22.12% 25.45%

Return on Assets G=C/D 9.19% 10.63%

Return on Equity H=C/E 26.61% 17.33%

The profitability performance of Telstra and TPG is evaluated by the computation of

operating profit margin, return on assets and return on equity. Operating profit margin of

Telstra stood at 22.12% and that of TPG stood at 25.45% respectively indicating that profit

generation from operations of later company is more than former company. Return on assets

9

MASTER OF PROFESSIONAL ACCOUNTING

of TPG stood at 10.63% as against 9.19% for Telstra. This depicts that assets of TPG are

more efficient in generating revenue as against Telstra. Return on equity for TPG stood at

17.33% and that of Telstra stood at 26.61% indicating that Telstra is more efficient in

generating profit from its shareholder money.

Requirement d)

Requirement d:

Particulars Telstra TPG

(in million) (in million)

Earning per share (in $) A 0.325 0.479

Book Value per Share (n $) B 0.372 1.678

Market Price per Share C 3.210 5.600

Price-Earnings Ratio D=C/A 9.877 11.691

Market-to-Book Ratio E-C/B 8.635 3.338

Requirement e)

The past performance of companies can be assessed by looking at the previous

months share price and it can be seen that share piece of TPG is considerably higher than that

of Telstra. The share price of TPG in the current period stood at 6.11 compared to 3.35 for

Telstra. Furthermore, it can be seen that price earnings ratio of TPG that is 11.691 is more

than Telstra at 9.877. On other hand, the market to book value of TPG is significantly less at

3.338 than Telstra at 8.635. When looking at sales figures, net sales of TPG are 2539.5

compared to 28202 for Telstra. Operating profit on other hand for Telstra is considerably

higher than TPG by amount 5591.6. Total value of equity of Telstra is also more than TPG.

However, the market price per share for Telstra is considerably higher than TPG. Therefore,

from investor’s point of view, it can be inferred that Telstra has outperformed TPG in

generating return to its shareholders. Moreover, value of total assets, total equity and sales

generated by Telstra is higher than TPG. It is indicative of the fact that performance of

Telstra is better compared to TPG.

MASTER OF PROFESSIONAL ACCOUNTING

of TPG stood at 10.63% as against 9.19% for Telstra. This depicts that assets of TPG are

more efficient in generating revenue as against Telstra. Return on equity for TPG stood at

17.33% and that of Telstra stood at 26.61% indicating that Telstra is more efficient in

generating profit from its shareholder money.

Requirement d)

Requirement d:

Particulars Telstra TPG

(in million) (in million)

Earning per share (in $) A 0.325 0.479

Book Value per Share (n $) B 0.372 1.678

Market Price per Share C 3.210 5.600

Price-Earnings Ratio D=C/A 9.877 11.691

Market-to-Book Ratio E-C/B 8.635 3.338

Requirement e)

The past performance of companies can be assessed by looking at the previous

months share price and it can be seen that share piece of TPG is considerably higher than that

of Telstra. The share price of TPG in the current period stood at 6.11 compared to 3.35 for

Telstra. Furthermore, it can be seen that price earnings ratio of TPG that is 11.691 is more

than Telstra at 9.877. On other hand, the market to book value of TPG is significantly less at

3.338 than Telstra at 8.635. When looking at sales figures, net sales of TPG are 2539.5

compared to 28202 for Telstra. Operating profit on other hand for Telstra is considerably

higher than TPG by amount 5591.6. Total value of equity of Telstra is also more than TPG.

However, the market price per share for Telstra is considerably higher than TPG. Therefore,

from investor’s point of view, it can be inferred that Telstra has outperformed TPG in

generating return to its shareholders. Moreover, value of total assets, total equity and sales

generated by Telstra is higher than TPG. It is indicative of the fact that performance of

Telstra is better compared to TPG.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

