Advanced Taxation Essay: UK Measures to Avoid Tax Avoidance

VerifiedAdded on 2022/10/10

|12

|3511

|74

Essay

AI Summary

This essay critically evaluates the UK's approach to tax avoidance, focusing on the General Anti-Abuse Rule (GAAR) and Base Erosion and Profit Shifting (BEPS). It examines the attitudes towards tax avoidance in recent years, highlighting the increasing public scrutiny and the UK government's response. The essay analyzes HM Revenue & Customs' (HMRC) strategies, including the implementation of GAAR and other measures to manage the risk of tax avoidance. Furthermore, it assesses the impact of BEPS and the reactions of both the UK and international governments. The study explores the measures taken by the UK government to prevent tax avoidance, the necessity of the assessment of GAAR, and the role of HMRC in managing tax-related issues. The essay also touches upon the role of major audit firms in facilitating tax avoidance schemes and the impact of tax avoidance on the UK economy. It emphasizes the importance of tax planning and the significance of GAAR in curbing abusive tax arrangements and protecting the interests of loyal taxpayers. The essay concludes by examining the BEPS strategy adopted by individuals and multinational corporations and the framework implemented by OECD to tackle tax avoidance.

Running head: MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

Name of the Student

Name of the University

Author Note

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

The recent trends in business incidence of tax avoidance has increased. According to the

information of UK government tax avoidance among the individuals and the well-known

multinational corporations has become the usual scenario. Since tax avoidance is not an act of

crime in the eye of law thus it would be difficult for the government to control the possibility

of tax avoidance. The consequence of tax avoidance is beneficial from the view point of the

tax payer but it is not a positive aspect for the government of any country because it decrease

the amount of revenue earned from tax and distort the economic growth of the country.

Therefore, it can be said that tax avoidance is not only a method to reduce the tax expenses

but also the exploitation of the weakness and loopholes of the rules and regulation of the tax

laws. The study basically defines the measures taken by the government of United Kingdom

to prevent the possibility of tax avoidance and the necessity of the assessment of the GAAR.

There are three most significant ways to reduce the burden of tax rather save the

taxable income such as tax evasion, tax planning and tax avoidance. The most relevant and

legitimate manner of reducing the payment of tax are tax planning and tax avoidance. The

concept of tax avoidance refers to the tactful arrangement of certain incidents that may help

to reduce the liability to pay tax without accepting any illegal ways such as availing the tax

privileges, exemptions and tax rebates (Liu Schmidt-Eisenlohr and Guo 2017). The practice

of tax avoidance reduce the basic purpose of implementation of the rule and regulations of

Tax law. According to the economic condition of a country tax avoidance is regarded as one

of the most drastic situation. Since funds collected thorough implementation of tax on

individuals and business firms is the main source of income for the government to run the

economy of a particular country. Governments spend the amount of tax in different sectors

like social security, education, health, defence, transport, development of industrial sectors,

development of agricultural sectors, establishing proper infrastructure and implementation of

other developmental schemes (Ferry, Eckersley and Van Dooren, 2015). Therefore, in other

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

The recent trends in business incidence of tax avoidance has increased. According to the

information of UK government tax avoidance among the individuals and the well-known

multinational corporations has become the usual scenario. Since tax avoidance is not an act of

crime in the eye of law thus it would be difficult for the government to control the possibility

of tax avoidance. The consequence of tax avoidance is beneficial from the view point of the

tax payer but it is not a positive aspect for the government of any country because it decrease

the amount of revenue earned from tax and distort the economic growth of the country.

Therefore, it can be said that tax avoidance is not only a method to reduce the tax expenses

but also the exploitation of the weakness and loopholes of the rules and regulation of the tax

laws. The study basically defines the measures taken by the government of United Kingdom

to prevent the possibility of tax avoidance and the necessity of the assessment of the GAAR.

There are three most significant ways to reduce the burden of tax rather save the

taxable income such as tax evasion, tax planning and tax avoidance. The most relevant and

legitimate manner of reducing the payment of tax are tax planning and tax avoidance. The

concept of tax avoidance refers to the tactful arrangement of certain incidents that may help

to reduce the liability to pay tax without accepting any illegal ways such as availing the tax

privileges, exemptions and tax rebates (Liu Schmidt-Eisenlohr and Guo 2017). The practice

of tax avoidance reduce the basic purpose of implementation of the rule and regulations of

Tax law. According to the economic condition of a country tax avoidance is regarded as one

of the most drastic situation. Since funds collected thorough implementation of tax on

individuals and business firms is the main source of income for the government to run the

economy of a particular country. Governments spend the amount of tax in different sectors

like social security, education, health, defence, transport, development of industrial sectors,

development of agricultural sectors, establishing proper infrastructure and implementation of

other developmental schemes (Ferry, Eckersley and Van Dooren, 2015). Therefore, in other

2

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

words tax avoidance is a curse for the prospect and growth of a country (Riedel 2018).

Usually to save the taxable income individuals or the multinational corporations often

introduce the fake and artificial transaction purposefully to curb the rules and regulations of

the law. The scheme of avoiding the payment of tax is not always a boon for the taxpayers,

those who follows the trick to save the taxable income often end up by paying more along

with fines and penalties. According to the report produced by UK Houses Of Commons

Committee of Public Accounts in the years 2010-11 and 2014-15 the big four audit firms

such as PwC, Ernst & Young Delloitte and KPMG have played a crucial role in creating the

path of avoiding the payment of tax. The recent reports states that these firms provides tax

related advices that helps the multinational corporations to prepare an artificial presentation

on tax that reduce the burden of tax as per UK Government (Sikka 2015 ). According to the

annual report of ‘Her Majesty’s Revenue and Customs’ (HMRC) in the year ending 2014

states the main reason of tax gap are tax avoidance amounting to 35 billion UK Pound and

tax evasion amounting to 4.1 billion UK Pound (Sikka 2015 ).

