BDM 134 MSc International Accounting: Merlin Strategic Analysis

VerifiedAdded on 2023/06/04

|76

|18887

|456

Report

AI Summary

This report provides a comprehensive strategic, financial, and business analysis of Merlin Entertainment for investment purposes. It includes an overview of the firm's strategic position, highlighting its six strategic growth drivers and a mid-term strategy change in 2018. The financial analysis critically assesses profitability, ROE & ROCE, liquidity, working capital efficiency, asset efficiency, and financial gearing, comparing Merlin to competitors like Drayton Manor Park and Blackpool Pleasure Beach. Business valuation methods, including market capitalization, book value, P/E ratio, and discounted free cash flow, are used to determine a fair share price, leading to recommendations for dividend policy and debt management. The report concludes that Merlin is a good investment candidate due to its rising share price, positive prospects, and geographical diversification, although some returns may take longer to materialize.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017-18 BDM 134

MSc International Accounting

and Finance Project

Candidate Number: 931667

Word Count:

Section 1 – 518 words

Section 2 - 1,793 words – without SWOT

table

Section3 – 3,423 words

Section 4 – 2,843 words – without

Industry median graphs

Section 5 – 1,148 words

Section 6 – 1,057 words

Total words = 10,782 words

2

MSc International Accounting

and Finance Project

Candidate Number: 931667

Word Count:

Section 1 – 518 words

Section 2 - 1,793 words – without SWOT

table

Section3 – 3,423 words

Section 4 – 2,843 words – without

Industry median graphs

Section 5 – 1,148 words

Section 6 – 1,057 words

Total words = 10,782 words

2

Context Page Page

Section 1 – Executive Summary 5

Section 2 – Introduction and Strategic Analysis 7

2.1 - Merlin Entertainments Competitors 10

2.2 - Merlin’s Strategy 10

2.3 - SWOT for Merlin Entertainment 13

Section 3 - Literature Review and Introduction 15

3.1 - Methods of financial analysis that can be conducted using

publicly available information.

15

3.2 – Ration analysis 15

3.3 - Advantages of ratio analysis 16

3.4 – Trend analysis 16

3.5 - Advantages and Disadvantages of Trend Analysis: 17

3.6 - Vertical Analysis 17

3.7 – Horizontal Analysis 18

3.8 - Empirical evidence based on Merlin Entertainment: 18

3.9 - Methods and usefulness of business valuation techniques 19

3.10 - Extent to which financial analysis and valuations using

publicly available corporate information that provides a

faithful representation

22

3.11 - Conclusions regarding information and tools that needs to

be used in the completion of financial analysis and

company valuation

23

Section 4 – Financial Analysis 24

4.1 - Profitability 24

4.2 - ROE and ROCE 28

4.3 – Liquidity and Working Capital Efficiencies 29

4.4 - Total and non-current asset efficiency 34

4.5 - Financial Gearing 36

Section 5 – Business Valuation 39

Market Cap, Book Value per share, P/E ratio 39

5.1 - Discounted Free Cash Flow 41

5.2 - Conclusion 41

Section 6 – Conclusion 43

6.1 - Conclusions and Recommendations for Merlin 43

Appendix 1 - 48

1.1 - Balance sheet for DMP and BPB 2015, 2016 and 2017 50

3

Section 1 – Executive Summary 5

Section 2 – Introduction and Strategic Analysis 7

2.1 - Merlin Entertainments Competitors 10

2.2 - Merlin’s Strategy 10

2.3 - SWOT for Merlin Entertainment 13

Section 3 - Literature Review and Introduction 15

3.1 - Methods of financial analysis that can be conducted using

publicly available information.

15

3.2 – Ration analysis 15

3.3 - Advantages of ratio analysis 16

3.4 – Trend analysis 16

3.5 - Advantages and Disadvantages of Trend Analysis: 17

3.6 - Vertical Analysis 17

3.7 – Horizontal Analysis 18

3.8 - Empirical evidence based on Merlin Entertainment: 18

3.9 - Methods and usefulness of business valuation techniques 19

3.10 - Extent to which financial analysis and valuations using

publicly available corporate information that provides a

faithful representation

22

3.11 - Conclusions regarding information and tools that needs to

be used in the completion of financial analysis and

company valuation

23

Section 4 – Financial Analysis 24

4.1 - Profitability 24

4.2 - ROE and ROCE 28

4.3 – Liquidity and Working Capital Efficiencies 29

4.4 - Total and non-current asset efficiency 34

4.5 - Financial Gearing 36

Section 5 – Business Valuation 39

Market Cap, Book Value per share, P/E ratio 39

5.1 - Discounted Free Cash Flow 41

5.2 - Conclusion 41

Section 6 – Conclusion 43

6.1 - Conclusions and Recommendations for Merlin 43

Appendix 1 - 48

1.1 - Balance sheet for DMP and BPB 2015, 2016 and 2017 50

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 - Income Satatements for Merlin 2015, 2016 and 2017 51

