BTAX1 Assignment: Self-Employment and Rental Income Tax Analysis

VerifiedAdded on 2022/07/28

|14

|1488

|25

Homework Assignment

AI Summary

This assignment solution covers the calculation of taxable income from self-employment and rental properties. For self-employment income, it includes the treatment of commissions, salaries paid to relatives, vehicle expenses, convention costs, and the calculation of Capital Cost Allowance (CCA) for ...

Running head: BTAX 1

BTax 1

Name of the Student:

Name of the University:

Authors Note:

BTax 1

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

BTAX 1

Contents

Answer 1:.........................................................................................................................................2

Answer 2:.........................................................................................................................................7

Answer 3:.......................................................................................................................................10

References:....................................................................................................................................13

BTAX 1

Contents

Answer 1:.........................................................................................................................................2

Answer 2:.........................................................................................................................................7

Answer 3:.......................................................................................................................................10

References:....................................................................................................................................13

2

BTAX 1

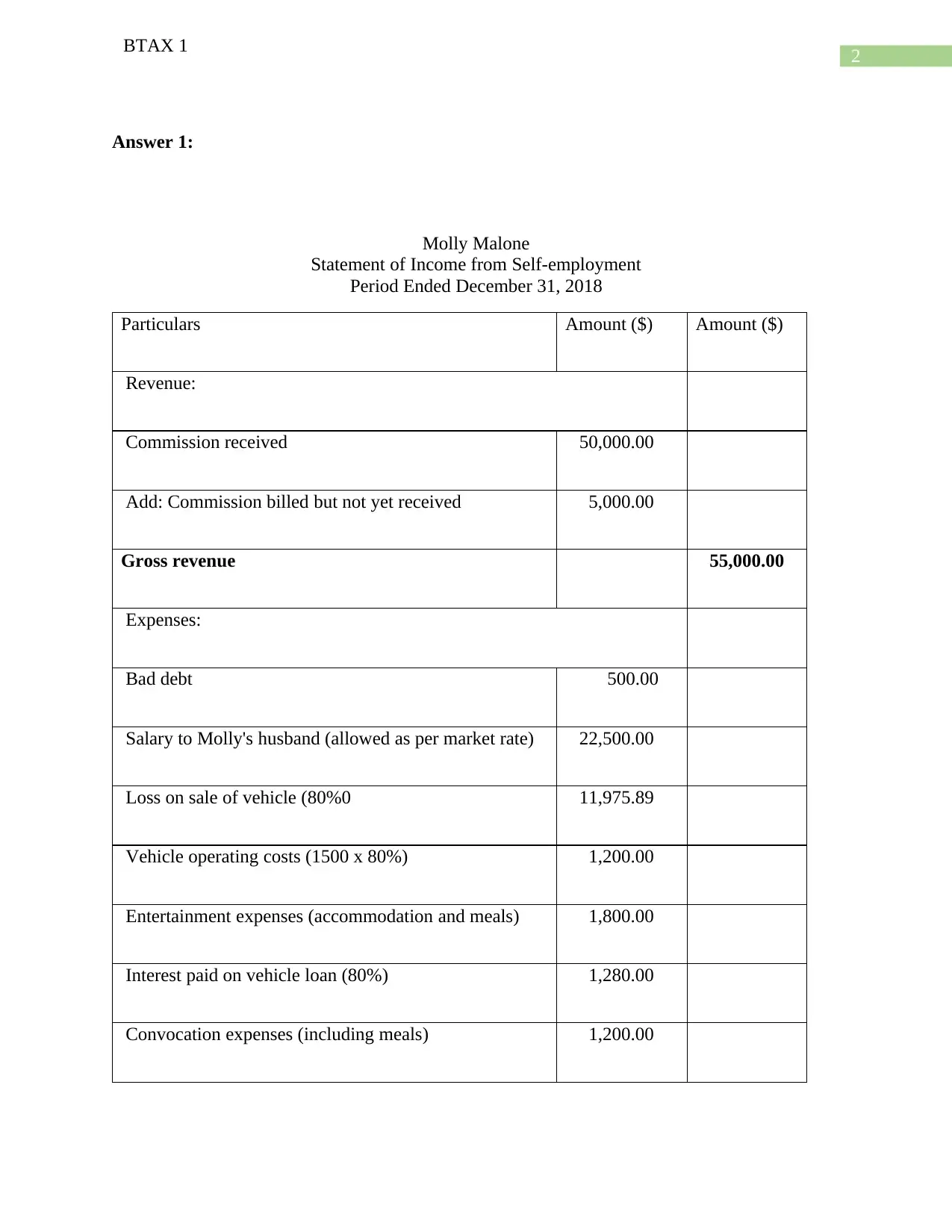

Answer 1:

Molly Malone

Statement of Income from Self-employment

Period Ended December 31, 2018

Particulars Amount ($) Amount ($)

Revenue:

Commission received 50,000.00

Add: Commission billed but not yet received 5,000.00

Gross revenue 55,000.00

Expenses:

Bad debt 500.00

Salary to Molly's husband (allowed as per market rate) 22,500.00

Loss on sale of vehicle (80%0 11,975.89

Vehicle operating costs (1500 x 80%) 1,200.00

Entertainment expenses (accommodation and meals) 1,800.00

Interest paid on vehicle loan (80%) 1,280.00

Convocation expenses (including meals) 1,200.00

BTAX 1

Answer 1:

Molly Malone

Statement of Income from Self-employment

Period Ended December 31, 2018

Particulars Amount ($) Amount ($)

Revenue:

Commission received 50,000.00

Add: Commission billed but not yet received 5,000.00

Gross revenue 55,000.00

Expenses:

Bad debt 500.00

Salary to Molly's husband (allowed as per market rate) 22,500.00

Loss on sale of vehicle (80%0 11,975.89

Vehicle operating costs (1500 x 80%) 1,200.00

Entertainment expenses (accommodation and meals) 1,800.00

Interest paid on vehicle loan (80%) 1,280.00

Convocation expenses (including meals) 1,200.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

