Financial Management Report: EasyJet Valuation and Capital Analysis

VerifiedAdded on 2020/01/07

|13

|3537

|169

Report

AI Summary

This report provides a detailed financial analysis of EasyJet, covering various valuation methods and the estimation of the cost of capital. It begins by exploring methods for estimating the cost of capital, including cost of debt before and after tax, and the weighted average cost of capital (WACC), along with their limitations. The report then applies these methods to EasyJet's financial data. Furthermore, the report delves into different valuation techniques, such as the discounted cash flow (DCF) model, price-to-earnings (PE) ratio, and EV/EBITDA ratio, interpreting the results and offering insights into EasyJet's intrinsic value. The report includes detailed tables with calculations for cost of debt, equity, WACC, cash flows, and valuation multiples, providing a comprehensive overview of the financial analysis performed.

FINANCIAL MANAGEMENT IN

ORGANIZATION

ORGANIZATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

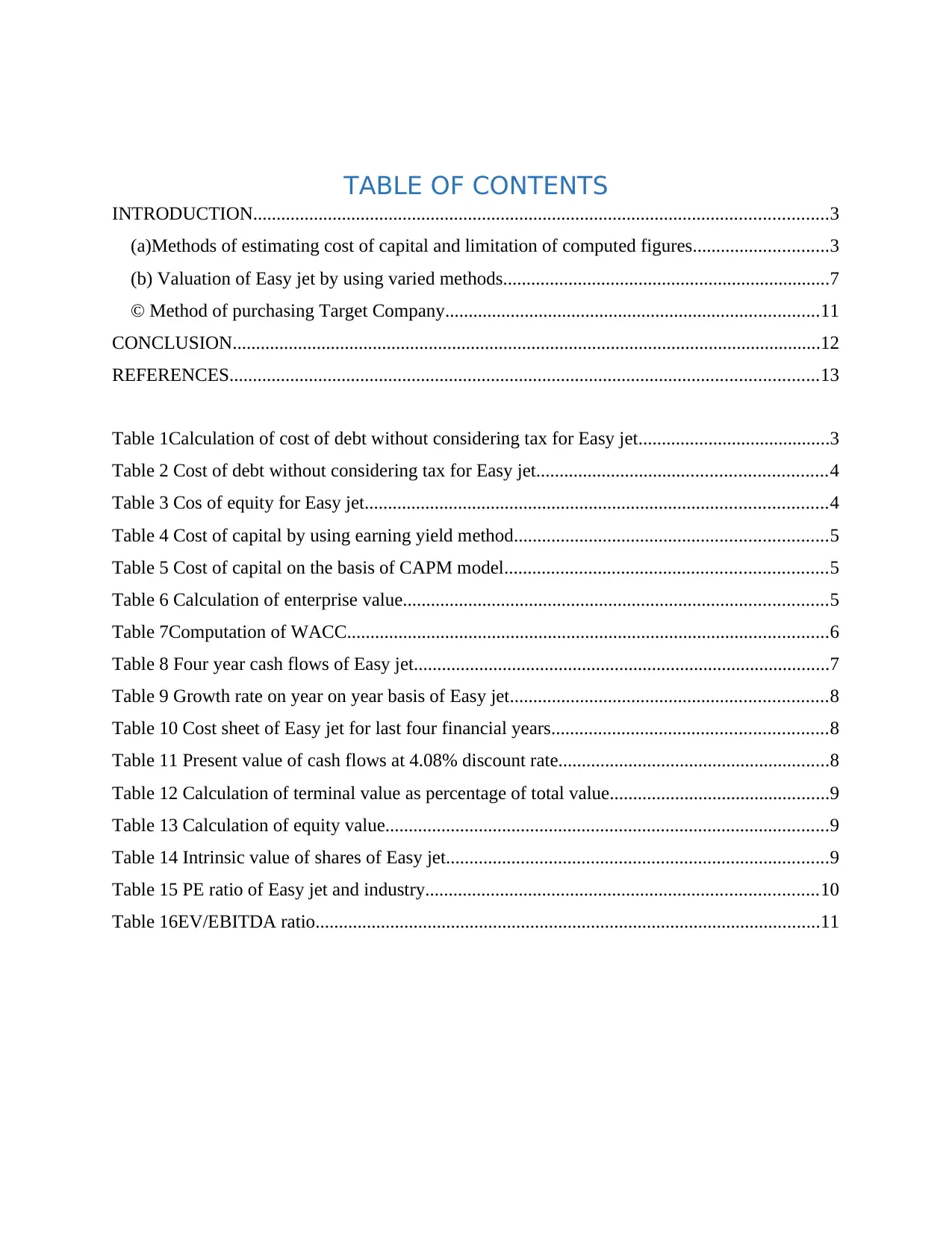

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

(a)Methods of estimating cost of capital and limitation of computed figures.............................3

(b) Valuation of Easy jet by using varied methods......................................................................7

© Method of purchasing Target Company................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Table 1Calculation of cost of debt without considering tax for Easy jet.........................................3

Table 2 Cost of debt without considering tax for Easy jet..............................................................4

Table 3 Cos of equity for Easy jet...................................................................................................4

Table 4 Cost of capital by using earning yield method...................................................................5

Table 5 Cost of capital on the basis of CAPM model.....................................................................5

Table 6 Calculation of enterprise value...........................................................................................5

Table 7Computation of WACC.......................................................................................................6

Table 8 Four year cash flows of Easy jet.........................................................................................7

Table 9 Growth rate on year on year basis of Easy jet....................................................................8

Table 10 Cost sheet of Easy jet for last four financial years...........................................................8

Table 11 Present value of cash flows at 4.08% discount rate..........................................................8

Table 12 Calculation of terminal value as percentage of total value...............................................9

Table 13 Calculation of equity value...............................................................................................9

Table 14 Intrinsic value of shares of Easy jet..................................................................................9

Table 15 PE ratio of Easy jet and industry....................................................................................10

Table 16EV/EBITDA ratio............................................................................................................11

INTRODUCTION...........................................................................................................................3

(a)Methods of estimating cost of capital and limitation of computed figures.............................3

(b) Valuation of Easy jet by using varied methods......................................................................7

© Method of purchasing Target Company................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Table 1Calculation of cost of debt without considering tax for Easy jet.........................................3

Table 2 Cost of debt without considering tax for Easy jet..............................................................4

Table 3 Cos of equity for Easy jet...................................................................................................4

Table 4 Cost of capital by using earning yield method...................................................................5

Table 5 Cost of capital on the basis of CAPM model.....................................................................5

Table 6 Calculation of enterprise value...........................................................................................5

Table 7Computation of WACC.......................................................................................................6

Table 8 Four year cash flows of Easy jet.........................................................................................7

Table 9 Growth rate on year on year basis of Easy jet....................................................................8

Table 10 Cost sheet of Easy jet for last four financial years...........................................................8

Table 11 Present value of cash flows at 4.08% discount rate..........................................................8

Table 12 Calculation of terminal value as percentage of total value...............................................9

Table 13 Calculation of equity value...............................................................................................9

Table 14 Intrinsic value of shares of Easy jet..................................................................................9

Table 15 PE ratio of Easy jet and industry....................................................................................10

Table 16EV/EBITDA ratio............................................................................................................11

