Auditing Report: Auditing Negligence, Liability, and Ethical Dilemmas

VerifiedAdded on 2022/08/24

|10

|1936

|33

Report

AI Summary

This report delves into the critical aspects of auditor negligence and liability, examining the legal and ethical responsibilities of auditors. It explores the elements of the tort of negligence, including duty of care, breach of duty, and damage, and analyzes how these elements impact auditors' liabilities to third parties. The report also addresses the concept of audit risk and situations where auditors may issue incorrect opinions despite following proper procedures. Furthermore, it outlines strategies for reducing auditors' liability and discusses the ethical dilemmas auditors face, using the American Accounting Association model to evaluate the ethical implications of documenting material adjustments in working papers. The report provides a comprehensive overview of the challenges and responsibilities auditors encounter in ensuring financial statement integrity.

Running head: AUDITING

Auditing

Name of the Student

Name of the University

Author’s Note

Auditing

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

Question 1........................................................................................................................................2

Introduction..................................................................................................................................2

Requirement 1..............................................................................................................................2

Requirement 2..............................................................................................................................2

Requirement 3..............................................................................................................................3

Requirement 4..............................................................................................................................3

Conclusion...................................................................................................................................3

Question 2........................................................................................................................................4

References........................................................................................................................................8

Table of Contents

Question 1........................................................................................................................................2

Introduction..................................................................................................................................2

Requirement 1..............................................................................................................................2

Requirement 2..............................................................................................................................2

Requirement 3..............................................................................................................................3

Requirement 4..............................................................................................................................3

Conclusion...................................................................................................................................3

Question 2........................................................................................................................................4

References........................................................................................................................................8

2AUDITING

Question 1

Introduction

Negligence from the end of the auditor is a serious offence in the audit profession which

leads to the development of liabilities of the auditors. Auditors’ liabilities create legal

proceedings and lawsuits against the auditors (Alzola, 2017). This report discusses about

different aspects of auditors’ negligence.

Requirement 1

The legislation of tort of negligence provides the right to any third party to sue the auditor

in case he/she involves in breaching the duty of care which creates loss for the third party. Three

elements of the tort of negligence are discussed below:

1. Duty of Care – This element of tort of negligence states that OEV has duty of care towards

Framed as it is responsible for auditing the financial statements of the client and issue

appropriate audit opinion through assessing the acquired audit evidence (Goudkamp, 2017).

2. Breach of Duty – This takes place when OEV fails in fulfilling its duty of care for acting

reasonably in some aspect. Duty of care is violated in case OEV does not act in a reasonable

manner for preventing predictable damages to Framed. More specifically, this can be breached in

case OEV is negligent in the audit of Framed (Rahman & Bremer, 2017).

3. Damage – This can be considered as the loss suffered by Framed because of the incorrect act

of OEV. This also refers to the amount of money that might be paid to Framed as a

compensation for the damage suffered due to the negligence of OEV (Goudkamp, 2017).

4. Relationship between Breach of Duty and Damage – The lost and damage of the plaintiff

must be due the violation of duty of care. In the provided case, the users of the audited financial

statements of Framed like VicBank and other creditors might face loss and damage as there was

material misstatement in sales.

Requirement 2

There are situations where wrong audit opinion is issued by the auditors even after

correctly conducting the audit procedures and this creates audit risk. It means errors in the

Question 1

Introduction

Negligence from the end of the auditor is a serious offence in the audit profession which

leads to the development of liabilities of the auditors. Auditors’ liabilities create legal

proceedings and lawsuits against the auditors (Alzola, 2017). This report discusses about

different aspects of auditors’ negligence.

Requirement 1

The legislation of tort of negligence provides the right to any third party to sue the auditor

in case he/she involves in breaching the duty of care which creates loss for the third party. Three

elements of the tort of negligence are discussed below:

1. Duty of Care – This element of tort of negligence states that OEV has duty of care towards

Framed as it is responsible for auditing the financial statements of the client and issue

appropriate audit opinion through assessing the acquired audit evidence (Goudkamp, 2017).

