Financial Performance Analysis of Metro Bank: A Comprehensive Report

VerifiedAdded on 2023/01/11

|13

|3298

|96

Report

AI Summary

This report presents a comprehensive financial analysis of Metro Bank, a commercial financial intermediary listed on the London Stock Exchange. It begins with an introduction to modern banking and the selection of Metro Bank as a case study. The report then delves into the bank's nature, business activities, and income structure, supported by visual aids such as graphs and tables. A critical analysis of Metro Bank's assets and liabilities, along with its income structure, is provided, followed by an evaluation of the bank's performance using ratio analysis (profitability, efficiency, asset quality, and capital adequacy ratios) from 2017 to 2019, a period marked by significant economic changes due to Brexit. The report further assesses the impact of changes in the banking sector, including regulations and Fintech developments, on Metro Bank's performance. Finally, it provides an assessment of the expected future performance of Metro Bank, drawing conclusions based on the analysis.

Modern banking

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Introduction of Metro bank along with its nature and business activities...................................1

Critically analysis of the bank’s assets & liability and income structure that has changed over

the time........................................................................................................................................1

Critically evaluating bank’s performance over the period by using ratio analysis......................3

Critically evaluating the ways in which banking sector changes impacts the Metro bank’s

performance.................................................................................................................................8

Assessment of an expected future performance of Metro bank..................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Introduction of Metro bank along with its nature and business activities...................................1

Critically analysis of the bank’s assets & liability and income structure that has changed over

the time........................................................................................................................................1

Critically evaluating bank’s performance over the period by using ratio analysis......................3

Critically evaluating the ways in which banking sector changes impacts the Metro bank’s

performance.................................................................................................................................8

Assessment of an expected future performance of Metro bank..................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

The concept of modern banking is referred as the banking activities which are conducted

using electronic modes. This banking approach no longer follows the traditional way and is

highly based upon the technology (Begenau and Landvoigt, 2018). The main aim of this report is

to build an understanding regarding traditional and modern financial intermediary theories along

with analysing financial performance of a bank and how it can be managed. For this purpose, a

large scale listed bank has been selected which is the Metro bank. This bank is a commercial

financial intermediary that is listed on the London stock exchange.

In this report, detail information of the selected bank is discussed along with its nature and

business activities. Furthermore, in this report assets and liabilities along with income structure

of Metro bank are also critically analysed that are supported by graphs and tables. The method of

ratio analysis is used for analysing the bank’s performance on the basis of four distinct ratios.

Lastly, in this report an analysis have been made regarding the factors which impact on the

selected bank’s performance.

MAIN BODY

Introduction of Metro bank along with its nature and business activities

Metro bank is a public limited company which operates in United Kingdom. The nature of

this bank is that it is a retail and commercial bank which sells its banking products and services

to earn profit and ensure growth and survival. The headquarters of this bank is in London, United

Kingdom and is operating in total 70 locations. The business activities of Metro bank include

accepting deposits, granting loans and the products of this bank include credit cards, consumer

banking and corporate banking (Annual reports of Metro Bank Plc. 2020).

This bank is a high revenue generating organisation which is listed at London stock

exchange.

Critically analysis of the bank’s assets & liability and income structure that has changed over the

time

Metro Bank is a large scale bank which is currently facing record revenues. The income

structure of this company is analysed below by considering their net sales from previous years.

