Sweet Menu Restaurant Finance Report: Sources, Costs and Analysis

VerifiedAdded on 2019/12/04

|20

|6271

|378

Report

AI Summary

This report provides a comprehensive financial analysis of the Sweet Menu Restaurant. It begins by identifying various internal and external sources of finance available to a business, discussing their implications, and determining the most appropriate sources for the restaurant's expansion plans. The report then delves into the costs associated with different financing options and emphasizes the importance of financial planning. It outlines the information needed by decision-makers, analyzes the impact of financing choices on financial statements, and assesses a four-month cash budget to guide financial decisions. Furthermore, the report explores unit cost calculations, pricing strategies, and evaluates the viability of two potential projects using diverse investment methods. The final sections cover the main elements of financial statements, different statements used by organizations, and the calculation and comparison of various financial ratios to assess the restaurant's financial position. The report culminates with a discussion on the most suitable financing methods for the restaurant's expansion, considering the advantages, disadvantages, and suitability of each option.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance available to a business.......................................................................1

1.2 Implication of sources of finance.....................................................................................2

1.3 Appropriate sources of finance for Sweet Menu Restaurant............................................3

TASK 2............................................................................................................................................4

2.1 Cost of different sources of finance..................................................................................4

2.2 Importance of financial planning for Sweet Menu restaurant..........................................4

2.3 Information needed by decision maker of Sweet Menu Restaurant.................................5

2.4 Impact of sources of finance identified on financial statements......................................5

TASK 3............................................................................................................................................6

3.1 Analyze of the cash budget in order to take appropriate decisions..................................6

3.2 Calculation of unit cost and relevant pricing decisions....................................................6

3.3 Viability of two projects using various investment methods...........................................6

TASK 4............................................................................................................................................7

4.1 Main elements of financial statements.............................................................................7

4.2 Different statements used by different organization........................................................7

4.3 Calculation of various ratios.............................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance available to a business.......................................................................1

1.2 Implication of sources of finance.....................................................................................2

1.3 Appropriate sources of finance for Sweet Menu Restaurant............................................3

TASK 2............................................................................................................................................4

2.1 Cost of different sources of finance..................................................................................4

2.2 Importance of financial planning for Sweet Menu restaurant..........................................4

2.3 Information needed by decision maker of Sweet Menu Restaurant.................................5

2.4 Impact of sources of finance identified on financial statements......................................5

TASK 3............................................................................................................................................6

3.1 Analyze of the cash budget in order to take appropriate decisions..................................6

3.2 Calculation of unit cost and relevant pricing decisions....................................................6

3.3 Viability of two projects using various investment methods...........................................6

TASK 4............................................................................................................................................7

4.1 Main elements of financial statements.............................................................................7

4.2 Different statements used by different organization........................................................7

4.3 Calculation of various ratios.............................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................12

INTRODUCTION

Financial management refers to the management of funds in an effective and efficient

manner in order to accomplish the objectives of the organizations. It is a function that is directly

associated with the top management. In other words it could be said that finance is the science

that manage all the activities related to banking, investment made by the company in order to

achieve the desired objective. Therefore, the following report depict about the various sources of

finance available with the company to raise its capital. In this cost of various sources of finance

available with the company is also gadfly. In this report impact of various sources of finance on

financial statements are discussed. In this report four month budget of the company is going to

be analyzed to find out the actual position of the company. At last, various ratios are calculated

and compared in order to find out the position of the both the companies.

TASK 1

1.1 Sources of finance available to a business.

There are various types of internal and external sources of finance of available with the

company which in turn will aid the company to meet its various requirement of finance.

Internal sources of finance

Friends and family: - It is one of the internal sources of finance of available with the

company in order to raise its finance. Company can borrow money from its friends or any

family members. It is one of the easiest methods to raise finance. Sale of fixed assets: - Company can also raise its finance by selling out the obsolescent

assets. By selling unwanted assets company will be able to meet its both short term and

long term requirement of funds depending upon the size of the assets (Beaver, McNichols

and Rhie, 2005.

External sources of finance

Issue of shares and debenture: - In order to meet the long term requirement of finance

company can issue shares and debentures to the general public. By issuing shares and

debenture company can raise large amount of capital within a short period of time.

Hire purchase: - in this method company can raise its finance by hiring the assets or

property. In this method company can use the use the asset without purchasing it. This

method can be used by the company in order to meet its long term requirement of

1

Financial management refers to the management of funds in an effective and efficient

manner in order to accomplish the objectives of the organizations. It is a function that is directly

associated with the top management. In other words it could be said that finance is the science

that manage all the activities related to banking, investment made by the company in order to

achieve the desired objective. Therefore, the following report depict about the various sources of

finance available with the company to raise its capital. In this cost of various sources of finance

available with the company is also gadfly. In this report impact of various sources of finance on

financial statements are discussed. In this report four month budget of the company is going to

be analyzed to find out the actual position of the company. At last, various ratios are calculated

and compared in order to find out the position of the both the companies.

TASK 1

1.1 Sources of finance available to a business.

There are various types of internal and external sources of finance of available with the

company which in turn will aid the company to meet its various requirement of finance.

Internal sources of finance

Friends and family: - It is one of the internal sources of finance of available with the

company in order to raise its finance. Company can borrow money from its friends or any

family members. It is one of the easiest methods to raise finance. Sale of fixed assets: - Company can also raise its finance by selling out the obsolescent

assets. By selling unwanted assets company will be able to meet its both short term and

long term requirement of funds depending upon the size of the assets (Beaver, McNichols

and Rhie, 2005.

