Information about goodwill method - Memo

VerifiedAdded on 2021/02/19

|8

|2599

|58

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Memo

To: Accounting Colleagues

From: BDO

Date: 22nd September, 2019

Subject: Information about goodwill method, IAS 36and AASB 136.

Goodwill is defined as an established reputation of business which is regarded as quantifiable

asset (Srinivasan and Kottam, 2018). It is recorded when purchase price of business is higher than its

fair value . As per the clarifications given by govt companies can record goodwill which is more

appropriate for the business. As per the govt requirements companies are required to perform

impairment tests once over a year. Impairment refers to bring the value of goodwill to it current market

value and on decline record it as impairment for respective year(AbuGhazaleh, Al-Hares and Haddad,

(2012)). The report will cover Memo about the issues raises regarding Goodwill and Impairment project

related to replacement of impairment only approach with amortization. Impairment project is for giving

better information to users of financial statements and also gives accurate financial of company.

Removal of mandatory impairment test will make the process cost efficient and the complexity of

mandatory impairment tests.. It is written for supporting impairment only approach of recording

goodwill over amortization approach. Reintroducing amortization will not give clear and reliable

information to users (Chalmers, Godfrey and Webster, (2011)) . Further study will also give draft of

short letter to be issued to one of the firm's client (Griffiths, 2015).

Goodwill refers to reputation and worth that a business gains over a period. This reputation gets

converted into monetary terms that will emerge future benefits for company over and above its normal

profits. In brief it is a reputation of firm which is computed on expected profits above normal profits. In

accounting terms goodwill is an intangible asset. (Zaman, Hossain and Rahman, 2018). Accounting of

goodwill has always been controversial topic among academics and accounting standards professional

bodies. The topic of debate is which method of goodwill gives better representation of underlying

economic characteristic and value. Amortization method of goodwill is having a fixed expense that is

charged in each reporting over the useful life of goodwill. Amortization gives more assets and income

on balance sheet. It reduces the tax burden till the asset is in use by company. Amortization method was

To: Accounting Colleagues

From: BDO

Date: 22nd September, 2019

Subject: Information about goodwill method, IAS 36and AASB 136.

Goodwill is defined as an established reputation of business which is regarded as quantifiable

asset (Srinivasan and Kottam, 2018). It is recorded when purchase price of business is higher than its

fair value . As per the clarifications given by govt companies can record goodwill which is more

appropriate for the business. As per the govt requirements companies are required to perform

impairment tests once over a year. Impairment refers to bring the value of goodwill to it current market

value and on decline record it as impairment for respective year(AbuGhazaleh, Al-Hares and Haddad,

(2012)). The report will cover Memo about the issues raises regarding Goodwill and Impairment project

related to replacement of impairment only approach with amortization. Impairment project is for giving

better information to users of financial statements and also gives accurate financial of company.

Removal of mandatory impairment test will make the process cost efficient and the complexity of

mandatory impairment tests.. It is written for supporting impairment only approach of recording

goodwill over amortization approach. Reintroducing amortization will not give clear and reliable

information to users (Chalmers, Godfrey and Webster, (2011)) . Further study will also give draft of

short letter to be issued to one of the firm's client (Griffiths, 2015).

Goodwill refers to reputation and worth that a business gains over a period. This reputation gets

converted into monetary terms that will emerge future benefits for company over and above its normal

profits. In brief it is a reputation of firm which is computed on expected profits above normal profits. In

accounting terms goodwill is an intangible asset. (Zaman, Hossain and Rahman, 2018). Accounting of

goodwill has always been controversial topic among academics and accounting standards professional

bodies. The topic of debate is which method of goodwill gives better representation of underlying

economic characteristic and value. Amortization method of goodwill is having a fixed expense that is

charged in each reporting over the useful life of goodwill. Amortization gives more assets and income

on balance sheet. It reduces the tax burden till the asset is in use by company. Amortization method was

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

not accepted as it was not accounting for real decrease in economic value of goodwill but based on false

assumptions that goodwill decreases with straight value over time. Another issue with amortization is

related to negative relation to equity value (Gibbons and Hazy, 2017). Considering the disadvantages of

amortization methods in goodwill treatment a new approach of impairment only is adopted over

amortization. This approach is adopted by companies as it reflects more reliable economic value of

company. AASB came with this approach after conducting studies and tests about more effective

approach that shows more accurately economic impact of goodwill on enterprise. Para 90 of IAS 36

required that acquisition of goodwill in business combination is tested annually irrespective of any

impairment indicator. Impairment only approach provides users of financial statement information to

calculate return on capital invested and for ensuring that CGU has ioncreased carrying amount of CGU

net assets (IFRS, Agenda ref 18B, 2019),(Glaum, Landsman and Wyrwa, S. (2018)). In this method if

carrying value is more than fair value of company than value of goodwill needs to be reduced in such

way that it is carrying value equals to the fair value of company. (Carvalho, Rodrigues and Ferreira,