MASTER OF PROFESSIONAL ACCOUNTING

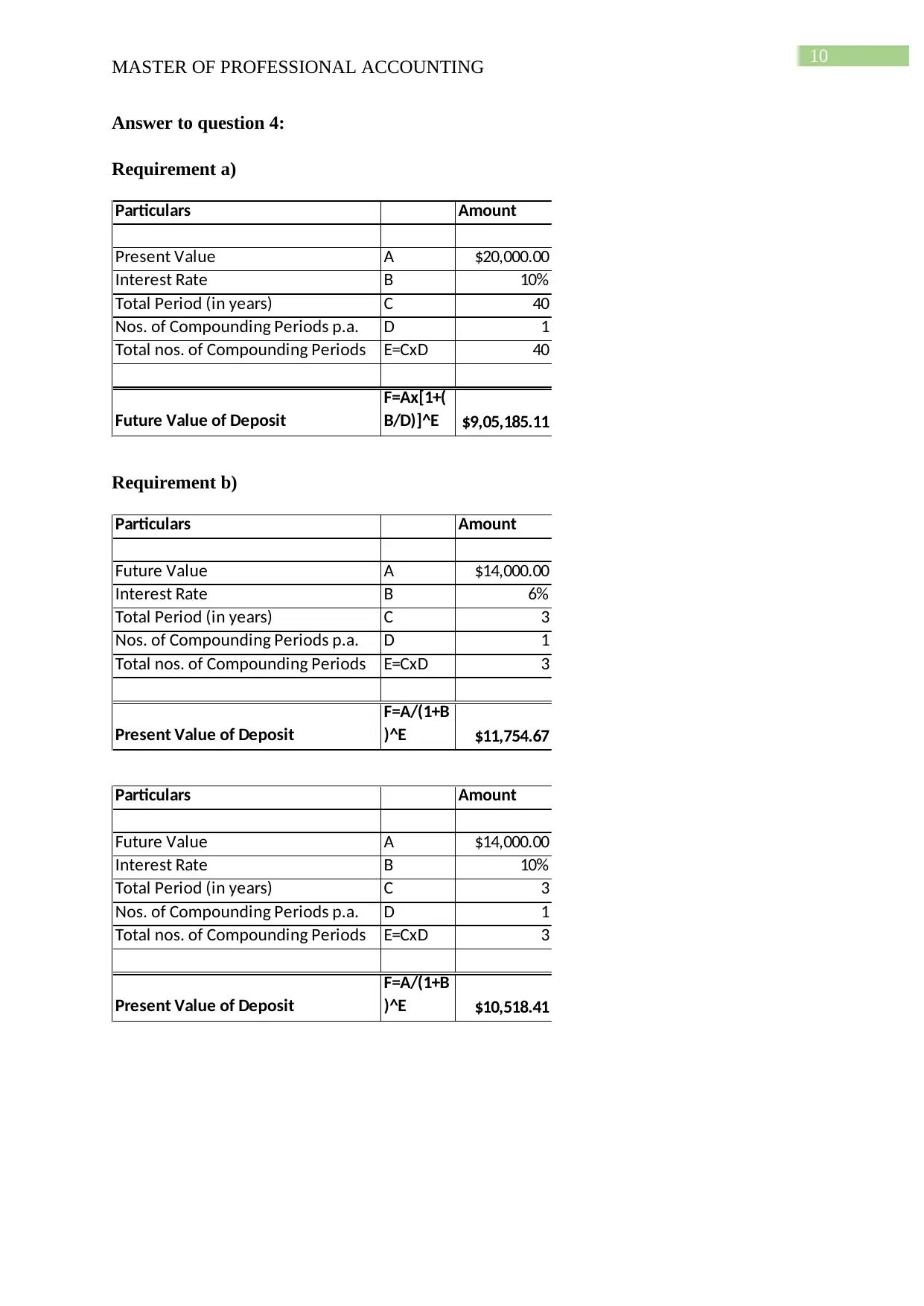

Answer to question 4:

Requirement a)

Particulars Amount

Present Value A $20,000.00

Interest Rate B 10%

Total Period (in years) C 40

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 40

Future Value of Deposit

F=Ax[1+(

B/D)]^E $9,05,185.11

Requirement b)