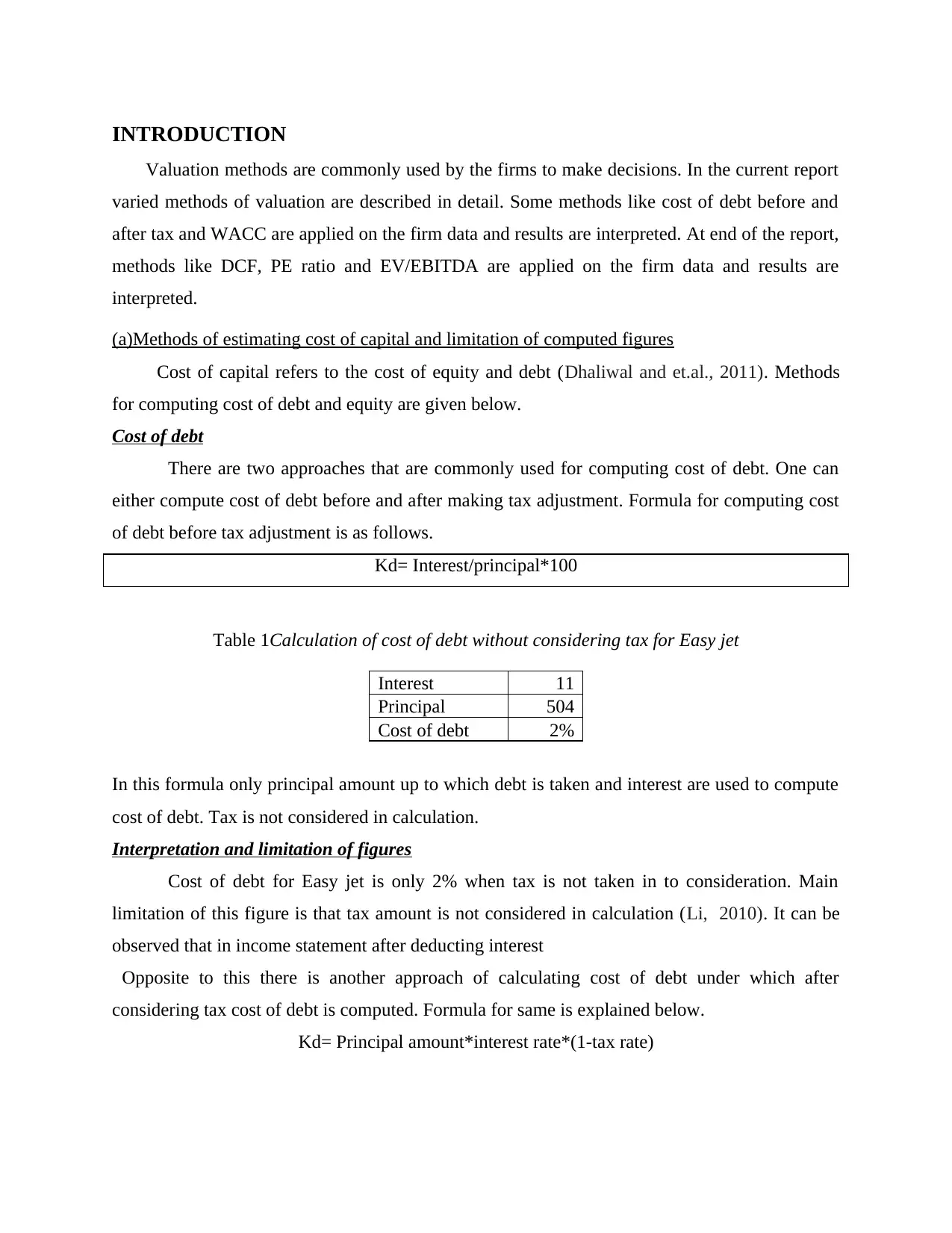

INTRODUCTION

Valuation methods are commonly used by the firms to make decisions. In the current report

varied methods of valuation are described in detail. Some methods like cost of debt before and

after tax and WACC are applied on the firm data and results are interpreted. At end of the report,

methods like DCF, PE ratio and EV/EBITDA are applied on the firm data and results are

interpreted.

(a)Methods of estimating cost of capital and limitation of computed figures

Cost of capital refers to the cost of equity and debt (Dhaliwal and et.al., 2011). Methods

for computing cost of debt and equity are given below.

Cost of debt

There are two approaches that are commonly used for computing cost of debt. One can

either compute cost of debt before and after making tax adjustment. Formula for computing cost

of debt before tax adjustment is as follows.

Kd= Interest/principal*100

Table 1Calculation of cost of debt without considering tax for Easy jet

Interest 11

Principal 504

Cost of debt 2%

In this formula only principal amount up to which debt is taken and interest are used to compute

cost of debt. Tax is not considered in calculation.

Interpretation and limitation of figures

Cost of debt for Easy jet is only 2% when tax is not taken in to consideration. Main

limitation of this figure is that tax amount is not considered in calculation (Li, 2010). It can be

observed that in income statement after deducting interest

Opposite to this there is another approach of calculating cost of debt under which after

considering tax cost of debt is computed. Formula for same is explained below.

Kd= Principal amount*interest rate*(1-tax rate)

Valuation methods are commonly used by the firms to make decisions. In the current report

varied methods of valuation are described in detail. Some methods like cost of debt before and

after tax and WACC are applied on the firm data and results are interpreted. At end of the report,

methods like DCF, PE ratio and EV/EBITDA are applied on the firm data and results are

interpreted.

(a)Methods of estimating cost of capital and limitation of computed figures

Cost of capital refers to the cost of equity and debt (Dhaliwal and et.al., 2011). Methods

for computing cost of debt and equity are given below.

Cost of debt

There are two approaches that are commonly used for computing cost of debt. One can

either compute cost of debt before and after making tax adjustment. Formula for computing cost

of debt before tax adjustment is as follows.

Kd= Interest/principal*100

Table 1Calculation of cost of debt without considering tax for Easy jet

Interest 11

Principal 504

Cost of debt 2%

In this formula only principal amount up to which debt is taken and interest are used to compute

cost of debt. Tax is not considered in calculation.

Interpretation and limitation of figures

Cost of debt for Easy jet is only 2% when tax is not taken in to consideration. Main

limitation of this figure is that tax amount is not considered in calculation (Li, 2010). It can be

observed that in income statement after deducting interest

Opposite to this there is another approach of calculating cost of debt under which after

considering tax cost of debt is computed. Formula for same is explained below.

Kd= Principal amount*interest rate*(1-tax rate)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

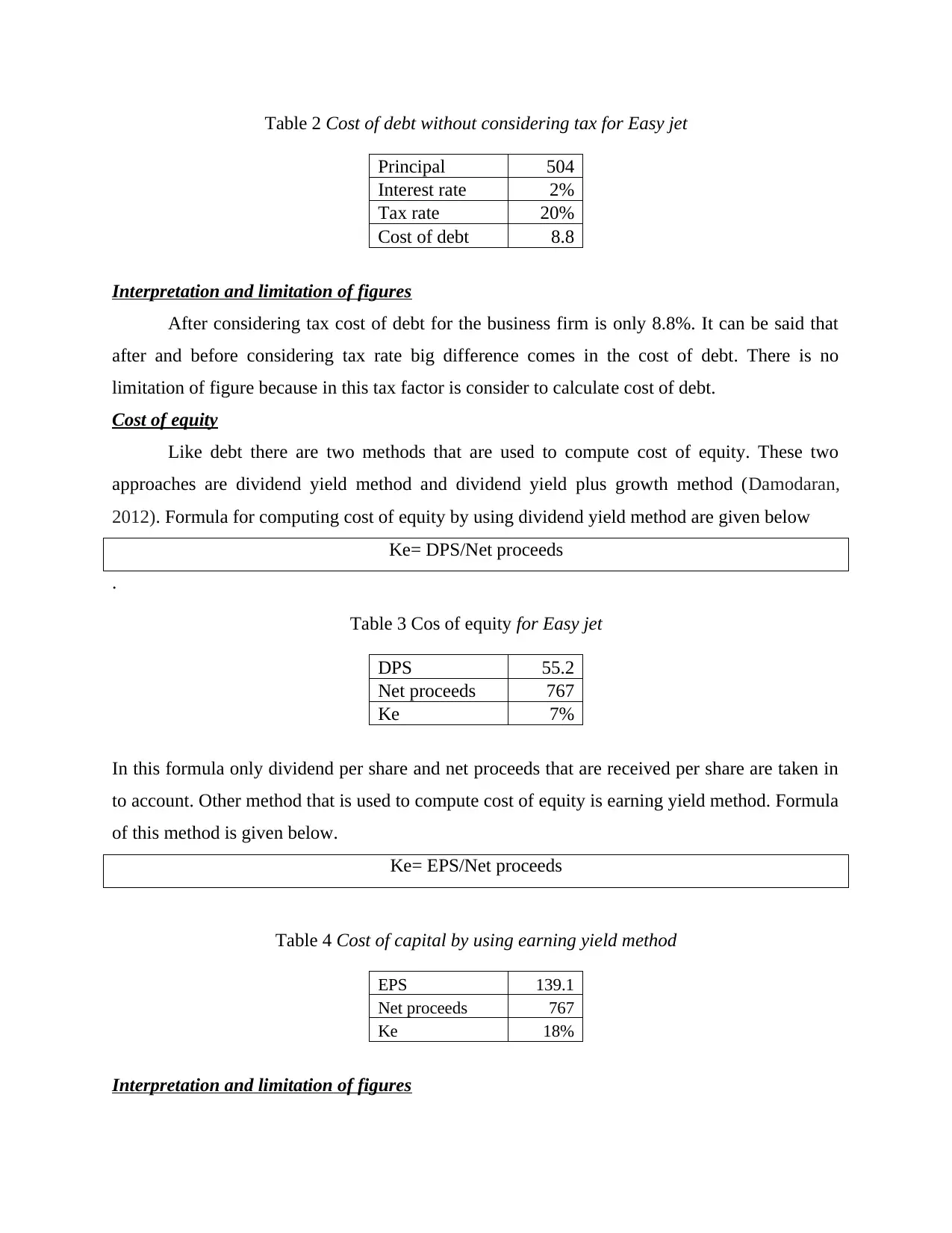

Table 2 Cost of debt without considering tax for Easy jet

Principal 504

Interest rate 2%

Tax rate 20%

Cost of debt 8.8

Interpretation and limitation of figures

After considering tax cost of debt for the business firm is only 8.8%. It can be said that

