MA611 Auditing: Material Misstatement Risk Assessment Report

VerifiedAdded on 2023/03/17

|16

|3300

|39

Report

AI Summary

This report, prepared for the MA611 Auditing course, analyzes the Bank of Queensland's financial statements and associated risks. It begins with an executive summary and proceeds to detail the results of analytical procedures, including ratio and horizontal analyses of key financial figures such as net profit, operating cash flow, and asset values over a three-year period. The report identifies areas of potential risk, highlighting fluctuations in operating cash flows and asset utilization. It then explores the risk of material misstatement at both the financial report level, examining inherent risks related to management integrity, experience, and external pressures, and at the assertion level, focusing on net profit and cash flow from operations. The report concludes with a discussion of the influence of analytical procedures on audit planning decisions. The report also includes key assertions and audit procedures to mitigate risk. The assignment adheres to APA 6th edition referencing guidelines.

MASTERS OF PROFESSIONAL ACCOUNTING

MA611- Auditing

Page | 1

MA611- Auditing

Page | 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Executive Summary...................................................................................................................3

1- Results of Analytical Procedures...........................................................................................4

Analytical Procedures............................................................................................................4

Influence of analytical procedures on audit planning decisions............................................7

2- Risk of Material Misstatement (Inherent Risk) at the Financial Report Level......................8

3- Risk of Material Misstatement (Inherent Risk) at the Assertion Level...............................11

References................................................................................................................................15

Page | 2

Executive Summary...................................................................................................................3

1- Results of Analytical Procedures...........................................................................................4

Analytical Procedures............................................................................................................4

Influence of analytical procedures on audit planning decisions............................................7

2- Risk of Material Misstatement (Inherent Risk) at the Financial Report Level......................8

3- Risk of Material Misstatement (Inherent Risk) at the Assertion Level...............................11

References................................................................................................................................15

Page | 2

Executive Summary

This report is based on various aspects of audit planning Bank of Queensland. Auditing is the

process of investigating financial, operations, statutory and other relational requirements. In

this report, the application of analytical procedures on financial statements of the Bank of

Queensland has been undertaken. Net profit, operating cash flows, current assets and total

assets are risk factors of Bank of Queensland on the basis of an analytical procedure for the

last 3 years. Management has been considered as the inherent risk factor that needs to be

considered while planning audit. Nature of business, the volume of transactions and industry

factors are important considerations and on these bases inherent risk is identified for planning

audit procedures. At last, the risk of material misstatement at the assertion level has been

discussed. Net profit, operating cash flows and impairment on loans and advances are three

accounts at risk of material misstatement at the assertion level.

Page | 3

This report is based on various aspects of audit planning Bank of Queensland. Auditing is the

process of investigating financial, operations, statutory and other relational requirements. In

this report, the application of analytical procedures on financial statements of the Bank of

Queensland has been undertaken. Net profit, operating cash flows, current assets and total

assets are risk factors of Bank of Queensland on the basis of an analytical procedure for the

last 3 years. Management has been considered as the inherent risk factor that needs to be

considered while planning audit. Nature of business, the volume of transactions and industry

factors are important considerations and on these bases inherent risk is identified for planning

audit procedures. At last, the risk of material misstatement at the assertion level has been

discussed. Net profit, operating cash flows and impairment on loans and advances are three

accounts at risk of material misstatement at the assertion level.