Particulars Amount

Future Value A $14,000.00

Interest Rate B 6%

Total Period (in years) C 3

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 3

Present Value of Deposit

F=A/(1+B

)^E $11,754.67

Particulars Amount

Future Value A $14,000.00

Interest Rate B 10%

Total Period (in years) C 3

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 3

Present Value of Deposit

F=A/(1+B

)^E $10,518.41

MASTER OF PROFESSIONAL ACCOUNTING

Answer to question 4:

Requirement a)

Particulars Amount

Present Value A $20,000.00

Interest Rate B 10%

Total Period (in years) C 40

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 40

Future Value of Deposit

F=Ax[1+(

B/D)]^E $9,05,185.11

Requirement b)

Particulars Amount

Future Value A $14,000.00

Interest Rate B 6%

Total Period (in years) C 3

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 3

Present Value of Deposit

F=A/(1+B

)^E $11,754.67

Particulars Amount

Future Value A $14,000.00

Interest Rate B 10%

Total Period (in years) C 3

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 3

Present Value of Deposit

F=A/(1+B

)^E $10,518.41

11

MASTER OF PROFESSIONAL ACCOUNTING

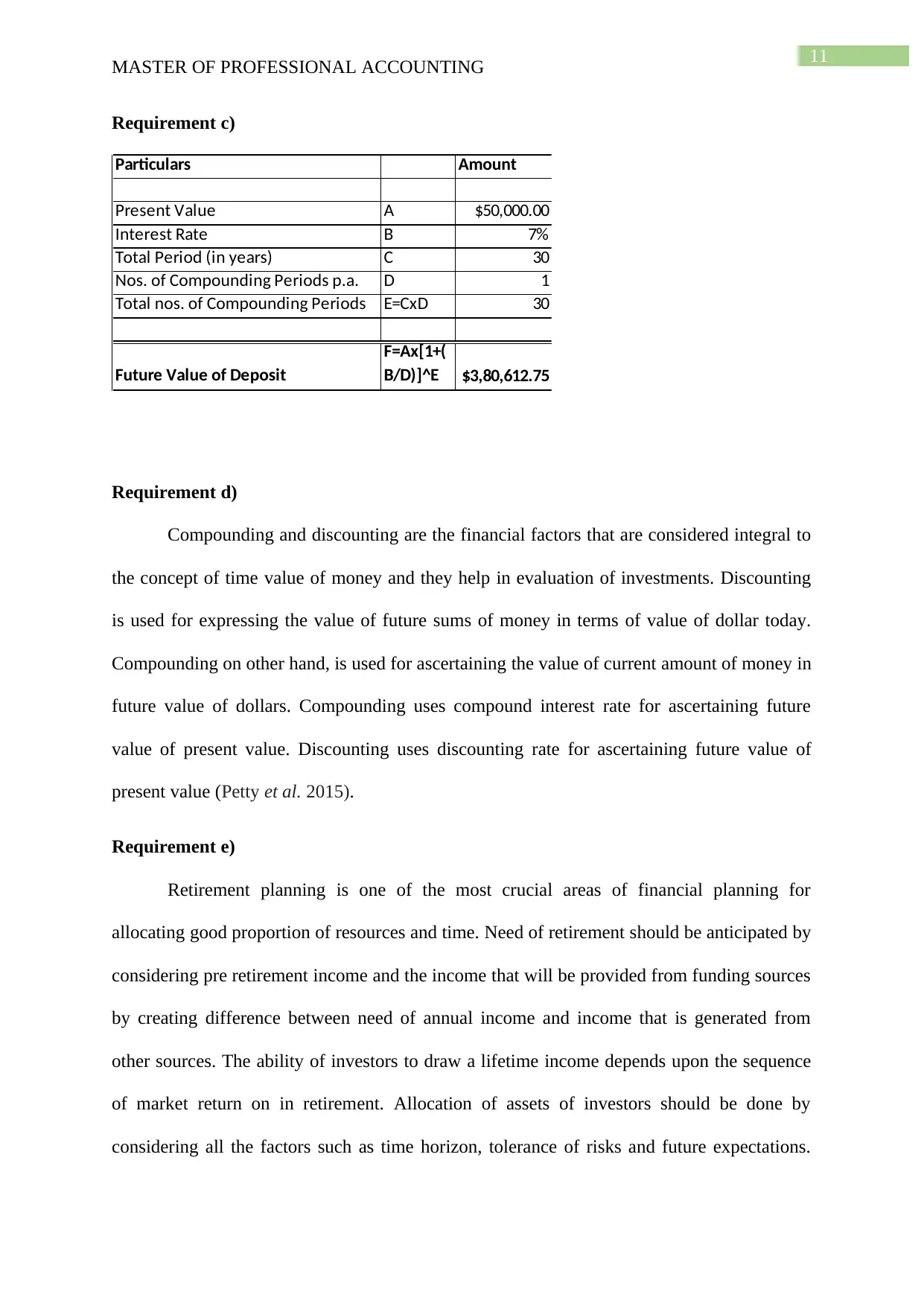

Requirement c)

Particulars Amount

Present Value A $50,000.00

Interest Rate B 7%

Total Period (in years) C 30

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 30

Future Value of Deposit

F=Ax[1+(

B/D)]^E $3,80,612.75

Requirement d)

Compounding and discounting are the financial factors that are considered integral to

the concept of time value of money and they help in evaluation of investments. Discounting

is used for expressing the value of future sums of money in terms of value of dollar today.

Compounding on other hand, is used for ascertaining the value of current amount of money in

future value of dollars. Compounding uses compound interest rate for ascertaining future

value of present value. Discounting uses discounting rate for ascertaining future value of

present value (Petty et al. 2015).

Requirement e)

Retirement planning is one of the most crucial areas of financial planning for

allocating good proportion of resources and time. Need of retirement should be anticipated by

considering pre retirement income and the income that will be provided from funding sources

by creating difference between need of annual income and income that is generated from

other sources. The ability of investors to draw a lifetime income depends upon the sequence

of market return on in retirement. Allocation of assets of investors should be done by

considering all the factors such as time horizon, tolerance of risks and future expectations.

MASTER OF PROFESSIONAL ACCOUNTING