The increasing trend of tax avoidance has changed the attitude of UK government and

evaluate the reasons of the increase in tax avoidance among the individuals and large

multinational corporations. The aim of UK government is to implement a fair system of

payment of tax within the country to avoid conflictions. As the revolution of technology has

changed the world of business and trade it is important for a government to change their

system, rules and provisions of paying tax accordingly. As per the knowledge of UK

government HMRC is the non-ministerial department that is responsible for collecting tax on

behalf of the government. The HMRC explains that the success of taxation system depends

on the prudence of tax payer such as paying adequate amount of tax, filling of return with in

time and complying the provisions of tax (Lord and Culling 2016). HMRC has taken several

measures to control the nature of tax avoidance among the individuals and business

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

words tax avoidance is a curse for the prospect and growth of a country (Riedel 2018).

Usually to save the taxable income individuals or the multinational corporations often

introduce the fake and artificial transaction purposefully to curb the rules and regulations of

the law. The scheme of avoiding the payment of tax is not always a boon for the taxpayers,

those who follows the trick to save the taxable income often end up by paying more along

with fines and penalties. According to the report produced by UK Houses Of Commons

Committee of Public Accounts in the years 2010-11 and 2014-15 the big four audit firms

such as PwC, Ernst & Young Delloitte and KPMG have played a crucial role in creating the

path of avoiding the payment of tax. The recent reports states that these firms provides tax

related advices that helps the multinational corporations to prepare an artificial presentation

on tax that reduce the burden of tax as per UK Government (Sikka 2015 ). According to the

annual report of ‘Her Majesty’s Revenue and Customs’ (HMRC) in the year ending 2014

states the main reason of tax gap are tax avoidance amounting to 35 billion UK Pound and

tax evasion amounting to 4.1 billion UK Pound (Sikka 2015 ).

The increasing trend of tax avoidance has changed the attitude of UK government and

evaluate the reasons of the increase in tax avoidance among the individuals and large

multinational corporations. The aim of UK government is to implement a fair system of

payment of tax within the country to avoid conflictions. As the revolution of technology has

changed the world of business and trade it is important for a government to change their

system, rules and provisions of paying tax accordingly. As per the knowledge of UK

government HMRC is the non-ministerial department that is responsible for collecting tax on

behalf of the government. The HMRC explains that the success of taxation system depends

on the prudence of tax payer such as paying adequate amount of tax, filling of return with in

time and complying the provisions of tax (Lord and Culling 2016). HMRC has taken several

measures to control the nature of tax avoidance among the individuals and business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