Page | 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

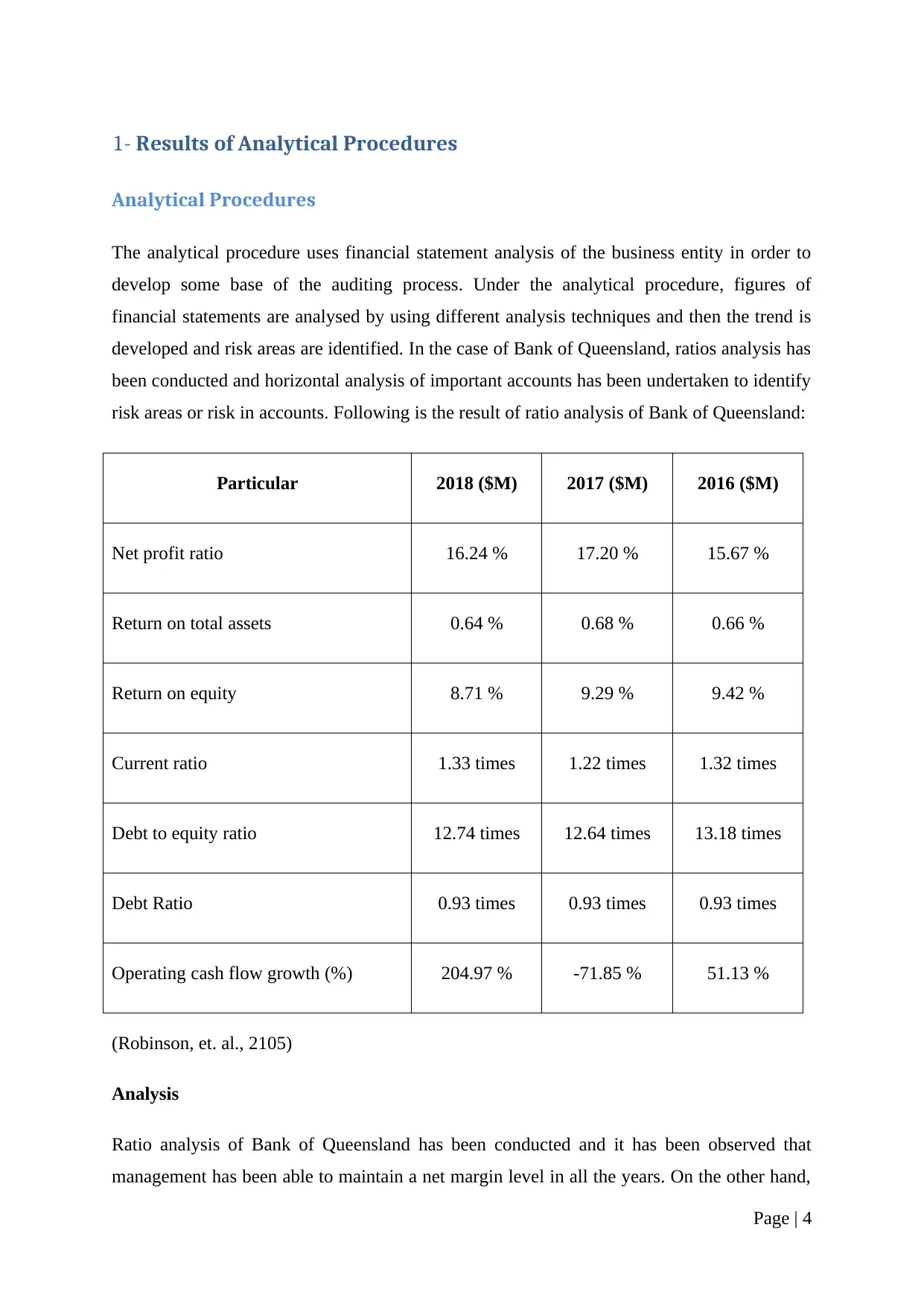

1- Results of Analytical Procedures

Analytical Procedures

The analytical procedure uses financial statement analysis of the business entity in order to

develop some base of the auditing process. Under the analytical procedure, figures of

financial statements are analysed by using different analysis techniques and then the trend is

developed and risk areas are identified. In the case of Bank of Queensland, ratios analysis has

been conducted and horizontal analysis of important accounts has been undertaken to identify

risk areas or risk in accounts. Following is the result of ratio analysis of Bank of Queensland:

Particular 2018 ($M) 2017 ($M) 2016 ($M)

Net profit ratio 16.24 % 17.20 % 15.67 %

Return on total assets 0.64 % 0.68 % 0.66 %

Return on equity 8.71 % 9.29 % 9.42 %

Current ratio 1.33 times 1.22 times 1.32 times

Debt to equity ratio 12.74 times 12.64 times 13.18 times

Debt Ratio 0.93 times 0.93 times 0.93 times

Operating cash flow growth (%) 204.97 % -71.85 % 51.13 %

(Robinson, et. al., 2105)

Analysis

Ratio analysis of Bank of Queensland has been conducted and it has been observed that

management has been able to maintain a net margin level in all the years. On the other hand,

Page | 4

Analytical Procedures

The analytical procedure uses financial statement analysis of the business entity in order to

develop some base of the auditing process. Under the analytical procedure, figures of

financial statements are analysed by using different analysis techniques and then the trend is

developed and risk areas are identified. In the case of Bank of Queensland, ratios analysis has

been conducted and horizontal analysis of important accounts has been undertaken to identify

risk areas or risk in accounts. Following is the result of ratio analysis of Bank of Queensland:

Particular 2018 ($M) 2017 ($M) 2016 ($M)