Requirement c)

Particulars Amount

Present Value A $50,000.00

Interest Rate B 7%

Total Period (in years) C 30

Nos. of Compounding Periods p.a. D 1

Total nos. of Compounding Periods E=CxD 30

Future Value of Deposit

F=Ax[1+(

B/D)]^E $3,80,612.75

Requirement d)

Compounding and discounting are the financial factors that are considered integral to

the concept of time value of money and they help in evaluation of investments. Discounting

is used for expressing the value of future sums of money in terms of value of dollar today.

Compounding on other hand, is used for ascertaining the value of current amount of money in

future value of dollars. Compounding uses compound interest rate for ascertaining future

value of present value. Discounting uses discounting rate for ascertaining future value of

present value (Petty et al. 2015).

Requirement e)

Retirement planning is one of the most crucial areas of financial planning for

allocating good proportion of resources and time. Need of retirement should be anticipated by

considering pre retirement income and the income that will be provided from funding sources

by creating difference between need of annual income and income that is generated from

other sources. The ability of investors to draw a lifetime income depends upon the sequence

of market return on in retirement. Allocation of assets of investors should be done by

considering all the factors such as time horizon, tolerance of risks and future expectations.

12

MASTER OF PROFESSIONAL ACCOUNTING

Formulation of overall investment plan investors should be done in conjunction with top

priorities of retirement. Moreover, the period of portfolio of investment should be extended if

planned retirement date intends to be shifted. The probability of earning return can be

increased by staying in equities in greater proportion and for greater period. Saving needs for

accumulating more return during retirement is determined by the factor interest rate. The

payment from contribution plan to investors or employees during retirement is influenced by

the interest rate factor (Ormrod 2015).

Answer to question 5:

Introduction:

The report is prepared for studying the effects of cash rate on tourism sector of

Australia. For the purpose of analysis, reasons associated with the change in cash rates have

been ascertained and yearly data on cash rates for time period of ten years ranging from 2007

to 2017 have been collected. The target cash rate is set by Reserve Bank of Australia that is

used as instrument of monetary policy (Andor et al. 2015). In order to keep cash rate at

target, the approach employed by bank to supply enough funds.