after and before considering tax rate big difference comes in the cost of debt. There is no

limitation of figure because in this tax factor is consider to calculate cost of debt.

Cost of equity

Like debt there are two methods that are used to compute cost of equity. These two

approaches are dividend yield method and dividend yield plus growth method (Damodaran,

2012). Formula for computing cost of equity by using dividend yield method are given below

Ke= DPS/Net proceeds

.

Table 3 Cos of equity for Easy jet

DPS 55.2

Net proceeds 767

Ke 7%

In this formula only dividend per share and net proceeds that are received per share are taken in

to account. Other method that is used to compute cost of equity is earning yield method. Formula

of this method is given below.

Ke= EPS/Net proceeds

Table 4 Cost of capital by using earning yield method

EPS 139.1

Net proceeds 767

Ke 18%

Interpretation and limitation of figures

Principal 504

Interest rate 2%

Tax rate 20%

Cost of debt 8.8

Interpretation and limitation of figures

After considering tax cost of debt for the business firm is only 8.8%. It can be said that

after and before considering tax rate big difference comes in the cost of debt. There is no

limitation of figure because in this tax factor is consider to calculate cost of debt.

Cost of equity

Like debt there are two methods that are used to compute cost of equity. These two

approaches are dividend yield method and dividend yield plus growth method (Damodaran,

2012). Formula for computing cost of equity by using dividend yield method are given below

Ke= DPS/Net proceeds

.

Table 3 Cos of equity for Easy jet

DPS 55.2

Net proceeds 767

Ke 7%

In this formula only dividend per share and net proceeds that are received per share are taken in

to account. Other method that is used to compute cost of equity is earning yield method. Formula

of this method is given below.

Ke= EPS/Net proceeds

Table 4 Cost of capital by using earning yield method

EPS 139.1

Net proceeds 767

Ke 18%

Interpretation and limitation of figures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

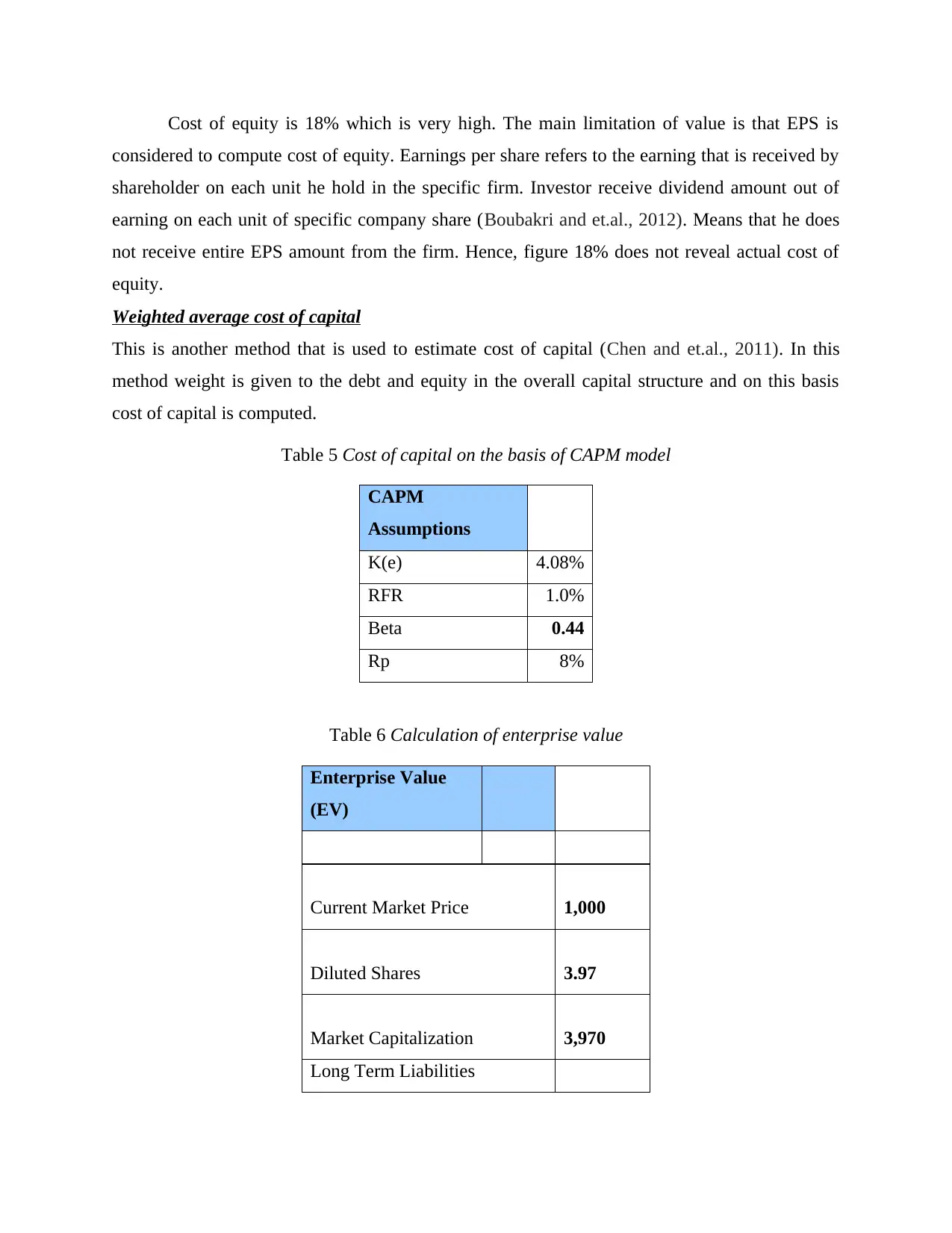

Cost of equity is 18% which is very high. The main limitation of value is that EPS is

considered to compute cost of equity. Earnings per share refers to the earning that is received by

shareholder on each unit he hold in the specific firm. Investor receive dividend amount out of

earning on each unit of specific company share (Boubakri and et.al., 2012). Means that he does

not receive entire EPS amount from the firm. Hence, figure 18% does not reveal actual cost of

equity.

Weighted average cost of capital

This is another method that is used to estimate cost of capital (Chen and et.al., 2011). In this

method weight is given to the debt and equity in the overall capital structure and on this basis

cost of capital is computed.

Table 5 Cost of capital on the basis of CAPM model

CAPM

Assumptions

K(e) 4.08%

RFR 1.0%

Beta 0.44

Rp 8%

Table 6 Calculation of enterprise value

Enterprise Value

(EV)

Current Market Price 1,000

Diluted Shares 3.97

Market Capitalization 3,970

Long Term Liabilities

considered to compute cost of equity. Earnings per share refers to the earning that is received by

shareholder on each unit he hold in the specific firm. Investor receive dividend amount out of

earning on each unit of specific company share (Boubakri and et.al., 2012). Means that he does

not receive entire EPS amount from the firm. Hence, figure 18% does not reveal actual cost of

equity.

Weighted average cost of capital

This is another method that is used to estimate cost of capital (Chen and et.al., 2011). In this

method weight is given to the debt and equity in the overall capital structure and on this basis

cost of capital is computed.