Net profit ratio 16.24 % 17.20 % 15.67 %

Return on total assets 0.64 % 0.68 % 0.66 %

Return on equity 8.71 % 9.29 % 9.42 %

Current ratio 1.33 times 1.22 times 1.32 times

Debt to equity ratio 12.74 times 12.64 times 13.18 times

Debt Ratio 0.93 times 0.93 times 0.93 times

Operating cash flow growth (%) 204.97 % -71.85 % 51.13 %

(Robinson, et. al., 2105)

Analysis

Ratio analysis of Bank of Queensland has been conducted and it has been observed that

management has been able to maintain a net margin level in all the years. On the other hand,

Page | 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

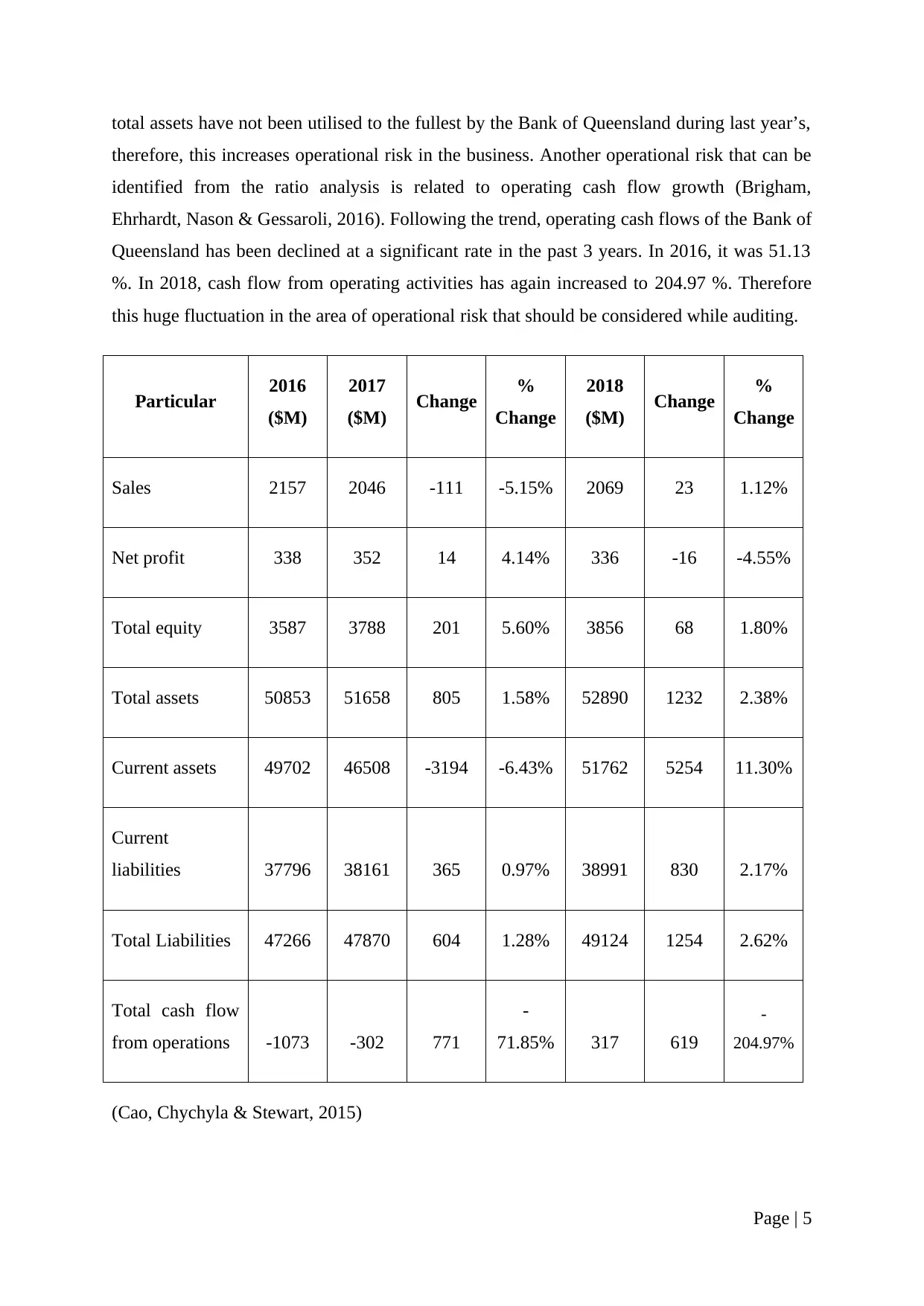

total assets have not been utilised to the fullest by the Bank of Queensland during last year’s,

therefore, this increases operational risk in the business. Another operational risk that can be

identified from the ratio analysis is related to operating cash flow growth (Brigham,

Ehrhardt, Nason & Gessaroli, 2016). Following the trend, operating cash flows of the Bank of

Queensland has been declined at a significant rate in the past 3 years. In 2016, it was 51.13

%. In 2018, cash flow from operating activities has again increased to 204.97 %. Therefore

this huge fluctuation in the area of operational risk that should be considered while auditing.