BTAX 1

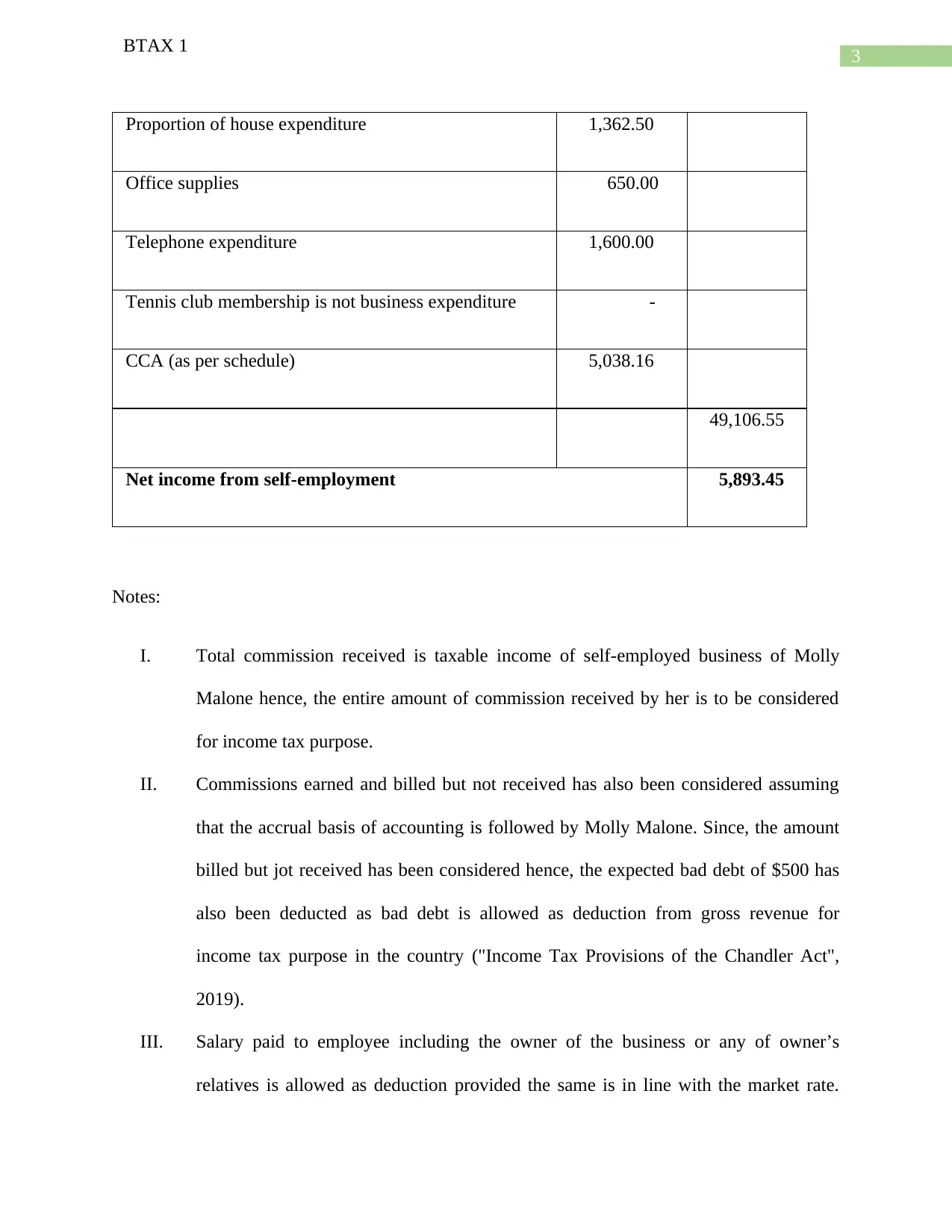

Proportion of house expenditure 1,362.50

Office supplies 650.00

Telephone expenditure 1,600.00

Tennis club membership is not business expenditure -

CCA (as per schedule) 5,038.16

49,106.55

Net income from self-employment 5,893.45

Notes:

I. Total commission received is taxable income of self-employed business of Molly

Malone hence, the entire amount of commission received by her is to be considered

for income tax purpose.

II. Commissions earned and billed but not received has also been considered assuming

that the accrual basis of accounting is followed by Molly Malone. Since, the amount

billed but jot received has been considered hence, the expected bad debt of $500 has

also been deducted as bad debt is allowed as deduction from gross revenue for

income tax purpose in the country ("Income Tax Provisions of the Chandler Act",

2019).

III. Salary paid to employee including the owner of the business or any of owner’s

relatives is allowed as deduction provided the same is in line with the market rate.

BTAX 1

Proportion of house expenditure 1,362.50

Office supplies 650.00

Telephone expenditure 1,600.00

Tennis club membership is not business expenditure -

CCA (as per schedule) 5,038.16

49,106.55

Net income from self-employment 5,893.45

Notes:

I. Total commission received is taxable income of self-employed business of Molly

Malone hence, the entire amount of commission received by her is to be considered

for income tax purpose.

II. Commissions earned and billed but not received has also been considered assuming

that the accrual basis of accounting is followed by Molly Malone. Since, the amount

billed but jot received has been considered hence, the expected bad debt of $500 has

also been deducted as bad debt is allowed as deduction from gross revenue for

income tax purpose in the country ("Income Tax Provisions of the Chandler Act",

2019).

III. Salary paid to employee including the owner of the business or any of owner’s

relatives is allowed as deduction provided the same is in line with the market rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