2016)

2

assumptions that goodwill decreases with straight value over time. Another issue with amortization is

related to negative relation to equity value (Gibbons and Hazy, 2017). Considering the disadvantages of

amortization methods in goodwill treatment a new approach of impairment only is adopted over

amortization. This approach is adopted by companies as it reflects more reliable economic value of

company. AASB came with this approach after conducting studies and tests about more effective

approach that shows more accurately economic impact of goodwill on enterprise. Para 90 of IAS 36

required that acquisition of goodwill in business combination is tested annually irrespective of any

impairment indicator. Impairment only approach provides users of financial statement information to

calculate return on capital invested and for ensuring that CGU has ioncreased carrying amount of CGU

net assets (IFRS, Agenda ref 18B, 2019),(Glaum, Landsman and Wyrwa, S. (2018)). In this method if

carrying value is more than fair value of company than value of goodwill needs to be reduced in such

way that it is carrying value equals to the fair value of company. (Carvalho, Rodrigues and Ferreira,

2016)

2

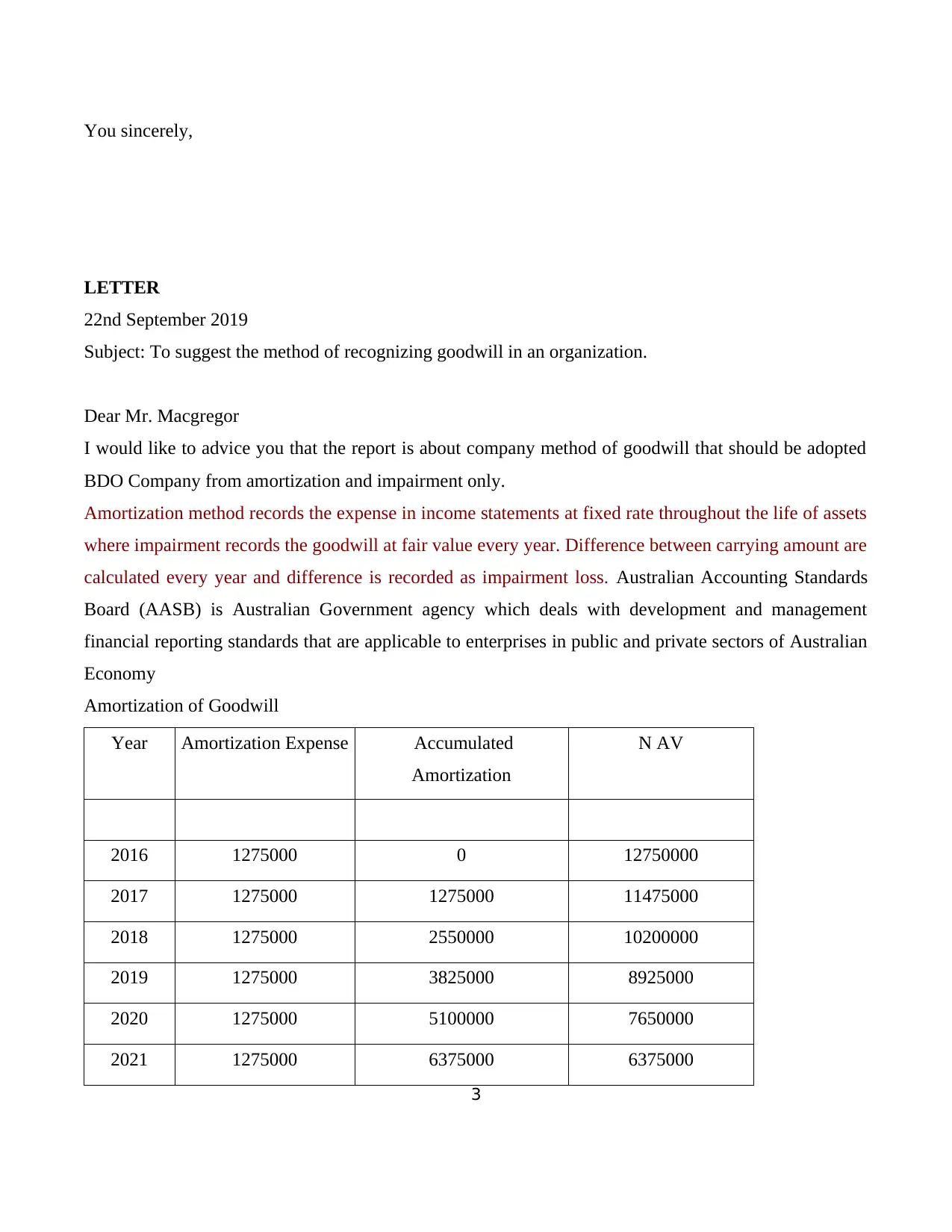

You sincerely,

LETTER

22nd September 2019

Subject: To suggest the method of recognizing goodwill in an organization.

Dear Mr. Macgregor

I would like to advice you that the report is about company method of goodwill that should be adopted

BDO Company from amortization and impairment only.

Amortization method records the expense in income statements at fixed rate throughout the life of assets

where impairment records the goodwill at fair value every year. Difference between carrying amount are

calculated every year and difference is recorded as impairment loss. Australian Accounting Standards

Board (AASB) is Australian Government agency which deals with development and management

financial reporting standards that are applicable to enterprises in public and private sectors of Australian

Economy

Amortization of Goodwill

Year Amortization Expense Accumulated

Amortization

N AV

2016 1275000 0 12750000

2017 1275000 1275000 11475000

2018 1275000 2550000 10200000

2019 1275000 3825000 8925000

2020 1275000 5100000 7650000

2021 1275000 6375000 6375000

3

LETTER

22nd September 2019

Subject: To suggest the method of recognizing goodwill in an organization.

Dear Mr. Macgregor

I would like to advice you that the report is about company method of goodwill that should be adopted

BDO Company from amortization and impairment only.

Amortization method records the expense in income statements at fixed rate throughout the life of assets

where impairment records the goodwill at fair value every year. Difference between carrying amount are

calculated every year and difference is recorded as impairment loss. Australian Accounting Standards

Board (AASB) is Australian Government agency which deals with development and management

financial reporting standards that are applicable to enterprises in public and private sectors of Australian