1.3 - Income statements for DMP 2015, 2016 and 2017 51

1.4 - Income statement for Blackpool Pleasure Beach 2015, 2016

and 2017 results

52

1.5 - Cashflow Statements of DMP, BPB and Merlin 52

1.6 - Industry Medians – Reuters 53

Appendix 2 - 54

2.1 - Liquidity, Working Capital Efficiency and Total and Non-Current

Asset Efficiency Calculations

54

Appendix 3 - 55

3.1 - Financial Gearing 55

3.2 - Merlin calculations 55

3.3 - BPB calculations 55

3.4 - DMP calculations 56

Appendix 4 - 57

4.1 - Profitability ratios. Income Satatements extracts for Merlin

2015, 2016 and 2017

57

4.2 - Profitability calculations 58

4.3 - ROCE for Merlin with taxes in 2017 58

4.4 - Income statements for DMP 2015, 2016 and 2017 58

4.5 - Income Statement for Blackpool Pleasure Beach 2015, 2016

and 2017 results

59

4.6 - DMP and Merlin extracts for hotel prices 59

Appendix 5 - 60

5.0 - Business valuation calculations 60

5.1 - Merlin interim 2018 cashflow extracts 61

5.2 - Merlin Interim income statement and balance sheet 2018. 62

5.3 - Interim 2018 revenue growth of Merlin 63

Appendix 6 – 63

Discounted free cash flow calculations 63

6.1 - Extracts for CAPM 64

6.2 - Growth rate calculation for free cash flow 66

6.3 - Second method to ascertain growth rate 67

6.4 - WACC fir Merlin 67

6.5 - DFCF calculation 67

Appendix 7 - 69

7.1 - Book Value calculation of Merlin Entertainment 69

7.2 - P/E ratio calculation 69

References - 71

4

1.3 - Income statements for DMP 2015, 2016 and 2017 51

1.4 - Income statement for Blackpool Pleasure Beach 2015, 2016

and 2017 results

52

1.5 - Cashflow Statements of DMP, BPB and Merlin 52

1.6 - Industry Medians – Reuters 53

Appendix 2 - 54

2.1 - Liquidity, Working Capital Efficiency and Total and Non-Current

Asset Efficiency Calculations

54

Appendix 3 - 55

3.1 - Financial Gearing 55

3.2 - Merlin calculations 55

3.3 - BPB calculations 55

3.4 - DMP calculations 56

Appendix 4 - 57

4.1 - Profitability ratios. Income Satatements extracts for Merlin

2015, 2016 and 2017

57

4.2 - Profitability calculations 58

4.3 - ROCE for Merlin with taxes in 2017 58

4.4 - Income statements for DMP 2015, 2016 and 2017 58

4.5 - Income Statement for Blackpool Pleasure Beach 2015, 2016

and 2017 results

59

4.6 - DMP and Merlin extracts for hotel prices 59

Appendix 5 - 60

5.0 - Business valuation calculations 60

5.1 - Merlin interim 2018 cashflow extracts 61

5.2 - Merlin Interim income statement and balance sheet 2018. 62

5.3 - Interim 2018 revenue growth of Merlin 63

Appendix 6 – 63

Discounted free cash flow calculations 63

6.1 - Extracts for CAPM 64

6.2 - Growth rate calculation for free cash flow 66

6.3 - Second method to ascertain growth rate 67

6.4 - WACC fir Merlin 67

6.5 - DFCF calculation 67

Appendix 7 - 69

7.1 - Book Value calculation of Merlin Entertainment 69

7.2 - P/E ratio calculation 69

References - 71

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section 1- Executive Summary

This report was undertaken to understand the strategic, financial and business analysis of

Merlin Entertainment for investment purposes. An overview of the firm and an analysis of the

strategic position was undertaken in section two, which states Merlin has six strategic growth

drivers to achieve by 2020 and this will increase their asset base. Furthermore, Merlin

changed a portion of their strategy mid-term 2018 for better returns to be attained. Due to

the crash at Alton Towers and terrorism scares at London, Merlin had lower visitor numbers

in 2017, however, interim results 2018 state that there is a rise in revenue turnover of 4.5%

from previous results suggesting a small recovery is taking place.