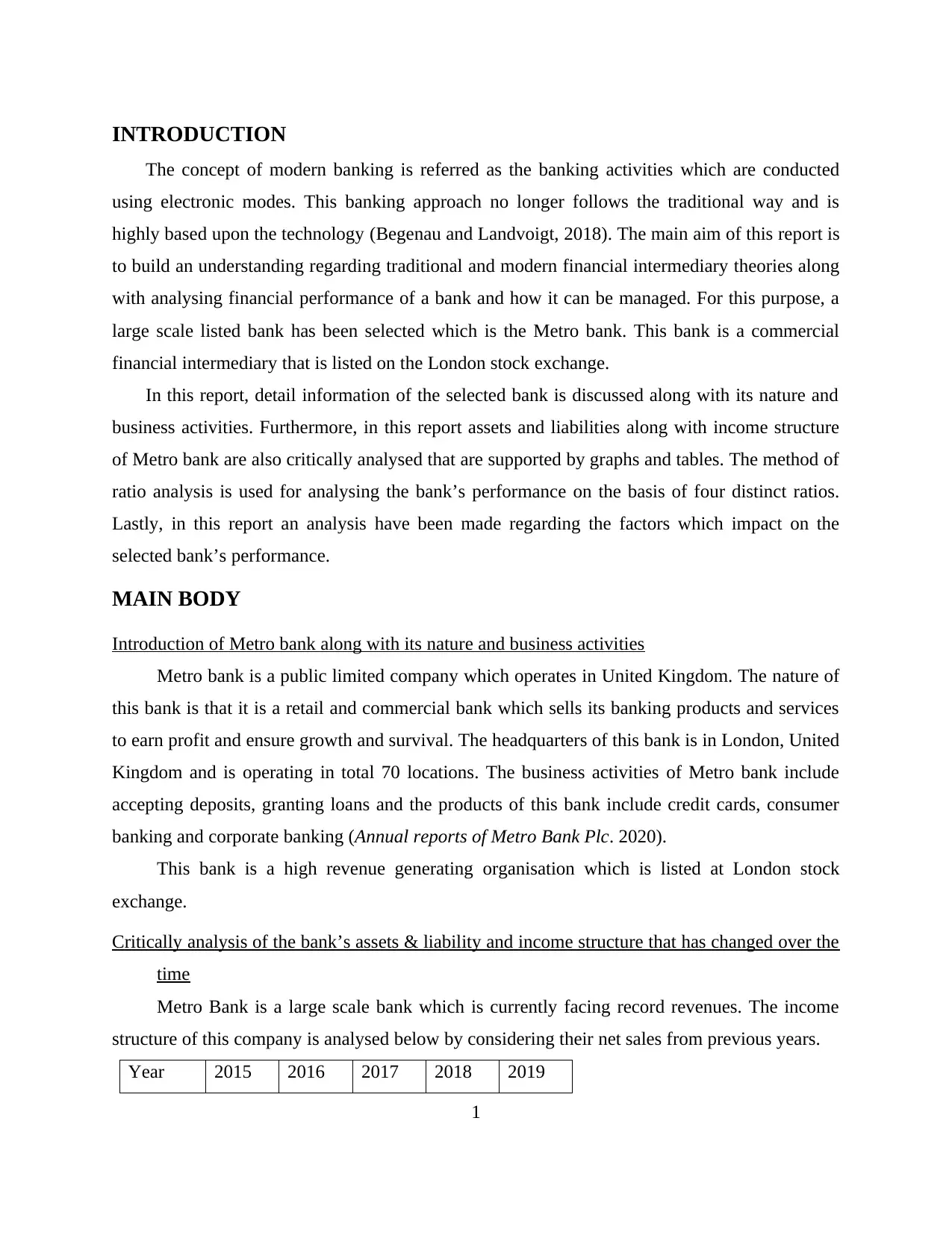

Year 2015 2016 2017 2018 2019

1

The concept of modern banking is referred as the banking activities which are conducted

using electronic modes. This banking approach no longer follows the traditional way and is

highly based upon the technology (Begenau and Landvoigt, 2018). The main aim of this report is

to build an understanding regarding traditional and modern financial intermediary theories along

with analysing financial performance of a bank and how it can be managed. For this purpose, a

large scale listed bank has been selected which is the Metro bank. This bank is a commercial

financial intermediary that is listed on the London stock exchange.

In this report, detail information of the selected bank is discussed along with its nature and

business activities. Furthermore, in this report assets and liabilities along with income structure

of Metro bank are also critically analysed that are supported by graphs and tables. The method of

ratio analysis is used for analysing the bank’s performance on the basis of four distinct ratios.

Lastly, in this report an analysis have been made regarding the factors which impact on the

selected bank’s performance.

MAIN BODY

Introduction of Metro bank along with its nature and business activities

Metro bank is a public limited company which operates in United Kingdom. The nature of

this bank is that it is a retail and commercial bank which sells its banking products and services

to earn profit and ensure growth and survival. The headquarters of this bank is in London, United

Kingdom and is operating in total 70 locations. The business activities of Metro bank include

accepting deposits, granting loans and the products of this bank include credit cards, consumer

banking and corporate banking (Annual reports of Metro Bank Plc. 2020).

This bank is a high revenue generating organisation which is listed at London stock

exchange.

Critically analysis of the bank’s assets & liability and income structure that has changed over the

time

Metro Bank is a large scale bank which is currently facing record revenues. The income

structure of this company is analysed below by considering their net sales from previous years.

Year 2015 2016 2017 2018 2019

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Turnove

r

120.2 195.11 293.7 404.1 415.6

Net

profit

-49.2 -16.75 10.8 27.1 -182.6

The income which Metro Bank plc. has acquired is presented in a graph above which this

company has earned from their sales revenue. It can be seen from above graph that the sales

revenue of this company is continuously increasing every year which implies that this bank is

continuously associating with new clients. The pattern of increasing revenue is not followed by

the net profit of Metro Bank Plc. as the till 2018, the profit of this company was increasing but in

year 2019, Metro Plc. faced immense loss of 182 thousand pounds. The income of Metro Plc. has

changed over time and the biggest reason behind the losses of this company is the BREXIT

impact which declines the income of this company in year 2019.

Assets and liabilities of Metro Bank Plc. are gathered from the annual reports of this

company. This information is presented below using a graph and table.

2019 2018 2017 2016

Total assets 21,400,00

0

21,647,00

0

16,355,35

5

10,057,28

8

Total

liabilities

19,817,00

0

20,244,00

0

15,259,46

6 9,252,753

2

r

120.2 195.11 293.7 404.1 415.6

Net

profit

-49.2 -16.75 10.8 27.1 -182.6

The income which Metro Bank plc. has acquired is presented in a graph above which this

company has earned from their sales revenue. It can be seen from above graph that the sales

revenue of this company is continuously increasing every year which implies that this bank is

continuously associating with new clients. The pattern of increasing revenue is not followed by

the net profit of Metro Bank Plc. as the till 2018, the profit of this company was increasing but in

year 2019, Metro Plc. faced immense loss of 182 thousand pounds. The income of Metro Plc. has

changed over time and the biggest reason behind the losses of this company is the BREXIT

impact which declines the income of this company in year 2019.

Assets and liabilities of Metro Bank Plc. are gathered from the annual reports of this

company. This information is presented below using a graph and table.

