Financial Accounting: Statement Analysis and Journal Entries

VerifiedAdded on 2020/03/28

|10

|1565

|33

Homework Assignment

AI Summary

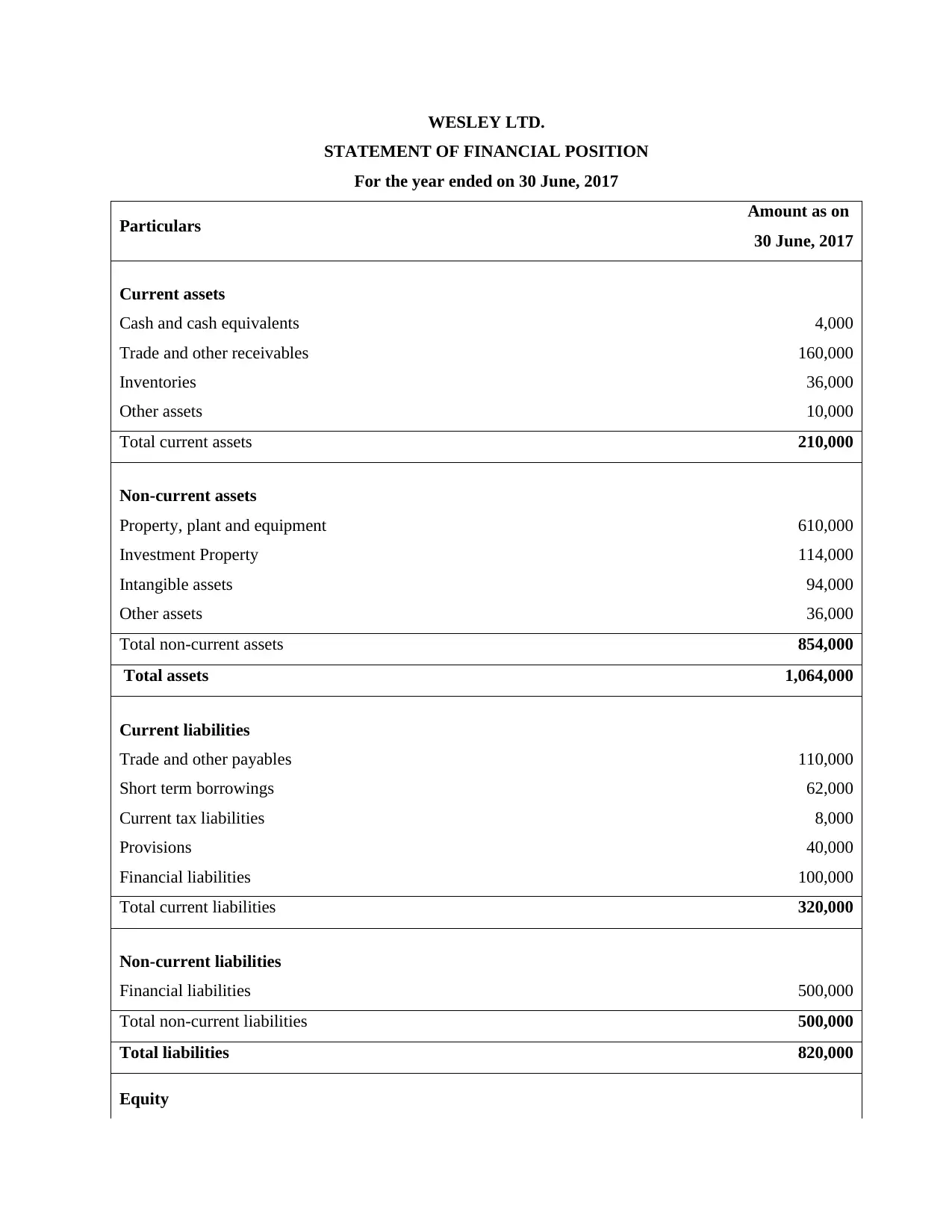