The financial analysis of Merlin is conducted in section four of the report and critically

analyses the profitability, ROE & ROCE, liquidity and working capital efficiency, total and

non-current asset efficiency and financial gearing of Merlin Entertainment alongside Drayton

Manor Park and Blackpool Pleasure Beach. The profitability ratios of Merlin are positive

except for the U.K which stated static results, the reason Merlin changed their strategy

midway 2018 indicating quick reactions from the board.

Overall Merlin are ahead of competitors and industry medians with all the above analysis

except for total and non-current asset efficiency and financial gearing in the industry. Merlin’s

total and non-current assets efficiency revealed investments that are going to be realised in

the future. The firms have a high gearing ratio of around 50% debt to equity which is rising

every year as the firm takes on more debt.

Business valuation of Merlin revealed that there was a fall in the share price in 2017 (£3.63)

and this had recovered in 2018 to £4 per share. The reason the share price reduced in 2017

was because Merlin issued extra ordinary shares as part of their group employee share

incentive scheme and costs increases did not match revenue increases due to static

turnover in the U.K. Merlin’s market capitalisation as at 29/09/2018 is £4.09 billion. 2017

book value of Merlin is £1.53 indicating the market has over valued the share price, and on

that basis Merlin’s market per share is positive and fair as they have intellectual property in

their total assets which are going to be realised to profits moving forward.

However, both valuation methods did not incorporate future earnings of Merlin so a

discounted free cashflow method was used which determined a share price of £11.88 based

on a cashflow growth rate of 6%. The recommendations that were given in the report was to

retain dividend payments for a certain period or even take on extra debt to achieve a share

price close to £11.88.

5

This report was undertaken to understand the strategic, financial and business analysis of

Merlin Entertainment for investment purposes. An overview of the firm and an analysis of the

strategic position was undertaken in section two, which states Merlin has six strategic growth

drivers to achieve by 2020 and this will increase their asset base. Furthermore, Merlin

changed a portion of their strategy mid-term 2018 for better returns to be attained. Due to

the crash at Alton Towers and terrorism scares at London, Merlin had lower visitor numbers

in 2017, however, interim results 2018 state that there is a rise in revenue turnover of 4.5%

from previous results suggesting a small recovery is taking place.

The financial analysis of Merlin is conducted in section four of the report and critically

analyses the profitability, ROE & ROCE, liquidity and working capital efficiency, total and

non-current asset efficiency and financial gearing of Merlin Entertainment alongside Drayton

Manor Park and Blackpool Pleasure Beach. The profitability ratios of Merlin are positive

except for the U.K which stated static results, the reason Merlin changed their strategy

midway 2018 indicating quick reactions from the board.

Overall Merlin are ahead of competitors and industry medians with all the above analysis

except for total and non-current asset efficiency and financial gearing in the industry. Merlin’s

total and non-current assets efficiency revealed investments that are going to be realised in

the future. The firms have a high gearing ratio of around 50% debt to equity which is rising

every year as the firm takes on more debt.

Business valuation of Merlin revealed that there was a fall in the share price in 2017 (£3.63)

and this had recovered in 2018 to £4 per share. The reason the share price reduced in 2017

was because Merlin issued extra ordinary shares as part of their group employee share

incentive scheme and costs increases did not match revenue increases due to static

turnover in the U.K. Merlin’s market capitalisation as at 29/09/2018 is £4.09 billion. 2017

book value of Merlin is £1.53 indicating the market has over valued the share price, and on

that basis Merlin’s market per share is positive and fair as they have intellectual property in

their total assets which are going to be realised to profits moving forward.

However, both valuation methods did not incorporate future earnings of Merlin so a

discounted free cashflow method was used which determined a share price of £11.88 based

on a cashflow growth rate of 6%. The recommendations that were given in the report was to

retain dividend payments for a certain period or even take on extra debt to achieve a share

price close to £11.88.

5

This report concluded that due to the rising share price and the prospects of the company

looking positive moving forward, Merlin is a good candidate for investment. Merlin have a

geographical portfolio and the losses of the firm can be averaged out making Merlin a less

risky firm to invest in. However, returns from certain investments may take longer to realise

into profits while some returns may be realised sooner.

