Financial Analysis and Ratio Evaluation

VerifiedAdded on 2019/12/03

|24

|3996

|149

Essay

AI Summary

A financial analysis of two companies, Southwood Electricals and Westbrook Engineering, is provided. The analysis includes an examination of their profits and losses at various levels, as well as the effects of fluctuations in break-even point (BEP). The financial performance of both companies is evaluated using various accounting ratios, including liquidity ratios, activity ratios, and profitability ratios. The results indicate that Southwood Electricals needs to focus on improving its liquidity position, while Westbrook Engineering has an excellent activity level but may require improvement in profitability. Overall, the analysis highlights the importance of financial management in ensuring investment decisions are taken appropriately.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MFRD

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Introduction......................................................................................................................................1

Task 1 Finance as a resource...........................................................................................................1

Sources of Finance.......................................................................................................................1

Implications of each source.........................................................................................................3

Case Studies.................................................................................................................................4

Task 2 Understand the implications of finance as a source.............................................................5

Financial planning.......................................................................................................................5

Financial decision making...........................................................................................................5

Sample of Financial Statements...................................................................................................6

Task 3 Making Financial Decisions................................................................................................8

Analysing the sales budget and cash forecast..............................................................................8

Investment appraisal methods....................................................................................................10

Costing and pricing review........................................................................................................13

Impact on the profits..................................................................................................................16

Task 4 analysing the financial performance..................................................................................17

Accounting terminology............................................................................................................17

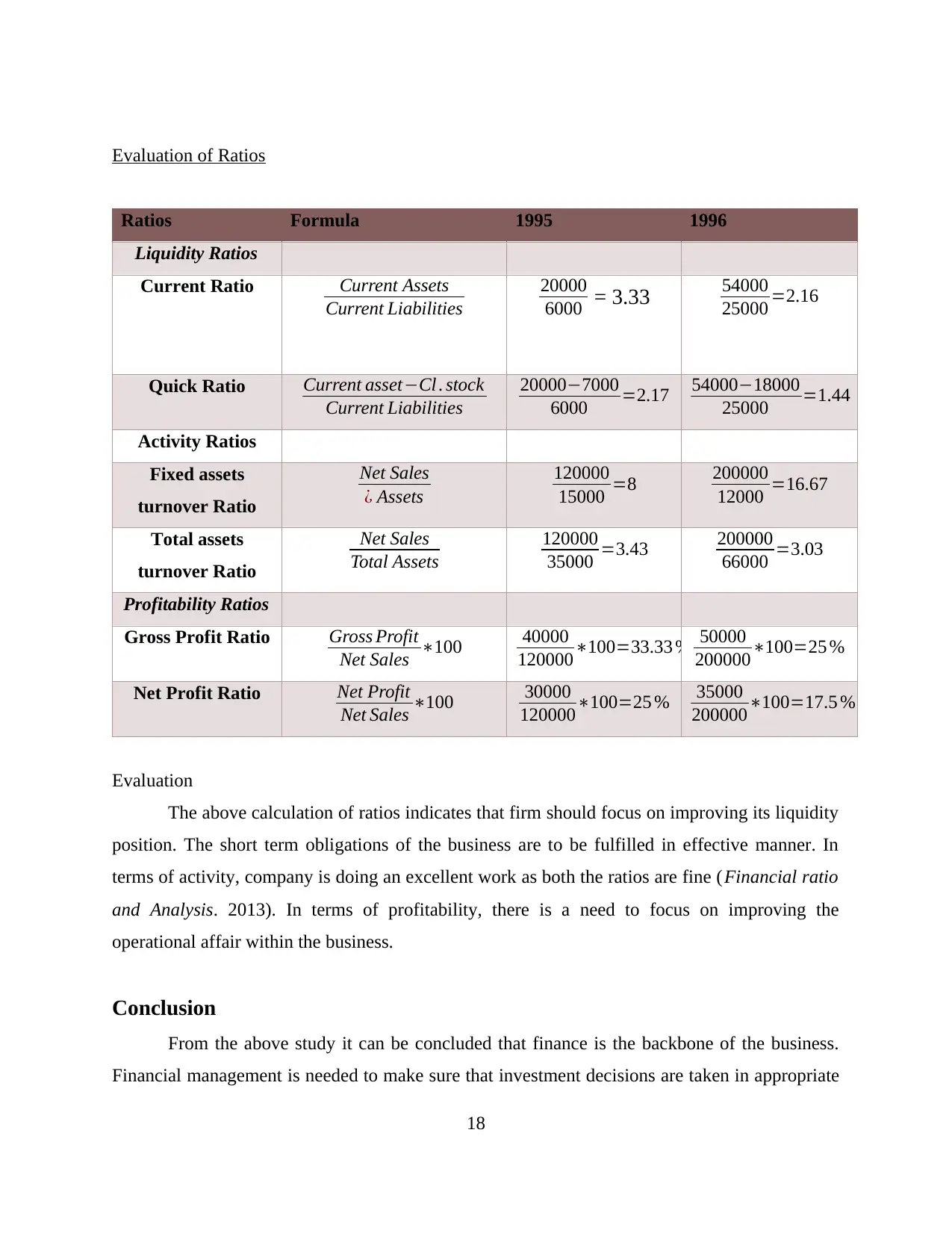

Evaluation of Ratios..................................................................................................................18

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

Introduction......................................................................................................................................1

Task 1 Finance as a resource...........................................................................................................1

Sources of Finance.......................................................................................................................1

Implications of each source.........................................................................................................3

Case Studies.................................................................................................................................4

Task 2 Understand the implications of finance as a source.............................................................5

Financial planning.......................................................................................................................5

Financial decision making...........................................................................................................5

Sample of Financial Statements...................................................................................................6

Task 3 Making Financial Decisions................................................................................................8

Analysing the sales budget and cash forecast..............................................................................8

Investment appraisal methods....................................................................................................10

Costing and pricing review........................................................................................................13

Impact on the profits..................................................................................................................16

Task 4 analysing the financial performance..................................................................................17

Accounting terminology............................................................................................................17

Evaluation of Ratios..................................................................................................................18

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

LIST OF FIGURES

Figure 1: Source of Finance.............................................................................................................1

Figure 2 Positive and Negative implications of Internal Sources....................................................3

Figure 3: Positive and Negative implications of External Sources.................................................4

Figure 1: Source of Finance.............................................................................................................1

Figure 2 Positive and Negative implications of Internal Sources....................................................3

Figure 3: Positive and Negative implications of External Sources.................................................4

List of tables

Table 1 Format of Income Statement..............................................................................................7

Table 2: Format of Balance Sheet...................................................................................................7

Table 3 Sales Budget.......................................................................................................................8

Table 4: Cash Flow Forecasts..........................................................................................................9

Table 5: Calculation of ARR.........................................................................................................10

Table 6: Calculation of IRR...........................................................................................................12

Table 7 NPV calculation for project A..........................................................................................12

Table 8: NPV calculation for project B.........................................................................................13

Table 9: Impact on Break Even Point............................................................................................14

Table 10: Profit and Loss at various levels....................................................................................16

Table 11¨ Effects of fluctuations in BEP.......................................................................................16

Table 1 Format of Income Statement..............................................................................................7

Table 2: Format of Balance Sheet...................................................................................................7

Table 3 Sales Budget.......................................................................................................................8

Table 4: Cash Flow Forecasts..........................................................................................................9

Table 5: Calculation of ARR.........................................................................................................10

Table 6: Calculation of IRR...........................................................................................................12

Table 7 NPV calculation for project A..........................................................................................12

Table 8: NPV calculation for project B.........................................................................................13

Table 9: Impact on Break Even Point............................................................................................14

Table 10: Profit and Loss at various levels....................................................................................16

Table 11¨ Effects of fluctuations in BEP.......................................................................................16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction

Managing financial resources is a difficult task as it needs effective financial planning. It

is important to do planning at every step in order to attain productive results for the business. The

purpose of this report is to evaluate how the financial is being managed within business. It will

identify the appropriate sources of finance for a business. It will also show the use of monetary

information for different stakeholders. At last the report will end in analysing the company