Table 5 Cost of capital on the basis of CAPM model

CAPM

Assumptions

K(e) 4.08%

RFR 1.0%

Beta 0.44

Rp 8%

Table 6 Calculation of enterprise value

Enterprise Value

(EV)

Current Market Price 1,000

Diluted Shares 3.97

Market Capitalization 3,970

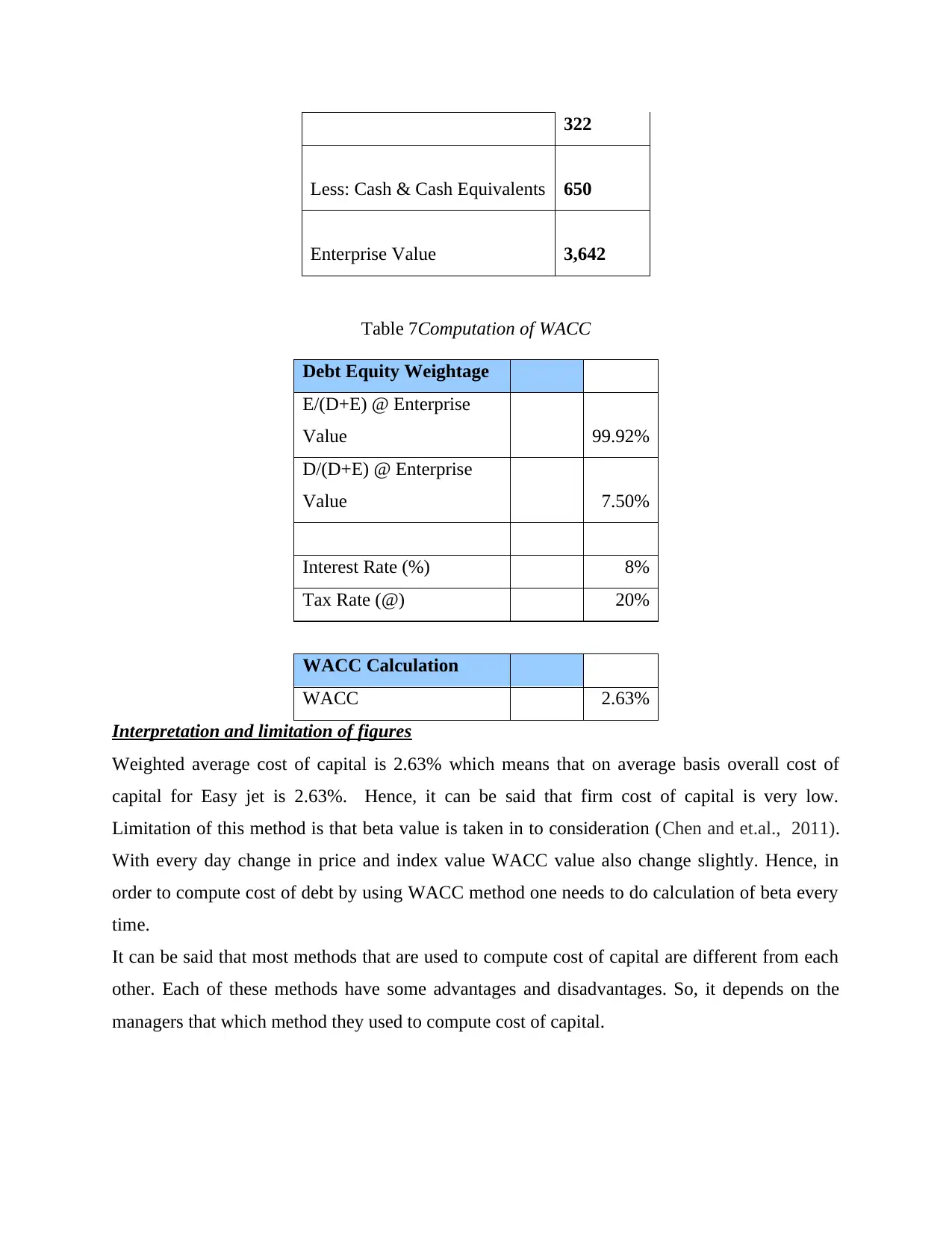

Long Term Liabilities

322

Less: Cash & Cash Equivalents 650

Enterprise Value 3,642

Table 7Computation of WACC

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 99.92%

D/(D+E) @ Enterprise

Value 7.50%

Interest Rate (%) 8%

Tax Rate (@) 20%

WACC Calculation

WACC 2.63%

Interpretation and limitation of figures

Weighted average cost of capital is 2.63% which means that on average basis overall cost of

capital for Easy jet is 2.63%. Hence, it can be said that firm cost of capital is very low.

Limitation of this method is that beta value is taken in to consideration (Chen and et.al., 2011).

With every day change in price and index value WACC value also change slightly. Hence, in

order to compute cost of debt by using WACC method one needs to do calculation of beta every

time.

It can be said that most methods that are used to compute cost of capital are different from each

other. Each of these methods have some advantages and disadvantages. So, it depends on the

managers that which method they used to compute cost of capital.

Less: Cash & Cash Equivalents 650

Enterprise Value 3,642

Table 7Computation of WACC

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 99.92%

D/(D+E) @ Enterprise

Value 7.50%

Interest Rate (%) 8%

Tax Rate (@) 20%

WACC Calculation

WACC 2.63%

Interpretation and limitation of figures

Weighted average cost of capital is 2.63% which means that on average basis overall cost of

capital for Easy jet is 2.63%. Hence, it can be said that firm cost of capital is very low.

Limitation of this method is that beta value is taken in to consideration (Chen and et.al., 2011).

With every day change in price and index value WACC value also change slightly. Hence, in

order to compute cost of debt by using WACC method one needs to do calculation of beta every

time.

It can be said that most methods that are used to compute cost of capital are different from each

other. Each of these methods have some advantages and disadvantages. So, it depends on the

managers that which method they used to compute cost of capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