518 words

6

looking positive moving forward, Merlin is a good candidate for investment. Merlin have a

geographical portfolio and the losses of the firm can be averaged out making Merlin a less

risky firm to invest in. However, returns from certain investments may take longer to realise

into profits while some returns may be realised sooner.

518 words

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 2 – Introduction and Strategic Analysis

Merlin Entertainment are a UK based company that are in business in the leisure industry.

Merlin was incorporated in September 2013, and is headquartered in Poole Dorset, England

and has 3 parent shareholders. Blackstone (NYSE: BX), KIRKBI A/S and CVC Capital

Partners (‘CVC’). Merlin run and own 124 attractions in 25 countries covering four

continents, they also operate 18 hotels, six holiday villages across the four continents. Merlin

is Europe’s Number one entertainer in attractions and they are the second most visited

attraction operator in the world (Merlin Entertainments, 2018).

Merlin is listed on the London stock exchange and is on the FTSE 100. Recently, due to

health and safety issues at Alton Towers, Merlin share price has been declining, and there

was a fall in the FTSE. However, they decided to split the asset-backed theme parks and the

Legoland franchise from Midway (Financial Times, 2017a). By doing so, Merlin has created

value by the split. As Merlin is on the London stock exchange, they need to comply with the

UK Corporate Governance Code, The Disclosure and Transparency Rule and the Listings

rule (Merlin Entertainments, 2018).

Merlin take the responsibility of corporate governance very seriously. They are committed to

high standards of corporate governance across the whole group and their shareholders. The

main board at merlin take the responsibility of the strategy and the management of their

strategy by holding 6 meetings throughout the year, and more if needed, to ensure

objectives are met. Also, the way the chairman and board of directors under each committee

are nominated are in accordance with UK Corporate Governance Code and the Listing Rule.

Merlin is in the theme park industry and have a Health & Safety and Security Committee

along-side the standard committees, Audit, Nomination and Remuneration (Merlin

Entertainments, 2018).

Merlin is required to prepare their group accounts annual financial statements in accordance

with International Financial Reporting Standards (IFRS) that are adopted by the EU

(Adopted IFRS) and all the law that is applicable. The company’s annual financial

statements must be prepared to confer with the UK Accounting Standards and FRS 101

(Reduced Disclosure Framework) (Merlin Annual Report, 2016).

As mentioned above Merlin has many commodities that complement each other. Such as,

the hotels which are located in the theme parks, so visitors stay longer.

7

Merlin Entertainment are a UK based company that are in business in the leisure industry.

Merlin was incorporated in September 2013, and is headquartered in Poole Dorset, England

and has 3 parent shareholders. Blackstone (NYSE: BX), KIRKBI A/S and CVC Capital

Partners (‘CVC’). Merlin run and own 124 attractions in 25 countries covering four

continents, they also operate 18 hotels, six holiday villages across the four continents. Merlin

is Europe’s Number one entertainer in attractions and they are the second most visited

attraction operator in the world (Merlin Entertainments, 2018).

Merlin is listed on the London stock exchange and is on the FTSE 100. Recently, due to

health and safety issues at Alton Towers, Merlin share price has been declining, and there

was a fall in the FTSE. However, they decided to split the asset-backed theme parks and the

Legoland franchise from Midway (Financial Times, 2017a). By doing so, Merlin has created

value by the split. As Merlin is on the London stock exchange, they need to comply with the

UK Corporate Governance Code, The Disclosure and Transparency Rule and the Listings

rule (Merlin Entertainments, 2018).

Merlin take the responsibility of corporate governance very seriously. They are committed to

high standards of corporate governance across the whole group and their shareholders. The

main board at merlin take the responsibility of the strategy and the management of their

strategy by holding 6 meetings throughout the year, and more if needed, to ensure

objectives are met. Also, the way the chairman and board of directors under each committee

are nominated are in accordance with UK Corporate Governance Code and the Listing Rule.

Merlin is in the theme park industry and have a Health & Safety and Security Committee

along-side the standard committees, Audit, Nomination and Remuneration (Merlin

Entertainments, 2018).

Merlin is required to prepare their group accounts annual financial statements in accordance

with International Financial Reporting Standards (IFRS) that are adopted by the EU

(Adopted IFRS) and all the law that is applicable. The company’s annual financial

statements must be prepared to confer with the UK Accounting Standards and FRS 101

(Reduced Disclosure Framework) (Merlin Annual Report, 2016).