External sources of finance

Issue of shares and debenture: - In order to meet the long term requirement of finance

company can issue shares and debentures to the general public. By issuing shares and

debenture company can raise large amount of capital within a short period of time.

Hire purchase: - in this method company can raise its finance by hiring the assets or

property. In this method company can use the use the asset without purchasing it. This

method can be used by the company in order to meet its long term requirement of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

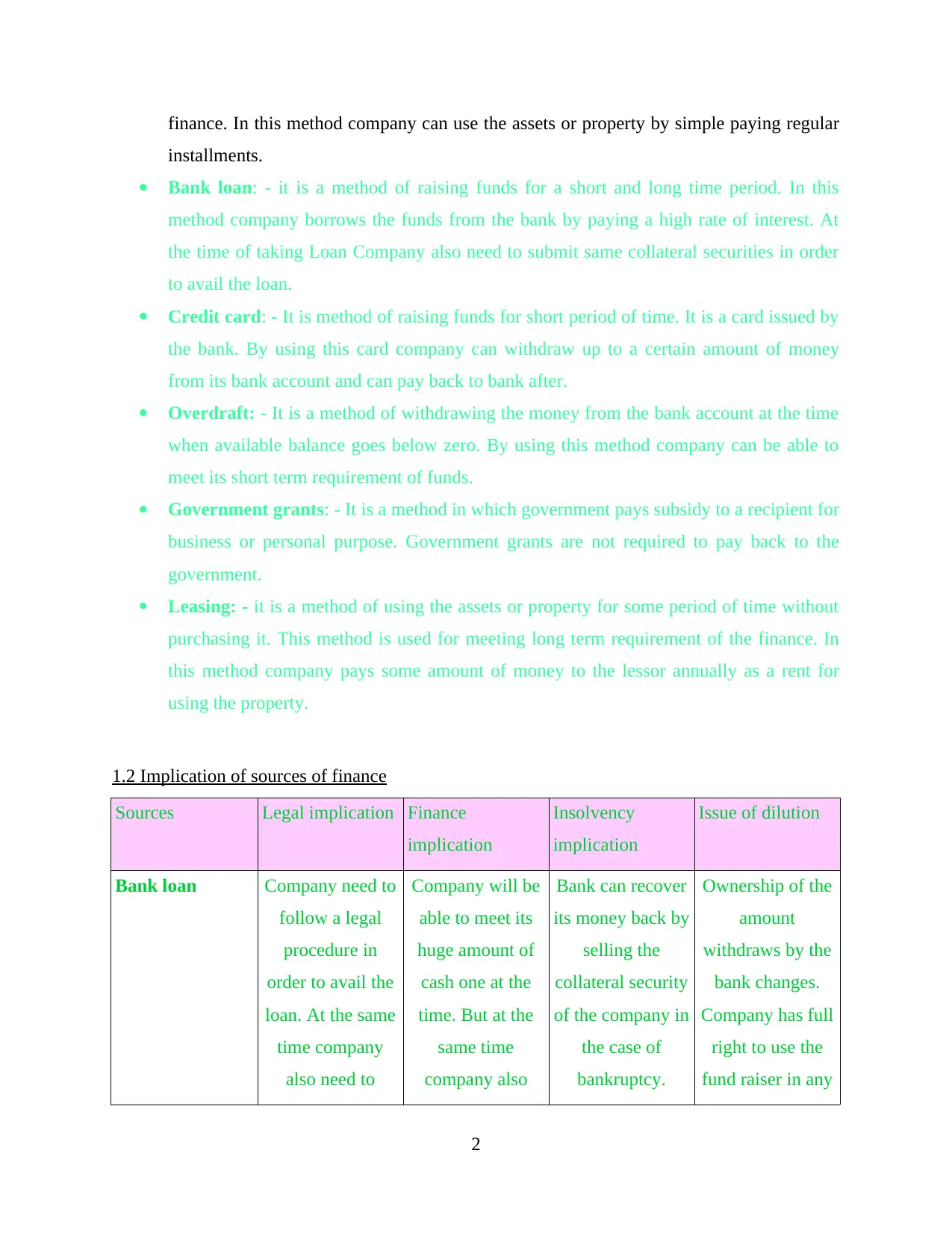

finance. In this method company can use the assets or property by simple paying regular

installments.

Bank loan: - it is a method of raising funds for a short and long time period. In this

method company borrows the funds from the bank by paying a high rate of interest. At

the time of taking Loan Company also need to submit same collateral securities in order

to avail the loan.

Credit card: - It is method of raising funds for short period of time. It is a card issued by

the bank. By using this card company can withdraw up to a certain amount of money

from its bank account and can pay back to bank after.

Overdraft: - It is a method of withdrawing the money from the bank account at the time

when available balance goes below zero. By using this method company can be able to

meet its short term requirement of funds.

Government grants: - It is a method in which government pays subsidy to a recipient for

business or personal purpose. Government grants are not required to pay back to the

government.

Leasing: - it is a method of using the assets or property for some period of time without

purchasing it. This method is used for meeting long term requirement of the finance. In

this method company pays some amount of money to the lessor annually as a rent for

using the property.

