Harvard Square Inc. Case: Managerial Accounting & Costing Methods

VerifiedAdded on 2023/04/19

|10

|1859

|185

Case Study

AI Summary

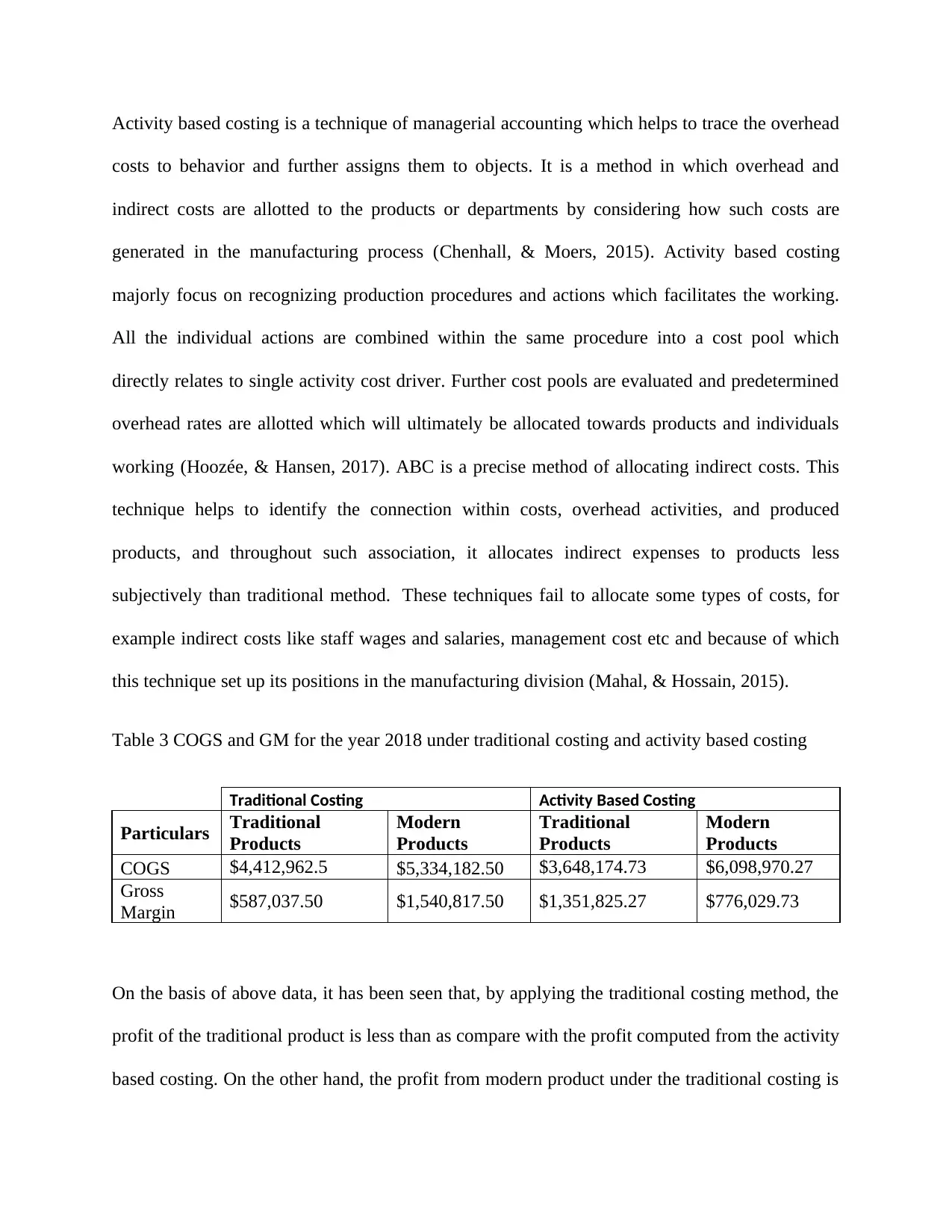

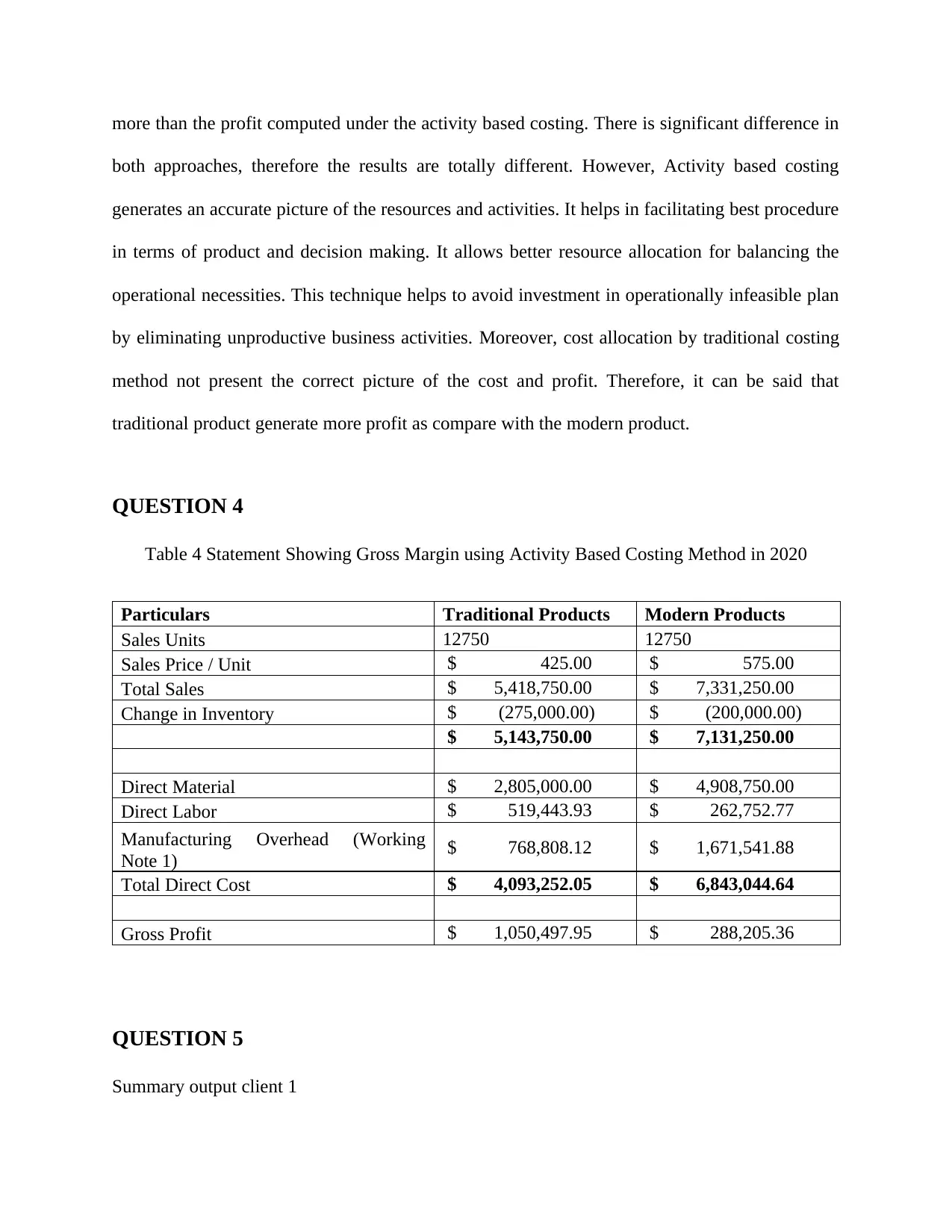

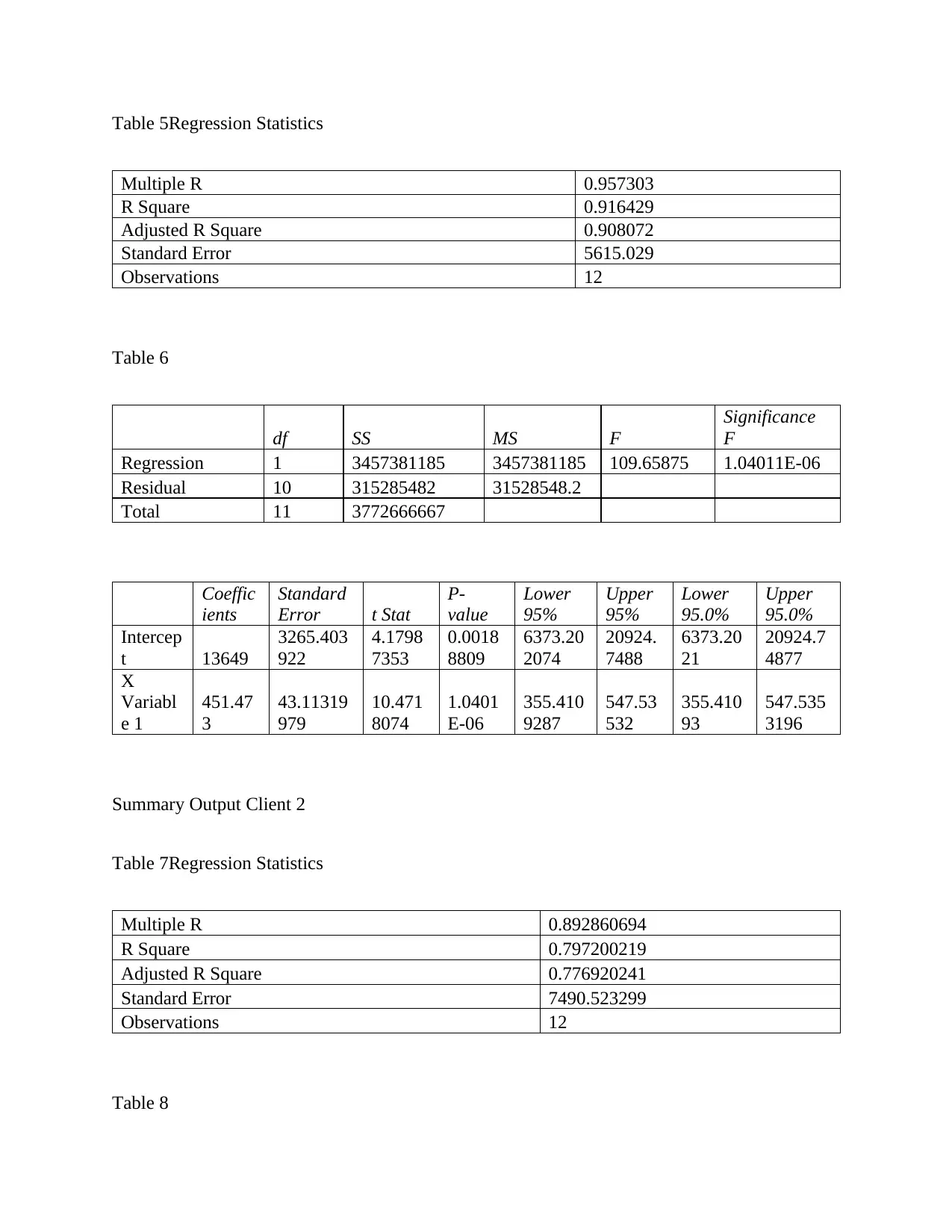

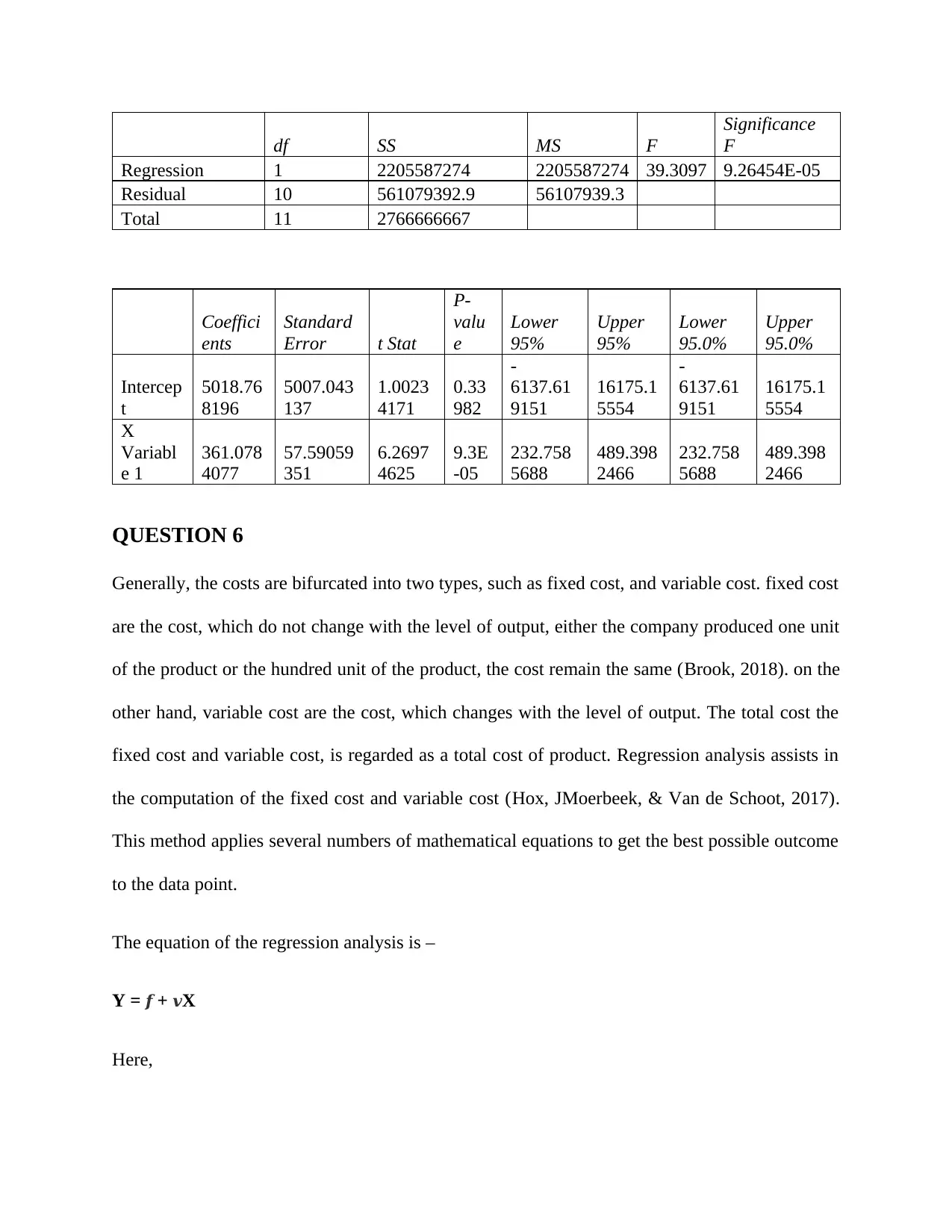

This assignment presents a comprehensive case study focusing on managerial accounting principles, specifically comparing traditional costing and activity-based costing (ABC) methods. The analysis revolves around Harvard Square Inc., a manufacturing company with Traditional and Modern product lines. The assignment includes calculating gross margins under both costing methods, analyzing the differences in profitability, and performing a regression analysis to determine fixed and variable costs. The study further extends to forecasting gross margins for 2020 using ABC. It also interprets regression outputs for two clients, emphasizing the significance of R-squared in assessing cost variances. The document concludes by highlighting the usefulness of regression analysis in bifurcating fixed and variable costs. Desklib offers this solution along with other study resources for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.