As mentioned above Merlin has many commodities that complement each other. Such as,

the hotels which are located in the theme parks, so visitors stay longer.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Merlin Entertainments, 2018)

Merlin have two products –

Midway and

Theme parks.

Their Midway attractions are indoor with a two-hour experience of fun and are located

around city centres and resorts; these are Sea-Life Centre, The Dungeons, Madame

Tussauds, Shrek’s Adventure, Warwick Castle, The Eye Brand and Legoland Discovery

centres. There are 104 Midway attractions spread across Merlin’s global portfolio which has

accounted for 44% of Merlin’s revenue in 2016. Merlin are growing their Midway attractions

across the globe with 100+ locations that they have identified (Introduction to Merlin

Entertainments, 2016).

Merlin has three operating groups, Midway, theme parks and the Legoland parks. Theme

parks have a 1-3-day fun experience that have onsite accommodation for visitors. There are

6 parks, Alton Towers, Thorpe Park, Chessington World of Adventures, Warwick Castle,

Gardaland, and Heide Park that accounted for 22% of revenue for the group in 2016. Merlin

has 7 Legoland Parks across its global portfolio and a 34% revenue stream for the group in

2016 (Introduction to Merlin Entertainments, 2016).

Merlin has many complementary commercial operations that run throughout their three

operating groups. Merlin has restaurants, games, shops that sell trophies and photos of

visitors, so they can cherish their memories. They sell drinks and slush throughout their

theme parks for thirsty visitors and are constantly making updates to their attractions with the

help of their research and development team, Merlin Magic Making (Merlin Entertainments,

2018). Merlin are in the family entertainment industry with strong brands, their market are

adults and children’s off all ages, this gives Merlin an advantage as their market is everyone

who wants to enjoy fun days out and a couple of days break. Merlin has even targeted

8

Merlin have two products –

Midway and

Theme parks.

Their Midway attractions are indoor with a two-hour experience of fun and are located

around city centres and resorts; these are Sea-Life Centre, The Dungeons, Madame

Tussauds, Shrek’s Adventure, Warwick Castle, The Eye Brand and Legoland Discovery

centres. There are 104 Midway attractions spread across Merlin’s global portfolio which has

accounted for 44% of Merlin’s revenue in 2016. Merlin are growing their Midway attractions

across the globe with 100+ locations that they have identified (Introduction to Merlin

Entertainments, 2016).

Merlin has three operating groups, Midway, theme parks and the Legoland parks. Theme

parks have a 1-3-day fun experience that have onsite accommodation for visitors. There are

6 parks, Alton Towers, Thorpe Park, Chessington World of Adventures, Warwick Castle,

Gardaland, and Heide Park that accounted for 22% of revenue for the group in 2016. Merlin

has 7 Legoland Parks across its global portfolio and a 34% revenue stream for the group in

2016 (Introduction to Merlin Entertainments, 2016).

Merlin has many complementary commercial operations that run throughout their three

operating groups. Merlin has restaurants, games, shops that sell trophies and photos of

visitors, so they can cherish their memories. They sell drinks and slush throughout their

theme parks for thirsty visitors and are constantly making updates to their attractions with the

help of their research and development team, Merlin Magic Making (Merlin Entertainments,

2018). Merlin are in the family entertainment industry with strong brands, their market are

adults and children’s off all ages, this gives Merlin an advantage as their market is everyone

who wants to enjoy fun days out and a couple of days break. Merlin has even targeted

8

babies as their market, by opening CBeebies world in Alton Towers; they even have a

CBeebies hotel at the resort.

(CBeebies Land and Hotel, 2018)

Over view of the market for Merlin seems positive as there are many emerging middle-

classes globally that are willing to travel for entertainment as fares for flights are low; 1.8

billion visitors are anticipated to travel by 2030, this is an increase of three-folds from 2000

results (Merlin Entertainment, Annual reports and 2017; p19). However, the International

environment seems volatile due to visa restrictions in some areas such as, People’s

Republic of China have visa restrictions to fly to Hong Kong because of terror attack

activities. Also, terror attacks in the heart of London are the reason Merlin had a decrease in

revenue in London, 2017. Terror attacks have affected foreign exchange rates on

international tourism bringing exchange rate losses to Merlin, but this is not a permanent risk

to Merlin as security tightens up globally (Merlin Entertainment, Annual reports and 2017;

p19).

9

CBeebies hotel at the resort.