2019 2018 2017 2016

Total assets 21,400,00

0

21,647,00

0

16,355,35

5

10,057,28

8

Total

liabilities

19,817,00

0

20,244,00

0

15,259,46

6 9,252,753

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

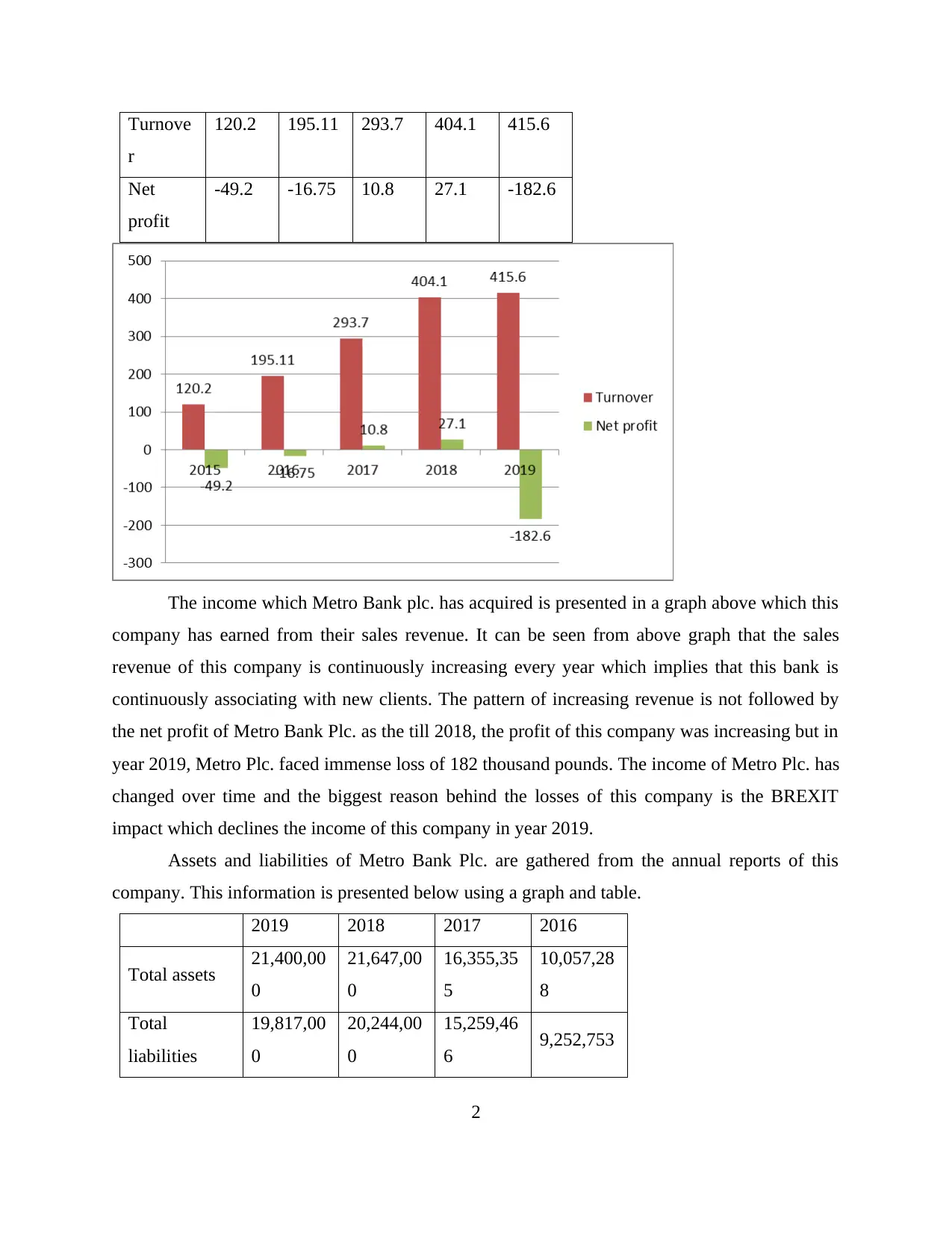

2019 2018 2017 2016

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

Total assets

Total liabilities

From the graphical representation, the trend of Metro Bank Plc.’s assets and liabilities can

be acquired. The total assets of this company are increasing every year due to which it can be

said that the assets of this company are showing increasing trend. On the other hand, total

liabilities of Metro Bank has also changed over time as till 2018, the liabilities of this company

were continuously increasing resulting in appropriate debt equity ratio but in year 2019, the

value of total liabilities decline and resulted in non suitable debt ratio and current ratio.

Critically evaluating bank’s performance over the period by using ratio analysis

It is important to analyse an organisation’s performance in order to identify their position

in market. The best technique or tool to critically analyse the Metro Bank Plc.’s financial

performance is ratio analysis. It must be noted that ratio analysis is a quantitative method that

helps in gaining information regarding company’s profitability, liquidity, solvency and others.

This analysis also helps in the comparative assessment between companies and between years of

the same company. The period of 2017 to 2019 is considered as must crucial for this company

due to commencement and execution of BREXIT; considering this the ratio analysis of these

years will be calculated and critically analysed.

Ratios which are considered for analysing the financial performance of Metro Bank Plc.

are profitability, efficiency, asset quality and capital adequacy ratios. All these ratios are

identified and presented below along with their interpretation for the selected period of 3 years.

Profitability ratios:

3

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

Total assets

Total liabilities

From the graphical representation, the trend of Metro Bank Plc.’s assets and liabilities can

be acquired. The total assets of this company are increasing every year due to which it can be

said that the assets of this company are showing increasing trend. On the other hand, total

liabilities of Metro Bank has also changed over time as till 2018, the liabilities of this company

were continuously increasing resulting in appropriate debt equity ratio but in year 2019, the

value of total liabilities decline and resulted in non suitable debt ratio and current ratio.

Critically evaluating bank’s performance over the period by using ratio analysis

It is important to analyse an organisation’s performance in order to identify their position

in market. The best technique or tool to critically analyse the Metro Bank Plc.’s financial

performance is ratio analysis. It must be noted that ratio analysis is a quantitative method that

helps in gaining information regarding company’s profitability, liquidity, solvency and others.

This analysis also helps in the comparative assessment between companies and between years of

the same company. The period of 2017 to 2019 is considered as must crucial for this company

due to commencement and execution of BREXIT; considering this the ratio analysis of these

years will be calculated and critically analysed.

Ratios which are considered for analysing the financial performance of Metro Bank Plc.

are profitability, efficiency, asset quality and capital adequacy ratios. All these ratios are

identified and presented below along with their interpretation for the selected period of 3 years.

Profitability ratios:

3

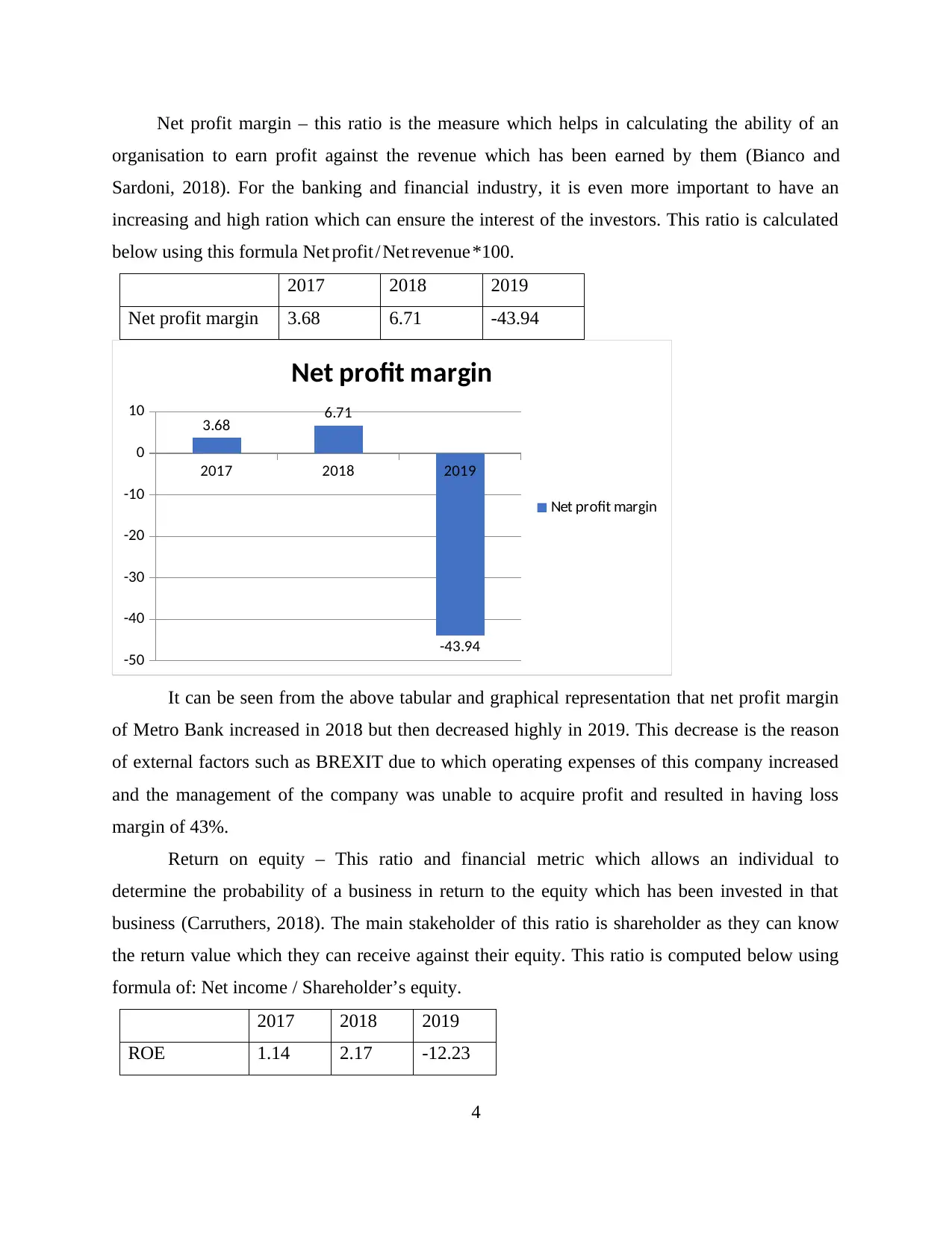

Net profit margin – this ratio is the measure which helps in calculating the ability of an

organisation to earn profit against the revenue which has been earned by them (Bianco and

Sardoni, 2018). For the banking and financial industry, it is even more important to have an

increasing and high ration which can ensure the interest of the investors. This ratio is calculated

below using this formula Net profit / Net revenue *100.

2017 2018 2019

Net profit margin 3.68 6.71 -43.94

2017 2018 2019

-50

-40

-30

-20

-10

0

10 3.68 6.71

-43.94

Net profit margin

Net profit margin

It can be seen from the above tabular and graphical representation that net profit margin

of Metro Bank increased in 2018 but then decreased highly in 2019. This decrease is the reason

of external factors such as BREXIT due to which operating expenses of this company increased

and the management of the company was unable to acquire profit and resulted in having loss

margin of 43%.

Return on equity – This ratio and financial metric which allows an individual to

determine the probability of a business in return to the equity which has been invested in that

business (Carruthers, 2018). The main stakeholder of this ratio is shareholder as they can know

the return value which they can receive against their equity. This ratio is computed below using

formula of: Net income / Shareholder’s equity.

2017 2018 2019

ROE 1.14 2.17 -12.23

4

organisation to earn profit against the revenue which has been earned by them (Bianco and

Sardoni, 2018). For the banking and financial industry, it is even more important to have an

increasing and high ration which can ensure the interest of the investors. This ratio is calculated

below using this formula Net profit / Net revenue *100.

2017 2018 2019

Net profit margin 3.68 6.71 -43.94

2017 2018 2019

-50

-40

-30

-20

-10

0

10 3.68 6.71

-43.94

Net profit margin

Net profit margin

It can be seen from the above tabular and graphical representation that net profit margin

of Metro Bank increased in 2018 but then decreased highly in 2019. This decrease is the reason

of external factors such as BREXIT due to which operating expenses of this company increased

and the management of the company was unable to acquire profit and resulted in having loss

margin of 43%.

Return on equity – This ratio and financial metric which allows an individual to

determine the probability of a business in return to the equity which has been invested in that

business (Carruthers, 2018). The main stakeholder of this ratio is shareholder as they can know

the return value which they can receive against their equity. This ratio is computed below using

formula of: Net income / Shareholder’s equity.