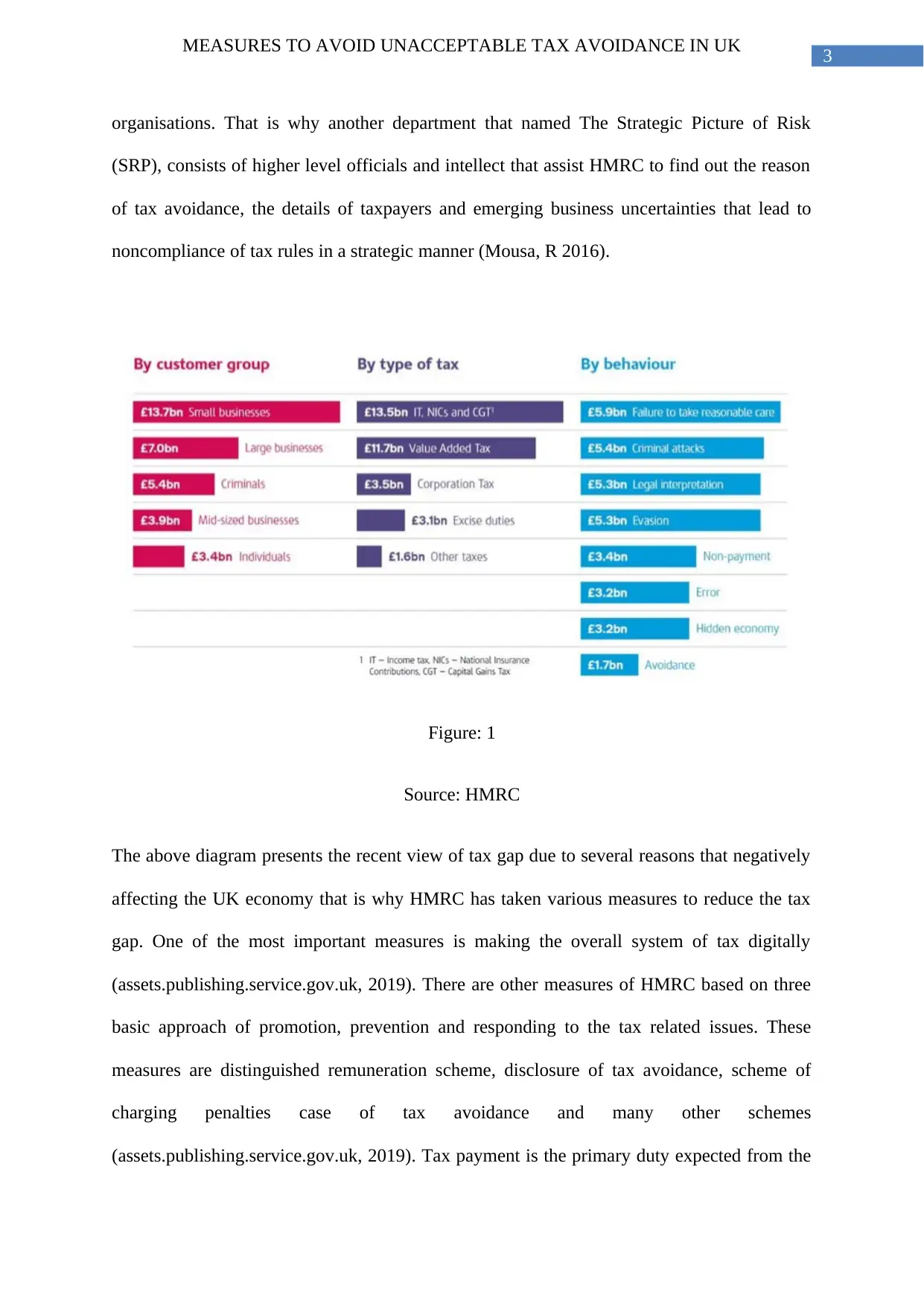

organisations. That is why another department that named The Strategic Picture of Risk

(SRP), consists of higher level officials and intellect that assist HMRC to find out the reason

of tax avoidance, the details of taxpayers and emerging business uncertainties that lead to

noncompliance of tax rules in a strategic manner (Mousa, R 2016).

Figure: 1

Source: HMRC

The above diagram presents the recent view of tax gap due to several reasons that negatively

affecting the UK economy that is why HMRC has taken various measures to reduce the tax

gap. One of the most important measures is making the overall system of tax digitally

(assets.publishing.service.gov.uk, 2019). There are other measures of HMRC based on three

basic approach of promotion, prevention and responding to the tax related issues. These

measures are distinguished remuneration scheme, disclosure of tax avoidance, scheme of

charging penalties case of tax avoidance and many other schemes

(assets.publishing.service.gov.uk, 2019). Tax payment is the primary duty expected from the

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

organisations. That is why another department that named The Strategic Picture of Risk

(SRP), consists of higher level officials and intellect that assist HMRC to find out the reason

of tax avoidance, the details of taxpayers and emerging business uncertainties that lead to

noncompliance of tax rules in a strategic manner (Mousa, R 2016).

Figure: 1

Source: HMRC

The above diagram presents the recent view of tax gap due to several reasons that negatively

affecting the UK economy that is why HMRC has taken various measures to reduce the tax

gap. One of the most important measures is making the overall system of tax digitally

(assets.publishing.service.gov.uk, 2019). There are other measures of HMRC based on three

basic approach of promotion, prevention and responding to the tax related issues. These

measures are distinguished remuneration scheme, disclosure of tax avoidance, scheme of

charging penalties case of tax avoidance and many other schemes

(assets.publishing.service.gov.uk, 2019). Tax payment is the primary duty expected from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

business organisations and from the individuals, rather it is the part of corporate social

responsibility for the business organisation (Campbell and Helleloid 2016). The main reason

of avoiding tax liability among the individual and multinational corporations are the problem

of double taxation, complex rules and regulations to be followed, the process of maintaining

records is time consuming and costly moreover those who pay tax on a regular basis could

get proper document that would support the payment of tax (Riedel 2018). The entrepreneurs

of recent competitive business world find it difficult that is why the incidence of tax

avoidance has increased.

The term GAAR means General anti-avoidance rule. The provisions of GAAR came

into action in Finance Act of UK in the year 2013 (commons.allard.ubc.ca, 2017). The aim

and objective of the report of GAAR is to prepare a guidelines that would reduce the tax gap

and make the citizens of the UK aware of payment of tax. Moreover the rules and regulations

of GAAR detains the tax payers to engage themselves into illegal agreements along with

others who promote such illegal activities. If a taxpayer disagrees and tries to curb the

provisions of GAAR, it will take immediate steps that permits the higher officials to adjust

the amount of tax which is justifiable and reasonable in all aspect. The recent obstacles

prevailing in the UK market states the problem of double taxation, overriding of non-

deductible losses and huge cost of compliance hinders the growth and increase the possibility

of arising tax avoidance (siepweb.it, 2015). From the very beginning the problem of tax

avoidance came into existence in the economy of UK which can be defined with the help of

famous a case study named ‘Ramsay Principle’ rather W.T. Ramsay LTD versus Inland

Revenue Commissioners, where it explains that W.T. Ramsey Ltd earned gains from capital,

chargeable under capital gain tax. The company wanted to avoid the burden of tax that is why

it had created fake capital loss to achieve the benefit of exemption (Knol et al. 2017). After

that the custom of tax avoidance has increase rapidly. According to the Patrick Cannon one of

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

business organisations and from the individuals, rather it is the part of corporate social

responsibility for the business organisation (Campbell and Helleloid 2016). The main reason

of avoiding tax liability among the individual and multinational corporations are the problem

of double taxation, complex rules and regulations to be followed, the process of maintaining

records is time consuming and costly moreover those who pay tax on a regular basis could

get proper document that would support the payment of tax (Riedel 2018). The entrepreneurs

of recent competitive business world find it difficult that is why the incidence of tax

avoidance has increased.