(CBeebies Land and Hotel, 2018)

Over view of the market for Merlin seems positive as there are many emerging middle-

classes globally that are willing to travel for entertainment as fares for flights are low; 1.8

billion visitors are anticipated to travel by 2030, this is an increase of three-folds from 2000

results (Merlin Entertainment, Annual reports and 2017; p19). However, the International

environment seems volatile due to visa restrictions in some areas such as, People’s

Republic of China have visa restrictions to fly to Hong Kong because of terror attack

activities. Also, terror attacks in the heart of London are the reason Merlin had a decrease in

revenue in London, 2017. Terror attacks have affected foreign exchange rates on

international tourism bringing exchange rate losses to Merlin, but this is not a permanent risk

to Merlin as security tightens up globally (Merlin Entertainment, Annual reports and 2017;

p19).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

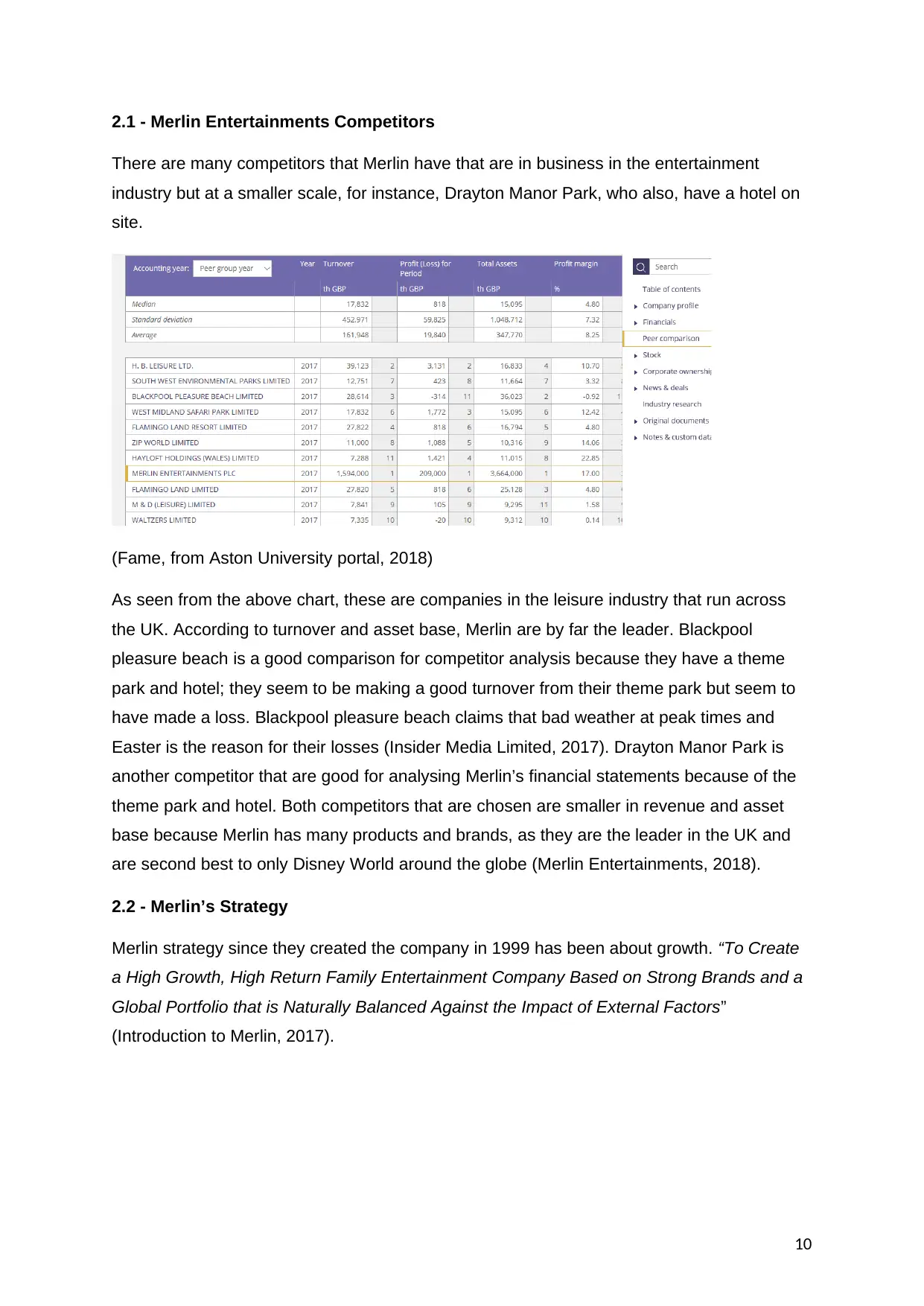

2.1 - Merlin Entertainments Competitors

There are many competitors that Merlin have that are in business in the entertainment

industry but at a smaller scale, for instance, Drayton Manor Park, who also, have a hotel on

site.

