Metro Bank Performance: Analysis of Financial Statements and Ratios

VerifiedAdded on 2023/01/12

|14

|4045

|92

Report

AI Summary

This report provides a comprehensive financial analysis of Metro Bank, examining its performance over a nine-year period. It begins with an overview of the bank's nature and business activities, followed by a critical analysis of changes in its income statement and balance sheet. The report assesses the bank's financial performance using key ratios such as profitability, efficiency, asset quality, and capital adequacy. It also evaluates the impact of changes in the banking sector, including regulations, FinTech developments, and consolidation, on Metro Bank's performance. The analysis includes income trends, balance sheet trends, and a debt-equity graph, providing a detailed understanding of the bank's financial position. Furthermore, the report analyzes various financial ratios, including gross profit margin, net profit margin, asset turnover ratio, fixed asset turnover ratio, asset quality ratios, and capital adequacy ratios, to assess the bank's efficiency and financial health. The report concludes with an assessment of the expected future performance of Metro Bank.

MODERN

BANKING

BANKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Overview..........................................................................................................................................3

Critically analyze how bank’s income statement and balance sheet changed over time.................4

Critically analyze the bank’s performance over the selected period using ratios............................6

Evaluate how the banking sector changes have impacted Metro Bank performance......................9

a. Changes in bank regulation....................................................................................................10

b. Increase impact of FinTech developments on banking business...........................................10

c. Consolidation in the banking sector of the particular country...............................................11

d. Other issues occur changes in the global banking markets...................................................11

Assessment of the expected future performance of Metro Bank...................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

APPENDICES...............................................................................................................................14

INTRODUCTION...........................................................................................................................3

Overview..........................................................................................................................................3

Critically analyze how bank’s income statement and balance sheet changed over time.................4

Critically analyze the bank’s performance over the selected period using ratios............................6

Evaluate how the banking sector changes have impacted Metro Bank performance......................9

a. Changes in bank regulation....................................................................................................10

b. Increase impact of FinTech developments on banking business...........................................10

c. Consolidation in the banking sector of the particular country...............................................11

d. Other issues occur changes in the global banking markets...................................................11

Assessment of the expected future performance of Metro Bank...................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

APPENDICES...............................................................................................................................14

INTRODUCTION

This project consists of project report of commercial bank which is Metro Bank; having

international business all over the world. This project report starts with overview of Metro Bank

in terms of its nature and business activities. Assessment of changes in bank’s asset and liability

and income structure will show variance in the structure of bank through analysis of past 9 years

report of selected bank. Metro Bank financial performance has been analyzed through financial

key performance indicators such as profitability, efficiency, asset quality and capital adequacy

ratios. Also changes of banking sector like in bank regulation, impact of FinTech developments

on banking business, etc. on performance of Metro Bank has been evaluated.

Overview

Metro Bank. is an American multinational investment bank and financial services company

headquartered in New York City. It comes under one of the top 50 valuable bank all over the

world by market capitalization (MTRO METRO BANK PLC ORD 0.0001P, 2020).

Metro Bank is considered a universal bank and custodian bank. The Metro Bank brand, is used

by the departments of investment banking, asset management, private banking, private asset

management, and treasury and securities services.

Nature of business and activities: It is a major provider of various investment banking and

financial services. Trustworthy activity within private banking and private asset management is

carried out under Metro Bank. The brand is used for credit card services in the United States and

Canada, the bank's retail banking activities in the United States, and commercial banking. Both

the retail and commercial bank and the bank's corporate headquarters are located at 270 Park

Avenue in Midtown Manhattan, New York City.

This project consists of project report of commercial bank which is Metro Bank; having

international business all over the world. This project report starts with overview of Metro Bank

in terms of its nature and business activities. Assessment of changes in bank’s asset and liability

and income structure will show variance in the structure of bank through analysis of past 9 years

report of selected bank. Metro Bank financial performance has been analyzed through financial

key performance indicators such as profitability, efficiency, asset quality and capital adequacy

ratios. Also changes of banking sector like in bank regulation, impact of FinTech developments

on banking business, etc. on performance of Metro Bank has been evaluated.

Overview

Metro Bank. is an American multinational investment bank and financial services company

headquartered in New York City. It comes under one of the top 50 valuable bank all over the

world by market capitalization (MTRO METRO BANK PLC ORD 0.0001P, 2020).

Metro Bank is considered a universal bank and custodian bank. The Metro Bank brand, is used

by the departments of investment banking, asset management, private banking, private asset

management, and treasury and securities services.

Nature of business and activities: It is a major provider of various investment banking and

financial services. Trustworthy activity within private banking and private asset management is

carried out under Metro Bank. The brand is used for credit card services in the United States and

Canada, the bank's retail banking activities in the United States, and commercial banking. Both

the retail and commercial bank and the bank's corporate headquarters are located at 270 Park

Avenue in Midtown Manhattan, New York City.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Critically analyze how bank’s income statement and balance sheet