BTAX 1

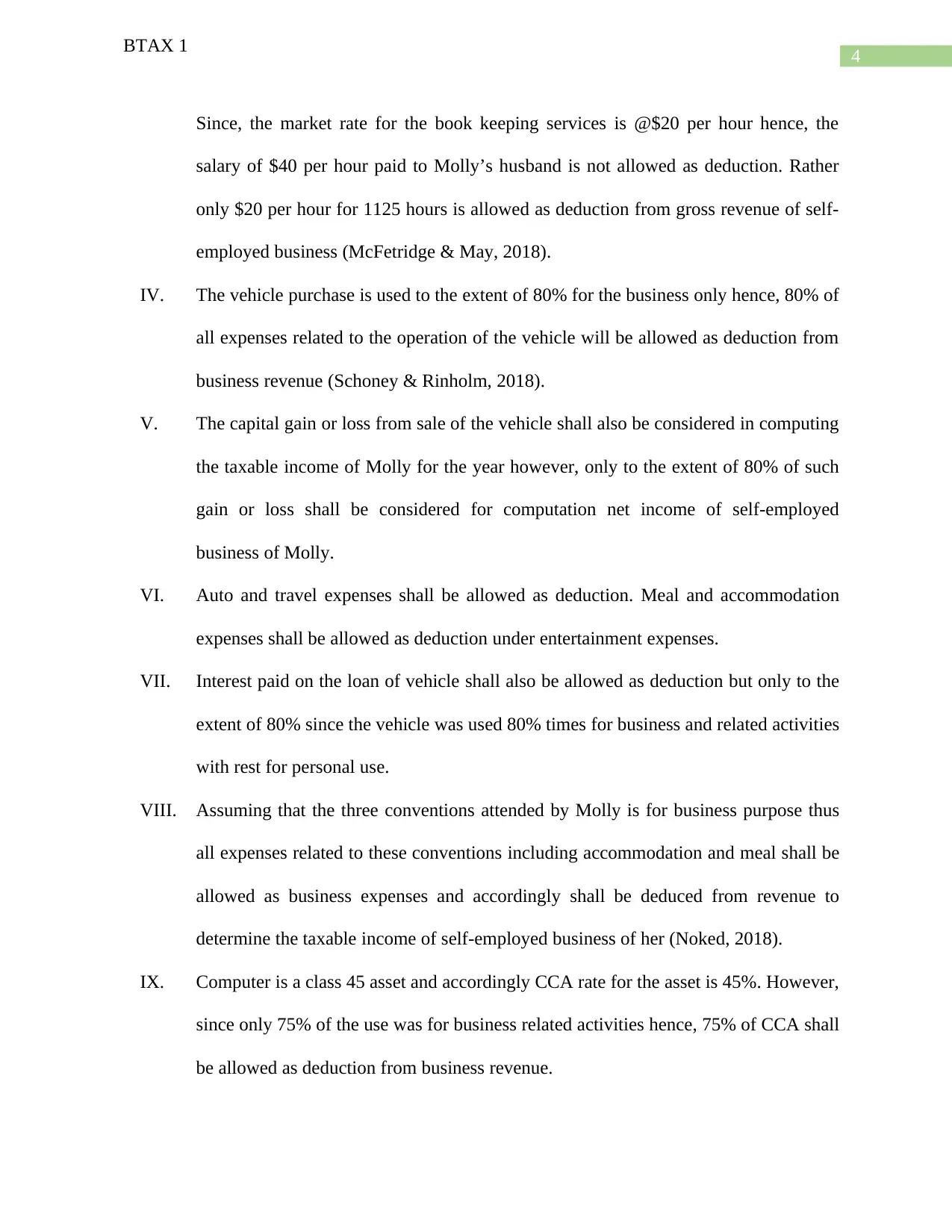

Since, the market rate for the book keeping services is @$20 per hour hence, the

salary of $40 per hour paid to Molly’s husband is not allowed as deduction. Rather

only $20 per hour for 1125 hours is allowed as deduction from gross revenue of self-

employed business (McFetridge & May, 2018).

IV. The vehicle purchase is used to the extent of 80% for the business only hence, 80% of

all expenses related to the operation of the vehicle will be allowed as deduction from

business revenue (Schoney & Rinholm, 2018).

V. The capital gain or loss from sale of the vehicle shall also be considered in computing

the taxable income of Molly for the year however, only to the extent of 80% of such

gain or loss shall be considered for computation net income of self-employed

business of Molly.

VI. Auto and travel expenses shall be allowed as deduction. Meal and accommodation

expenses shall be allowed as deduction under entertainment expenses.

VII. Interest paid on the loan of vehicle shall also be allowed as deduction but only to the

extent of 80% since the vehicle was used 80% times for business and related activities

with rest for personal use.

VIII. Assuming that the three conventions attended by Molly is for business purpose thus

all expenses related to these conventions including accommodation and meal shall be

allowed as business expenses and accordingly shall be deduced from revenue to

determine the taxable income of self-employed business of her (Noked, 2018).

IX. Computer is a class 45 asset and accordingly CCA rate for the asset is 45%. However,

since only 75% of the use was for business related activities hence, 75% of CCA shall

be allowed as deduction from business revenue.

BTAX 1

Since, the market rate for the book keeping services is @$20 per hour hence, the

salary of $40 per hour paid to Molly’s husband is not allowed as deduction. Rather

only $20 per hour for 1125 hours is allowed as deduction from gross revenue of self-

employed business (McFetridge & May, 2018).

IV. The vehicle purchase is used to the extent of 80% for the business only hence, 80% of

all expenses related to the operation of the vehicle will be allowed as deduction from

business revenue (Schoney & Rinholm, 2018).

V. The capital gain or loss from sale of the vehicle shall also be considered in computing

the taxable income of Molly for the year however, only to the extent of 80% of such

gain or loss shall be considered for computation net income of self-employed

business of Molly.

VI. Auto and travel expenses shall be allowed as deduction. Meal and accommodation

expenses shall be allowed as deduction under entertainment expenses.

VII. Interest paid on the loan of vehicle shall also be allowed as deduction but only to the

extent of 80% since the vehicle was used 80% times for business and related activities

with rest for personal use.

VIII. Assuming that the three conventions attended by Molly is for business purpose thus

all expenses related to these conventions including accommodation and meal shall be

allowed as business expenses and accordingly shall be deduced from revenue to

determine the taxable income of self-employed business of her (Noked, 2018).