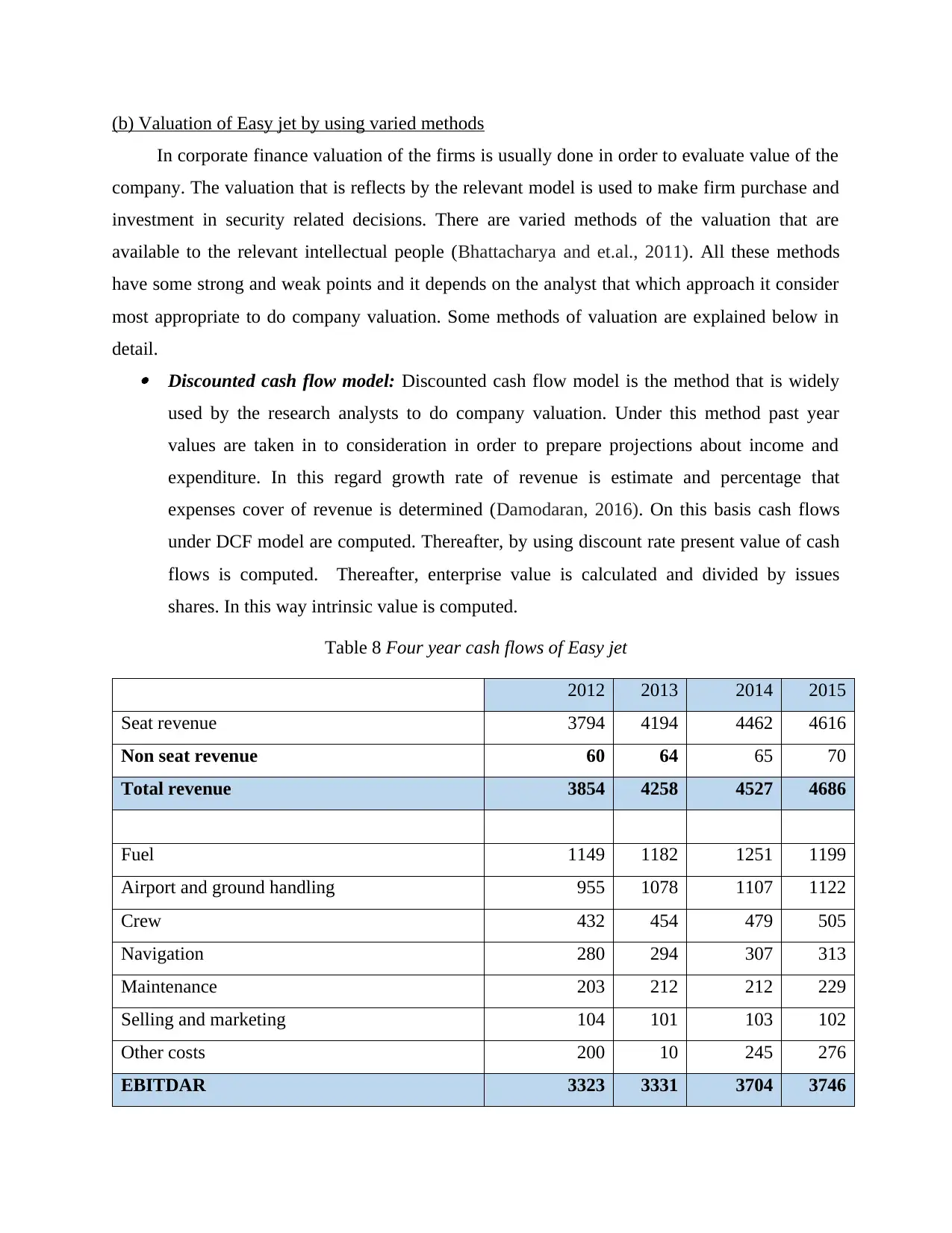

(b) Valuation of Easy jet by using varied methods

In corporate finance valuation of the firms is usually done in order to evaluate value of the

company. The valuation that is reflects by the relevant model is used to make firm purchase and

investment in security related decisions. There are varied methods of the valuation that are

available to the relevant intellectual people (Bhattacharya and et.al., 2011). All these methods

have some strong and weak points and it depends on the analyst that which approach it consider

most appropriate to do company valuation. Some methods of valuation are explained below in

detail. Discounted cash flow model: Discounted cash flow model is the method that is widely

used by the research analysts to do company valuation. Under this method past year

values are taken in to consideration in order to prepare projections about income and

expenditure. In this regard growth rate of revenue is estimate and percentage that

expenses cover of revenue is determined (Damodaran, 2016). On this basis cash flows

under DCF model are computed. Thereafter, by using discount rate present value of cash

flows is computed. Thereafter, enterprise value is calculated and divided by issues

shares. In this way intrinsic value is computed.

Table 8 Four year cash flows of Easy jet

2012 2013 2014 2015

Seat revenue 3794 4194 4462 4616

Non seat revenue 60 64 65 70

Total revenue 3854 4258 4527 4686

Fuel 1149 1182 1251 1199

Airport and ground handling 955 1078 1107 1122

Crew 432 454 479 505

Navigation 280 294 307 313

Maintenance 203 212 212 229

Selling and marketing 104 101 103 102

Other costs 200 10 245 276

EBITDAR 3323 3331 3704 3746

In corporate finance valuation of the firms is usually done in order to evaluate value of the

company. The valuation that is reflects by the relevant model is used to make firm purchase and

investment in security related decisions. There are varied methods of the valuation that are

available to the relevant intellectual people (Bhattacharya and et.al., 2011). All these methods

have some strong and weak points and it depends on the analyst that which approach it consider

most appropriate to do company valuation. Some methods of valuation are explained below in

detail. Discounted cash flow model: Discounted cash flow model is the method that is widely

used by the research analysts to do company valuation. Under this method past year

values are taken in to consideration in order to prepare projections about income and

expenditure. In this regard growth rate of revenue is estimate and percentage that

expenses cover of revenue is determined (Damodaran, 2016). On this basis cash flows

under DCF model are computed. Thereafter, by using discount rate present value of cash

flows is computed. Thereafter, enterprise value is calculated and divided by issues

shares. In this way intrinsic value is computed.