2017 2018 2019

ROE 1.14 2.17 -12.23

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 2018 2019

-14

-12

-10

-8

-6

-4

-2

0

2

4

1.14 2.17

-12.23

ROE

ROE

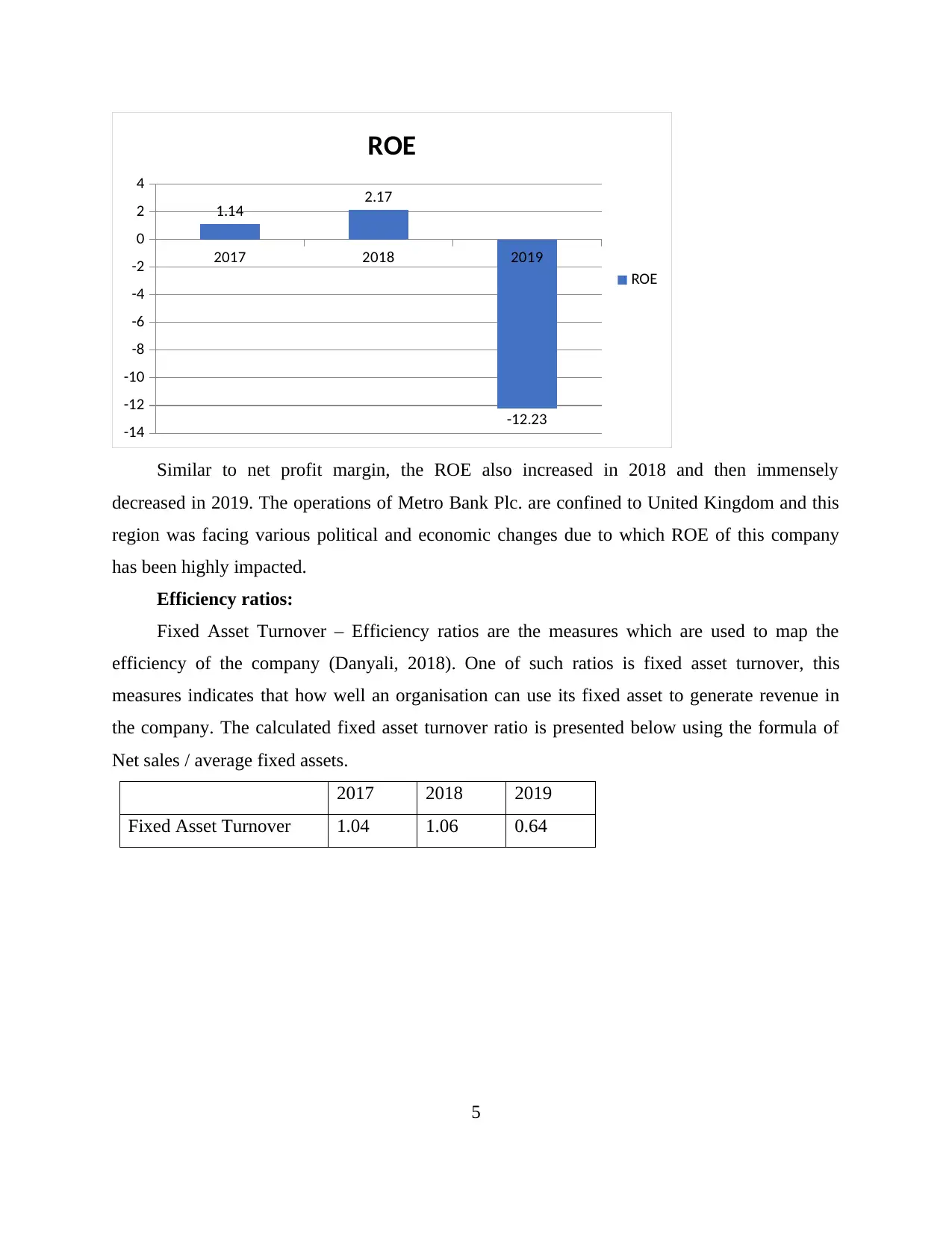

Similar to net profit margin, the ROE also increased in 2018 and then immensely

decreased in 2019. The operations of Metro Bank Plc. are confined to United Kingdom and this

region was facing various political and economic changes due to which ROE of this company

has been highly impacted.

Efficiency ratios:

Fixed Asset Turnover – Efficiency ratios are the measures which are used to map the

efficiency of the company (Danyali, 2018). One of such ratios is fixed asset turnover, this

measures indicates that how well an organisation can use its fixed asset to generate revenue in

the company. The calculated fixed asset turnover ratio is presented below using the formula of

Net sales / average fixed assets.

2017 2018 2019

Fixed Asset Turnover 1.04 1.06 0.64

5

-14

-12

-10

-8

-6

-4

-2

0

2

4

1.14 2.17

-12.23

ROE

ROE

Similar to net profit margin, the ROE also increased in 2018 and then immensely

decreased in 2019. The operations of Metro Bank Plc. are confined to United Kingdom and this

region was facing various political and economic changes due to which ROE of this company

has been highly impacted.

Efficiency ratios:

Fixed Asset Turnover – Efficiency ratios are the measures which are used to map the

efficiency of the company (Danyali, 2018). One of such ratios is fixed asset turnover, this

measures indicates that how well an organisation can use its fixed asset to generate revenue in

the company. The calculated fixed asset turnover ratio is presented below using the formula of

Net sales / average fixed assets.