The term GAAR means General anti-avoidance rule. The provisions of GAAR came

into action in Finance Act of UK in the year 2013 (commons.allard.ubc.ca, 2017). The aim

and objective of the report of GAAR is to prepare a guidelines that would reduce the tax gap

and make the citizens of the UK aware of payment of tax. Moreover the rules and regulations

of GAAR detains the tax payers to engage themselves into illegal agreements along with

others who promote such illegal activities. If a taxpayer disagrees and tries to curb the

provisions of GAAR, it will take immediate steps that permits the higher officials to adjust

the amount of tax which is justifiable and reasonable in all aspect. The recent obstacles

prevailing in the UK market states the problem of double taxation, overriding of non-

deductible losses and huge cost of compliance hinders the growth and increase the possibility

of arising tax avoidance (siepweb.it, 2015). From the very beginning the problem of tax

avoidance came into existence in the economy of UK which can be defined with the help of

famous a case study named ‘Ramsay Principle’ rather W.T. Ramsay LTD versus Inland

Revenue Commissioners, where it explains that W.T. Ramsey Ltd earned gains from capital,

chargeable under capital gain tax. The company wanted to avoid the burden of tax that is why

it had created fake capital loss to achieve the benefit of exemption (Knol et al. 2017). After

that the custom of tax avoidance has increase rapidly. According to the Patrick Cannon one of

5

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

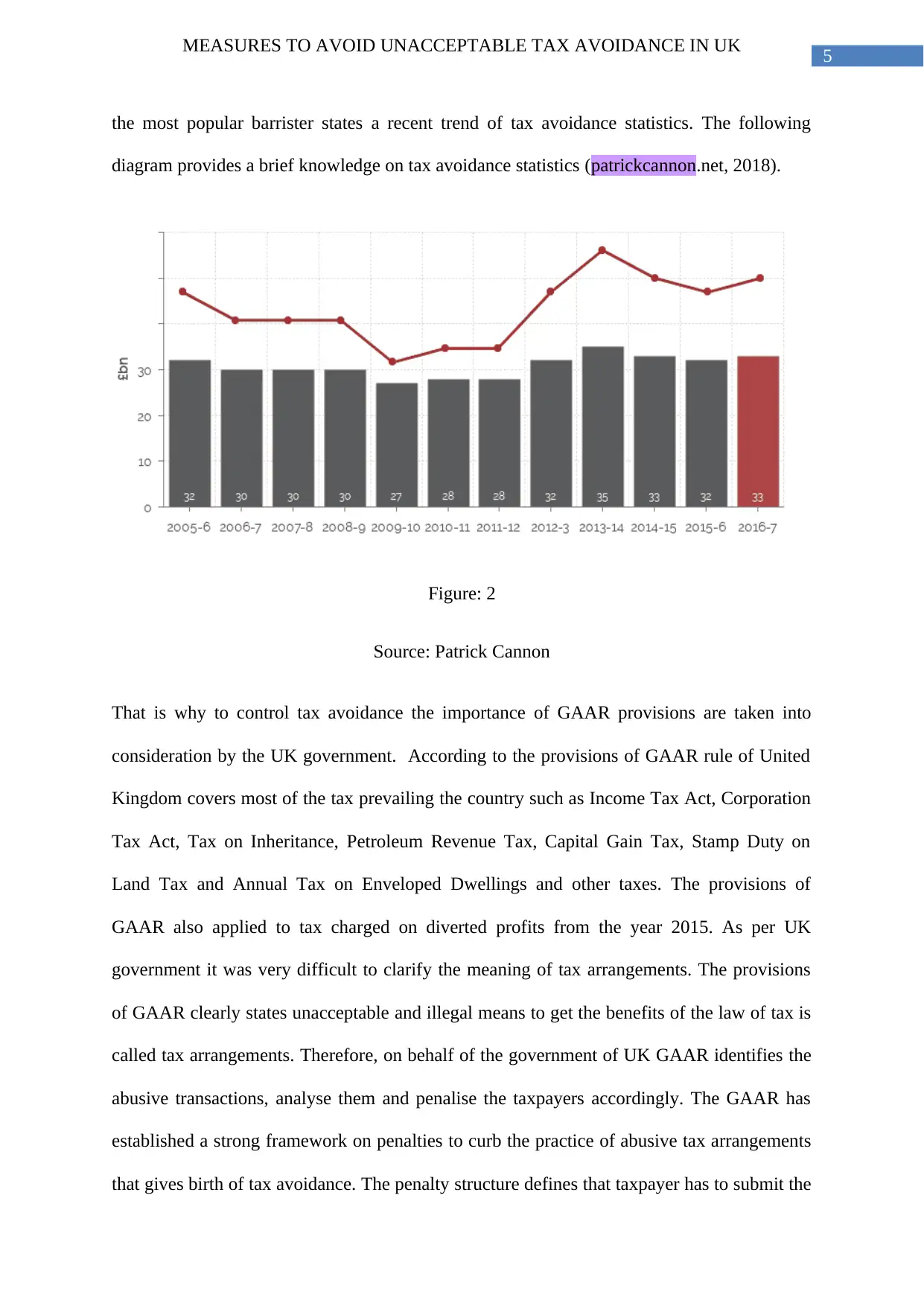

the most popular barrister states a recent trend of tax avoidance statistics. The following

diagram provides a brief knowledge on tax avoidance statistics (patrickcannon.net, 2018).