Table 8 Four year cash flows of Easy jet

2012 2013 2014 2015

Seat revenue 3794 4194 4462 4616

Non seat revenue 60 64 65 70

Total revenue 3854 4258 4527 4686

Fuel 1149 1182 1251 1199

Airport and ground handling 955 1078 1107 1122

Crew 432 454 479 505

Navigation 280 294 307 313

Maintenance 203 212 212 229

Selling and marketing 104 101 103 102

Other costs 200 10 245 276

EBITDAR 3323 3331 3704 3746

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

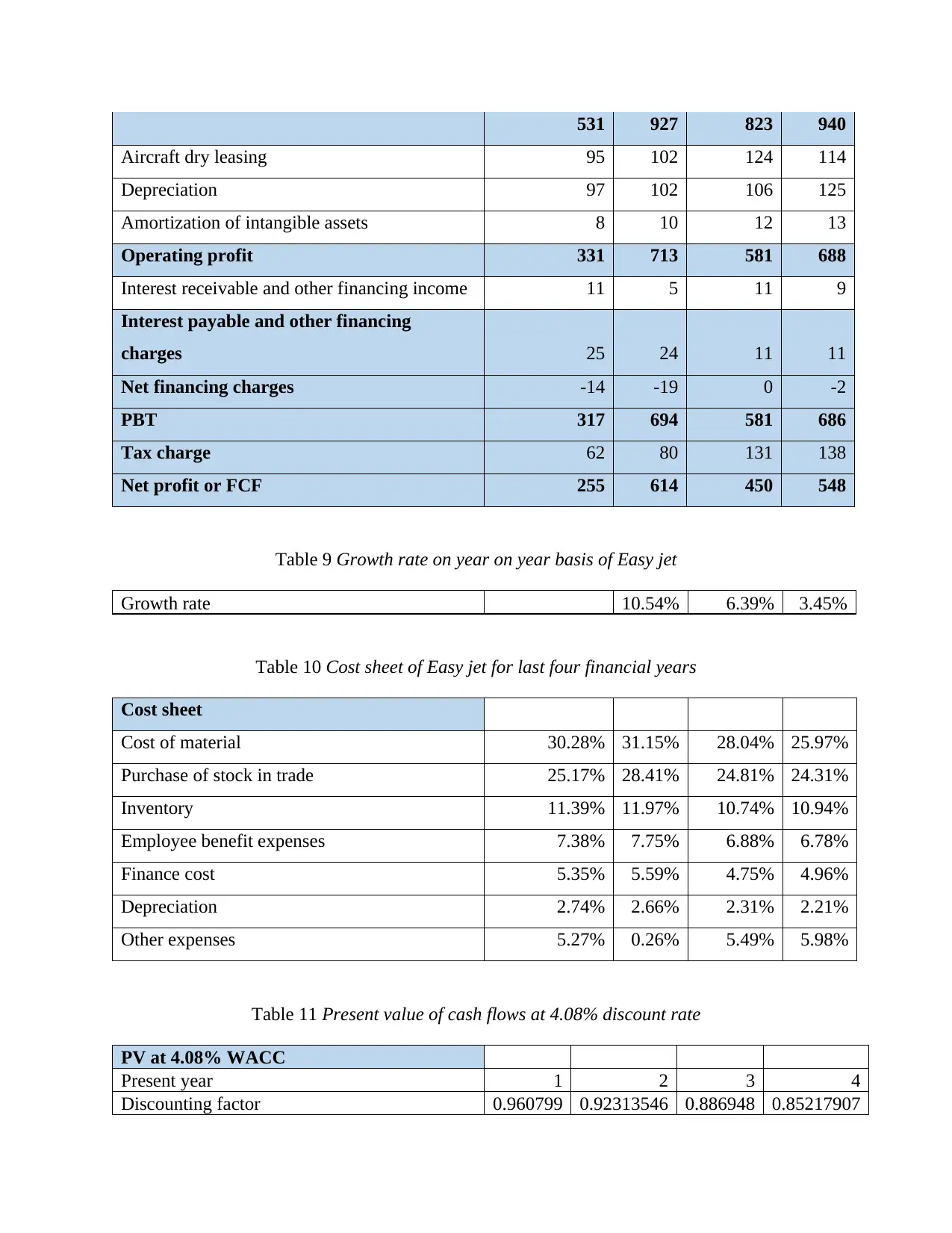

531 927 823 940

Aircraft dry leasing 95 102 124 114

Depreciation 97 102 106 125

Amortization of intangible assets 8 10 12 13

Operating profit 331 713 581 688

Interest receivable and other financing income 11 5 11 9

Interest payable and other financing

charges 25 24 11 11

Net financing charges -14 -19 0 -2

PBT 317 694 581 686

Tax charge 62 80 131 138

Net profit or FCF 255 614 450 548

Table 9 Growth rate on year on year basis of Easy jet

Growth rate 10.54% 6.39% 3.45%

Table 10 Cost sheet of Easy jet for last four financial years

Cost sheet

Cost of material 30.28% 31.15% 28.04% 25.97%

Purchase of stock in trade 25.17% 28.41% 24.81% 24.31%

Inventory 11.39% 11.97% 10.74% 10.94%

Employee benefit expenses 7.38% 7.75% 6.88% 6.78%

Finance cost 5.35% 5.59% 4.75% 4.96%

Depreciation 2.74% 2.66% 2.31% 2.21%

Other expenses 5.27% 0.26% 5.49% 5.98%

Table 11 Present value of cash flows at 4.08% discount rate

PV at 4.08% WACC

Present year 1 2 3 4

Discounting factor 0.960799 0.92313546 0.886948 0.85217907

Aircraft dry leasing 95 102 124 114

Depreciation 97 102 106 125

Amortization of intangible assets 8 10 12 13

Operating profit 331 713 581 688

Interest receivable and other financing income 11 5 11 9

Interest payable and other financing

charges 25 24 11 11

Net financing charges -14 -19 0 -2

PBT 317 694 581 686

Tax charge 62 80 131 138

Net profit or FCF 255 614 450 548

Table 9 Growth rate on year on year basis of Easy jet

Growth rate 10.54% 6.39% 3.45%

Table 10 Cost sheet of Easy jet for last four financial years

Cost sheet

Cost of material 30.28% 31.15% 28.04% 25.97%

Purchase of stock in trade 25.17% 28.41% 24.81% 24.31%

Inventory 11.39% 11.97% 10.74% 10.94%

Employee benefit expenses 7.38% 7.75% 6.88% 6.78%

Finance cost 5.35% 5.59% 4.75% 4.96%

Depreciation 2.74% 2.66% 2.31% 2.21%

Other expenses 5.27% 0.26% 5.49% 5.98%

Table 11 Present value of cash flows at 4.08% discount rate

PV at 4.08% WACC

Present year 1 2 3 4

Discounting factor 0.960799 0.92313546 0.886948 0.85217907

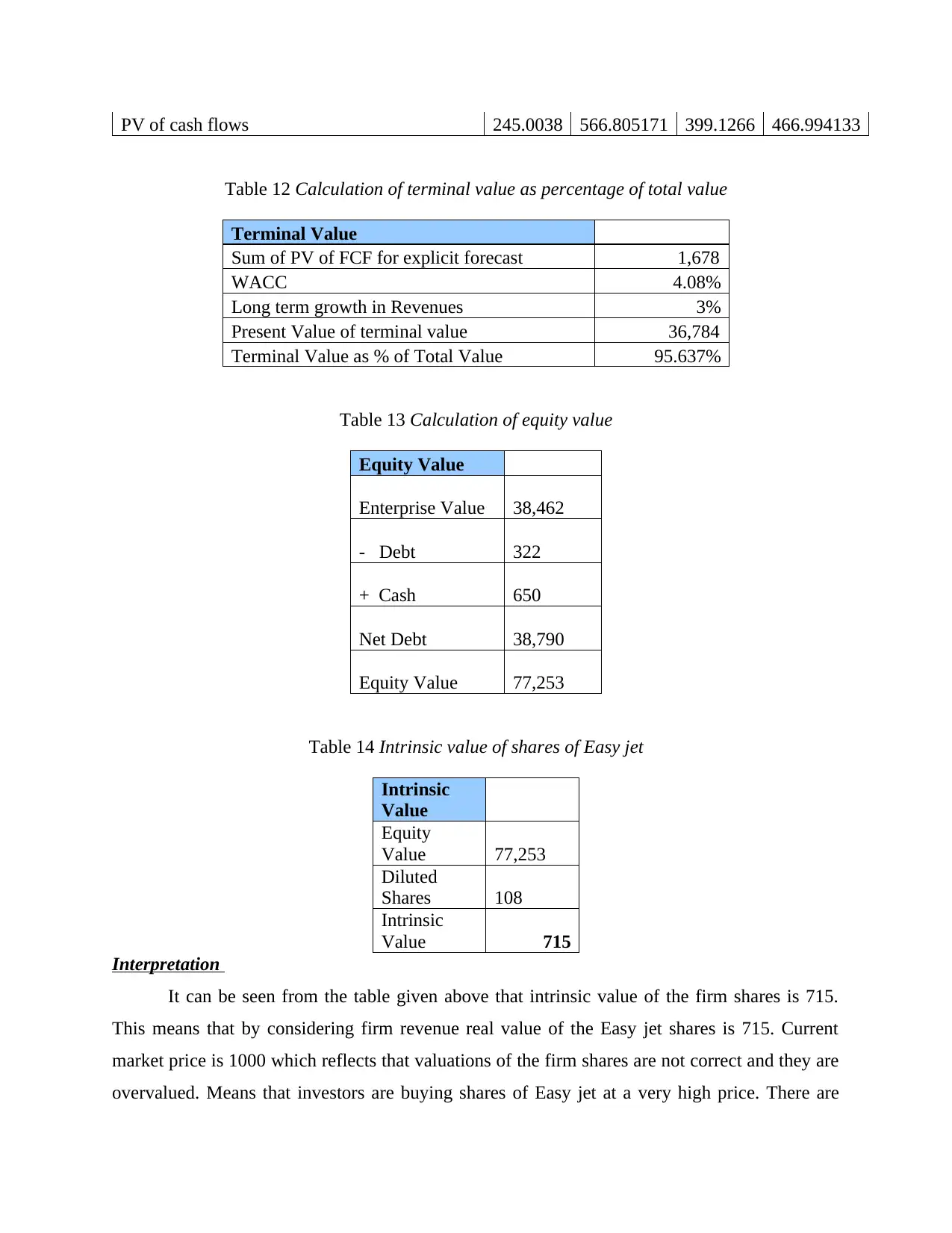

PV of cash flows 245.0038 566.805171 399.1266 466.994133

Table 12 Calculation of terminal value as percentage of total value

Terminal Value

Sum of PV of FCF for explicit forecast 1,678

WACC 4.08%

Long term growth in Revenues 3%

Present Value of terminal value 36,784

Terminal Value as % of Total Value 95.637%

Table 13 Calculation of equity value

Equity Value

Enterprise Value 38,462

- Debt 322

+ Cash 650

Net Debt 38,790

Equity Value 77,253

Table 14 Intrinsic value of shares of Easy jet

Intrinsic

Value

Equity

Value 77,253

Diluted

Shares 108

Intrinsic

Value 715

Interpretation

It can be seen from the table given above that intrinsic value of the firm shares is 715.

This means that by considering firm revenue real value of the Easy jet shares is 715. Current

market price is 1000 which reflects that valuations of the firm shares are not correct and they are

overvalued. Means that investors are buying shares of Easy jet at a very high price. There are

Table 12 Calculation of terminal value as percentage of total value

Terminal Value

Sum of PV of FCF for explicit forecast 1,678

WACC 4.08%

Long term growth in Revenues 3%

Present Value of terminal value 36,784

Terminal Value as % of Total Value 95.637%

Table 13 Calculation of equity value

Equity Value

Enterprise Value 38,462

- Debt 322

+ Cash 650

Net Debt 38,790

Equity Value 77,253

Table 14 Intrinsic value of shares of Easy jet

Intrinsic

Value

Equity

Value 77,253

Diluted

Shares 108

Intrinsic

Value 715

Interpretation

It can be seen from the table given above that intrinsic value of the firm shares is 715.