statements and the ratios

Task 1 Finance as a resource

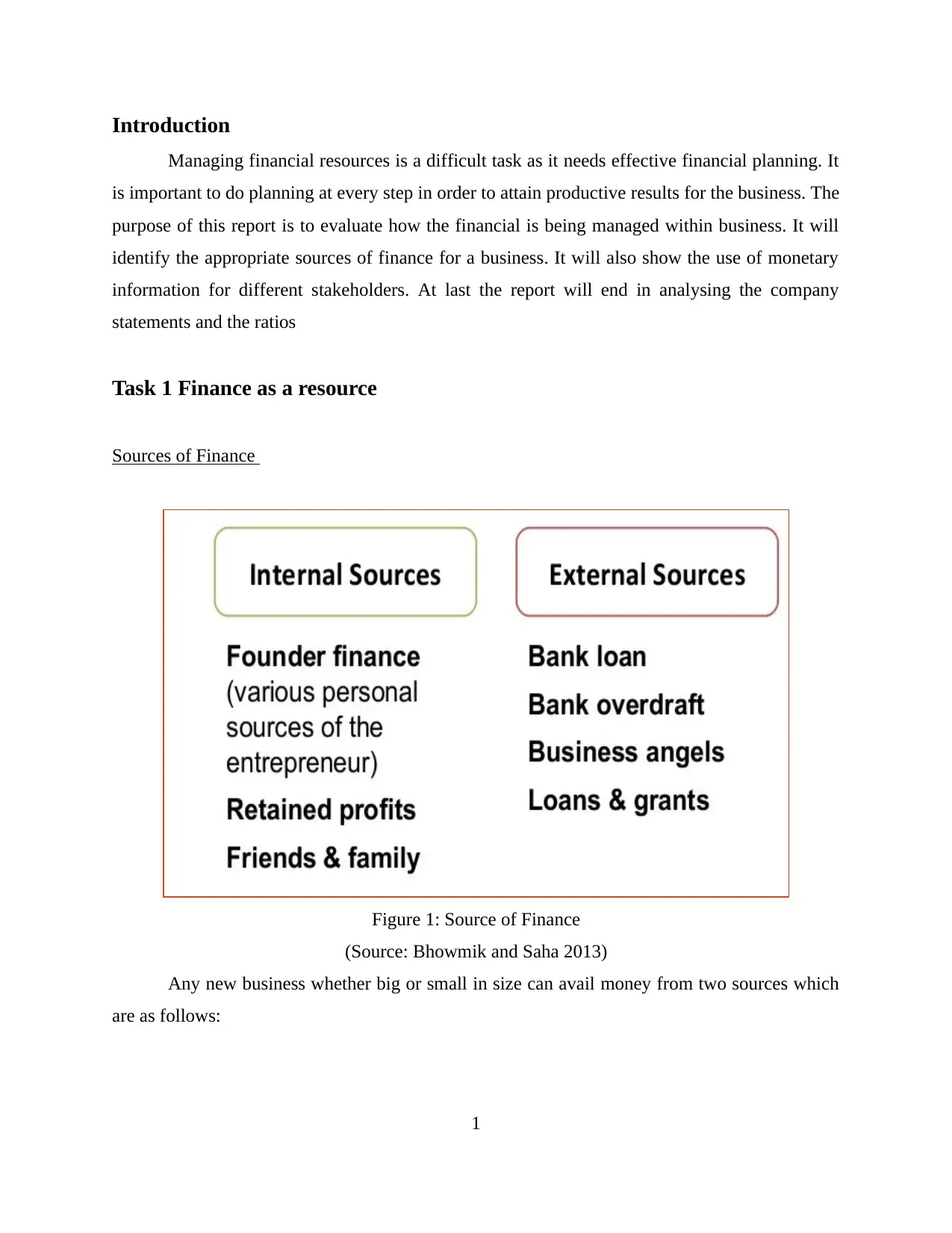

Sources of Finance

Figure 1: Source of Finance

(Source: Bhowmik and Saha 2013)

Any new business whether big or small in size can avail money from two sources which

are as follows:

1

Managing financial resources is a difficult task as it needs effective financial planning. It

is important to do planning at every step in order to attain productive results for the business. The

purpose of this report is to evaluate how the financial is being managed within business. It will

identify the appropriate sources of finance for a business. It will also show the use of monetary

information for different stakeholders. At last the report will end in analysing the company

statements and the ratios

Task 1 Finance as a resource

Sources of Finance

Figure 1: Source of Finance

(Source: Bhowmik and Saha 2013)

Any new business whether big or small in size can avail money from two sources which

are as follows:

1

Internal Sources

Retained profits – It is the amount of money derived after the payment of divided to the

shareholders and after the withdrawing of capital from the partners. It is also regarded as

the ploughing back of profits (Kitchen and Confetto, 2010)

Friends & Family – Money can also be arranged from easily available options such as

from friends, family and close ones.

External Sources:

Bank Loan – These days’ loans are available for the business from several financial

institutions. Loan are provided with the range from 1 to 25 years. It is the most

commonly available option for the entrepreneurs (Ball, Jayaraman and Shivakumar,

2012)

Bank overdraft - All businesses are required to keep their personal accounts through

which transactions are performed. All the deposits and withdrawals are performed from

the side of the bank. The overdraft are issued to fulfil the differences between the

proceeds and its costs.

Business angels – These people offers capital for the start-up generally in exchange for

convertible debt or ownership equity (Bonaci, Matiş and Strouhal, 2008).

Trade credit – It is a kind of short term money which is given to the borrower in order to

pay for the goods which are received. It offers flexibility at the initial stages of the

business.

2

Retained profits – It is the amount of money derived after the payment of divided to the

shareholders and after the withdrawing of capital from the partners. It is also regarded as

the ploughing back of profits (Kitchen and Confetto, 2010)

Friends & Family – Money can also be arranged from easily available options such as

from friends, family and close ones.

External Sources:

Bank Loan – These days’ loans are available for the business from several financial

institutions. Loan are provided with the range from 1 to 25 years. It is the most

commonly available option for the entrepreneurs (Ball, Jayaraman and Shivakumar,

2012)

Bank overdraft - All businesses are required to keep their personal accounts through

which transactions are performed. All the deposits and withdrawals are performed from

the side of the bank. The overdraft are issued to fulfil the differences between the

proceeds and its costs.

Business angels – These people offers capital for the start-up generally in exchange for

convertible debt or ownership equity (Bonaci, Matiş and Strouhal, 2008).

Trade credit – It is a kind of short term money which is given to the borrower in order to

pay for the goods which are received. It offers flexibility at the initial stages of the

business.

2

Implications of each source

Figure 2 Positive and Negative implications of Internal Sources

There are positive and negative implications associated with the identified sources of

finance above:

Trade credit - This source of finance is offered within a bounded time limit. The cycle for trade

credit runs for a period of 28 days (Goldman and Carrier, 2010). Company is required to return

back the credit within the stated time period. The credit is also obtained on the basis of a good

image and reputation.

Bank overdraft – Very high interest charges are associated with the bank overdraft. There is

option to exceed the prescribed limit of overdraft in case if more finance is required. Here the

power and control to operate the account remains with the bank (Joseph, 2013)

Bank Loans – Every bank has its own rate of interests. The business will required to fulfil all the

legal formalities and paper work in order to derive the loan. In case if the borrower proves to be

faulty in payments then bank has the right to cease his business operations and to declare

bankruptcy.

Retained profits – For this option to become successful, it is needed that business should earn

high amount of profits in the early stages of functioning. However there are no issues related

with ownership and control (Keller, 2013).

3

Advantages

Economical

Flexibility

Low rate of risk

Serve long term purposes

Disadvantages

Fixed burden

Charge on assets

Diificulty of raising

finance

Factor of

Uncertainty

Figure 2 Positive and Negative implications of Internal Sources

There are positive and negative implications associated with the identified sources of

finance above:

Trade credit - This source of finance is offered within a bounded time limit. The cycle for trade

credit runs for a period of 28 days (Goldman and Carrier, 2010). Company is required to return

back the credit within the stated time period. The credit is also obtained on the basis of a good

image and reputation.

Bank overdraft – Very high interest charges are associated with the bank overdraft. There is

option to exceed the prescribed limit of overdraft in case if more finance is required. Here the

power and control to operate the account remains with the bank (Joseph, 2013)

Bank Loans – Every bank has its own rate of interests. The business will required to fulfil all the

legal formalities and paper work in order to derive the loan. In case if the borrower proves to be

faulty in payments then bank has the right to cease his business operations and to declare

bankruptcy.

Retained profits – For this option to become successful, it is needed that business should earn

high amount of profits in the early stages of functioning. However there are no issues related

with ownership and control (Keller, 2013).

3

Advantages

Economical

Flexibility

Low rate of risk

Serve long term purposes

Disadvantages

Fixed burden

Charge on assets

Diificulty of raising

finance

Factor of

Uncertainty

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Angels – Under this case, as money is raised from outside investors hence they could

demand for convertible debts or ownership equity. This will have an impact on ownership and

control.

Friend and family – As discussed earlier it is the most easily available option for raising the

money (Lampe and Hofmann, 2013). However it can be adopted only when the borrower shares

a good bonding with his friend and family.

Figure 3: Positive and Negative implications of External Sources

Case Studies

Case -1 Small start-up of venture

Smith is seeking to start a new business related to the manufacturing of chairs. At the

starting, he focused on getting small contracts and orders from the clients. A sum of £ 6000 was

needed for start-up and he was the sole owner of the business (Abraham, Deo and Irvine, 2008).

Case -2 Expansion of business through partnership

After 3 years of operations, Smith decided to expand the business through involving

some partners into it. More cash was arranged through the capitals invested from the partners.

Money was also arranged by selling of an old land worth £20000. The business started taking big

orders.

4

Advantages

No obligation to repay the

money

Provide secured financing

No interest and set up fees

can facilitate faster growth

Disadvantages

time consuming process

possible loss of control

Many legal and regulatory

issues to be fulfilled

Due diligence is normally

required

demand for convertible debts or ownership equity. This will have an impact on ownership and

control.

Friend and family – As discussed earlier it is the most easily available option for raising the

money (Lampe and Hofmann, 2013). However it can be adopted only when the borrower shares

a good bonding with his friend and family.

Figure 3: Positive and Negative implications of External Sources

Case Studies

Case -1 Small start-up of venture

Smith is seeking to start a new business related to the manufacturing of chairs. At the

starting, he focused on getting small contracts and orders from the clients. A sum of £ 6000 was

needed for start-up and he was the sole owner of the business (Abraham, Deo and Irvine, 2008).

Case -2 Expansion of business through partnership

After 3 years of operations, Smith decided to expand the business through involving

some partners into it. More cash was arranged through the capitals invested from the partners.

Money was also arranged by selling of an old land worth £20000. The business started taking big

orders.

4

Advantages

No obligation to repay the

money

Provide secured financing

No interest and set up fees

can facilitate faster growth

Disadvantages

time consuming process

possible loss of control

Many legal and regulatory

issues to be fulfilled

Due diligence is normally

required

Case- 3 More expansion

For further expansion they all registered themselves by a public limited corporation. In

this they manner they are able to sell their shares (Bonaci, Matiş and Strouhal, 2008). Further

growth and development was achieved through the reinvested profits.

Task 2 Understand the implications of finance as a source

Financial planning

Financial planning plays a crucial role in the functioning of the business operations. It

helps in identifying the risks and uncertainties associated with the new venture. It takes into

consideration different types of factors such as funds, location, legal aspects and resources etc

(Booker, 2006). It is also about estimating the finance needed for the business. It is helpful in

framing of financial policies related to management, procurement and investment of the money.