Particular 2016

($M)

2017

($M) Change %

Change

2018

($M) Change %

Change

Sales 2157 2046 -111 -5.15% 2069 23 1.12%

Net profit 338 352 14 4.14% 336 -16 -4.55%

Total equity 3587 3788 201 5.60% 3856 68 1.80%

Total assets 50853 51658 805 1.58% 52890 1232 2.38%

Current assets 49702 46508 -3194 -6.43% 51762 5254 11.30%

Current

liabilities 37796 38161 365 0.97% 38991 830 2.17%

Total Liabilities 47266 47870 604 1.28% 49124 1254 2.62%

Total cash flow

from operations -1073 -302 771

-

71.85% 317 619

-

204.97%

(Cao, Chychyla & Stewart, 2015)

Page | 5

therefore, this increases operational risk in the business. Another operational risk that can be

identified from the ratio analysis is related to operating cash flow growth (Brigham,

Ehrhardt, Nason & Gessaroli, 2016). Following the trend, operating cash flows of the Bank of

Queensland has been declined at a significant rate in the past 3 years. In 2016, it was 51.13

%. In 2018, cash flow from operating activities has again increased to 204.97 %. Therefore

this huge fluctuation in the area of operational risk that should be considered while auditing.

Particular 2016

($M)

2017

($M) Change %

Change

2018

($M) Change %

Change

Sales 2157 2046 -111 -5.15% 2069 23 1.12%

Net profit 338 352 14 4.14% 336 -16 -4.55%

Total equity 3587 3788 201 5.60% 3856 68 1.80%

Total assets 50853 51658 805 1.58% 52890 1232 2.38%

Current assets 49702 46508 -3194 -6.43% 51762 5254 11.30%

Current

liabilities 37796 38161 365 0.97% 38991 830 2.17%

Total Liabilities 47266 47870 604 1.28% 49124 1254 2.62%

Total cash flow

from operations -1073 -302 771

-

71.85% 317 619

-

204.97%

(Cao, Chychyla & Stewart, 2015)

Page | 5

Analysis:

From the above analysis of financial figures of the past 3 years, it can be observed that total

assets and specifically current assets as well have shown high fluctuation in all 3 years. On

the 0ther hand, total cash flow from business operations have also shown fluctuating results

and are fluctuations are peculiar (Plumlee, Rixom & Rosman, 2014). Therefore detailed

investigation of operating expenses and incomes should be undertaken while auditing of

Bank of Queensland.