Discussion:

Australian tourism industry has witnessed difficult conditions pertaining to demand

because of several factors such as Australian dollar depreciation, subdued economic

conditions and higher exchange rate accompanies by downturn in business travel and slow

growth in spending by household. A stable cash rate might encourage people to money and

increase the willingness of consumers to extend them in spending. This would have favorable

impact on business of tourism industry, as increased spending would increase the income of

industry as a whole.

MASTER OF PROFESSIONAL ACCOUNTING

Formulation of overall investment plan investors should be done in conjunction with top

priorities of retirement. Moreover, the period of portfolio of investment should be extended if

planned retirement date intends to be shifted. The probability of earning return can be

increased by staying in equities in greater proportion and for greater period. Saving needs for

accumulating more return during retirement is determined by the factor interest rate. The

payment from contribution plan to investors or employees during retirement is influenced by

the interest rate factor (Ormrod 2015).

Answer to question 5:

Introduction:

The report is prepared for studying the effects of cash rate on tourism sector of

Australia. For the purpose of analysis, reasons associated with the change in cash rates have

been ascertained and yearly data on cash rates for time period of ten years ranging from 2007

to 2017 have been collected. The target cash rate is set by Reserve Bank of Australia that is

used as instrument of monetary policy (Andor et al. 2015). In order to keep cash rate at

target, the approach employed by bank to supply enough funds.

Discussion:

Australian tourism industry has witnessed difficult conditions pertaining to demand

because of several factors such as Australian dollar depreciation, subdued economic

conditions and higher exchange rate accompanies by downturn in business travel and slow

growth in spending by household. A stable cash rate might encourage people to money and

increase the willingness of consumers to extend them in spending. This would have favorable

impact on business of tourism industry, as increased spending would increase the income of