It is also useful in managing cash outflow and cash inflow within the company. There is a need

to maintain stability in the operations and this is not possible without doing financial planning

(Broadbent and Cullen, 2012).

It will also select the appropriate investment with right financial needs and objectives.

Planning also helps in fixing the most suitable capital structure for the business. A link can be

established between the present and future financial requirements through this function. The

income within the business can be managed in appropriate manner (Hawawini and Viallet,

2010). Company can keep it hard earned cash through tax planning, proper budgeting and

sensible spending. Through planning cash flow can be increased and increased cash flow results

in increase in capital also. Presence of adequate capital ensures the organization to think about

making other investments. The planning helps in achieving coordination between several

business activities such as production, marketing, human resource management etc. In this

manner company will be able to understand how amount of funds are required for paying the

taxes and payment for other expenses (Ittelson, 2009).

Financial decision making

The Finance department of an organization is responsible for producing variety of

information which assists in making of several decisions. The financial information produced

5

For further expansion they all registered themselves by a public limited corporation. In

this they manner they are able to sell their shares (Bonaci, Matiş and Strouhal, 2008). Further

growth and development was achieved through the reinvested profits.

Task 2 Understand the implications of finance as a source

Financial planning

Financial planning plays a crucial role in the functioning of the business operations. It

helps in identifying the risks and uncertainties associated with the new venture. It takes into

consideration different types of factors such as funds, location, legal aspects and resources etc

(Booker, 2006). It is also about estimating the finance needed for the business. It is helpful in

framing of financial policies related to management, procurement and investment of the money.

It is also useful in managing cash outflow and cash inflow within the company. There is a need

to maintain stability in the operations and this is not possible without doing financial planning

(Broadbent and Cullen, 2012).

It will also select the appropriate investment with right financial needs and objectives.

Planning also helps in fixing the most suitable capital structure for the business. A link can be

established between the present and future financial requirements through this function. The

income within the business can be managed in appropriate manner (Hawawini and Viallet,

2010). Company can keep it hard earned cash through tax planning, proper budgeting and

sensible spending. Through planning cash flow can be increased and increased cash flow results

in increase in capital also. Presence of adequate capital ensures the organization to think about

making other investments. The planning helps in achieving coordination between several

business activities such as production, marketing, human resource management etc. In this

manner company will be able to understand how amount of funds are required for paying the

taxes and payment for other expenses (Ittelson, 2009).

Financial decision making

The Finance department of an organization is responsible for producing variety of

information which assists in making of several decisions. The financial information produced

5

from the financial statements is very useful for different types of decision makers. The types of

information can be listed as follows:

Costing information

Value of the total assets and total liabilities

Figures of the net profit and gross profit

Amount of cash flow at the end of the financial period

Information about the sales and revenues (Siano, Kitchen and Confetto, 2010)

Cash flow from financing, investing and operating activities

Cash budget, sales budget, purchase budget, etc

The information need for various decision makers is as follows:

Employees – These people require financial information in order to take decisions about

their career opportunities and growth within the company.

Creditors – These are the ones who have lend their money to the firm. They need

information so that they can identify whether business has the potential to make timely

payments or not (Bhowmik and Saha, 2013)

Tax authorities – The tax authorities are responsible for assuring that whether company is

making timely payment of taxes or not.

Shareholders – These people take investment decision related to buying and selling of

shares. Shareholders always are of an expectation that company’s share will perform well

in the market as this offers them high dividends.

Lenders – Lending bodies wants to have a check on liquidity and gearing position of the

business before rendering the loan. It is to be assured that whether borrower is capable of

paying the loan back or not (Kitchen and Confetto, 2010)

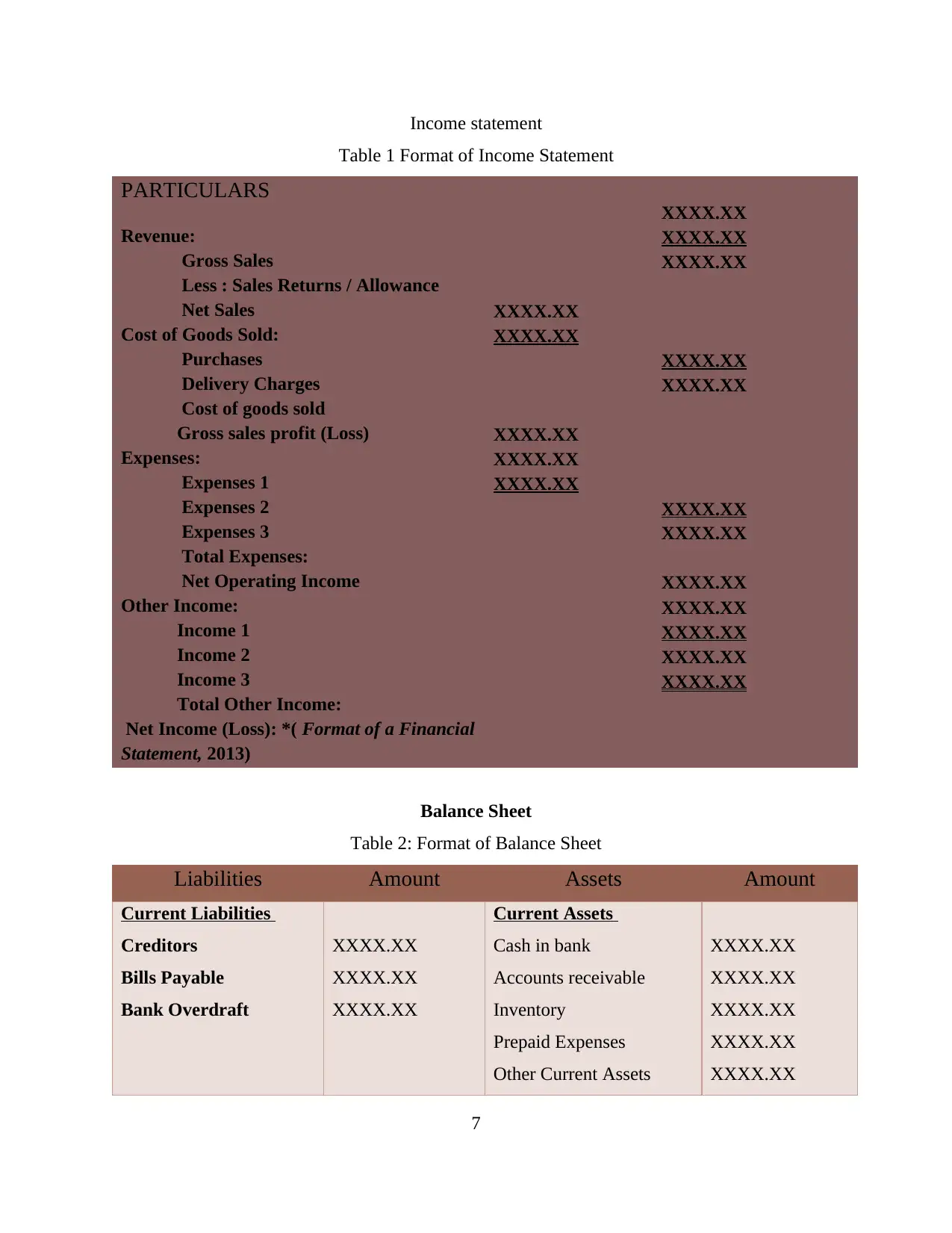

Sample of Financial Statements

Given below are the samples of income statement and balance sheet.

6

information can be listed as follows:

Costing information

Value of the total assets and total liabilities

Figures of the net profit and gross profit

Amount of cash flow at the end of the financial period

Information about the sales and revenues (Siano, Kitchen and Confetto, 2010)

Cash flow from financing, investing and operating activities

Cash budget, sales budget, purchase budget, etc

The information need for various decision makers is as follows:

Employees – These people require financial information in order to take decisions about

their career opportunities and growth within the company.

Creditors – These are the ones who have lend their money to the firm. They need

information so that they can identify whether business has the potential to make timely

payments or not (Bhowmik and Saha, 2013)

Tax authorities – The tax authorities are responsible for assuring that whether company is

making timely payment of taxes or not.

Shareholders – These people take investment decision related to buying and selling of

shares. Shareholders always are of an expectation that company’s share will perform well

in the market as this offers them high dividends.

Lenders – Lending bodies wants to have a check on liquidity and gearing position of the

business before rendering the loan. It is to be assured that whether borrower is capable of

paying the loan back or not (Kitchen and Confetto, 2010)

Sample of Financial Statements

Given below are the samples of income statement and balance sheet.