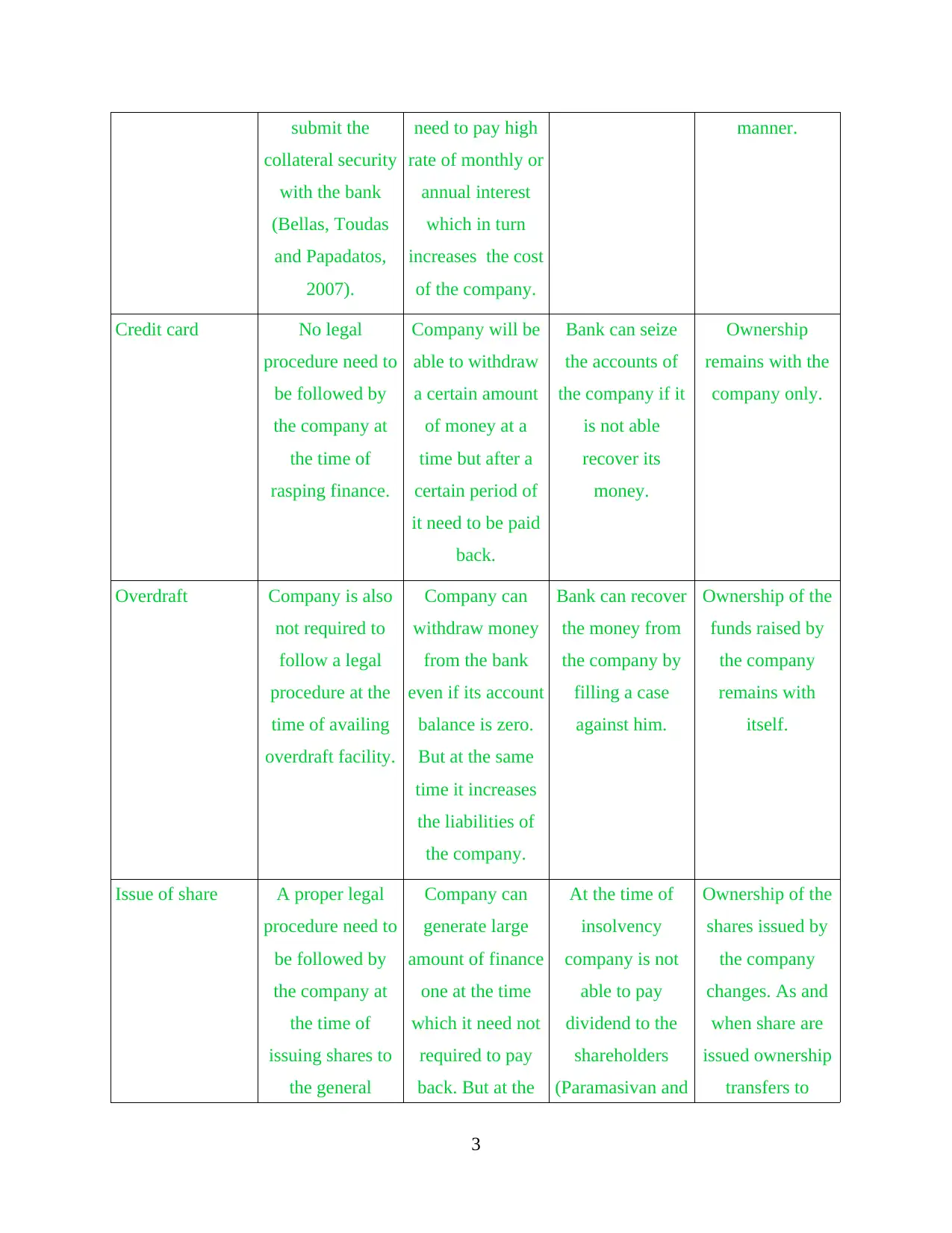

1.2 Implication of sources of finance

Sources Legal implication Finance

implication

Insolvency

implication

Issue of dilution

Bank loan Company need to

follow a legal

procedure in

order to avail the

loan. At the same

time company

also need to

Company will be

able to meet its

huge amount of

cash one at the

time. But at the

same time

company also

Bank can recover

its money back by

selling the

collateral security

of the company in

the case of

bankruptcy.

Ownership of the

amount

withdraws by the

bank changes.

Company has full

right to use the

fund raiser in any

2

installments.

Bank loan: - it is a method of raising funds for a short and long time period. In this

method company borrows the funds from the bank by paying a high rate of interest. At

the time of taking Loan Company also need to submit same collateral securities in order

to avail the loan.

Credit card: - It is method of raising funds for short period of time. It is a card issued by

the bank. By using this card company can withdraw up to a certain amount of money

from its bank account and can pay back to bank after.

Overdraft: - It is a method of withdrawing the money from the bank account at the time

when available balance goes below zero. By using this method company can be able to

meet its short term requirement of funds.

Government grants: - It is a method in which government pays subsidy to a recipient for

business or personal purpose. Government grants are not required to pay back to the

government.

Leasing: - it is a method of using the assets or property for some period of time without

purchasing it. This method is used for meeting long term requirement of the finance. In

this method company pays some amount of money to the lessor annually as a rent for

using the property.

1.2 Implication of sources of finance

Sources Legal implication Finance

implication

Insolvency

implication

Issue of dilution

Bank loan Company need to

follow a legal

procedure in

order to avail the

loan. At the same

time company

also need to

Company will be

able to meet its

huge amount of

cash one at the

time. But at the

same time

company also

Bank can recover

its money back by

selling the

collateral security

of the company in

the case of

bankruptcy.