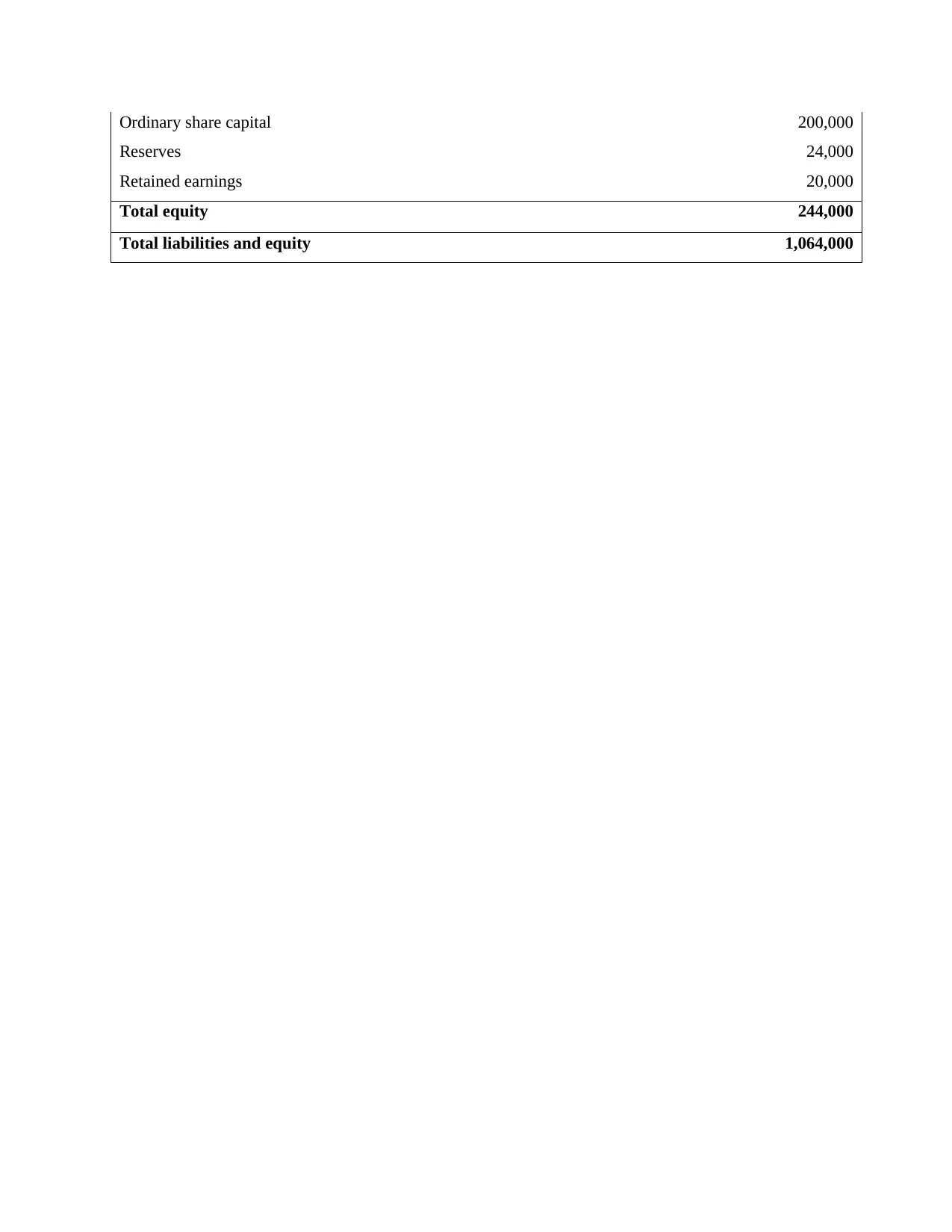

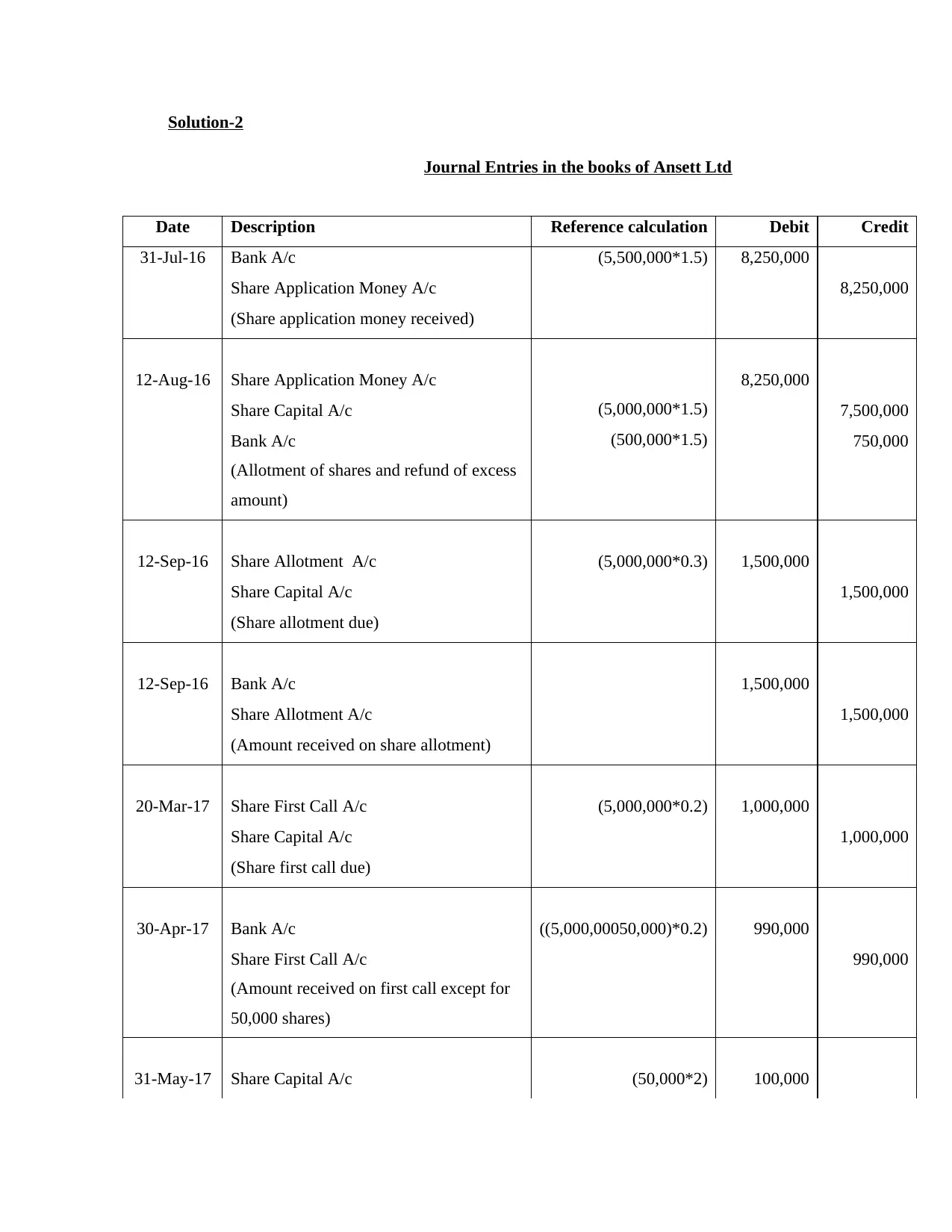

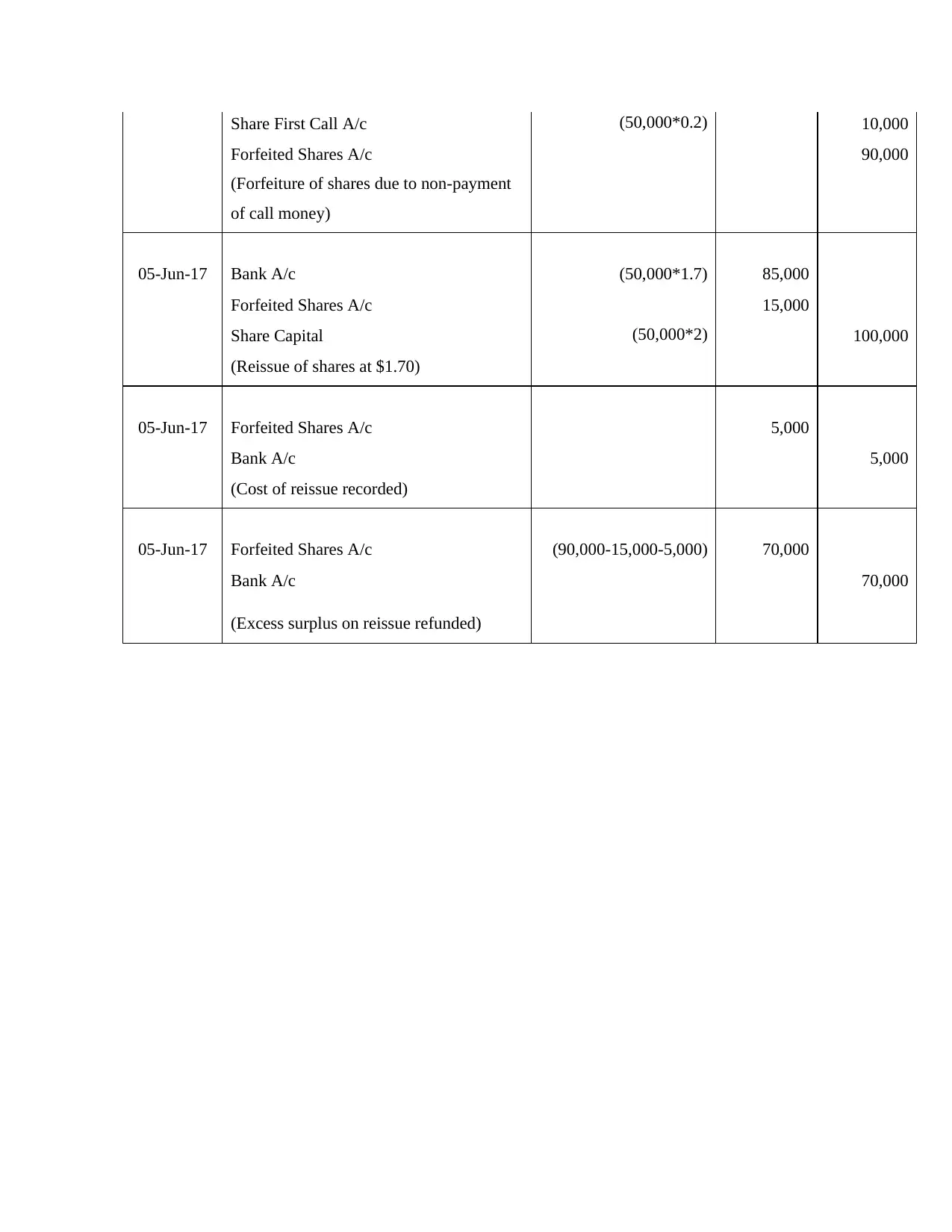

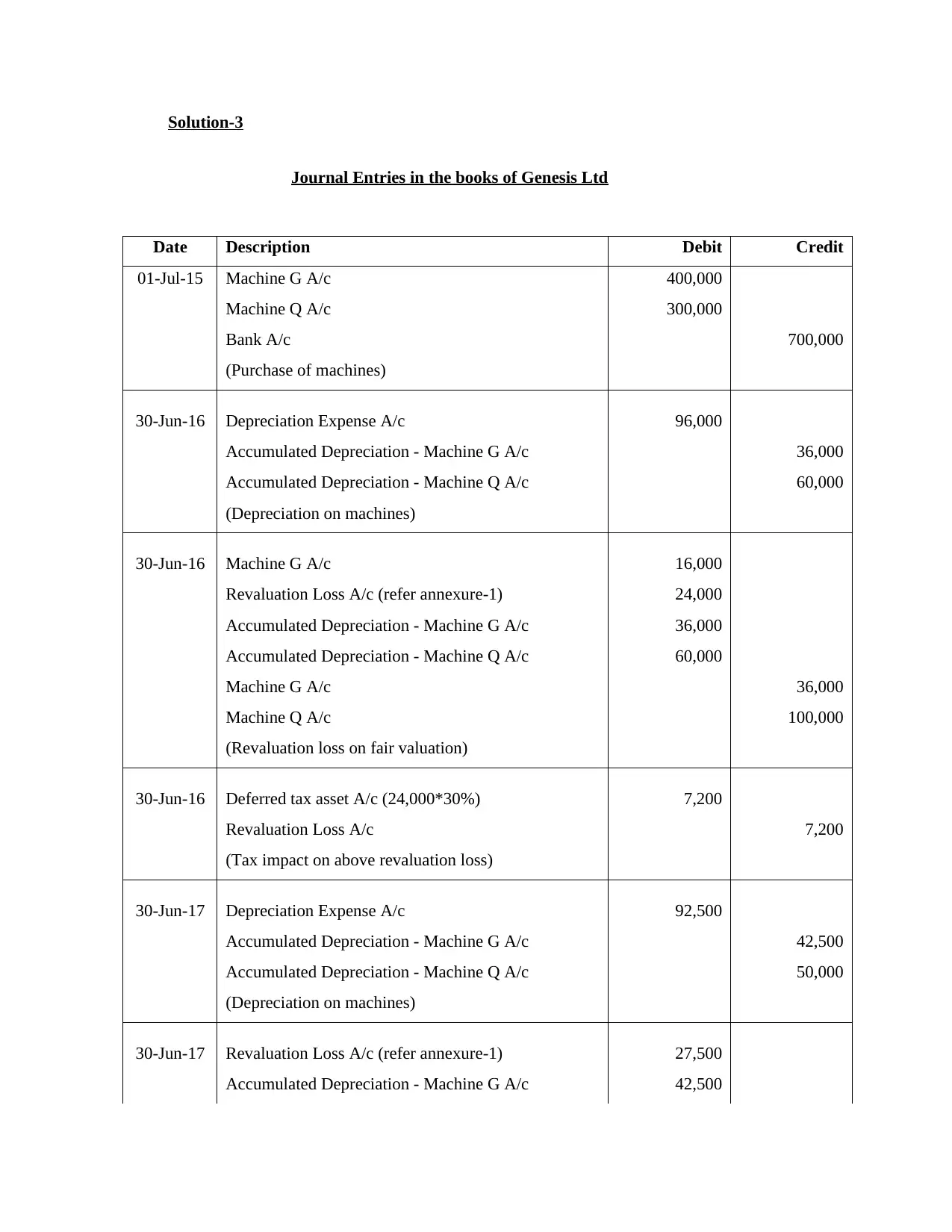