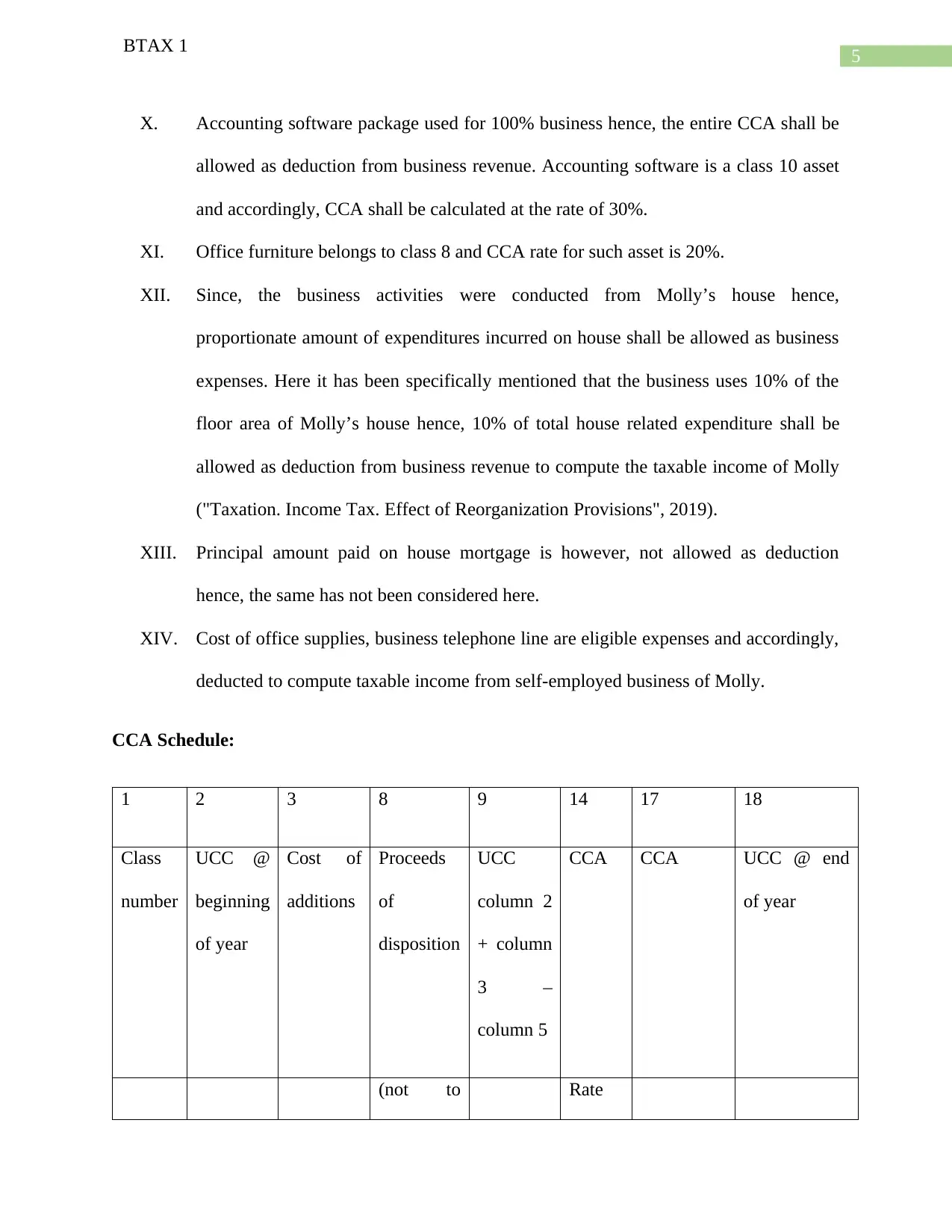

IX. Computer is a class 45 asset and accordingly CCA rate for the asset is 45%. However,

since only 75% of the use was for business related activities hence, 75% of CCA shall

be allowed as deduction from business revenue.

5

BTAX 1

X. Accounting software package used for 100% business hence, the entire CCA shall be

allowed as deduction from business revenue. Accounting software is a class 10 asset

and accordingly, CCA shall be calculated at the rate of 30%.

XI. Office furniture belongs to class 8 and CCA rate for such asset is 20%.

XII. Since, the business activities were conducted from Molly’s house hence,

proportionate amount of expenditures incurred on house shall be allowed as business

expenses. Here it has been specifically mentioned that the business uses 10% of the

floor area of Molly’s house hence, 10% of total house related expenditure shall be

allowed as deduction from business revenue to compute the taxable income of Molly

("Taxation. Income Tax. Effect of Reorganization Provisions", 2019).

XIII. Principal amount paid on house mortgage is however, not allowed as deduction

hence, the same has not been considered here.

XIV. Cost of office supplies, business telephone line are eligible expenses and accordingly,

deducted to compute taxable income from self-employed business of Molly.

CCA Schedule:

1 2 3 8 9 14 17 18

Class

number

UCC @

beginning

of year

Cost of

additions

Proceeds

of

disposition

UCC

column 2

+ column

3 –

column 5

CCA CCA UCC @ end

of year

(not to Rate

BTAX 1

X. Accounting software package used for 100% business hence, the entire CCA shall be

allowed as deduction from business revenue. Accounting software is a class 10 asset

and accordingly, CCA shall be calculated at the rate of 30%.

XI. Office furniture belongs to class 8 and CCA rate for such asset is 20%.

XII. Since, the business activities were conducted from Molly’s house hence,

proportionate amount of expenditures incurred on house shall be allowed as business

expenses. Here it has been specifically mentioned that the business uses 10% of the

floor area of Molly’s house hence, 10% of total house related expenditure shall be

allowed as deduction from business revenue to compute the taxable income of Molly

("Taxation. Income Tax. Effect of Reorganization Provisions", 2019).

XIII. Principal amount paid on house mortgage is however, not allowed as deduction

hence, the same has not been considered here.

XIV. Cost of office supplies, business telephone line are eligible expenses and accordingly,

deducted to compute taxable income from self-employed business of Molly.

CCA Schedule:

1 2 3 8 9 14 17 18

Class

number

UCC @

beginning

of year

Cost of

additions

Proceeds

of

disposition

UCC

column 2

+ column

3 –

column 5

CCA CCA UCC @ end

of year

(not to Rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

BTAX 1

exceed the

capital

cost)

8 1,000.0

0

1,000.0

0

20% 100.8

2

8,002.00

10 800.0

0

800.0

0

30% 120.9

9

679.01

10.1 58,000.0

0

20,000.00 38,000.0

0

30% 4,391.0

1

33,608.99

45 2,500.0

0

2,500.0

0

45% 425.3

4

2,074.66

5,038.1

6

Note:

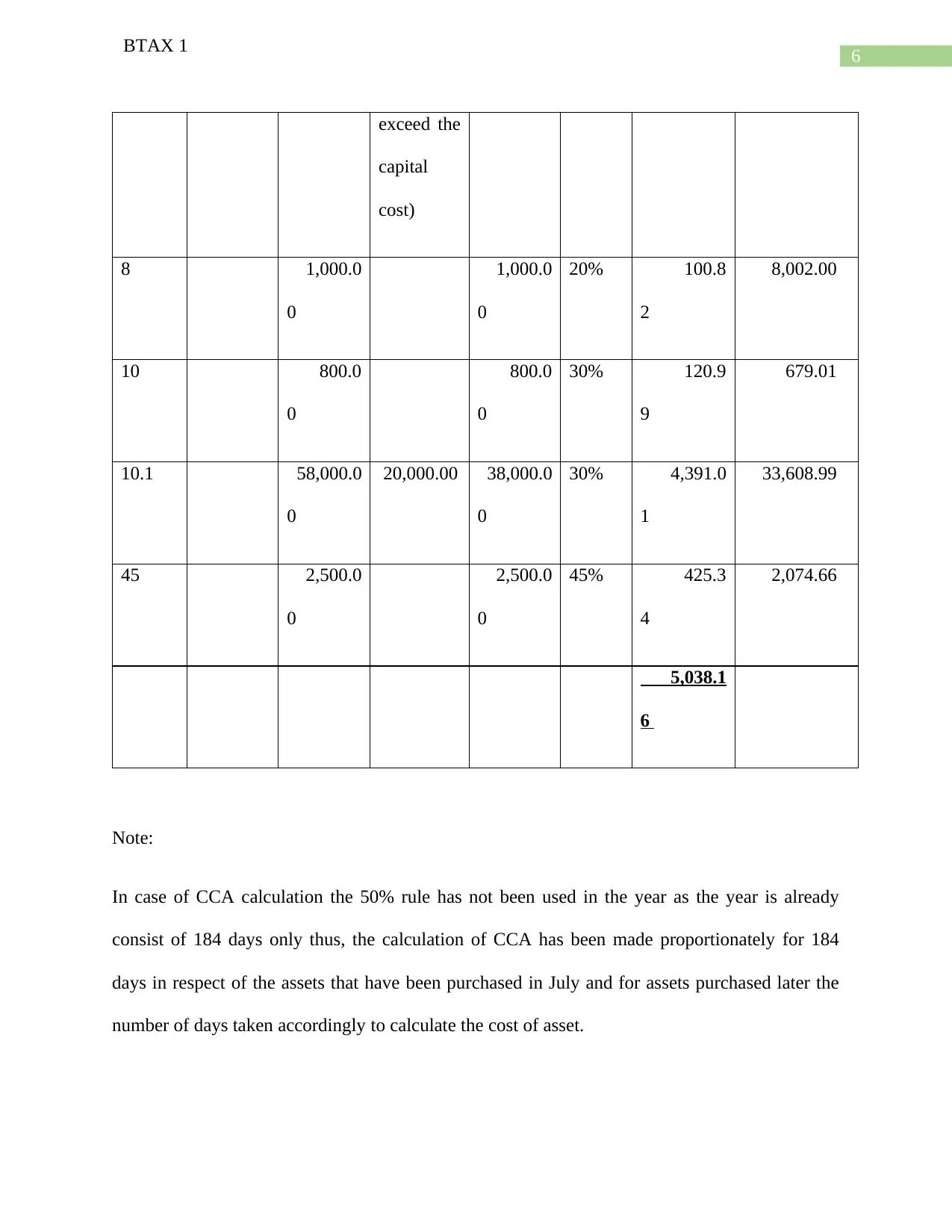

In case of CCA calculation the 50% rule has not been used in the year as the year is already

consist of 184 days only thus, the calculation of CCA has been made proportionately for 184

days in respect of the assets that have been purchased in July and for assets purchased later the

number of days taken accordingly to calculate the cost of asset.

BTAX 1

exceed the

capital

cost)

8 1,000.0

0

1,000.0

0

20% 100.8

2

8,002.00

10 800.0

0

800.0

0

30% 120.9

9

679.01

10.1 58,000.0

0

20,000.00 38,000.0

0

30% 4,391.0

1

33,608.99

45 2,500.0

0

2,500.0

0

45% 425.3

4

2,074.66

5,038.1

6

Note:

In case of CCA calculation the 50% rule has not been used in the year as the year is already

consist of 184 days only thus, the calculation of CCA has been made proportionately for 184

days in respect of the assets that have been purchased in July and for assets purchased later the

number of days taken accordingly to calculate the cost of asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

BTAX 1

In the above schedule CCA has been calculated only for business portion as the proportion of the

asset used for personal use is not eligible for deduction from business revenue. Thus, vehicle and

computer 80% and 75% respectively have been considered for calculation of CCA for the year.

However, UCC ending balance reflects the book value of these assets in their entirety and not

only for the portion used in business (Verma, 2019).

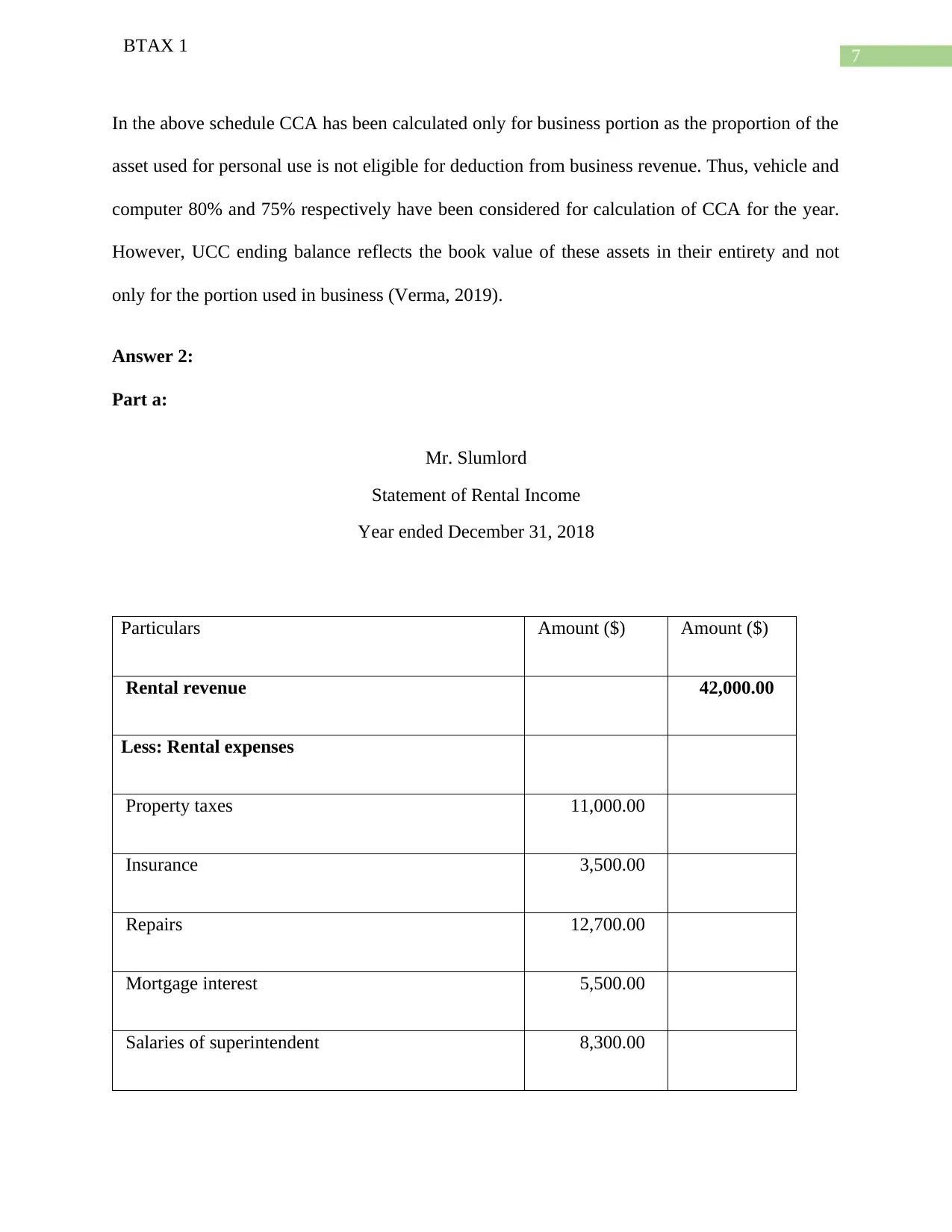

Answer 2:

Part a:

Mr. Slumlord

Statement of Rental Income

Year ended December 31, 2018

Particulars Amount ($) Amount ($)

Rental revenue 42,000.00

Less: Rental expenses

Property taxes 11,000.00

Insurance 3,500.00

Repairs 12,700.00

Mortgage interest 5,500.00

Salaries of superintendent 8,300.00

BTAX 1

In the above schedule CCA has been calculated only for business portion as the proportion of the

asset used for personal use is not eligible for deduction from business revenue. Thus, vehicle and

computer 80% and 75% respectively have been considered for calculation of CCA for the year.

However, UCC ending balance reflects the book value of these assets in their entirety and not

only for the portion used in business (Verma, 2019).