Ownership of the

amount

withdraws by the

bank changes.

Company has full

right to use the

fund raiser in any

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

submit the

collateral security

with the bank

(Bellas, Toudas

and Papadatos,

2007).

need to pay high

rate of monthly or

annual interest

which in turn

increases the cost

of the company.

manner.

Credit card No legal

procedure need to

be followed by

the company at

the time of

rasping finance.

Company will be

able to withdraw

a certain amount

of money at a

time but after a

certain period of

it need to be paid

back.

Bank can seize

the accounts of

the company if it

is not able

recover its

money.

Ownership

remains with the

company only.

Overdraft Company is also

not required to

follow a legal

procedure at the

time of availing

overdraft facility.

Company can

withdraw money

from the bank

even if its account

balance is zero.

But at the same

time it increases

the liabilities of

the company.

Bank can recover

the money from

the company by

filling a case

against him.

Ownership of the

funds raised by

the company

remains with

itself.

Issue of share A proper legal

procedure need to

be followed by

the company at

the time of

issuing shares to

the general

Company can

generate large

amount of finance

one at the time

which it need not

required to pay

back. But at the

At the time of

insolvency

company is not

able to pay

dividend to the

shareholders

(Paramasivan and

Ownership of the

shares issued by

the company

changes. As and

when share are

issued ownership

transfers to

3

collateral security

with the bank

(Bellas, Toudas

and Papadatos,

2007).

need to pay high

rate of monthly or

annual interest

which in turn

increases the cost

of the company.

manner.

Credit card No legal

procedure need to

be followed by

the company at

the time of

rasping finance.

Company will be

able to withdraw

a certain amount

of money at a

time but after a

certain period of

it need to be paid

back.

Bank can seize

the accounts of

the company if it

is not able

recover its

money.

Ownership

remains with the

company only.

Overdraft Company is also

not required to

follow a legal

procedure at the

time of availing

overdraft facility.

Company can

withdraw money

from the bank

even if its account

balance is zero.

But at the same

time it increases

the liabilities of

the company.

Bank can recover

the money from

the company by

filling a case

against him.

Ownership of the

funds raised by

the company

remains with

itself.

Issue of share A proper legal

procedure need to

be followed by

the company at

the time of

issuing shares to

the general

Company can

generate large

amount of finance

one at the time

which it need not

required to pay

back. But at the

At the time of

insolvency

company is not

able to pay

dividend to the

shareholders

(Paramasivan and

Ownership of the

shares issued by

the company

changes. As and

when share are

issued ownership

transfers to

3

public. same time

company need to

pay interest and

dividend to the

shareholder

which in turn

reduces the profit

margin of the

company.

Subramanian,

n.d.).

shareholder.