Economy

Amortization of Goodwill

Year Amortization Expense Accumulated

Amortization

N AV

2016 1275000 0 12750000

2017 1275000 1275000 11475000

2018 1275000 2550000 10200000

2019 1275000 3825000 8925000

2020 1275000 5100000 7650000

2021 1275000 6375000 6375000

3

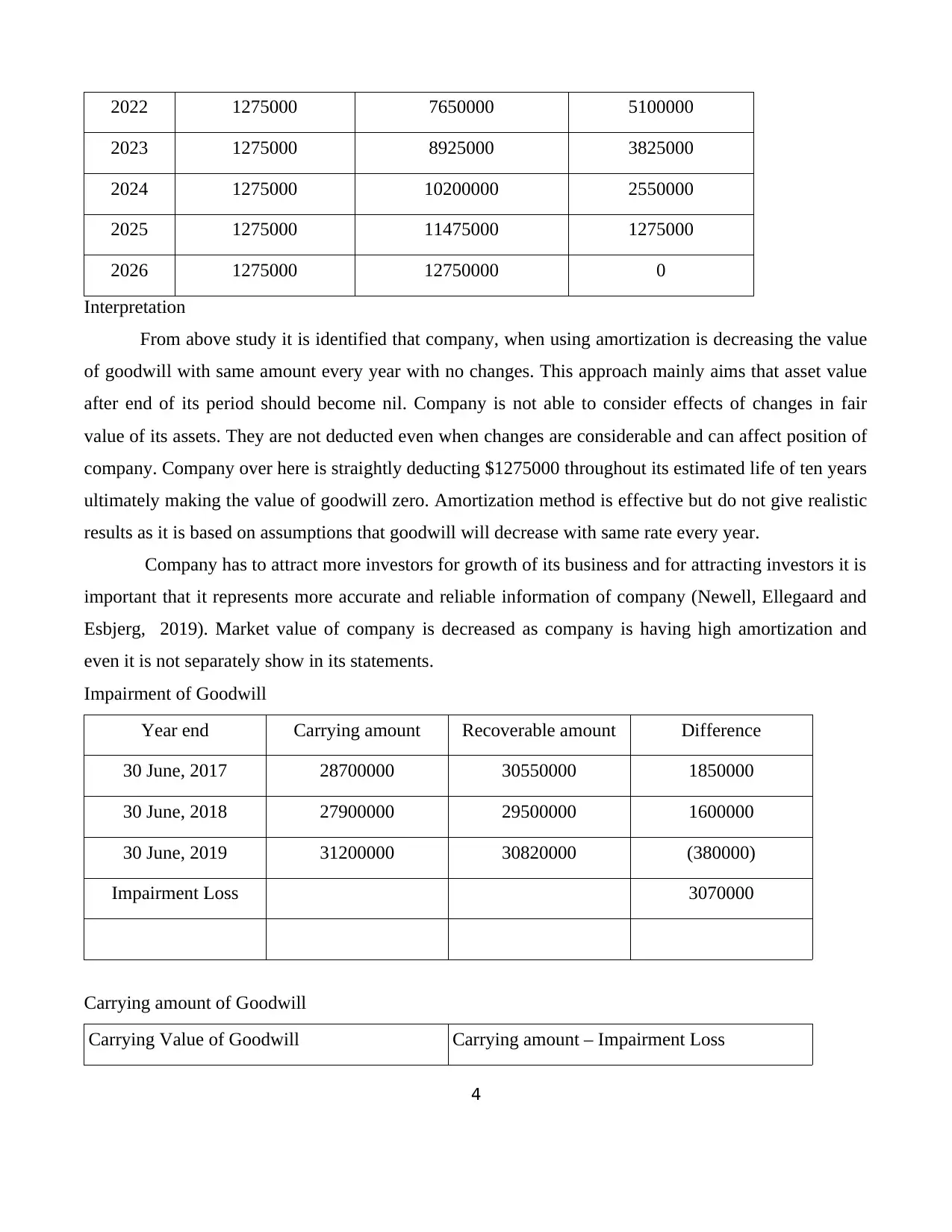

2022 1275000 7650000 5100000

2023 1275000 8925000 3825000

2024 1275000 10200000 2550000

2025 1275000 11475000 1275000

2026 1275000 12750000 0

Interpretation

From above study it is identified that company, when using amortization is decreasing the value

of goodwill with same amount every year with no changes. This approach mainly aims that asset value

after end of its period should become nil. Company is not able to consider effects of changes in fair

value of its assets. They are not deducted even when changes are considerable and can affect position of

company. Company over here is straightly deducting $1275000 throughout its estimated life of ten years

ultimately making the value of goodwill zero. Amortization method is effective but do not give realistic

results as it is based on assumptions that goodwill will decrease with same rate every year.

Company has to attract more investors for growth of its business and for attracting investors it is

important that it represents more accurate and reliable information of company (Newell, Ellegaard and

Esbjerg, 2019). Market value of company is decreased as company is having high amortization and

even it is not separately show in its statements.

Impairment of Goodwill

Year end Carrying amount Recoverable amount Difference

30 June, 2017 28700000 30550000 1850000

30 June, 2018 27900000 29500000 1600000

30 June, 2019 31200000 30820000 (380000)

Impairment Loss 3070000

Carrying amount of Goodwill

Carrying Value of Goodwill Carrying amount – Impairment Loss

4

2023 1275000 8925000 3825000

2024 1275000 10200000 2550000

2025 1275000 11475000 1275000

2026 1275000 12750000 0

Interpretation

From above study it is identified that company, when using amortization is decreasing the value

of goodwill with same amount every year with no changes. This approach mainly aims that asset value

after end of its period should become nil. Company is not able to consider effects of changes in fair

value of its assets. They are not deducted even when changes are considerable and can affect position of

company. Company over here is straightly deducting $1275000 throughout its estimated life of ten years

ultimately making the value of goodwill zero. Amortization method is effective but do not give realistic

results as it is based on assumptions that goodwill will decrease with same rate every year.

Company has to attract more investors for growth of its business and for attracting investors it is

important that it represents more accurate and reliable information of company (Newell, Ellegaard and

Esbjerg, 2019). Market value of company is decreased as company is having high amortization and

even it is not separately show in its statements.