industry as a whole.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

MASTER OF PROFESSIONAL ACCOUNTING

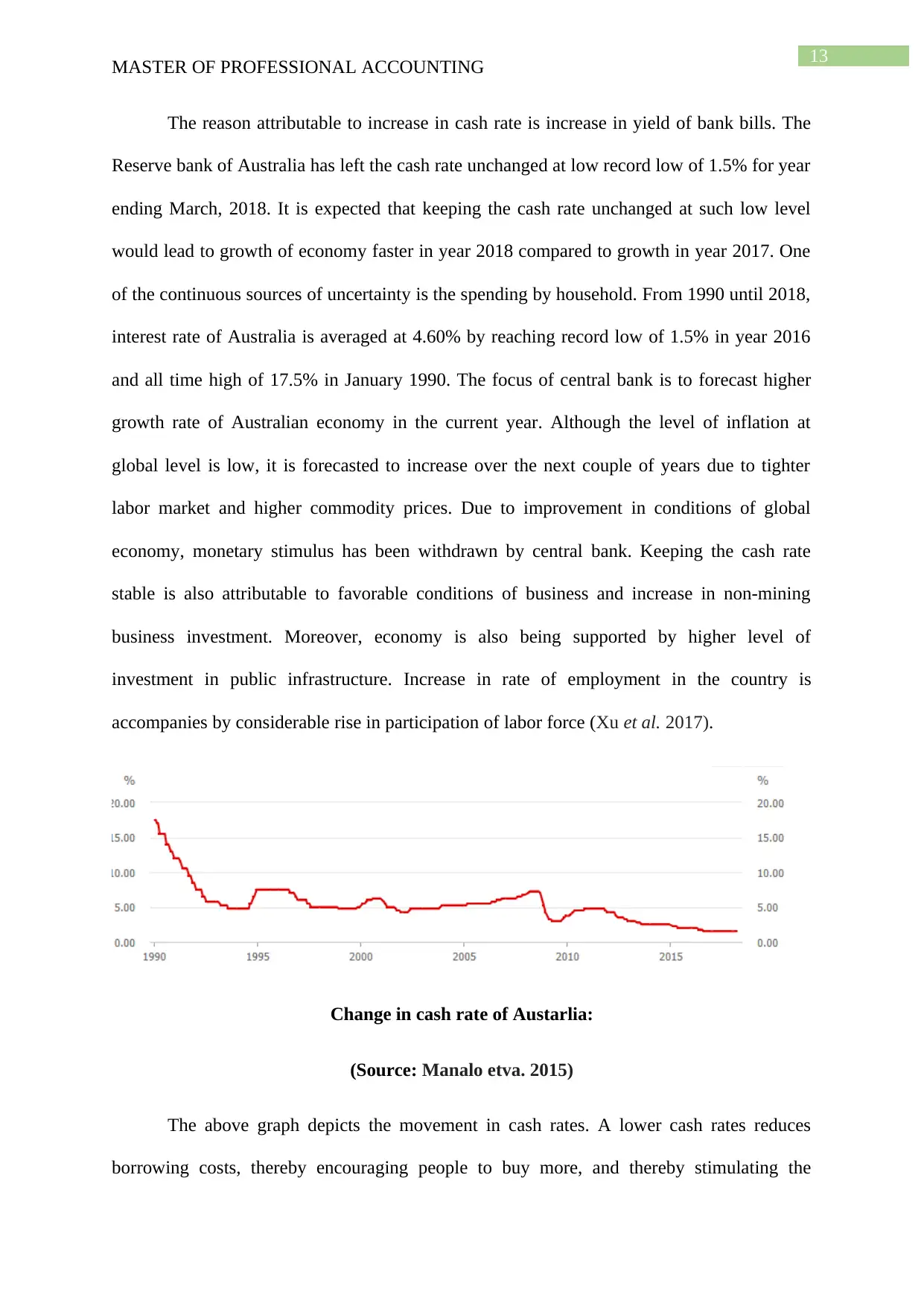

The reason attributable to increase in cash rate is increase in yield of bank bills. The

Reserve bank of Australia has left the cash rate unchanged at low record low of 1.5% for year

ending March, 2018. It is expected that keeping the cash rate unchanged at such low level

would lead to growth of economy faster in year 2018 compared to growth in year 2017. One

of the continuous sources of uncertainty is the spending by household. From 1990 until 2018,

interest rate of Australia is averaged at 4.60% by reaching record low of 1.5% in year 2016

and all time high of 17.5% in January 1990. The focus of central bank is to forecast higher

growth rate of Australian economy in the current year. Although the level of inflation at

global level is low, it is forecasted to increase over the next couple of years due to tighter

labor market and higher commodity prices. Due to improvement in conditions of global

economy, monetary stimulus has been withdrawn by central bank. Keeping the cash rate

stable is also attributable to favorable conditions of business and increase in non-mining

business investment. Moreover, economy is also being supported by higher level of

investment in public infrastructure. Increase in rate of employment in the country is

accompanies by considerable rise in participation of labor force (Xu et al. 2017).

Change in cash rate of Austarlia:

(Source: Manalo etva. 2015)

The above graph depicts the movement in cash rates. A lower cash rates reduces

borrowing costs, thereby encouraging people to buy more, and thereby stimulating the

MASTER OF PROFESSIONAL ACCOUNTING

The reason attributable to increase in cash rate is increase in yield of bank bills. The

Reserve bank of Australia has left the cash rate unchanged at low record low of 1.5% for year

ending March, 2018. It is expected that keeping the cash rate unchanged at such low level

would lead to growth of economy faster in year 2018 compared to growth in year 2017. One

of the continuous sources of uncertainty is the spending by household. From 1990 until 2018,

interest rate of Australia is averaged at 4.60% by reaching record low of 1.5% in year 2016

and all time high of 17.5% in January 1990. The focus of central bank is to forecast higher

growth rate of Australian economy in the current year. Although the level of inflation at

global level is low, it is forecasted to increase over the next couple of years due to tighter

labor market and higher commodity prices. Due to improvement in conditions of global

economy, monetary stimulus has been withdrawn by central bank. Keeping the cash rate

stable is also attributable to favorable conditions of business and increase in non-mining

business investment. Moreover, economy is also being supported by higher level of

investment in public infrastructure. Increase in rate of employment in the country is

accompanies by considerable rise in participation of labor force (Xu et al. 2017).