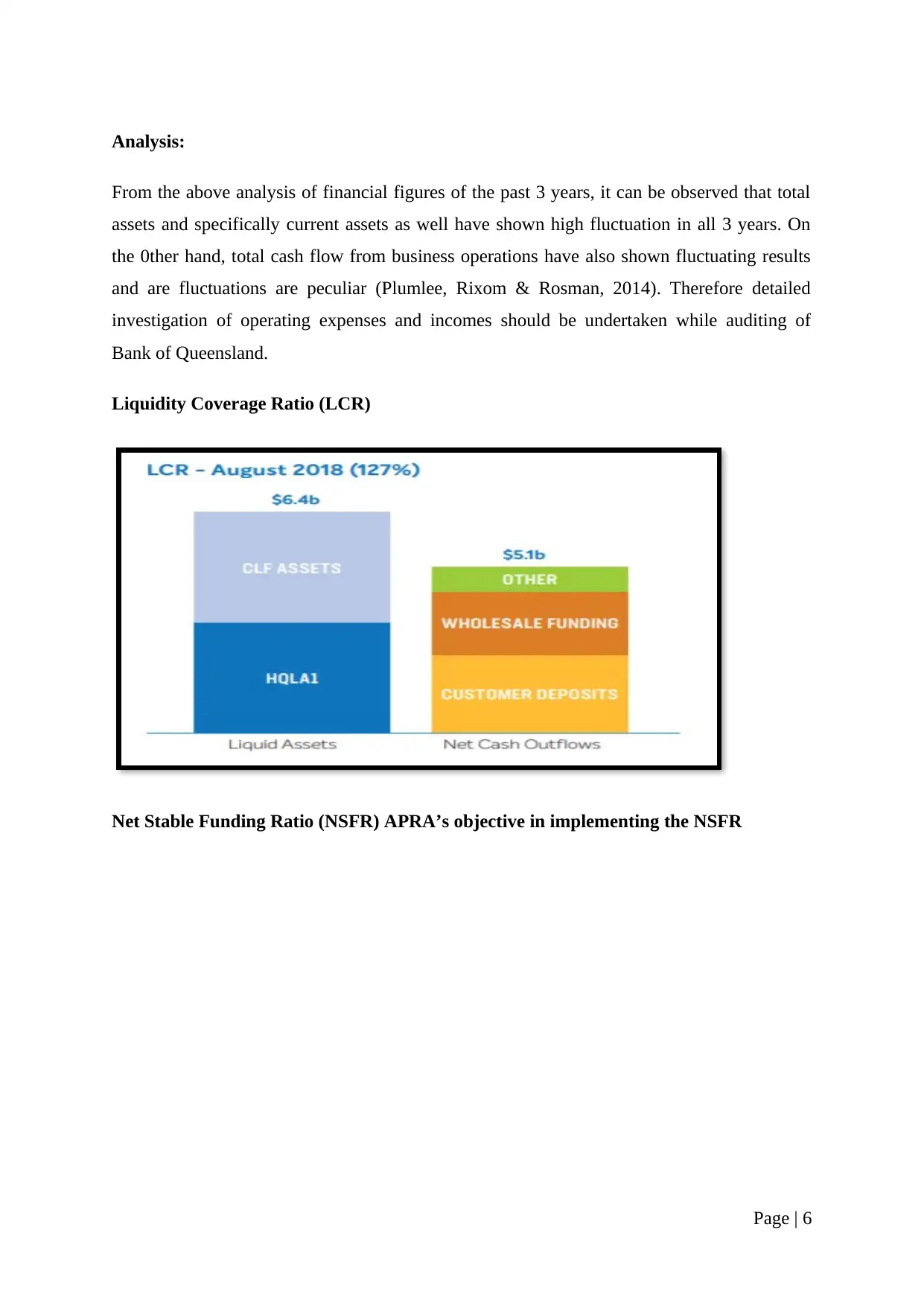

Liquidity Coverage Ratio (LCR)

Net Stable Funding Ratio (NSFR) APRA’s objective in implementing the NSFR

Page | 6

From the above analysis of financial figures of the past 3 years, it can be observed that total

assets and specifically current assets as well have shown high fluctuation in all 3 years. On

the 0ther hand, total cash flow from business operations have also shown fluctuating results

and are fluctuations are peculiar (Plumlee, Rixom & Rosman, 2014). Therefore detailed

investigation of operating expenses and incomes should be undertaken while auditing of

Bank of Queensland.

Liquidity Coverage Ratio (LCR)

Net Stable Funding Ratio (NSFR) APRA’s objective in implementing the NSFR

Page | 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Since Bank of Queensland is a banking corporation, therefore, various banking rules related

to maintaining cash and cash equivalents need to be investigating while auditing. Cash

reserve ratio and statutory liquidity ratios are to be maintained by banks and the same will be

analysed while auditing.

Influence of analytical procedures on audit planning decisions

Analytical procedures conducted on the financial statements of the business entity always

influences various decisions that auditor needs to undertake in the audit planning stage. The

analytical procedure presents a clear picture of past financial performance and highlights

different accounts that are to be considered important or material while verifying figures or

accounts (Eilifsen, Messier, Glover & Prawitt, 2013). In the case of Bank of Queensland,

apart from inherent risks involved in business operations, there are many other factors are to

be taken into account.

Conclusion: While performing analysis and horizontal analysis of financial statements many

accounts comes into picture which requires detailed investigation. Therefore because of

analytical procedures, the auditor is able to plan risk areas in the financial statements of the

business entities. It can be said that the results of analytical procedures becomes base for

planning and performing audit in every business organisation.

Page | 7

to maintaining cash and cash equivalents need to be investigating while auditing. Cash

reserve ratio and statutory liquidity ratios are to be maintained by banks and the same will be

analysed while auditing.

