ACC00152: MicroNet Tech Options Evaluation and Recommendation Report

VerifiedAdded on 2023/01/19

|4

|1466

|88

Report

AI Summary

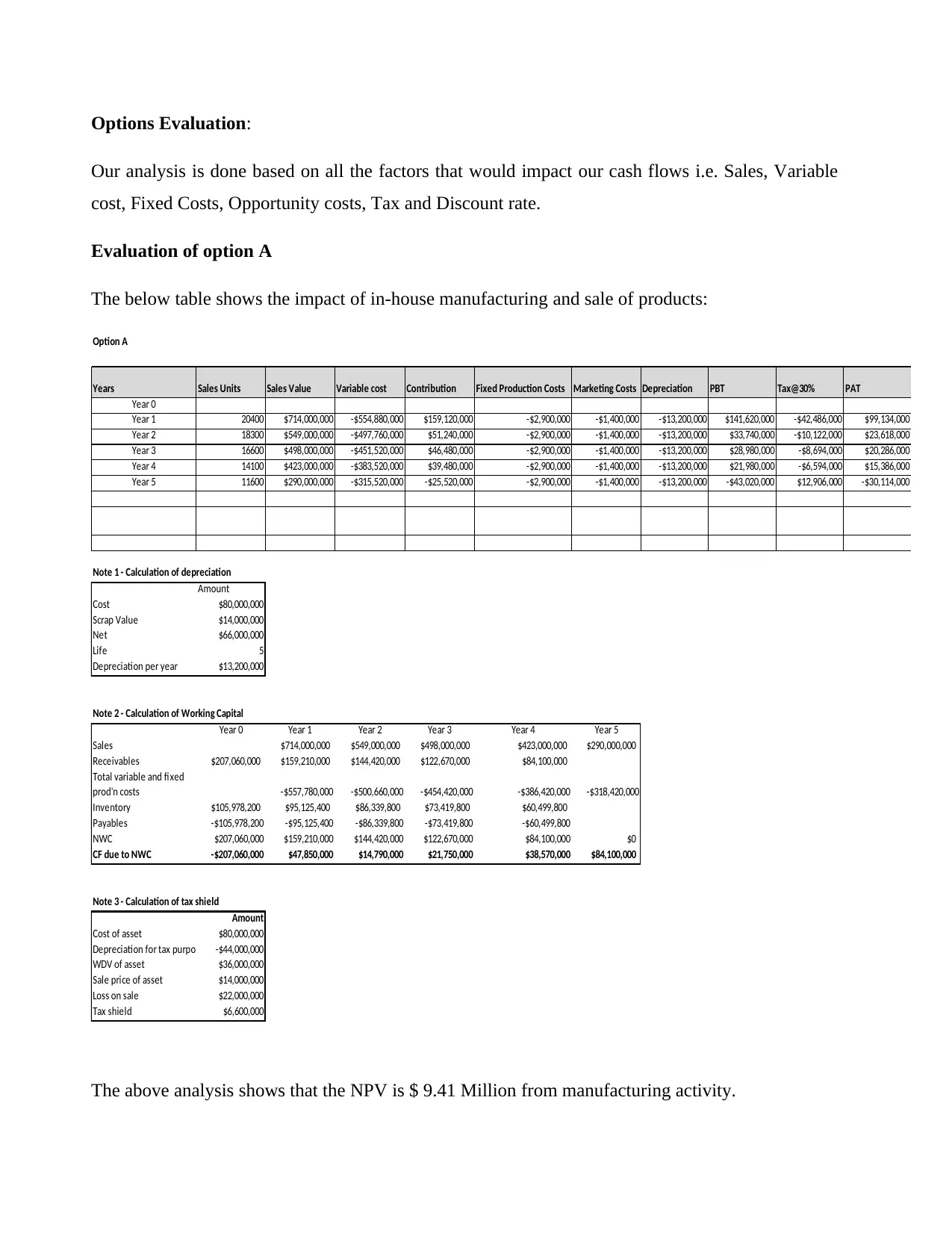

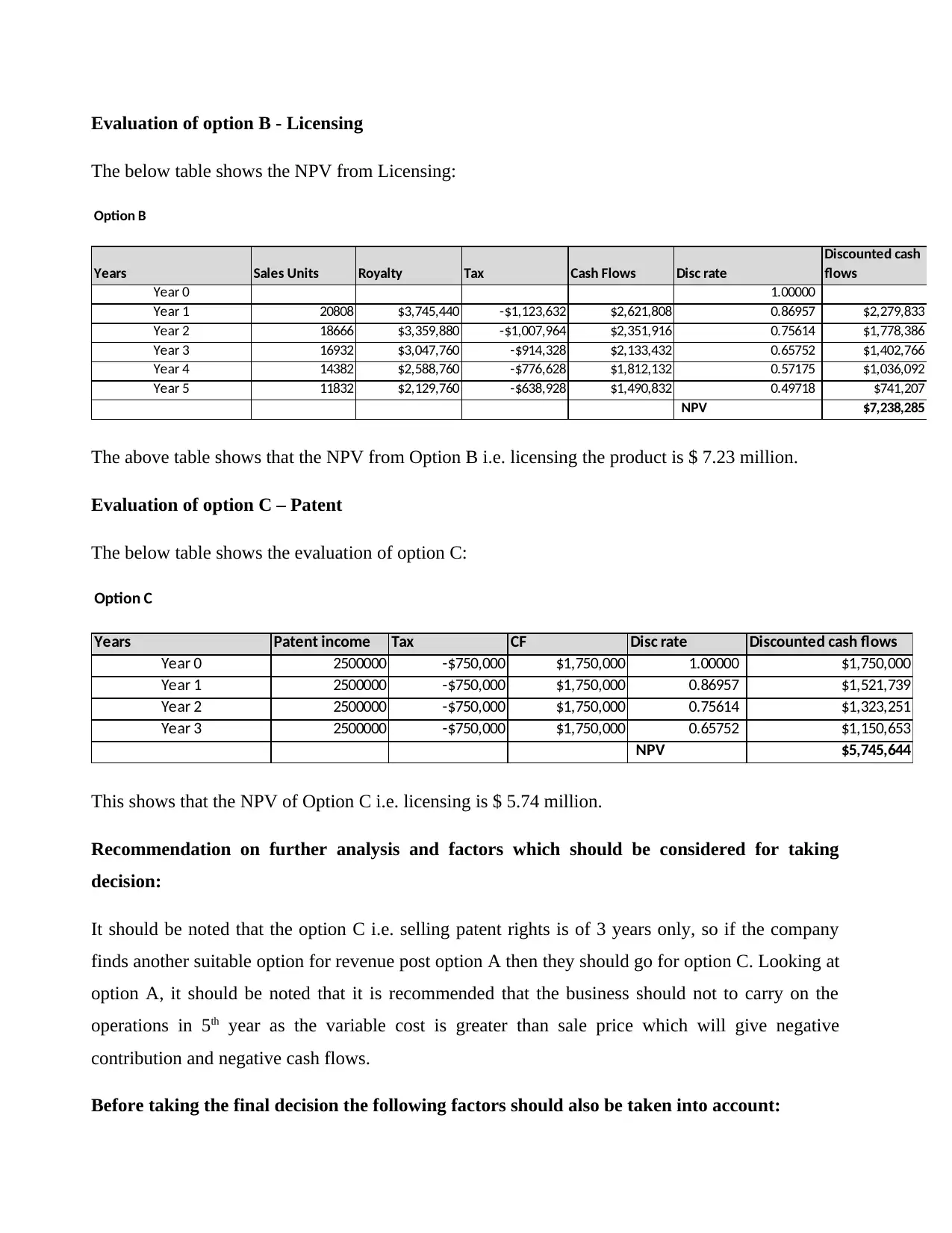

This memorandum, prepared for the Board of Directors of MicroNet Technologies Ltd (MNT), evaluates three options for commercializing a new technology: in-house manufacturing and sales (Option A), licensing (Option B), and selling patent rights (Option C). The analysis, based on a Net Present Value (NPV) approach, considers factors such as sales, variable and fixed costs, taxes, and discount rates. Option A is identified as the most financially attractive, with an NPV of $9.41 million, followed by Option B ($7.23 million) and Option C ($5.74 million). The report recommends Option A for four years, considering its higher growth potential, but cautions against continuing into the fifth year due to increasing variable costs. It also suggests considering factors such as the labor force, market competition, risk tolerance, customer demand, available investment capital, and sunk costs before making a final decision. The report includes detailed calculations for each option, including depreciation, working capital, and tax shield calculations, to support the recommendations.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.