Impairment of Goodwill

Year end Carrying amount Recoverable amount Difference

30 June, 2017 28700000 30550000 1850000

30 June, 2018 27900000 29500000 1600000

30 June, 2019 31200000 30820000 (380000)

Impairment Loss 3070000

Carrying amount of Goodwill

Carrying Value of Goodwill Carrying amount – Impairment Loss

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

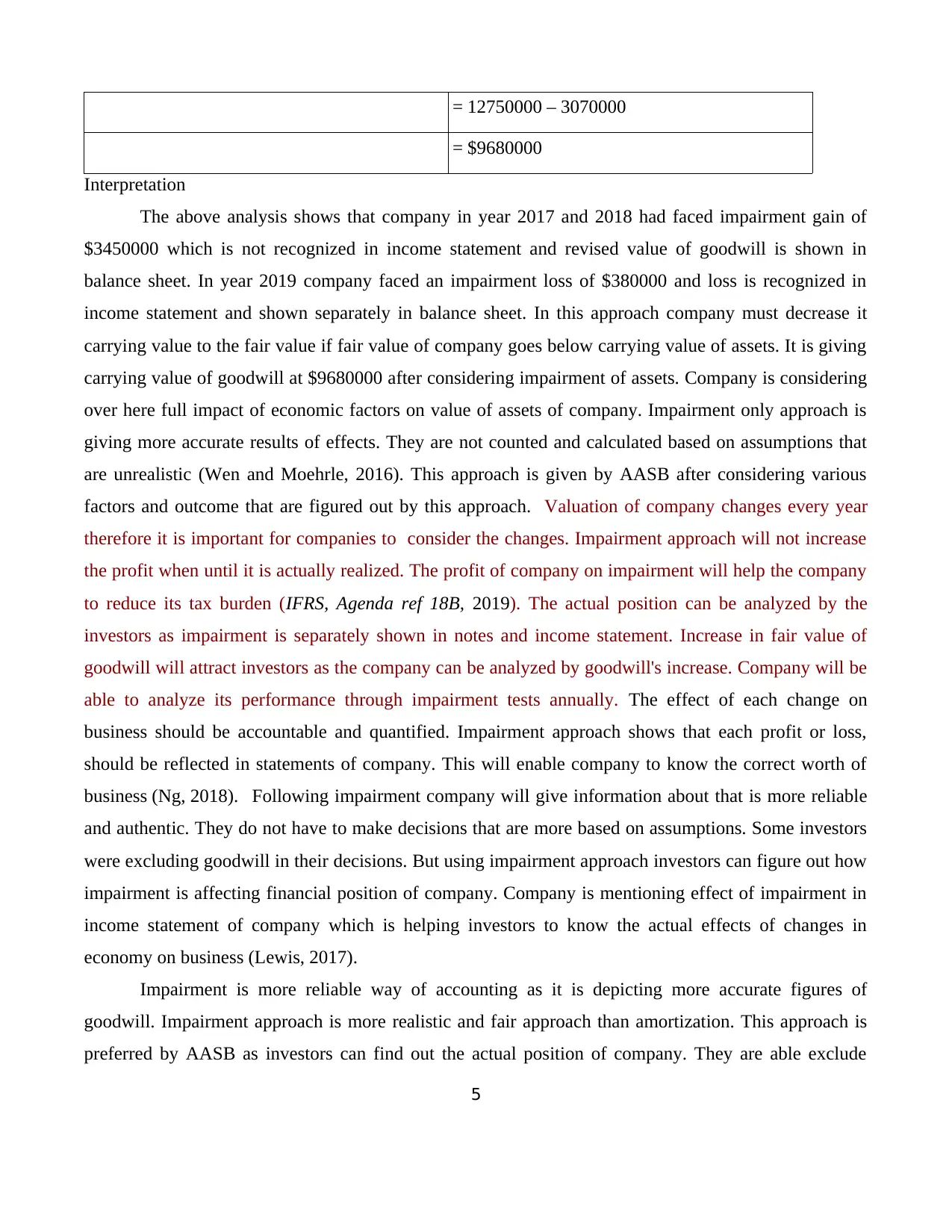

= 12750000 – 3070000

= $9680000

Interpretation

The above analysis shows that company in year 2017 and 2018 had faced impairment gain of

$3450000 which is not recognized in income statement and revised value of goodwill is shown in

balance sheet. In year 2019 company faced an impairment loss of $380000 and loss is recognized in

income statement and shown separately in balance sheet. In this approach company must decrease it

carrying value to the fair value if fair value of company goes below carrying value of assets. It is giving

carrying value of goodwill at $9680000 after considering impairment of assets. Company is considering

over here full impact of economic factors on value of assets of company. Impairment only approach is

giving more accurate results of effects. They are not counted and calculated based on assumptions that

are unrealistic (Wen and Moehrle, 2016). This approach is given by AASB after considering various

factors and outcome that are figured out by this approach. Valuation of company changes every year

therefore it is important for companies to consider the changes. Impairment approach will not increase

the profit when until it is actually realized. The profit of company on impairment will help the company

