Finance Assignment 1: Materiality Analysis - Tabcorp Holdings Limited

VerifiedAdded on 2023/06/07

|6

|989

|338

Report

AI Summary

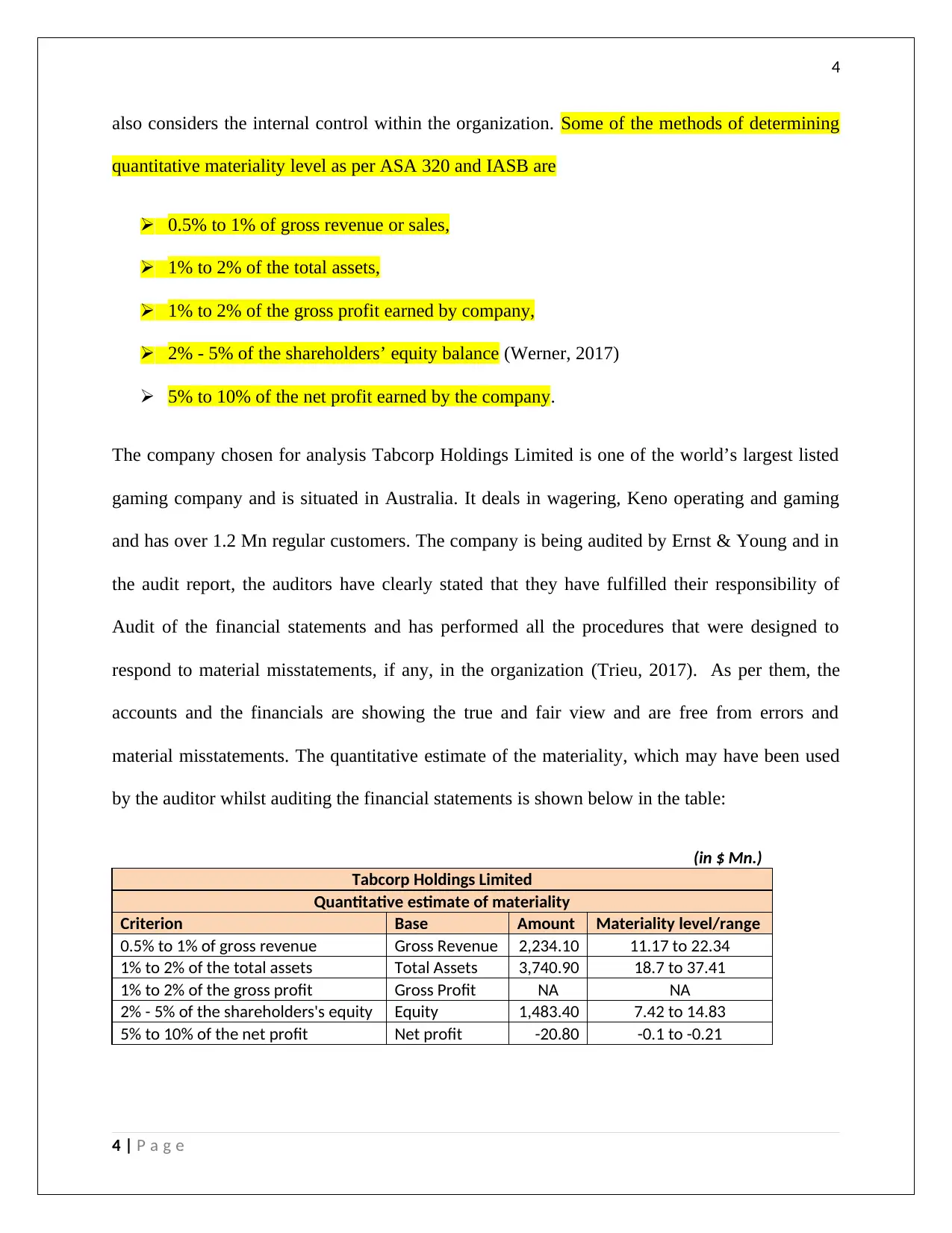

This finance assignment delves into the concept of materiality within the audit of financial statements, as defined by ASA 320. It emphasizes the auditor's responsibility to apply materiality in planning and executing audits, highlighting its role in evaluating the impact of misstatements on financial statements. The report discusses both quantitative and qualitative aspects of materiality, outlining the steps for determining materiality levels using financial metrics like revenue, assets, and equity, as well as qualitative considerations such as disclosures and accounting policies. The assignment uses Tabcorp Holdings Limited as a case study to illustrate the practical application of materiality, providing a quantitative estimate of materiality based on the company's financial data and the auditor's perspective. The report concludes by emphasizing the importance of materiality in providing reasonable assurance to financial statement users and the auditor's professional judgment in determining appropriate materiality levels.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.