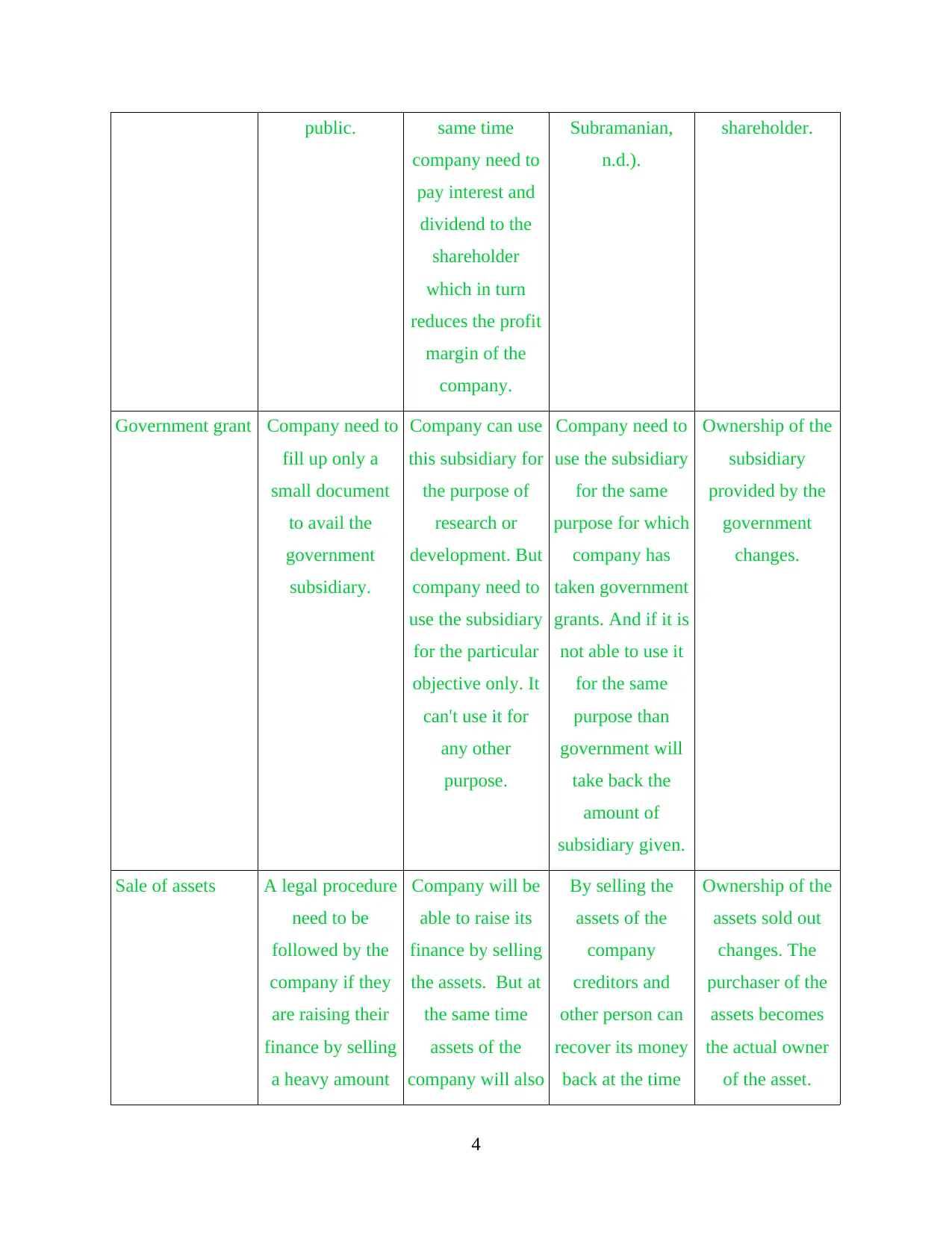

Government grant Company need to

fill up only a

small document

to avail the

government

subsidiary.

Company can use

this subsidiary for

the purpose of

research or

development. But

company need to

use the subsidiary

for the particular

objective only. It

can't use it for

any other

purpose.

Company need to

use the subsidiary

for the same

purpose for which

company has

taken government

grants. And if it is

not able to use it

for the same

purpose than

government will

take back the

amount of

subsidiary given.

Ownership of the

subsidiary

provided by the

government

changes.

Sale of assets A legal procedure

need to be

followed by the

company if they

are raising their

finance by selling

a heavy amount

Company will be

able to raise its

finance by selling

the assets. But at

the same time

assets of the

company will also

By selling the

assets of the

company

creditors and

other person can

recover its money

back at the time

Ownership of the

assets sold out

changes. The

purchaser of the

assets becomes

the actual owner

of the asset.

4

company need to

pay interest and

dividend to the

shareholder

which in turn

reduces the profit

margin of the

company.

Subramanian,

n.d.).

shareholder.

Government grant Company need to

fill up only a

small document

to avail the

government

subsidiary.

Company can use

this subsidiary for

the purpose of

research or

development. But

company need to

use the subsidiary

for the particular

objective only. It

can't use it for

any other

purpose.

Company need to

use the subsidiary

for the same

purpose for which

company has

taken government

grants. And if it is

not able to use it

for the same

purpose than

government will

take back the

amount of

subsidiary given.

Ownership of the

subsidiary

provided by the

government

changes.

Sale of assets A legal procedure

need to be

followed by the

company if they

are raising their

finance by selling

a heavy amount

Company will be

able to raise its

finance by selling

the assets. But at

the same time

assets of the

company will also

By selling the

assets of the

company

creditors and

other person can

recover its money

back at the time

Ownership of the

assets sold out

changes. The

purchaser of the

assets becomes

the actual owner

of the asset.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of asset. reduces (Bentz,

2007).

of insolvency.

Higher purchase

and leasing

A complete legal

procedure need to

be followed by

the company. A

legal contract has

been made

between lessor

and the lessee in

order to use the

assets.

Company can use

the assets without

purchasing it. But

at the same time

rent in form of

installments need

to pay whose total

cost increases the

actual cost of the

asset.

At the time of

insolvency actual

owner of the

property can take

back its property.

Ownership of the

asset leased

remains with the

actual owner of

the assets only.

1.3 Appropriate sources of finance for Sweet Menu Restaurant

There are various sources of finance which Sweet Menu Restaurant can considered in

order to raise its funds for expanding its business. But the most appropriate sources of finance

which Restaurant can use in order to fulfill their requirement of £3, 00,000 to £5, 00,000 are

Sources Advantages Disadvantages Suitability

Issue of shares and

debentures

Sweet Menu

Restaurant can issue

shares and debentures

in order to raise its

finance. In this method

company is not

required to pay back

the amount borrowed

after sometime. It

always remains with

the company.

Company need to pay

high interest and

dividend to the

shareholders in lieu of

the share issued out of

the profit earned by

the company. If

company faces the

condition of losses

than also it need to pay

interest to the share

and debentures holders

This is one of the

safest methods of

raising the funds. This

method can be used by

the Sweet Menu

Restaurant to raise its

capital by £5, 00,000

in order to expand its

business by opening

new branches.

5

2007).

of insolvency.

Higher purchase

and leasing

A complete legal

procedure need to

be followed by

the company. A

legal contract has

been made

between lessor

and the lessee in

order to use the

assets.

Company can use

the assets without

purchasing it. But

at the same time

rent in form of

installments need

to pay whose total

cost increases the

actual cost of the

asset.

At the time of

insolvency actual

owner of the

property can take

back its property.

Ownership of the

asset leased

remains with the

actual owner of

the assets only.

1.3 Appropriate sources of finance for Sweet Menu Restaurant

There are various sources of finance which Sweet Menu Restaurant can considered in

order to raise its funds for expanding its business. But the most appropriate sources of finance

which Restaurant can use in order to fulfill their requirement of £3, 00,000 to £5, 00,000 are

Sources Advantages Disadvantages Suitability

Issue of shares and

debentures

Sweet Menu

Restaurant can issue

shares and debentures

in order to raise its

finance. In this method

company is not

required to pay back

the amount borrowed

after sometime. It

always remains with

the company.