This means that by considering firm revenue real value of the Easy jet shares is 715. Current

market price is 1000 which reflects that valuations of the firm shares are not correct and they are

overvalued. Means that investors are buying shares of Easy jet at a very high price. There are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

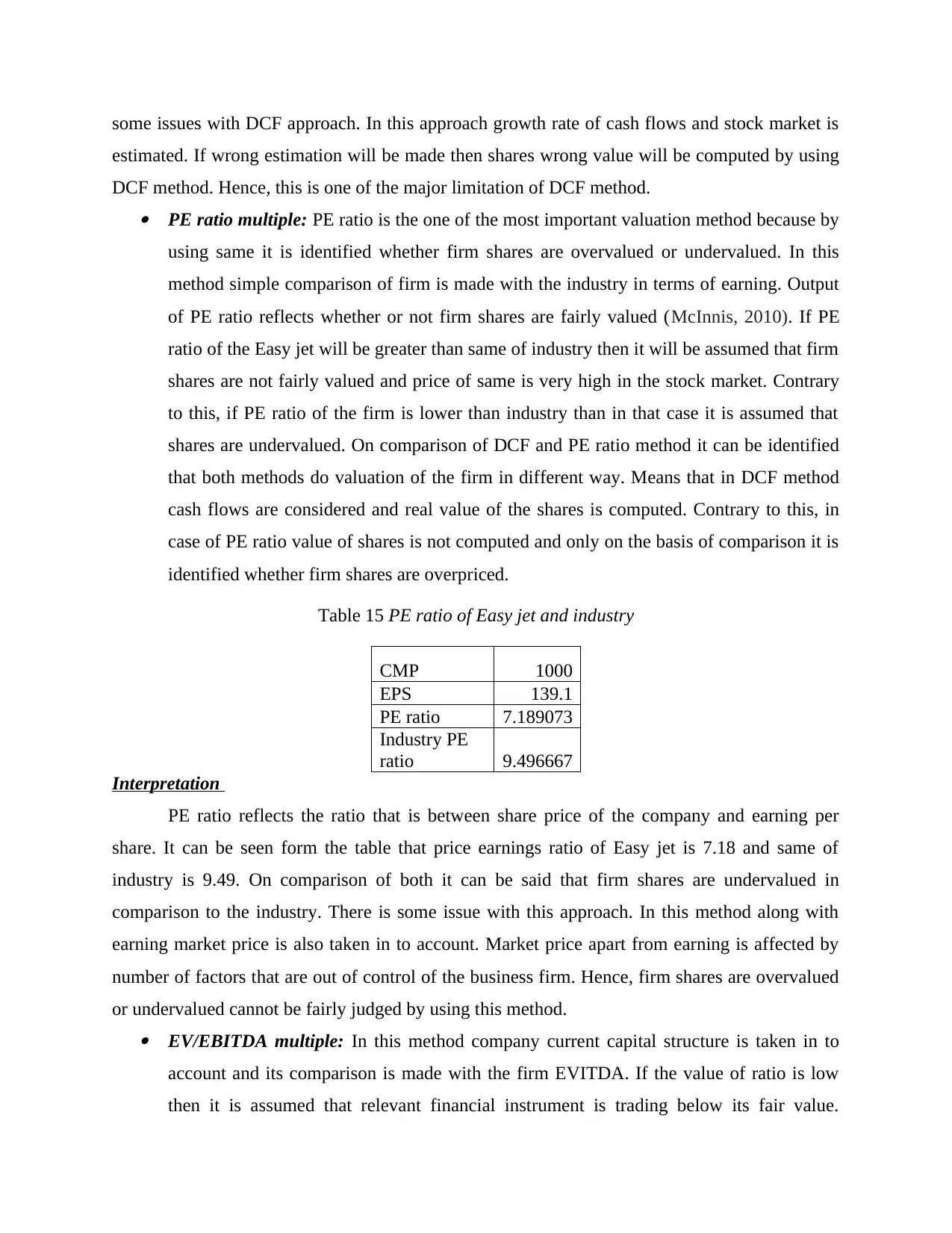

some issues with DCF approach. In this approach growth rate of cash flows and stock market is

estimated. If wrong estimation will be made then shares wrong value will be computed by using

DCF method. Hence, this is one of the major limitation of DCF method. PE ratio multiple: PE ratio is the one of the most important valuation method because by

using same it is identified whether firm shares are overvalued or undervalued. In this

method simple comparison of firm is made with the industry in terms of earning. Output

of PE ratio reflects whether or not firm shares are fairly valued (McInnis, 2010). If PE

ratio of the Easy jet will be greater than same of industry then it will be assumed that firm

shares are not fairly valued and price of same is very high in the stock market. Contrary

to this, if PE ratio of the firm is lower than industry than in that case it is assumed that

shares are undervalued. On comparison of DCF and PE ratio method it can be identified

that both methods do valuation of the firm in different way. Means that in DCF method

cash flows are considered and real value of the shares is computed. Contrary to this, in

case of PE ratio value of shares is not computed and only on the basis of comparison it is

identified whether firm shares are overpriced.

Table 15 PE ratio of Easy jet and industry

CMP 1000

EPS 139.1

PE ratio 7.189073

Industry PE

ratio 9.496667

Interpretation

PE ratio reflects the ratio that is between share price of the company and earning per

share. It can be seen form the table that price earnings ratio of Easy jet is 7.18 and same of

industry is 9.49. On comparison of both it can be said that firm shares are undervalued in

comparison to the industry. There is some issue with this approach. In this method along with

earning market price is also taken in to account. Market price apart from earning is affected by

number of factors that are out of control of the business firm. Hence, firm shares are overvalued

or undervalued cannot be fairly judged by using this method. EV/EBITDA multiple: In this method company current capital structure is taken in to

account and its comparison is made with the firm EVITDA. If the value of ratio is low

then it is assumed that relevant financial instrument is trading below its fair value.

estimated. If wrong estimation will be made then shares wrong value will be computed by using

DCF method. Hence, this is one of the major limitation of DCF method. PE ratio multiple: PE ratio is the one of the most important valuation method because by

using same it is identified whether firm shares are overvalued or undervalued. In this

method simple comparison of firm is made with the industry in terms of earning. Output

of PE ratio reflects whether or not firm shares are fairly valued (McInnis, 2010). If PE

ratio of the Easy jet will be greater than same of industry then it will be assumed that firm

shares are not fairly valued and price of same is very high in the stock market. Contrary

to this, if PE ratio of the firm is lower than industry than in that case it is assumed that

shares are undervalued. On comparison of DCF and PE ratio method it can be identified

that both methods do valuation of the firm in different way. Means that in DCF method

cash flows are considered and real value of the shares is computed. Contrary to this, in

case of PE ratio value of shares is not computed and only on the basis of comparison it is

identified whether firm shares are overpriced.

Table 15 PE ratio of Easy jet and industry

CMP 1000

EPS 139.1

PE ratio 7.189073

Industry PE

ratio 9.496667

Interpretation

PE ratio reflects the ratio that is between share price of the company and earning per

share. It can be seen form the table that price earnings ratio of Easy jet is 7.18 and same of

industry is 9.49. On comparison of both it can be said that firm shares are undervalued in

comparison to the industry. There is some issue with this approach. In this method along with

earning market price is also taken in to account. Market price apart from earning is affected by

number of factors that are out of control of the business firm. Hence, firm shares are overvalued

or undervalued cannot be fairly judged by using this method. EV/EBITDA multiple: In this method company current capital structure is taken in to

account and its comparison is made with the firm EVITDA. If the value of ratio is low

then it is assumed that relevant financial instrument is trading below its fair value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