2. Breach of Duty – This takes place when OEV fails in fulfilling its duty of care for acting

reasonably in some aspect. Duty of care is violated in case OEV does not act in a reasonable

manner for preventing predictable damages to Framed. More specifically, this can be breached in

case OEV is negligent in the audit of Framed (Rahman & Bremer, 2017).

3. Damage – This can be considered as the loss suffered by Framed because of the incorrect act

of OEV. This also refers to the amount of money that might be paid to Framed as a

compensation for the damage suffered due to the negligence of OEV (Goudkamp, 2017).

4. Relationship between Breach of Duty and Damage – The lost and damage of the plaintiff

must be due the violation of duty of care. In the provided case, the users of the audited financial

statements of Framed like VicBank and other creditors might face loss and damage as there was

material misstatement in sales.

Requirement 2

There are situations where wrong audit opinion is issued by the auditors even after

correctly conducting the audit procedures and this creates audit risk. It means errors in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

financial statements cannot be removed even after maintaining all the auditing standards and

principles. For this reason, it is not considered as the accountability of the auditors to detect and

report on these errors. Like this concept, misstatements in sales and receivable cannot be

considered as the responsibility and accountability of the auditor of OEV and this reduces the

possibility of the liquidator of Framed to be successful against the case of OEV (Gimbar, Hansen

& Ozlanski, 2016).

Requirement 3

Followings are the methods that can be used for reducing OEV’s liability to the

liquidators of Framed.

1. The audit firm can enter into the Liability Limitation Agreement so that the liability to

the liquidator of Framed is minimized.

2. The auditors of OEV need to ensure not to be careless while conducting audit which can

reduce the liability to the liquidator of Framed.

3. It is needed for the audit firm to ensure including disclaimer of liability to the Framed by

mentioning it in the report of the auditors. This assists in minimizing the audit liability to

the liquidator of Framed (Gimbar, Hansen & Ozlanski, 2016).

Requirement 4

Financial statements have two kinds of users which are recognized users and restricted

predictable users. Variety of decisions is made by the latter group of users through the use of

audited financial statements; such as financial position, performance and liquidity situation is

assessed by these users while providing loans or issuing new shares (Samsonova-Taddei &

Humphrey, 2015). Since they largely use the audited financial statements for various purposed,

the auditors are responsible and accountable to them unintentionally. As per this concept,

VicBank is the latter types of users of audited financial statements that make the auditor of OEV

responsible to it. This increases the chances of VicBank against OEV.

Conclusion

The above analysis shows that three elements of tort of negligence of auditors are

essential for determining the liability of the auditors in case there is any case of negligence.

financial statements cannot be removed even after maintaining all the auditing standards and

principles. For this reason, it is not considered as the accountability of the auditors to detect and

report on these errors. Like this concept, misstatements in sales and receivable cannot be

considered as the responsibility and accountability of the auditor of OEV and this reduces the

possibility of the liquidator of Framed to be successful against the case of OEV (Gimbar, Hansen

& Ozlanski, 2016).

Requirement 3

Followings are the methods that can be used for reducing OEV’s liability to the

liquidators of Framed.

1. The audit firm can enter into the Liability Limitation Agreement so that the liability to

the liquidator of Framed is minimized.

2. The auditors of OEV need to ensure not to be careless while conducting audit which can

reduce the liability to the liquidator of Framed.

3. It is needed for the audit firm to ensure including disclaimer of liability to the Framed by

mentioning it in the report of the auditors. This assists in minimizing the audit liability to

the liquidator of Framed (Gimbar, Hansen & Ozlanski, 2016).