Company need to pay

high interest and

dividend to the

shareholders in lieu of

the share issued out of

the profit earned by

the company. If

company faces the

condition of losses

than also it need to pay

interest to the share

and debentures holders

This is one of the

safest methods of

raising the funds. This

method can be used by

the Sweet Menu

Restaurant to raise its

capital by £5, 00,000

in order to expand its

business by opening

new branches.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Brigham, 2013).

Sale of assets By using this method

Sweet Menu restaurant

can raise its capital by

disposing out the

unwanted/ obsolescent

assets. In this method

company can raise its

finance without

borrowing from

anyone.

Loss can be faced by

the company if

company is not able to

sell the asset at its

depreciated value.

This method is also

useful for the Sweet

Menu Restaurant in

order to expand its

business. They can

also use this method

for purchasing the new

assets.

Bank loan By using this method

Sweet Menu

Restaurant can be able

to raise finance for

both short and long

period of time by

simply paying the

collateral security. It is

one of the safe

methods of raising

funds.

Company need to pay

high rate of interest to

the bank which

reduces the profit

margin of the

company. At the same

time company also

need to submit the

collateral security.

This is a method

suitable for expanding

the business, purchase

of assets, paying

dividend to the

shareholder or for

conducting the

research.

TASK 2

2.1 Cost of different sources of finance

To open the proposed new branches, Sweet Menu Restaurant can raise its finance by issuing

the shares and debentures or by selling the fixed asset. But at the same time, use of this method

will enhance the cost of the company.

Issue of shares and debentures: - Sweet Menu restaurant can raise their finance by

issuing shares and debentures to the general public. But at the same time it increases the

cost of the company. Company need pay high rate of dividend and interest to the equity

6

Sale of assets By using this method

Sweet Menu restaurant

can raise its capital by

disposing out the

unwanted/ obsolescent

assets. In this method

company can raise its

finance without

borrowing from

anyone.

Loss can be faced by

the company if

company is not able to

sell the asset at its

depreciated value.

This method is also

useful for the Sweet

Menu Restaurant in

order to expand its

business. They can

also use this method

for purchasing the new

assets.

Bank loan By using this method

Sweet Menu

Restaurant can be able

to raise finance for

both short and long

period of time by

simply paying the

collateral security. It is

one of the safe

methods of raising

funds.

Company need to pay

high rate of interest to

the bank which

reduces the profit

margin of the

company. At the same

time company also

need to submit the

collateral security.

This is a method

suitable for expanding

the business, purchase

of assets, paying

dividend to the

shareholder or for

conducting the

research.

TASK 2

2.1 Cost of different sources of finance

To open the proposed new branches, Sweet Menu Restaurant can raise its finance by issuing

the shares and debentures or by selling the fixed asset. But at the same time, use of this method

will enhance the cost of the company.

Issue of shares and debentures: - Sweet Menu restaurant can raise their finance by

issuing shares and debentures to the general public. But at the same time it increases the

cost of the company. Company need pay high rate of dividend and interest to the equity

6

and debentures holders even if the company is facing loss condition (Dontoh, Ronen and

Sarath, 2008). This in turn reduces the profit margin of the company.

Sale of fixed assets: - By selling the fixed assets company can raise its finance to expand

its business and at the same time is able to meet its short term and middle term

requirement of finance. But at the same time it can impact the cost of the company.

Assets of the company will be reduced. If company is not able to sell its assets at the

deprecated value than in that case company can face loss condition.

Bank loan: - By taking bank Loan Company will be able to meet requirement of finance.

But at the same time it increases the various types of fixed and variable cost of the

company like arrangement fee, late payment charges, and admin charges. At the same

time company also need to be paid high rate of interest to the bank.

Overdraft: - By using this method company can withdraw money from the bank even if

its account balance is zero. But at the same time it increases the cost of the company.

Company need to pay higher rate of interest on the amount withdrawn if it exceeds the

certain limit. Normally cost of interest and other fee paid increases the actual cost of

amount withdrawn. Thus, at the same time company need to have good credit score than

only it can avail the overdraft facility.

Issue of share: - By issuing the shares company can meet long term requirement of

finance. But at the same it increases its cost. Company need to invest on the

advertisement, printing and posting share certificates, hosting annual meeting, providing

financial statements and many more cost. At the same time company also need to pay

dividend to the shareholder which reduces the profit margin of the company.

2.2 Importance of financial planning for Sweet Menu restaurant

Financial planning of all the activities in advance will aid the Sweet Menu restaurant to

achieve various desired goals and objectives easily.

Able to distribute finance properly to each and every department: - Financial

planning of all the activities in advance aids the company to distribute the finance

available with the company properly in each and every department. This in turn will aid

the Sweet Menu restaurant to avoid the condition of excessive and shortage of finance

(Eccles and Holt, 2005).

7

Sarath, 2008). This in turn reduces the profit margin of the company.

Sale of fixed assets: - By selling the fixed assets company can raise its finance to expand

its business and at the same time is able to meet its short term and middle term

requirement of finance. But at the same time it can impact the cost of the company.

Assets of the company will be reduced. If company is not able to sell its assets at the

deprecated value than in that case company can face loss condition.

Bank loan: - By taking bank Loan Company will be able to meet requirement of finance.

But at the same time it increases the various types of fixed and variable cost of the

company like arrangement fee, late payment charges, and admin charges. At the same

time company also need to be paid high rate of interest to the bank.

