Microeconomics Assignment on Market Equilibrium and Firm Behavior

VerifiedAdded on 2023/06/08

|17

|1791

|432

Homework Assignment

AI Summary

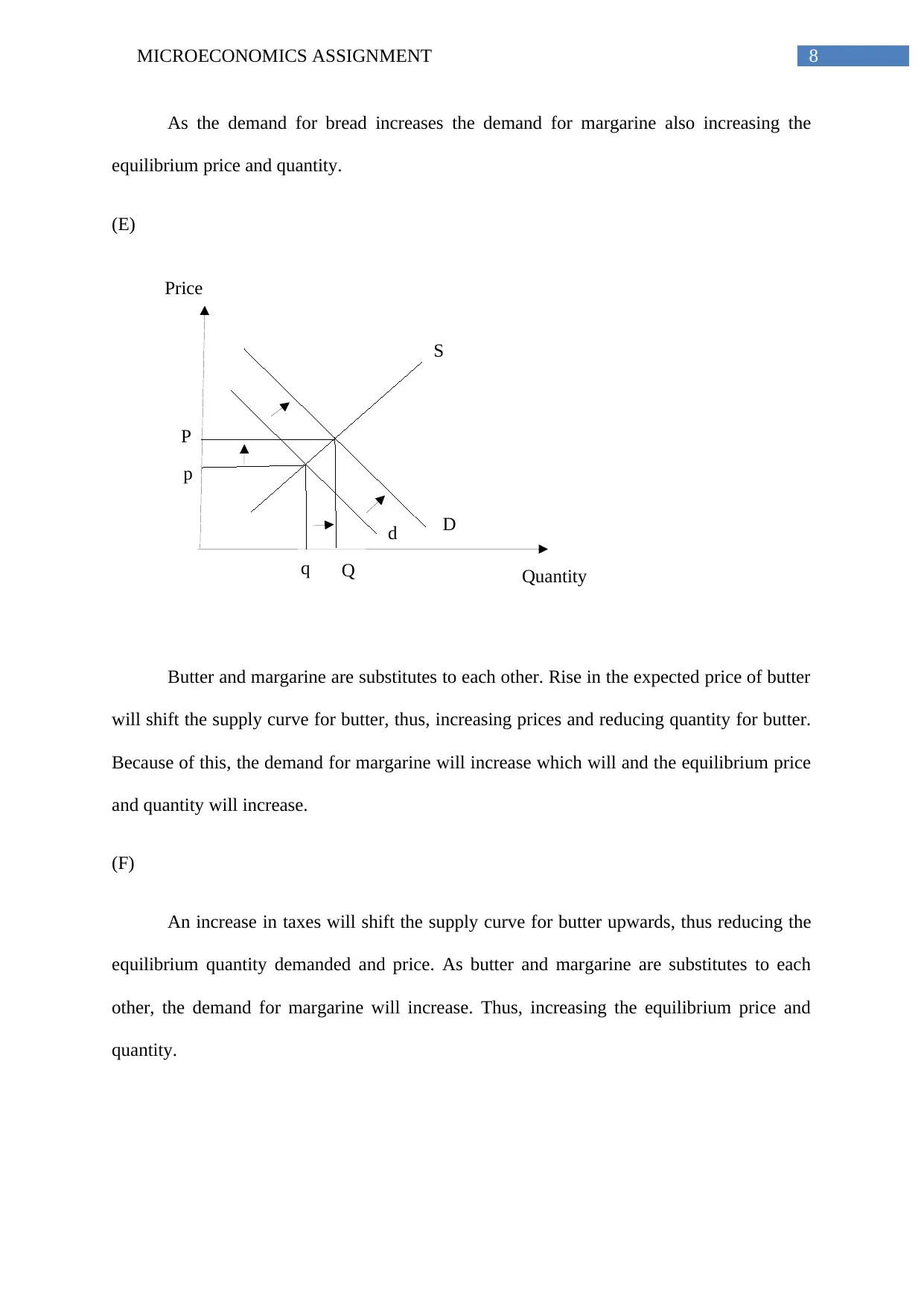

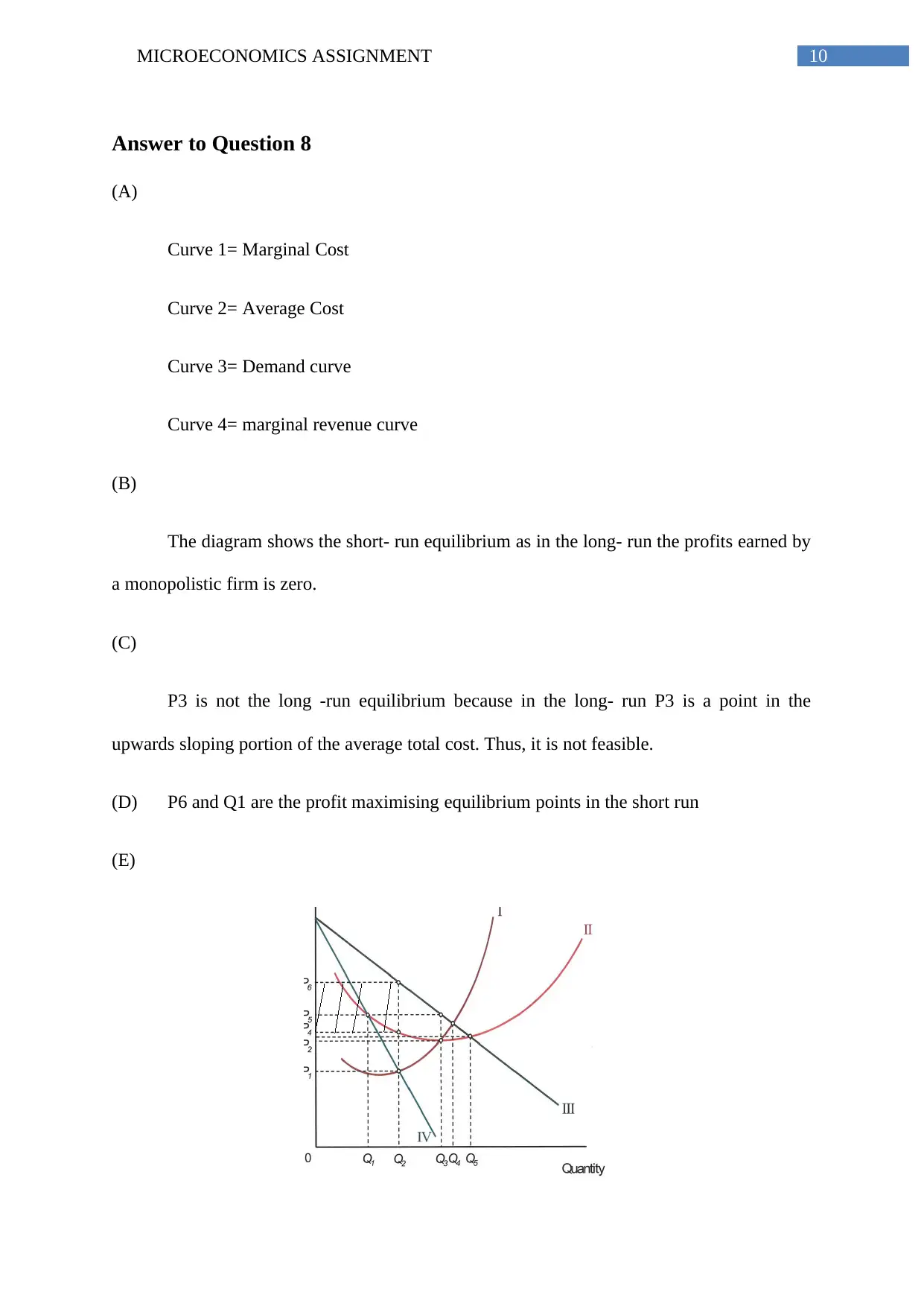

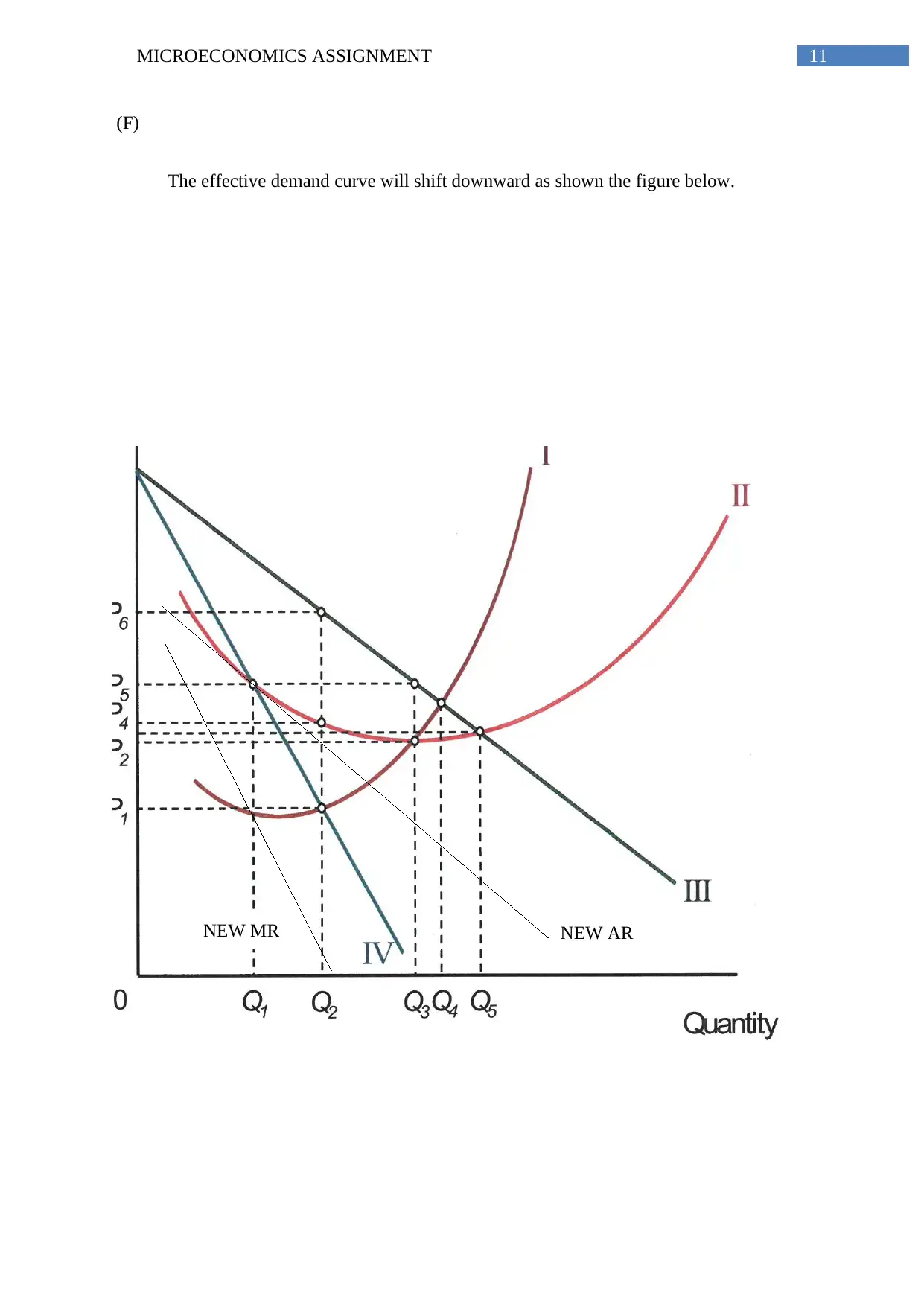

This microeconomics assignment explores various concepts including firm behavior in different market structures, the impact of shifts in supply and demand on market equilibrium, and the characteristics of public goods. The assignment analyzes cost curves, profit maximization strategies for firms in both perfect and imperfect competition, and the effects of increasing, decreasing, and constant cost industries on long-run supply. It also examines how changes in the prices of related goods (substitutes and complements) affect the equilibrium price and quantity in the margarine market. Furthermore, the assignment discusses the short-run equilibrium of a monopolistic firm and the impact of substitute availability on its demand curve. Finally, it analyzes the effects of oil price changes on related markets like automobiles, home insulation, and tires, and explains why public goods are typically provided by the government rather than private firms, highlighting the challenges of privatization and the importance of marginal benefit equaling marginal cost for efficient provision. Desklib provides this solution and many other resources to aid students in their studies.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.