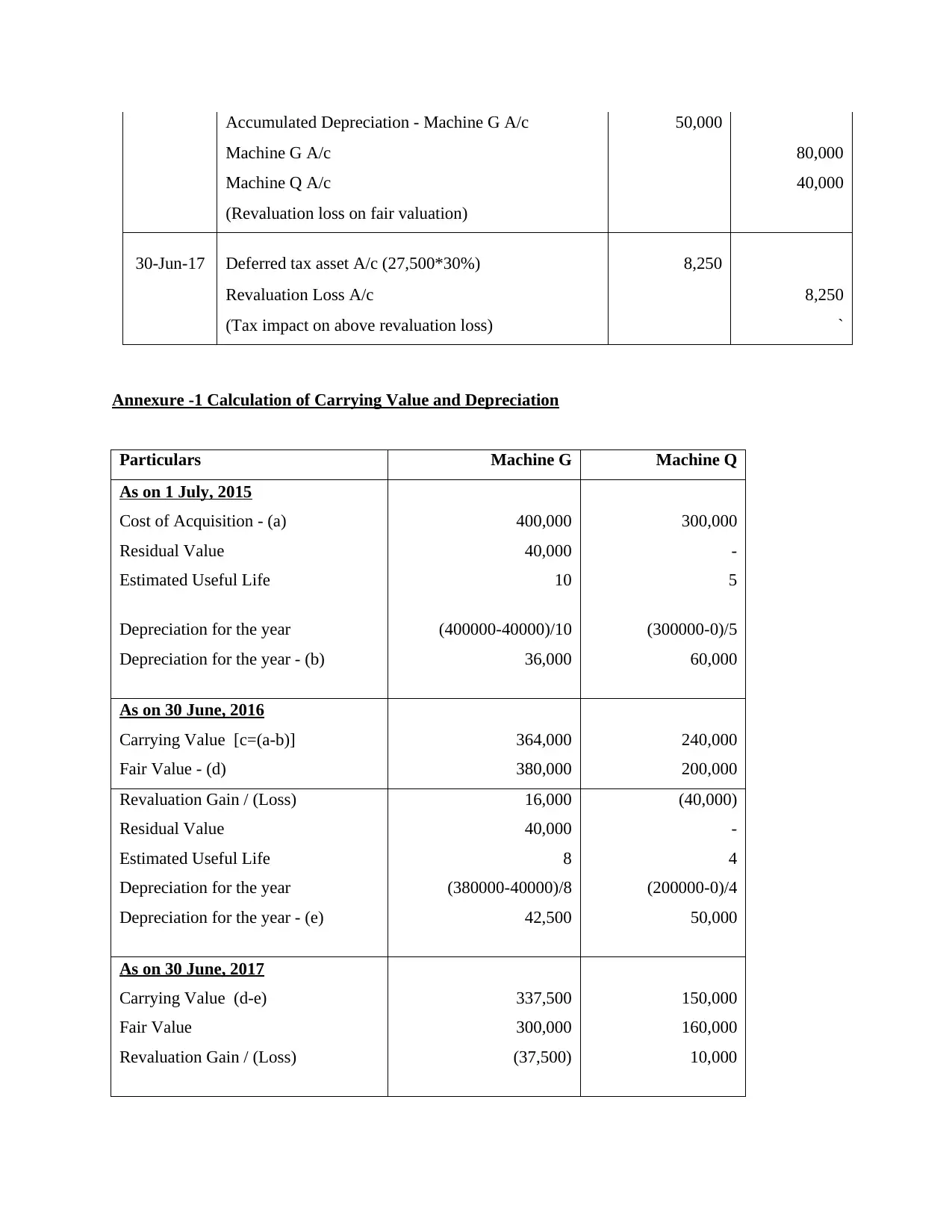

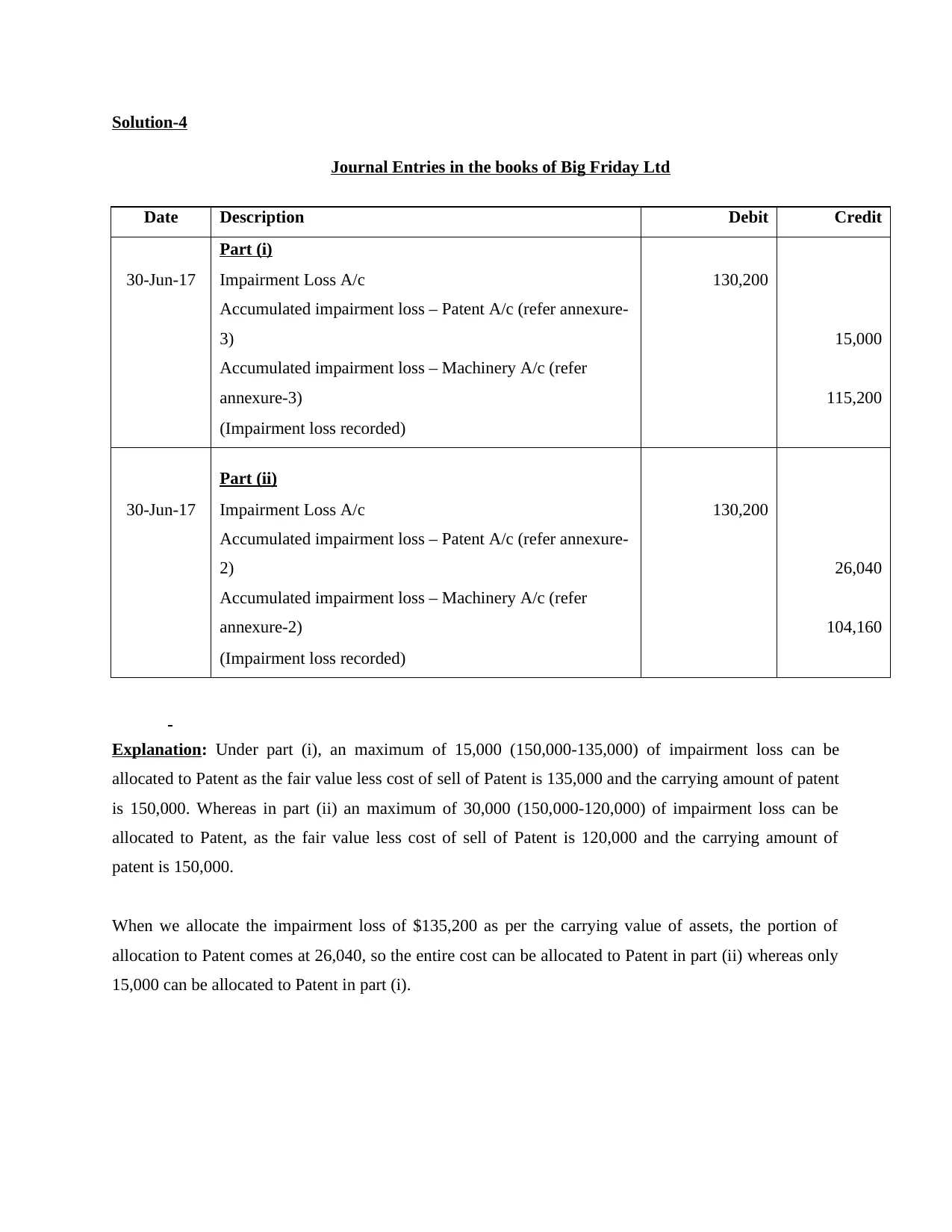

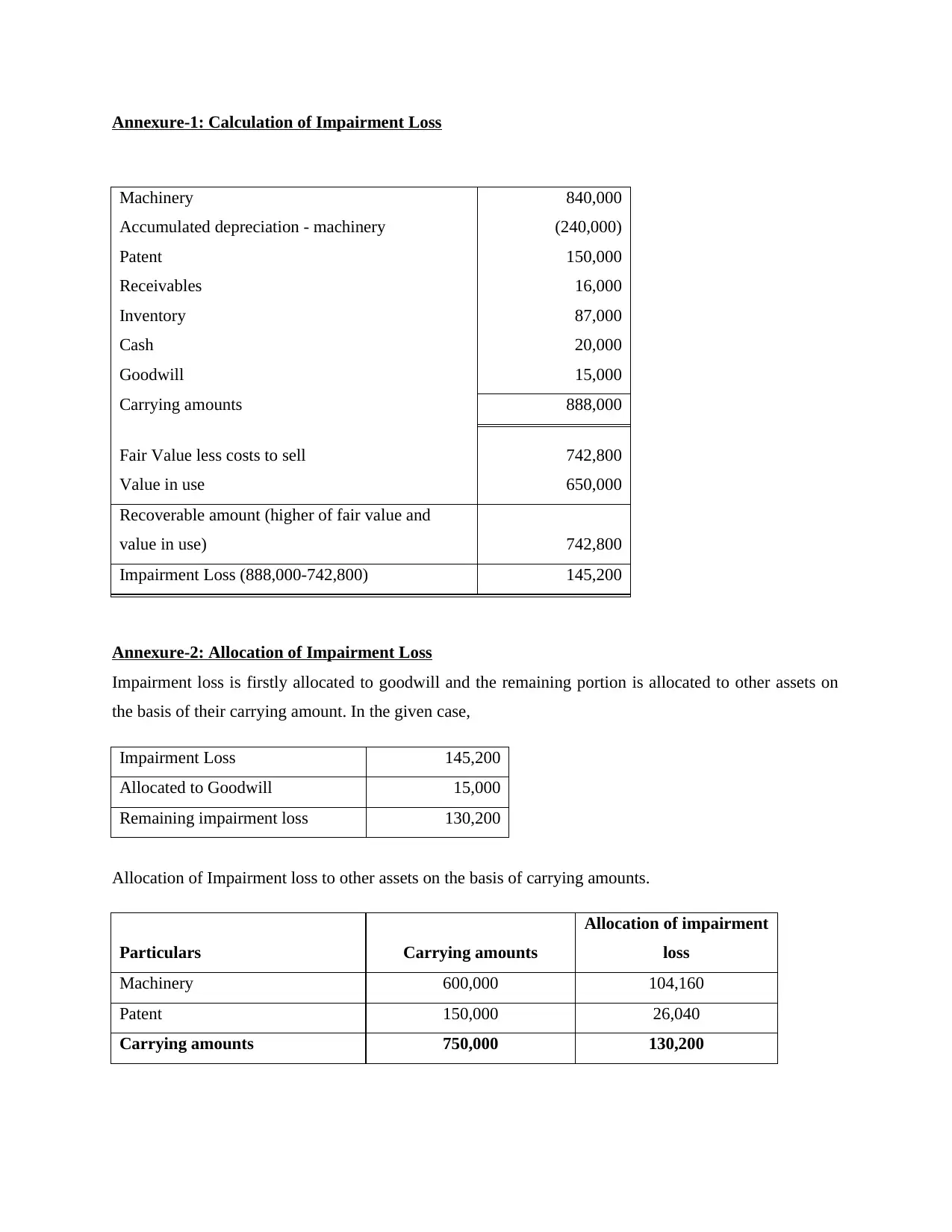

This document presents comprehensive solutions to a financial accounting assignment. The first solution addresses issues with a statement of financial position, including classification errors and incorrect groupings, providing a corrected version adhering to AASB 101 standards. The second solution offers detailed journal entries for share transactions, including share application, allotment, and forfeiture, in the books of Ansett Ltd. The third solution provides journal entries for machine depreciation, revaluation losses, and deferred tax assets for Genesis Ltd, along with calculations for carrying value and depreciation. Finally, the fourth solution demonstrates the recording of impairment losses for Big Friday Ltd, including allocation to goodwill, machinery, and patents under different scenarios, with detailed calculations.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.