Report: Maximizing Shareholder Wealth for ANZ Banking Group Limited

VerifiedAdded on 2023/04/24

|9

|1816

|170

Report

AI Summary

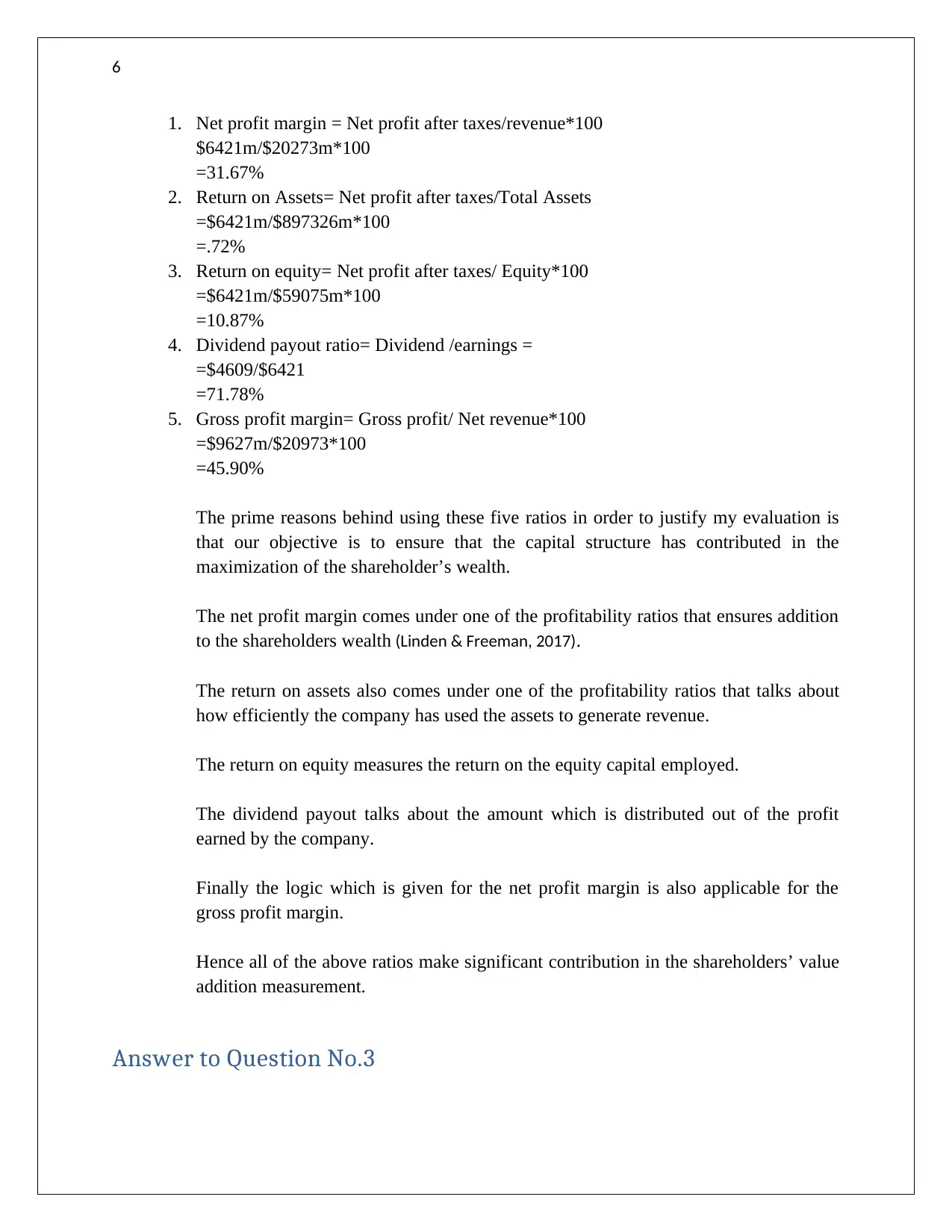

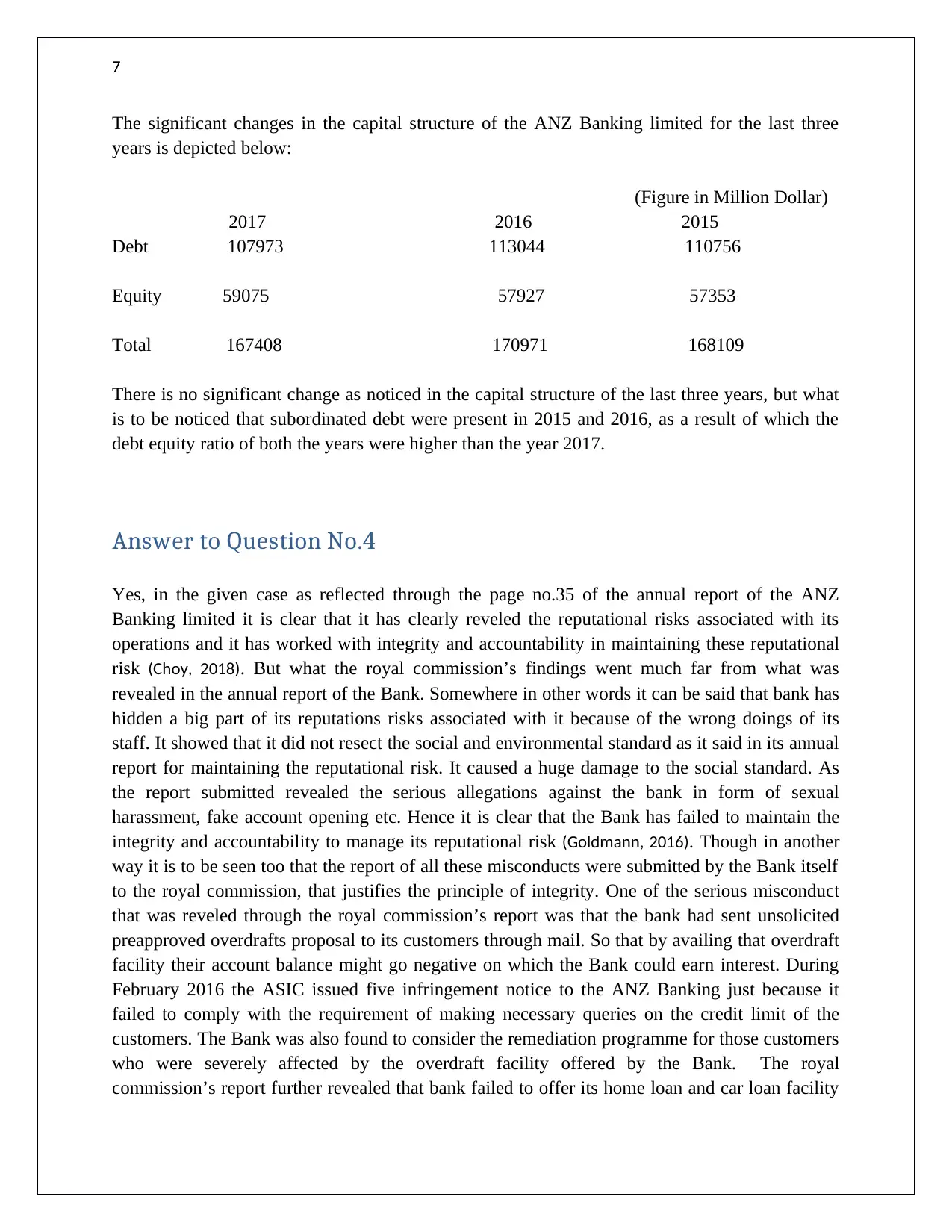

This report, prepared by a finance team member of ANZ Banking Group Limited, evaluates the bank's success in maximizing shareholder wealth. It analyzes the capital structure, categorizing it into debt and equity, and calculates the weighted average cost of capital (WACC). The report utilizes the CAPM model to assess the return on risk and compares ANZ's capital structure with a competitor. It examines key financial ratios like net profit margin, return on assets, and dividend payout ratio to gauge financial performance. The report also investigates changes in the capital structure over three years and critically assesses the adequacy of ANZ's disclosures, particularly concerning reputational risks and the findings of the banking royal commission. The analysis reveals insights into ANZ's financial strategies and their impact on shareholder value, highlighting both strengths and weaknesses in its approach to wealth maximization.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.