Requirement 4

Financial statements have two kinds of users which are recognized users and restricted

predictable users. Variety of decisions is made by the latter group of users through the use of

audited financial statements; such as financial position, performance and liquidity situation is

assessed by these users while providing loans or issuing new shares (Samsonova-Taddei &

Humphrey, 2015). Since they largely use the audited financial statements for various purposed,

the auditors are responsible and accountable to them unintentionally. As per this concept,

VicBank is the latter types of users of audited financial statements that make the auditor of OEV

responsible to it. This increases the chances of VicBank against OEV.

Conclusion

The above analysis shows that three elements of tort of negligence of auditors are

essential for determining the liability of the auditors in case there is any case of negligence.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

Moreover, whether a third-party will be able to win against the auditors depend on the nature of

the third party. These are crucial aspects in the tort of negligence.

Question 2

American Accounting Association Model Decision-making process

1. Determine the facts

The facts are that revenue overstatement is

the outcome of a material cut-off error

exposed by Jack; the senior audit manager

has provided direction to Jack not to

document this in the working paper

although the rule is to document any

material adjustment in the working paper.

2. Define the ethical issues

Whether it is needed to document the

material adjustment in revenue and

receivable in the working paper or not is

the main ethical issue in here. The charges

of neglecting the professional

responsibilities and due care would be on

Jack in case he does not document the

material adjustment in the working paper

by agreeing with Bruce (Knechel &

Salterio, 2016).

Moreover, whether a third-party will be able to win against the auditors depend on the nature of

the third party. These are crucial aspects in the tort of negligence.

Question 2

American Accounting Association Model Decision-making process

1. Determine the facts

The facts are that revenue overstatement is

the outcome of a material cut-off error

exposed by Jack; the senior audit manager

has provided direction to Jack not to

document this in the working paper

although the rule is to document any

material adjustment in the working paper.

2. Define the ethical issues

Whether it is needed to document the

material adjustment in revenue and

receivable in the working paper or not is

the main ethical issue in here. The charges

of neglecting the professional

responsibilities and due care would be on

Jack in case he does not document the

material adjustment in the working paper

by agreeing with Bruce (Knechel &

Salterio, 2016).

5AUDITING

American Accounting Association Model Decision-making process

3. Identify the major principles, rules, and values

Followings are the major principle and

values in this case:

1. Integrity – The auditors need to be

honest and straightforward while

conducting the audits; and this puts the

obligation on them to be fair in the auditing

practices (apesb.org.au, 2020).

2. Objectivity – The auditors are also

responsible for ensuring the fact that the

auditing judgments are not compromised

because of conflict of interest, wrong

influence and bias (Espinosa-Pike &

Barrainkua, 2016).

On a whole, the auditors should be aware

of the situations and issues which can

compromise the above-mentioned auditing

principles. Considering the provided case,

these principles and values have major

relevance in this case.

4. Specify the alternatives

There are two alternatives available in this

case:

Alternative 1 – Jack does document the

material adjustments in the working paper

Alternative 2 – Correct actions are taken

by Jack as he mentions the audit

adjustments in the working paper by not

complying with Bruce (Dewi & Dewi,

2018).

American Accounting Association Model Decision-making process

3. Identify the major principles, rules, and values

Followings are the major principle and

values in this case:

1. Integrity – The auditors need to be

honest and straightforward while

conducting the audits; and this puts the

obligation on them to be fair in the auditing

practices (apesb.org.au, 2020).

2. Objectivity – The auditors are also

responsible for ensuring the fact that the

auditing judgments are not compromised

because of conflict of interest, wrong

influence and bias (Espinosa-Pike &

Barrainkua, 2016).

On a whole, the auditors should be aware

of the situations and issues which can

compromise the above-mentioned auditing

principles. Considering the provided case,

these principles and values have major

relevance in this case.