6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Income statement

Table 1 Format of Income Statement

PARTICULARS

Revenue:

Gross Sales

Less : Sales Returns / Allowance

Net Sales

Cost of Goods Sold:

Purchases

Delivery Charges

Cost of goods sold

Gross sales profit (Loss)

Expenses:

Expenses 1

Expenses 2

Expenses 3

Total Expenses:

Net Operating Income

Other Income:

Income 1

Income 2

Income 3

Total Other Income:

Net Income (Loss): *( Format of a Financial

Statement, 2013)

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Balance Sheet

Table 2: Format of Balance Sheet

Liabilities Amount Assets Amount

Current Liabilities

Creditors

Bills Payable

Bank Overdraft

XXXX.XX

XXXX.XX

XXXX.XX

Current Assets

Cash in bank

Accounts receivable

Inventory

Prepaid Expenses

Other Current Assets

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

7

Table 1 Format of Income Statement

PARTICULARS

Revenue:

Gross Sales

Less : Sales Returns / Allowance

Net Sales

Cost of Goods Sold:

Purchases

Delivery Charges

Cost of goods sold

Gross sales profit (Loss)

Expenses:

Expenses 1

Expenses 2

Expenses 3

Total Expenses:

Net Operating Income

Other Income:

Income 1

Income 2

Income 3

Total Other Income:

Net Income (Loss): *( Format of a Financial

Statement, 2013)

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Balance Sheet

Table 2: Format of Balance Sheet

Liabilities Amount Assets Amount

Current Liabilities

Creditors

Bills Payable

Bank Overdraft

XXXX.XX

XXXX.XX

XXXX.XX

Current Assets

Cash in bank

Accounts receivable

Inventory

Prepaid Expenses

Other Current Assets

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

7

Fixed Liabilities

Bank Loan

Secured Loan

Other long term Loan

Capital and Net Profit

XXXX.XX

XXXX.XX

XXXX.XX

Total Current Assets

Fixed Assets

Machinery & Equipment’s

Furniture & Fixtures

Leasehold Improvements

Land & Buildings

Other Fixed Assets (Less

Accumulated

depreciation)

Total Fixed Assets

Other Assets

Intangibles

Deposits

Goodwill

Other

Total assets

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Task 3 Making Financial Decisions

Analysing the sales budget and cash forecast

Table 3 Sales Budget

Month Monthly

budget

Cumulative

Budget

Actual

Monthly

Actual

Cumulative

Variance

July 2,30,000 2,30,000 2,15,000 2,15,000 -15,000

August 2,30,000 4,60,000 2,20,000 4,35,000 -25,000

8

Bank Loan

Secured Loan

Other long term Loan

Capital and Net Profit

XXXX.XX

XXXX.XX

XXXX.XX

Total Current Assets

Fixed Assets

Machinery & Equipment’s

Furniture & Fixtures

Leasehold Improvements

Land & Buildings

Other Fixed Assets (Less

Accumulated

depreciation)

Total Fixed Assets

Other Assets

Intangibles

Deposits

Goodwill

Other

Total assets

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Task 3 Making Financial Decisions

Analysing the sales budget and cash forecast

Table 3 Sales Budget

Month Monthly

budget

Cumulative

Budget

Actual

Monthly

Actual

Cumulative

Variance

July 2,30,000 2,30,000 2,15,000 2,15,000 -15,000

August 2,30,000 4,60,000 2,20,000 4,35,000 -25,000

8

September 2,70,000 7,30,000 2,45,000 6,80,000 -50,000

October 2,65,000 9,95,000 2,35,000 9,15,000 -80,000

November 2,65,000 1,260,000 237,000 1,152,000 -108,000

December 300,000 1,560,000 270,000 1,422,000 -138,000

January 250,000 1,810,000

February 265,000 2,075,000

March 300,000 2,375,000

April 325,000 2,700,000

May 325,000 3,025,000

June 350,000 3,375,000

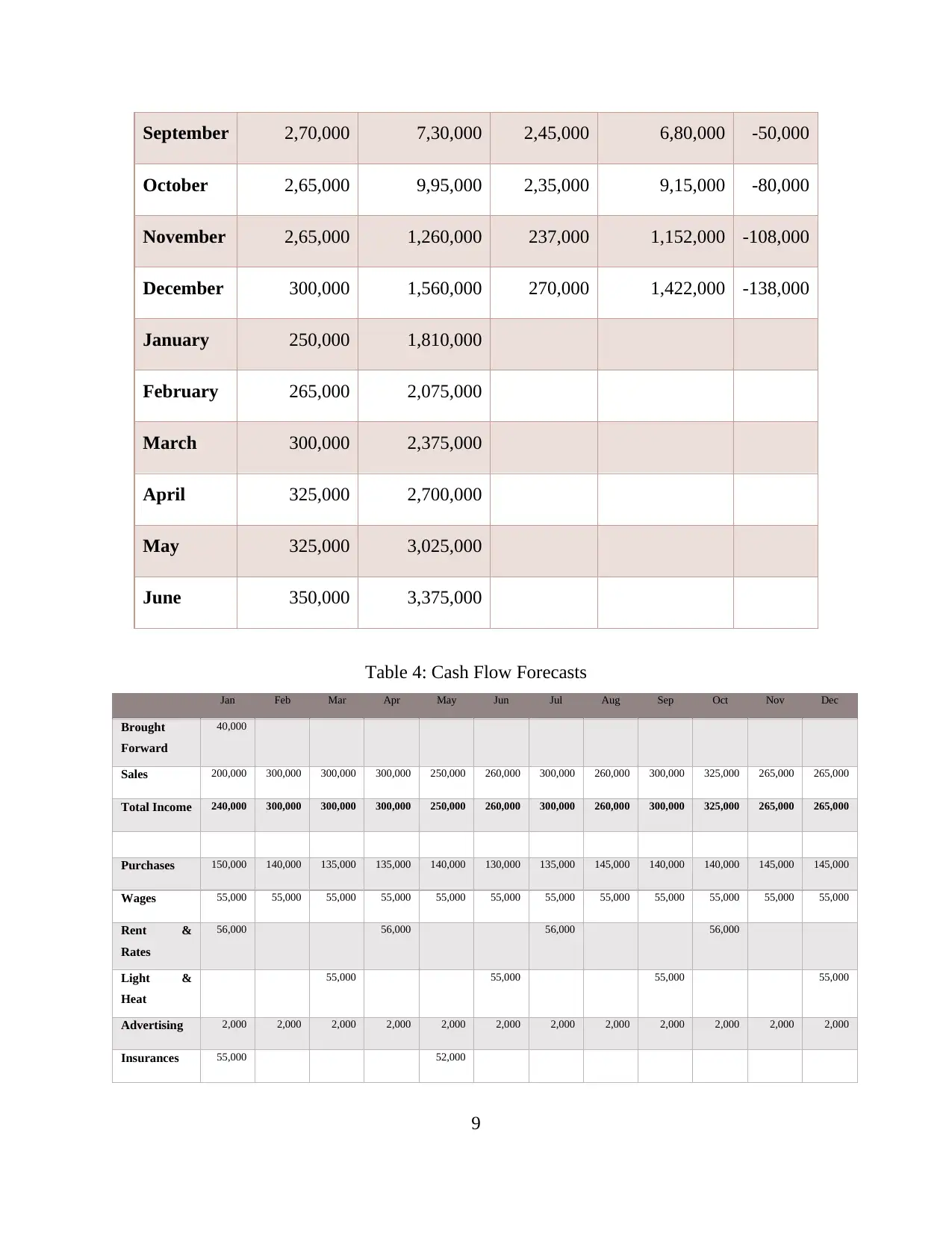

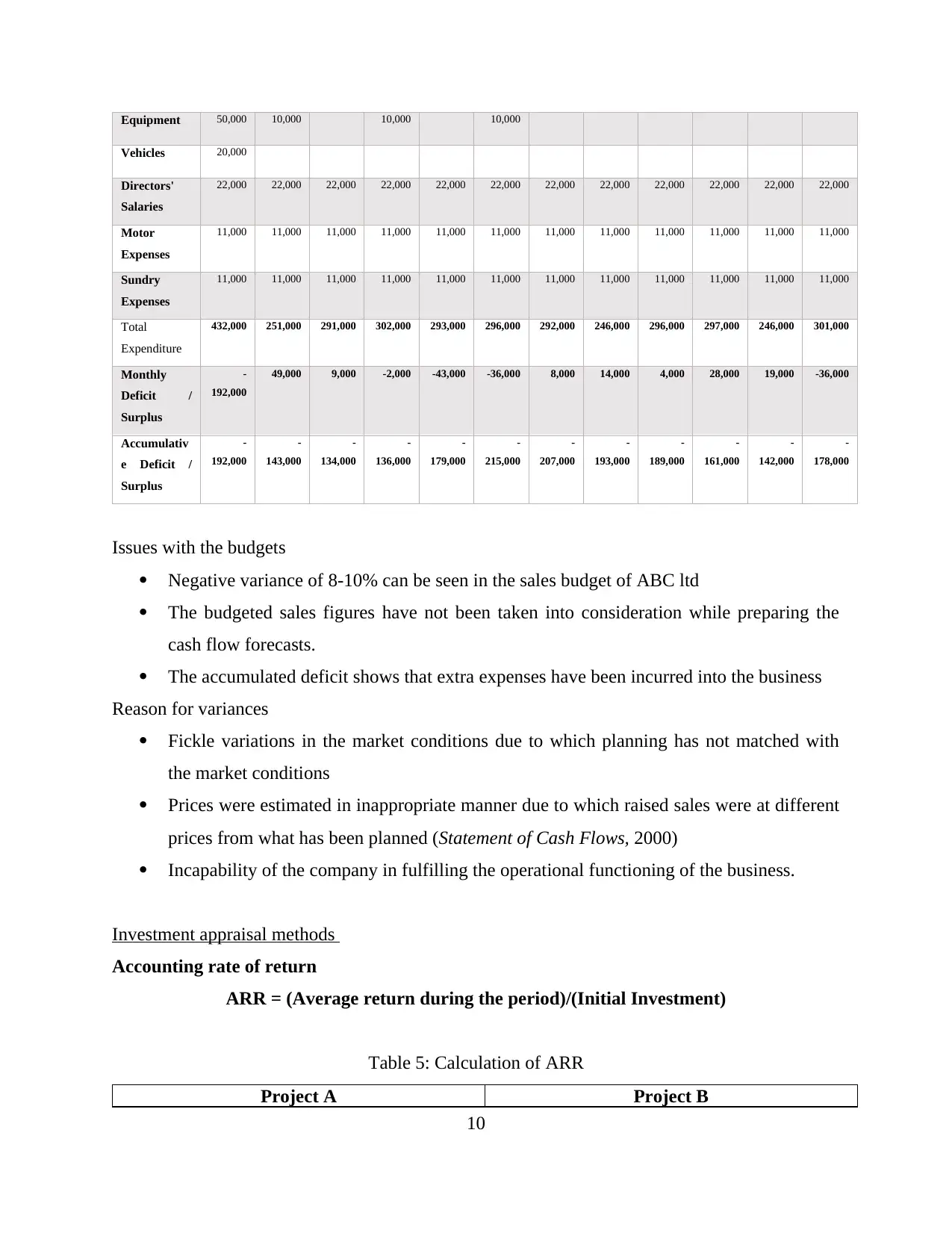

Table 4: Cash Flow Forecasts

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Brought

Forward

40,000

Sales 200,000 300,000 300,000 300,000 250,000 260,000 300,000 260,000 300,000 325,000 265,000 265,000