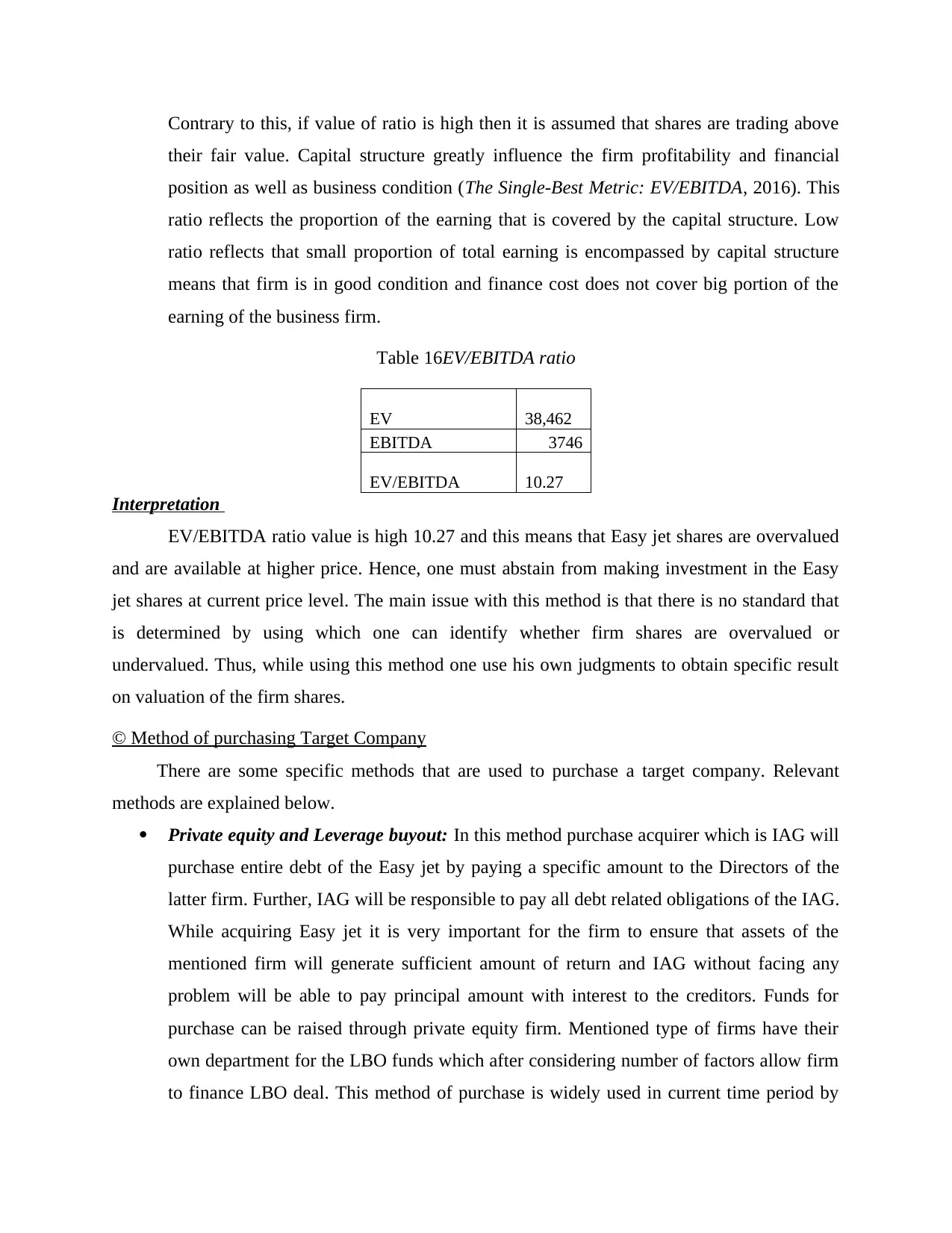

Contrary to this, if value of ratio is high then it is assumed that shares are trading above

their fair value. Capital structure greatly influence the firm profitability and financial

position as well as business condition (The Single-Best Metric: EV/EBITDA, 2016). This

ratio reflects the proportion of the earning that is covered by the capital structure. Low

ratio reflects that small proportion of total earning is encompassed by capital structure

means that firm is in good condition and finance cost does not cover big portion of the

earning of the business firm.

Table 16EV/EBITDA ratio

EV 38,462

EBITDA 3746

EV/EBITDA 10.27

Interpretation

EV/EBITDA ratio value is high 10.27 and this means that Easy jet shares are overvalued

and are available at higher price. Hence, one must abstain from making investment in the Easy

jet shares at current price level. The main issue with this method is that there is no standard that

is determined by using which one can identify whether firm shares are overvalued or

undervalued. Thus, while using this method one use his own judgments to obtain specific result

on valuation of the firm shares.

© Method of purchasing Target Company

There are some specific methods that are used to purchase a target company. Relevant

methods are explained below.

Private equity and Leverage buyout: In this method purchase acquirer which is IAG will

purchase entire debt of the Easy jet by paying a specific amount to the Directors of the

latter firm. Further, IAG will be responsible to pay all debt related obligations of the IAG.

While acquiring Easy jet it is very important for the firm to ensure that assets of the

mentioned firm will generate sufficient amount of return and IAG without facing any

problem will be able to pay principal amount with interest to the creditors. Funds for

purchase can be raised through private equity firm. Mentioned type of firms have their

own department for the LBO funds which after considering number of factors allow firm

to finance LBO deal. This method of purchase is widely used in current time period by

their fair value. Capital structure greatly influence the firm profitability and financial

position as well as business condition (The Single-Best Metric: EV/EBITDA, 2016). This

ratio reflects the proportion of the earning that is covered by the capital structure. Low

ratio reflects that small proportion of total earning is encompassed by capital structure

means that firm is in good condition and finance cost does not cover big portion of the

earning of the business firm.

Table 16EV/EBITDA ratio

EV 38,462

EBITDA 3746

EV/EBITDA 10.27

Interpretation

EV/EBITDA ratio value is high 10.27 and this means that Easy jet shares are overvalued

and are available at higher price. Hence, one must abstain from making investment in the Easy

jet shares at current price level. The main issue with this method is that there is no standard that

is determined by using which one can identify whether firm shares are overvalued or

undervalued. Thus, while using this method one use his own judgments to obtain specific result

on valuation of the firm shares.

© Method of purchasing Target Company

There are some specific methods that are used to purchase a target company. Relevant

methods are explained below.

Private equity and Leverage buyout: In this method purchase acquirer which is IAG will

purchase entire debt of the Easy jet by paying a specific amount to the Directors of the

latter firm. Further, IAG will be responsible to pay all debt related obligations of the IAG.

While acquiring Easy jet it is very important for the firm to ensure that assets of the

mentioned firm will generate sufficient amount of return and IAG without facing any

problem will be able to pay principal amount with interest to the creditors. Funds for

purchase can be raised through private equity firm. Mentioned type of firms have their

own department for the LBO funds which after considering number of factors allow firm

to finance LBO deal. This method of purchase is widely used in current time period by

the business firms. It can be said that this method of firm purchase is appropriate for the

IAG.

Retained earnings and debt (Equity purchase): This is another method of firm purchase

and under this IAG needs to purchase equity stock in the Easy jet. It will need to purchase

60% shares of the Easy jet in order to obtain to substantial control on same. Like leverage

buyout this method of purchase is quite popular among the business firms (Dhaliwal and

et.al., 2011). It can be said that equity purchase is the traditional method that is followed

by one firm to acquire other one. In order to finance equity purchase firm can take loan

from the banks. If one bank is not ready to finance entire deal than consortium finance

can be used to arrange entire amount of finance. Retained earnings can also be used by

the firm to purchase Easy jet. There is no cost of the mentioned source of finance and due

to this reason it is commonly used by the business firms for acquiring other firm.

On comparison of both source of finance it can be said it will be better to purchase Easy

jet by using retained earnings and debt. This is because in case of private equity PE firm will

obtain stake in IAG and will affects its decision making process. Moreover, cost of finance

through PE is also high in comparison to debt. Hence, it can be said that it will be better to

acquire Easy jet by raising fund from debt than private equity.

CONCLUSION

On the basis of above discussion it is concluded that there are varied techniques of valuation

and all of them have some positive and negative points. Hence, with due care specific valuation

method must be used by the managers to make decisions. Debt must be used to finance purchase

of firm relative to equity because cost of finance is low in case of former one.

IAG.

Retained earnings and debt (Equity purchase): This is another method of firm purchase

and under this IAG needs to purchase equity stock in the Easy jet. It will need to purchase

60% shares of the Easy jet in order to obtain to substantial control on same. Like leverage

buyout this method of purchase is quite popular among the business firms (Dhaliwal and

et.al., 2011). It can be said that equity purchase is the traditional method that is followed

by one firm to acquire other one. In order to finance equity purchase firm can take loan

from the banks. If one bank is not ready to finance entire deal than consortium finance

can be used to arrange entire amount of finance. Retained earnings can also be used by

the firm to purchase Easy jet. There is no cost of the mentioned source of finance and due

to this reason it is commonly used by the business firms for acquiring other firm.

On comparison of both source of finance it can be said it will be better to purchase Easy

jet by using retained earnings and debt. This is because in case of private equity PE firm will

obtain stake in IAG and will affects its decision making process. Moreover, cost of finance

through PE is also high in comparison to debt. Hence, it can be said that it will be better to

acquire Easy jet by raising fund from debt than private equity.

CONCLUSION

On the basis of above discussion it is concluded that there are varied techniques of valuation

and all of them have some positive and negative points. Hence, with due care specific valuation

method must be used by the managers to make decisions. Debt must be used to finance purchase

of firm relative to equity because cost of finance is low in case of former one.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.