Influence of analytical procedures on audit planning decisions

Analytical procedures conducted on the financial statements of the business entity always

influences various decisions that auditor needs to undertake in the audit planning stage. The

analytical procedure presents a clear picture of past financial performance and highlights

different accounts that are to be considered important or material while verifying figures or

accounts (Eilifsen, Messier, Glover & Prawitt, 2013). In the case of Bank of Queensland,

apart from inherent risks involved in business operations, there are many other factors are to

be taken into account.

Conclusion: While performing analysis and horizontal analysis of financial statements many

accounts comes into picture which requires detailed investigation. Therefore because of

analytical procedures, the auditor is able to plan risk areas in the financial statements of the

business entities. It can be said that the results of analytical procedures becomes base for

planning and performing audit in every business organisation.

Page | 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2- Risk of Material Misstatement (Inherent Risk) at the Financial

Report Level

Inherent risk is the risk that every business organisation possesses and these are an

uncontrollable risk. Inherent risk has been classified under various categories and varies from

business to business. Operational risk, legal risk, credit risk, market risk, etc. are some

inherent risk related to business entities.

Table showing different aspects of directors of Bank of Queensland during 2017-2018:

Name Position Educational

Background

Experience

ROGER DAVIS Chairman

Non-Executive

Independent Director

B.Econ. (Hons) and

Master of Philosophy

Over 33 years

JON SUTTON Managing Director &

CEO Executive Director

Over 20 years

BRUCE

CARTER

Non-Executive

Independent Director

B Econ, MBA, FAICD,

FICA

Over 14 years

RICHARD

HAIRE

Non-Executive

Independent Director

B.Ec, FAICD Over 29 years

JOHN LORIMER Non-Executive

Independent Director

B Com Over 30 years

WARWICK

NEGUS

Non-Executive

Independent Director

B Bus, M Com, SF Fin Over 30 years

Page | 8

Report Level

Inherent risk is the risk that every business organisation possesses and these are an

uncontrollable risk. Inherent risk has been classified under various categories and varies from

business to business. Operational risk, legal risk, credit risk, market risk, etc. are some

inherent risk related to business entities.

Table showing different aspects of directors of Bank of Queensland during 2017-2018:

Name Position Educational

Background

Experience

ROGER DAVIS Chairman

Non-Executive

Independent Director

B.Econ. (Hons) and

Master of Philosophy

Over 33 years

JON SUTTON Managing Director &

CEO Executive Director

Over 20 years

BRUCE

CARTER

Non-Executive

Independent Director

B Econ, MBA, FAICD,

FICA

Over 14 years

RICHARD

HAIRE

Non-Executive

Independent Director

B.Ec, FAICD Over 29 years

JOHN LORIMER Non-Executive

Independent Director

B Com Over 30 years

WARWICK

NEGUS

Non-Executive

Independent Director

B Bus, M Com, SF Fin Over 30 years

Page | 8

KAREN

PENROSE

Non-Executive

Independent Director

B Com, CPA, FAICD Over 20 years

MICHELLE

TREDENICK

Non-Executive

Independent Director

B Sc., FAICD, F Fin Over 30 years

DAVID WILLIS Non-Executive

Independent Director

B Com, ACA, ICA Over 35 years

MARGARET

(MARGIE)

SEALE

Non-Executive

Independent Director

BA, FAICD Over 25 years

In the case of Bank of Queensland, the following are major factors or area of inherent risk:

a. The integrity of management (i.e., the directors): Integrity of management can be

assessed by identifying no of independent and dependent directors in overall management. In

case of Bank of Queensland, there are 9 independent directors out of 10. On the other hand,

the Federal government in Australia has also mandated all the banking companies to establish

a Royal Commission that will take care of financial and superannuation system of banking

companies. Apart from the Royal Commission, there are various other committees and

groups that undertake the integrity of directors. Therefore it can be concluded that the

inherent risk of the integrity of management will at the lower side.

b. Management (i.e., Director) experience, knowledge and changes during the period:

From the above table of directors, it can be observed that majority of directors of Bank of

Queensland is well educated, has adequate experience to manage business affairs of banking

corporation and reliance can be placed on them on the basis of educational background (Pike,

Curtis & Chui, 2013). On the basis of the above-mentioned point, Bank of Queensland has

very fewer changes in their directors in the last reporting period i.e. 2017-2018. From the

annual report of the Bank of Queensland, it can be analysed that there are fewer changes in

Page | 9

PENROSE

Non-Executive

Independent Director

B Com, CPA, FAICD Over 20 years

MICHELLE

TREDENICK

Non-Executive

Independent Director

B Sc., FAICD, F Fin Over 30 years

DAVID WILLIS Non-Executive

Independent Director

B Com, ACA, ICA Over 35 years

MARGARET

(MARGIE)