Total Income 240,000 300,000 300,000 300,000 250,000 260,000 300,000 260,000 300,000 325,000 265,000 265,000

Purchases 150,000 140,000 135,000 135,000 140,000 130,000 135,000 145,000 140,000 140,000 145,000 145,000

Wages 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000

Rent &

Rates

56,000 56,000 56,000 56,000

Light &

Heat

55,000 55,000 55,000 55,000

Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000

Insurances 55,000 52,000

9

October 2,65,000 9,95,000 2,35,000 9,15,000 -80,000

November 2,65,000 1,260,000 237,000 1,152,000 -108,000

December 300,000 1,560,000 270,000 1,422,000 -138,000

January 250,000 1,810,000

February 265,000 2,075,000

March 300,000 2,375,000

April 325,000 2,700,000

May 325,000 3,025,000

June 350,000 3,375,000

Table 4: Cash Flow Forecasts

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Brought

Forward

40,000

Sales 200,000 300,000 300,000 300,000 250,000 260,000 300,000 260,000 300,000 325,000 265,000 265,000

Total Income 240,000 300,000 300,000 300,000 250,000 260,000 300,000 260,000 300,000 325,000 265,000 265,000

Purchases 150,000 140,000 135,000 135,000 140,000 130,000 135,000 145,000 140,000 140,000 145,000 145,000

Wages 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000

Rent &

Rates

56,000 56,000 56,000 56,000

Light &

Heat

55,000 55,000 55,000 55,000

Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000

Insurances 55,000 52,000

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Equipment 50,000 10,000 10,000 10,000

Vehicles 20,000

Directors'

Salaries

22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000

Motor

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Sundry

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Total

Expenditure

432,000 251,000 291,000 302,000 293,000 296,000 292,000 246,000 296,000 297,000 246,000 301,000

Monthly

Deficit /

Surplus

-

192,000

49,000 9,000 -2,000 -43,000 -36,000 8,000 14,000 4,000 28,000 19,000 -36,000

Accumulativ

e Deficit /

Surplus

-

192,000

-

143,000

-

134,000

-

136,000

-

179,000

-

215,000

-

207,000

-

193,000

-

189,000

-

161,000

-

142,000

-

178,000

Issues with the budgets

Negative variance of 8-10% can be seen in the sales budget of ABC ltd

The budgeted sales figures have not been taken into consideration while preparing the

cash flow forecasts.

The accumulated deficit shows that extra expenses have been incurred into the business

Reason for variances

Fickle variations in the market conditions due to which planning has not matched with

the market conditions

Prices were estimated in inappropriate manner due to which raised sales were at different

prices from what has been planned (Statement of Cash Flows, 2000)

Incapability of the company in fulfilling the operational functioning of the business.

Investment appraisal methods

Accounting rate of return

ARR = (Average return during the period)/(Initial Investment)

Table 5: Calculation of ARR

Project A Project B

10

Vehicles 20,000

Directors'

Salaries

22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000

Motor

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Sundry

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Total

Expenditure

432,000 251,000 291,000 302,000 293,000 296,000 292,000 246,000 296,000 297,000 246,000 301,000

Monthly

Deficit /

Surplus

-

192,000

49,000 9,000 -2,000 -43,000 -36,000 8,000 14,000 4,000 28,000 19,000 -36,000

Accumulativ

e Deficit /

Surplus

-

192,000

-

143,000

-

134,000

-

136,000

-

179,000

-

215,000

-

207,000

-

193,000

-

189,000

-

161,000

-

142,000

-

178,000

Issues with the budgets

Negative variance of 8-10% can be seen in the sales budget of ABC ltd

The budgeted sales figures have not been taken into consideration while preparing the

cash flow forecasts.

The accumulated deficit shows that extra expenses have been incurred into the business

Reason for variances

Fickle variations in the market conditions due to which planning has not matched with

the market conditions

Prices were estimated in inappropriate manner due to which raised sales were at different

prices from what has been planned (Statement of Cash Flows, 2000)

Incapability of the company in fulfilling the operational functioning of the business.

Investment appraisal methods

Accounting rate of return

ARR = (Average return during the period)/(Initial Investment)

Table 5: Calculation of ARR

Project A Project B

10

ARR=810,000/450,000

ARR=1.8

ARR=180 %

ARR=680,000/450,000

ARR=1.5

ARR=150 %

Results – According to the ARR technique, the results are indicating that ABC Ltd should make

investment in proposal A as it is delivering a high rate of return.

Payback Period

Year Project A Project B

Cash flow (£) Cumulative value Cash flow (£) Cumulative

value

Initial Cost 450000 450000

1 180000 180000 60000 60000

2 230000 410000 120000 180000

3 280000 690000 250000 430000

4 120000 810000 250000 680000

Payback period = (Initial Investment) / (Cash Inflow per period)

For uneven cash flows,

Pay back period=A + B

C

A = last year value with a negative cumulative cash flow

B = absolute value of cumulative cash flow at the end of the period A

C = total cash flow while the period after A

For project A = 2+ 450000−410000

690000

= 2.05 years

11

ARR=1.8

ARR=180 %

ARR=680,000/450,000

ARR=1.5

ARR=150 %

Results – According to the ARR technique, the results are indicating that ABC Ltd should make

investment in proposal A as it is delivering a high rate of return.

Payback Period

Year Project A Project B

Cash flow (£) Cumulative value Cash flow (£) Cumulative

value

Initial Cost 450000 450000

1 180000 180000 60000 60000

2 230000 410000 120000 180000

3 280000 690000 250000 430000

4 120000 810000 250000 680000

Payback period = (Initial Investment) / (Cash Inflow per period)

For uneven cash flows,

Pay back period=A + B

C

A = last year value with a negative cumulative cash flow

B = absolute value of cumulative cash flow at the end of the period A

C = total cash flow while the period after A

For project A = 2+ 450000−410000

690000

= 2.05 years

11

For project B = 3+ 450000−430000

680000

= 3.02 years

According to the results of payback technique, ABC should make investment in project A

because it is recovering the initial costs in less period of time as compared to project B.

Internal Rate of Return

Table 6: Calculation of IRR

Year Cash Flow -

project A

PV

factor

@29%

PV @ 29%

- Project A

Cash Flow -

project B

PV factor

@ 15%

PV @ 15% -

Project B

1 180 0.78 139.53 60 0.87 52.17

2 230 0.60 138.21 120 0.76 90.74

3 280 0.47 130.43 250 0.66 164.38

4 120 0.36 43.33 250 0.57 142.94

Total

PV

451.51 450.23

Results – According to the IRR technique, the results are indicating that company should make

investment in project A because it is having better and higher internal rate of return.

Net present Value

Table 7 NPV calculation for project A

Year Cash flow (£) P.V. factor@ 10% Present Value (£)

1 180000 0.94 169200

2 230000 0.89 204700

3 280000 0.84 235200

4 120000 0.79 94800

Total Present value 703900

12

680000

= 3.02 years

According to the results of payback technique, ABC should make investment in project A

because it is recovering the initial costs in less period of time as compared to project B.

Internal Rate of Return

Table 6: Calculation of IRR

Year Cash Flow -

project A

PV

factor

@29%

PV @ 29%

- Project A

Cash Flow -

project B

PV factor

@ 15%

PV @ 15% -

Project B

1 180 0.78 139.53 60 0.87 52.17

2 230 0.60 138.21 120 0.76 90.74

3 280 0.47 130.43 250 0.66 164.38

4 120 0.36 43.33 250 0.57 142.94

Total

PV

451.51 450.23

Results – According to the IRR technique, the results are indicating that company should make

investment in project A because it is having better and higher internal rate of return.

Net present Value

Table 7 NPV calculation for project A

Year Cash flow (£) P.V. factor@ 10% Present Value (£)