Change in cash rate of Austarlia:

(Source: Manalo etva. 2015)

The above graph depicts the movement in cash rates. A lower cash rates reduces

borrowing costs, thereby encouraging people to buy more, and thereby stimulating the

14

MASTER OF PROFESSIONAL ACCOUNTING

economy of country. On other hand, spending in economy is encouraged by higher interest

rate. Level of supply and demand in economy and ultimately inflation level is effected by rise

or fall in rate of interest. It is perceived that cash rate set of RBA will remain on hold until

there is probable hike in rate and the risk is associated with the fact that rate will not rise until

2019 nonetheless. In the current scenario, there is unusual low wage and inflation trends and

improvement in trading and local partner economies. The unchanged rate of cash since the

last sixteen months from the perspective of monetary policy seems to persist in another year

as well. Moreover, there have no change in forecast of inflation and rate of growth. There

was no mentioning of consumer price index and it is viewed that over the year, the underline

rate of inflation will now be about 0.25%. It is expected that RBA will leave the cash rate

unchanged at level of 1.5% for the remainder of 2018. There was compassionate

development of wages and rates of inflation. The first rate in rise is witnessed in current

market pricing around March, 2019. Australian dollar will probably be the country’s buffer

against the rising overseas rate of interest. There is no urgency for central bank to raise the

cash rate until there is improvement in growth of wage rates. In fact, any change in cast rate

would misguide business and sector such as tourism given the level of spending by household

(Karadag 2015). In this regard, the key questions faced by officials of bank are the

reconciliation of balance between household spending and employment growth.

Conclusion:

From the analysis of above discussed factors, it can be seen that cash rate would be

stable at the rate of 1.5% in the remainder of current year. The reason is attributable to

several economic factors such as wage rate and inflation rate in the economy. However, it is

expected that bank will have tighter policy in light of weakness in inflation and retail sales.

Increased focus on bank on the financial stability is indicative of the fact that the rates will be

MASTER OF PROFESSIONAL ACCOUNTING

economy of country. On other hand, spending in economy is encouraged by higher interest

rate. Level of supply and demand in economy and ultimately inflation level is effected by rise

or fall in rate of interest. It is perceived that cash rate set of RBA will remain on hold until

there is probable hike in rate and the risk is associated with the fact that rate will not rise until

2019 nonetheless. In the current scenario, there is unusual low wage and inflation trends and

improvement in trading and local partner economies. The unchanged rate of cash since the

last sixteen months from the perspective of monetary policy seems to persist in another year

as well. Moreover, there have no change in forecast of inflation and rate of growth. There

was no mentioning of consumer price index and it is viewed that over the year, the underline

rate of inflation will now be about 0.25%. It is expected that RBA will leave the cash rate

unchanged at level of 1.5% for the remainder of 2018. There was compassionate

development of wages and rates of inflation. The first rate in rise is witnessed in current

market pricing around March, 2019. Australian dollar will probably be the country’s buffer

against the rising overseas rate of interest. There is no urgency for central bank to raise the

cash rate until there is improvement in growth of wage rates. In fact, any change in cast rate

would misguide business and sector such as tourism given the level of spending by household

(Karadag 2015). In this regard, the key questions faced by officials of bank are the

reconciliation of balance between household spending and employment growth.

Conclusion:

From the analysis of above discussed factors, it can be seen that cash rate would be

stable at the rate of 1.5% in the remainder of current year. The reason is attributable to

several economic factors such as wage rate and inflation rate in the economy. However, it is

expected that bank will have tighter policy in light of weakness in inflation and retail sales.

Increased focus on bank on the financial stability is indicative of the fact that the rates will be

15

MASTER OF PROFESSIONAL ACCOUNTING

moved off the prevailing low historic levels as long as it is felt that level of inflation in the

economy is headed in the right direction (Manalo et al. 2015).

References list:

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of

Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Atkinson, A., Messy, F.A., Rabinovich, L. and Yoong, J., 2015. Financial education for long-

term savings and investments: review of research and literature. OECD Working Papers on

Finance, Insurance and Private Pensions, (39), p.0_1.