changed over time

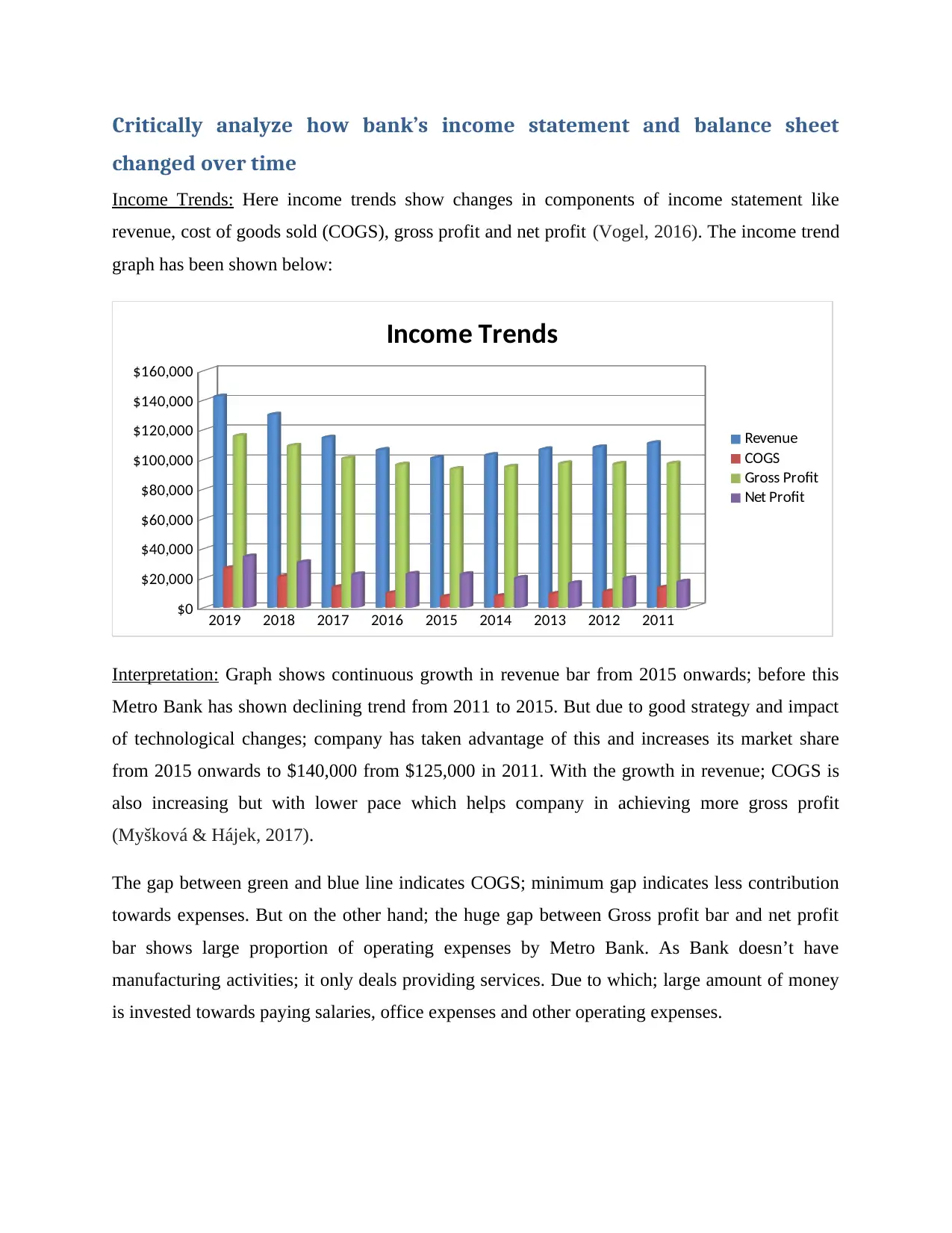

Income Trends: Here income trends show changes in components of income statement like

revenue, cost of goods sold (COGS), gross profit and net profit (Vogel, 2016). The income trend

graph has been shown below:

2019 2018 2017 2016 2015 2014 2013 2012 2011

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

Income Trends

Revenue

COGS

Gross Profit

Net Profit

Interpretation: Graph shows continuous growth in revenue bar from 2015 onwards; before this

Metro Bank has shown declining trend from 2011 to 2015. But due to good strategy and impact

of technological changes; company has taken advantage of this and increases its market share

from 2015 onwards to $140,000 from $125,000 in 2011. With the growth in revenue; COGS is

also increasing but with lower pace which helps company in achieving more gross profit

(Myšková & Hájek, 2017).

The gap between green and blue line indicates COGS; minimum gap indicates less contribution

towards expenses. But on the other hand; the huge gap between Gross profit bar and net profit

bar shows large proportion of operating expenses by Metro Bank. As Bank doesn’t have

manufacturing activities; it only deals providing services. Due to which; large amount of money

is invested towards paying salaries, office expenses and other operating expenses.

changed over time

Income Trends: Here income trends show changes in components of income statement like

revenue, cost of goods sold (COGS), gross profit and net profit (Vogel, 2016). The income trend

graph has been shown below:

2019 2018 2017 2016 2015 2014 2013 2012 2011

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

Income Trends

Revenue

COGS

Gross Profit

Net Profit

Interpretation: Graph shows continuous growth in revenue bar from 2015 onwards; before this

Metro Bank has shown declining trend from 2011 to 2015. But due to good strategy and impact

of technological changes; company has taken advantage of this and increases its market share

from 2015 onwards to $140,000 from $125,000 in 2011. With the growth in revenue; COGS is

also increasing but with lower pace which helps company in achieving more gross profit

(Myšková & Hájek, 2017).

The gap between green and blue line indicates COGS; minimum gap indicates less contribution

towards expenses. But on the other hand; the huge gap between Gross profit bar and net profit

bar shows large proportion of operating expenses by Metro Bank. As Bank doesn’t have

manufacturing activities; it only deals providing services. Due to which; large amount of money

is invested towards paying salaries, office expenses and other operating expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