Figure: 2

Source: Patrick Cannon

That is why to control tax avoidance the importance of GAAR provisions are taken into

consideration by the UK government. According to the provisions of GAAR rule of United

Kingdom covers most of the tax prevailing the country such as Income Tax Act, Corporation

Tax Act, Tax on Inheritance, Petroleum Revenue Tax, Capital Gain Tax, Stamp Duty on

Land Tax and Annual Tax on Enveloped Dwellings and other taxes. The provisions of

GAAR also applied to tax charged on diverted profits from the year 2015. As per UK

government it was very difficult to clarify the meaning of tax arrangements. The provisions

of GAAR clearly states unacceptable and illegal means to get the benefits of the law of tax is

called tax arrangements. Therefore, on behalf of the government of UK GAAR identifies the

abusive transactions, analyse them and penalise the taxpayers accordingly. The GAAR has

established a strong framework on penalties to curb the practice of abusive tax arrangements

that gives birth of tax avoidance. The penalty structure defines that taxpayer has to submit the

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

the most popular barrister states a recent trend of tax avoidance statistics. The following

diagram provides a brief knowledge on tax avoidance statistics (patrickcannon.net, 2018).

Figure: 2

Source: Patrick Cannon

That is why to control tax avoidance the importance of GAAR provisions are taken into

consideration by the UK government. According to the provisions of GAAR rule of United

Kingdom covers most of the tax prevailing the country such as Income Tax Act, Corporation

Tax Act, Tax on Inheritance, Petroleum Revenue Tax, Capital Gain Tax, Stamp Duty on

Land Tax and Annual Tax on Enveloped Dwellings and other taxes. The provisions of

GAAR also applied to tax charged on diverted profits from the year 2015. As per UK

government it was very difficult to clarify the meaning of tax arrangements. The provisions

of GAAR clearly states unacceptable and illegal means to get the benefits of the law of tax is

called tax arrangements. Therefore, on behalf of the government of UK GAAR identifies the

abusive transactions, analyse them and penalise the taxpayers accordingly. The GAAR has

established a strong framework on penalties to curb the practice of abusive tax arrangements

that gives birth of tax avoidance. The penalty structure defines that taxpayer has to submit the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

return on tax without any error and flaws. It also states that it is the duty of the assesse to

disclose if the person has entered in the abusive tax arrangement. If the assesse fails to

comply with the provision will be liable for penalties. The provision relating to penalty came

into action on 15th of September 2016 (gaar_parts_a_b_c_2018, 2018).Therefore as per the

GAAR guideline, it is a part of all the tax laws of UK, the taxpayers should abide by the

provisions of GAAR while preparing the return on self-assessment .The necessity of GAAR

is not only for identifying and analysing the reasons tax avoidance but also it protects

interests the loyal taxpayers. The prevailing turbulence of double taxation, overriding of tax

on non-deductible losses and the tax gap have brutally affected the honest taxpayers. Thus,

GAAR has taken several policies to protect them, which requires the HMRC to take

necessary actions regarding abusive tax arrangements, conduct the examination of double

reasonableness, establishment of the advisory panel and other relevant measures (Helliwell

2018). To make the rules of GAAR more successful the management monitors whether

HMRC applies the rules on a regular basis. The legislator of GAAR states that counteraction

to retaliate the practice of tax avoidance should be taken by the HMRC after obtaining the

notice of consent from them. It also clarifies that when the officials of HMRC takes the help

of GAAR rule in detecting tax arrangements a prior application should be produced to the

advisory panel. Since HMRC takes the responsibility of tax collection on behalf of the

government, the management of GAAR allows HMRC to take the immediate steps like the

legislator of GAAR to stop the assesse to take the benefit of tax derived from tax illegal tax

arrangements. However, the GAAR guidelines explains that when the provisional

counterattack is done to top the unacceptable benefit of tax avoidance it has to take the

approval from the legislator of GAAR along with the responsible management of HMRC

(Jones 2015).

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

return on tax without any error and flaws. It also states that it is the duty of the assesse to

disclose if the person has entered in the abusive tax arrangement. If the assesse fails to

comply with the provision will be liable for penalties. The provision relating to penalty came

into action on 15th of September 2016 (gaar_parts_a_b_c_2018, 2018).Therefore as per the

GAAR guideline, it is a part of all the tax laws of UK, the taxpayers should abide by the

provisions of GAAR while preparing the return on self-assessment .The necessity of GAAR

is not only for identifying and analysing the reasons tax avoidance but also it protects

interests the loyal taxpayers. The prevailing turbulence of double taxation, overriding of tax

on non-deductible losses and the tax gap have brutally affected the honest taxpayers. Thus,

GAAR has taken several policies to protect them, which requires the HMRC to take

necessary actions regarding abusive tax arrangements, conduct the examination of double

reasonableness, establishment of the advisory panel and other relevant measures (Helliwell

2018). To make the rules of GAAR more successful the management monitors whether

HMRC applies the rules on a regular basis. The legislator of GAAR states that counteraction

to retaliate the practice of tax avoidance should be taken by the HMRC after obtaining the

notice of consent from them. It also clarifies that when the officials of HMRC takes the help

of GAAR rule in detecting tax arrangements a prior application should be produced to the

advisory panel. Since HMRC takes the responsibility of tax collection on behalf of the

government, the management of GAAR allows HMRC to take the immediate steps like the

legislator of GAAR to stop the assesse to take the benefit of tax derived from tax illegal tax

arrangements. However, the GAAR guidelines explains that when the provisional

counterattack is done to top the unacceptable benefit of tax avoidance it has to take the

approval from the legislator of GAAR along with the responsible management of HMRC