to reduce its tax burden (IFRS, Agenda ref 18B, 2019). The actual position can be analyzed by the

investors as impairment is separately shown in notes and income statement. Increase in fair value of

goodwill will attract investors as the company can be analyzed by goodwill's increase. Company will be

able to analyze its performance through impairment tests annually. The effect of each change on

business should be accountable and quantified. Impairment approach shows that each profit or loss,

should be reflected in statements of company. This will enable company to know the correct worth of

business (Ng, 2018). Following impairment company will give information about that is more reliable

and authentic. They do not have to make decisions that are more based on assumptions. Some investors

were excluding goodwill in their decisions. But using impairment approach investors can figure out how

impairment is affecting financial position of company. Company is mentioning effect of impairment in

income statement of company which is helping investors to know the actual effects of changes in

economy on business (Lewis, 2017).

Impairment is more reliable way of accounting as it is depicting more accurate figures of

goodwill. Impairment approach is more realistic and fair approach than amortization. This approach is

preferred by AASB as investors can find out the actual position of company. They are able exclude

5

= $9680000

Interpretation

The above analysis shows that company in year 2017 and 2018 had faced impairment gain of

$3450000 which is not recognized in income statement and revised value of goodwill is shown in

balance sheet. In year 2019 company faced an impairment loss of $380000 and loss is recognized in

income statement and shown separately in balance sheet. In this approach company must decrease it

carrying value to the fair value if fair value of company goes below carrying value of assets. It is giving

carrying value of goodwill at $9680000 after considering impairment of assets. Company is considering

over here full impact of economic factors on value of assets of company. Impairment only approach is

giving more accurate results of effects. They are not counted and calculated based on assumptions that

are unrealistic (Wen and Moehrle, 2016). This approach is given by AASB after considering various

factors and outcome that are figured out by this approach. Valuation of company changes every year

therefore it is important for companies to consider the changes. Impairment approach will not increase

the profit when until it is actually realized. The profit of company on impairment will help the company

to reduce its tax burden (IFRS, Agenda ref 18B, 2019). The actual position can be analyzed by the

investors as impairment is separately shown in notes and income statement. Increase in fair value of

goodwill will attract investors as the company can be analyzed by goodwill's increase. Company will be

able to analyze its performance through impairment tests annually. The effect of each change on

business should be accountable and quantified. Impairment approach shows that each profit or loss,

should be reflected in statements of company. This will enable company to know the correct worth of

business (Ng, 2018). Following impairment company will give information about that is more reliable

and authentic. They do not have to make decisions that are more based on assumptions. Some investors

were excluding goodwill in their decisions. But using impairment approach investors can figure out how

impairment is affecting financial position of company. Company is mentioning effect of impairment in

income statement of company which is helping investors to know the actual effects of changes in

economy on business (Lewis, 2017).

Impairment is more reliable way of accounting as it is depicting more accurate figures of

goodwill. Impairment approach is more realistic and fair approach than amortization. This approach is

preferred by AASB as investors can find out the actual position of company. They are able exclude

5

goodwill as it is separately included in income statement and balance sheet, they can know the actual

effect on goodwill because of the economic issues on firm whereas amortization approach did not

consider current issues faced by company but decreased its value straightly (Bath, Manzano-Nieves and

Goodwill, 2016).Accounting firm can carry on with impairment approach as it regularly tests the fair

value of goodwill and enables company and investors to give more accurate and reliable information of

company (IFRS, Agenda ref 18B, 2019). This awareness will help them to take decisions related to

improvements and prevention so that it is not affected much. It should adopt impairment only approach

which is more transparent. They also do not give right idea about image of company position. (d'Arcy

and Tarca, 2018).

Amortization is complex and costly which do not takes into account impairment losses . It can be

figured out by calculating results from both approaches that results which are more reliable and

satisfactory are given by impairment approach. They are not able to figure out the exact difference and

effect which company is facing. The company do not consider any changes and therefore not reflected in

statements of accounts (Smith and Morgan, 2018). Company will not show high rate even when they are

actual performing as their profits will be declined by amortization (IFRS, Agenda ref 18B, 2019).

Whereas in impairment losses due to changes in valuation are separately recorded so that it can be

identified that downfall is related to impairment and when rise is seen in values the reduced value of

assets will be adjusted according to the amount which was deducted. This will maintain position of

company more effectively inclusive of changes. Investors will get attracted when they are able to make

more authentic decisions (Saastamoinen and Pajunen, 2016).