SEALE

Non-Executive

Independent Director

BA, FAICD Over 25 years

In the case of Bank of Queensland, the following are major factors or area of inherent risk:

a. The integrity of management (i.e., the directors): Integrity of management can be

assessed by identifying no of independent and dependent directors in overall management. In

case of Bank of Queensland, there are 9 independent directors out of 10. On the other hand,

the Federal government in Australia has also mandated all the banking companies to establish

a Royal Commission that will take care of financial and superannuation system of banking

companies. Apart from the Royal Commission, there are various other committees and

groups that undertake the integrity of directors. Therefore it can be concluded that the

inherent risk of the integrity of management will at the lower side.

b. Management (i.e., Director) experience, knowledge and changes during the period:

From the above table of directors, it can be observed that majority of directors of Bank of

Queensland is well educated, has adequate experience to manage business affairs of banking

corporation and reliance can be placed on them on the basis of educational background (Pike,

Curtis & Chui, 2013). On the basis of the above-mentioned point, Bank of Queensland has

very fewer changes in their directors in the last reporting period i.e. 2017-2018. From the

annual report of the Bank of Queensland, it can be analysed that there are fewer changes in

Page | 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

directors, the majority of directors are well experienced and educated. Therefore this inherent

risk is at a controlled level during 2017-2018.

c. Unusual pressure on management (i.e., the directors): Under this inherent risk,

management or directors of business entity is tends to pressurised because of their duties,

responsibilities and because of statutory requirements. Since the Bank of Queensland is a

banking corporation, therefore, there are many statutory requirements that management needs

to take care of. These requirements include maintaining liquidity Coverage Ratio (LCR) and

Net Stable Funding Ratio (NSFR) APRA’s objective in implementing the NSFR. Apart from

these requirements, there are other requirements as well from the Federal Government and

states government as well (Palepu, Healy & Peek, 2013). Therefore, it can be observed that

inherent risk related to unusual pressure on management is at higher side.

d. Nature of the entity’s business: Nature of business also plays an important role in

analysing the inherent risk of the business entity. Bank of Queensland is engaged in the

banking business, therefore, there are various operational transactions, financial transactions

and many statutory requirements to be fulfilled. Nature of business of Bank of Queensland

leads to any inherent risks like operational risk, legal risk and credit risk.

e. Factors affecting the industry in which the entity operates: Risk Factors like market

risk, credit risk, liquidity risk, reputation risk, business risk and operational risk are some

examples that affect business operations of Bank of Queensland. Therefore, it can be

observed that inherent risk because of these factors is at a higher level (Pike, Curtis & Chui,

2013).

Conclusion: It can be concluded that overall inherent risk of Bank of Queensland is at the

higher side because of their nature of the business, the volume of transactions, pressure on

management and other uncontrollable risks related to banking business.

Page | 10

risk is at a controlled level during 2017-2018.

c. Unusual pressure on management (i.e., the directors): Under this inherent risk,

management or directors of business entity is tends to pressurised because of their duties,

responsibilities and because of statutory requirements. Since the Bank of Queensland is a

banking corporation, therefore, there are many statutory requirements that management needs

to take care of. These requirements include maintaining liquidity Coverage Ratio (LCR) and

Net Stable Funding Ratio (NSFR) APRA’s objective in implementing the NSFR. Apart from

these requirements, there are other requirements as well from the Federal Government and

states government as well (Palepu, Healy & Peek, 2013). Therefore, it can be observed that

inherent risk related to unusual pressure on management is at higher side.

d. Nature of the entity’s business: Nature of business also plays an important role in

analysing the inherent risk of the business entity. Bank of Queensland is engaged in the

banking business, therefore, there are various operational transactions, financial transactions

and many statutory requirements to be fulfilled. Nature of business of Bank of Queensland

leads to any inherent risks like operational risk, legal risk and credit risk.

e. Factors affecting the industry in which the entity operates: Risk Factors like market

risk, credit risk, liquidity risk, reputation risk, business risk and operational risk are some

examples that affect business operations of Bank of Queensland. Therefore, it can be

observed that inherent risk because of these factors is at a higher level (Pike, Curtis & Chui,

2013).

Conclusion: It can be concluded that overall inherent risk of Bank of Queensland is at the

higher side because of their nature of the business, the volume of transactions, pressure on

management and other uncontrollable risks related to banking business.

