SIT718 Real World Analytics: Downer EDI Share Price Analysis Report

VerifiedAdded on 2022/10/10

|8

|1488

|25

Report

AI Summary

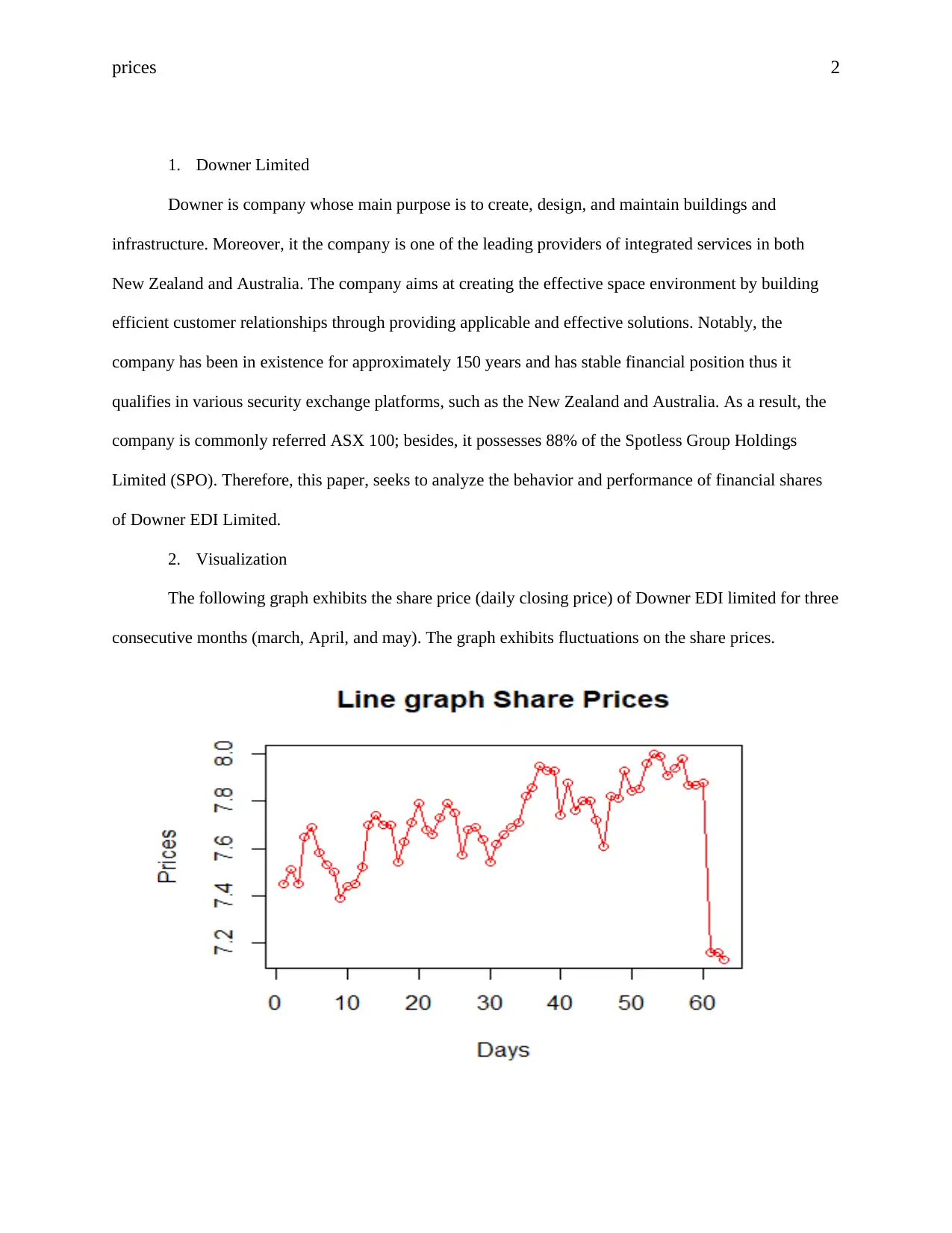

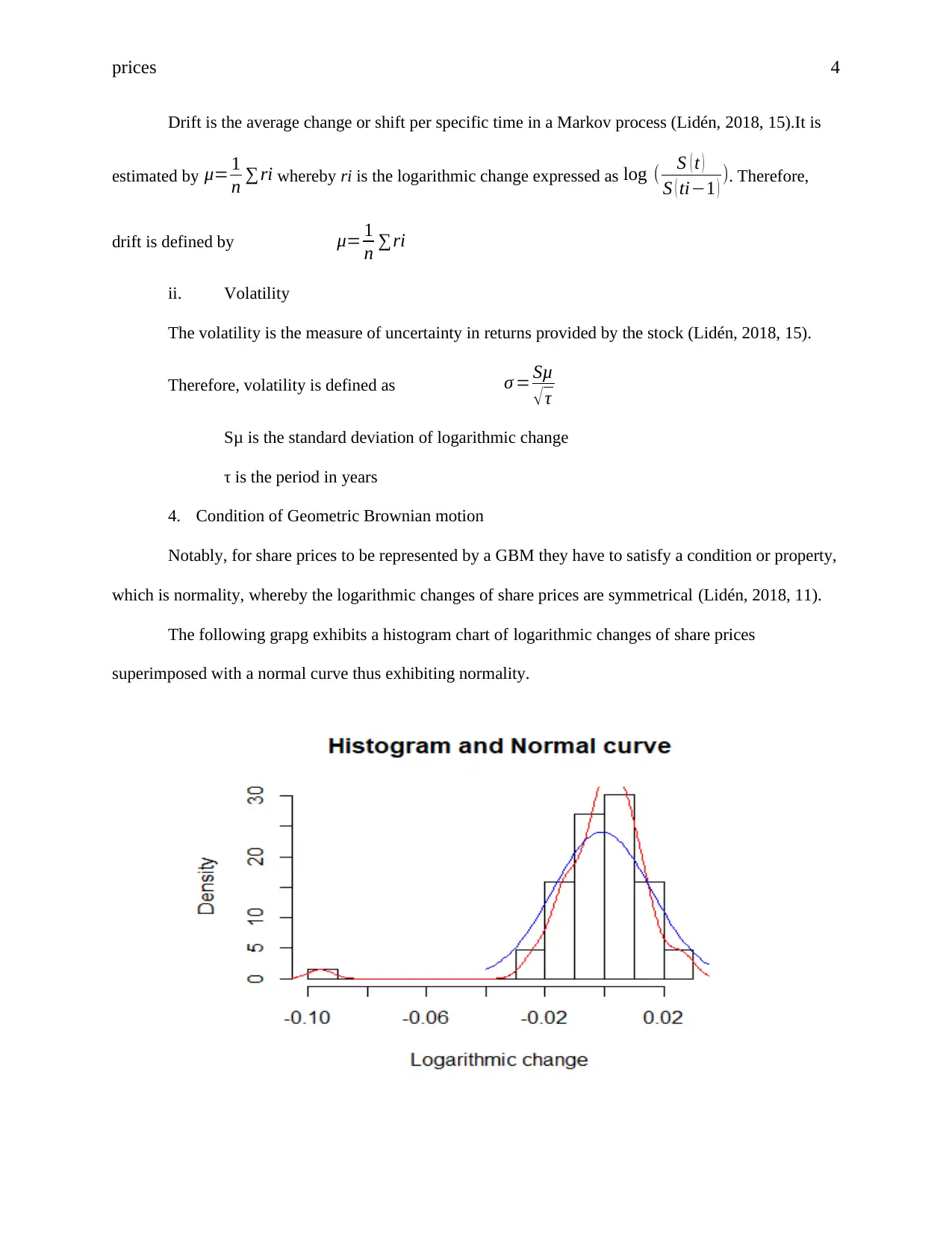

This report analyzes the share price behavior of Downer EDI Limited using historical data from March, April, and May. The analysis employs the Geometric Brownian Motion (GBM) model, calculating drift and volatility to predict future share prices. The report presents the visualizations of the data, detailing the fluctuations in share prices and the application of GBM. The study calculates drift and volatility for different time intervals (three months and the last month), demonstrating how these parameters change and affect the model's predictive accuracy. The report includes an R code for the analysis and concludes by comparing the model's predictions with the actual published share prices, highlighting discrepancies due to factors like new information and financial liabilities, as evident from Downer's debt and liabilities data. The report also references Simply Wall to explain the impact of debt on business.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.