Microeconomic Theories

Explain the concept of opportunity cost and analyze the effect of certain events on the market for beef using demand and supply analysis.

10 Pages1703 Words328 Views

Added on 2022-11-14

About This Document

This document discusses opportunity cost, normal goods, supply and demand for beef and heroin, price ceiling, and loss-minimizing quantity in microeconomics.

Microeconomic Theories

Explain the concept of opportunity cost and analyze the effect of certain events on the market for beef using demand and supply analysis.

Added on 2022-11-14

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Economic Analysis and Strategies

|16

|2042

|205

Opportunity Cost, Demand and Supply

|11

|1437

|197

Opportunity Cost, Demand and Supply

|11

|1451

|73

Economics: Opportunity Cost, Beef Market, Heroin Supply, Maximum Price, Firm Shutdown

|12

|1172

|123

Economic Principle

|10

|1500

|99

Business Economics Assignment Report

|10

|1616

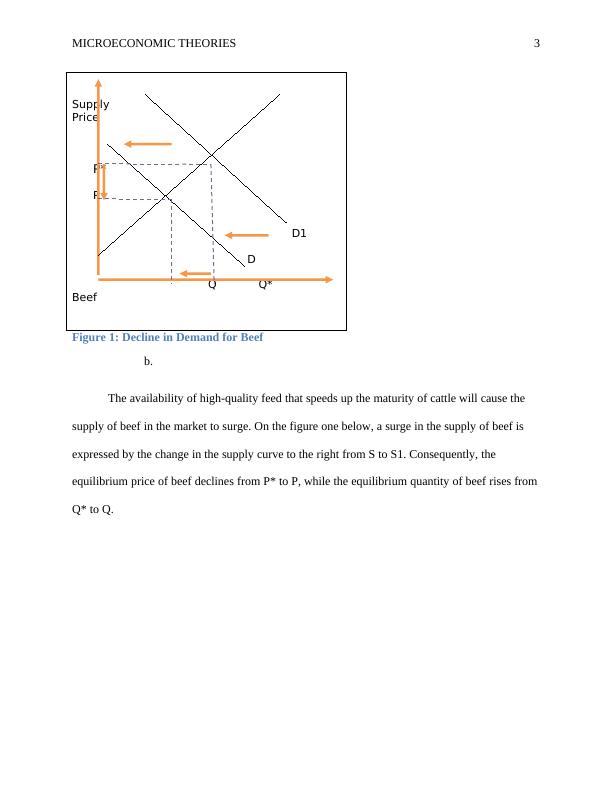

|20