(Fame, from Aston University portal, 2018)

As seen from the above chart, these are companies in the leisure industry that run across

the UK. According to turnover and asset base, Merlin are by far the leader. Blackpool

pleasure beach is a good comparison for competitor analysis because they have a theme

park and hotel; they seem to be making a good turnover from their theme park but seem to

have made a loss. Blackpool pleasure beach claims that bad weather at peak times and

Easter is the reason for their losses (Insider Media Limited, 2017). Drayton Manor Park is

another competitor that are good for analysing Merlin’s financial statements because of the

theme park and hotel. Both competitors that are chosen are smaller in revenue and asset

base because Merlin has many products and brands, as they are the leader in the UK and

are second best to only Disney World around the globe (Merlin Entertainments, 2018).

2.2 - Merlin’s Strategy

Merlin strategy since they created the company in 1999 has been about growth. “To Create

a High Growth, High Return Family Entertainment Company Based on Strong Brands and a

Global Portfolio that is Naturally Balanced Against the Impact of External Factors”

(Introduction to Merlin, 2017).

10

There are many competitors that Merlin have that are in business in the entertainment

industry but at a smaller scale, for instance, Drayton Manor Park, who also, have a hotel on

site.

(Fame, from Aston University portal, 2018)

As seen from the above chart, these are companies in the leisure industry that run across

the UK. According to turnover and asset base, Merlin are by far the leader. Blackpool

pleasure beach is a good comparison for competitor analysis because they have a theme

park and hotel; they seem to be making a good turnover from their theme park but seem to

have made a loss. Blackpool pleasure beach claims that bad weather at peak times and

Easter is the reason for their losses (Insider Media Limited, 2017). Drayton Manor Park is

another competitor that are good for analysing Merlin’s financial statements because of the

theme park and hotel. Both competitors that are chosen are smaller in revenue and asset

base because Merlin has many products and brands, as they are the leader in the UK and

are second best to only Disney World around the globe (Merlin Entertainments, 2018).

2.2 - Merlin’s Strategy

Merlin strategy since they created the company in 1999 has been about growth. “To Create

a High Growth, High Return Family Entertainment Company Based on Strong Brands and a

Global Portfolio that is Naturally Balanced Against the Impact of External Factors”

(Introduction to Merlin, 2017).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Introduction to Merlin, 2017; p 4)

According to the above chart, Merlin analyses revenue by weather exposure. Blackpool

made a loss because their theme park is an outdoor entertainment. Because Merlin has

indoor entertainment such as the Sea Life Centre not only are they not effected by the

weather, but they run all year around generating 61% of annual profits. Also, they have

increased in size by an extra 40 sites and moved in 7 new countries from 2011 to 2016.

However, 2017 medium-term adjustments were made to the strategy, and capital allocation

reduced at midway attractions and was allocated to accommodation as strong returns and

productivity was reported (Merlin, 2017: p19). Merlin’s cash flow risk is kept at a minimum by

having strong relationships with lenders and keeping an eye on the debt market, so funds

can be attained at the right price and time to meet strategy (Merlin, 2017: p39).

(Introduction to Merlin, 2017; p 5)

As you can see from the above context, Merlin has increased leisure spend in a 10-year

span, from 2015 to 2025. They have invested in short breaks and hit the city centre as a

11

According to the above chart, Merlin analyses revenue by weather exposure. Blackpool

made a loss because their theme park is an outdoor entertainment. Because Merlin has

indoor entertainment such as the Sea Life Centre not only are they not effected by the

weather, but they run all year around generating 61% of annual profits. Also, they have

increased in size by an extra 40 sites and moved in 7 new countries from 2011 to 2016.

However, 2017 medium-term adjustments were made to the strategy, and capital allocation

reduced at midway attractions and was allocated to accommodation as strong returns and

productivity was reported (Merlin, 2017: p19). Merlin’s cash flow risk is kept at a minimum by

having strong relationships with lenders and keeping an eye on the debt market, so funds

can be attained at the right price and time to meet strategy (Merlin, 2017: p39).