Yours Sincerely

6

effect on goodwill because of the economic issues on firm whereas amortization approach did not

consider current issues faced by company but decreased its value straightly (Bath, Manzano-Nieves and

Goodwill, 2016).Accounting firm can carry on with impairment approach as it regularly tests the fair

value of goodwill and enables company and investors to give more accurate and reliable information of

company (IFRS, Agenda ref 18B, 2019). This awareness will help them to take decisions related to

improvements and prevention so that it is not affected much. It should adopt impairment only approach

which is more transparent. They also do not give right idea about image of company position. (d'Arcy

and Tarca, 2018).

Amortization is complex and costly which do not takes into account impairment losses . It can be

figured out by calculating results from both approaches that results which are more reliable and

satisfactory are given by impairment approach. They are not able to figure out the exact difference and

effect which company is facing. The company do not consider any changes and therefore not reflected in

statements of accounts (Smith and Morgan, 2018). Company will not show high rate even when they are

actual performing as their profits will be declined by amortization (IFRS, Agenda ref 18B, 2019).

Whereas in impairment losses due to changes in valuation are separately recorded so that it can be

identified that downfall is related to impairment and when rise is seen in values the reduced value of

assets will be adjusted according to the amount which was deducted. This will maintain position of

company more effectively inclusive of changes. Investors will get attracted when they are able to make

more authentic decisions (Saastamoinen and Pajunen, 2016).

Yours Sincerely

6

REFERENCES

AbuGhazaleh, N.M., Al-Hares, O.M. and Haddad, A.E. (2012), 'The value relevance of goodwill

impairments: UK evidence', International Journal of Economics and Finance, Vol. 4 No. 4. pp.

206-216.

Chalmers, K.G., Godfrey, J.M. and Webster, J.C. (2011), 'Does a goodwill impairment regime better

reflect the underlying economic attributes of goodwill?', Accounting & Finance, Vol. 51 No. 3.

pp. 634-660.

Glaum, M., Landsman, W.R. and Wyrwa, S. (2018), 'Goodwill impairment: The effects of public

enforcement and monitoring by institutional investors', The Accounting Review, Vol. 93 No. 6.

pp. 149-180.”

Bath, K.G., Manzano-Nieves, G. and Goodwill, H., 2016. Early life stress accelerates behavioral and

neural maturation of the hippocampus in male mice. Hormones and behavior. 82. pp.64-71.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The recognition of goodwill and other intangible

assets in business combinations–The Portuguese case. Australian Accounting Review. 26(1).

pp.4-20.

d'Arcy, A. and Tarca, A., 2018. Reviewing IFRS goodwill accounting research: Implementation effects

and cross-country differences. The International Journal of Accounting. 53(3). pp.203-226.

Gibbons, J. and Hazy, J.K., 2017. Leading a Large‐Scale Distributed Social Enterprise: How the

Leadership Culture at Goodwill Industries Creates and Distributes Value in

Communities. Nonprofit Management and Leadership. 27(3). pp.299-316.

Griffiths, J., 2015. Star Industrial Co Ltd v Yap Kwee Kor: The End of Goodwill in the Tort of Passing

Off. Chapter to be published in its final form in Landmark Cases in Property Law, ed S Douglas,

R Hickey & E Waring (Hart Publishing, 2015). pp.277-289.

Lewis, O., 2017. Starbucks (HK) Case Note: The Ambiguous Limb of Goodwill and the Tort of Passing

Off. Victoria U. Wellington L. Rev. 48. p.55.

Liu, G., Zhang, J. and Tang, W., 2015. Strategic transfer pricing in a marketing–operations interface

with quality level and advertising dependent goodwill. Omega. 56. pp.1-15.

Newell, W.J., Ellegaard, C. and Esbjerg, L., 2019. The effects of goodwill and competence trust on

strategic information sharing in buyer–supplier relationships. Journal of Business & Industrial

Marketing. 34(2). pp.389-400.

Ng, C., 2018. Goodwill without Borders. The Law Quarterly Review.

Saastamoinen, J. and Pajunen, K., 2016. Management discretion and the role of the stock market in

goodwill impairment decisions-evidence from Finland. International Journal of Managerial and

Financial Accounting. 8(2). pp.172-195.

Smith, J. and Morgan, A., 2018. Court of Appeal of England and Wales rules on validity of trade mark

in light of prior existing localized goodwill. Journal of Intellectual Property Law &

Practice. 13(6). pp.436-437.

Srinivasan, S. and Kottam, V.K.R., 2018. Solar photovoltaic module production: Environmental

footprint, management horizons and investor goodwill. Renewable and Sustainable Energy

Reviews. 81. pp.874-882.