4. Specify the alternatives

There are two alternatives available in this

case:

Alternative 1 – Jack does document the

material adjustments in the working paper

Alternative 2 – Correct actions are taken

by Jack as he mentions the audit

adjustments in the working paper by not

complying with Bruce (Dewi & Dewi,

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

American Accounting Association Model Decision-making process

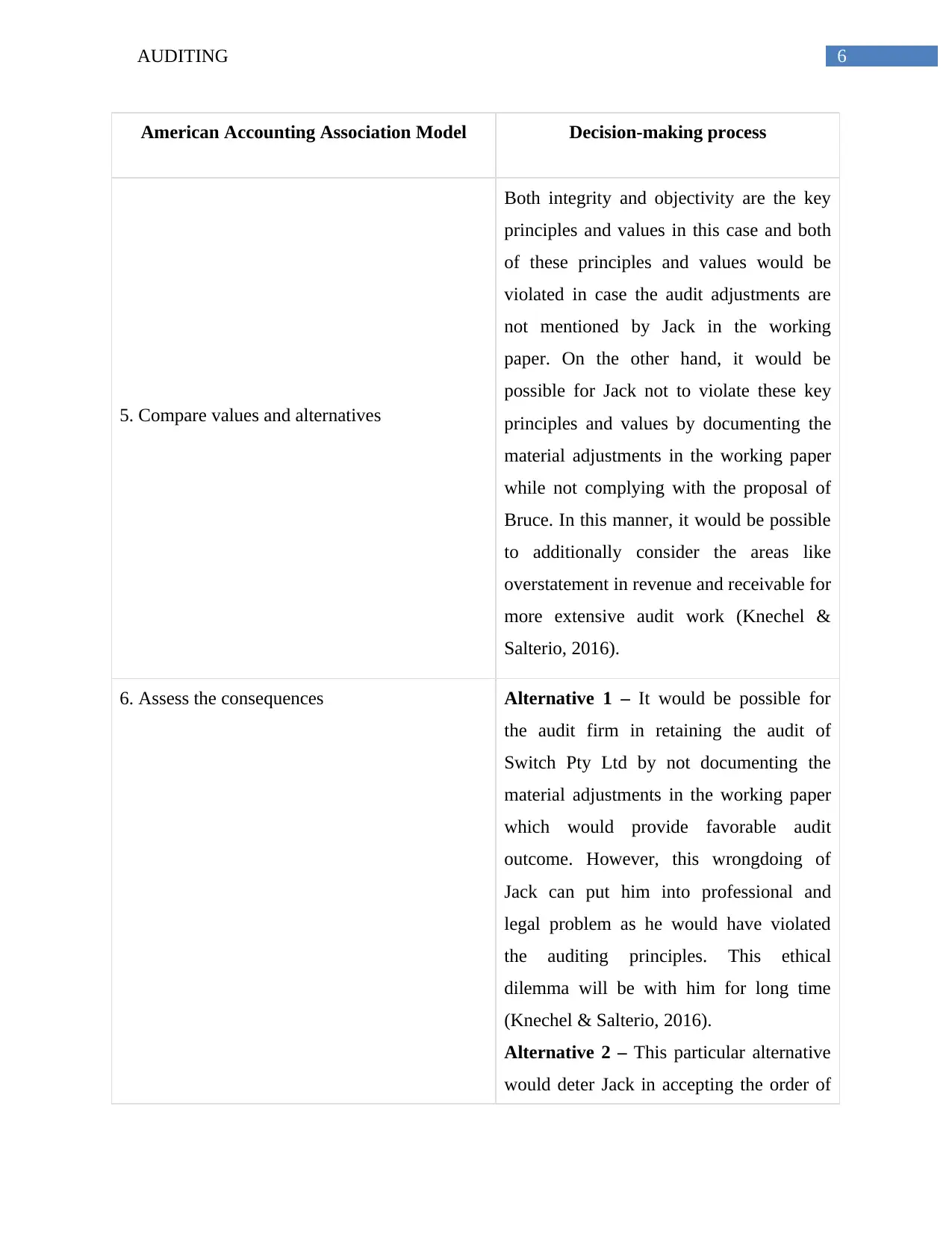

5. Compare values and alternatives

Both integrity and objectivity are the key

principles and values in this case and both

of these principles and values would be

violated in case the audit adjustments are

not mentioned by Jack in the working

paper. On the other hand, it would be

possible for Jack not to violate these key

principles and values by documenting the

material adjustments in the working paper

while not complying with the proposal of

Bruce. In this manner, it would be possible

to additionally consider the areas like

overstatement in revenue and receivable for

more extensive audit work (Knechel &

Salterio, 2016).