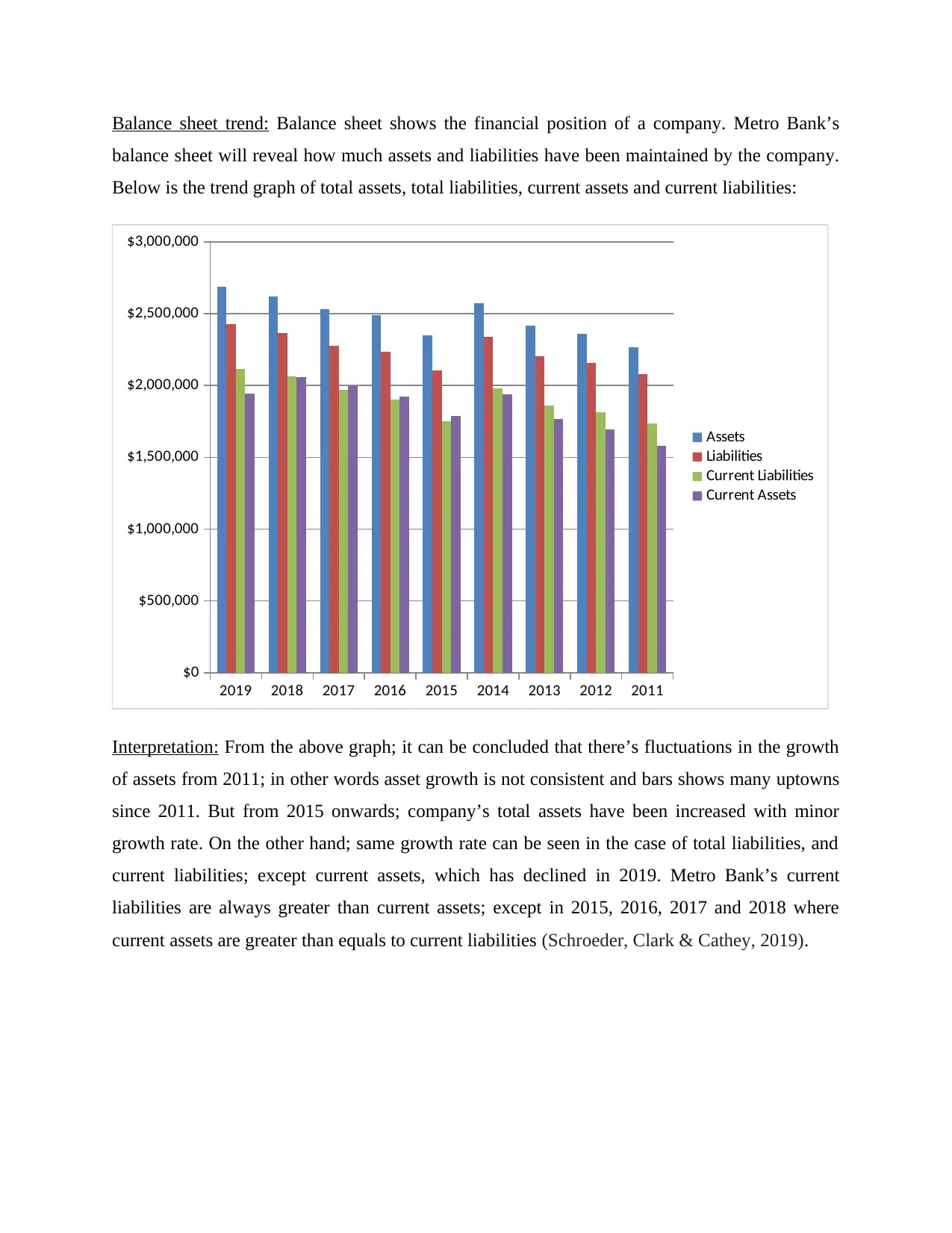

Balance sheet trend: Balance sheet shows the financial position of a company. Metro Bank’s

balance sheet will reveal how much assets and liabilities have been maintained by the company.

Below is the trend graph of total assets, total liabilities, current assets and current liabilities:

2019 2018 2017 2016 2015 2014 2013 2012 2011

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

Assets

Liabilities

Current Liabilities

Current Assets

Interpretation: From the above graph; it can be concluded that there’s fluctuations in the growth

of assets from 2011; in other words asset growth is not consistent and bars shows many uptowns

since 2011. But from 2015 onwards; company’s total assets have been increased with minor

growth rate. On the other hand; same growth rate can be seen in the case of total liabilities, and

current liabilities; except current assets, which has declined in 2019. Metro Bank’s current

liabilities are always greater than current assets; except in 2015, 2016, 2017 and 2018 where

current assets are greater than equals to current liabilities (Schroeder, Clark & Cathey, 2019).

balance sheet will reveal how much assets and liabilities have been maintained by the company.

Below is the trend graph of total assets, total liabilities, current assets and current liabilities:

2019 2018 2017 2016 2015 2014 2013 2012 2011

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

Assets

Liabilities

Current Liabilities

Current Assets

Interpretation: From the above graph; it can be concluded that there’s fluctuations in the growth

of assets from 2011; in other words asset growth is not consistent and bars shows many uptowns

since 2011. But from 2015 onwards; company’s total assets have been increased with minor

growth rate. On the other hand; same growth rate can be seen in the case of total liabilities, and

current liabilities; except current assets, which has declined in 2019. Metro Bank’s current

liabilities are always greater than current assets; except in 2015, 2016, 2017 and 2018 where

current assets are greater than equals to current liabilities (Schroeder, Clark & Cathey, 2019).