2017 2018 2019

Fixed Asset Turnover 1.04 1.06 0.64

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 2018 2019

0

0.2

0.4

0.6

0.8

1

1.2

1.04 1.06

0.64

Fixed Asset Turnover

Fixed Asset Turnover

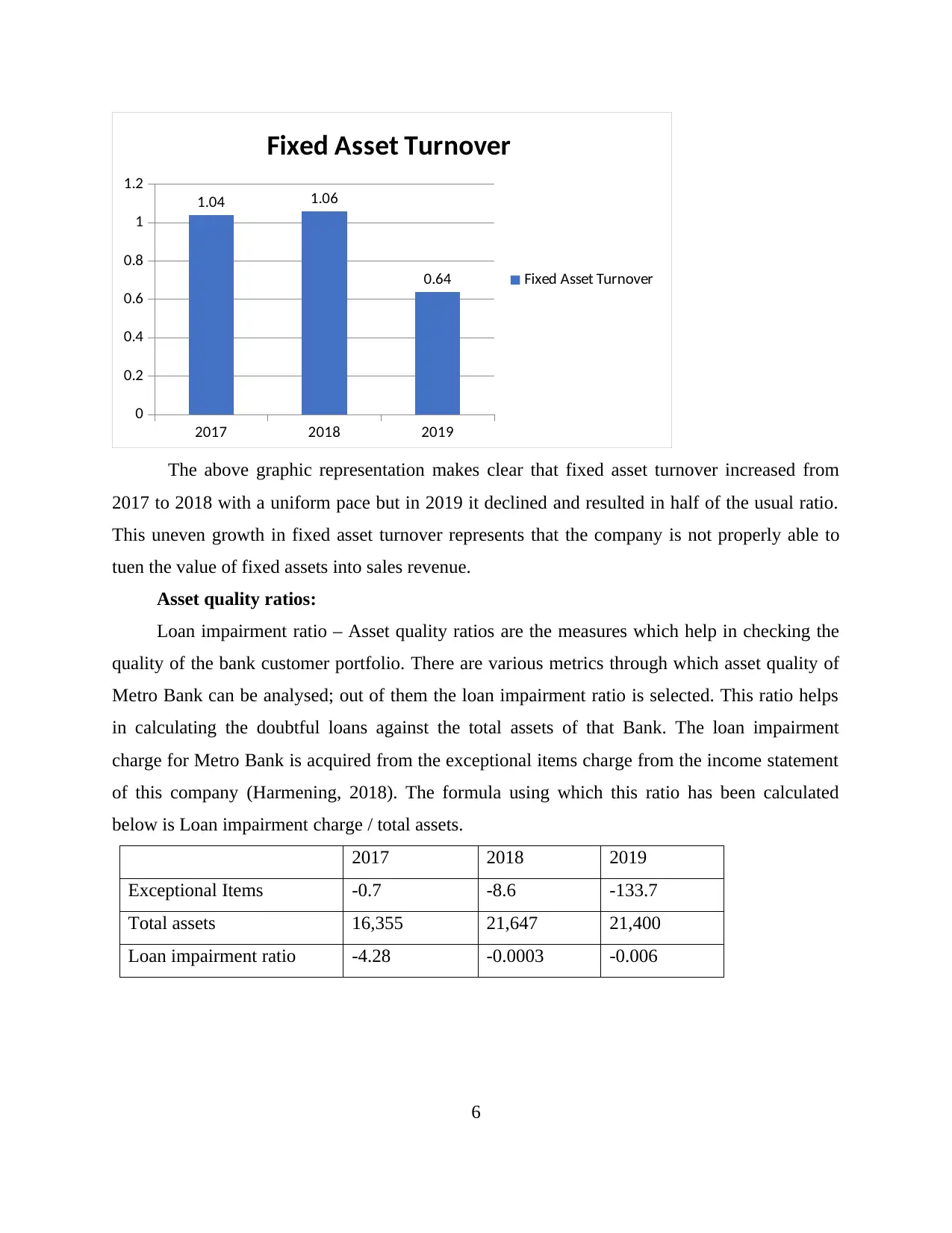

The above graphic representation makes clear that fixed asset turnover increased from

2017 to 2018 with a uniform pace but in 2019 it declined and resulted in half of the usual ratio.

This uneven growth in fixed asset turnover represents that the company is not properly able to

tuen the value of fixed assets into sales revenue.

Asset quality ratios:

Loan impairment ratio – Asset quality ratios are the measures which help in checking the

quality of the bank customer portfolio. There are various metrics through which asset quality of

Metro Bank can be analysed; out of them the loan impairment ratio is selected. This ratio helps

in calculating the doubtful loans against the total assets of that Bank. The loan impairment

charge for Metro Bank is acquired from the exceptional items charge from the income statement

of this company (Harmening, 2018). The formula using which this ratio has been calculated

below is Loan impairment charge / total assets.

2017 2018 2019

Exceptional Items -0.7 -8.6 -133.7

Total assets 16,355 21,647 21,400

Loan impairment ratio -4.28 -0.0003 -0.006

6

0

0.2

0.4

0.6

0.8

1

1.2

1.04 1.06

0.64

Fixed Asset Turnover

Fixed Asset Turnover

The above graphic representation makes clear that fixed asset turnover increased from

2017 to 2018 with a uniform pace but in 2019 it declined and resulted in half of the usual ratio.

This uneven growth in fixed asset turnover represents that the company is not properly able to

tuen the value of fixed assets into sales revenue.

Asset quality ratios:

Loan impairment ratio – Asset quality ratios are the measures which help in checking the

quality of the bank customer portfolio. There are various metrics through which asset quality of

Metro Bank can be analysed; out of them the loan impairment ratio is selected. This ratio helps

in calculating the doubtful loans against the total assets of that Bank. The loan impairment

charge for Metro Bank is acquired from the exceptional items charge from the income statement

of this company (Harmening, 2018). The formula using which this ratio has been calculated

below is Loan impairment charge / total assets.