1 180000 0.94 169200

2 230000 0.89 204700

3 280000 0.84 235200

4 120000 0.79 94800

Total Present value 703900

12

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

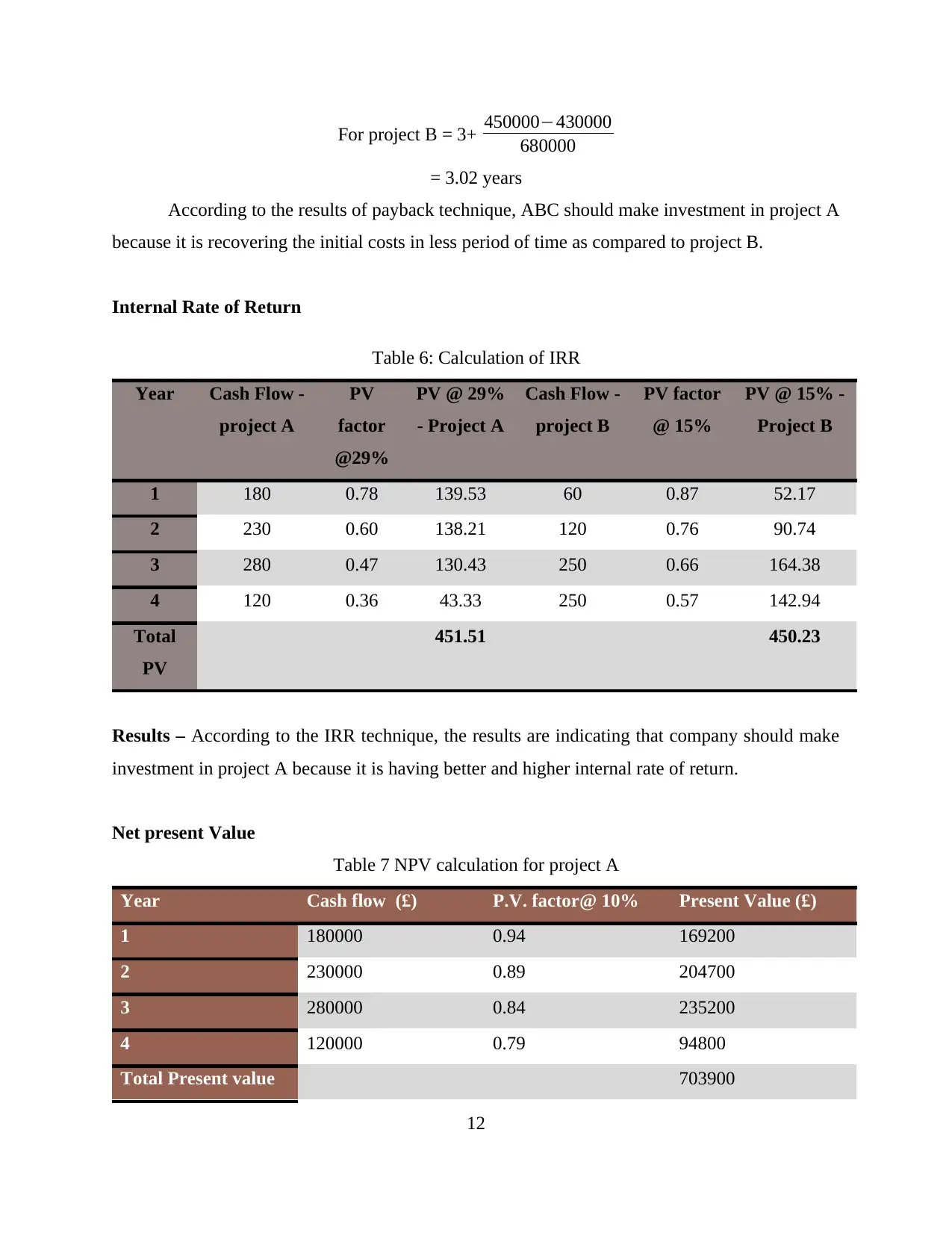

Initial investment (450000)

Net Present value 253900

Table 8: NPV calculation for project B

Year Cash flow (£) P.V. factor@ 10% Present Value (£)

1 60000 0.94 56400

2 120000 0.89 106800

3 250000 0.84 210000

4 250000 0.79 197500

Total Present value 570700

Initial investment (450000)

Net Present value 120700

Results - As per the results of NPV technique, ABC ltd should make investment in project A

because its NPV value is higher as compared to project B.

Recommendation

After analysing the results of all the investment appraisal techniques, it is recommended

that ABC should make investment in project A because it is better in terms of revenue, profits

and returns as compared to project B. It has the potential to bring substantial savings and cost

reductions for the company

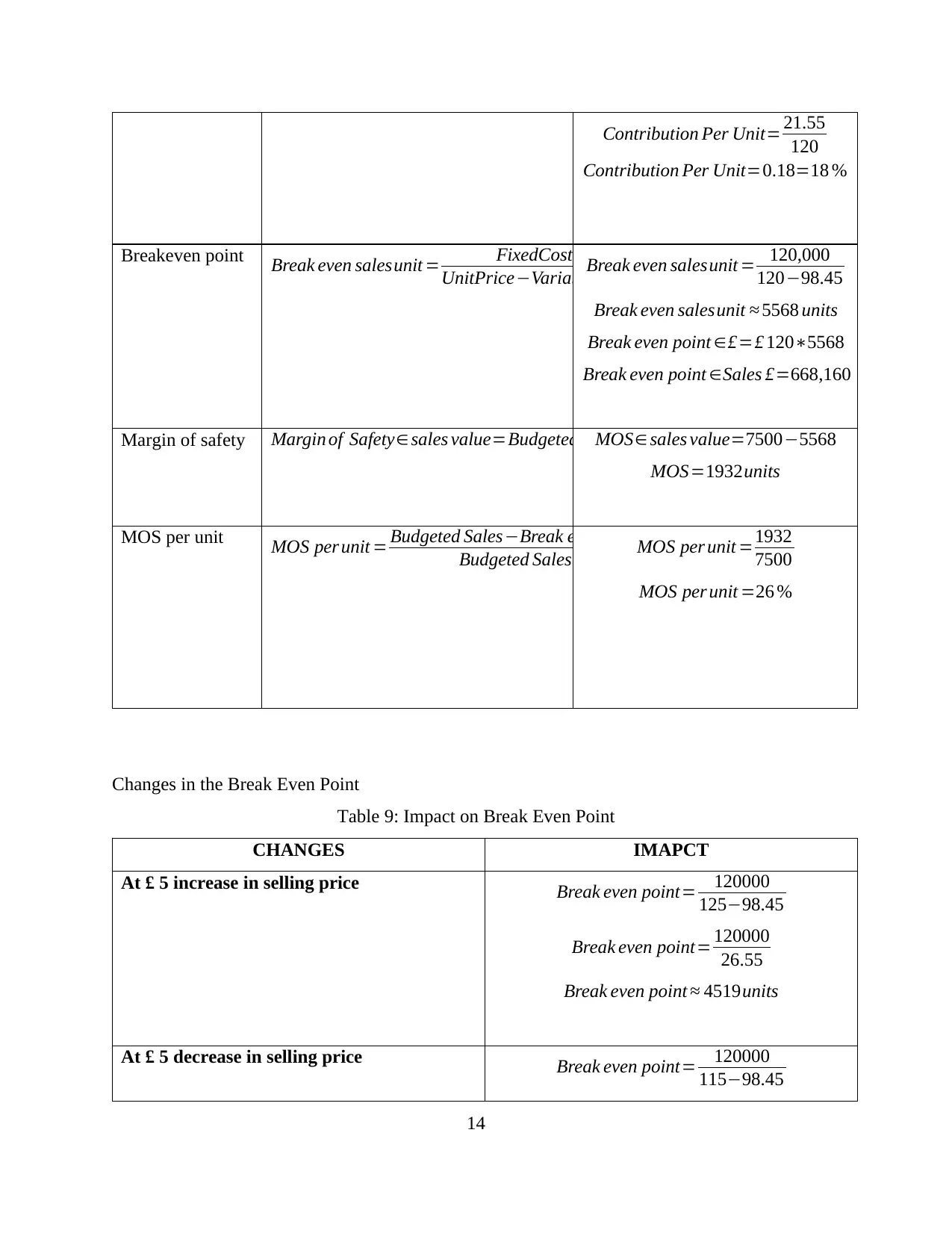

Costing and pricing review

FORMULA CALCULATION

Contribution

Margin Ratio

Contribution per Unit = (Unit

Contribution Margin) / (Unit Price)

Unit CM = Unit Price - Variable cost

per unit

v

ariable cost per unit=52.50+35.75+10.20

Variable cost per unit =£ 98.45

Unit CM =120−98.45

Unit CM =21.55

13

Net Present value 253900

Table 8: NPV calculation for project B

Year Cash flow (£) P.V. factor@ 10% Present Value (£)

1 60000 0.94 56400

2 120000 0.89 106800

3 250000 0.84 210000

4 250000 0.79 197500

Total Present value 570700

Initial investment (450000)

Net Present value 120700

Results - As per the results of NPV technique, ABC ltd should make investment in project A

because its NPV value is higher as compared to project B.

Recommendation

After analysing the results of all the investment appraisal techniques, it is recommended

that ABC should make investment in project A because it is better in terms of revenue, profits

and returns as compared to project B. It has the potential to bring substantial savings and cost

reductions for the company

Costing and pricing review

FORMULA CALCULATION

Contribution

Margin Ratio

Contribution per Unit = (Unit

Contribution Margin) / (Unit Price)

Unit CM = Unit Price - Variable cost

per unit

v

ariable cost per unit=52.50+35.75+10.20

Variable cost per unit =£ 98.45

Unit CM =120−98.45

Unit CM =21.55

13

Contribution Per Unit= 21.55

120

Contribution Per Unit=0.18=18 %

Breakeven point Break even salesunit = FixedCost

UnitPrice−Variable cost

Break even salesunit = 120,000

120−98.45

Break even salesunit ≈ 5568 units

Break even point ∈£=£ 120∗5568

Break even point ∈Sales £=668,160

Margin of safety Margin of Safety∈sales value=Budgeted sales−Break even salesMOS∈ sales value=7500−5568

MOS=1932units

MOS per unit MOS per unit = Budgeted Sales−Break even sales

Budgeted Sales MOS per unit =1932

7500

MOS per unit =26 %

Changes in the Break Even Point

Table 9: Impact on Break Even Point

CHANGES IMAPCT

At £ 5 increase in selling price Break even point= 120000

125−98.45

Break even point= 120000

26.55

Break even point ≈ 4519units

At £ 5 decrease in selling price Break even point= 120000

115−98.45

14

120

Contribution Per Unit=0.18=18 %

Breakeven point Break even salesunit = FixedCost

UnitPrice−Variable cost

Break even salesunit = 120,000

120−98.45

Break even salesunit ≈ 5568 units

Break even point ∈£=£ 120∗5568

Break even point ∈Sales £=668,160

Margin of safety Margin of Safety∈sales value=Budgeted sales−Break even salesMOS∈ sales value=7500−5568