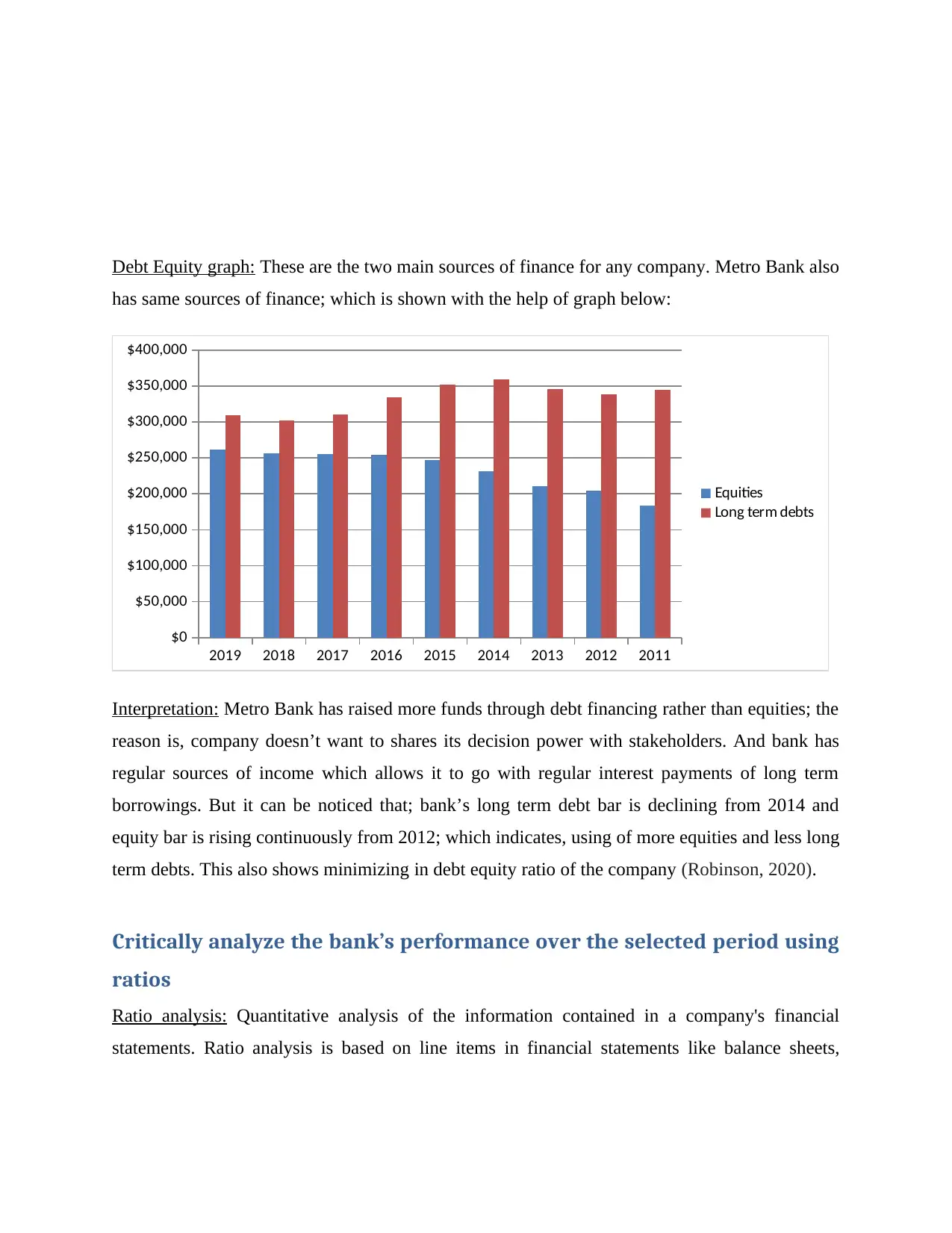

Debt Equity graph: These are the two main sources of finance for any company. Metro Bank also

has same sources of finance; which is shown with the help of graph below:

2019 2018 2017 2016 2015 2014 2013 2012 2011

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

Equities

Long term debts

Interpretation: Metro Bank has raised more funds through debt financing rather than equities; the

reason is, company doesn’t want to shares its decision power with stakeholders. And bank has

regular sources of income which allows it to go with regular interest payments of long term

borrowings. But it can be noticed that; bank’s long term debt bar is declining from 2014 and

equity bar is rising continuously from 2012; which indicates, using of more equities and less long

term debts. This also shows minimizing in debt equity ratio of the company (Robinson, 2020).

Critically analyze the bank’s performance over the selected period using

ratios

Ratio analysis: Quantitative analysis of the information contained in a company's financial

statements. Ratio analysis is based on line items in financial statements like balance sheets,

has same sources of finance; which is shown with the help of graph below:

2019 2018 2017 2016 2015 2014 2013 2012 2011

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

Equities

Long term debts

Interpretation: Metro Bank has raised more funds through debt financing rather than equities; the

reason is, company doesn’t want to shares its decision power with stakeholders. And bank has

regular sources of income which allows it to go with regular interest payments of long term

borrowings. But it can be noticed that; bank’s long term debt bar is declining from 2014 and

equity bar is rising continuously from 2012; which indicates, using of more equities and less long

term debts. This also shows minimizing in debt equity ratio of the company (Robinson, 2020).

Critically analyze the bank’s performance over the selected period using

ratios

Ratio analysis: Quantitative analysis of the information contained in a company's financial

statements. Ratio analysis is based on line items in financial statements like balance sheets,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

income statements and cash flow statements; the ratios of one item to another item or

combination - or a combination of items - are then calculated (de Medeiros, and et.al., 2017).

Types of ratio analysis:

Profitability ratio: This is commonly called as a percentage of gross profit, of course, is the

difference between a company's sales or products and / or services and costs the company a lot to

provide those products and / or services.

Types of profitability ratio:

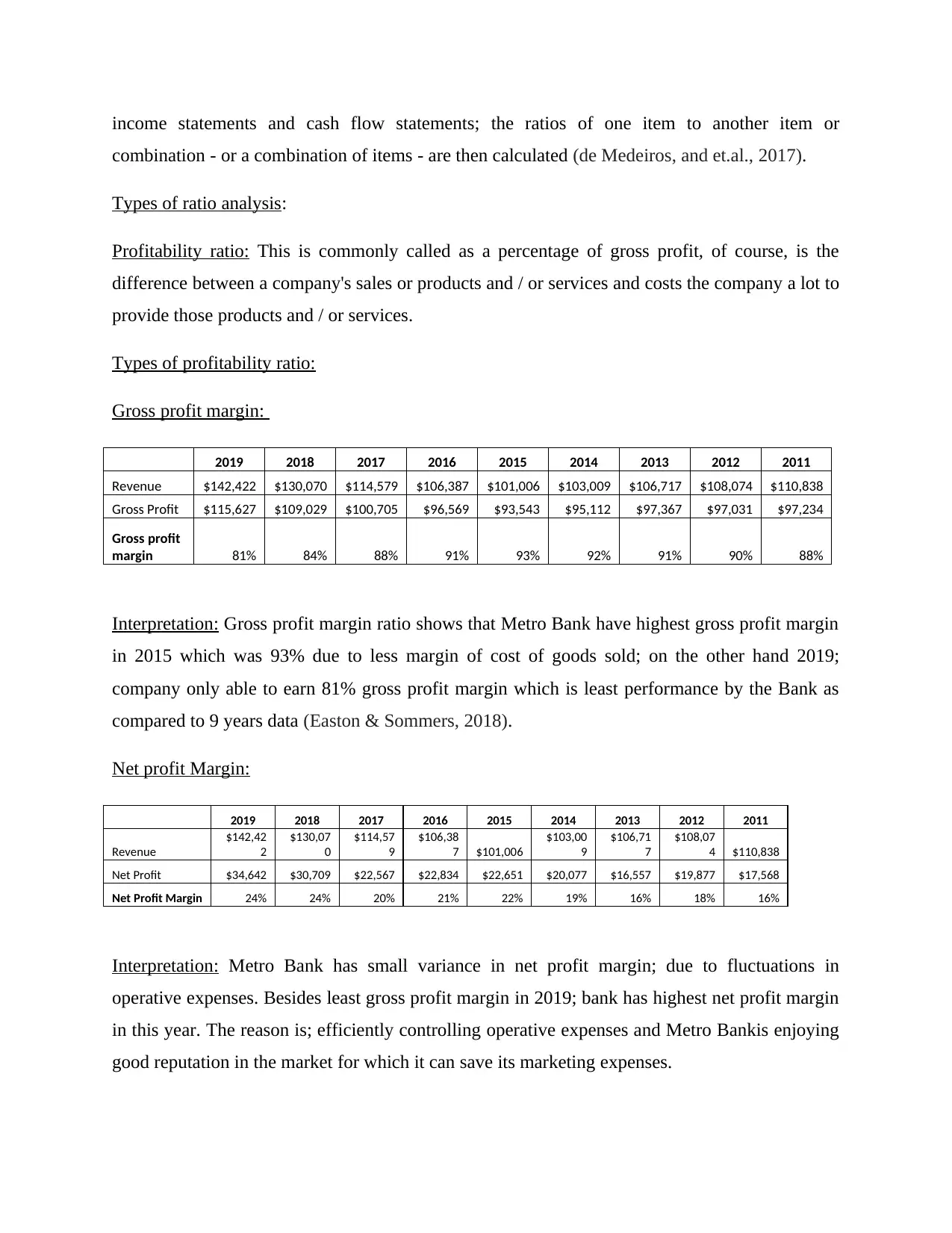

Gross profit margin:

2019 2018 2017 2016 2015 2014 2013 2012 2011

Revenue $142,422 $130,070 $114,579 $106,387 $101,006 $103,009 $106,717 $108,074 $110,838

Gross Profit $115,627 $109,029 $100,705 $96,569 $93,543 $95,112 $97,367 $97,031 $97,234

Gross profit

margin 81% 84% 88% 91% 93% 92% 91% 90% 88%

Interpretation: Gross profit margin ratio shows that Metro Bank have highest gross profit margin

in 2015 which was 93% due to less margin of cost of goods sold; on the other hand 2019;

company only able to earn 81% gross profit margin which is least performance by the Bank as

compared to 9 years data (Easton & Sommers, 2018).

Net profit Margin:

2019 2018 2017 2016 2015 2014 2013 2012 2011

Revenue

$142,42

2

$130,07

0

$114,57

9

$106,38

7 $101,006

$103,00

9

$106,71

7

$108,07

4 $110,838

Net Profit $34,642 $30,709 $22,567 $22,834 $22,651 $20,077 $16,557 $19,877 $17,568

Net Profit Margin 24% 24% 20% 21% 22% 19% 16% 18% 16%

Interpretation: Metro Bank has small variance in net profit margin; due to fluctuations in

operative expenses. Besides least gross profit margin in 2019; bank has highest net profit margin

in this year. The reason is; efficiently controlling operative expenses and Metro Bankis enjoying

good reputation in the market for which it can save its marketing expenses.

combination - or a combination of items - are then calculated (de Medeiros, and et.al., 2017).

Types of ratio analysis:

Profitability ratio: This is commonly called as a percentage of gross profit, of course, is the

difference between a company's sales or products and / or services and costs the company a lot to

provide those products and / or services.

Types of profitability ratio:

Gross profit margin:

2019 2018 2017 2016 2015 2014 2013 2012 2011

Revenue $142,422 $130,070 $114,579 $106,387 $101,006 $103,009 $106,717 $108,074 $110,838

Gross Profit $115,627 $109,029 $100,705 $96,569 $93,543 $95,112 $97,367 $97,031 $97,234

Gross profit

margin 81% 84% 88% 91% 93% 92% 91% 90% 88%

Interpretation: Gross profit margin ratio shows that Metro Bank have highest gross profit margin

in 2015 which was 93% due to less margin of cost of goods sold; on the other hand 2019;

company only able to earn 81% gross profit margin which is least performance by the Bank as

compared to 9 years data (Easton & Sommers, 2018).

Net profit Margin:

2019 2018 2017 2016 2015 2014 2013 2012 2011

Revenue

$142,42

2

$130,07

0

$114,57

9

$106,38

7 $101,006

$103,00

9

$106,71

7

$108,07

4 $110,838

Net Profit $34,642 $30,709 $22,567 $22,834 $22,651 $20,077 $16,557 $19,877 $17,568

Net Profit Margin 24% 24% 20% 21% 22% 19% 16% 18% 16%

Interpretation: Metro Bank has small variance in net profit margin; due to fluctuations in

operative expenses. Besides least gross profit margin in 2019; bank has highest net profit margin

in this year. The reason is; efficiently controlling operative expenses and Metro Bankis enjoying

good reputation in the market for which it can save its marketing expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Efficiency ratio: The efficiency ratio, also known as the activity ratio, is used by analysts to

measure the performance of a company's short-term or current performance. All these ratios use

the number in a company's current assets or current liabilities, which measure the operation of

the business.

Types of efficiency ratio:

Assets turnover ratio: Formula = revenue / total assets

2019 2018 2017 2016 2015 2014 2013 2012 2011

Revenue $142,422 $130,070 $114,579 $106,387 $101,006 $103,009 $106,717 $108,074 $110,838

Assets

$2,687,37

9 $2,622,532

$2,533,60

0

$2,490,97

2

$2,351,69

8 $2,572,274

$2,415,68

9

$2,359,14

1 $2,265,792

Assets

Turnover

ratio 5% 5% 5% 4% 4% 4% 4% 5% 5%

Interpretation: This ratio shows how efficiently total assets are utilized for generating revenue.

There’s little bit variations in this ratio over the past 9 years But 5% is the maximum ratio which

Metro Bank has achieved up to 2019 (Campisi, Gitto & Morea, 2017),

Fixed assets turnover ratio: Formula = Total revenue / Fixed assets

2019 2018 2017 2016 2015 2014 2013 2012 2011

Revenue

$142,42

2 $130,070

$114,57

9

$106,38

7 $101,006

$103,00

9 $106,717

$108,07

4 $110,838

Fixed assets

$743,98

1 $564,128

$537,20

8

$565,92

1 $564,430

$631,94

5 $649,773

$664,48

7 $684,045

Fixed assets turnover ratio 19% 23% 21% 19% 18% 16% 16% 16% 16%

Interpretation: The highest fixed assets turnover ratio achieved by the company is in 2018, the

trend shows continuously increasing growth; except in 2019 where growth declined by 4%. And

this shows less efficiency by bank to convert its fixed assets into revenue.