2017 2018 2019

Exceptional Items -0.7 -8.6 -133.7

Total assets 16,355 21,647 21,400

Loan impairment ratio -4.28 -0.0003 -0.006

6

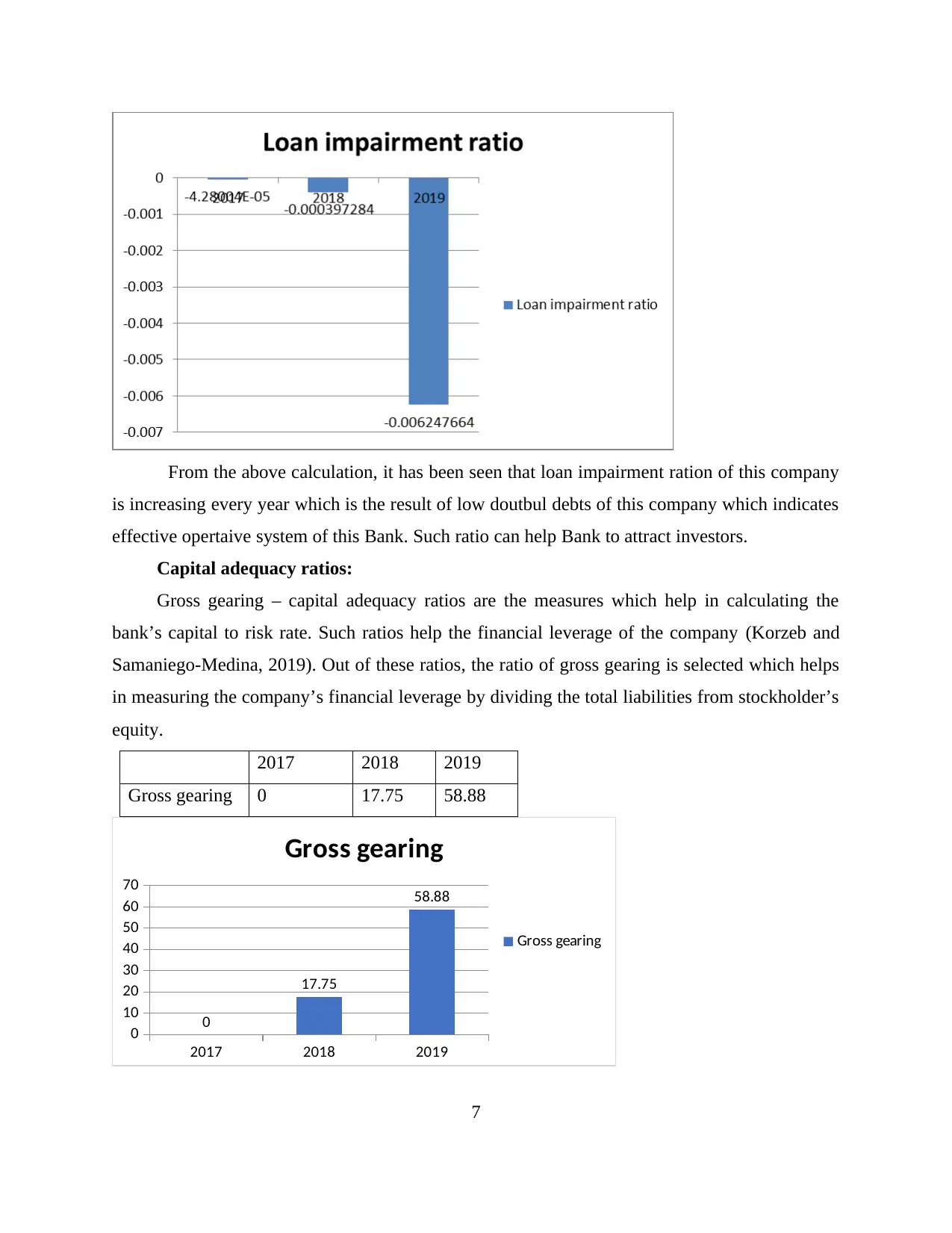

From the above calculation, it has been seen that loan impairment ration of this company

is increasing every year which is the result of low doutbul debts of this company which indicates

effective opertaive system of this Bank. Such ratio can help Bank to attract investors.

Capital adequacy ratios:

Gross gearing – capital adequacy ratios are the measures which help in calculating the

bank’s capital to risk rate. Such ratios help the financial leverage of the company (Korzeb and

Samaniego-Medina, 2019). Out of these ratios, the ratio of gross gearing is selected which helps

in measuring the company’s financial leverage by dividing the total liabilities from stockholder’s

equity.

2017 2018 2019

Gross gearing 0 17.75 58.88

2017 2018 2019

0

10

20

30

40

50

60

70

0

17.75

58.88

Gross gearing

Gross gearing

7

is increasing every year which is the result of low doutbul debts of this company which indicates

effective opertaive system of this Bank. Such ratio can help Bank to attract investors.

Capital adequacy ratios:

Gross gearing – capital adequacy ratios are the measures which help in calculating the

bank’s capital to risk rate. Such ratios help the financial leverage of the company (Korzeb and

Samaniego-Medina, 2019). Out of these ratios, the ratio of gross gearing is selected which helps

in measuring the company’s financial leverage by dividing the total liabilities from stockholder’s

equity.

2017 2018 2019

Gross gearing 0 17.75 58.88

2017 2018 2019

0

10

20

30

40

50

60

70

0

17.75

58.88

Gross gearing

Gross gearing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above analysis, it has been seen that gross greating ratio of this company is

continously increasing which means the company is becoming more able to acquire high equity

and the capital adequacy in this Bank is higher.

From the above overall analysis, it has been clear that besides year 2019, this Bank has

been proven to efectively operating in market by earning relibale revenues and incomes.

Critically evaluating the ways in which banking sector changes impacts the Metro bank’s

performance

Changes in bank regulation:

The banking industry of United kingdom is the collection of all the banking institutions

which operate in the region of UK. All the banking institutions are authorised and regulated by a

central authority which is known as Financial conduct authority. This institution provides certain

guidelines and policies which are mandatory to be followed by every bank. Any change in these

guidelines or regulations influence the operations of banks. Due to Brexit, the banking

regulations in United kingdom changed which impacted every bank including Metro Bank Plc.

On year 2019, FCA changed overdraft regulations due to which banks had to ‘re design their

overdraft products. This change in bank regulation impacted Metro Bank due to liabilities of this

company showed a declining trend which further impacted the debt equity ratio of this company.

Another banking regulation which changed in 2019 was that FCA increased the consumer

protection on banking products. This regulation was amended to control the push payment scams

and protect the interest of vulnerable customers. This change in regulation resulted in changes in

electronic transactions policies due to which Metro Bank faced heavy losses in 2019 (Majid,

2020).

Increase impact of FinTech developments on banking business

Fin tech refers to the financial technology that aims to compete with traditional banking

system in order to provide convince to consumers. Fintech is an emerging industry which a is

continuously developing due to which traditional banking system of United kingdom has be

highly influenced. The sector of Fintech is a collection of organisations that use technology to

provide financial services to their customers. The industry of Fintech is changing the perception

of people and ‘re shaping the financial system of entire world. Like any country, United

8

continously increasing which means the company is becoming more able to acquire high equity

and the capital adequacy in this Bank is higher.

From the above overall analysis, it has been clear that besides year 2019, this Bank has

been proven to efectively operating in market by earning relibale revenues and incomes.

Critically evaluating the ways in which banking sector changes impacts the Metro bank’s

performance

Changes in bank regulation:

The banking industry of United kingdom is the collection of all the banking institutions

which operate in the region of UK. All the banking institutions are authorised and regulated by a

central authority which is known as Financial conduct authority. This institution provides certain

guidelines and policies which are mandatory to be followed by every bank. Any change in these

guidelines or regulations influence the operations of banks. Due to Brexit, the banking

regulations in United kingdom changed which impacted every bank including Metro Bank Plc.

On year 2019, FCA changed overdraft regulations due to which banks had to ‘re design their

overdraft products. This change in bank regulation impacted Metro Bank due to liabilities of this

company showed a declining trend which further impacted the debt equity ratio of this company.

Another banking regulation which changed in 2019 was that FCA increased the consumer

protection on banking products. This regulation was amended to control the push payment scams

and protect the interest of vulnerable customers. This change in regulation resulted in changes in

electronic transactions policies due to which Metro Bank faced heavy losses in 2019 (Majid,

2020).

Increase impact of FinTech developments on banking business

Fin tech refers to the financial technology that aims to compete with traditional banking

system in order to provide convince to consumers. Fintech is an emerging industry which a is

continuously developing due to which traditional banking system of United kingdom has be

highly influenced. The sector of Fintech is a collection of organisations that use technology to

provide financial services to their customers. The industry of Fintech is changing the perception

of people and ‘re shaping the financial system of entire world. Like any country, United

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

kingdom is also influenced by Fintech due to which banking institutions of this region are

influenced adversely.