(Jones 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

The term Base erosion and profit shifting (BEPS) means the strategy of arrangements

of tax adopted by the individuals and mostly the large multinational corporations to misuse

the gap of tax law to save taxable income (Brauner 2014). It was introduced in the year 2013

by OECD (www.oecd.org, 2019). According to the information of OECD, most of the

government of developing countries collect their funds from corporate income tax but the

practice of BEPS affect the country excessively. The strategy of BEPS decreases the revenue

of countries amounting to USD 100-240 billion (www.oecd.org, 2019). As per the

information of OECD, it has prepared a strong framework relating to BEPS which provides

assistance to 130 countries all over the world along with 15 measures that would successfully

tackle the reasons and possibilities of tax avoidance. The aim of this framework is to improve

the rules and regulations of the system of tax and maintain the transparency to enhance the

economic development. Though the recent economic dilemma and loss of government

revenue indicates tax avoidance is unacceptable but it is not always illegal (Birks 2017). Thus

the multinational corporations that operates in foreign countries can use the system of BEPS

to achieve competitive advantage while conducting the course of business within the

domestic territory. Therefore, to control the extremity of tax avoidance and control the

problems of tax gap within the economy the package of BEPS has disclosed several policies

that would provide assistance of the government. OECD, G20 countries and other developing

countries have involved in the proper implementation of the package of BEPS and actively

took part in improvement of the standard of anti-BEPS internationally to create economic

value and implement rules continuously. The BEPS package has taken several actions that

retaliate the unauthorised arrangements of tax. The sixth action plan of BEPS suggest specific

rules that rectify the abuse of treaty (www.oecd.org, 2019). On the other hand the thirteenth

action of BEPS also explains that the multinational firms need to prepare a report on income,

profit earned for a financial year and the amount of taxes paid and activities on economy

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

The term Base erosion and profit shifting (BEPS) means the strategy of arrangements

of tax adopted by the individuals and mostly the large multinational corporations to misuse

the gap of tax law to save taxable income (Brauner 2014). It was introduced in the year 2013

by OECD (www.oecd.org, 2019). According to the information of OECD, most of the

government of developing countries collect their funds from corporate income tax but the

practice of BEPS affect the country excessively. The strategy of BEPS decreases the revenue

of countries amounting to USD 100-240 billion (www.oecd.org, 2019). As per the

information of OECD, it has prepared a strong framework relating to BEPS which provides

assistance to 130 countries all over the world along with 15 measures that would successfully

tackle the reasons and possibilities of tax avoidance. The aim of this framework is to improve

the rules and regulations of the system of tax and maintain the transparency to enhance the

economic development. Though the recent economic dilemma and loss of government

revenue indicates tax avoidance is unacceptable but it is not always illegal (Birks 2017). Thus

the multinational corporations that operates in foreign countries can use the system of BEPS

to achieve competitive advantage while conducting the course of business within the

domestic territory. Therefore, to control the extremity of tax avoidance and control the

problems of tax gap within the economy the package of BEPS has disclosed several policies

that would provide assistance of the government. OECD, G20 countries and other developing

countries have involved in the proper implementation of the package of BEPS and actively

took part in improvement of the standard of anti-BEPS internationally to create economic

value and implement rules continuously. The BEPS package has taken several actions that

retaliate the unauthorised arrangements of tax. The sixth action plan of BEPS suggest specific

rules that rectify the abuse of treaty (www.oecd.org, 2019). On the other hand the thirteenth

action of BEPS also explains that the multinational firms need to prepare a report on income,

profit earned for a financial year and the amount of taxes paid and activities on economy

8

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

(www.oecd.org, 2019). Further the fourteenth action of BEPS package requires to improvise

the pre-determined resolutions on tax related conflictions arises among the different

jurisdiction (www.oecd.org, 2019). Therefore, it can be said that BEPS is not only a negative

aspect for particular country’s economy but also the BEPS package and its actions are

positively dealing in controlling the tax disputes. In the recent economic turbulence the UK

and the international government have reacted against the practice of BEPS. There are several

reforms taken place to retaliate the continuous decrease in revenue which can be explained

with the help of Google and Amazon. As a globally reputed firms Google and Amazon

attacked the headlines for avoiding payment of tax. According to the UK government the

practice became the habit from the perspective of the management of Google and Amazon.

Though these companies had complied the UK tax structure but the increased complications

in the system of UK tax made them to avoid the payment of tax taking the help of BEPS. As

per record of UK government Amazon paid £1.8 billion as tax expense against sales of £3.35

billion, on the other hand Google paid only £6 million where the total turnover amounting to

£395million (bbc.com, 2013). These MNCs able to transferred the profit to other jurisdiction

where rate of tax is low in the form of assets or associated risks (erasmuslawreview.nl, 2017).

From the above discussion it can be said the government has taken several policies to

analyse and detect the tax gap. It is the foremost duty of the government to take reasonable

steps to control the increasing trend of tax avoidance. Since tax avoidance is not illegal in the

eye of law individuals and MNCs take the undue advantages of the tax law which is very

difficult for the government to detect the unacceptable arrangements. Therefore, it can be said

that government should abide by the provisions of GAAR, rules of HMRC and the actions of

BEPS package strictly.