Overdraft: - By using this method company can withdraw money from the bank even if

its account balance is zero. But at the same time it increases the cost of the company.

Company need to pay higher rate of interest on the amount withdrawn if it exceeds the

certain limit. Normally cost of interest and other fee paid increases the actual cost of

amount withdrawn. Thus, at the same time company need to have good credit score than

only it can avail the overdraft facility.

Issue of share: - By issuing the shares company can meet long term requirement of

finance. But at the same it increases its cost. Company need to invest on the

advertisement, printing and posting share certificates, hosting annual meeting, providing

financial statements and many more cost. At the same time company also need to pay

dividend to the shareholder which reduces the profit margin of the company.

2.2 Importance of financial planning for Sweet Menu restaurant

Financial planning of all the activities in advance will aid the Sweet Menu restaurant to

achieve various desired goals and objectives easily.

Able to distribute finance properly to each and every department: - Financial

planning of all the activities in advance aids the company to distribute the finance

available with the company properly in each and every department. This in turn will aid

the Sweet Menu restaurant to avoid the condition of excessive and shortage of finance

(Eccles and Holt, 2005).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Flow of funds can be managed: - Financial planning also aids the company to manage

the inflow and outflow of funds from within and outside the organization. This in turn

will assist the company to maintain the balance between receipt and payment.

Reduces the condition of uncertainty :-Planning of all the financial activities in

advance will assist the Sweet Menu restaurant to reduce the level of uncertainty which

could be faced by the restaurant due to change in business environment.

Maximum utilization of resources can be made: - Planning of all the activities in the

company, Sweet Menu restaurant will be able to utilize the available resources to the full

extend. Utilization of the resources to the full extent will aid the company to reduce the

wastage of the company (Sullivan, 2009).

To manage income more efficiently: - Financial planning will aid the Sweet Menu

Restaurant to easily manage income generated by the company in more efficient manner.

Managing all the income efficiently will assist the company increase its profit margin.

To increase the cash flow and monitor spending habits and expenses: - Planning of

all the financial activities in advance will assist the Sweet Menu Restaurant to monitor

the spending habits and expenses of the company. At the same time it increases the flow

of cash within the organizations.

To build a long term capital base and shape financial future:- Financial planning of

all the activities will help the Sweet Menu restaurant to build a long term capital base

which in turn shapes the financial future activities of the company.

Sale forecast: - Sweet Menu Restaurant will also be to forecast its sales by planning all

the financial activities in advance.

2.3 Information needed by decision maker of Sweet Menu Restaurant

Various types of information are needed by different decision maker of the Sweet Menu

restaurant. Some of them are listed below:-

Shareholders: - Shareholders are one of the valuable persons to the organization. These

individual invest their personal saving in order to avail high return on investment by the

company (Efendi, Srivastava and Swanson, 2007). These shareholders invest in company

by seeing its financial position. Therefore, in order to see the position of the company

shareholders wants all types of financial statements. They also prefer these statements in

8

the inflow and outflow of funds from within and outside the organization. This in turn

will assist the company to maintain the balance between receipt and payment.

Reduces the condition of uncertainty :-Planning of all the financial activities in

advance will assist the Sweet Menu restaurant to reduce the level of uncertainty which

could be faced by the restaurant due to change in business environment.

Maximum utilization of resources can be made: - Planning of all the activities in the

company, Sweet Menu restaurant will be able to utilize the available resources to the full

extend. Utilization of the resources to the full extent will aid the company to reduce the

wastage of the company (Sullivan, 2009).

To manage income more efficiently: - Financial planning will aid the Sweet Menu

Restaurant to easily manage income generated by the company in more efficient manner.

Managing all the income efficiently will assist the company increase its profit margin.

To increase the cash flow and monitor spending habits and expenses: - Planning of

all the financial activities in advance will assist the Sweet Menu Restaurant to monitor

the spending habits and expenses of the company. At the same time it increases the flow

of cash within the organizations.

To build a long term capital base and shape financial future:- Financial planning of

all the activities will help the Sweet Menu restaurant to build a long term capital base

which in turn shapes the financial future activities of the company.

Sale forecast: - Sweet Menu Restaurant will also be to forecast its sales by planning all

the financial activities in advance.

2.3 Information needed by decision maker of Sweet Menu Restaurant

Various types of information are needed by different decision maker of the Sweet Menu

restaurant. Some of them are listed below:-

Shareholders: - Shareholders are one of the valuable persons to the organization. These

individual invest their personal saving in order to avail high return on investment by the

company (Efendi, Srivastava and Swanson, 2007). These shareholders invest in company

by seeing its financial position. Therefore, in order to see the position of the company

shareholders wants all types of financial statements. They also prefer these statements in

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

order to decide whether the company is in a position to pay them high return on

investment or not.

Employees: - They are the persons who work for the betterment of the restaurant. They

simply want healthy working environment, job securities and respect from all the other

members present in the organization. They only want to see the income and expenditure

account of the company to find out whether the company is generating profit or not.

Suppliers: - they are the persons who supply raw material to the Sweet Menu restaurant.

They simply want to see the financial statements of the company in order to decide

whether the company is in a position to pay them for the goods supplied by them or not

(Ross, 2008).

Government: - Government is a body of individual who affects the working of the

organization. They simply want to see the financial statement and company's audit report

in order to find out the company’s position. And at the same time find out the amount of

tax need to be paid by the company out of the profit earned.