Wen, H. and Moehrle, S.R., 2016. Accounting for goodwill: An academic literature review and analysis

to inform the debate. Research in Accounting Regulation. 28(1). pp.11-21.

Zaman, M.H., Hossain, M.A. and Rahman, M.S., 2018. Goodwill automotive: Taking light engineering

from survival mode to sustainable. SAGE Publications: SAGE Business Cases Originals.

7

AbuGhazaleh, N.M., Al-Hares, O.M. and Haddad, A.E. (2012), 'The value relevance of goodwill

impairments: UK evidence', International Journal of Economics and Finance, Vol. 4 No. 4. pp.

206-216.

Chalmers, K.G., Godfrey, J.M. and Webster, J.C. (2011), 'Does a goodwill impairment regime better

reflect the underlying economic attributes of goodwill?', Accounting & Finance, Vol. 51 No. 3.

pp. 634-660.

Glaum, M., Landsman, W.R. and Wyrwa, S. (2018), 'Goodwill impairment: The effects of public

enforcement and monitoring by institutional investors', The Accounting Review, Vol. 93 No. 6.

pp. 149-180.”

Bath, K.G., Manzano-Nieves, G. and Goodwill, H., 2016. Early life stress accelerates behavioral and

neural maturation of the hippocampus in male mice. Hormones and behavior. 82. pp.64-71.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The recognition of goodwill and other intangible

assets in business combinations–The Portuguese case. Australian Accounting Review. 26(1).

pp.4-20.

d'Arcy, A. and Tarca, A., 2018. Reviewing IFRS goodwill accounting research: Implementation effects

and cross-country differences. The International Journal of Accounting. 53(3). pp.203-226.

Gibbons, J. and Hazy, J.K., 2017. Leading a Large‐Scale Distributed Social Enterprise: How the

Leadership Culture at Goodwill Industries Creates and Distributes Value in

Communities. Nonprofit Management and Leadership. 27(3). pp.299-316.

Griffiths, J., 2015. Star Industrial Co Ltd v Yap Kwee Kor: The End of Goodwill in the Tort of Passing

Off. Chapter to be published in its final form in Landmark Cases in Property Law, ed S Douglas,

R Hickey & E Waring (Hart Publishing, 2015). pp.277-289.

Lewis, O., 2017. Starbucks (HK) Case Note: The Ambiguous Limb of Goodwill and the Tort of Passing

Off. Victoria U. Wellington L. Rev. 48. p.55.

Liu, G., Zhang, J. and Tang, W., 2015. Strategic transfer pricing in a marketing–operations interface

with quality level and advertising dependent goodwill. Omega. 56. pp.1-15.

Newell, W.J., Ellegaard, C. and Esbjerg, L., 2019. The effects of goodwill and competence trust on

strategic information sharing in buyer–supplier relationships. Journal of Business & Industrial

Marketing. 34(2). pp.389-400.

Ng, C., 2018. Goodwill without Borders. The Law Quarterly Review.

Saastamoinen, J. and Pajunen, K., 2016. Management discretion and the role of the stock market in

goodwill impairment decisions-evidence from Finland. International Journal of Managerial and

Financial Accounting. 8(2). pp.172-195.

Smith, J. and Morgan, A., 2018. Court of Appeal of England and Wales rules on validity of trade mark

in light of prior existing localized goodwill. Journal of Intellectual Property Law &

Practice. 13(6). pp.436-437.

Srinivasan, S. and Kottam, V.K.R., 2018. Solar photovoltaic module production: Environmental

footprint, management horizons and investor goodwill. Renewable and Sustainable Energy

Reviews. 81. pp.874-882.

Wen, H. and Moehrle, S.R., 2016. Accounting for goodwill: An academic literature review and analysis

to inform the debate. Research in Accounting Regulation. 28(1). pp.11-21.

Zaman, M.H., Hossain, M.A. and Rahman, M.S., 2018. Goodwill automotive: Taking light engineering

from survival mode to sustainable. SAGE Publications: SAGE Business Cases Originals.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Online

IFRS, Agenda ref 18B. 2019. [ONLINE] Available through

<https://www.ifrs.org/-/media/feature/meetings/2019/june/iasb/ap18b-goodwill-and-impairment.pdf>

8

IFRS, Agenda ref 18B. 2019. [ONLINE] Available through

<https://www.ifrs.org/-/media/feature/meetings/2019/june/iasb/ap18b-goodwill-and-impairment.pdf>

8

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.