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

(www.oecd.org, 2019). Further the fourteenth action of BEPS package requires to improvise

the pre-determined resolutions on tax related conflictions arises among the different

jurisdiction (www.oecd.org, 2019). Therefore, it can be said that BEPS is not only a negative

aspect for particular country’s economy but also the BEPS package and its actions are

positively dealing in controlling the tax disputes. In the recent economic turbulence the UK

and the international government have reacted against the practice of BEPS. There are several

reforms taken place to retaliate the continuous decrease in revenue which can be explained

with the help of Google and Amazon. As a globally reputed firms Google and Amazon

attacked the headlines for avoiding payment of tax. According to the UK government the

practice became the habit from the perspective of the management of Google and Amazon.

Though these companies had complied the UK tax structure but the increased complications

in the system of UK tax made them to avoid the payment of tax taking the help of BEPS. As

per record of UK government Amazon paid £1.8 billion as tax expense against sales of £3.35

billion, on the other hand Google paid only £6 million where the total turnover amounting to

£395million (bbc.com, 2013). These MNCs able to transferred the profit to other jurisdiction

where rate of tax is low in the form of assets or associated risks (erasmuslawreview.nl, 2017).

From the above discussion it can be said the government has taken several policies to

analyse and detect the tax gap. It is the foremost duty of the government to take reasonable

steps to control the increasing trend of tax avoidance. Since tax avoidance is not illegal in the

eye of law individuals and MNCs take the undue advantages of the tax law which is very

difficult for the government to detect the unacceptable arrangements. Therefore, it can be said

that government should abide by the provisions of GAAR, rules of HMRC and the actions of

BEPS package strictly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

Reference:

assets.publishing.service.gov.uk (2019). [online] Assets.publishing.service.gov.uk. Available

at: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/

attachment_data/file/785551/tackling_tax_avoidance_evasion_and_other_forms_of_non-

compliance_web.pdf [Accessed 28 Sep. 2019].

Bird, R. and Davis-Nozemack, K., 2018. Tax avoidance as a sustainability problem. Journal

of Business Ethics, 151(4), pp.1009-1025.

Birks, J., 2017. Tax avoidance as an anti-austerity issue: The progress of a protest issue

through the public sphere. European Journal of Communication, 32(4), pp.296-311.

Brauner, Y., 2014. What the BEPS. Fla. Tax Rev., 16, p.55.

Campbell, K. and Helleloid, D., 2016. Starbucks: Social responsibility and tax

avoidance. Journal of Accounting Education, 37, pp.38-60.

commons.allard.ubc.ca (2017). [ebook] Available at:

http://commons.allard.ubc.ca/cgi/viewcontent.cgi?article=1059&context=fac_pubs [Accessed

28 Sep. 2019].

erasmuslawreview.nl (2017). Post-BEPS Tax Advisory and Tax Structuring from a Tax

Practitioner’s View · Erasmus Law Review · Erasmus Law Review. [online]

Erasmuslawreview.nl. Available at:

http://www.erasmuslawreview.nl/tijdschrift/ELR/2017/1/ELR_2017_10_01_006/fullscreen

[Accessed 28 Sep. 2019].

Ferry, L., Eckersley, P. and Van Dooren, W., 2015. Local taxation and spending as a share of

GDP in large Western European countries. Environment and Planning A, pp.1779-1780.

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

Reference:

assets.publishing.service.gov.uk (2019). [online] Assets.publishing.service.gov.uk. Available

at: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/

attachment_data/file/785551/tackling_tax_avoidance_evasion_and_other_forms_of_non-

compliance_web.pdf [Accessed 28 Sep. 2019].

Bird, R. and Davis-Nozemack, K., 2018. Tax avoidance as a sustainability problem. Journal

of Business Ethics, 151(4), pp.1009-1025.

Birks, J., 2017. Tax avoidance as an anti-austerity issue: The progress of a protest issue

through the public sphere. European Journal of Communication, 32(4), pp.296-311.

Brauner, Y., 2014. What the BEPS. Fla. Tax Rev., 16, p.55.

Campbell, K. and Helleloid, D., 2016. Starbucks: Social responsibility and tax

avoidance. Journal of Accounting Education, 37, pp.38-60.

commons.allard.ubc.ca (2017). [ebook] Available at:

http://commons.allard.ubc.ca/cgi/viewcontent.cgi?article=1059&context=fac_pubs [Accessed

28 Sep. 2019].

erasmuslawreview.nl (2017). Post-BEPS Tax Advisory and Tax Structuring from a Tax

Practitioner’s View · Erasmus Law Review · Erasmus Law Review. [online]

Erasmuslawreview.nl. Available at:

http://www.erasmuslawreview.nl/tijdschrift/ELR/2017/1/ELR_2017_10_01_006/fullscreen

[Accessed 28 Sep. 2019].

Ferry, L., Eckersley, P. and Van Dooren, W., 2015. Local taxation and spending as a share of

GDP in large Western European countries. Environment and Planning A, pp.1779-1780.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

Freedman, J., 2016. General Anti-Avoidance Rules (GAARs)–A Key Element of Tax

Systems in the Post-BEPS Tax World? The UK GAAR.

gaar_parts_a_b_c_2018 (2018). [ebook] Available at: http://gaar_parts_a_b_c_2018.pdf

[Accessed 28 Sep. 2019].

Helliwell, R.A., 2018. What role does the UK general anti-abuse rule play in preventing tax

avoidance using loan relationships and how does this role affect the way we should

conceptualise the GAAR when applied to other corporation tax matters? (Doctoral

dissertation, University of Birmingham).

James, S.R., 2016. Accounting and Taxation: UK. Wolters Kluwer.