Customer: - Customers are the persons who want value for the money spend. These

individual is not required any types of financial statements for taking decisions. They

simply want best quality products at reasonable rates.

Banker: - Bankers are the persons who provide loan and other facility to the company.

These bankers simply want the financial statements and balance sheet of the company in

order to decide whether company is in a position to pay back the loan or not.

Community: - Community simply prefers annual report of the company in order to find

out the CSR of the company in order to take various necessary decisions.

Owner: - Owner is a person who actually has started the business by investing its

personal saving into it. They use financial statements and balance sheet in order to see

how much profit it is generating and whether company is growing or not.

Manager: - Manager is the individual who works for the wealth of the company. They

want financial statements and balance sheet in order to find out the growth rate of the

company. At the same time it also uses these statements to develop various strategies to

achieve the company set target and objective.

9

investment or not.

Employees: - They are the persons who work for the betterment of the restaurant. They

simply want healthy working environment, job securities and respect from all the other

members present in the organization. They only want to see the income and expenditure

account of the company to find out whether the company is generating profit or not.

Suppliers: - they are the persons who supply raw material to the Sweet Menu restaurant.

They simply want to see the financial statements of the company in order to decide

whether the company is in a position to pay them for the goods supplied by them or not

(Ross, 2008).

Government: - Government is a body of individual who affects the working of the

organization. They simply want to see the financial statement and company's audit report

in order to find out the company’s position. And at the same time find out the amount of

tax need to be paid by the company out of the profit earned.

Customer: - Customers are the persons who want value for the money spend. These

individual is not required any types of financial statements for taking decisions. They

simply want best quality products at reasonable rates.

Banker: - Bankers are the persons who provide loan and other facility to the company.

These bankers simply want the financial statements and balance sheet of the company in

order to decide whether company is in a position to pay back the loan or not.

Community: - Community simply prefers annual report of the company in order to find

out the CSR of the company in order to take various necessary decisions.

Owner: - Owner is a person who actually has started the business by investing its

personal saving into it. They use financial statements and balance sheet in order to see

how much profit it is generating and whether company is growing or not.

Manager: - Manager is the individual who works for the wealth of the company. They

want financial statements and balance sheet in order to find out the growth rate of the

company. At the same time it also uses these statements to develop various strategies to

achieve the company set target and objective.

9

2.4 Impact of sources of finance identified on financial statements

Sale of fixed assets: - Entry of sale of fixed assets will be shown on the asset side of the

balance sheet. This will be deducted from the fixed assets sold and at the same time cash

will also increase.

Friends and family: - No entry will be made for the borrowing made by the friends and

family. But if interest is paid to them than in that case its entry will be shown in

expenditure side of the profit and loss account under the head of interest paid (Lennard,

2007).

Issue of shares and debentures: - Entry of issue of shares and debentures will be shown

on the liability side of the balance sheet under the head of Share capital.

Hire purchasing: - Only entry of installment paid by the Sweet Menu restaurant will be

shown on the expenditure side in the profit and loss account (Refer to appendix 1).

TASK 3

3.1 Analyze of the cash budget in order to take appropriate decisions

After analyzing the cash budget of the company it could be concluded that inflow and

outflow of the funds is constantly changing. In the month of September it is seen that payment

made by the company was more than the double of the income generated by the company. Thus,

at the same time it seen that payment paid by the Blue Island Restaurant is less as compared to

the sales made for the two months. But again in the month of December payment of the company

increases as compared to the income generated. Therefore, at last it could be concluded that

company is not using appropriate strategies. This in turn is creating imbalance in the flow of

funds.

3.2 Calculation of unit cost and relevant pricing decisions

(Enclosed in appendix 2)

Unit price = 16-4-2= £10

From the following calculation it could be analyzed that per unit cost of every meal is

£10. This cost is calculated by deducting the Mark up price and VAT from the Final price of per

meal.

10

Sale of fixed assets: - Entry of sale of fixed assets will be shown on the asset side of the

balance sheet. This will be deducted from the fixed assets sold and at the same time cash

will also increase.

Friends and family: - No entry will be made for the borrowing made by the friends and

family. But if interest is paid to them than in that case its entry will be shown in

expenditure side of the profit and loss account under the head of interest paid (Lennard,

2007).

Issue of shares and debentures: - Entry of issue of shares and debentures will be shown

on the liability side of the balance sheet under the head of Share capital.

Hire purchasing: - Only entry of installment paid by the Sweet Menu restaurant will be

shown on the expenditure side in the profit and loss account (Refer to appendix 1).

TASK 3

3.1 Analyze of the cash budget in order to take appropriate decisions

After analyzing the cash budget of the company it could be concluded that inflow and

outflow of the funds is constantly changing. In the month of September it is seen that payment

made by the company was more than the double of the income generated by the company. Thus,

at the same time it seen that payment paid by the Blue Island Restaurant is less as compared to

the sales made for the two months. But again in the month of December payment of the company

increases as compared to the income generated. Therefore, at last it could be concluded that

company is not using appropriate strategies. This in turn is creating imbalance in the flow of

funds.

3.2 Calculation of unit cost and relevant pricing decisions

(Enclosed in appendix 2)

Unit price = 16-4-2= £10

From the following calculation it could be analyzed that per unit cost of every meal is

£10. This cost is calculated by deducting the Mark up price and VAT from the Final price of per

meal.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.