Assets quality ratio: The quality of assets of non-banking financial companies (NBFCs) declined

during the first six months of the current financial year. Their integrated non-performing assets

(GNPA) ratio increased from 6.1 percent in March 2019 to 6.3 percent in September 2019. Here

the report of Metro Bank:

measure the performance of a company's short-term or current performance. All these ratios use

the number in a company's current assets or current liabilities, which measure the operation of

the business.

Types of efficiency ratio:

Assets turnover ratio: Formula = revenue / total assets

2019 2018 2017 2016 2015 2014 2013 2012 2011

Revenue $142,422 $130,070 $114,579 $106,387 $101,006 $103,009 $106,717 $108,074 $110,838

Assets

$2,687,37

9 $2,622,532

$2,533,60

0

$2,490,97

2

$2,351,69

8 $2,572,274

$2,415,68

9

$2,359,14

1 $2,265,792

Assets

Turnover

ratio 5% 5% 5% 4% 4% 4% 4% 5% 5%

Interpretation: This ratio shows how efficiently total assets are utilized for generating revenue.

There’s little bit variations in this ratio over the past 9 years But 5% is the maximum ratio which

Metro Bank has achieved up to 2019 (Campisi, Gitto & Morea, 2017),

Fixed assets turnover ratio: Formula = Total revenue / Fixed assets

2019 2018 2017 2016 2015 2014 2013 2012 2011

Revenue

$142,42

2 $130,070

$114,57

9

$106,38

7 $101,006

$103,00

9 $106,717

$108,07

4 $110,838

Fixed assets

$743,98

1 $564,128

$537,20

8

$565,92

1 $564,430

$631,94

5 $649,773

$664,48

7 $684,045

Fixed assets turnover ratio 19% 23% 21% 19% 18% 16% 16% 16% 16%

Interpretation: The highest fixed assets turnover ratio achieved by the company is in 2018, the

trend shows continuously increasing growth; except in 2019 where growth declined by 4%. And

this shows less efficiency by bank to convert its fixed assets into revenue.

Assets quality ratio: The quality of assets of non-banking financial companies (NBFCs) declined

during the first six months of the current financial year. Their integrated non-performing assets

(GNPA) ratio increased from 6.1 percent in March 2019 to 6.3 percent in September 2019. Here

the report of Metro Bank:

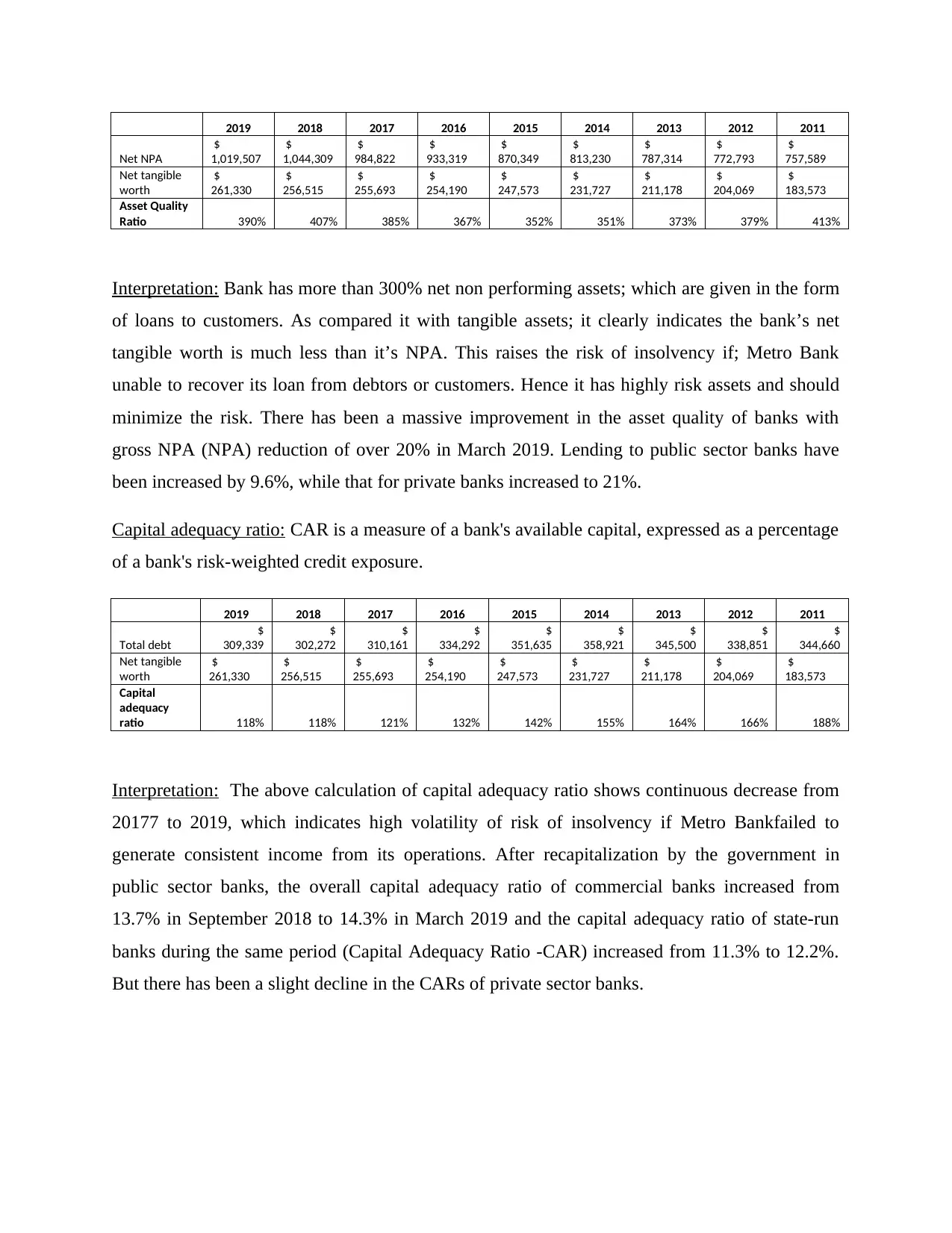

2019 2018 2017 2016 2015 2014 2013 2012 2011

Net NPA

$

1,019,507

$

1,044,309

$

984,822

$

933,319

$

870,349

$

813,230

$

787,314

$

772,793

$

757,589

Net tangible

worth

$

261,330

$

256,515

$

255,693

$

254,190

$

247,573

$

231,727

$

211,178

$

204,069

$

183,573

Asset Quality

Ratio 390% 407% 385% 367% 352% 351% 373% 379% 413%

Interpretation: Bank has more than 300% net non performing assets; which are given in the form

of loans to customers. As compared it with tangible assets; it clearly indicates the bank’s net

tangible worth is much less than it’s NPA. This raises the risk of insolvency if; Metro Bank

unable to recover its loan from debtors or customers. Hence it has highly risk assets and should

minimize the risk. There has been a massive improvement in the asset quality of banks with

gross NPA (NPA) reduction of over 20% in March 2019. Lending to public sector banks have

been increased by 9.6%, while that for private banks increased to 21%.