Jones, E., 2015. Exmoor Coast Boat Cruises Ltd v HM Revenue and Customs

Commissioners: [2014] UKFTT 1103 (TC): First-Tier Tribunal (Tax Chamber): HHJ Barbara

Mosedale: 17 December 2014. Oxford Journal of Law and Religion, 4(2), pp.332-333.

Knoll, B., Riedel, N., Shamsfakhr, F. and Strohmaier, K., 2017. Corporate tax evasion and

avoidance in developing countries. In The Routledge Companion to Tax Avoidance

Research (pp. 225-241). Routledge.

Liu, L., Schmidt-Eisenlohr, T. and Guo, D., 2017. International transfer pricing and tax

avoidance: Evidence from linked trade-tax statistics in the UK. FRB International Finance

Discussion Paper, (1214).

Lord, J. and Culling, A., 2016. OR In HM Revenue & Customs. Impact, 2(2), pp.30-33.

Mousa, R., 2016. The evolution of electronic filing process at the UK's HM Revenue and

Customs: The case of XBRL adoption. eJTR, 14, p.206.

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

Freedman, J., 2016. General Anti-Avoidance Rules (GAARs)–A Key Element of Tax

Systems in the Post-BEPS Tax World? The UK GAAR.

gaar_parts_a_b_c_2018 (2018). [ebook] Available at: http://gaar_parts_a_b_c_2018.pdf

[Accessed 28 Sep. 2019].

Helliwell, R.A., 2018. What role does the UK general anti-abuse rule play in preventing tax

avoidance using loan relationships and how does this role affect the way we should

conceptualise the GAAR when applied to other corporation tax matters? (Doctoral

dissertation, University of Birmingham).

James, S.R., 2016. Accounting and Taxation: UK. Wolters Kluwer.

Jones, E., 2015. Exmoor Coast Boat Cruises Ltd v HM Revenue and Customs

Commissioners: [2014] UKFTT 1103 (TC): First-Tier Tribunal (Tax Chamber): HHJ Barbara

Mosedale: 17 December 2014. Oxford Journal of Law and Religion, 4(2), pp.332-333.

Knoll, B., Riedel, N., Shamsfakhr, F. and Strohmaier, K., 2017. Corporate tax evasion and

avoidance in developing countries. In The Routledge Companion to Tax Avoidance

Research (pp. 225-241). Routledge.

Liu, L., Schmidt-Eisenlohr, T. and Guo, D., 2017. International transfer pricing and tax

avoidance: Evidence from linked trade-tax statistics in the UK. FRB International Finance

Discussion Paper, (1214).

Lord, J. and Culling, A., 2016. OR In HM Revenue & Customs. Impact, 2(2), pp.30-33.

Mousa, R., 2016. The evolution of electronic filing process at the UK's HM Revenue and

Customs: The case of XBRL adoption. eJTR, 14, p.206.

11

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

patrickcannon.net (2018). UK Tax Evasion Statistics 2018 - Patrick Cannon. [online] Patrick

Cannon. Available at: https://www.patrickcannon.net/insights/uk-tax-evasion-statistics/

[Accessed 28 Sep. 2019].

Riedel, N., 2018. Quantifying international tax avoidance: A review of the academic

literature. Review of Economics, 69(2), pp.169-181.

Shome, P., 2019. General Anti-Avoidance Rules (GAAR): A Critical Analysis. Revista de

Direito Internacional Econômico e Tributário, 13(1), pp.331-355.

siepweb.it (2015). [ebook] Available at:

http://www.siepweb.it/siep/images/joomd/1437057317Bernardi_WP_SIEP_696.pdf

[Accessed 28 Sep. 2019].

Sikka, P., 2015. No accounting for tax avoidance. The Political Quarterly, 86(3), pp.427-433.

www.bbc.com (2013). The rise of 'tax shaming'. [online] BBC News. Available at:

https://www.bbc.com/news/magazine-20560359 [Accessed 28 Sep. 2019].

www.oecd.org (2019). Action 14 - OECD BEPS. [online] Oecd.org. Available at:

http://www.oecd.org/tax/beps/beps-actions/action14/ [Accessed 28 Sep. 2019].

MEASURES TO AVOID UNACCEPTABLE TAX AVOIDANCE IN UK

patrickcannon.net (2018). UK Tax Evasion Statistics 2018 - Patrick Cannon. [online] Patrick

Cannon. Available at: https://www.patrickcannon.net/insights/uk-tax-evasion-statistics/

[Accessed 28 Sep. 2019].

Riedel, N., 2018. Quantifying international tax avoidance: A review of the academic

literature. Review of Economics, 69(2), pp.169-181.

Shome, P., 2019. General Anti-Avoidance Rules (GAAR): A Critical Analysis. Revista de

Direito Internacional Econômico e Tributário, 13(1), pp.331-355.

siepweb.it (2015). [ebook] Available at:

http://www.siepweb.it/siep/images/joomd/1437057317Bernardi_WP_SIEP_696.pdf

[Accessed 28 Sep. 2019].

Sikka, P., 2015. No accounting for tax avoidance. The Political Quarterly, 86(3), pp.427-433.

www.bbc.com (2013). The rise of 'tax shaming'. [online] BBC News. Available at:

https://www.bbc.com/news/magazine-20560359 [Accessed 28 Sep. 2019].

www.oecd.org (2019). Action 14 - OECD BEPS. [online] Oecd.org. Available at:

http://www.oecd.org/tax/beps/beps-actions/action14/ [Accessed 28 Sep. 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.