Burns, R. and Walker, J., 2015. Capital budgeting surveys: the future is now.

De Nardi, M., French, E. and Jones, J.B., 2016. Savings after retirement: A survey. Annual

Review of Economics, 8, pp.177-204.

MASTER OF PROFESSIONAL ACCOUNTING

moved off the prevailing low historic levels as long as it is felt that level of inflation in the

economy is headed in the right direction (Manalo et al. 2015).

References list:

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of

Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Atkinson, A., Messy, F.A., Rabinovich, L. and Yoong, J., 2015. Financial education for long-

term savings and investments: review of research and literature. OECD Working Papers on

Finance, Insurance and Private Pensions, (39), p.0_1.

Burns, R. and Walker, J., 2015. Capital budgeting surveys: the future is now.

De Nardi, M., French, E. and Jones, J.B., 2016. Savings after retirement: A survey. Annual

Review of Economics, 8, pp.177-204.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

MASTER OF PROFESSIONAL ACCOUNTING

Goda, G.S., Levy, M.R., Manchester, C.F., Sojourner, A. and Tasoff, J., 2015. The role of

time preferences and exponential-growth bias in retirement savings (No. w21482). National

Bureau of Economic Research.

Hanna, S.D., Kim, K.T. and Chen, S.C.C., 2016. Retirement savings. In Handbook of

consumer finance research (pp. 33-43). Springer, Cham.

Hong, H.A., KIM, J.B. and Welker, M., 2017. Divergence of cash flow and voting rights,

opacity, and stock price crash risk: international evidence. Journal of Accounting

Research, 55(5), pp.1167-1212.

Karadag, H., 2015. Financial management challenges in small and medium-sized enterprises:

A strategic management approach. Emerging Markets Journal, 5(1), p.26.

Manalo, J., Perera, D. and Rees, D.M., 2015. Exchange rate movements and the Australian

economy. Economic Modelling, 47, pp.53-62.

Moutinho, L. and Vargas-Sanchez, A. eds., 2018. Strategic Management in Tourism, CABI

Tourism Texts. Cabi.

Ormrod, N.G., 2015. Business Models: A Unit of Analysis for Company Performance.

Petty, J.W., Titman, S., Keown, A.J., Martin, P., Martin, J.D. and Burrow, M.,

2015. Financial management: Principles and applications. Pearson Higher Education AU.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

MASTER OF PROFESSIONAL ACCOUNTING

Goda, G.S., Levy, M.R., Manchester, C.F., Sojourner, A. and Tasoff, J., 2015. The role of

time preferences and exponential-growth bias in retirement savings (No. w21482). National

Bureau of Economic Research.

Hanna, S.D., Kim, K.T. and Chen, S.C.C., 2016. Retirement savings. In Handbook of

consumer finance research (pp. 33-43). Springer, Cham.

Hong, H.A., KIM, J.B. and Welker, M., 2017. Divergence of cash flow and voting rights,

opacity, and stock price crash risk: international evidence. Journal of Accounting

Research, 55(5), pp.1167-1212.

Karadag, H., 2015. Financial management challenges in small and medium-sized enterprises:

A strategic management approach. Emerging Markets Journal, 5(1), p.26.

Manalo, J., Perera, D. and Rees, D.M., 2015. Exchange rate movements and the Australian

economy. Economic Modelling, 47, pp.53-62.

Moutinho, L. and Vargas-Sanchez, A. eds., 2018. Strategic Management in Tourism, CABI

Tourism Texts. Cabi.

Ormrod, N.G., 2015. Business Models: A Unit of Analysis for Company Performance.

Petty, J.W., Titman, S., Keown, A.J., Martin, P., Martin, J.D. and Burrow, M.,

2015. Financial management: Principles and applications. Pearson Higher Education AU.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

17

MASTER OF PROFESSIONAL ACCOUNTING

Xu, R., Chen, H. and Zhao, L.J., 2017. Predicting Corporate Venture Capital Investment.

MASTER OF PROFESSIONAL ACCOUNTING

Xu, R., Chen, H. and Zhao, L.J., 2017. Predicting Corporate Venture Capital Investment.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.