Capital adequacy ratio: CAR is a measure of a bank's available capital, expressed as a percentage

of a bank's risk-weighted credit exposure.

2019 2018 2017 2016 2015 2014 2013 2012 2011

Total debt

$

309,339

$

302,272

$

310,161

$

334,292

$

351,635

$

358,921

$

345,500

$

338,851

$

344,660

Net tangible

worth

$

261,330

$

256,515

$

255,693

$

254,190

$

247,573

$

231,727

$

211,178

$

204,069

$

183,573

Capital

adequacy

ratio 118% 118% 121% 132% 142% 155% 164% 166% 188%

Interpretation: The above calculation of capital adequacy ratio shows continuous decrease from

20177 to 2019, which indicates high volatility of risk of insolvency if Metro Bankfailed to

generate consistent income from its operations. After recapitalization by the government in

public sector banks, the overall capital adequacy ratio of commercial banks increased from

13.7% in September 2018 to 14.3% in March 2019 and the capital adequacy ratio of state-run

banks during the same period (Capital Adequacy Ratio -CAR) increased from 11.3% to 12.2%.

But there has been a slight decline in the CARs of private sector banks.

Net NPA

$

1,019,507

$

1,044,309

$

984,822

$

933,319

$

870,349

$

813,230

$

787,314

$

772,793

$

757,589

Net tangible

worth

$

261,330

$

256,515

$

255,693

$

254,190

$

247,573

$

231,727

$

211,178

$

204,069

$

183,573

Asset Quality

Ratio 390% 407% 385% 367% 352% 351% 373% 379% 413%

Interpretation: Bank has more than 300% net non performing assets; which are given in the form

of loans to customers. As compared it with tangible assets; it clearly indicates the bank’s net

tangible worth is much less than it’s NPA. This raises the risk of insolvency if; Metro Bank

unable to recover its loan from debtors or customers. Hence it has highly risk assets and should

minimize the risk. There has been a massive improvement in the asset quality of banks with

gross NPA (NPA) reduction of over 20% in March 2019. Lending to public sector banks have

been increased by 9.6%, while that for private banks increased to 21%.

Capital adequacy ratio: CAR is a measure of a bank's available capital, expressed as a percentage

of a bank's risk-weighted credit exposure.

2019 2018 2017 2016 2015 2014 2013 2012 2011

Total debt

$

309,339

$

302,272

$

310,161

$

334,292

$

351,635

$

358,921

$

345,500

$

338,851

$

344,660

Net tangible

worth

$

261,330

$

256,515

$

255,693

$

254,190

$

247,573

$

231,727

$

211,178

$

204,069

$

183,573

Capital

adequacy

ratio 118% 118% 121% 132% 142% 155% 164% 166% 188%

Interpretation: The above calculation of capital adequacy ratio shows continuous decrease from

20177 to 2019, which indicates high volatility of risk of insolvency if Metro Bankfailed to

generate consistent income from its operations. After recapitalization by the government in

public sector banks, the overall capital adequacy ratio of commercial banks increased from

13.7% in September 2018 to 14.3% in March 2019 and the capital adequacy ratio of state-run

banks during the same period (Capital Adequacy Ratio -CAR) increased from 11.3% to 12.2%.

But there has been a slight decline in the CARs of private sector banks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Evaluate how the banking sector changes have impacted Metro Bank

performance

Banking sector has track many changes over the period of time in terms of technology, way of

operations and delivery of services. Some of these changes have been discussed below:

a. Changes in bank regulation

The Federal Reserve System (also known as the Federal Reserve or simply the Fed) is the central

banking system of the United States which regulates all public and commercial banks in New

York and other states of America. The US Central Bank Federal Reserve has not made any

changes in interest rates. The central bank committee decided to keep the interest rates at 1.25-

1.5 per cent after the meeting. Emerging markets around the world have breathed a sigh of relief.

Impact on Metro Bank: Bank interest rates is expected to be increased in future; which will

provide more opportunity to banks to raise its loan amount but at the same time; its liability to

pay more interest on savings by general public will also increase. This will affect overall net

profit margin of the company in next financial year 2020 (Metro Bank Balance Sheet 2005-2020

JPM, 2020).

b. Increase impact of FinTech developments on banking business

FinTech refers to the integration of technology into financial services; it is also knows as

digitalization of banking services. The review proposes that public sector banks need to embrace

FinTech, which is revolutionizing the global financial landscape. FinTech has rapidly changed

the way information is refined by banks.

Banks always provide transaction intermediaries necessary to provide humanitarian assistance by

recording in "centralized" databases. With years of technological innovation, the banking

industry is improving its financial processes and products, and is now slowly adapting to digital

transformation and financial technology models. However, there is a technology that is not only

digital, fast and secure, but also a "distributed" database that records the visible transactions of

all stakeholders involved in its network across international borders, which means providing full

transparency capability do. To this end, banks may no longer need to help deliver business

(Yarbro & Mehlenbeck, 2016).

performance

Banking sector has track many changes over the period of time in terms of technology, way of

operations and delivery of services. Some of these changes have been discussed below:

a. Changes in bank regulation

The Federal Reserve System (also known as the Federal Reserve or simply the Fed) is the central

banking system of the United States which regulates all public and commercial banks in New

York and other states of America. The US Central Bank Federal Reserve has not made any

changes in interest rates. The central bank committee decided to keep the interest rates at 1.25-

1.5 per cent after the meeting. Emerging markets around the world have breathed a sigh of relief.

