Microeconomics Assignment: Football Production and Market Analysis

VerifiedAdded on 2022/08/09

|9

|931

|18

Homework Assignment

AI Summary

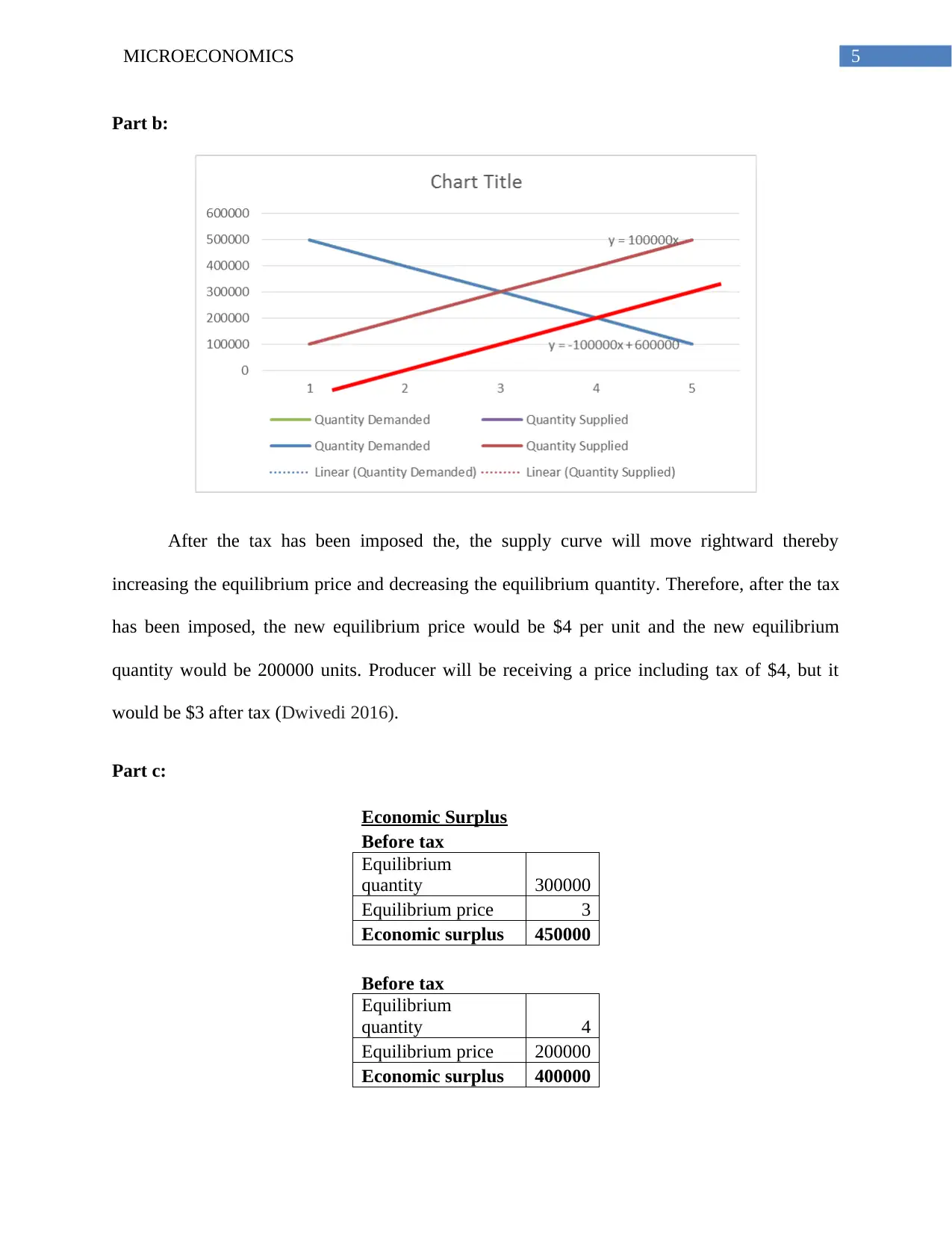

This microeconomics assignment presents a comprehensive analysis of various economic concepts. Question 1 delves into the production of souvenir footballs, calculating total, marginal, and average product, along with costs such as wages, fixed costs, variable costs, and marginal costs. Question 2 examines market equilibrium, supply and demand, and the impact of taxation, including the calculation of economic surplus and deadweight loss. Question 3 explores the effects of reducing marginal tax rates on tax collection and savings. Finally, Question 4 analyzes oil price fluctuations in the global market, considering supply and demand dynamics. The assignment incorporates relevant economic concepts and provides detailed calculations and explanations to enhance understanding.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.