(Introduction to Merlin, 2017; p 5)

As you can see from the above context, Merlin has increased leisure spend in a 10-year

span, from 2015 to 2025. They have invested in short breaks and hit the city centre as a

11

location for their all year around Midway attractions in many countries around the world.

Legoland has been a big hit for Merlin Entertainment as holding global exclusive rights to the

brand name as their competitive advantage.

Merlin has six strategic growth drivers to hit by 2020.

1- They add new rides to existing theme parks, so visitors can enjoy a new experience.

2- Strategic synergies are created by merlin, so they can extend operational efficiency

and exploit larger markets with buying power.

3- Turning theme parks into short breaks by adding 2000 new rooms for visitors by

2020.

4- Midway roll out are clustered around the globe to take advantage of lower operating

and marketing costs and cross selling advantages.

5- Creating new Lego Land theme parks around the globe.

6- Any opportunity of acquisitions that complement their existing business. Merlin is also

holding tour bus operations (Introduction to Merlin, 2017; p 6).

Merlin has 2 strategic synergies, Merlin Annual Pass and accesso roll out to bring in

revenue. The Annual pass allows customers access to Merlin’s attraction around the country

they purchase in. Merlin has three types of annual passes. Standard pass that allows

discounts across its attractions. Premium pass holders get free drinks and extra perks

around their attractions plus free parking at some attractions. VIP pass holders have access

to all theme parks around the globe. This helps Merlin with advanced cashflows and

assurance that complementary products will generate revenue such as their restaurants and

gift shops (Introduction to Merlin, 2017; p 12). Merlin has achieved high growth in revenue

from these annual passes in UK, Germany, Australia and the USA. Cashflows are averaged

out during the year for accounting purposes.

Accesso roll out is a way of selling tickets to visitors in a fast and convenient way. Merlin

holds mobile sales and ticketing that help with up-selling, cross-selling, quick-selling with

their SAAS software as a service. They also work on que busting for efficiency. Furthermore,

Merlin hold group promotions for extra revenue using a number of brands such as Tesco,

News International, McDonalds and Kellogg’s. Recently, Merlin has joined in partnership

with Coca-Cola, who offer 50% of entry at their 30 attractions in the U.K when the customer

returns their 500ml bottle (Introduction to Merlin, 2017; p 12) (Merlin Entertainment,

Recycling Initiative, 2018).

12

Legoland has been a big hit for Merlin Entertainment as holding global exclusive rights to the

brand name as their competitive advantage.

Merlin has six strategic growth drivers to hit by 2020.

1- They add new rides to existing theme parks, so visitors can enjoy a new experience.

2- Strategic synergies are created by merlin, so they can extend operational efficiency

and exploit larger markets with buying power.

3- Turning theme parks into short breaks by adding 2000 new rooms for visitors by

2020.

4- Midway roll out are clustered around the globe to take advantage of lower operating

and marketing costs and cross selling advantages.

5- Creating new Lego Land theme parks around the globe.

6- Any opportunity of acquisitions that complement their existing business. Merlin is also

holding tour bus operations (Introduction to Merlin, 2017; p 6).

Merlin has 2 strategic synergies, Merlin Annual Pass and accesso roll out to bring in

revenue. The Annual pass allows customers access to Merlin’s attraction around the country

they purchase in. Merlin has three types of annual passes. Standard pass that allows

discounts across its attractions. Premium pass holders get free drinks and extra perks

around their attractions plus free parking at some attractions. VIP pass holders have access

to all theme parks around the globe. This helps Merlin with advanced cashflows and

assurance that complementary products will generate revenue such as their restaurants and

gift shops (Introduction to Merlin, 2017; p 12). Merlin has achieved high growth in revenue

from these annual passes in UK, Germany, Australia and the USA. Cashflows are averaged

out during the year for accounting purposes.

Accesso roll out is a way of selling tickets to visitors in a fast and convenient way. Merlin

holds mobile sales and ticketing that help with up-selling, cross-selling, quick-selling with

their SAAS software as a service. They also work on que busting for efficiency. Furthermore,

Merlin hold group promotions for extra revenue using a number of brands such as Tesco,

News International, McDonalds and Kellogg’s. Recently, Merlin has joined in partnership

with Coca-Cola, who offer 50% of entry at their 30 attractions in the U.K when the customer

returns their 500ml bottle (Introduction to Merlin, 2017; p 12) (Merlin Entertainment,

Recycling Initiative, 2018).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 76

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.