6. Assess the consequences Alternative 1 – It would be possible for

the audit firm in retaining the audit of

Switch Pty Ltd by not documenting the

material adjustments in the working paper

which would provide favorable audit

outcome. However, this wrongdoing of

Jack can put him into professional and

legal problem as he would have violated

the auditing principles. This ethical

dilemma will be with him for long time

(Knechel & Salterio, 2016).

Alternative 2 – This particular alternative

would deter Jack in accepting the order of

American Accounting Association Model Decision-making process

5. Compare values and alternatives

Both integrity and objectivity are the key

principles and values in this case and both

of these principles and values would be

violated in case the audit adjustments are

not mentioned by Jack in the working

paper. On the other hand, it would be

possible for Jack not to violate these key

principles and values by documenting the

material adjustments in the working paper

while not complying with the proposal of

Bruce. In this manner, it would be possible

to additionally consider the areas like

overstatement in revenue and receivable for

more extensive audit work (Knechel &

Salterio, 2016).

6. Assess the consequences Alternative 1 – It would be possible for

the audit firm in retaining the audit of

Switch Pty Ltd by not documenting the

material adjustments in the working paper

which would provide favorable audit

outcome. However, this wrongdoing of

Jack can put him into professional and

legal problem as he would have violated

the auditing principles. This ethical

dilemma will be with him for long time

(Knechel & Salterio, 2016).

Alternative 2 – This particular alternative

would deter Jack in accepting the order of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

American Accounting Association Model Decision-making process

Bruce and not to mention the material

adjustments in the working papers of the

audit (Naslmosavi, 2015). Thus, there is a

high probability that the audit-client

relationship between OEV and Switch Pty

Ltd would be affected since this would

eliminate the issue of favorable audit

outcome for the audit client; and OEV may

not receive the next audit tender of Switch

Pty Ltd. The positive is that there would

not be any violation of the auditing

principles of integrity and objectivity by

Jack; and this would probably increase the

goodwill of OEV as an audit firm in the

industry. As a result, it would be possible

to retain public confidence on the auditing

profession (Naslmosavi, 2015).

7. Make your decision

By considering the above alternatives and

discussions, it would be ethical to choose

Alternative 2 where Jack would be required

to document the audit adjustments in the

working paper (Naslmosavi, 2015).

American Accounting Association Model Decision-making process

Bruce and not to mention the material

adjustments in the working papers of the

audit (Naslmosavi, 2015). Thus, there is a

high probability that the audit-client

relationship between OEV and Switch Pty

Ltd would be affected since this would

eliminate the issue of favorable audit

outcome for the audit client; and OEV may

not receive the next audit tender of Switch

Pty Ltd. The positive is that there would

not be any violation of the auditing

principles of integrity and objectivity by

Jack; and this would probably increase the

goodwill of OEV as an audit firm in the

industry. As a result, it would be possible

to retain public confidence on the auditing

profession (Naslmosavi, 2015).

7. Make your decision

By considering the above alternatives and

discussions, it would be ethical to choose

Alternative 2 where Jack would be required

to document the audit adjustments in the

working paper (Naslmosavi, 2015).

8AUDITING

References

Alzola, M. (2017). Beware of the watchdog: Rethinking the normative justification of gatekeeper

liability. Journal of business ethics, 140(4), 705-721.

Apesb.org.au. (2020). APES 110 Code of Ethics for Professional Accountants (including

Independence Standards). Retrieved 18 March 2020, from

https://www.apesb.org.au/uploads/home/02112018000152_APES_110_Restructured_Co

de_Nov_2018.pdf

ARDELEAN, A. (2015). Study regarding the Clarification of Ethical Dilemmas in Financial

Audit. Audit Financiar, 13(125).