Answer 2:

Part a:

Mr. Slumlord

Statement of Rental Income

Year ended December 31, 2018

Particulars Amount ($) Amount ($)

Rental revenue 42,000.00

Less: Rental expenses

Property taxes 11,000.00

Insurance 3,500.00

Repairs 12,700.00

Mortgage interest 5,500.00

Salaries of superintendent 8,300.00

8

BTAX 1

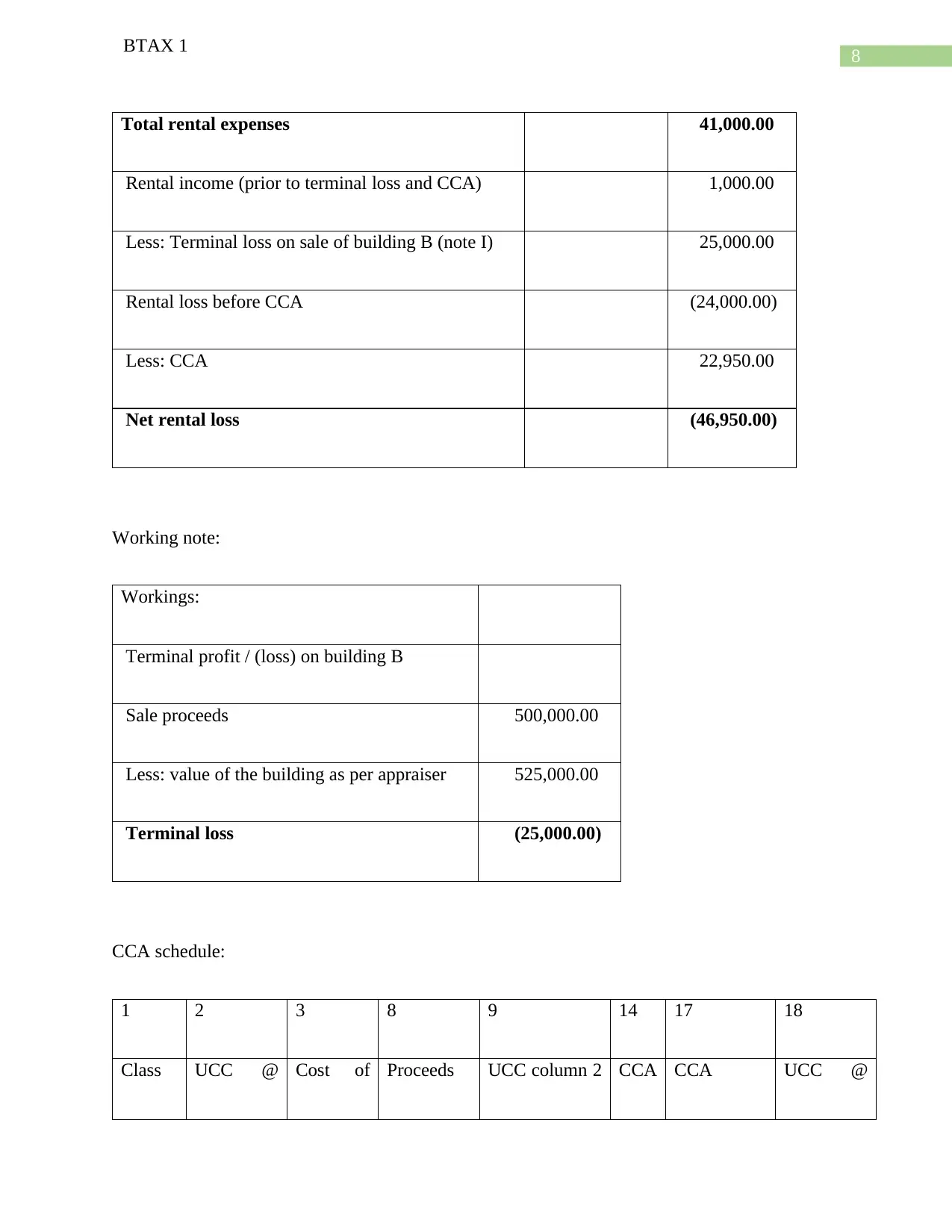

Total rental expenses 41,000.00

Rental income (prior to terminal loss and CCA) 1,000.00

Less: Terminal loss on sale of building B (note I) 25,000.00

Rental loss before CCA (24,000.00)

Less: CCA 22,950.00

Net rental loss (46,950.00)

Working note:

Workings:

Terminal profit / (loss) on building B

Sale proceeds 500,000.00

Less: value of the building as per appraiser 525,000.00

Terminal loss (25,000.00)

CCA schedule:

1 2 3 8 9 14 17 18

Class UCC @ Cost of Proceeds UCC column 2 CCA CCA UCC @

BTAX 1

Total rental expenses 41,000.00

Rental income (prior to terminal loss and CCA) 1,000.00

Less: Terminal loss on sale of building B (note I) 25,000.00

Rental loss before CCA (24,000.00)

Less: CCA 22,950.00

Net rental loss (46,950.00)

Working note:

Workings:

Terminal profit / (loss) on building B

Sale proceeds 500,000.00

Less: value of the building as per appraiser 525,000.00

Terminal loss (25,000.00)

CCA schedule:

1 2 3 8 9 14 17 18

Class UCC @ Cost of Proceeds UCC column 2 CCA CCA UCC @

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

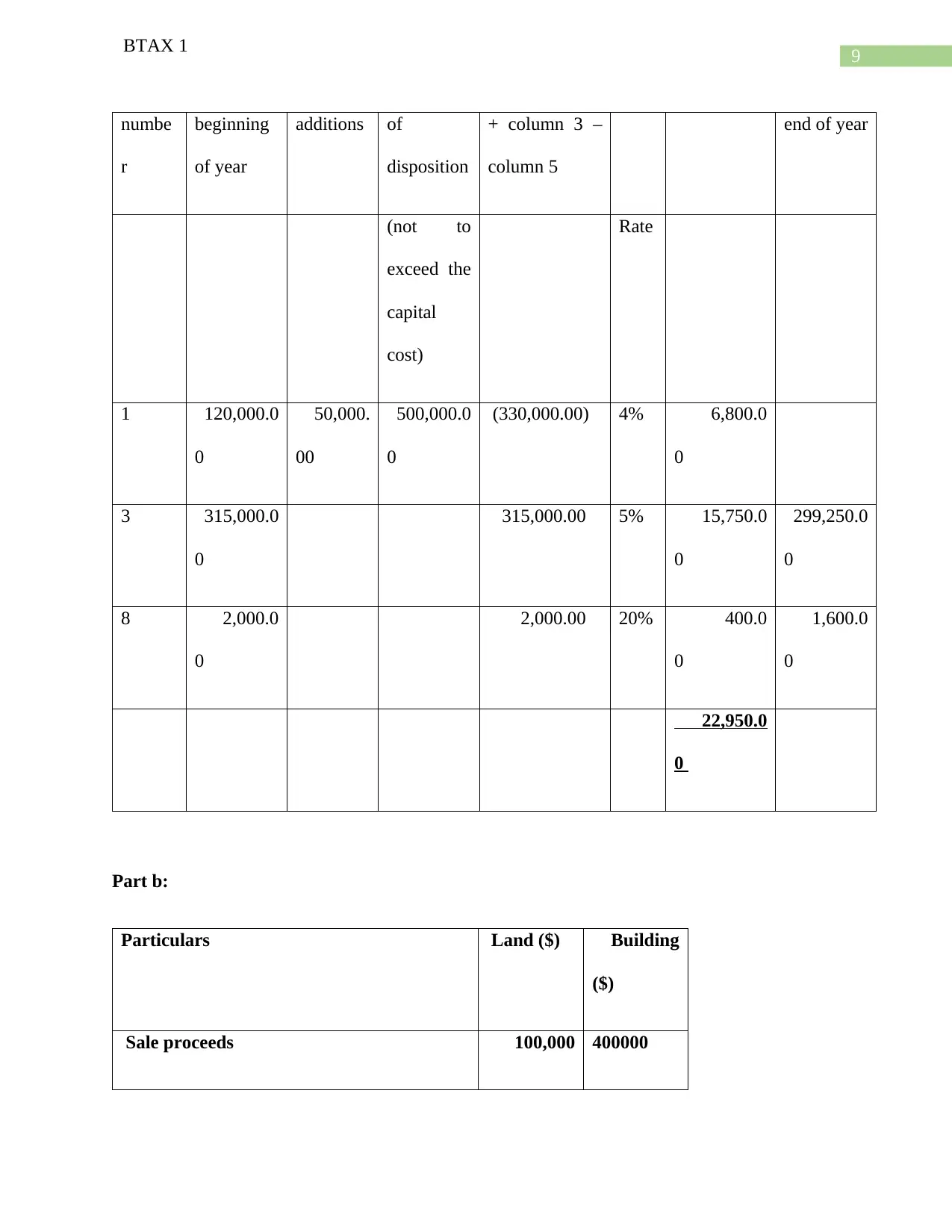

BTAX 1

numbe

r

beginning

of year

additions of

disposition

+ column 3 –

column 5

end of year

(not to

exceed the

capital

cost)

Rate

1 120,000.0

0

50,000.

00

500,000.0

0

(330,000.00) 4% 6,800.0

0

3 315,000.0

0

315,000.00 5% 15,750.0

0

299,250.0

0

8 2,000.0

0

2,000.00 20% 400.0

0

1,600.0

0

22,950.0

0

Part b:

Particulars Land ($) Building

($)

Sale proceeds 100,000 400000

BTAX 1

numbe

r

beginning

of year

additions of

disposition

+ column 3 –

column 5

end of year

(not to

exceed the

capital

cost)

Rate

1 120,000.0

0

50,000.

00

500,000.0

0

(330,000.00) 4% 6,800.0

0

3 315,000.0

0

315,000.00 5% 15,750.0

0

299,250.0

0

8 2,000.0

0

2,000.00 20% 400.0

0

1,600.0

0

22,950.0

0

Part b:

Particulars Land ($) Building

($)

Sale proceeds 100,000 400000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

BTAX 1

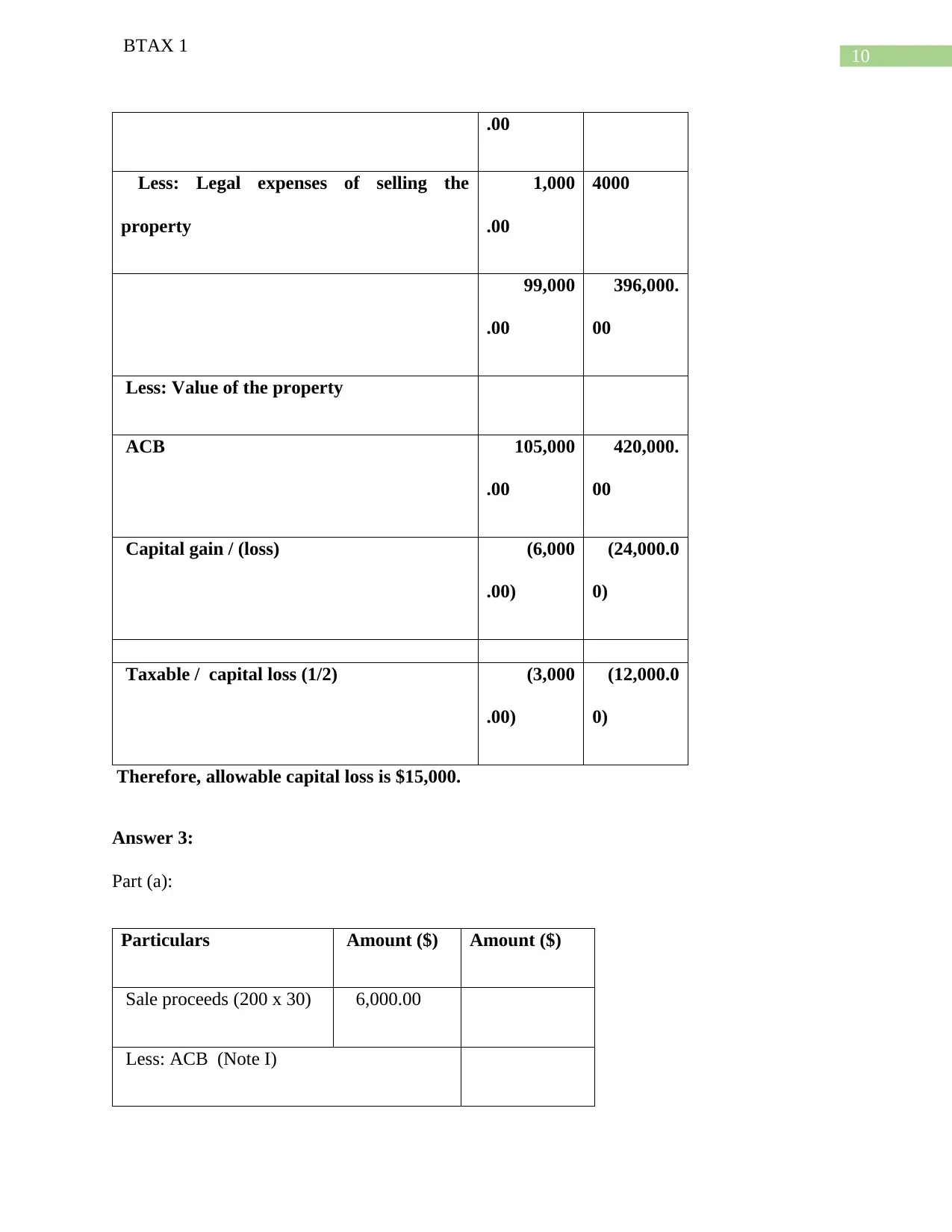

.00

Less: Legal expenses of selling the

property

1,000

.00

4000

99,000

.00

396,000.