MOS=1932units

MOS per unit MOS per unit = Budgeted Sales−Break even sales

Budgeted Sales MOS per unit =1932

7500

MOS per unit =26 %

Changes in the Break Even Point

Table 9: Impact on Break Even Point

CHANGES IMAPCT

At £ 5 increase in selling price Break even point= 120000

125−98.45

Break even point= 120000

26.55

Break even point ≈ 4519units

At £ 5 decrease in selling price Break even point= 120000

115−98.45

14

Break even point ≈ 7250 units

A ₤5,000 increase in fixed costs Break even point= 125000

120−98.45

Break even point= 125000

21.55

Break even point ≈ 5800 units

A ₤5,000 decrease in fixed costs Break even point= 115000

120−98.45

Break even point= 115000

21.55

Break even point ≈ 5336 units

₤5 increase in material or labour costs per

unit

Break even point= 125000

120−103.45

Break even point= 125000

16.55

Break even point=7553 units

₤5 decrease in material or labour costs per

unit

reak even point= 125000

120−93.45

Break even point= 125000

26.55

Break even point=4708units

Machine A

Contribution Per Unit 18%

Break Even Sales unit 5568 units

Break even in £ £668,160

Margin of Safety (sales value) 1932 units

15

A ₤5,000 increase in fixed costs Break even point= 125000

120−98.45

Break even point= 125000

21.55

Break even point ≈ 5800 units

A ₤5,000 decrease in fixed costs Break even point= 115000

120−98.45

Break even point= 115000

21.55

Break even point ≈ 5336 units

₤5 increase in material or labour costs per

unit

Break even point= 125000

120−103.45

Break even point= 125000

16.55

Break even point=7553 units

₤5 decrease in material or labour costs per

unit

reak even point= 125000

120−93.45

Break even point= 125000

26.55

Break even point=4708units

Machine A

Contribution Per Unit 18%

Break Even Sales unit 5568 units

Break even in £ £668,160

Margin of Safety (sales value) 1932 units

15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Margin of Safety per unit 26%

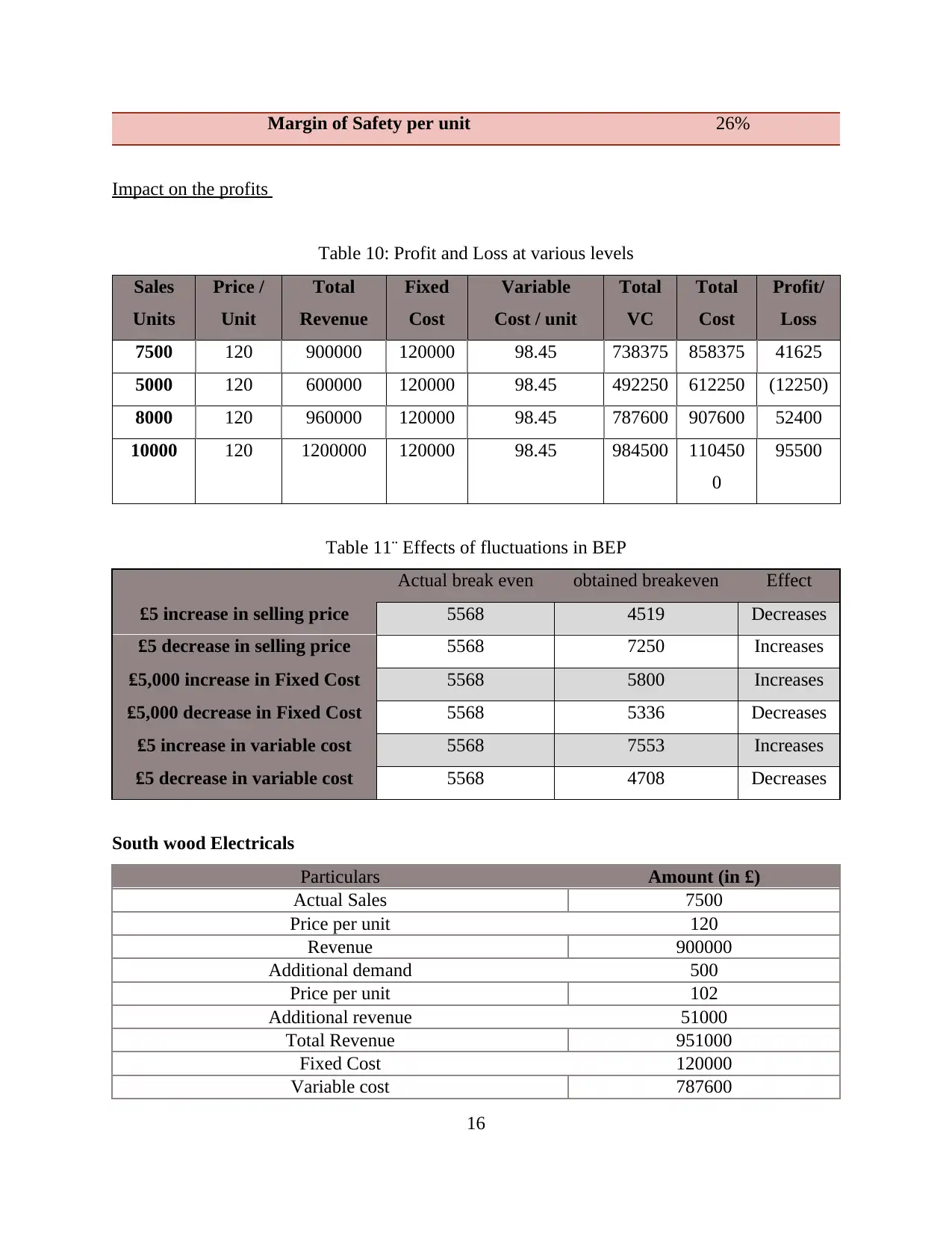

Impact on the profits

Table 10: Profit and Loss at various levels

Sales

Units

Price /

Unit

Total

Revenue

Fixed

Cost

Variable

Cost / unit

Total

VC

Total

Cost

Profit/

Loss

7500 120 900000 120000 98.45 738375 858375 41625

5000 120 600000 120000 98.45 492250 612250 (12250)

8000 120 960000 120000 98.45 787600 907600 52400

10000 120 1200000 120000 98.45 984500 110450

0

95500

Table 11¨ Effects of fluctuations in BEP

Actual break even obtained breakeven Effect

£5 increase in selling price 5568 4519 Decreases

£5 decrease in selling price 5568 7250 Increases

₤5,000 increase in Fixed Cost 5568 5800 Increases

₤5,000 decrease in Fixed Cost 5568 5336 Decreases

₤5 increase in variable cost 5568 7553 Increases

₤5 decrease in variable cost 5568 4708 Decreases

South wood Electricals

Particulars Amount (in £)

Actual Sales 7500

Price per unit 120

Revenue 900000

Additional demand 500

Price per unit 102

Additional revenue 51000

Total Revenue 951000

Fixed Cost 120000

Variable cost 787600

16

Impact on the profits

Table 10: Profit and Loss at various levels

Sales

Units

Price /

Unit

Total

Revenue

Fixed

Cost

Variable

Cost / unit

Total

VC

Total

Cost

Profit/

Loss

7500 120 900000 120000 98.45 738375 858375 41625

5000 120 600000 120000 98.45 492250 612250 (12250)

8000 120 960000 120000 98.45 787600 907600 52400

10000 120 1200000 120000 98.45 984500 110450

0

95500

Table 11¨ Effects of fluctuations in BEP

Actual break even obtained breakeven Effect

£5 increase in selling price 5568 4519 Decreases

£5 decrease in selling price 5568 7250 Increases

₤5,000 increase in Fixed Cost 5568 5800 Increases

₤5,000 decrease in Fixed Cost 5568 5336 Decreases

₤5 increase in variable cost 5568 7553 Increases

₤5 decrease in variable cost 5568 4708 Decreases

South wood Electricals

Particulars Amount (in £)