Page | 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3- Risk of Material Misstatement (Inherent Risk) at the Assertion

Level

Net profit

Net profit Profit 2017- $336.0 Million

Profit 2018- $352.0 Million

Why this account balance

is at significant risk of

material misstatement?

Risk of profitability is very significant from a perspective of

investor because one of the primary factors that are evaluated

by the investor before making an investment in the

organisation is a profit generated over the period of time.

Overall profitability of the organisation has decreased in 2018

as compared to 2017 in respect of the fact that overall revenue

generated by the organisation has slightly increased. On the

basis of this analysis, it can be said that profit generated by the

business organisation are very material unit taking decisions by

investors.

Key assertions Completeness- Management should evaluate whether the

company has recorded financial profits effectively and

efficiently or not (Titera, 2013).

Audit procedure to

address the risk

Auditor of the organisation should suggest to management to

make sure that indirect expenses are within the control of

management. Any kind of non-value addition expenses should

be decreased significantly in order to increase net profitability

(Cohen & Simnett¸2014).

Internal control that

would mitigate the risk

Quality control and implementation of policies and procedures

for controlling cost would be one of the most effective internal

controls to make sure that management is able to maintain net

Page | 11

Level

Net profit

Net profit Profit 2017- $336.0 Million

Profit 2018- $352.0 Million

Why this account balance

is at significant risk of

material misstatement?

Risk of profitability is very significant from a perspective of

investor because one of the primary factors that are evaluated

by the investor before making an investment in the

organisation is a profit generated over the period of time.

Overall profitability of the organisation has decreased in 2018

as compared to 2017 in respect of the fact that overall revenue

generated by the organisation has slightly increased. On the

basis of this analysis, it can be said that profit generated by the

business organisation are very material unit taking decisions by

investors.

Key assertions Completeness- Management should evaluate whether the

company has recorded financial profits effectively and

efficiently or not (Titera, 2013).

Audit procedure to

address the risk

Auditor of the organisation should suggest to management to

make sure that indirect expenses are within the control of

management. Any kind of non-value addition expenses should

be decreased significantly in order to increase net profitability

(Cohen & Simnett¸2014).

Internal control that

would mitigate the risk

Quality control and implementation of policies and procedures

for controlling cost would be one of the most effective internal

controls to make sure that management is able to maintain net

Page | 11

profitability over the period of time (Johnstone, Gramling &

Rittenberg, 2013).

Cash flow from operations

Cash flow from

operations

2016- -$1073 million

2017- -$302.0 million

2018- $317.0 million

Why this account balance

is at significant risk of

material misstatement?

Cash management is one of the most fraud-prone areas in

business organisation and it requires effective and efficient

audit procedure for evaluating its accuracy and relevance. In

the last four financial years management of the company has

generated negative cash inflow from business operations.

Negative cash inflows from business operations are one of the

major signs of mismanagement in the organisation (William

Jr., Glover & Prawitt, 2016). It is important that the business

organisation is able to generate positive cash inflow from

business operations as management should be able to generate

cash from its primary business.

Key assertions Accuracy- Auditor should evaluate whether all the transactions

in relation to collection and payment of cash has been recorded

or not.

Audit procedure to

address the risk

Auditor of the organisation should analyse and compare the

transactions recorded in cash with a bank statement of the

company. Reconciliation statement should be prepared by the

auditor and compare it with the reconciliation statement

prepared by management (Coetzee & Lubbe, 2014).

Page | 12

Rittenberg, 2013).

Cash flow from operations

Cash flow from

operations

2016- -$1073 million

2017- -$302.0 million

2018- $317.0 million

Why this account balance

is at significant risk of

material misstatement?

Cash management is one of the most fraud-prone areas in

business organisation and it requires effective and efficient

audit procedure for evaluating its accuracy and relevance. In

the last four financial years management of the company has

generated negative cash inflow from business operations.

Negative cash inflows from business operations are one of the

major signs of mismanagement in the organisation (William

Jr., Glover & Prawitt, 2016). It is important that the business

organisation is able to generate positive cash inflow from

business operations as management should be able to generate

cash from its primary business.

Key assertions Accuracy- Auditor should evaluate whether all the transactions

in relation to collection and payment of cash has been recorded

or not.

Audit procedure to

address the risk

Auditor of the organisation should analyse and compare the

transactions recorded in cash with a bank statement of the

company. Reconciliation statement should be prepared by the

auditor and compare it with the reconciliation statement

prepared by management (Coetzee & Lubbe, 2014).

Page | 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.