00

Less: Value of the property

ACB 105,000

.00

420,000.

00

Capital gain / (loss) (6,000

.00)

(24,000.0

0)

Taxable / capital loss (1/2) (3,000

.00)

(12,000.0

0)

Therefore, allowable capital loss is $15,000.

Answer 3:

Part (a):

Particulars Amount ($) Amount ($)

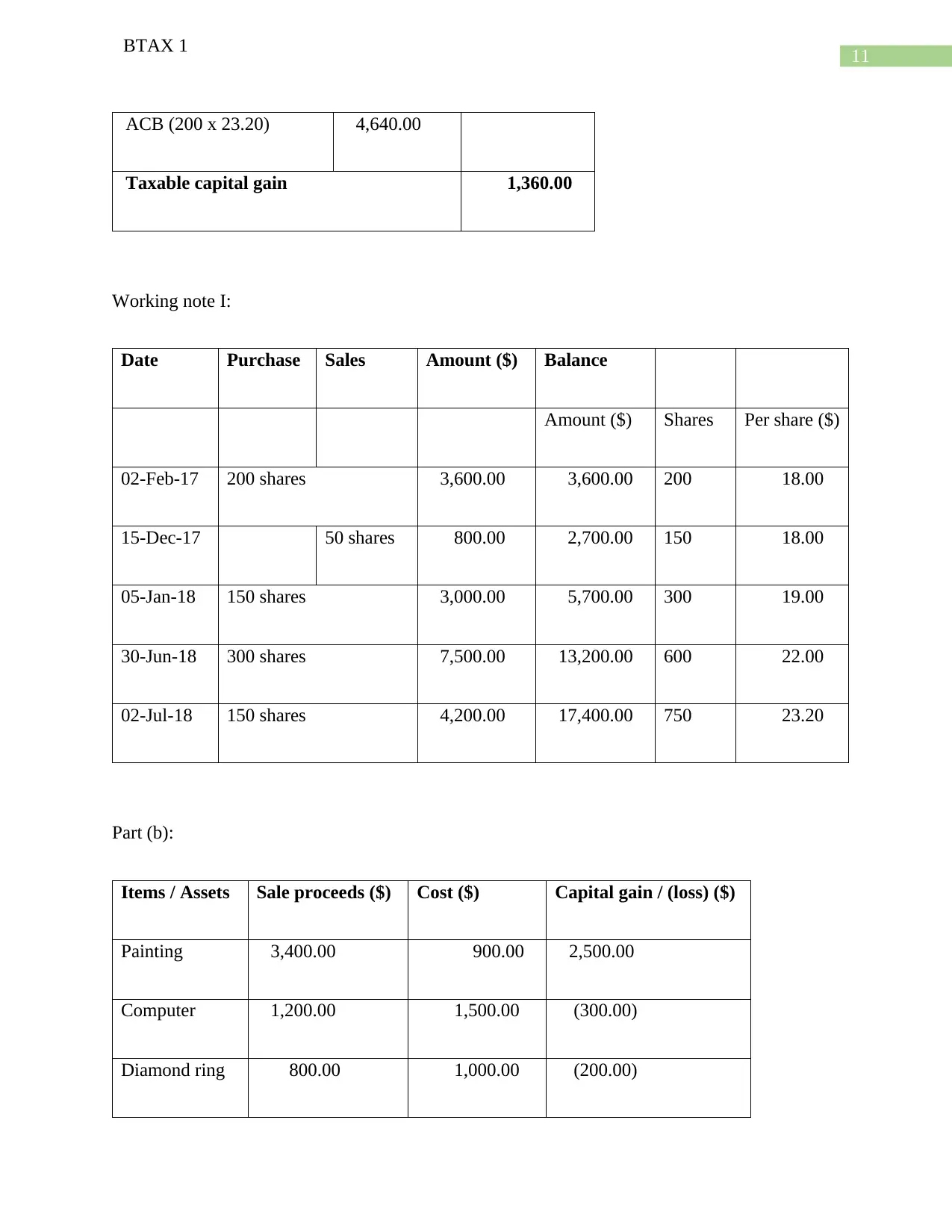

Sale proceeds (200 x 30) 6,000.00

Less: ACB (Note I)

BTAX 1

.00

Less: Legal expenses of selling the

property

1,000

.00

4000

99,000

.00

396,000.

00

Less: Value of the property

ACB 105,000

.00

420,000.

00

Capital gain / (loss) (6,000

.00)

(24,000.0

0)

Taxable / capital loss (1/2) (3,000

.00)

(12,000.0

0)

Therefore, allowable capital loss is $15,000.

Answer 3:

Part (a):

Particulars Amount ($) Amount ($)

Sale proceeds (200 x 30) 6,000.00

Less: ACB (Note I)

11

BTAX 1

ACB (200 x 23.20) 4,640.00

Taxable capital gain 1,360.00

Working note I:

Date Purchase Sales Amount ($) Balance

Amount ($) Shares Per share ($)

02-Feb-17 200 shares 3,600.00 3,600.00 200 18.00

15-Dec-17 50 shares 800.00 2,700.00 150 18.00

05-Jan-18 150 shares 3,000.00 5,700.00 300 19.00

30-Jun-18 300 shares 7,500.00 13,200.00 600 22.00

02-Jul-18 150 shares 4,200.00 17,400.00 750 23.20

Part (b):

Items / Assets Sale proceeds ($) Cost ($) Capital gain / (loss) ($)

Painting 3,400.00 900.00 2,500.00

Computer 1,200.00 1,500.00 (300.00)

Diamond ring 800.00 1,000.00 (200.00)

BTAX 1

ACB (200 x 23.20) 4,640.00

Taxable capital gain 1,360.00

Working note I:

Date Purchase Sales Amount ($) Balance

Amount ($) Shares Per share ($)

02-Feb-17 200 shares 3,600.00 3,600.00 200 18.00

15-Dec-17 50 shares 800.00 2,700.00 150 18.00

05-Jan-18 150 shares 3,000.00 5,700.00 300 19.00

30-Jun-18 300 shares 7,500.00 13,200.00 600 22.00

02-Jul-18 150 shares 4,200.00 17,400.00 750 23.20

Part (b):

Items / Assets Sale proceeds ($) Cost ($) Capital gain / (loss) ($)

Painting 3,400.00 900.00 2,500.00

Computer 1,200.00 1,500.00 (300.00)

Diamond ring 800.00 1,000.00 (200.00)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12

BTAX 1

BTAX 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

BTAX 1

References:

BTAX 1

References:

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.