Actual Sales 7500

Price per unit 120

Revenue 900000

Additional demand 500

Price per unit 102

Additional revenue 51000

Total Revenue 951000

Fixed Cost 120000

Variable cost 787600

16

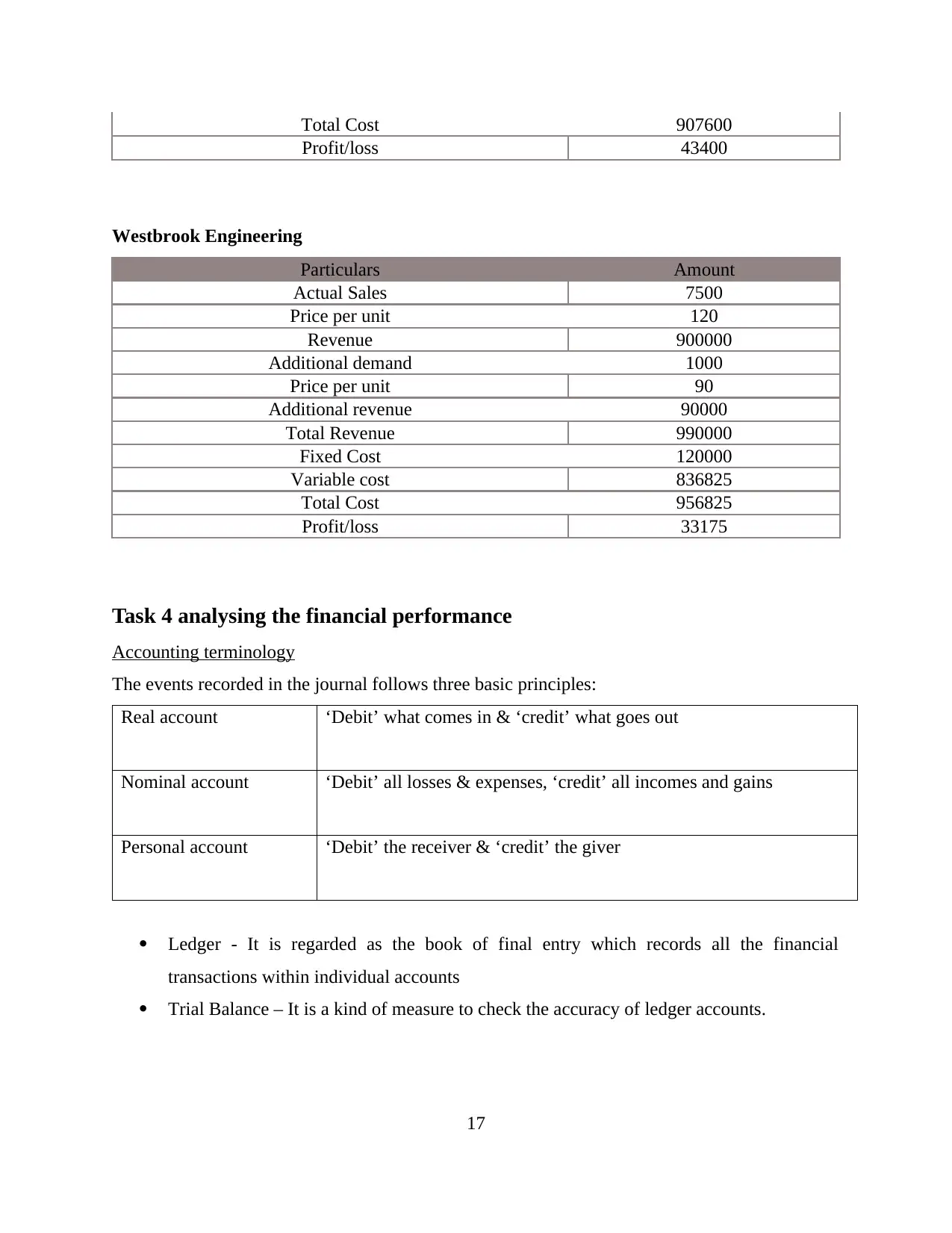

Total Cost 907600

Profit/loss 43400

Westbrook Engineering

Particulars Amount

Actual Sales 7500

Price per unit 120

Revenue 900000

Additional demand 1000

Price per unit 90

Additional revenue 90000

Total Revenue 990000

Fixed Cost 120000

Variable cost 836825

Total Cost 956825

Profit/loss 33175

Task 4 analysing the financial performance

Accounting terminology

The events recorded in the journal follows three basic principles:

Real account ‘Debit’ what comes in & ‘credit’ what goes out

Nominal account ‘Debit’ all losses & expenses, ‘credit’ all incomes and gains

Personal account ‘Debit’ the receiver & ‘credit’ the giver

Ledger - It is regarded as the book of final entry which records all the financial

transactions within individual accounts

Trial Balance – It is a kind of measure to check the accuracy of ledger accounts.

17

Profit/loss 43400

Westbrook Engineering

Particulars Amount

Actual Sales 7500

Price per unit 120

Revenue 900000

Additional demand 1000

Price per unit 90

Additional revenue 90000

Total Revenue 990000

Fixed Cost 120000

Variable cost 836825

Total Cost 956825

Profit/loss 33175

Task 4 analysing the financial performance

Accounting terminology

The events recorded in the journal follows three basic principles:

Real account ‘Debit’ what comes in & ‘credit’ what goes out

Nominal account ‘Debit’ all losses & expenses, ‘credit’ all incomes and gains

Personal account ‘Debit’ the receiver & ‘credit’ the giver

Ledger - It is regarded as the book of final entry which records all the financial

transactions within individual accounts

Trial Balance – It is a kind of measure to check the accuracy of ledger accounts.

17

Evaluation of Ratios

Ratios Formula 1995 1996

Liquidity Ratios

Current Ratio Current Assets

Current Liabilities

20000

6000 = 3.33 54000

25000 =2.16

Quick Ratio Current asset−Cl . stock

Current Liabilities

20000−7000

6000 =2.17 54000−18000

25000 =1.44

Activity Ratios

Fixed assets

turnover Ratio

Net Sales

¿ Assets

120000

15000 =8 200000

12000 =16.67

Total assets

turnover Ratio

Net Sales

Total Assets

120000

35000 =3.43 200000

66000 =3.03

Profitability Ratios

Gross Profit Ratio Gross Profit

Net Sales ∗100 40000

120000∗100=33.33 % 50000

200000∗100=25 %

Net Profit Ratio Net Profit

Net Sales ∗100 30000

120000∗100=25 % 35000

200000∗100=17.5 %

Evaluation

The above calculation of ratios indicates that firm should focus on improving its liquidity

position. The short term obligations of the business are to be fulfilled in effective manner. In

terms of activity, company is doing an excellent work as both the ratios are fine ( Financial ratio

and Analysis. 2013). In terms of profitability, there is a need to focus on improving the

operational affair within the business.

Conclusion

From the above study it can be concluded that finance is the backbone of the business.

Financial management is needed to make sure that investment decisions are taken in appropriate

18

Ratios Formula 1995 1996

Liquidity Ratios

Current Ratio Current Assets

Current Liabilities

20000

6000 = 3.33 54000

25000 =2.16

Quick Ratio Current asset−Cl . stock

Current Liabilities

20000−7000

6000 =2.17 54000−18000

25000 =1.44

Activity Ratios

Fixed assets

turnover Ratio

Net Sales

¿ Assets

120000

15000 =8 200000

12000 =16.67

Total assets

turnover Ratio

Net Sales

Total Assets

120000

35000 =3.43 200000

66000 =3.03

Profitability Ratios

Gross Profit Ratio Gross Profit

Net Sales ∗100 40000

120000∗100=33.33 % 50000

200000∗100=25 %

Net Profit Ratio Net Profit

Net Sales ∗100 30000

120000∗100=25 % 35000

200000∗100=17.5 %

Evaluation

The above calculation of ratios indicates that firm should focus on improving its liquidity

position. The short term obligations of the business are to be fulfilled in effective manner. In

terms of activity, company is doing an excellent work as both the ratios are fine ( Financial ratio

and Analysis. 2013). In terms of profitability, there is a need to focus on improving the

operational affair within the business.

Conclusion

From the above study it can be concluded that finance is the backbone of the business.

Financial management is needed to make sure that investment decisions are taken in appropriate

18

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

manner. Ratio analysis is an effective approach to measure financial performance despite of

having so many drawbacks.

19

having so many drawbacks.

19

References

Books and journals

Abraham, A., Deo, H. and Irvine, H., 2008. What lies beneath? Financial reporting and corporate

governance in Australian banks. Asian Review of Accounting. 16(1). pp. 4 – 20.

Ball, R., Jayaraman, S. and Shivakumar, L., 2012. Audited financial reporting and voluntary

disclosure as complements: A test of the confirmation hypothesis. Journal of Accounting

and Economics. 53(1). pp. 136-166

Bhowmik, K. S. and Saha, D., 2013. Sources of Finance. Financial Institution of the

Marginalized India Studies in Business and Economics. pp61-71.

Bonaci, G. C., Matiş, D. and Strouhal, J., 2008. Financial reporting paradigms for financial

instruments: Empirical study on the Czech and Romanian regulations. Journal of

International Trade Law and Policy. 7(2). pp. 101 – 122.

Bonaci, G. C., Matiş, D. and Strouhal, J., 2008. Financial reporting paradigms for financial

instruments: Empirical study on the Czech and Romanian regulations. Journal of

International Trade Law and Policy. 7(2). pp. 101 – 122.

Booker, J., 2006. Financial Planning Fundamentals. CCH Canadian Limited.

Broadbent, M. and Cullen, J., 2012. Managing Financial Resources. Routledge.

Goldman, C. and Carrier, J., 2010. Joint Financing in the New NHS: Thinking to the Future.

Journal of Integrated Care.18(6).pp.27 – 34.

Hawawini, G. and Viallet, C. 2010. Finance for Executives: Managing for Value Creation, South-

Western; 4th Revised edition

Ittelson, R. T., 2009. Financial Statements: A Step-by-Step Guide to Understanding and

Creating Financial Reports. Career Press.

Joseph, C., 2013. Advanced Credit Risk Analysis and Management. John Wiley & Sons.

20

Books and journals

Abraham, A., Deo, H. and Irvine, H., 2008. What lies beneath? Financial reporting and corporate

governance in Australian banks. Asian Review of Accounting. 16(1). pp. 4 – 20.

Ball, R., Jayaraman, S. and Shivakumar, L., 2012. Audited financial reporting and voluntary

disclosure as complements: A test of the confirmation hypothesis. Journal of Accounting

and Economics. 53(1). pp. 136-166

Bhowmik, K. S. and Saha, D., 2013. Sources of Finance. Financial Institution of the

Marginalized India Studies in Business and Economics. pp61-71.

Bonaci, G. C., Matiş, D. and Strouhal, J., 2008. Financial reporting paradigms for financial

instruments: Empirical study on the Czech and Romanian regulations. Journal of

International Trade Law and Policy. 7(2). pp. 101 – 122.

Bonaci, G. C., Matiş, D. and Strouhal, J., 2008. Financial reporting paradigms for financial

instruments: Empirical study on the Czech and Romanian regulations. Journal of

International Trade Law and Policy. 7(2). pp. 101 – 122.

Booker, J., 2006. Financial Planning Fundamentals. CCH Canadian Limited.

Broadbent, M. and Cullen, J., 2012. Managing Financial Resources. Routledge.

Goldman, C. and Carrier, J., 2010. Joint Financing in the New NHS: Thinking to the Future.

Journal of Integrated Care.18(6).pp.27 – 34.

Hawawini, G. and Viallet, C. 2010. Finance for Executives: Managing for Value Creation, South-

Western; 4th Revised edition

Ittelson, R. T., 2009. Financial Statements: A Step-by-Step Guide to Understanding and

Creating Financial Reports. Career Press.

Joseph, C., 2013. Advanced Credit Risk Analysis and Management. John Wiley & Sons.

20

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.