Due to high innovation in the Fintech projects, the organisations of Fintech is acquiring

success over grabbing attention of investors. Due to innovative products and services, the

investment flow which was usually in the support of Banking institution, is now exploring their

portfolio and investing fintech organisation, due to which it is hard for banking organisations like

Metro Bank to operate in absence of adequate capital. As analysed in ratio analysis, a major

reason for Metro Bank to face losses is their lack of capital (Popova and Butakova, 2019).

Consolidation in the banking sector of the particular country

Metro Bank Plc. Is a large scale financial institution of United Kingdom which is

impacted by every activity in the banking industry. The major factor due to which profitability

and survival chances of an organisation gets impacted is the consolidation of competitors brands.

This type of issue results in increase in market share of the consolidated companies which

obviously reducing market share of other companies. The reason behind declining market share

and profitability of Metro Bank is the major consolidations in the industry. The recent example

of such consolidation is Shawbrook and FirstRand’s £1.1bn purchase of Aldermore (Pilnik,

Radionov and Yazykov, 2018).

In case of losses and lost of market share, financial institutions opt for consolidation. This

option of merging of two or more companies into one is most use in financial sector. This

method of consolidation allows losses making organisations to merge their operations, market

share and goodwill by which they gain high share in market and also consolidation also helps in

to be in news which attracts attention of consumers as well.

Issues relevant to the changes observed in the global banking markets or particular

country’s banking markets

After the global recession, the banking sector of United kingdom faced a firm stability

until 2018 and this stability resulted in various issues which were bought due to changes in

banking market of United Kingdom. The industry of Banking has recently faced various changes

which includes changes in strategic regulations, promotion of electronic transactions, product

amendments for retail banking sector and empathises on mobile banking services. All these

changes influenced the operations of Metro Bank Plc. Due to which they have to ‘re design and

develop their services as well as their strategies to compete in market (Smolyansky, 2019).

9

influenced adversely.

Due to high innovation in the Fintech projects, the organisations of Fintech is acquiring

success over grabbing attention of investors. Due to innovative products and services, the

investment flow which was usually in the support of Banking institution, is now exploring their

portfolio and investing fintech organisation, due to which it is hard for banking organisations like

Metro Bank to operate in absence of adequate capital. As analysed in ratio analysis, a major

reason for Metro Bank to face losses is their lack of capital (Popova and Butakova, 2019).

Consolidation in the banking sector of the particular country

Metro Bank Plc. Is a large scale financial institution of United Kingdom which is

impacted by every activity in the banking industry. The major factor due to which profitability

and survival chances of an organisation gets impacted is the consolidation of competitors brands.

This type of issue results in increase in market share of the consolidated companies which

obviously reducing market share of other companies. The reason behind declining market share

and profitability of Metro Bank is the major consolidations in the industry. The recent example

of such consolidation is Shawbrook and FirstRand’s £1.1bn purchase of Aldermore (Pilnik,

Radionov and Yazykov, 2018).

In case of losses and lost of market share, financial institutions opt for consolidation. This

option of merging of two or more companies into one is most use in financial sector. This

method of consolidation allows losses making organisations to merge their operations, market

share and goodwill by which they gain high share in market and also consolidation also helps in

to be in news which attracts attention of consumers as well.

Issues relevant to the changes observed in the global banking markets or particular

country’s banking markets

After the global recession, the banking sector of United kingdom faced a firm stability

until 2018 and this stability resulted in various issues which were bought due to changes in

banking market of United Kingdom. The industry of Banking has recently faced various changes

which includes changes in strategic regulations, promotion of electronic transactions, product

amendments for retail banking sector and empathises on mobile banking services. All these

changes influenced the operations of Metro Bank Plc. Due to which they have to ‘re design and

develop their services as well as their strategies to compete in market (Smolyansky, 2019).

9

Assessment of an expected future performance of Metro bank

From the analysis which has been conducted above, it has been observed that from last

ten years Metro Bank Plc is operating smoothly as it’s profits and revenues are increasing which

an increasing rate. The banking institution which has been selected for this report is Metro Bank

which is listed on London stock exchange and only operate till the boundaries of United

Kingdom. The position of this company was shattered due to economic breakdown and global

recession which happened a decade ago. The years past decade was well used by Metro Bank to

‘re introduce their products and services in market so that they can earn reliable profits and

survive in a competitive market of United Kingdom. Observing the above analysis, ensured the

success of this company which they were enjoying till 2019. The revenues and profits of this

company was at its peak and this company also acquired their record sales.

This success of Metro Bank Plc get influenced due to Brexit implementation in 2019 that

also lead to heavy losses to this company. The future of this company will also have to suffer the

consequences of Brexit and the future complications which are ahead of the operationsof this

bank due to global medical breakdown (Covid 19).

CONCLUSION

From the above report, it has been concluded that modern baking is the system which

empathise on electronic transactions and financial technology institutions. The above report is

the summarization of financial performance and position of Metro Bank Plc in United Kingdom

market from which it has been concluded that Metro Plc was in good position until Brexit

consequences impacted the operations of this company and also the future of this bank has to

suffer due to recent complications of global economic breakdown due to Covid 19.

10

From the analysis which has been conducted above, it has been observed that from last

ten years Metro Bank Plc is operating smoothly as it’s profits and revenues are increasing which

an increasing rate. The banking institution which has been selected for this report is Metro Bank

which is listed on London stock exchange and only operate till the boundaries of United

Kingdom. The position of this company was shattered due to economic breakdown and global

recession which happened a decade ago. The years past decade was well used by Metro Bank to

‘re introduce their products and services in market so that they can earn reliable profits and

survive in a competitive market of United Kingdom. Observing the above analysis, ensured the

success of this company which they were enjoying till 2019. The revenues and profits of this

company was at its peak and this company also acquired their record sales.

This success of Metro Bank Plc get influenced due to Brexit implementation in 2019 that

also lead to heavy losses to this company. The future of this company will also have to suffer the

consequences of Brexit and the future complications which are ahead of the operationsof this

bank due to global medical breakdown (Covid 19).

CONCLUSION

From the above report, it has been concluded that modern baking is the system which

empathise on electronic transactions and financial technology institutions. The above report is

the summarization of financial performance and position of Metro Bank Plc in United Kingdom

market from which it has been concluded that Metro Plc was in good position until Brexit

consequences impacted the operations of this company and also the future of this bank has to

suffer due to recent complications of global economic breakdown due to Covid 19.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.