Dewi, I. G. A. A. P., & Dewi, P. P. (2018). Big Five Personality, Ethical Sensitivity, and

Performance of Auditors. International research journal of management, IT and social

sciences, 5(2), 195-209.

Espinosa-Pike, M., & Barrainkua, I. (2016). An exploratory study of the pressures and ethical

dilemmas in the audit conflict. Revista de Contabilidad, 19(1), 10-20.

Gimbar, C., Hansen, B., & Ozlanski, M. E. (2016). Early evidence on the effects of critical audit

matters on auditor liability. Current Issues in Auditing, 10(1), A24-A33.

Gimbar, C., Hansen, B., & Ozlanski, M. E. (2016). The effects of critical audit matter paragraphs

and accounting standard precision on auditor liability. The Accounting Review, 91(6),

1629-1646.

Goudkamp, J. (2017). The contributory negligence doctrine: four commercial law

problems. Lloyd's Maritime and Commercial Law Quarterly, Forthcoming.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Taylor & Francis.

Naslmosavi, S. (2015). The Effect of Ethics on Auditor's Judgment in Ethical Dilemma

Conditions: Evidence from Iranian Auditors. Available at SSRN 2584308.

References

Alzola, M. (2017). Beware of the watchdog: Rethinking the normative justification of gatekeeper

liability. Journal of business ethics, 140(4), 705-721.

Apesb.org.au. (2020). APES 110 Code of Ethics for Professional Accountants (including

Independence Standards). Retrieved 18 March 2020, from

https://www.apesb.org.au/uploads/home/02112018000152_APES_110_Restructured_Co

de_Nov_2018.pdf

ARDELEAN, A. (2015). Study regarding the Clarification of Ethical Dilemmas in Financial

Audit. Audit Financiar, 13(125).

Dewi, I. G. A. A. P., & Dewi, P. P. (2018). Big Five Personality, Ethical Sensitivity, and

Performance of Auditors. International research journal of management, IT and social

sciences, 5(2), 195-209.

Espinosa-Pike, M., & Barrainkua, I. (2016). An exploratory study of the pressures and ethical

dilemmas in the audit conflict. Revista de Contabilidad, 19(1), 10-20.

Gimbar, C., Hansen, B., & Ozlanski, M. E. (2016). Early evidence on the effects of critical audit

matters on auditor liability. Current Issues in Auditing, 10(1), A24-A33.

Gimbar, C., Hansen, B., & Ozlanski, M. E. (2016). The effects of critical audit matter paragraphs

and accounting standard precision on auditor liability. The Accounting Review, 91(6),

1629-1646.

Goudkamp, J. (2017). The contributory negligence doctrine: four commercial law

problems. Lloyd's Maritime and Commercial Law Quarterly, Forthcoming.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Taylor & Francis.

Naslmosavi, S. (2015). The Effect of Ethics on Auditor's Judgment in Ethical Dilemma

Conditions: Evidence from Iranian Auditors. Available at SSRN 2584308.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

Rahman, K. M., & Bremer, M. (2017). The Implications of The Toshiba Accounting Scandal for

auditor Liabilities in Japan. Nazan University, (1704), 1-17.

Samsonova-Taddei, A., & Humphrey, C. (2015). Risk and the construction of a European audit

policy agenda: The case of auditor liability. Accounting, Organizations and Society, 41,

55-72.

Rahman, K. M., & Bremer, M. (2017). The Implications of The Toshiba Accounting Scandal for

auditor Liabilities in Japan. Nazan University, (1704), 1-17.

Samsonova-Taddei, A., & Humphrey, C. (2015). Risk and the construction of a European audit

policy agenda: The case of auditor liability. Accounting, Organizations and Society, 41,

55-72.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.