Impact on Metro Bank: Bank interest rates is expected to be increased in future; which will

provide more opportunity to banks to raise its loan amount but at the same time; its liability to

pay more interest on savings by general public will also increase. This will affect overall net

profit margin of the company in next financial year 2020 (Metro Bank Balance Sheet 2005-2020

JPM, 2020).

b. Increase impact of FinTech developments on banking business

FinTech refers to the integration of technology into financial services; it is also knows as

digitalization of banking services. The review proposes that public sector banks need to embrace

FinTech, which is revolutionizing the global financial landscape. FinTech has rapidly changed

the way information is refined by banks.

Banks always provide transaction intermediaries necessary to provide humanitarian assistance by

recording in "centralized" databases. With years of technological innovation, the banking

industry is improving its financial processes and products, and is now slowly adapting to digital

transformation and financial technology models. However, there is a technology that is not only

digital, fast and secure, but also a "distributed" database that records the visible transactions of

all stakeholders involved in its network across international borders, which means providing full

transparency capability do. To this end, banks may no longer need to help deliver business

(Yarbro & Mehlenbeck, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The block chain has provided the right kind of support, at the right time, at the right time, with

the opportunity to make the necessary trust changes between stakeholders: the beginning of a

new non-mediated era seems to be the humanitarian future of the system.

c. Consolidation in the banking sector of the particular country

In the future, technology will determine the modalities of banking. This includes huge data,

cloud computing, smart phones and other similar inventions. Consolidation within American

industry has led to a very high 50 percent inside bank amount and to bring about sweetness in

relationships during the preceding 20 years. Our paper has reviewed important changes within

the business in this period. The association redefines the macroeconomic forces behind design

and the microeconomics etiquette of thinking; Reviews the results of actual research on mixing

what has been impacted on things like banking disputes, efficiency, productivity, speculative

connectors and availability and evaluation of banking organizations. And theories on how

recurring patterns of progress can influence the functioning of force business structure. As the

21st century expands, we find that some of the forces that drove the design of the union inside

the past no longer appear significant or are reduced to a very small extent (Smith, Betts & Smith,

2018).

By concretizing this data in our estimation, we imagine that money-related businesses may

experience a slight to coordinate decline inside the volume of relationships over the course of

five to 10 years.

d. Other issues occur changes in the global banking markets

The worldwide budgetary emergency prompted a reintegration of the advantages and dangers of

the account - including administrations related to universal money - which many viewers accept

were too large and overly confusing and whose items, e.g. However, complex investigations and

subsidiaries appeared to offer very little value although several risks have arisen.

Fringe has grown rapidly over the course of two years, with banking coming back around the

world. In the early three months of 2008, the total remote bank lending fell drastically in the

wake of the crimping. The decay was particularly large in direct cross-fringe advances; Debt

through external members is continuously increasing. This patronage was largely driven by

showcase powers, as their wealth reports under promoted banks were reduced. Be that as it may,

the opportunity to make the necessary trust changes between stakeholders: the beginning of a

new non-mediated era seems to be the humanitarian future of the system.

c. Consolidation in the banking sector of the particular country

In the future, technology will determine the modalities of banking. This includes huge data,

cloud computing, smart phones and other similar inventions. Consolidation within American

industry has led to a very high 50 percent inside bank amount and to bring about sweetness in

relationships during the preceding 20 years. Our paper has reviewed important changes within

the business in this period. The association redefines the macroeconomic forces behind design

and the microeconomics etiquette of thinking; Reviews the results of actual research on mixing

what has been impacted on things like banking disputes, efficiency, productivity, speculative

connectors and availability and evaluation of banking organizations. And theories on how

recurring patterns of progress can influence the functioning of force business structure. As the

21st century expands, we find that some of the forces that drove the design of the union inside

the past no longer appear significant or are reduced to a very small extent (Smith, Betts & Smith,

2018).

By concretizing this data in our estimation, we imagine that money-related businesses may

experience a slight to coordinate decline inside the volume of relationships over the course of

five to 10 years.

d. Other issues occur changes in the global banking markets

The worldwide budgetary emergency prompted a reintegration of the advantages and dangers of

the account - including administrations related to universal money - which many viewers accept

were too large and overly confusing and whose items, e.g. However, complex investigations and

subsidiaries appeared to offer very little value although several risks have arisen.

Fringe has grown rapidly over the course of two years, with banking coming back around the

world. In the early three months of 2008, the total remote bank lending fell drastically in the

wake of the crimping. The decay was particularly large in direct cross-fringe advances; Debt

through external members is continuously increasing. This patronage was largely driven by

showcase powers, as their wealth reports under promoted banks were reduced. Be that as it may,

some domestic administrative changes have added to the craving to withdraw their command

posts (Smith, Betts & Smith, 2018).

Assessment of the expected future performance of Metro Bank

Hence, on the basis of above project report; it can be assessed that Metro Bank which is leading

commercial bank in United States of America has bright future and lots of big opportunities are

waiting for the company. On the basis of trend analysis; it can be expected that its revenue will

be grow in upcoming year 2020 and simultaneously more efficient controlling of operative

activities will definitely improve net profit of the company. It is also estimated that Metro

Bankwill mix more equity fund for sources of financing compare with long term debt. This will

affect the decision making power of the company.

CONCLUSION

After analysis of whole report; it can be concluded that digitalization has changed the philosophy

of bank from only providing savings to customer to security, providing loan, tracking

information’s and many more facilities. Ratio’s have their own limitation, as it cannot

differentiate between huge amount and less amount. Profitability ratio or Gross margin is the

amount of each dollar of sales that the company is able to keep as gross profit.

posts (Smith, Betts & Smith, 2018).

Assessment of the expected future performance of Metro Bank

Hence, on the basis of above project report; it can be assessed that Metro Bank which is leading

commercial bank in United States of America has bright future and lots of big opportunities are

waiting for the company. On the basis of trend analysis; it can be expected that its revenue will

be grow in upcoming year 2020 and simultaneously more efficient controlling of operative

activities will definitely improve net profit of the company. It is also estimated that Metro

Bankwill mix more equity fund for sources of financing compare with long term debt. This will

affect the decision making power of the company.

CONCLUSION

After analysis of whole report; it can be concluded that digitalization has changed the philosophy

of bank from only providing savings to customer to security, providing loan, tracking

information’s and many more facilities. Ratio’s have their own limitation, as it cannot

differentiate between huge amount and less amount. Profitability ratio or Gross margin is the

amount of each dollar of sales that the company is able to keep as gross profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.